Stock Return Analysis: Statistics for Business and Finance

VerifiedAdded on 2023/06/03

|15

|3064

|264

Report

AI Summary

This report provides a comprehensive statistical analysis of stock returns for General Dynamics (GD) and Boeing (BA), along with the S&P 500 (GSPC). The analysis includes calculating returns, conducting Jarque-Berra tests to assess normality, evaluating the risk-return relationship, and performing hypothesis tests to compare average returns and variances. The Capital Asset Pricing Model (CAPM) is employed to estimate beta and interpret its significance, along with R-squared and confidence intervals. The report also examines whether GD stock is a neutral stock and assesses the normality of error terms in ordinary least squares regression. Statistical software like Microsoft Excel and SPSS were used for computations and analysis, with detailed results presented in tables and interpretations provided for each test and model.

Running Head: STATISTICS FOR BUSINESS AND FINANCE ASSIGNMENT

STATISTICS FOR BUSINESS AND FINANCE ASSIGNMENT

Student’s Name

Institution Affiliation

STATISTICS FOR BUSINESS AND FINANCE ASSIGNMENT

Student’s Name

Institution Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

Contents

1. Computation of the return of the three series of stock prices...............................................................3

1.1. Jarque-Berra test: Are GD and Boeing Stocks’ Returns normally distributed or not?................3

1.2. Risk–return relationship...............................................................................................................4

2. Hypothesis test at 0.05% significant level: Is average returns of GD stock is equal to 2.8% or

different?.....................................................................................................................................................5

3. Hypothesis test at 0.05% significant level: Are the variances of GD and Boeing (BA) stocks similar

or different?.................................................................................................................................................5

4. Hypothesis test at 0.05% significant level: Are the average returns of GD and BA stocks equal or

not?..............................................................................................................................................................6

5. CAPM Model..........................................................................................................................................7

5.0. Computation of excess return of GD and excess market return........................................................7

5.1. CAPM Estimation.............................................................................................................................7

5.2. Interpretation of CAPM Beta............................................................................................................8

5.3. Interpretation of R 2.........................................................................................................................8

5.4. Interpretation of confidence interval for CAPM Beta.......................................................................8

6. Hypothesis test using confidence interval approach at 0.05% significant level: Is GD stock a neutral

stock or not?................................................................................................................................................8

7. Hypothesis test at 0.05% significant level: Is error term in ordinary least squares normally distributed

or not?.........................................................................................................................................................9

Reference...................................................................................................................................................10

APPENDIX...............................................................................................................................................10

Table 1: Computed Returns for GSPC, GD and BA stock prices..........................................................10

Table 2: Computed Excess Returns for GD...........................................................................................12

Contents

1. Computation of the return of the three series of stock prices...............................................................3

1.1. Jarque-Berra test: Are GD and Boeing Stocks’ Returns normally distributed or not?................3

1.2. Risk–return relationship...............................................................................................................4

2. Hypothesis test at 0.05% significant level: Is average returns of GD stock is equal to 2.8% or

different?.....................................................................................................................................................5

3. Hypothesis test at 0.05% significant level: Are the variances of GD and Boeing (BA) stocks similar

or different?.................................................................................................................................................5

4. Hypothesis test at 0.05% significant level: Are the average returns of GD and BA stocks equal or

not?..............................................................................................................................................................6

5. CAPM Model..........................................................................................................................................7

5.0. Computation of excess return of GD and excess market return........................................................7

5.1. CAPM Estimation.............................................................................................................................7

5.2. Interpretation of CAPM Beta............................................................................................................8

5.3. Interpretation of R 2.........................................................................................................................8

5.4. Interpretation of confidence interval for CAPM Beta.......................................................................8

6. Hypothesis test using confidence interval approach at 0.05% significant level: Is GD stock a neutral

stock or not?................................................................................................................................................8

7. Hypothesis test at 0.05% significant level: Is error term in ordinary least squares normally distributed

or not?.........................................................................................................................................................9

Reference...................................................................................................................................................10

APPENDIX...............................................................................................................................................10

Table 1: Computed Returns for GSPC, GD and BA stock prices..........................................................10

Table 2: Computed Excess Returns for GD...........................................................................................12

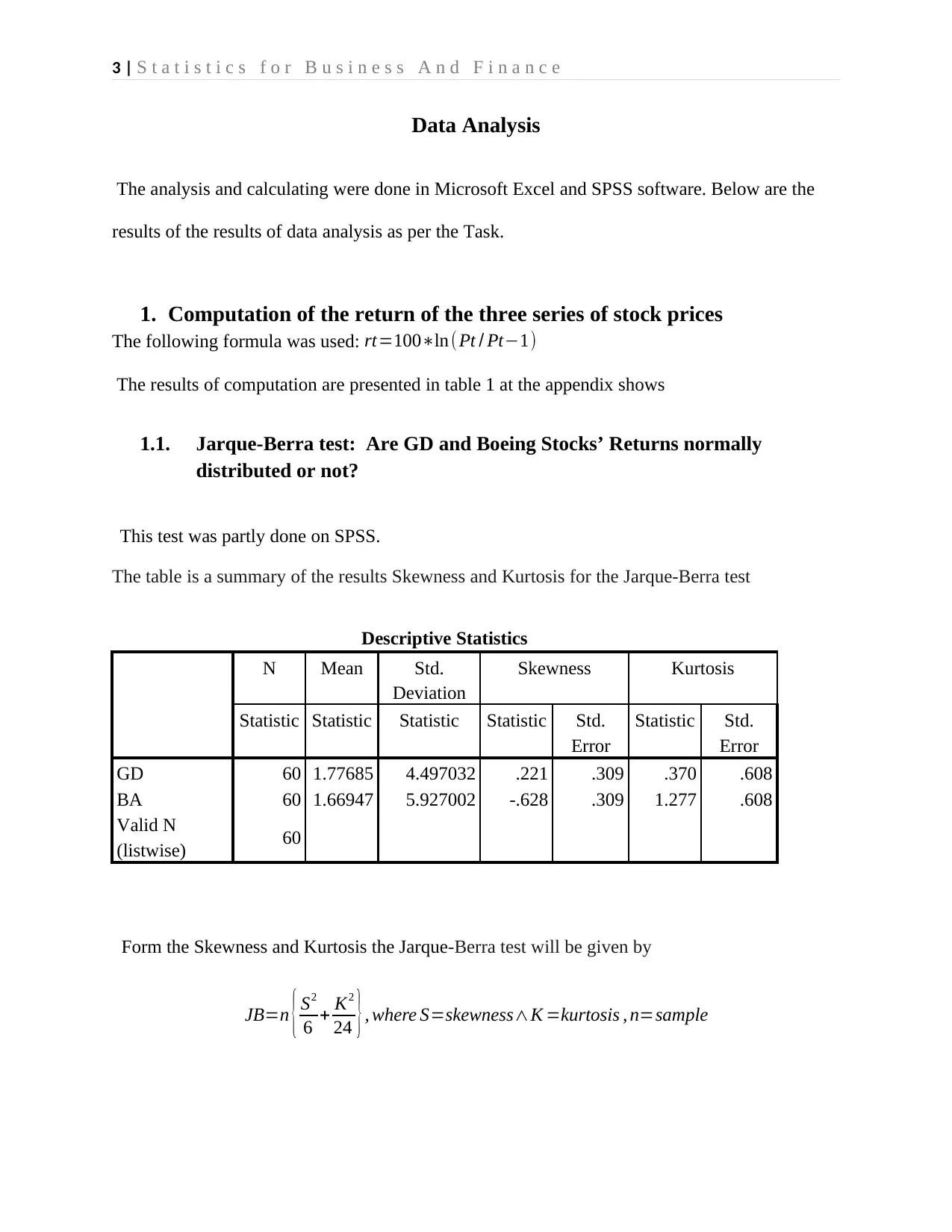

3 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

Data Analysis

The analysis and calculating were done in Microsoft Excel and SPSS software. Below are the

results of the results of data analysis as per the Task.

