Statistical Analysis of Boeing and IBM Stock Returns: A Finance Report

VerifiedAdded on 2020/05/16

|13

|3814

|251

Report

AI Summary

This report delves into the volatility and risk inherent in the stock market, focusing on the analysis of price indexes for Boeing (BA) and International Business Machines (IBM) from December 2010 to May 2016. The study incorporates the S&P500 index and the 10-year US Treasury Bill to evaluate market performance, employing the Capital Asset Pricing Model (CAPM). The report examines line charts of close prices, calculates returns, and performs summary statistics, including Jarque-Bera tests for normality. It tests average returns, compares risks associated with BA and IBM, and analyzes average returns using z-tests and t-tests. The report also includes a CAPM calculation using linear regression, interpreting coefficients and constructing confidence intervals, and concludes with a discussion on preferable neutral price returns and a normal probability plot in OLS. The statistical analysis is conducted to assess the relationship between risk and return for the selected stocks, providing insights into investment strategies and market dynamics.

Running head: STATISTICS FOR BUSINESS AND FINANCE

Statistics for Business and Finance

Name of the Student:

Name of the University:

Author’s note:

Statistics for Business and Finance

Name of the Student:

Name of the University:

Author’s note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1STATISTICS FOR BUSINESS AND FINANCE

Table of Contents

Introduction:................................................................................................................................................................................................2

Discussion and Data Analysis:....................................................................................................................................................................2

1. Line Charts of Close prices:.............................................................................................................................................................2

2. Calculation with return prices:..........................................................................................................................................................3

2.a. Calculation of returns:...................................................................................................................................................................3

2.b. Summary Statistics:......................................................................................................................................................................5

2.c. Jarque - Bera test of normality:.....................................................................................................................................................5

3. Testing of average return price of Boeing:.......................................................................................................................................5

4. Comparison of risk associated to each of the BA and IBM price returns:.......................................................................................6

5. Comparison of average returns of each of the two investing price returns:.....................................................................................6

6. Calculation of Excess Return and Excess Return:............................................................................................................................8

7. CAPM calculation by linear regression method:..............................................................................................................................9

7.a. Estimation of CAPM using linear regression:..............................................................................................................................9

7.b. Interpretation of Coefficients:.....................................................................................................................................................10

7.c. Interpretation of R2:.....................................................................................................................................................................10

7.d. Construction of 95% confidence interval for Slope Efficient:...................................................................................................11

8. Preferable neutral Price Return:......................................................................................................................................................11

9. Normal Probability Plot in OLS:....................................................................................................................................................11

Annotated Bibliography:...........................................................................................................................................................................13

Table of Contents

Introduction:................................................................................................................................................................................................2

Discussion and Data Analysis:....................................................................................................................................................................2

1. Line Charts of Close prices:.............................................................................................................................................................2

2. Calculation with return prices:..........................................................................................................................................................3

2.a. Calculation of returns:...................................................................................................................................................................3

2.b. Summary Statistics:......................................................................................................................................................................5

2.c. Jarque - Bera test of normality:.....................................................................................................................................................5

3. Testing of average return price of Boeing:.......................................................................................................................................5

4. Comparison of risk associated to each of the BA and IBM price returns:.......................................................................................6

5. Comparison of average returns of each of the two investing price returns:.....................................................................................6

6. Calculation of Excess Return and Excess Return:............................................................................................................................8

7. CAPM calculation by linear regression method:..............................................................................................................................9

7.a. Estimation of CAPM using linear regression:..............................................................................................................................9

7.b. Interpretation of Coefficients:.....................................................................................................................................................10

7.c. Interpretation of R2:.....................................................................................................................................................................10

7.d. Construction of 95% confidence interval for Slope Efficient:...................................................................................................11

8. Preferable neutral Price Return:......................................................................................................................................................11

9. Normal Probability Plot in OLS:....................................................................................................................................................11

Annotated Bibliography:...........................................................................................................................................................................13

2STATISTICS FOR BUSINESS AND FINANCE

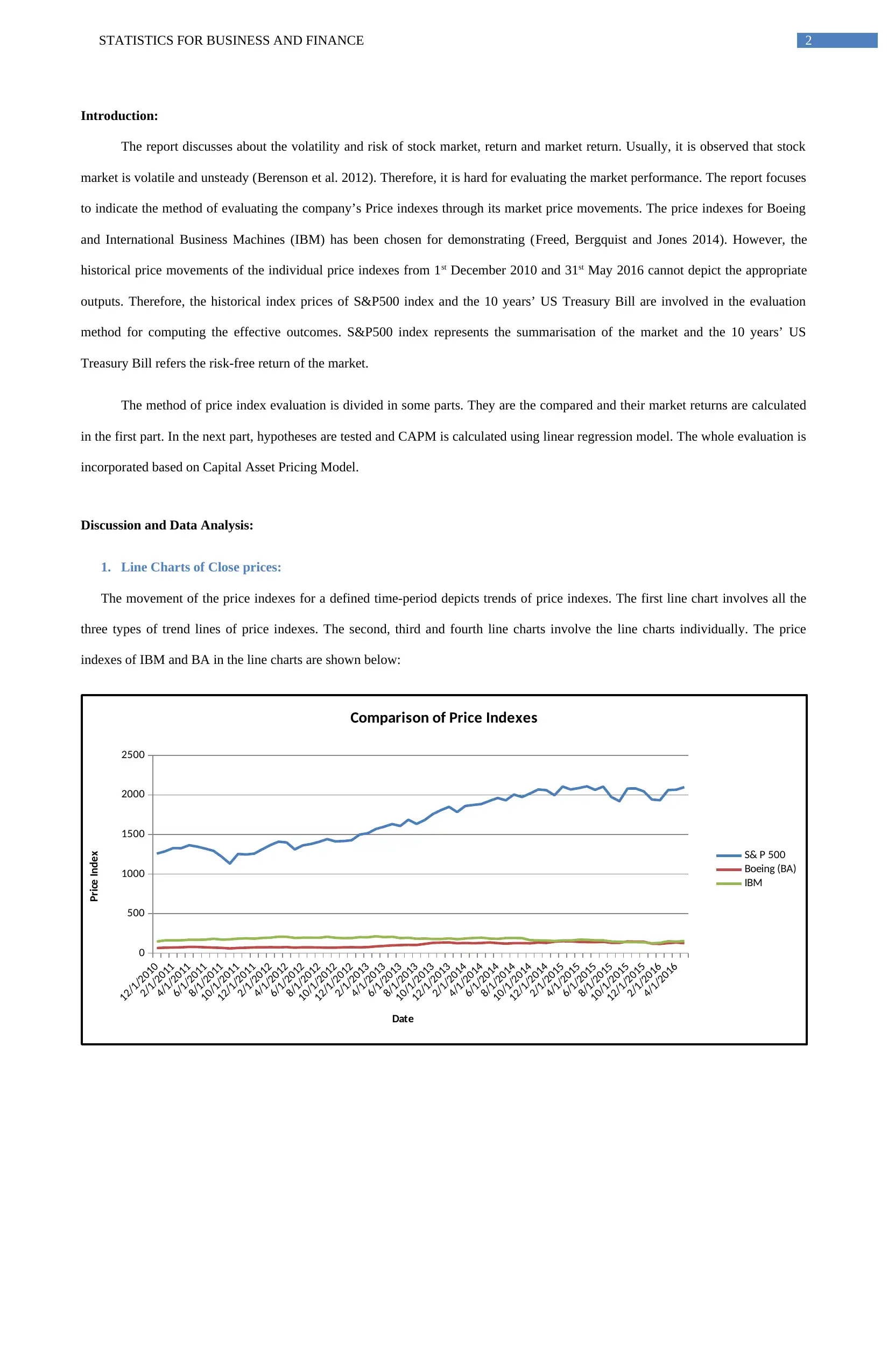

Introduction:

The report discusses about the volatility and risk of stock market, return and market return. Usually, it is observed that stock

market is volatile and unsteady (Berenson et al. 2012). Therefore, it is hard for evaluating the market performance. The report focuses

to indicate the method of evaluating the company’s Price indexes through its market price movements. The price indexes for Boeing

and International Business Machines (IBM) has been chosen for demonstrating (Freed, Bergquist and Jones 2014). However, the

historical price movements of the individual price indexes from 1st December 2010 and 31st May 2016 cannot depict the appropriate

outputs. Therefore, the historical index prices of S&P500 index and the 10 years’ US Treasury Bill are involved in the evaluation

method for computing the effective outcomes. S&P500 index represents the summarisation of the market and the 10 years’ US

Treasury Bill refers the risk-free return of the market.

