Stell Co Ltd Financial and Management Accounting Analysis Report

VerifiedAdded on 2023/06/11

|11

|2667

|120

Report

AI Summary

This report provides a detailed financial and management accounting analysis of Stell Co Ltd. It includes calculations of gross and net profit, ratio analysis, reasons for declining profits and cash flow problems, and strategies for financial improvement. The report also covers break-even point computation, uses of break-even analysis, and the adoption of activity-based costing. Furthermore, it calculates significant variances, explains their causes and consequences, recommends business improvement strategies, and presents the advantages and disadvantages of switching from incremental-based budgeting to zero-based budgeting. This student contributed assignment is available on Desklib, a platform offering a range of study tools and resources.

FINANCIAL and

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1..................................................................................................................................3

1 Calculation of Gross Profit And Net Profit by Stell Co Ltd in each accounting year............3

2. Calculating ratio.......................................................................................................................3

3. Providing the reasons for the company’s declining profits and cash flow problems between

2020 and 2021..............................................................................................................................4

4. Providing three strategies to improve the financial position................................................5

QUESTION 2..................................................................................................................................6

1 Computation of Break even point............................................................................................6

2. Explaining uses of Break Even Analysis to enable the firm to set profitable sales revenue

targets...........................................................................................................................................6

3. Outlining supply of more accurate management accounting information and the adoption of

the Activity Based Costing for accomplishing short and long term objectives...........................7

QUESTION 3..................................................................................................................................7

1. Calculating th three most significant variances:......................................................................7

2 Explaining the causes of these variances..................................................................................9

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen............................................................................................................................9

4. Recommending strategies for business improvements..........................................................10

5. Presenting advantages disadvantages of a switch from Incremental Based Budgeting to ZBB

...................................................................................................................................................10

REFERENCES..............................................................................................................................11

QUESTION 1..................................................................................................................................3

1 Calculation of Gross Profit And Net Profit by Stell Co Ltd in each accounting year............3

2. Calculating ratio.......................................................................................................................3

3. Providing the reasons for the company’s declining profits and cash flow problems between

2020 and 2021..............................................................................................................................4

4. Providing three strategies to improve the financial position................................................5

QUESTION 2..................................................................................................................................6

1 Computation of Break even point............................................................................................6

2. Explaining uses of Break Even Analysis to enable the firm to set profitable sales revenue

targets...........................................................................................................................................6

3. Outlining supply of more accurate management accounting information and the adoption of

the Activity Based Costing for accomplishing short and long term objectives...........................7

QUESTION 3..................................................................................................................................7

1. Calculating th three most significant variances:......................................................................7

2 Explaining the causes of these variances..................................................................................9

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen............................................................................................................................9

4. Recommending strategies for business improvements..........................................................10

5. Presenting advantages disadvantages of a switch from Incremental Based Budgeting to ZBB

...................................................................................................................................................10

REFERENCES..............................................................................................................................11