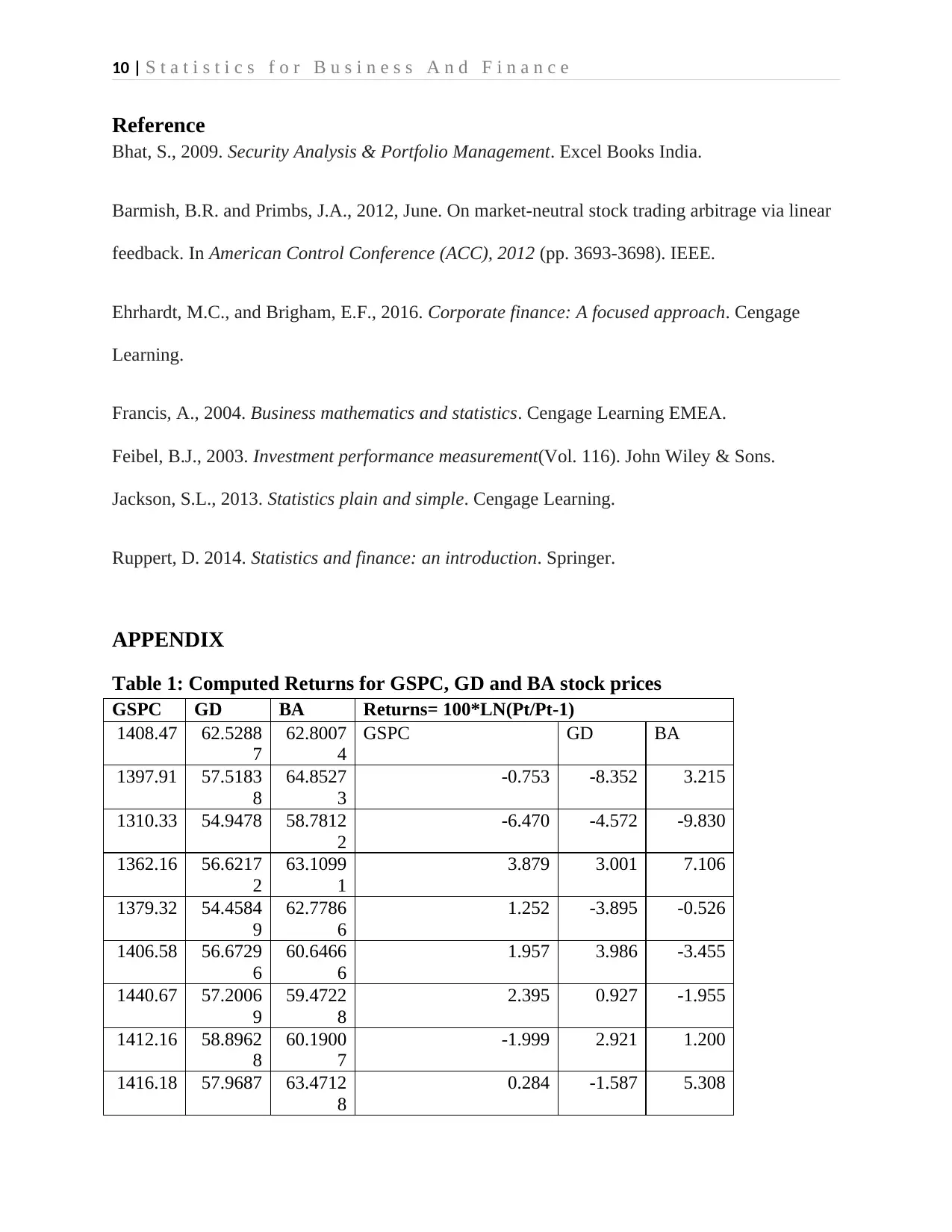

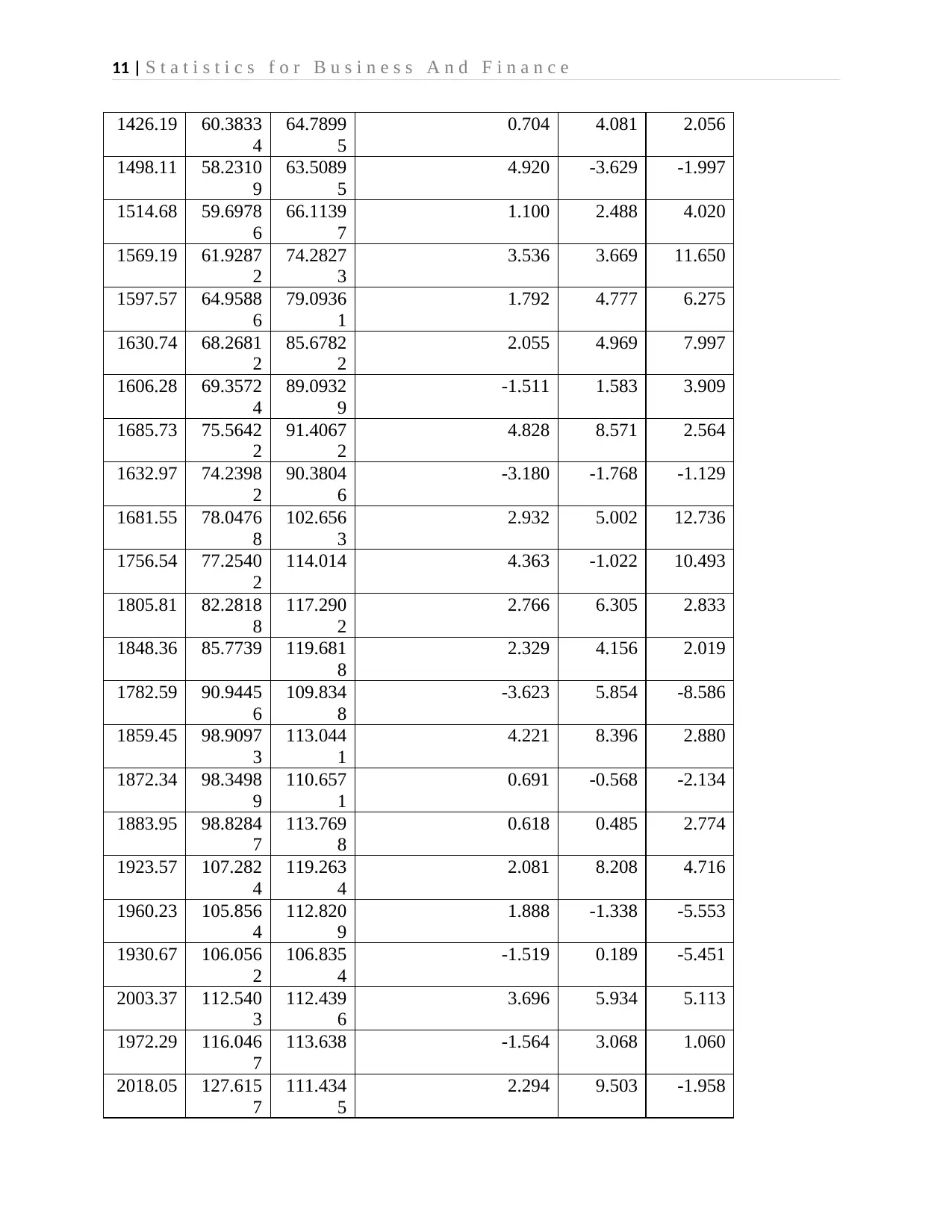

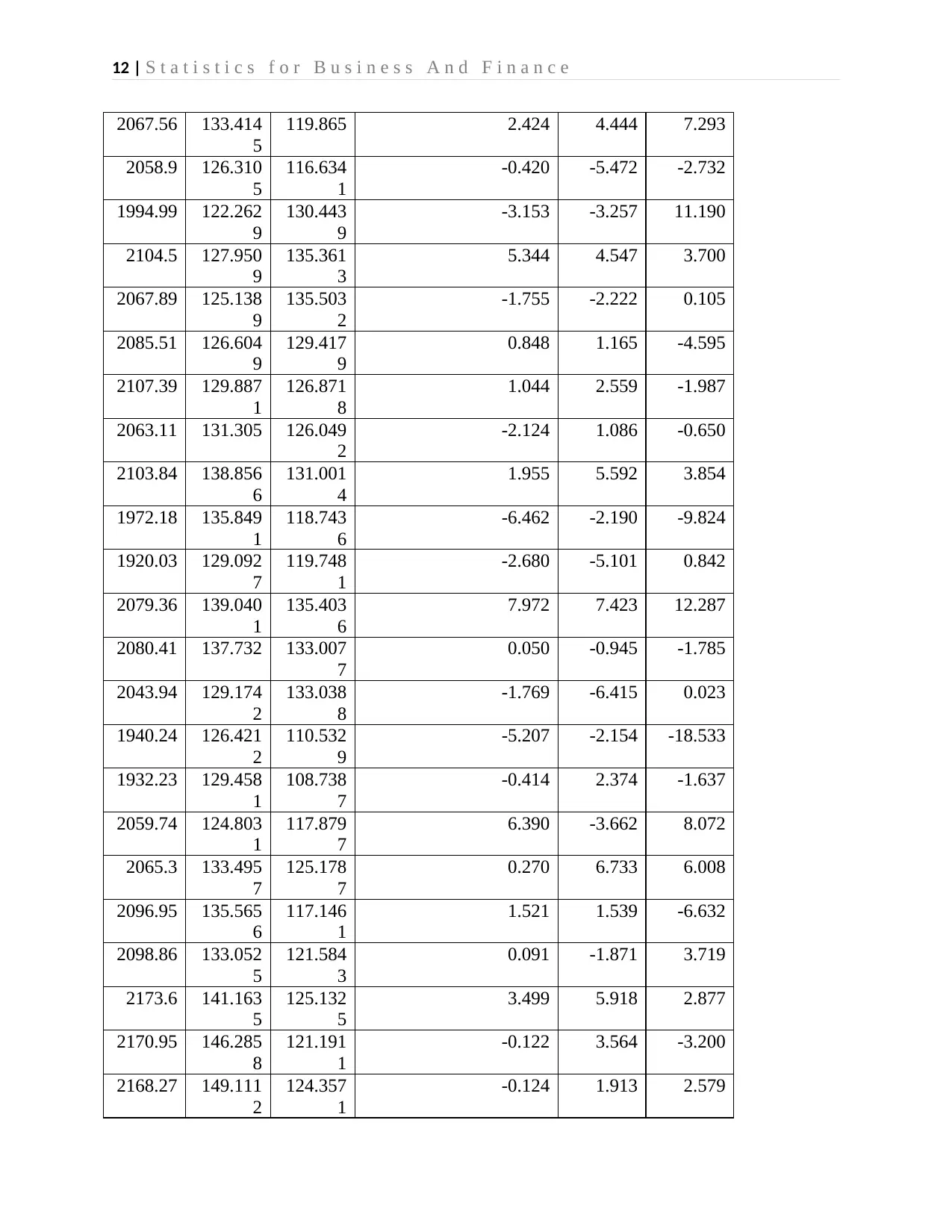

1. Computation of the return of the three series of stock prices

The following formula was used: rt=100∗ln(Pt / Pt−1)

The results of computation are presented in table 1 at the appendix shows

1.1. Jarque-Berra test: Are GD and Boeing Stocks’ Returns normally

distributed or not?

This test was partly done on SPSS.

The table is a summary of the results Skewness and Kurtosis for the Jarque-Berra test

Descriptive Statistics

N Mean Std.

Deviation

Skewness Kurtosis

Statistic Statistic Statistic Statistic Std.

Error

Statistic Std.

Error

GD 60 1.77685 4.497032 .221 .309 .370 .608

BA 60 1.66947 5.927002 -.628 .309 1.277 .608

Valid N

(listwise) 60

Form the Skewness and Kurtosis the Jarque-Berra test will be given by

JB=n { S2

6 + K2

24 }, where S=skewness∧K =kurtosis , n=sample

Data Analysis

The analysis and calculating were done in Microsoft Excel and SPSS software. Below are the

results of the results of data analysis as per the Task.

1. Computation of the return of the three series of stock prices

The following formula was used: rt=100∗ln(Pt / Pt−1)