The method of price index evaluation is divided in some parts. They are the compared and their market returns are calculated

in the first part. In the next part, hypotheses are tested and CAPM is calculated using linear regression model. The whole evaluation is

incorporated based on Capital Asset Pricing Model.

Discussion and Data Analysis:

1. Line Charts of Close prices:

The movement of the price indexes for a defined time-period depicts trends of price indexes. The first line chart involves all the

three types of trend lines of price indexes. The second, third and fourth line charts involve the line charts individually. The price

indexes of IBM and BA in the line charts are shown below:

12/1/2010

2/1/2011

4/1/2011

6/1/2011

8/1/2011

10/1/2011

12/1/2011

2/1/2012

4/1/2012

6/1/2012

8/1/2012

10/1/2012

12/1/2012

2/1/2013

4/1/2013

6/1/2013

8/1/2013

10/1/2013

12/1/2013

2/1/2014

4/1/2014

6/1/2014

8/1/2014

10/1/2014

12/1/2014

2/1/2015

4/1/2015

6/1/2015

8/1/2015

10/1/2015

12/1/2015

2/1/2016

4/1/2016

0

500

1000

1500

2000

2500

Comparison of Price Indexes

S& P 500

Boeing (BA)

IBM

Date

Price Index

Introduction:

The report discusses about the volatility and risk of stock market, return and market return. Usually, it is observed that stock

market is volatile and unsteady (Berenson et al. 2012). Therefore, it is hard for evaluating the market performance. The report focuses

to indicate the method of evaluating the company’s Price indexes through its market price movements. The price indexes for Boeing

and International Business Machines (IBM) has been chosen for demonstrating (Freed, Bergquist and Jones 2014). However, the

historical price movements of the individual price indexes from 1st December 2010 and 31st May 2016 cannot depict the appropriate

outputs. Therefore, the historical index prices of S&P500 index and the 10 years’ US Treasury Bill are involved in the evaluation

method for computing the effective outcomes. S&P500 index represents the summarisation of the market and the 10 years’ US

Treasury Bill refers the risk-free return of the market.

The method of price index evaluation is divided in some parts. They are the compared and their market returns are calculated

in the first part. In the next part, hypotheses are tested and CAPM is calculated using linear regression model. The whole evaluation is

incorporated based on Capital Asset Pricing Model.

Discussion and Data Analysis:

1. Line Charts of Close prices:

The movement of the price indexes for a defined time-period depicts trends of price indexes. The first line chart involves all the

three types of trend lines of price indexes. The second, third and fourth line charts involve the line charts individually. The price

indexes of IBM and BA in the line charts are shown below:

12/1/2010

2/1/2011

4/1/2011

6/1/2011

8/1/2011

10/1/2011

12/1/2011

2/1/2012

4/1/2012

6/1/2012

8/1/2012

10/1/2012

12/1/2012

2/1/2013

4/1/2013

6/1/2013

8/1/2013

10/1/2013

12/1/2013

2/1/2014

4/1/2014

6/1/2014

8/1/2014

10/1/2014

12/1/2014

2/1/2015

4/1/2015

6/1/2015

8/1/2015

10/1/2015

12/1/2015

2/1/2016

4/1/2016

0

500

1000

1500

2000

2500

Comparison of Price Indexes

S& P 500

Boeing (BA)

IBM

Date

Price Index

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3STATISTICS FOR BUSINESS AND FINANCE

12/1/2010

2/1/2011

4/1/2011

6/1/2011

8/1/2011

10/1/2011

12/1/2011

2/1/2012

4/1/2012

6/1/2012

8/1/2012

10/1/2012

12/1/2012

2/1/2013

4/1/2013

6/1/2013

8/1/2013

10/1/2013

12/1/2013

2/1/2014

4/1/2014

6/1/2014

8/1/2014

10/1/2014

12/1/2014

2/1/2015

4/1/2015

6/1/2015

8/1/2015

10/1/2015

12/1/2015

2/1/2016

4/1/2016

0

500

1000

1500

2000

2500

S&P500 Price Index

S& P 500

Date

Price Index

12/1/2010

2/1/2011

4/1/2011

6/1/2011

8/1/2011

10/1/2011

12/1/2011

2/1/2012

4/1/2012

6/1/2012

8/1/2012

10/1/2012

12/1/2012

2/1/2013

4/1/2013

6/1/2013

8/1/2013

10/1/2013

12/1/2013

2/1/2014

4/1/2014

6/1/2014

8/1/2014

10/1/2014

12/1/2014

2/1/2015

4/1/2015

6/1/2015

8/1/2015

10/1/2015

12/1/2015

2/1/2016

4/1/2016

0

20

40

60

80

100

120

140

160

Boeing (BA) Price Index

Boeing (BA)

Date

Price Index

12/1/2010

2/1/2011

4/1/2011

6/1/2011

8/1/2011

10/1/2011

12/1/2011

2/1/2012

4/1/2012

6/1/2012

8/1/2012

10/1/2012

12/1/2012

2/1/2013

4/1/2013

6/1/2013

8/1/2013

10/1/2013

12/1/2013

2/1/2014

4/1/2014

6/1/2014

8/1/2014

10/1/2014

12/1/2014

2/1/2015

4/1/2015

6/1/2015

8/1/2015

10/1/2015

12/1/2015

2/1/2016

4/1/2016

0

50

100

150

200

250

IBM Price Index

IBM

Date

Price Index

It could be inferred from the above line charts that the price indexes of both S&P500 and BA have increased from 01/12/2010

to 31/05/2016. The IBM price index has increased and then decreased within this period. It has better stationary trend in case of IBM

price index than BA price index.