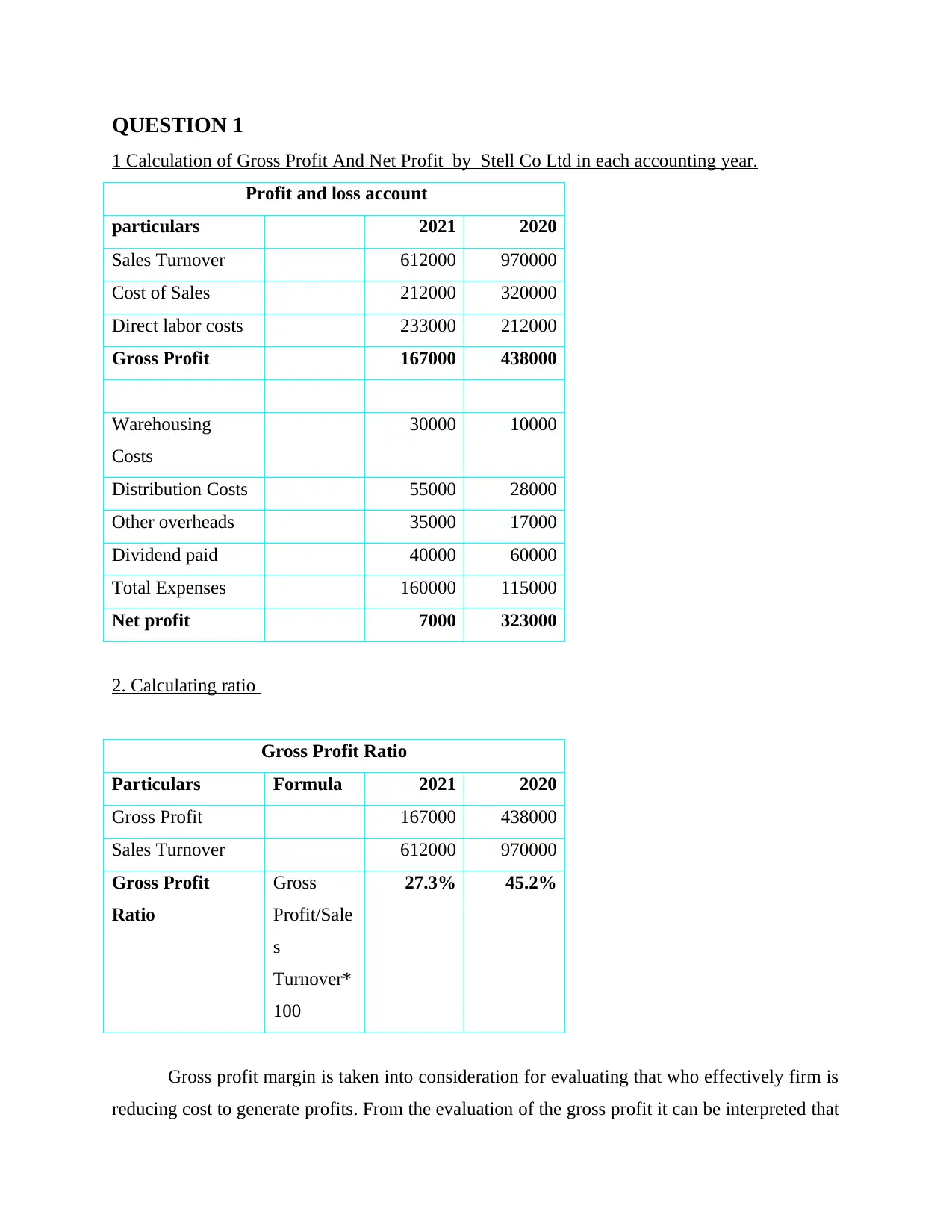

QUESTION 1

1 Calculation of Gross Profit And Net Profit by Stell Co Ltd in each accounting year.

Profit and loss account

particulars 2021 2020

Sales Turnover 612000 970000

Cost of Sales 212000 320000

Direct labor costs 233000 212000

Gross Profit 167000 438000

Warehousing

Costs

30000 10000

Distribution Costs 55000 28000

Other overheads 35000 17000

Dividend paid 40000 60000

Total Expenses 160000 115000

Net profit 7000 323000

2. Calculating ratio

Gross Profit Ratio

Particulars Formula 2021 2020

Gross Profit 167000 438000

Sales Turnover 612000 970000

Gross Profit

Ratio

Gross

Profit/Sale

s

Turnover*

100

27.3% 45.2%

Gross profit margin is taken into consideration for evaluating that who effectively firm is

reducing cost to generate profits. From the evaluation of the gross profit it can be interpreted that

1 Calculation of Gross Profit And Net Profit by Stell Co Ltd in each accounting year.

Profit and loss account

particulars 2021 2020

Sales Turnover 612000 970000

Cost of Sales 212000 320000

Direct labor costs 233000 212000

Gross Profit 167000 438000

Warehousing

Costs

30000 10000

Distribution Costs 55000 28000

Other overheads 35000 17000

Dividend paid 40000 60000

Total Expenses 160000 115000

Net profit 7000 323000

2. Calculating ratio

Gross Profit Ratio

Particulars Formula 2021 2020

Gross Profit 167000 438000

Sales Turnover 612000 970000

Gross Profit

Ratio

Gross

Profit/Sale

s

Turnover*

100

27.3% 45.2%

Gross profit margin is taken into consideration for evaluating that who effectively firm is

reducing cost to generate profits. From the evaluation of the gross profit it can be interpreted that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

there is decreasing of profits which is indicating that company's revenue generating capacity in

current year as compared to the previous has declined. The other cause that can be articulated fro

the decrease in profitability is higher cost of goods sold. The gross profit ideal ratio is 10-20%

which is lower than articulated figure and previous year performance it is less. On the basis of

this, it can be said that firm needs to make improvement in overall performance. This allows to

ensure that cost structure is formulated properly to attract stakeholders for investment (Masdupi,

Tasman and Davista, 2018).