The results of computation are presented in table 1 at the appendix shows

1.1. Jarque-Berra test: Are GD and Boeing Stocks’ Returns normally

distributed or not?

This test was partly done on SPSS.

The table is a summary of the results Skewness and Kurtosis for the Jarque-Berra test

Descriptive Statistics

N Mean Std.

Deviation

Skewness Kurtosis

Statistic Statistic Statistic Statistic Std.

Error

Statistic Std.

Error

GD 60 1.77685 4.497032 .221 .309 .370 .608

BA 60 1.66947 5.927002 -.628 .309 1.277 .608

Valid N

(listwise) 60

Form the Skewness and Kurtosis the Jarque-Berra test will be given by

JB=n { S2

6 + K2

24 }, where S=skewness∧K =kurtosis , n=sample

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

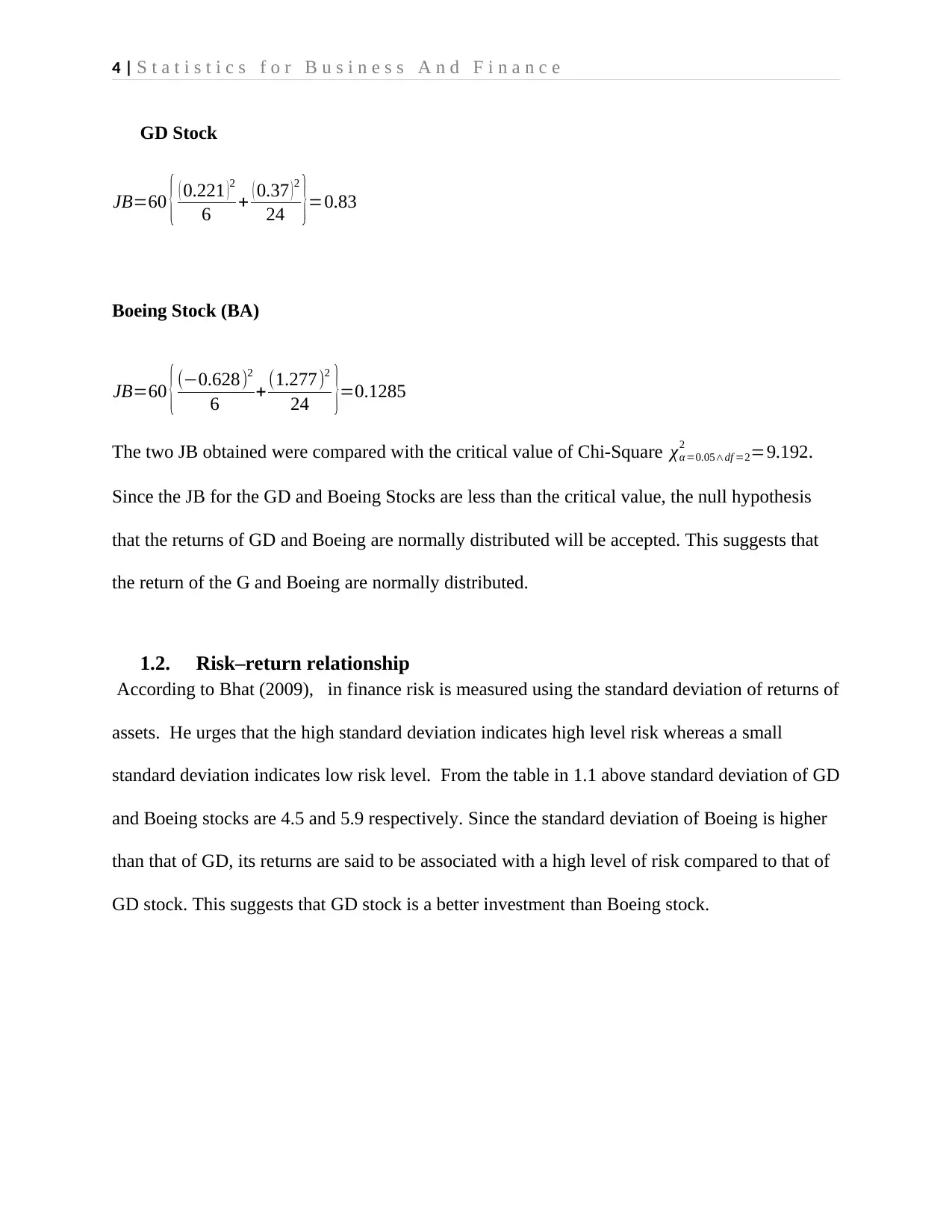

GD Stock

JB=60 { ( 0.221 )2

6 + ( 0.37 )2

24 }=0.83

Boeing Stock (BA)

JB=60 { (−0.628)2

6 + (1.277)2

24 }=0.1285

The two JB obtained were compared with the critical value of Chi-Square χα =0.05∧df =2

2 =9.192.

Since the JB for the GD and Boeing Stocks are less than the critical value, the null hypothesis

that the returns of GD and Boeing are normally distributed will be accepted. This suggests that

the return of the G and Boeing are normally distributed.