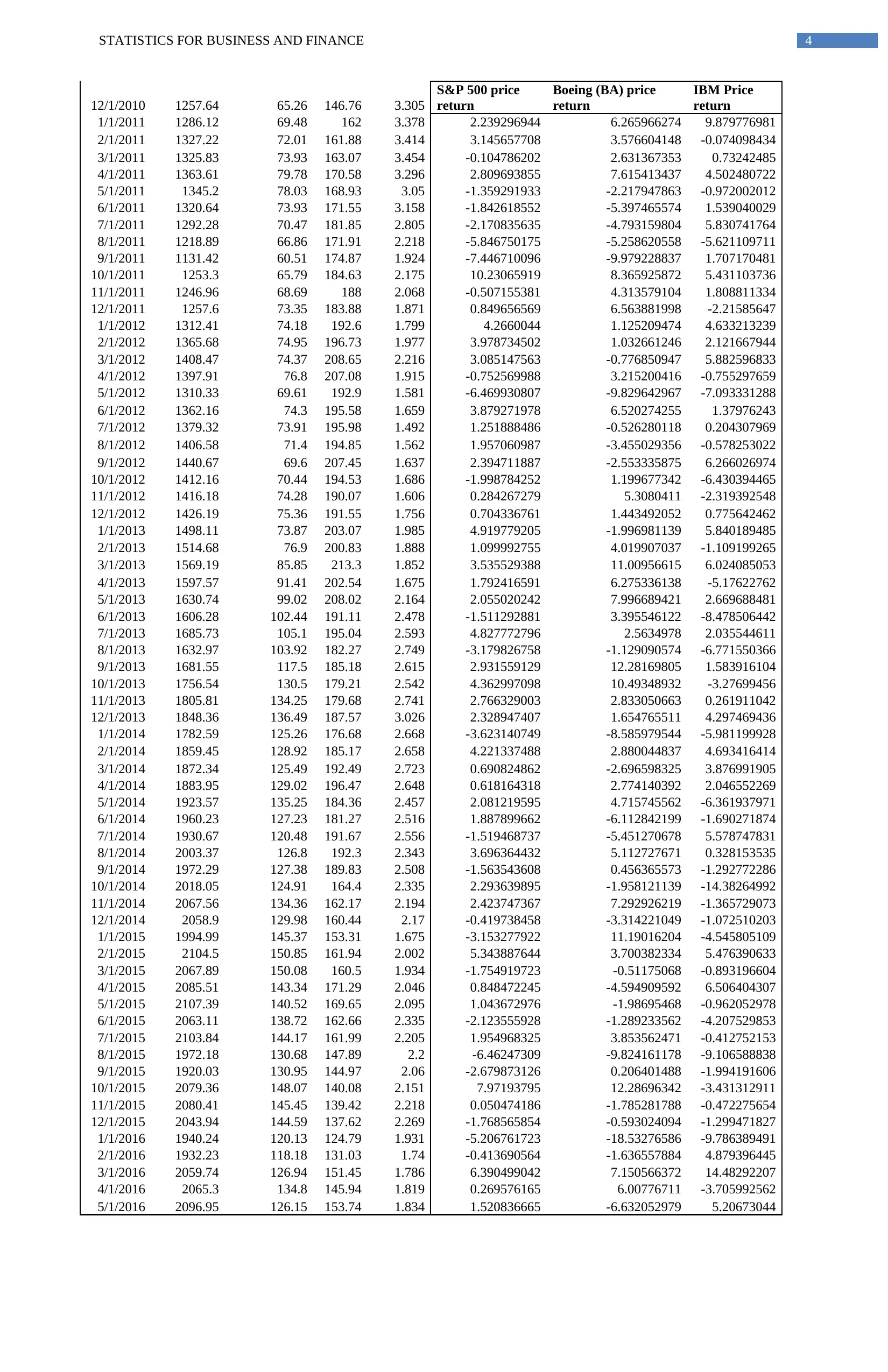

2. Calculation with return prices:

2.a. Calculation of returns:

Price Indexes Price Returns

Date

S& P 500

price

Boeing (BA)

price

IBM

price

T-Bill

price

S&P 500 price

return

Boeing (BA) price

return

IBM Price

return

12/1/2010

2/1/2011

4/1/2011

6/1/2011

8/1/2011

10/1/2011

12/1/2011

2/1/2012

4/1/2012

6/1/2012

8/1/2012

10/1/2012

12/1/2012

2/1/2013

4/1/2013

6/1/2013

8/1/2013

10/1/2013

12/1/2013

2/1/2014

4/1/2014

6/1/2014

8/1/2014

10/1/2014

12/1/2014

2/1/2015

4/1/2015

6/1/2015

8/1/2015

10/1/2015

12/1/2015

2/1/2016

4/1/2016

0

500

1000

1500

2000

2500

S&P500 Price Index

S& P 500

Date

Price Index

12/1/2010

2/1/2011

4/1/2011

6/1/2011

8/1/2011

10/1/2011

12/1/2011

2/1/2012

4/1/2012

6/1/2012

8/1/2012

10/1/2012

12/1/2012

2/1/2013

4/1/2013

6/1/2013

8/1/2013

10/1/2013

12/1/2013

2/1/2014

4/1/2014

6/1/2014

8/1/2014

10/1/2014

12/1/2014

2/1/2015

4/1/2015

6/1/2015

8/1/2015

10/1/2015

12/1/2015

2/1/2016

4/1/2016

0

20

40

60

80

100

120

140

160

Boeing (BA) Price Index

Boeing (BA)

Date

Price Index

12/1/2010

2/1/2011

4/1/2011

6/1/2011

8/1/2011

10/1/2011

12/1/2011

2/1/2012

4/1/2012

6/1/2012

8/1/2012

10/1/2012

12/1/2012

2/1/2013

4/1/2013

6/1/2013

8/1/2013

10/1/2013

12/1/2013

2/1/2014

4/1/2014

6/1/2014

8/1/2014

10/1/2014

12/1/2014

2/1/2015

4/1/2015

6/1/2015

8/1/2015

10/1/2015

12/1/2015

2/1/2016

4/1/2016

0

50

100

150

200

250

IBM Price Index

IBM

Date

Price Index

It could be inferred from the above line charts that the price indexes of both S&P500 and BA have increased from 01/12/2010

to 31/05/2016. The IBM price index has increased and then decreased within this period. It has better stationary trend in case of IBM

price index than BA price index.

2. Calculation with return prices:

2.a. Calculation of returns:

Price Indexes Price Returns

Date

S& P 500

price

Boeing (BA)

price

IBM

price

T-Bill

price

S&P 500 price

return

Boeing (BA) price

return

IBM Price

return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4STATISTICS FOR BUSINESS AND FINANCE