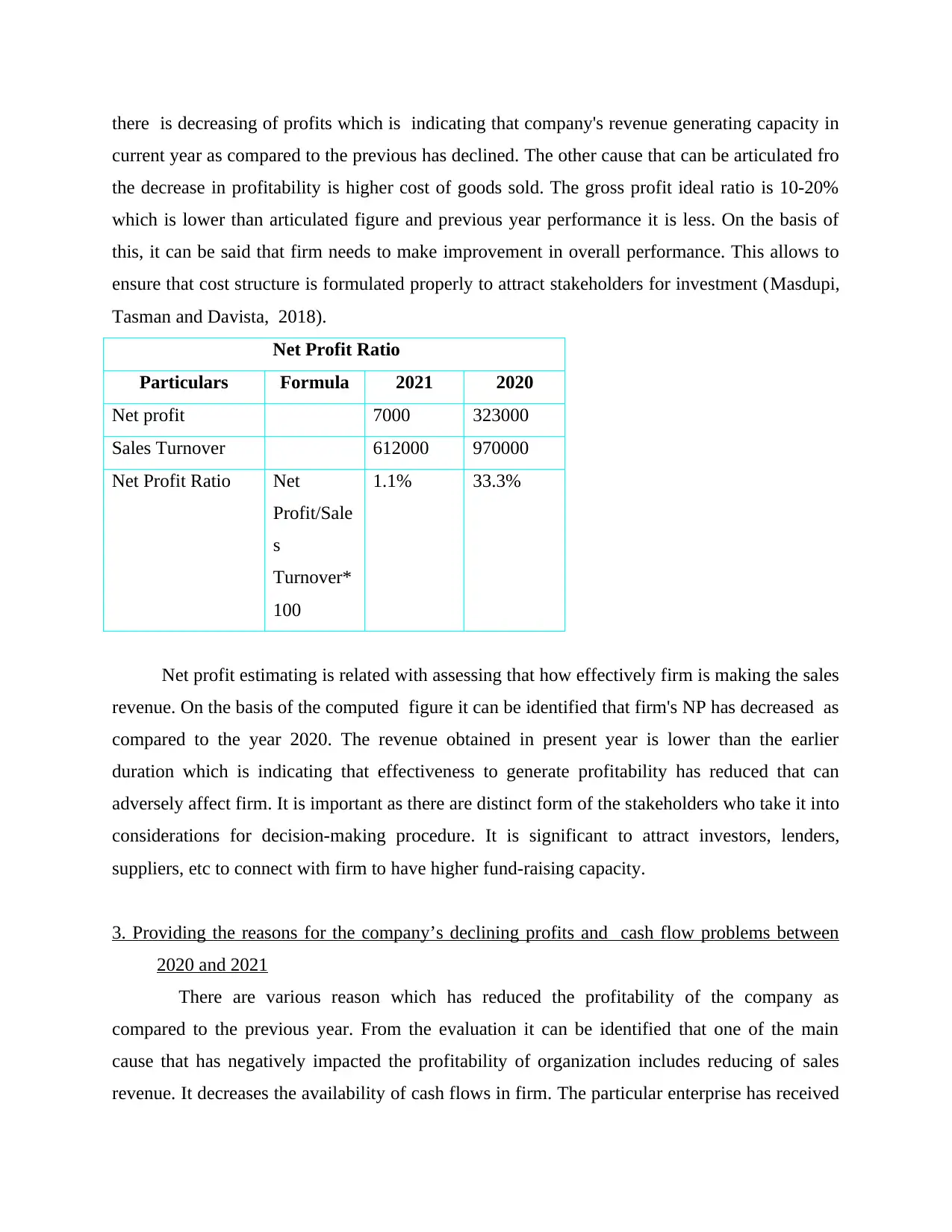

Net Profit Ratio

Particulars Formula 2021 2020

Net profit 7000 323000

Sales Turnover 612000 970000

Net Profit Ratio Net

Profit/Sale

s

Turnover*

100

1.1% 33.3%

Net profit estimating is related with assessing that how effectively firm is making the sales

revenue. On the basis of the computed figure it can be identified that firm's NP has decreased as

compared to the year 2020. The revenue obtained in present year is lower than the earlier

duration which is indicating that effectiveness to generate profitability has reduced that can

adversely affect firm. It is important as there are distinct form of the stakeholders who take it into

considerations for decision-making procedure. It is significant to attract investors, lenders,

suppliers, etc to connect with firm to have higher fund-raising capacity.

3. Providing the reasons for the company’s declining profits and cash flow problems between

2020 and 2021

There are various reason which has reduced the profitability of the company as

compared to the previous year. From the evaluation it can be identified that one of the main

cause that has negatively impacted the profitability of organization includes reducing of sales

revenue. It decreases the availability of cash flows in firm. The particular enterprise has received

current year as compared to the previous has declined. The other cause that can be articulated fro

the decrease in profitability is higher cost of goods sold. The gross profit ideal ratio is 10-20%

which is lower than articulated figure and previous year performance it is less. On the basis of

this, it can be said that firm needs to make improvement in overall performance. This allows to

ensure that cost structure is formulated properly to attract stakeholders for investment (Masdupi,

Tasman and Davista, 2018).

Net Profit Ratio

Particulars Formula 2021 2020

Net profit 7000 323000

Sales Turnover 612000 970000

Net Profit Ratio Net

Profit/Sale

s

Turnover*

100

1.1% 33.3%

Net profit estimating is related with assessing that how effectively firm is making the sales

revenue. On the basis of the computed figure it can be identified that firm's NP has decreased as

compared to the year 2020. The revenue obtained in present year is lower than the earlier

duration which is indicating that effectiveness to generate profitability has reduced that can

adversely affect firm. It is important as there are distinct form of the stakeholders who take it into

considerations for decision-making procedure. It is significant to attract investors, lenders,

suppliers, etc to connect with firm to have higher fund-raising capacity.

3. Providing the reasons for the company’s declining profits and cash flow problems between

2020 and 2021

There are various reason which has reduced the profitability of the company as

compared to the previous year. From the evaluation it can be identified that one of the main

cause that has negatively impacted the profitability of organization includes reducing of sales

revenue. It decreases the availability of cash flows in firm. The particular enterprise has received

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

low profitability due to decrease in cash flow which has impacted its ability to conduct the

divided efforts. In order to attract the investors the organization require paying attention on

having relevant level of satisfaction providing efforts in turn better customers to incline

profitability can be exerted by form. The other set of reasons for decreasing profitability due to

lower revenue is changing trend in market, ineffective quality performance, customer

dissatisfaction, rise of substitute products, etc which result in negatively affecting the momentary

condition of business.