1.2. Risk–return relationship

According to Bhat (2009), in finance risk is measured using the standard deviation of returns of

assets. He urges that the high standard deviation indicates high level risk whereas a small

standard deviation indicates low risk level. From the table in 1.1 above standard deviation of GD

and Boeing stocks are 4.5 and 5.9 respectively. Since the standard deviation of Boeing is higher

than that of GD, its returns are said to be associated with a high level of risk compared to that of

GD stock. This suggests that GD stock is a better investment than Boeing stock.

GD Stock

JB=60 { ( 0.221 )2

6 + ( 0.37 )2

24 }=0.83

Boeing Stock (BA)

JB=60 { (−0.628)2

6 + (1.277)2

24 }=0.1285

The two JB obtained were compared with the critical value of Chi-Square χα =0.05∧df =2

2 =9.192.

Since the JB for the GD and Boeing Stocks are less than the critical value, the null hypothesis

that the returns of GD and Boeing are normally distributed will be accepted. This suggests that

the return of the G and Boeing are normally distributed.

1.2. Risk–return relationship

According to Bhat (2009), in finance risk is measured using the standard deviation of returns of

assets. He urges that the high standard deviation indicates high level risk whereas a small

standard deviation indicates low risk level. From the table in 1.1 above standard deviation of GD

and Boeing stocks are 4.5 and 5.9 respectively. Since the standard deviation of Boeing is higher

than that of GD, its returns are said to be associated with a high level of risk compared to that of

GD stock. This suggests that GD stock is a better investment than Boeing stock.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

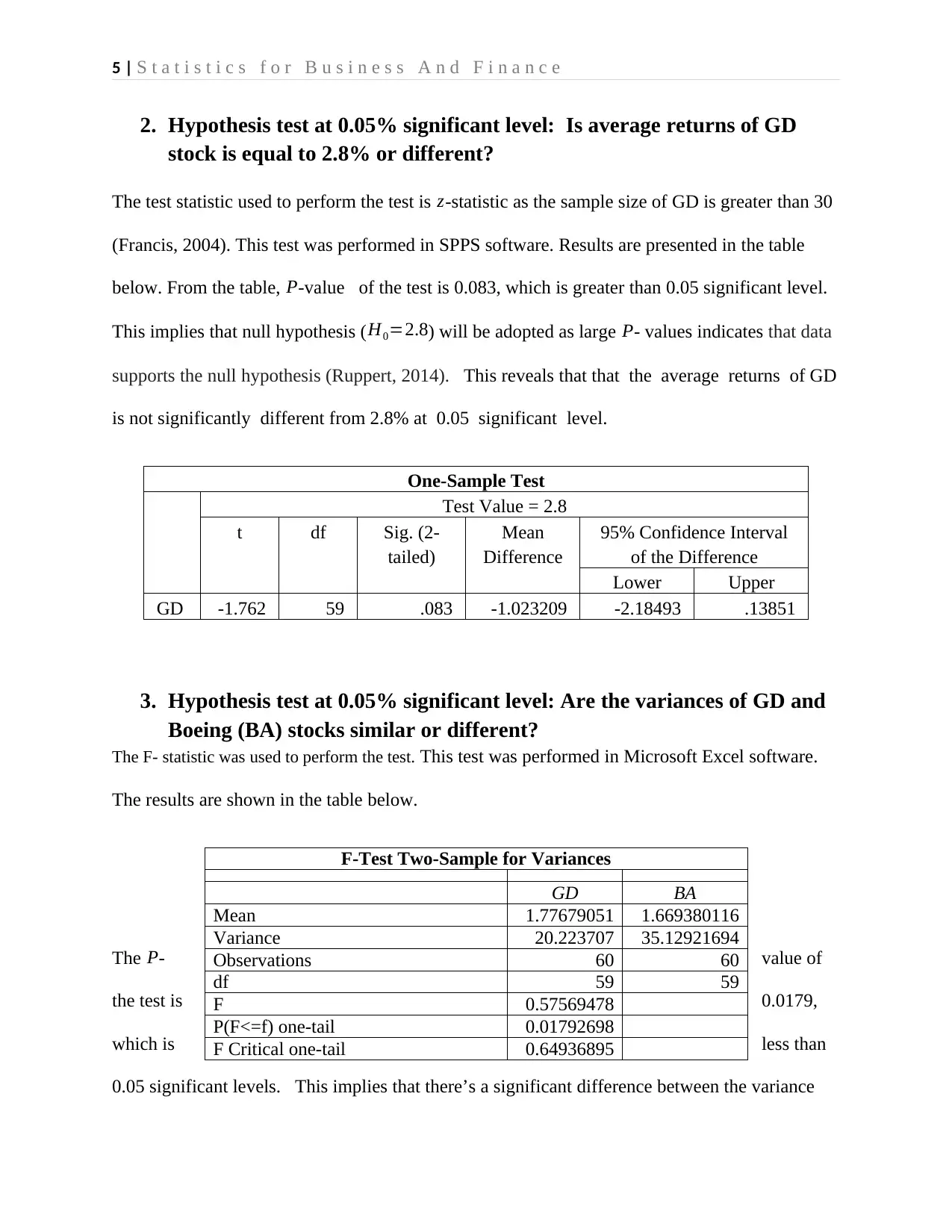

5 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

2. Hypothesis test at 0.05% significant level: Is average returns of GD

stock is equal to 2.8% or different?

The test statistic used to perform the test is z-statistic as the sample size of GD is greater than 30

(Francis, 2004). This test was performed in SPPS software. Results are presented in the table

below. From the table, P-value of the test is 0.083, which is greater than 0.05 significant level.

This implies that null hypothesis ( H0=2.8) will be adopted as large P- values indicates that data

supports the null hypothesis (Ruppert, 2014). This reveals that that the average returns of GD

is not significantly different from 2.8% at 0.05 significant level.

One-Sample Test

Test Value = 2.8

t df Sig. (2-

tailed)

Mean

Difference

95% Confidence Interval

of the Difference

Lower Upper

GD -1.762 59 .083 -1.023209 -2.18493 .13851

3. Hypothesis test at 0.05% significant level: Are the variances of GD and

Boeing (BA) stocks similar or different?

The F- statistic was used to perform the test. This test was performed in Microsoft Excel software.

The results are shown in the table below.

The P- value of

the test is 0.0179,

which is less than

0.05 significant levels. This implies that there’s a significant difference between the variance

F-Test Two-Sample for Variances

GD BA

Mean 1.77679051 1.669380116

Variance 20.223707 35.12921694

Observations 60 60

df 59 59

F 0.57569478

P(F<=f) one-tail 0.01792698

F Critical one-tail 0.64936895

2. Hypothesis test at 0.05% significant level: Is average returns of GD

stock is equal to 2.8% or different?

The test statistic used to perform the test is z-statistic as the sample size of GD is greater than 30

(Francis, 2004). This test was performed in SPPS software. Results are presented in the table

below. From the table, P-value of the test is 0.083, which is greater than 0.05 significant level.

This implies that null hypothesis ( H0=2.8) will be adopted as large P- values indicates that data

supports the null hypothesis (Ruppert, 2014). This reveals that that the average returns of GD

is not significantly different from 2.8% at 0.05 significant level.

One-Sample Test

Test Value = 2.8

t df Sig. (2-

tailed)

Mean

Difference

95% Confidence Interval

of the Difference

Lower Upper

GD -1.762 59 .083 -1.023209 -2.18493 .13851

3. Hypothesis test at 0.05% significant level: Are the variances of GD and

Boeing (BA) stocks similar or different?

The F- statistic was used to perform the test. This test was performed in Microsoft Excel software.

The results are shown in the table below.

The P- value of

the test is 0.0179,

which is less than

0.05 significant levels. This implies that there’s a significant difference between the variance

F-Test Two-Sample for Variances

GD BA

Mean 1.77679051 1.669380116

Variance 20.223707 35.12921694

Observations 60 60

df 59 59

F 0.57569478

P(F<=f) one-tail 0.01792698

F Critical one-tail 0.64936895

6 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

returns of GD and BA stock, which has been revealed by respective variances of the 20.22 and

96.47. High variance value an indicator of high risk while variance indicates low risks (Ehrhardt

& Brigham 2016). This implies that the returns of GD are associated with low risks due to

smaller variance whereas returns will be associated with higher risks.