12/1/2010 1257.64 65.26 146.76 3.305

S&P 500 price

return

Boeing (BA) price

return

IBM Price

return

1/1/2011 1286.12 69.48 162 3.378 2.239296944 6.265966274 9.879776981

2/1/2011 1327.22 72.01 161.88 3.414 3.145657708 3.576604148 -0.074098434

3/1/2011 1325.83 73.93 163.07 3.454 -0.104786202 2.631367353 0.73242485

4/1/2011 1363.61 79.78 170.58 3.296 2.809693855 7.615413437 4.502480722

5/1/2011 1345.2 78.03 168.93 3.05 -1.359291933 -2.217947863 -0.972002012

6/1/2011 1320.64 73.93 171.55 3.158 -1.842618552 -5.397465574 1.539040029

7/1/2011 1292.28 70.47 181.85 2.805 -2.170835635 -4.793159804 5.830741764

8/1/2011 1218.89 66.86 171.91 2.218 -5.846750175 -5.258620558 -5.621109711

9/1/2011 1131.42 60.51 174.87 1.924 -7.446710096 -9.979228837 1.707170481

10/1/2011 1253.3 65.79 184.63 2.175 10.23065919 8.365925872 5.431103736

11/1/2011 1246.96 68.69 188 2.068 -0.507155381 4.313579104 1.808811334

12/1/2011 1257.6 73.35 183.88 1.871 0.849656569 6.563881998 -2.21585647

1/1/2012 1312.41 74.18 192.6 1.799 4.2660044 1.125209474 4.633213239

2/1/2012 1365.68 74.95 196.73 1.977 3.978734502 1.032661246 2.121667944

3/1/2012 1408.47 74.37 208.65 2.216 3.085147563 -0.776850947 5.882596833

4/1/2012 1397.91 76.8 207.08 1.915 -0.752569988 3.215200416 -0.755297659

5/1/2012 1310.33 69.61 192.9 1.581 -6.469930807 -9.829642967 -7.093331288

6/1/2012 1362.16 74.3 195.58 1.659 3.879271978 6.520274255 1.37976243

7/1/2012 1379.32 73.91 195.98 1.492 1.251888486 -0.526280118 0.204307969

8/1/2012 1406.58 71.4 194.85 1.562 1.957060987 -3.455029356 -0.578253022

9/1/2012 1440.67 69.6 207.45 1.637 2.394711887 -2.553335875 6.266026974

10/1/2012 1412.16 70.44 194.53 1.686 -1.998784252 1.199677342 -6.430394465

11/1/2012 1416.18 74.28 190.07 1.606 0.284267279 5.3080411 -2.319392548

12/1/2012 1426.19 75.36 191.55 1.756 0.704336761 1.443492052 0.775642462

1/1/2013 1498.11 73.87 203.07 1.985 4.919779205 -1.996981139 5.840189485

2/1/2013 1514.68 76.9 200.83 1.888 1.099992755 4.019907037 -1.109199265

3/1/2013 1569.19 85.85 213.3 1.852 3.535529388 11.00956615 6.024085053

4/1/2013 1597.57 91.41 202.54 1.675 1.792416591 6.275336138 -5.17622762

5/1/2013 1630.74 99.02 208.02 2.164 2.055020242 7.996689421 2.669688481

6/1/2013 1606.28 102.44 191.11 2.478 -1.511292881 3.395546122 -8.478506442

7/1/2013 1685.73 105.1 195.04 2.593 4.827772796 2.5634978 2.035544611

8/1/2013 1632.97 103.92 182.27 2.749 -3.179826758 -1.129090574 -6.771550366

9/1/2013 1681.55 117.5 185.18 2.615 2.931559129 12.28169805 1.583916104

10/1/2013 1756.54 130.5 179.21 2.542 4.362997098 10.49348932 -3.27699456

11/1/2013 1805.81 134.25 179.68 2.741 2.766329003 2.833050663 0.261911042

12/1/2013 1848.36 136.49 187.57 3.026 2.328947407 1.654765511 4.297469436

1/1/2014 1782.59 125.26 176.68 2.668 -3.623140749 -8.585979544 -5.981199928

2/1/2014 1859.45 128.92 185.17 2.658 4.221337488 2.880044837 4.693416414

3/1/2014 1872.34 125.49 192.49 2.723 0.690824862 -2.696598325 3.876991905

4/1/2014 1883.95 129.02 196.47 2.648 0.618164318 2.774140392 2.046552269

5/1/2014 1923.57 135.25 184.36 2.457 2.081219595 4.715745562 -6.361937971

6/1/2014 1960.23 127.23 181.27 2.516 1.887899662 -6.112842199 -1.690271874

7/1/2014 1930.67 120.48 191.67 2.556 -1.519468737 -5.451270678 5.578747831

8/1/2014 2003.37 126.8 192.3 2.343 3.696364432 5.112727671 0.328153535

9/1/2014 1972.29 127.38 189.83 2.508 -1.563543608 0.456365573 -1.292772286

10/1/2014 2018.05 124.91 164.4 2.335 2.293639895 -1.958121139 -14.38264992

11/1/2014 2067.56 134.36 162.17 2.194 2.423747367 7.292926219 -1.365729073

12/1/2014 2058.9 129.98 160.44 2.17 -0.419738458 -3.314221049 -1.072510203

1/1/2015 1994.99 145.37 153.31 1.675 -3.153277922 11.19016204 -4.545805109

2/1/2015 2104.5 150.85 161.94 2.002 5.343887644 3.700382334 5.476390633

3/1/2015 2067.89 150.08 160.5 1.934 -1.754919723 -0.51175068 -0.893196604

4/1/2015 2085.51 143.34 171.29 2.046 0.848472245 -4.594909592 6.506404307

5/1/2015 2107.39 140.52 169.65 2.095 1.043672976 -1.98695468 -0.962052978

6/1/2015 2063.11 138.72 162.66 2.335 -2.123555928 -1.289233562 -4.207529853

7/1/2015 2103.84 144.17 161.99 2.205 1.954968325 3.853562471 -0.412752153

8/1/2015 1972.18 130.68 147.89 2.2 -6.46247309 -9.824161178 -9.106588838

9/1/2015 1920.03 130.95 144.97 2.06 -2.679873126 0.206401488 -1.994191606

10/1/2015 2079.36 148.07 140.08 2.151 7.97193795 12.28696342 -3.431312911

11/1/2015 2080.41 145.45 139.42 2.218 0.050474186 -1.785281788 -0.472275654

12/1/2015 2043.94 144.59 137.62 2.269 -1.768565854 -0.593024094 -1.299471827

1/1/2016 1940.24 120.13 124.79 1.931 -5.206761723 -18.53276586 -9.786389491

2/1/2016 1932.23 118.18 131.03 1.74 -0.413690564 -1.636557884 4.879396445

3/1/2016 2059.74 126.94 151.45 1.786 6.390499042 7.150566372 14.48292207

4/1/2016 2065.3 134.8 145.94 1.819 0.269576165 6.00776711 -3.705992562

5/1/2016 2096.95 126.15 153.74 1.834 1.520836665 -6.632052979 5.20673044

12/1/2010 1257.64 65.26 146.76 3.305

S&P 500 price

return

Boeing (BA) price

return

IBM Price

return

1/1/2011 1286.12 69.48 162 3.378 2.239296944 6.265966274 9.879776981

2/1/2011 1327.22 72.01 161.88 3.414 3.145657708 3.576604148 -0.074098434

3/1/2011 1325.83 73.93 163.07 3.454 -0.104786202 2.631367353 0.73242485

4/1/2011 1363.61 79.78 170.58 3.296 2.809693855 7.615413437 4.502480722

5/1/2011 1345.2 78.03 168.93 3.05 -1.359291933 -2.217947863 -0.972002012

6/1/2011 1320.64 73.93 171.55 3.158 -1.842618552 -5.397465574 1.539040029