There is increase of the cost in the overall structure of firm as both the direct and indirect

expenses of enterprise has inclined which is reducing its profit margin. In order to get he higher

profitability as compared to the previous year firm need to focus on developing such effective

strategy of lowering the expenditure of enterprise in turn higher margin can be established. On

the basis of this it can be interpreted that firm has uncured higher level of expenses for increasing

its revenue generating capacity but failed. The failure in inclining revenue and decreased the

cash flow as compared to previous year which ha adversely affected the financial condition of

the enterprise.

4. Providing three strategies to improve the financial position

It is recommended to the company to execute cost leadership strategy for the purpose of

reducing the expenses. This can be effectively exerted by identifying the irrelevant

aspects which are not significant contributing to profitability so that can be eliminated.

The particular approach can aid in attaining the organization objective of having

effective ability to decline expenses so that profits can be increased to boost financial

condition.

This is advised to the organization to apply price optimization system in turn customer

responses for the changing price level can be identified in order to attract buyers via

setting relevant price. It can provide assistance in receiving higher revenue to uplift

monetary condition.

It is suggested to the firm to give emphasis on implementing the variance analysis and

KPIs for gaining the information about standards so that motivating employees to meet

this so that higher potential can be derived. This can permit in increasing performance of

firm by having effective results to gain competitiveness.

divided efforts. In order to attract the investors the organization require paying attention on

having relevant level of satisfaction providing efforts in turn better customers to incline

profitability can be exerted by form. The other set of reasons for decreasing profitability due to

lower revenue is changing trend in market, ineffective quality performance, customer

dissatisfaction, rise of substitute products, etc which result in negatively affecting the momentary

condition of business.

There is increase of the cost in the overall structure of firm as both the direct and indirect

expenses of enterprise has inclined which is reducing its profit margin. In order to get he higher

profitability as compared to the previous year firm need to focus on developing such effective

strategy of lowering the expenditure of enterprise in turn higher margin can be established. On

the basis of this it can be interpreted that firm has uncured higher level of expenses for increasing

its revenue generating capacity but failed. The failure in inclining revenue and decreased the

cash flow as compared to previous year which ha adversely affected the financial condition of

the enterprise.

4. Providing three strategies to improve the financial position

It is recommended to the company to execute cost leadership strategy for the purpose of

reducing the expenses. This can be effectively exerted by identifying the irrelevant

aspects which are not significant contributing to profitability so that can be eliminated.

The particular approach can aid in attaining the organization objective of having

effective ability to decline expenses so that profits can be increased to boost financial

condition.

This is advised to the organization to apply price optimization system in turn customer

responses for the changing price level can be identified in order to attract buyers via

setting relevant price. It can provide assistance in receiving higher revenue to uplift

monetary condition.

It is suggested to the firm to give emphasis on implementing the variance analysis and

KPIs for gaining the information about standards so that motivating employees to meet

this so that higher potential can be derived. This can permit in increasing performance of

firm by having effective results to gain competitiveness.