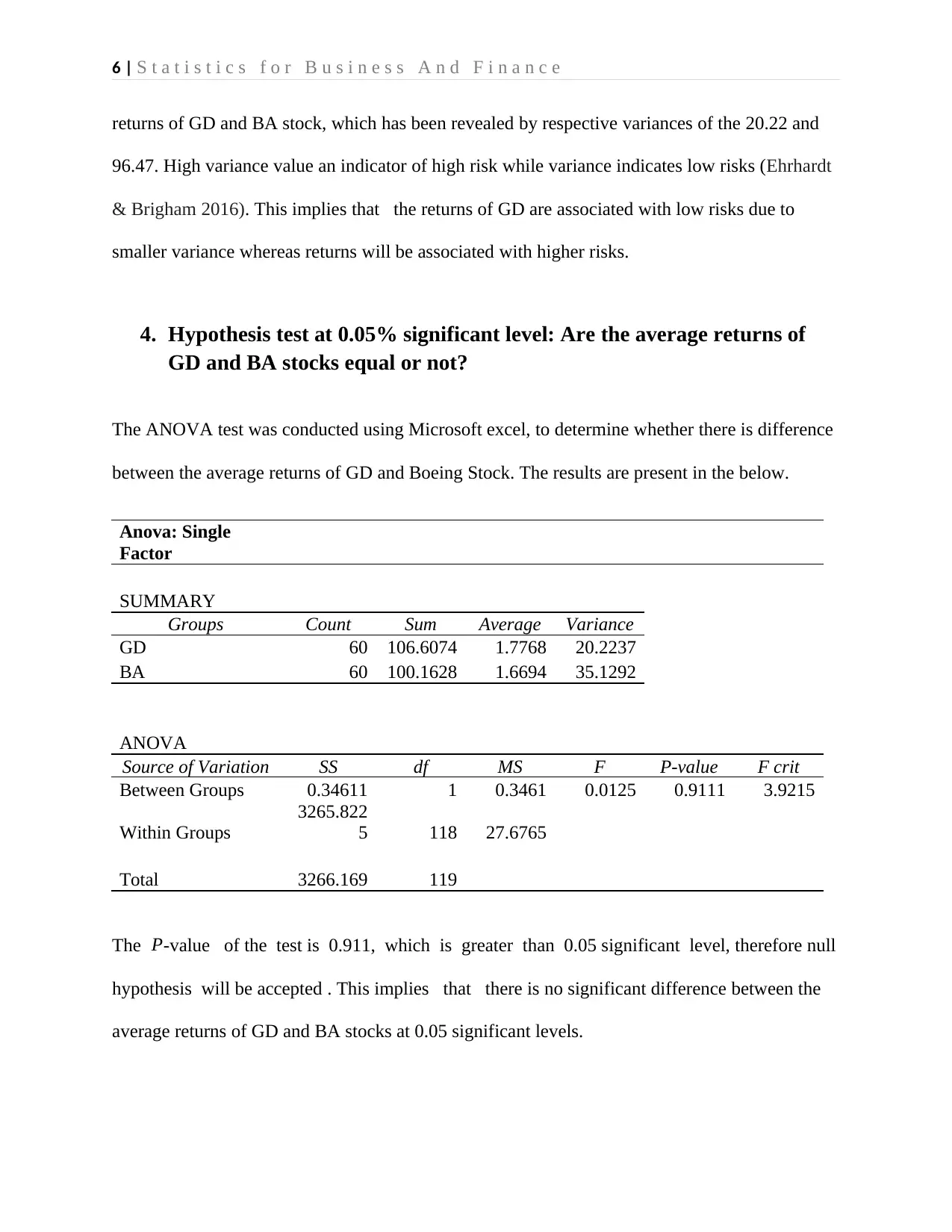

4. Hypothesis test at 0.05% significant level: Are the average returns of

GD and BA stocks equal or not?

The ANOVA test was conducted using Microsoft excel, to determine whether there is difference

between the average returns of GD and Boeing Stock. The results are present in the below.

Anova: Single

Factor

SUMMARY

Groups Count Sum Average Variance

GD 60 106.6074 1.7768 20.2237

BA 60 100.1628 1.6694 35.1292

ANOVA

Source of Variation SS df MS F P-value F crit

Between Groups 0.34611 1 0.3461 0.0125 0.9111 3.9215

Within Groups

3265.822

5 118 27.6765

Total 3266.169 119

The P-value of the test is 0.911, which is greater than 0.05 significant level, therefore null

hypothesis will be accepted . This implies that there is no significant difference between the

average returns of GD and BA stocks at 0.05 significant levels.

returns of GD and BA stock, which has been revealed by respective variances of the 20.22 and

96.47. High variance value an indicator of high risk while variance indicates low risks (Ehrhardt

& Brigham 2016). This implies that the returns of GD are associated with low risks due to

smaller variance whereas returns will be associated with higher risks.

4. Hypothesis test at 0.05% significant level: Are the average returns of

GD and BA stocks equal or not?

The ANOVA test was conducted using Microsoft excel, to determine whether there is difference

between the average returns of GD and Boeing Stock. The results are present in the below.

Anova: Single

Factor

SUMMARY

Groups Count Sum Average Variance

GD 60 106.6074 1.7768 20.2237

BA 60 100.1628 1.6694 35.1292

ANOVA

Source of Variation SS df MS F P-value F crit

Between Groups 0.34611 1 0.3461 0.0125 0.9111 3.9215

Within Groups

3265.822

5 118 27.6765

Total 3266.169 119

The P-value of the test is 0.911, which is greater than 0.05 significant level, therefore null

hypothesis will be accepted . This implies that there is no significant difference between the

average returns of GD and BA stocks at 0.05 significant levels.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

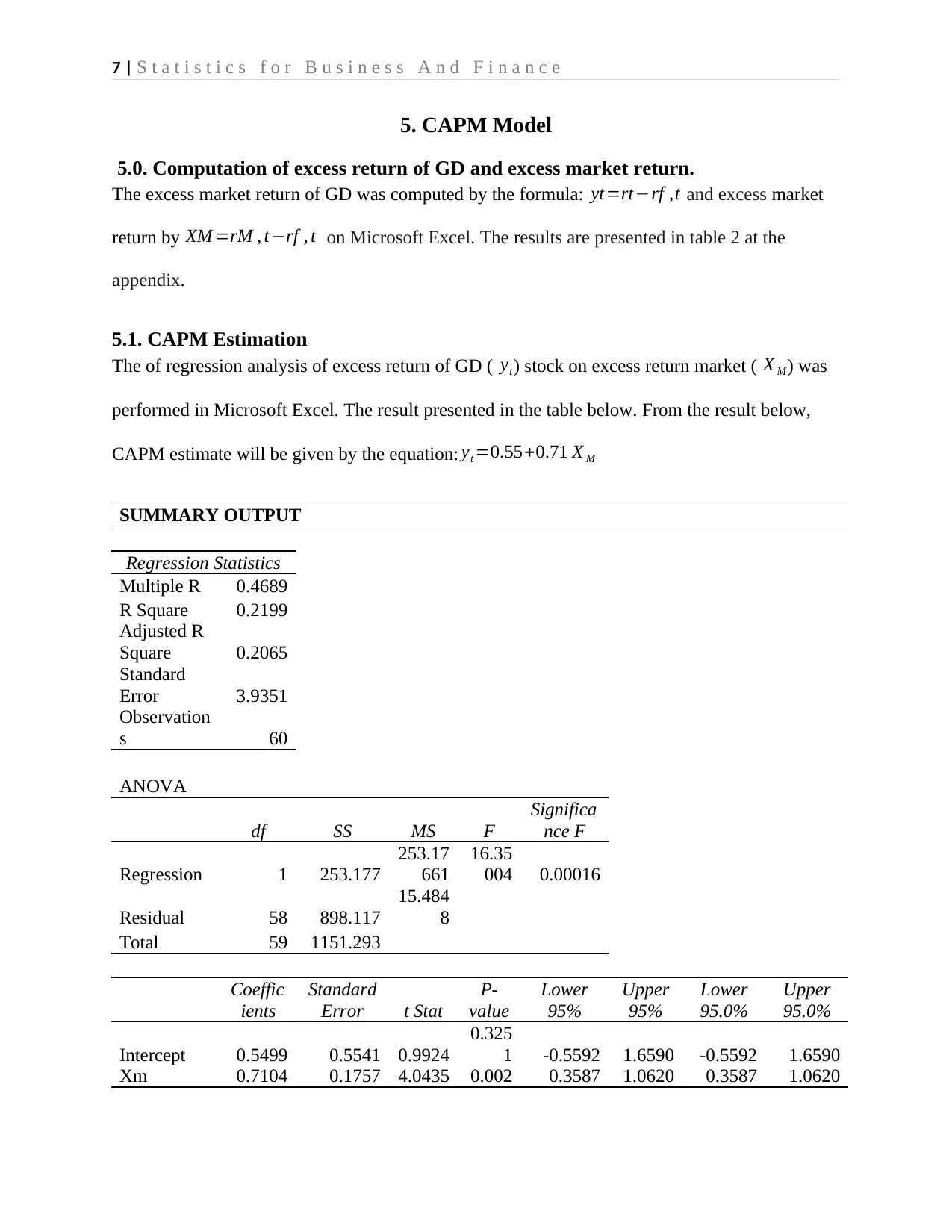

5. CAPM Model

5.0. Computation of excess return of GD and excess market return.

The excess market return of GD was computed by the formula: yt=rt−rf ,t and excess market

return by XM =rM , t−rf , t on Microsoft Excel. The results are presented in table 2 at the

appendix.