7/1/2011 1292.28 70.47 181.85 2.805 -2.170835635 -4.793159804 5.830741764

8/1/2011 1218.89 66.86 171.91 2.218 -5.846750175 -5.258620558 -5.621109711

9/1/2011 1131.42 60.51 174.87 1.924 -7.446710096 -9.979228837 1.707170481

10/1/2011 1253.3 65.79 184.63 2.175 10.23065919 8.365925872 5.431103736

11/1/2011 1246.96 68.69 188 2.068 -0.507155381 4.313579104 1.808811334

12/1/2011 1257.6 73.35 183.88 1.871 0.849656569 6.563881998 -2.21585647

1/1/2012 1312.41 74.18 192.6 1.799 4.2660044 1.125209474 4.633213239

2/1/2012 1365.68 74.95 196.73 1.977 3.978734502 1.032661246 2.121667944

3/1/2012 1408.47 74.37 208.65 2.216 3.085147563 -0.776850947 5.882596833

4/1/2012 1397.91 76.8 207.08 1.915 -0.752569988 3.215200416 -0.755297659

5/1/2012 1310.33 69.61 192.9 1.581 -6.469930807 -9.829642967 -7.093331288

6/1/2012 1362.16 74.3 195.58 1.659 3.879271978 6.520274255 1.37976243

7/1/2012 1379.32 73.91 195.98 1.492 1.251888486 -0.526280118 0.204307969

8/1/2012 1406.58 71.4 194.85 1.562 1.957060987 -3.455029356 -0.578253022

9/1/2012 1440.67 69.6 207.45 1.637 2.394711887 -2.553335875 6.266026974

10/1/2012 1412.16 70.44 194.53 1.686 -1.998784252 1.199677342 -6.430394465

11/1/2012 1416.18 74.28 190.07 1.606 0.284267279 5.3080411 -2.319392548

12/1/2012 1426.19 75.36 191.55 1.756 0.704336761 1.443492052 0.775642462

1/1/2013 1498.11 73.87 203.07 1.985 4.919779205 -1.996981139 5.840189485

2/1/2013 1514.68 76.9 200.83 1.888 1.099992755 4.019907037 -1.109199265

3/1/2013 1569.19 85.85 213.3 1.852 3.535529388 11.00956615 6.024085053

4/1/2013 1597.57 91.41 202.54 1.675 1.792416591 6.275336138 -5.17622762

5/1/2013 1630.74 99.02 208.02 2.164 2.055020242 7.996689421 2.669688481

6/1/2013 1606.28 102.44 191.11 2.478 -1.511292881 3.395546122 -8.478506442

7/1/2013 1685.73 105.1 195.04 2.593 4.827772796 2.5634978 2.035544611

8/1/2013 1632.97 103.92 182.27 2.749 -3.179826758 -1.129090574 -6.771550366

9/1/2013 1681.55 117.5 185.18 2.615 2.931559129 12.28169805 1.583916104

10/1/2013 1756.54 130.5 179.21 2.542 4.362997098 10.49348932 -3.27699456

11/1/2013 1805.81 134.25 179.68 2.741 2.766329003 2.833050663 0.261911042

12/1/2013 1848.36 136.49 187.57 3.026 2.328947407 1.654765511 4.297469436

1/1/2014 1782.59 125.26 176.68 2.668 -3.623140749 -8.585979544 -5.981199928

2/1/2014 1859.45 128.92 185.17 2.658 4.221337488 2.880044837 4.693416414

3/1/2014 1872.34 125.49 192.49 2.723 0.690824862 -2.696598325 3.876991905

4/1/2014 1883.95 129.02 196.47 2.648 0.618164318 2.774140392 2.046552269

5/1/2014 1923.57 135.25 184.36 2.457 2.081219595 4.715745562 -6.361937971

6/1/2014 1960.23 127.23 181.27 2.516 1.887899662 -6.112842199 -1.690271874

7/1/2014 1930.67 120.48 191.67 2.556 -1.519468737 -5.451270678 5.578747831

8/1/2014 2003.37 126.8 192.3 2.343 3.696364432 5.112727671 0.328153535

9/1/2014 1972.29 127.38 189.83 2.508 -1.563543608 0.456365573 -1.292772286

10/1/2014 2018.05 124.91 164.4 2.335 2.293639895 -1.958121139 -14.38264992

11/1/2014 2067.56 134.36 162.17 2.194 2.423747367 7.292926219 -1.365729073

12/1/2014 2058.9 129.98 160.44 2.17 -0.419738458 -3.314221049 -1.072510203

1/1/2015 1994.99 145.37 153.31 1.675 -3.153277922 11.19016204 -4.545805109

2/1/2015 2104.5 150.85 161.94 2.002 5.343887644 3.700382334 5.476390633

3/1/2015 2067.89 150.08 160.5 1.934 -1.754919723 -0.51175068 -0.893196604

4/1/2015 2085.51 143.34 171.29 2.046 0.848472245 -4.594909592 6.506404307

5/1/2015 2107.39 140.52 169.65 2.095 1.043672976 -1.98695468 -0.962052978

6/1/2015 2063.11 138.72 162.66 2.335 -2.123555928 -1.289233562 -4.207529853

7/1/2015 2103.84 144.17 161.99 2.205 1.954968325 3.853562471 -0.412752153

8/1/2015 1972.18 130.68 147.89 2.2 -6.46247309 -9.824161178 -9.106588838

9/1/2015 1920.03 130.95 144.97 2.06 -2.679873126 0.206401488 -1.994191606

10/1/2015 2079.36 148.07 140.08 2.151 7.97193795 12.28696342 -3.431312911

11/1/2015 2080.41 145.45 139.42 2.218 0.050474186 -1.785281788 -0.472275654

12/1/2015 2043.94 144.59 137.62 2.269 -1.768565854 -0.593024094 -1.299471827

1/1/2016 1940.24 120.13 124.79 1.931 -5.206761723 -18.53276586 -9.786389491

2/1/2016 1932.23 118.18 131.03 1.74 -0.413690564 -1.636557884 4.879396445

3/1/2016 2059.74 126.94 151.45 1.786 6.390499042 7.150566372 14.48292207

4/1/2016 2065.3 134.8 145.94 1.819 0.269576165 6.00776711 -3.705992562

5/1/2016 2096.95 126.15 153.74 1.834 1.520836665 -6.632052979 5.20673044

5STATISTICS FOR BUSINESS AND FINANCE

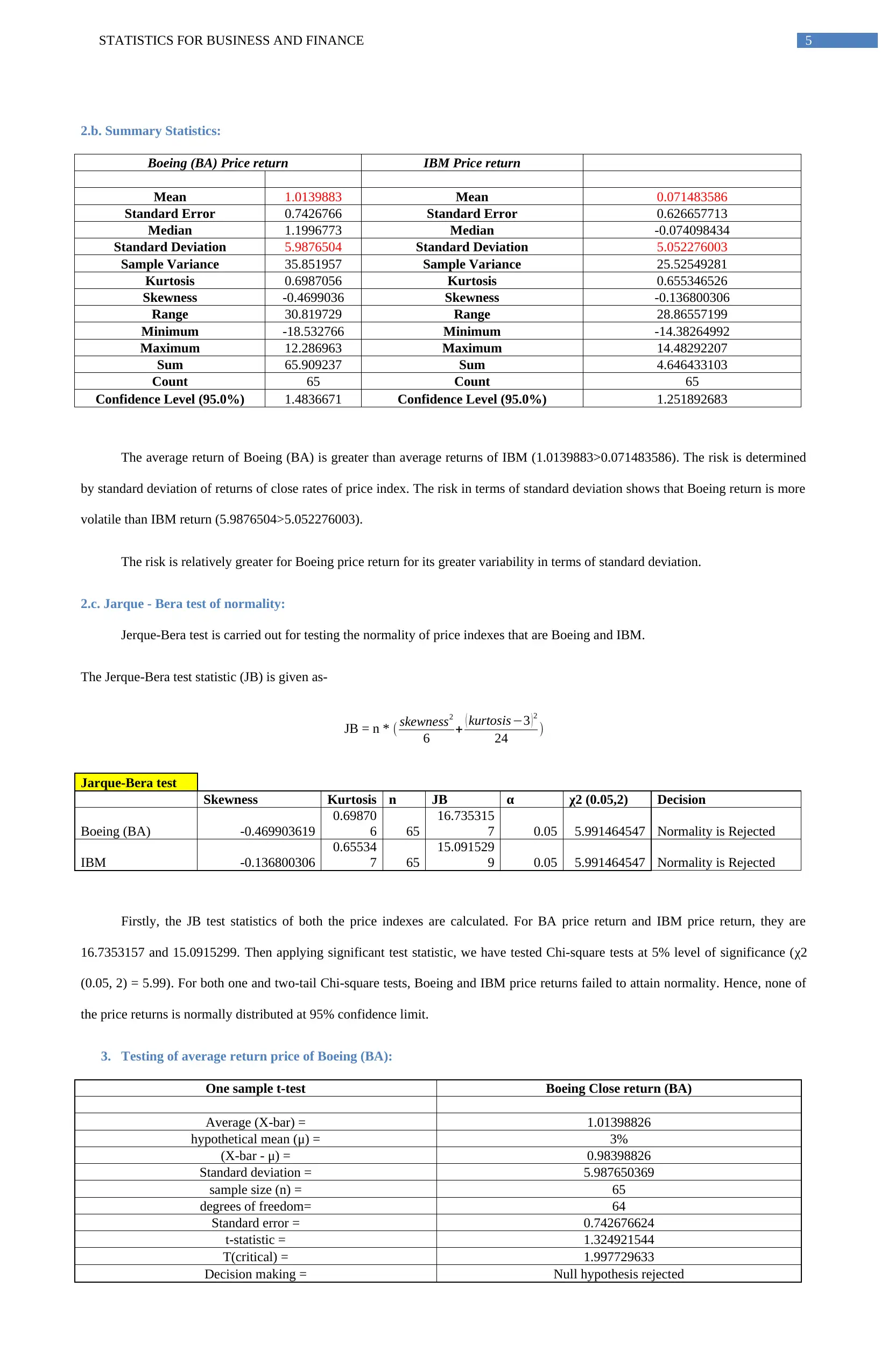

2.b. Summary Statistics:

Boeing (BA) Price return IBM Price return

Mean 1.0139883 Mean 0.071483586

Standard Error 0.7426766 Standard Error 0.626657713

Median 1.1996773 Median -0.074098434

Standard Deviation 5.9876504 Standard Deviation 5.052276003

Sample Variance 35.851957 Sample Variance 25.52549281

Kurtosis 0.6987056 Kurtosis 0.655346526

Skewness -0.4699036 Skewness -0.136800306

Range 30.819729 Range 28.86557199

Minimum -18.532766 Minimum -14.38264992

Maximum 12.286963 Maximum 14.48292207

Sum 65.909237 Sum 4.646433103

Count 65 Count 65

Confidence Level (95.0%) 1.4836671 Confidence Level (95.0%) 1.251892683

The average return of Boeing (BA) is greater than average returns of IBM (1.0139883>0.071483586). The risk is determined

by standard deviation of returns of close rates of price index. The risk in terms of standard deviation shows that Boeing return is more

volatile than IBM return (5.9876504>5.052276003).