QUESTION 2

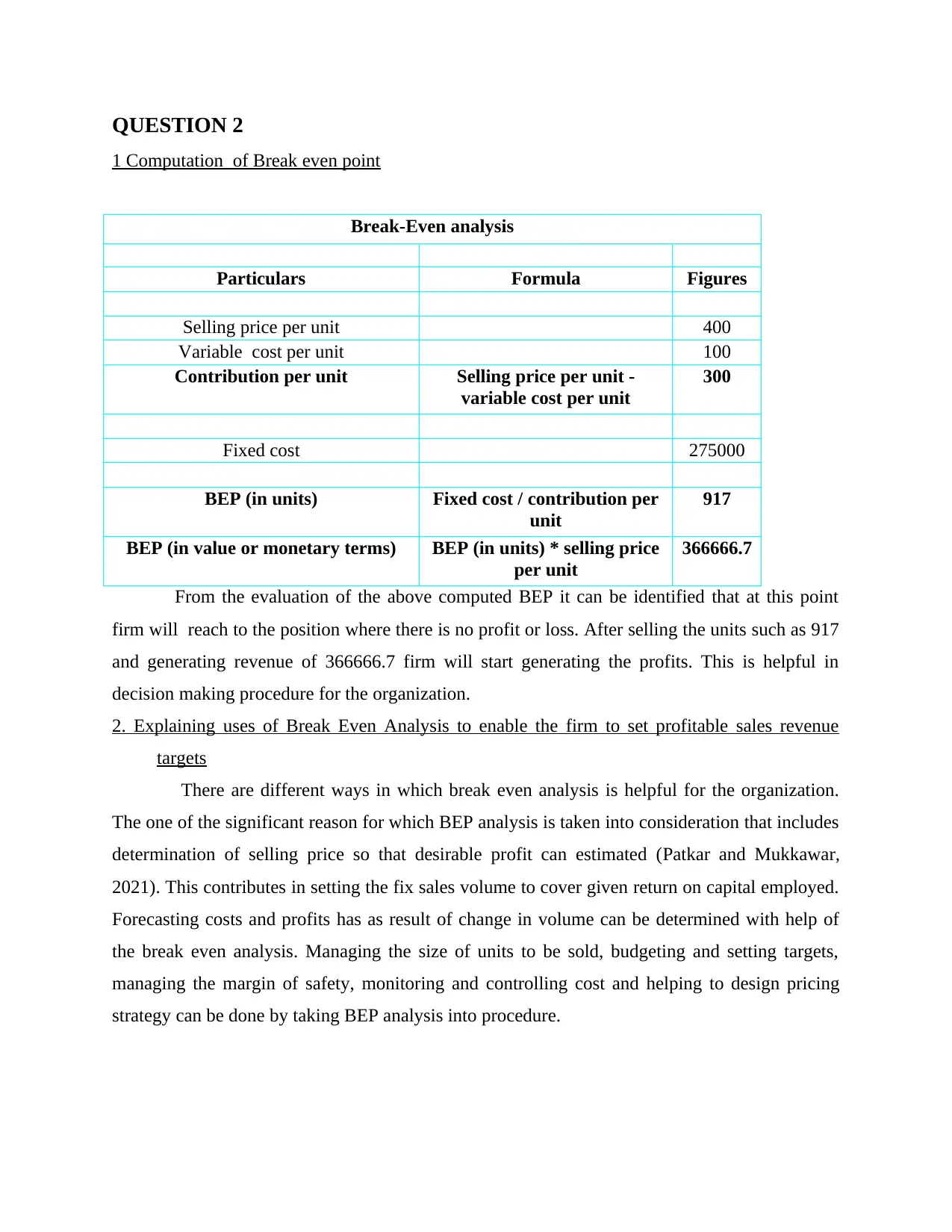

1 Computation of Break even point

Break-Even analysis

Particulars Formula Figures

Selling price per unit 400

Variable cost per unit 100

Contribution per unit Selling price per unit -

variable cost per unit

300

Fixed cost 275000

BEP (in units) Fixed cost / contribution per

unit

917

BEP (in value or monetary terms) BEP (in units) * selling price

per unit

366666.7

From the evaluation of the above computed BEP it can be identified that at this point

firm will reach to the position where there is no profit or loss. After selling the units such as 917

and generating revenue of 366666.7 firm will start generating the profits. This is helpful in

decision making procedure for the organization.

2. Explaining uses of Break Even Analysis to enable the firm to set profitable sales revenue

targets

There are different ways in which break even analysis is helpful for the organization.

The one of the significant reason for which BEP analysis is taken into consideration that includes

determination of selling price so that desirable profit can estimated (Patkar and Mukkawar,

2021). This contributes in setting the fix sales volume to cover given return on capital employed.

Forecasting costs and profits has as result of change in volume can be determined with help of

the break even analysis. Managing the size of units to be sold, budgeting and setting targets,

managing the margin of safety, monitoring and controlling cost and helping to design pricing

strategy can be done by taking BEP analysis into procedure.

1 Computation of Break even point

Break-Even analysis

Particulars Formula Figures

Selling price per unit 400

Variable cost per unit 100

Contribution per unit Selling price per unit -

variable cost per unit

300

Fixed cost 275000

BEP (in units) Fixed cost / contribution per

unit

917

BEP (in value or monetary terms) BEP (in units) * selling price

per unit

366666.7

From the evaluation of the above computed BEP it can be identified that at this point

firm will reach to the position where there is no profit or loss. After selling the units such as 917

and generating revenue of 366666.7 firm will start generating the profits. This is helpful in

decision making procedure for the organization.

2. Explaining uses of Break Even Analysis to enable the firm to set profitable sales revenue

targets

There are different ways in which break even analysis is helpful for the organization.

The one of the significant reason for which BEP analysis is taken into consideration that includes

determination of selling price so that desirable profit can estimated (Patkar and Mukkawar,

2021). This contributes in setting the fix sales volume to cover given return on capital employed.

Forecasting costs and profits has as result of change in volume can be determined with help of

the break even analysis. Managing the size of units to be sold, budgeting and setting targets,

managing the margin of safety, monitoring and controlling cost and helping to design pricing

strategy can be done by taking BEP analysis into procedure.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of this, it can be interpreted that organization with help of break even

analysis can forecast cost, setting appropriate targets for profits, etc so that enable to get effective

position in achieving significant ability to set profitability margin to meet revenue standard.

3. Outlining supply of more accurate management accounting information and the adoption of

the Activity Based Costing for accomplishing short and long term objectives

In order to achieve short and long term objectives it is important for the firm to give emphasis

on having effectual data insights so that prevailing lacking areas can be identified. Accurate

management accounting information gives ability to assess the crucial parts which can highly

contribute in attaining the organizational goals such as attracting customers, higher profitability,

sustainability, etc. Activity based budgeting is related with recognizing the practice that are

leading expanses to firm so that proper decision-making procedure to get desirable outcomes can

become possible (Wahab, Mohamad and Said, 2018). There are various advantages which can be

received by applying ABC that involve sh better insights of operational costs, adding competitive

edge, management of budget, improved budgetary control, improving relationship, etc so that

attaining short & long term objective can be done effectively. On the basis of this, it is

interpreted to adopt ABC so that the set of advantages can be received.