5.1. CAPM Estimation

The of regression analysis of excess return of GD ( yt) stock on excess return market ( X M) was

performed in Microsoft Excel. The result presented in the table below. From the result below,

CAPM estimate will be given by the equation: yt =0.55+0.71 X M

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.4689

R Square 0.2199

Adjusted R

Square 0.2065

Standard

Error 3.9351

Observation

s 60

ANOVA

df SS MS F

Significa

nce F

Regression 1 253.177

253.17

661

16.35

004 0.00016

Residual 58 898.117

15.484

8

Total 59 1151.293

Coeffic

ients

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.5499 0.5541 0.9924

0.325

1 -0.5592 1.6590 -0.5592 1.6590

Xm 0.7104 0.1757 4.0435 0.002 0.3587 1.0620 0.3587 1.0620

5. CAPM Model

5.0. Computation of excess return of GD and excess market return.

The excess market return of GD was computed by the formula: yt=rt−rf ,t and excess market

return by XM =rM , t−rf , t on Microsoft Excel. The results are presented in table 2 at the

appendix.

5.1. CAPM Estimation

The of regression analysis of excess return of GD ( yt) stock on excess return market ( X M) was

performed in Microsoft Excel. The result presented in the table below. From the result below,

CAPM estimate will be given by the equation: yt =0.55+0.71 X M

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.4689

R Square 0.2199

Adjusted R

Square 0.2065

Standard

Error 3.9351

Observation

s 60

ANOVA

df SS MS F

Significa

nce F

Regression 1 253.177

253.17

661

16.35

004 0.00016

Residual 58 898.117

15.484

8

Total 59 1151.293

Coeffic

ients

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.5499 0.5541 0.9924

0.325

1 -0.5592 1.6590 -0.5592 1.6590

Xm 0.7104 0.1757 4.0435 0.002 0.3587 1.0620 0.3587 1.0620

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

5.2. Interpretation of CAPM Beta

The CAPM Beta is given by the coefficient of excess market return (X M ), 0.71. This beta is less

than, indicating that the price of GD stock is less volatile than the market price (Feibel 2003).

This is an indicator of minimal risks associated with GD returns.

5.3. Interpretation of R2

The value of R2 is 0.2199%. R2 measures the variation of between the variable data and the

fitted values, R2 closer to 100% indicates that the model explains all the variations between

them (Jackson, 2013 ) . Since 0.2199 % is not close to 100% all the variations of excess return

of GD stock are not well fitted by the regression model.

5.4. Interpretation of confidence interval for CAPM Beta

From the table above the 95% confidence interval of CAPM Beta is (0.3587, 1.062). This

indicates that the volatility of the price of GD in the stock markets ranges between 0.3587 and

1.062

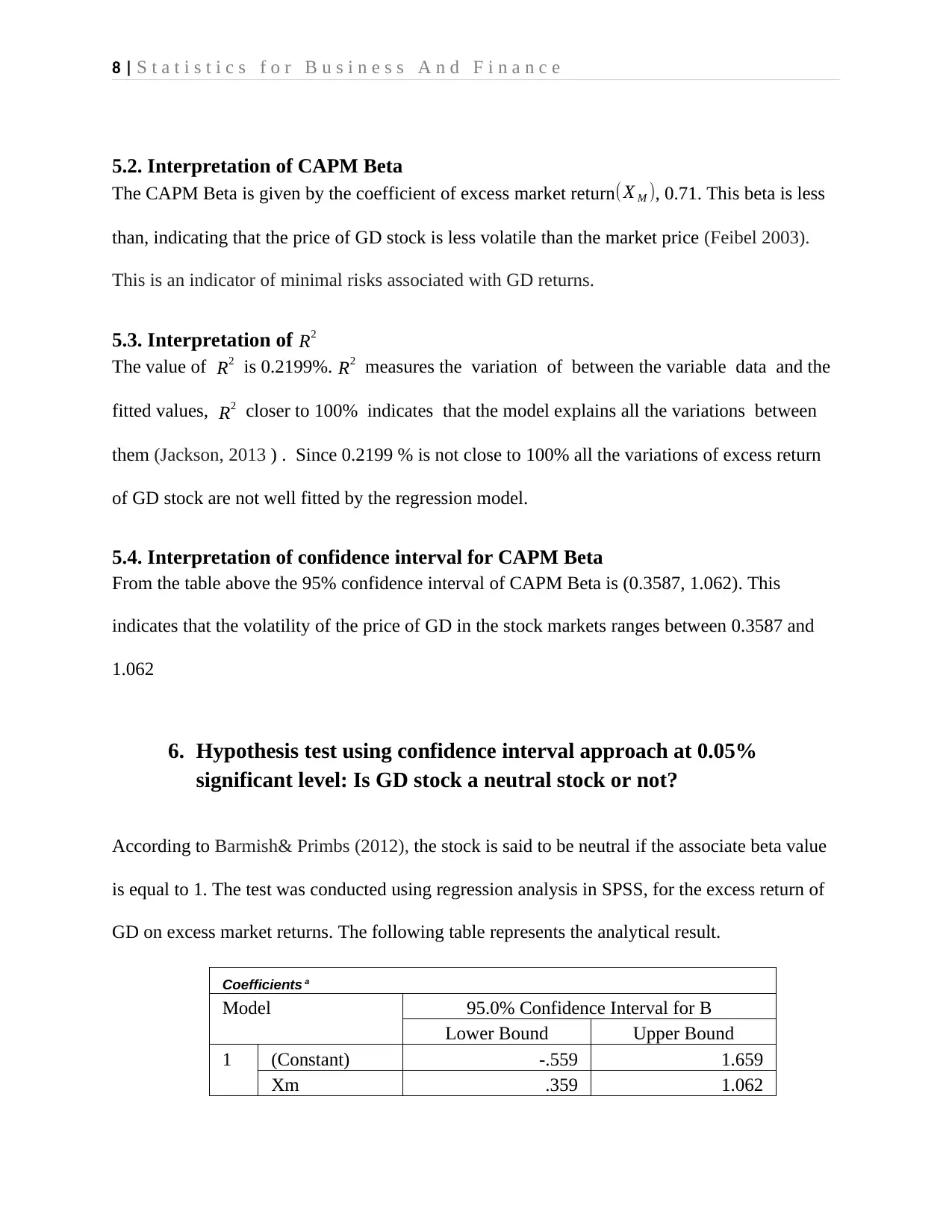

6. Hypothesis test using confidence interval approach at 0.05%

significant level: Is GD stock a neutral stock or not?

According to Barmish& Primbs (2012), the stock is said to be neutral if the associate beta value

is equal to 1. The test was conducted using regression analysis in SPSS, for the excess return of

GD on excess market returns. The following table represents the analytical result.

Coefficients a

Model 95.0% Confidence Interval for B

Lower Bound Upper Bound

1 (Constant) -.559 1.659

Xm .359 1.062

5.2. Interpretation of CAPM Beta

The CAPM Beta is given by the coefficient of excess market return (X M ), 0.71. This beta is less

than, indicating that the price of GD stock is less volatile than the market price (Feibel 2003).

This is an indicator of minimal risks associated with GD returns.

5.3. Interpretation of R2

The value of R2 is 0.2199%. R2 measures the variation of between the variable data and the

fitted values, R2 closer to 100% indicates that the model explains all the variations between

them (Jackson, 2013 ) . Since 0.2199 % is not close to 100% all the variations of excess return

of GD stock are not well fitted by the regression model.