The risk is relatively greater for Boeing price return for its greater variability in terms of standard deviation.

2.c. Jarque - Bera test of normality:

Jerque-Bera test is carried out for testing the normality of price indexes that are Boeing and IBM.

The Jerque-Bera test statistic (JB) is given as-

JB = n * ( skewness2

6 + ( kurtosis−3 ) 2

24 )

Jarque-Bera test

Skewness Kurtosis n JB α χ2 (0.05,2) Decision

Boeing (BA) -0.469903619

0.69870

6 65

16.735315

7 0.05 5.991464547 Normality is Rejected

IBM -0.136800306

0.65534

7 65

15.091529

9 0.05 5.991464547 Normality is Rejected

Firstly, the JB test statistics of both the price indexes are calculated. For BA price return and IBM price return, they are

16.7353157 and 15.0915299. Then applying significant test statistic, we have tested Chi-square tests at 5% level of significance (χ2

(0.05, 2) = 5.99). For both one and two-tail Chi-square tests, Boeing and IBM price returns failed to attain normality. Hence, none of

the price returns is normally distributed at 95% confidence limit.

3. Testing of average return price of Boeing (BA):

One sample t-test Boeing Close return (BA)

Average (X-bar) = 1.01398826

hypothetical mean (μ) = 3%

(X-bar - μ) = 0.98398826

Standard deviation = 5.987650369

sample size (n) = 65

degrees of freedom= 64

Standard error = 0.742676624

t-statistic = 1.324921544

T(critical) = 1.997729633

Decision making = Null hypothesis rejected

2.b. Summary Statistics:

Boeing (BA) Price return IBM Price return

Mean 1.0139883 Mean 0.071483586

Standard Error 0.7426766 Standard Error 0.626657713

Median 1.1996773 Median -0.074098434

Standard Deviation 5.9876504 Standard Deviation 5.052276003

Sample Variance 35.851957 Sample Variance 25.52549281

Kurtosis 0.6987056 Kurtosis 0.655346526

Skewness -0.4699036 Skewness -0.136800306

Range 30.819729 Range 28.86557199

Minimum -18.532766 Minimum -14.38264992

Maximum 12.286963 Maximum 14.48292207

Sum 65.909237 Sum 4.646433103

Count 65 Count 65

Confidence Level (95.0%) 1.4836671 Confidence Level (95.0%) 1.251892683

The average return of Boeing (BA) is greater than average returns of IBM (1.0139883>0.071483586). The risk is determined

by standard deviation of returns of close rates of price index. The risk in terms of standard deviation shows that Boeing return is more

volatile than IBM return (5.9876504>5.052276003).

The risk is relatively greater for Boeing price return for its greater variability in terms of standard deviation.

2.c. Jarque - Bera test of normality:

Jerque-Bera test is carried out for testing the normality of price indexes that are Boeing and IBM.

The Jerque-Bera test statistic (JB) is given as-

JB = n * ( skewness2

6 + ( kurtosis−3 ) 2

24 )

Jarque-Bera test

Skewness Kurtosis n JB α χ2 (0.05,2) Decision

Boeing (BA) -0.469903619

0.69870

6 65

16.735315

7 0.05 5.991464547 Normality is Rejected

IBM -0.136800306

0.65534

7 65

15.091529

9 0.05 5.991464547 Normality is Rejected

Firstly, the JB test statistics of both the price indexes are calculated. For BA price return and IBM price return, they are

16.7353157 and 15.0915299. Then applying significant test statistic, we have tested Chi-square tests at 5% level of significance (χ2

(0.05, 2) = 5.99). For both one and two-tail Chi-square tests, Boeing and IBM price returns failed to attain normality. Hence, none of

the price returns is normally distributed at 95% confidence limit.

3. Testing of average return price of Boeing (BA):

One sample t-test Boeing Close return (BA)

Average (X-bar) = 1.01398826

hypothetical mean (μ) = 3%

(X-bar - μ) = 0.98398826

Standard deviation = 5.987650369

sample size (n) = 65

degrees of freedom= 64

Standard error = 0.742676624

t-statistic = 1.324921544

T(critical) = 1.997729633

Decision making = Null hypothesis rejected

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6STATISTICS FOR BUSINESS AND FINANCE

A one-sample t-test determines whether the average price return of Boeing Close return (BA) is at least 3%. The t-statistic is -

t=( Xbar−μ)

( s

√n ) . The t-statistic is 1.324921544. At 5% level of significance, we reject the null hypothesis of average price return greater

than or equal to 0.03 as T0.05 < Tcric.

Therefore, the average price return of Boeing is not at least 3%.

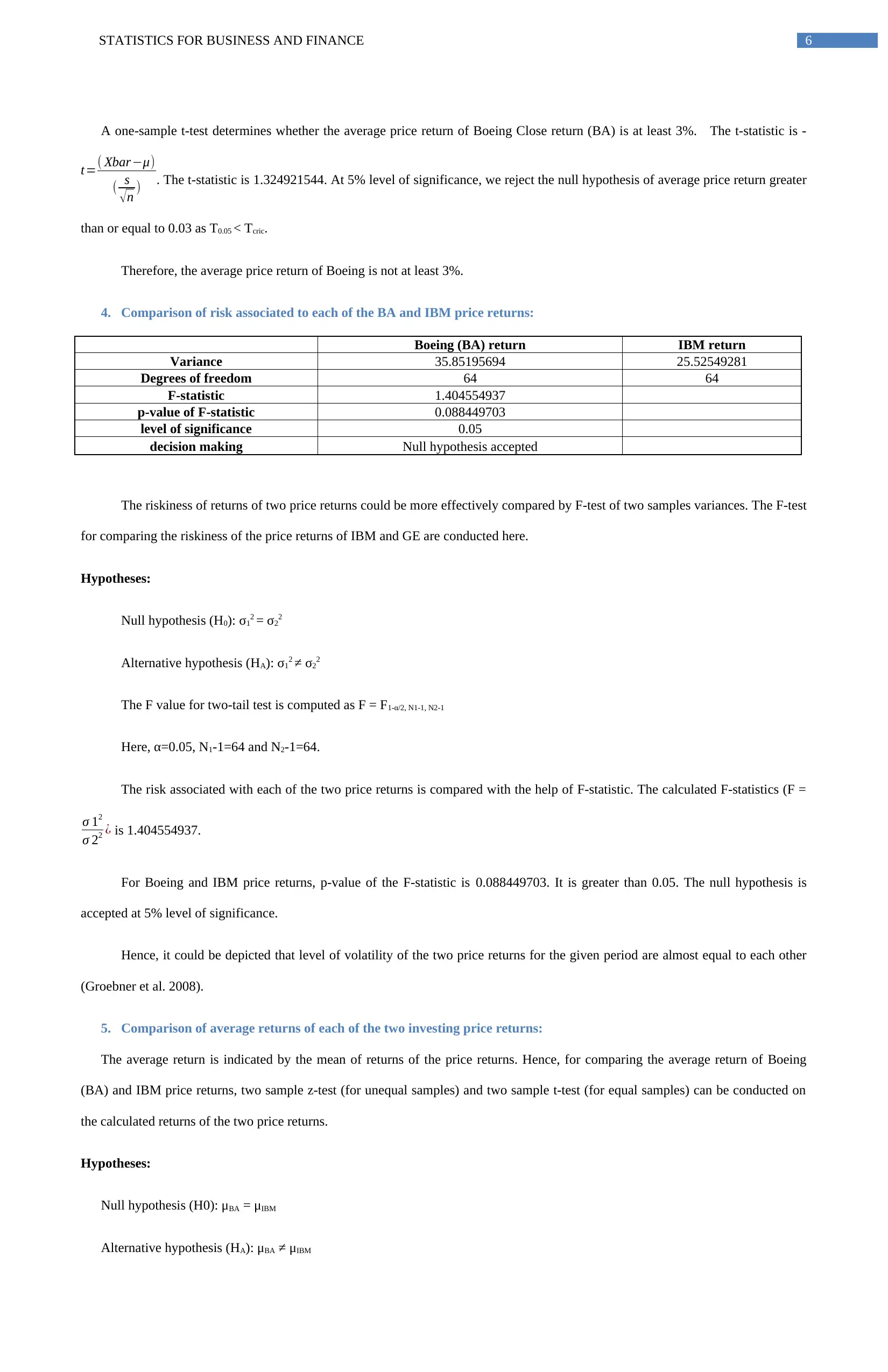

4. Comparison of risk associated to each of the BA and IBM price returns:

Boeing (BA) return IBM return

Variance 35.85195694 25.52549281

Degrees of freedom 64 64

F-statistic 1.404554937

p-value of F-statistic 0.088449703

level of significance 0.05

decision making Null hypothesis accepted

The riskiness of returns of two price returns could be more effectively compared by F-test of two samples variances. The F-test

for comparing the riskiness of the price returns of IBM and GE are conducted here.