QUESTION 3

1. Calculating th three most significant variances:

Labor variance= Standard cost of labor – actual cost of labor

= 170000-240000

=- 70000

Storage and Delivery = Standard cost of Storage and Delivery– actual cost of Storage and

Delivery

= 40000- 50000

= -10000

Power= Standard cost of power - actual cost of power

=70000-95000

=-70000

Working note:

Budget £ Actual varianc varian Outco

analysis can forecast cost, setting appropriate targets for profits, etc so that enable to get effective

position in achieving significant ability to set profitability margin to meet revenue standard.

3. Outlining supply of more accurate management accounting information and the adoption of

the Activity Based Costing for accomplishing short and long term objectives

In order to achieve short and long term objectives it is important for the firm to give emphasis

on having effectual data insights so that prevailing lacking areas can be identified. Accurate

management accounting information gives ability to assess the crucial parts which can highly

contribute in attaining the organizational goals such as attracting customers, higher profitability,

sustainability, etc. Activity based budgeting is related with recognizing the practice that are

leading expanses to firm so that proper decision-making procedure to get desirable outcomes can

become possible (Wahab, Mohamad and Said, 2018). There are various advantages which can be

received by applying ABC that involve sh better insights of operational costs, adding competitive

edge, management of budget, improved budgetary control, improving relationship, etc so that

attaining short & long term objective can be done effectively. On the basis of this, it is

interpreted to adopt ABC so that the set of advantages can be received.

QUESTION 3

1. Calculating th three most significant variances:

Labor variance= Standard cost of labor – actual cost of labor

= 170000-240000

=- 70000

Storage and Delivery = Standard cost of Storage and Delivery– actual cost of Storage and

Delivery

= 40000- 50000

= -10000

Power= Standard cost of power - actual cost of power

=70000-95000

=-70000

Working note:

