Citibank Stock Index Investment Case Study: Financial Analysis

VerifiedAdded on 2019/10/08

|4

|683

|298

Case Study

AI Summary

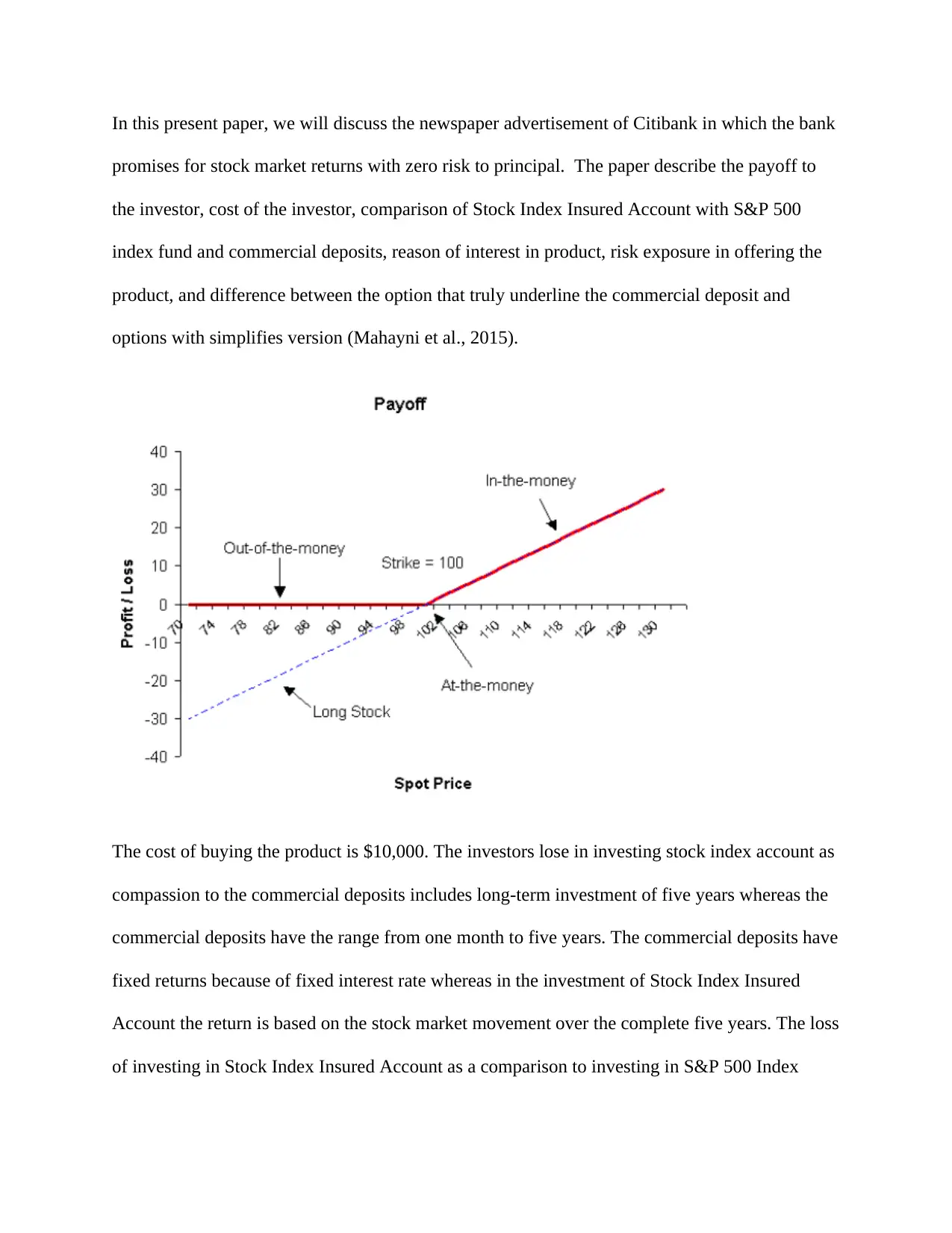

This case study examines Citibank's stock index investment product, focusing on its features, risks, and comparison with other investment options. The analysis covers the product's payoff, cost to investors, and a comparison with S&P 500 index funds and commercial deposits. It explores the reasons for investor interest, risk exposure, and the differences between options underlying commercial deposits and simplified options. The study highlights the benefits of zero-risk principal and the potential for high returns, while also addressing the bank's risk management strategies. References include Mahayni & Muck (2015), Chan, Kot, & Tang (2013), and Miao (2014).

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.