Hypotheses:

Null hypothesis (H0): σ12 = σ22

Alternative hypothesis (HA): σ12 ≠ σ22

The F value for two-tail test is computed as F = F1-α/2, N1-1, N2-1

Here, α=0.05, N1-1=64 and N2-1=64.

The risk associated with each of the two price returns is compared with the help of F-statistic. The calculated F-statistics (F =

σ 12

σ 22 ¿ is 1.404554937.

For Boeing and IBM price returns, p-value of the F-statistic is 0.088449703. It is greater than 0.05. The null hypothesis is

accepted at 5% level of significance.

Hence, it could be depicted that level of volatility of the two price returns for the given period are almost equal to each other

(Groebner et al. 2008).

5. Comparison of average returns of each of the two investing price returns:

The average return is indicated by the mean of returns of the price returns. Hence, for comparing the average return of Boeing

(BA) and IBM price returns, two sample z-test (for unequal samples) and two sample t-test (for equal samples) can be conducted on

the calculated returns of the two price returns.

Hypotheses:

Null hypothesis (H0): μBA = μIBM

Alternative hypothesis (HA): μBA ≠ μIBM

A one-sample t-test determines whether the average price return of Boeing Close return (BA) is at least 3%. The t-statistic is -

t=( Xbar−μ)

( s

√n ) . The t-statistic is 1.324921544. At 5% level of significance, we reject the null hypothesis of average price return greater

than or equal to 0.03 as T0.05 < Tcric.

Therefore, the average price return of Boeing is not at least 3%.

4. Comparison of risk associated to each of the BA and IBM price returns:

Boeing (BA) return IBM return

Variance 35.85195694 25.52549281

Degrees of freedom 64 64

F-statistic 1.404554937

p-value of F-statistic 0.088449703

level of significance 0.05

decision making Null hypothesis accepted

The riskiness of returns of two price returns could be more effectively compared by F-test of two samples variances. The F-test

for comparing the riskiness of the price returns of IBM and GE are conducted here.

Hypotheses:

Null hypothesis (H0): σ12 = σ22

Alternative hypothesis (HA): σ12 ≠ σ22

The F value for two-tail test is computed as F = F1-α/2, N1-1, N2-1

Here, α=0.05, N1-1=64 and N2-1=64.

The risk associated with each of the two price returns is compared with the help of F-statistic. The calculated F-statistics (F =

σ 12

σ 22 ¿ is 1.404554937.

For Boeing and IBM price returns, p-value of the F-statistic is 0.088449703. It is greater than 0.05. The null hypothesis is

accepted at 5% level of significance.

Hence, it could be depicted that level of volatility of the two price returns for the given period are almost equal to each other

(Groebner et al. 2008).

5. Comparison of average returns of each of the two investing price returns:

The average return is indicated by the mean of returns of the price returns. Hence, for comparing the average return of Boeing

(BA) and IBM price returns, two sample z-test (for unequal samples) and two sample t-test (for equal samples) can be conducted on

the calculated returns of the two price returns.

Hypotheses:

Null hypothesis (H0): μBA = μIBM

Alternative hypothesis (HA): μBA ≠ μIBM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7STATISTICS FOR BUSINESS AND FINANCE

The z-statistic is given as z¿ ( Xbar −μ)

( σ

√n ) and t-statistic is given as t=( Xbar−μ)

( s

√ n ) .

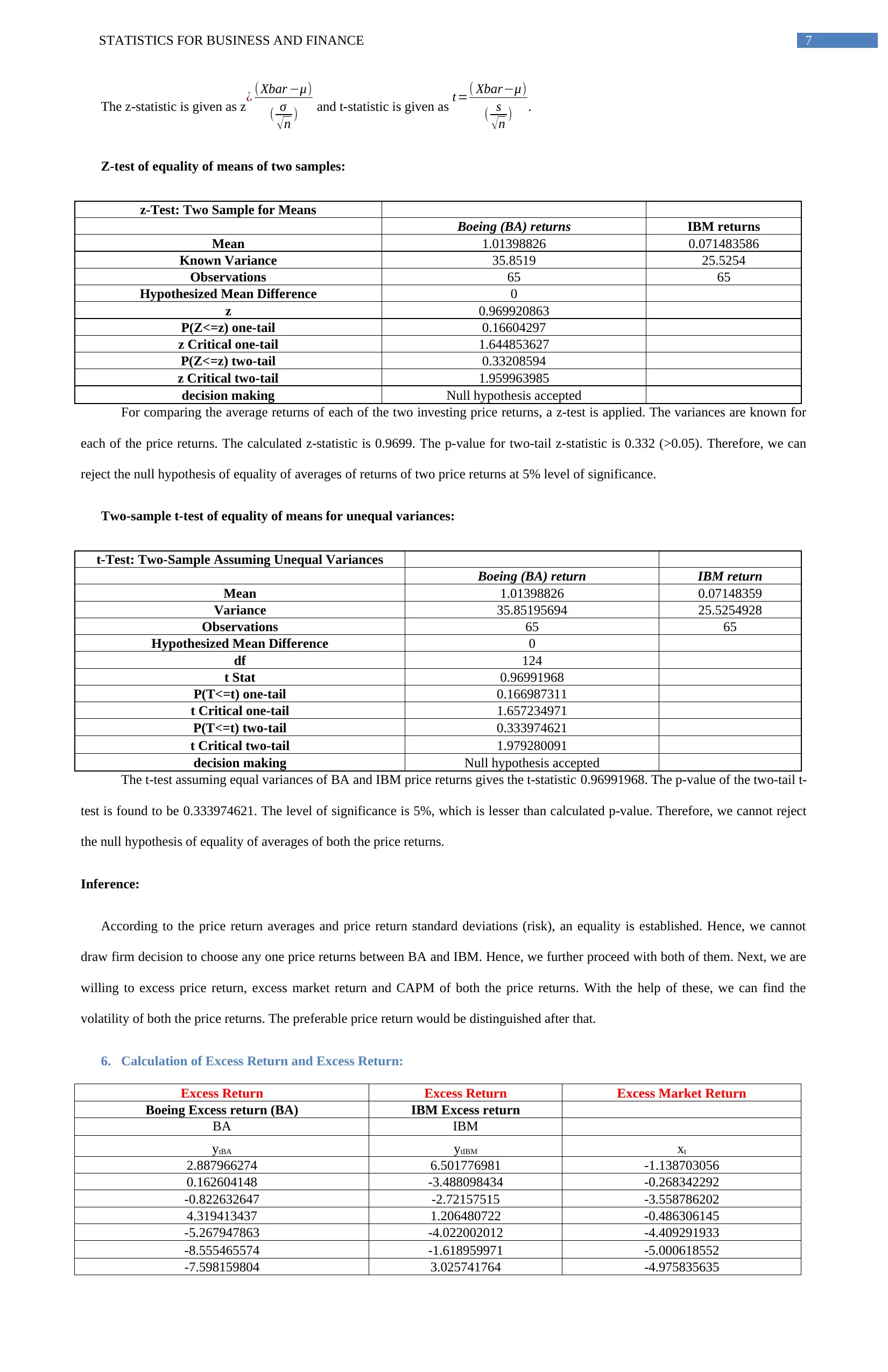

Z-test of equality of means of two samples:

z-Test: Two Sample for Means

Boeing (BA) returns IBM returns

Mean 1.01398826 0.071483586

Known Variance 35.8519 25.5254

Observations 65 65

Hypothesized Mean Difference 0

z 0.969920863

P(Z<=z) one-tail 0.16604297

z Critical one-tail 1.644853627

P(Z<=z) two-tail 0.33208594

z Critical two-tail 1.959963985

decision making Null hypothesis accepted

For comparing the average returns of each of the two investing price returns, a z-test is applied. The variances are known for

each of the price returns. The calculated z-statistic is 0.9699. The p-value for two-tail z-statistic is 0.332 (>0.05). Therefore, we can

reject the null hypothesis of equality of averages of returns of two price returns at 5% level of significance.