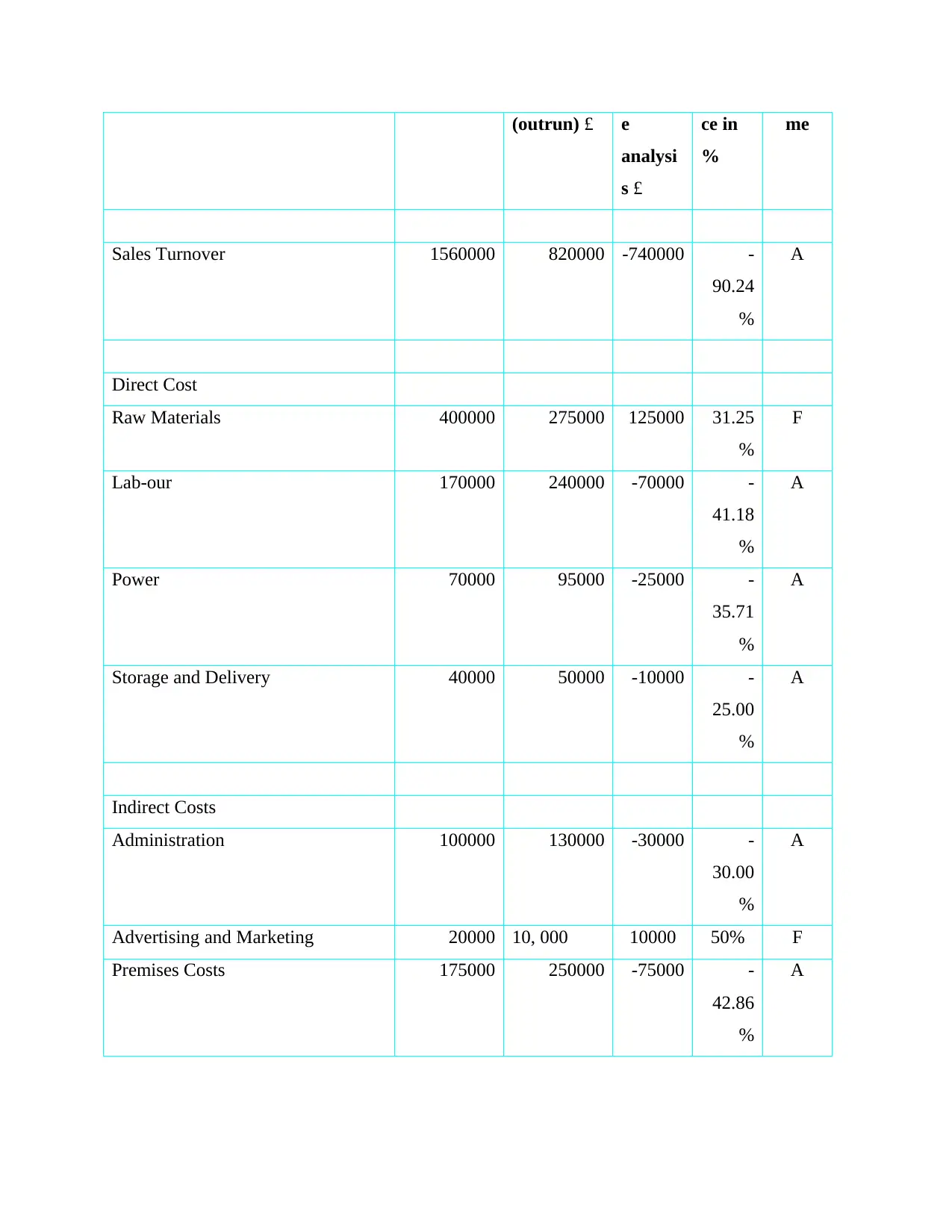

Budget £ Actual varianc varian Outco

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(outrun) £ e

analysi

s £

ce in

%

me

Sales Turnover 1560000 820000 -740000 -

90.24

%

A

Direct Cost

Raw Materials 400000 275000 125000 31.25

%

F

Lab-our 170000 240000 -70000 -

41.18

%

A

Power 70000 95000 -25000 -

35.71

%

A

Storage and Delivery 40000 50000 -10000 -

25.00

%

A

Indirect Costs

Administration 100000 130000 -30000 -

30.00

%

A

Advertising and Marketing 20000 10, 000 10000 50% F

Premises Costs 175000 250000 -75000 -

42.86

%

A

analysi

s £

ce in

%

me

Sales Turnover 1560000 820000 -740000 -

90.24

%

A

Direct Cost

Raw Materials 400000 275000 125000 31.25

%

F

Lab-our 170000 240000 -70000 -

41.18

%

A

Power 70000 95000 -25000 -

35.71

%

A

Storage and Delivery 40000 50000 -10000 -

25.00

%

A

Indirect Costs

Administration 100000 130000 -30000 -

30.00

%

A

Advertising and Marketing 20000 10, 000 10000 50% F

Premises Costs 175000 250000 -75000 -

42.86

%

A

2 Explaining the causes of these variances

Variances occurs in the company due to deviation arriving because of higher or lower cost as

compared to the estimated outcomes. From the evaluation of the calculated figure of variances it

can be interpreted that company is performing effectively in which positive outcome has been

derived such as raw material which is indicating that firm is performing good by reducing its

expenses in current time.

From the evaluation of the given information regarding the variance of labor it can be

identified that firm has failed to coordinate with the estimated expenditure. The main

reason behind is ineffective outcome generating capacity of employees, inappropriate

forecasting of labor cost, etc which is resulting into unfavorable performance.

Storage and Delivery cost of company is deviating in negative manner as compared to

the standard estimation of the expenses. The main reason behind the ineffective

performance of enterprise is due to careless handling of components, poor maintenance,

abnormal waste, etc. these are causing the firm to incur more expense in order to affect

firm adversely.

Power is one of the significant part of the direct cost that is required to be managed

effectively but particular organization failed due to certain causes such as adopting

defective wastage h of material by untrained workers, loss due to poor quality of material

utilized in usage of power, etc.

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen

From the evaluation it can be interpreted that particular firm will face the adverse impact

from the of the selected variance.

The consequence of labor variance can highly affect the overall cost structure of firm so

that can adversely influence the profit margin of business. It can affect the overall

efficiency level of production processes that can result in low products' formulation

which can majorly imbalance market force meeting capacity of firm.

Storage and delivery is essential part of supply chain of enterprise that has major

influence on the functioning on firm which can loss the effectiveness to meet the market

forces. Higher cost can affect the irrelevant formulation of customer dissatisfaction as

quality of product can be adversely get impacted.

Variances occurs in the company due to deviation arriving because of higher or lower cost as

compared to the estimated outcomes. From the evaluation of the calculated figure of variances it

can be interpreted that company is performing effectively in which positive outcome has been

derived such as raw material which is indicating that firm is performing good by reducing its

expenses in current time.

From the evaluation of the given information regarding the variance of labor it can be

identified that firm has failed to coordinate with the estimated expenditure. The main

reason behind is ineffective outcome generating capacity of employees, inappropriate

forecasting of labor cost, etc which is resulting into unfavorable performance.

Storage and Delivery cost of company is deviating in negative manner as compared to

the standard estimation of the expenses. The main reason behind the ineffective

performance of enterprise is due to careless handling of components, poor maintenance,

abnormal waste, etc. these are causing the firm to incur more expense in order to affect

firm adversely.

Power is one of the significant part of the direct cost that is required to be managed

effectively but particular organization failed due to certain causes such as adopting

defective wastage h of material by untrained workers, loss due to poor quality of material

utilized in usage of power, etc.

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen

From the evaluation it can be interpreted that particular firm will face the adverse impact

from the of the selected variance.

The consequence of labor variance can highly affect the overall cost structure of firm so

that can adversely influence the profit margin of business. It can affect the overall

efficiency level of production processes that can result in low products' formulation

which can majorly imbalance market force meeting capacity of firm.