5.4. Interpretation of confidence interval for CAPM Beta

From the table above the 95% confidence interval of CAPM Beta is (0.3587, 1.062). This

indicates that the volatility of the price of GD in the stock markets ranges between 0.3587 and

1.062

6. Hypothesis test using confidence interval approach at 0.05%

significant level: Is GD stock a neutral stock or not?

According to Barmish& Primbs (2012), the stock is said to be neutral if the associate beta value

is equal to 1. The test was conducted using regression analysis in SPSS, for the excess return of

GD on excess market returns. The following table represents the analytical result.

Coefficients a

Model 95.0% Confidence Interval for B

Lower Bound Upper Bound

1 (Constant) -.559 1.659

Xm .359 1.062

9 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

From the table above the confidence interval of the beta, the coefficient is (0.359, 1.062). Since

1 is within the confidence interval, then the null hypothesis that the stock GD is a neutral stock

will be adopted. This clearly reveals that GD stock is neutral stock.

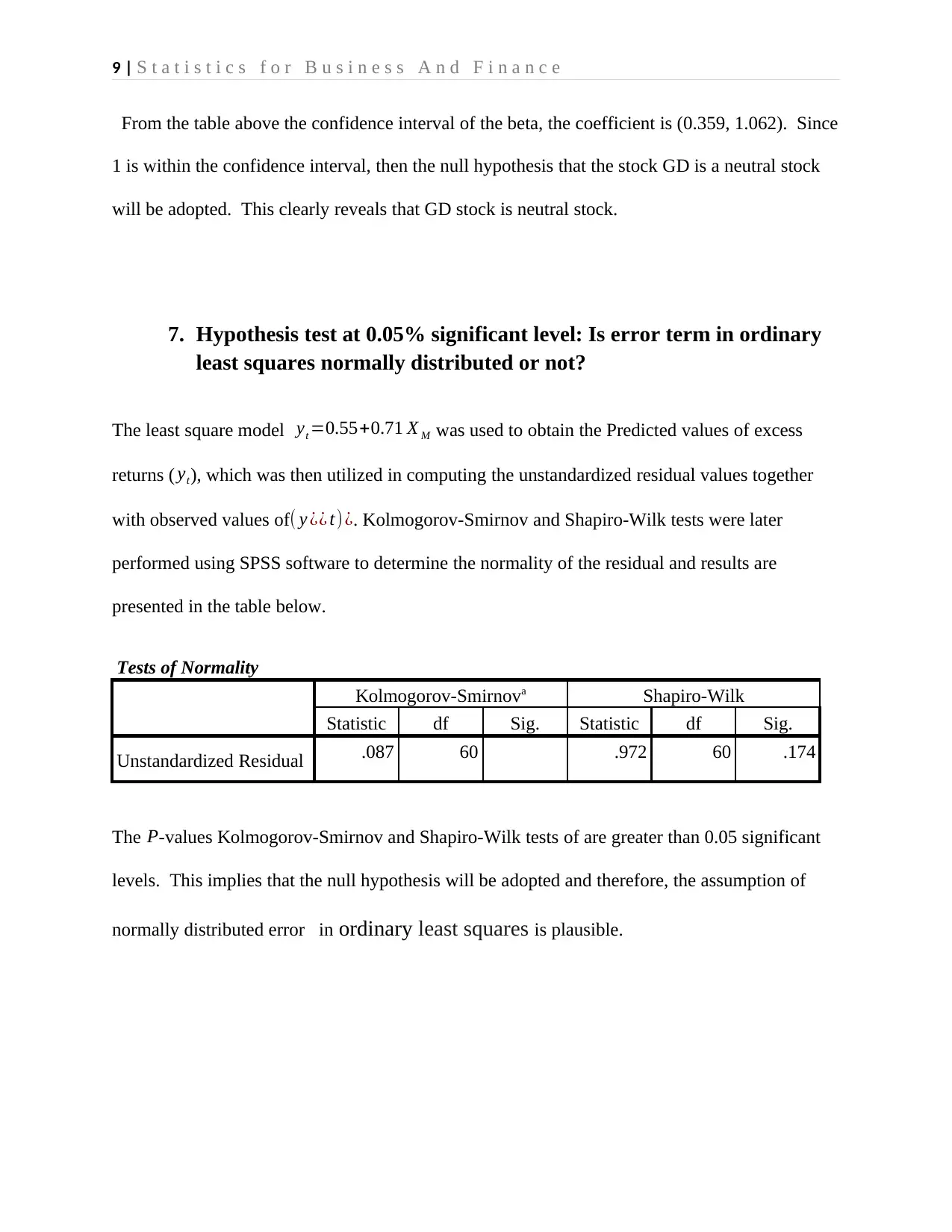

7. Hypothesis test at 0.05% significant level: Is error term in ordinary

least squares normally distributed or not?

The least square model yt =0.55+0.71 X M was used to obtain the Predicted values of excess

returns ( yt), which was then utilized in computing the unstandardized residual values together

with observed values of( y ¿¿ t) ¿. Kolmogorov-Smirnov and Shapiro-Wilk tests were later

performed using SPSS software to determine the normality of the residual and results are

presented in the table below.

Tests of Normality

Kolmogorov-Smirnova Shapiro-Wilk

Statistic df Sig. Statistic df Sig.

Unstandardized Residual .087 60 .972 60 .174

The P-values Kolmogorov-Smirnov and Shapiro-Wilk tests of are greater than 0.05 significant

levels. This implies that the null hypothesis will be adopted and therefore, the assumption of

normally distributed error in ordinary least squares is plausible.

From the table above the confidence interval of the beta, the coefficient is (0.359, 1.062). Since

1 is within the confidence interval, then the null hypothesis that the stock GD is a neutral stock

will be adopted. This clearly reveals that GD stock is neutral stock.

7. Hypothesis test at 0.05% significant level: Is error term in ordinary

least squares normally distributed or not?

The least square model yt =0.55+0.71 X M was used to obtain the Predicted values of excess

returns ( yt), which was then utilized in computing the unstandardized residual values together

with observed values of( y ¿¿ t) ¿. Kolmogorov-Smirnov and Shapiro-Wilk tests were later

performed using SPSS software to determine the normality of the residual and results are

presented in the table below.

Tests of Normality

Kolmogorov-Smirnova Shapiro-Wilk

Statistic df Sig. Statistic df Sig.

Unstandardized Residual .087 60 .972 60 .174

The P-values Kolmogorov-Smirnov and Shapiro-Wilk tests of are greater than 0.05 significant

levels. This implies that the null hypothesis will be adopted and therefore, the assumption of

normally distributed error in ordinary least squares is plausible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

Reference

Bhat, S., 2009. Security Analysis & Portfolio Management. Excel Books India.

Barmish, B.R. and Primbs, J.A., 2012, June. On market-neutral stock trading arbitrage via linear

feedback. In American Control Conference (ACC), 2012 (pp. 3693-3698). IEEE.

Ehrhardt, M.C., and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

Learning.

Francis, A., 2004. Business mathematics and statistics. Cengage Learning EMEA.

Feibel, B.J., 2003. Investment performance measurement(Vol. 116). John Wiley & Sons.

Jackson, S.L., 2013. Statistics plain and simple. Cengage Learning.

Ruppert, D. 2014. Statistics and finance: an introduction. Springer.

APPENDIX

Table 1: Computed Returns for GSPC, GD and BA stock prices

GSPC GD BA Returns= 100*LN(Pt/Pt-1)

1408.47 62.5288

7

62.8007

4

GSPC GD BA

1397.91 57.5183

8

64.8527

3

-0.753 -8.352 3.215

1310.33 54.9478 58.7812

2

-6.470 -4.572 -9.830

1362.16 56.6217

2

63.1099

1

3.879 3.001 7.106

1379.32 54.4584

9

62.7786

6

1.252 -3.895 -0.526

1406.58 56.6729

6

60.6466

6

1.957 3.986 -3.455

1440.67 57.2006

9

59.4722

8

2.395 0.927 -1.955

1412.16 58.8962

8

60.1900

7

-1.999 2.921 1.200

1416.18 57.9687 63.4712

8

0.284 -1.587 5.308

Reference

Bhat, S., 2009. Security Analysis & Portfolio Management. Excel Books India.