Storage and delivery is essential part of supply chain of enterprise that has major

influence on the functioning on firm which can loss the effectiveness to meet the market

forces. Higher cost can affect the irrelevant formulation of customer dissatisfaction as

quality of product can be adversely get impacted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Power cost increase can reduce the firm's financial resources so that overall growth&

development can get affected. It can lead to create the threat in employees to work

effectively in working areas. Price stability and mitigation o revenue can arise due to

inclination of higher expenditure of managing power.

4. Recommending strategies for business improvements

It is suggested to the company to implement the training and development which can

allow the employees to get the significant position to incline their efficiency in turn

accomplishing the role and responsibilities with opium utilization of resources can

become possible.

This is suggested to have the inventory management system in the procedure for

managing the storage and delivery expenses as it allows to avoid the situation of over or

under stocking. These can enable the firm to receive higher productiveness with

minimizing related cost.

It is advised to the organization to execute appropriate technology utilization which can

optimize power and decrease waste to gain higher desirable outcomes.

5. Presenting advantages disadvantages of a switch from Incremental Based Budgeting to ZBB

Incremental based budgeting is related with taking the current year budget by adding

increments for formulating new budget. There are few impacts that is faced by the company due

to implementation of increment that are both positive and negative. The one of the crucial benefit

include easiest budgeting approach but lacking areas involves promoting unnecessary pending,

discourage innovation, etc.

Zero based budgeting is related with formulating the budget from the scratch which aids

to offer the benefits like higher accuracy & efficiency, coordination & communication, reduction

in redundant activities, budget inflation (Beredugo, Azubike and Okon, 2019.). On the other

side, lacking areas includes time-consuming procedure, may be expensive, high manpower

requirements e and lack of expertise. On the basis of this, it can be articulated that ZBB method

implementation can offer these benefits and drawbacks to the specified organization.

development can get affected. It can lead to create the threat in employees to work

effectively in working areas. Price stability and mitigation o revenue can arise due to

inclination of higher expenditure of managing power.

4. Recommending strategies for business improvements

It is suggested to the company to implement the training and development which can

allow the employees to get the significant position to incline their efficiency in turn

accomplishing the role and responsibilities with opium utilization of resources can

become possible.

This is suggested to have the inventory management system in the procedure for

managing the storage and delivery expenses as it allows to avoid the situation of over or

under stocking. These can enable the firm to receive higher productiveness with

minimizing related cost.

It is advised to the organization to execute appropriate technology utilization which can

optimize power and decrease waste to gain higher desirable outcomes.

5. Presenting advantages disadvantages of a switch from Incremental Based Budgeting to ZBB

Incremental based budgeting is related with taking the current year budget by adding

increments for formulating new budget. There are few impacts that is faced by the company due

to implementation of increment that are both positive and negative. The one of the crucial benefit

include easiest budgeting approach but lacking areas involves promoting unnecessary pending,

discourage innovation, etc.

Zero based budgeting is related with formulating the budget from the scratch which aids

to offer the benefits like higher accuracy & efficiency, coordination & communication, reduction

in redundant activities, budget inflation (Beredugo, Azubike and Okon, 2019.). On the other

side, lacking areas includes time-consuming procedure, may be expensive, high manpower

requirements e and lack of expertise. On the basis of this, it can be articulated that ZBB method

implementation can offer these benefits and drawbacks to the specified organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Masdupi, E., Tasman, A. and Davista, A., 2018. The influence of liquidity, leverage and

profitability on financial distress of listed manufacturing companies in

Indonesia. Advances in Economics, Business and Management Research. 57(1).

Wahab, A. A., Mohamad, M. H. S. and Said, J. M., 2018. The implementation of activity-based

costing in the Accountant General’s Department of Malaysia. Asian Journal of

Accounting and Governance. 9. pp.63-76.

Beredugo, S. B., Azubike, J. U. and Okon, E. E., 2019. Comparative analysis of zero-based

budgeting and incremental budgeting techniques of government performance in

Nigeria. International Journal of Research and Innovation in Social Science. 3(6). pp.238-

243.

Patkar, A. and Mukkawar, S., 2021, November. Break even analysis & response of longer span

frames with or without post-tensioned beams in multipurpose hall. In IOP Conference

Series: Materials Science and Engineering (Vol. 1197, No. 1, p. 012011). IOP

Publishing.

Books and Journals

Masdupi, E., Tasman, A. and Davista, A., 2018. The influence of liquidity, leverage and

profitability on financial distress of listed manufacturing companies in

Indonesia. Advances in Economics, Business and Management Research. 57(1).

Wahab, A. A., Mohamad, M. H. S. and Said, J. M., 2018. The implementation of activity-based

costing in the Accountant General’s Department of Malaysia. Asian Journal of

Accounting and Governance. 9. pp.63-76.

Beredugo, S. B., Azubike, J. U. and Okon, E. E., 2019. Comparative analysis of zero-based

budgeting and incremental budgeting techniques of government performance in

Nigeria. International Journal of Research and Innovation in Social Science. 3(6). pp.238-

243.

Patkar, A. and Mukkawar, S., 2021, November. Break even analysis & response of longer span

frames with or without post-tensioned beams in multipurpose hall. In IOP Conference

Series: Materials Science and Engineering (Vol. 1197, No. 1, p. 012011). IOP

Publishing.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.