Barmish, B.R. and Primbs, J.A., 2012, June. On market-neutral stock trading arbitrage via linear

feedback. In American Control Conference (ACC), 2012 (pp. 3693-3698). IEEE.

Ehrhardt, M.C., and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

Learning.

Francis, A., 2004. Business mathematics and statistics. Cengage Learning EMEA.

Feibel, B.J., 2003. Investment performance measurement(Vol. 116). John Wiley & Sons.

Jackson, S.L., 2013. Statistics plain and simple. Cengage Learning.

Ruppert, D. 2014. Statistics and finance: an introduction. Springer.

APPENDIX

Table 1: Computed Returns for GSPC, GD and BA stock prices

GSPC GD BA Returns= 100*LN(Pt/Pt-1)

1408.47 62.5288

7

62.8007

4

GSPC GD BA

1397.91 57.5183

8

64.8527

3

-0.753 -8.352 3.215

1310.33 54.9478 58.7812

2

-6.470 -4.572 -9.830

1362.16 56.6217

2

63.1099

1

3.879 3.001 7.106

1379.32 54.4584

9

62.7786

6

1.252 -3.895 -0.526

1406.58 56.6729

6

60.6466

6

1.957 3.986 -3.455

1440.67 57.2006

9

59.4722

8

2.395 0.927 -1.955

1412.16 58.8962

8

60.1900

7

-1.999 2.921 1.200

1416.18 57.9687 63.4712

8

0.284 -1.587 5.308

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

1426.19 60.3833

4

64.7899

5

0.704 4.081 2.056

1498.11 58.2310

9

63.5089

5

4.920 -3.629 -1.997

1514.68 59.6978

6

66.1139

7

1.100 2.488 4.020

1569.19 61.9287

2

74.2827

3

3.536 3.669 11.650

1597.57 64.9588

6

79.0936

1

1.792 4.777 6.275

1630.74 68.2681

2

85.6782

2

2.055 4.969 7.997

1606.28 69.3572

4

89.0932

9

-1.511 1.583 3.909

1685.73 75.5642

2

91.4067

2

4.828 8.571 2.564

1632.97 74.2398

2

90.3804

6

-3.180 -1.768 -1.129

1681.55 78.0476

8

102.656

3

2.932 5.002 12.736

1756.54 77.2540

2

114.014 4.363 -1.022 10.493

1805.81 82.2818

8

117.290

2

2.766 6.305 2.833

1848.36 85.7739 119.681

8

2.329 4.156 2.019

1782.59 90.9445

6

109.834

8

-3.623 5.854 -8.586

1859.45 98.9097

3

113.044

1

4.221 8.396 2.880

1872.34 98.3498

9

110.657

1

0.691 -0.568 -2.134

1883.95 98.8284

7

113.769

8

0.618 0.485 2.774

1923.57 107.282

4

119.263

4

2.081 8.208 4.716

1960.23 105.856

4

112.820

9

1.888 -1.338 -5.553

1930.67 106.056

2

106.835

4

-1.519 0.189 -5.451

2003.37 112.540

3

112.439

6

3.696 5.934 5.113

1972.29 116.046

7

113.638 -1.564 3.068 1.060

2018.05 127.615

7

111.434

5

2.294 9.503 -1.958

1426.19 60.3833

4

64.7899

5

0.704 4.081 2.056

1498.11 58.2310

9

63.5089

5

4.920 -3.629 -1.997

1514.68 59.6978

6

66.1139

7

1.100 2.488 4.020

1569.19 61.9287

2

74.2827

3

3.536 3.669 11.650

1597.57 64.9588

6

79.0936

1

1.792 4.777 6.275

1630.74 68.2681

2

85.6782

2

2.055 4.969 7.997

1606.28 69.3572

4

89.0932

9

-1.511 1.583 3.909

1685.73 75.5642

2

91.4067

2

4.828 8.571 2.564

1632.97 74.2398

2

90.3804

6

-3.180 -1.768 -1.129

1681.55 78.0476

8

102.656

3

2.932 5.002 12.736

1756.54 77.2540

2

114.014 4.363 -1.022 10.493

1805.81 82.2818

8

117.290

2

2.766 6.305 2.833

1848.36 85.7739 119.681

8

2.329 4.156 2.019

1782.59 90.9445

6

109.834

8

-3.623 5.854 -8.586

1859.45 98.9097

3

113.044

1

4.221 8.396 2.880

1872.34 98.3498

9

110.657

1

0.691 -0.568 -2.134

1883.95 98.8284

7

113.769

8

0.618 0.485 2.774

1923.57 107.282

4

119.263

4

2.081 8.208 4.716

1960.23 105.856

4

112.820

9

1.888 -1.338 -5.553

1930.67 106.056

2

106.835

4

-1.519 0.189 -5.451

2003.37 112.540

3

112.439

6

3.696 5.934 5.113

1972.29 116.046

7

113.638 -1.564 3.068 1.060

2018.05 127.615

7

111.434

5

2.294 9.503 -1.958

12 | S t a t i s t i c s f o r B u s i n e s s A n d F i n a n c e

2067.56 133.414

5

119.865 2.424 4.444 7.293

2058.9 126.310

5

116.634

1

-0.420 -5.472 -2.732

1994.99 122.262

9

130.443

9

-3.153 -3.257 11.190

2104.5 127.950

9

135.361

3

5.344 4.547 3.700

2067.89 125.138

9

135.503

2

-1.755 -2.222 0.105

2085.51 126.604

9

129.417

9

0.848 1.165 -4.595

2107.39 129.887

1

126.871

8

1.044 2.559 -1.987

2063.11 131.305 126.049

2

-2.124 1.086 -0.650

2103.84 138.856

6

131.001

4

1.955 5.592 3.854

1972.18 135.849

1

118.743

6

-6.462 -2.190 -9.824

1920.03 129.092

7

119.748

1

-2.680 -5.101 0.842

2079.36 139.040

1

135.403

6

7.972 7.423 12.287

2080.41 137.732 133.007

7

0.050 -0.945 -1.785

2043.94 129.174

2

133.038

8

-1.769 -6.415 0.023

1940.24 126.421

2

110.532

9

-5.207 -2.154 -18.533

1932.23 129.458

1

108.738

7

-0.414 2.374 -1.637

2059.74 124.803

1

117.879

7

6.390 -3.662 8.072

2065.3 133.495

7

125.178

7

0.270 6.733 6.008

2096.95 135.565

6

117.146

1

1.521 1.539 -6.632

2098.86 133.052

5

121.584

3

0.091 -1.871 3.719

2173.6 141.163

5

125.132

5

3.499 5.918 2.877

2170.95 146.285

8

121.191

1

-0.122 3.564 -3.200

2168.27 149.111

2

124.357

1

-0.124 1.913 2.579

2067.56 133.414

5

119.865 2.424 4.444 7.293

2058.9 126.310

5

116.634

1

-0.420 -5.472 -2.732

1994.99 122.262

9

130.443

9

-3.153 -3.257 11.190

2104.5 127.950

9

135.361

3

5.344 4.547 3.700

2067.89 125.138

9

135.503

2

-1.755 -2.222 0.105

2085.51 126.604

9

129.417

9

0.848 1.165 -4.595

2107.39 129.887

1

126.871

8

1.044 2.559 -1.987

2063.11 131.305 126.049

2

-2.124 1.086 -0.650

2103.84 138.856

6

131.001

4

1.955 5.592 3.854

1972.18 135.849

1

118.743

6

-6.462 -2.190 -9.824

1920.03 129.092

7

119.748

1

-2.680 -5.101 0.842

2079.36 139.040

1

135.403

6

7.972 7.423 12.287

2080.41 137.732 133.007

7

0.050 -0.945 -1.785

2043.94 129.174

2

133.038

8

-1.769 -6.415 0.023

1940.24 126.421

2

110.532

9

-5.207 -2.154 -18.533

1932.23 129.458

1

108.738

7

-0.414 2.374 -1.637

2059.74 124.803

1

117.879

7

6.390 -3.662 8.072

2065.3 133.495

7

125.178

7

0.270 6.733 6.008

2096.95 135.565

6

117.146

1

1.521 1.539 -6.632

2098.86 133.052

5

121.584

3

0.091 -1.871 3.719

2173.6 141.163

5

125.132

5

3.499 5.918 2.877

2170.95 146.285

8

121.191

1

-0.122 3.564 -3.200

2168.27 149.111

2

124.357

1

-0.124 1.913 2.579

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.