Two-sample t-test of equality of means for unequal variances:

t-Test: Two-Sample Assuming Unequal Variances

Boeing (BA) return IBM return

Mean 1.01398826 0.07148359

Variance 35.85195694 25.5254928

Observations 65 65

Hypothesized Mean Difference 0

df 124

t Stat 0.96991968

P(T<=t) one-tail 0.166987311

t Critical one-tail 1.657234971

P(T<=t) two-tail 0.333974621

t Critical two-tail 1.979280091

decision making Null hypothesis accepted

The t-test assuming equal variances of BA and IBM price returns gives the t-statistic 0.96991968. The p-value of the two-tail t-

test is found to be 0.333974621. The level of significance is 5%, which is lesser than calculated p-value. Therefore, we cannot reject

the null hypothesis of equality of averages of both the price returns.

Inference:

According to the price return averages and price return standard deviations (risk), an equality is established. Hence, we cannot

draw firm decision to choose any one price returns between BA and IBM. Hence, we further proceed with both of them. Next, we are

willing to excess price return, excess market return and CAPM of both the price returns. With the help of these, we can find the

volatility of both the price returns. The preferable price return would be distinguished after that.

6. Calculation of Excess Return and Excess Return:

Excess Return Excess Return Excess Market Return

Boeing Excess return (BA) IBM Excess return

BA IBM

ytBA ytIBM xt

2.887966274 6.501776981 -1.138703056

0.162604148 -3.488098434 -0.268342292

-0.822632647 -2.72157515 -3.558786202

4.319413437 1.206480722 -0.486306145

-5.267947863 -4.022002012 -4.409291933

-8.555465574 -1.618959971 -5.000618552

-7.598159804 3.025741764 -4.975835635

The z-statistic is given as z¿ ( Xbar −μ)

( σ

√n ) and t-statistic is given as t=( Xbar−μ)

( s

√ n ) .

Z-test of equality of means of two samples:

z-Test: Two Sample for Means

Boeing (BA) returns IBM returns

Mean 1.01398826 0.071483586

Known Variance 35.8519 25.5254

Observations 65 65

Hypothesized Mean Difference 0

z 0.969920863

P(Z<=z) one-tail 0.16604297

z Critical one-tail 1.644853627

P(Z<=z) two-tail 0.33208594

z Critical two-tail 1.959963985

decision making Null hypothesis accepted

For comparing the average returns of each of the two investing price returns, a z-test is applied. The variances are known for

each of the price returns. The calculated z-statistic is 0.9699. The p-value for two-tail z-statistic is 0.332 (>0.05). Therefore, we can

reject the null hypothesis of equality of averages of returns of two price returns at 5% level of significance.

Two-sample t-test of equality of means for unequal variances:

t-Test: Two-Sample Assuming Unequal Variances

Boeing (BA) return IBM return

Mean 1.01398826 0.07148359

Variance 35.85195694 25.5254928

Observations 65 65

Hypothesized Mean Difference 0

df 124

t Stat 0.96991968

P(T<=t) one-tail 0.166987311

t Critical one-tail 1.657234971

P(T<=t) two-tail 0.333974621

t Critical two-tail 1.979280091

decision making Null hypothesis accepted

The t-test assuming equal variances of BA and IBM price returns gives the t-statistic 0.96991968. The p-value of the two-tail t-

test is found to be 0.333974621. The level of significance is 5%, which is lesser than calculated p-value. Therefore, we cannot reject

the null hypothesis of equality of averages of both the price returns.

Inference:

According to the price return averages and price return standard deviations (risk), an equality is established. Hence, we cannot

draw firm decision to choose any one price returns between BA and IBM. Hence, we further proceed with both of them. Next, we are

willing to excess price return, excess market return and CAPM of both the price returns. With the help of these, we can find the

volatility of both the price returns. The preferable price return would be distinguished after that.

6. Calculation of Excess Return and Excess Return:

Excess Return Excess Return Excess Market Return

Boeing Excess return (BA) IBM Excess return

BA IBM

ytBA ytIBM xt

2.887966274 6.501776981 -1.138703056

0.162604148 -3.488098434 -0.268342292

-0.822632647 -2.72157515 -3.558786202

4.319413437 1.206480722 -0.486306145

-5.267947863 -4.022002012 -4.409291933

-8.555465574 -1.618959971 -5.000618552

-7.598159804 3.025741764 -4.975835635

8STATISTICS FOR BUSINESS AND FINANCE

-7.476620558 -7.839109711 -8.064750175

-11.90322884 -0.216829519 -9.370710096

6.190925872 3.256103736 8.055659186

2.245579104 -0.259188666 -2.575155381

4.692881998 -4.08685647 -1.021343431

-0.673790526 2.834213239 2.4670044

-0.944338754 0.144667944 2.001734502

-2.992850947 3.666596833 0.869147563

1.300200416 -2.670297659 -2.667569988

-11.41064297 -8.674331288 -8.050930807

4.861274255 -0.27923757 2.220271978

-2.018280118 -1.287692031 -0.240111514

-5.017029356 -2.140253022 0.395060987

-4.190335875 4.629026974 0.757711887

-0.486322658 -8.116394465 -3.684784252

3.7020411 -3.925392548 -1.321732721

-0.312507948 -0.980357538 -1.051663239

-3.981981139 3.855189485 2.934779205

2.131907037 -2.997199265 -0.788007245

9.157566153 4.172085053 1.683529388

4.600336138 -6.85122762 0.117416591

5.832689421 0.505688481 -0.108979758

0.917546122 -10.95650644 -3.989292881

-0.0295022 -0.557455389 2.234772796

-3.878090574 -9.520550366 -5.928826758

9.666698047 -1.031083896 0.316559129

7.951489318 -5.81899456 1.820997098

0.092050663 -2.479088958 0.025329003

-1.371234489 1.271469436 -0.697052593

-11.25397954 -8.649199928 -6.291140749

0.222044837 2.035416414 1.563337488

-5.419598325 1.153991905 -2.032175138

0.126140392 -0.601447731 -2.029835682

2.258745562 -8.818937971 -0.375780405

-8.628842199 -4.206271874 -0.628100338

-8.007270678 3.022747831 -4.075468737

2.769727671 -2.014846465 1.353364432

-2.051634427 -3.800772286 -4.071543608

-4.293121139 -16.71764992 -0.041360105

5.098926219 -3.559729073 0.229747367

-5.484221049 -3.242510203 -2.589738458

9.515162035 -6.220805109 -4.828277922

1.698382334 3.474390633 3.341887644

-2.44575068 -2.827196604 -3.688919723

-6.640909592 4.460404307 -1.197527755

-4.08195468 -3.057052978 -1.051327024

-3.624233562 -6.542529853 -4.458555928

1.648562471 -2.617752153 -0.250031675

-12.02416118 -11.30658884 -8.66247309

-1.853598512 -4.054191606 -4.739873126

10.13596342 -5.582312911 5.82093795

-4.003281788 -2.690275654 -2.167525814

-2.862024094 -3.568471827 -4.037565854

-20.46376586 -11.71738949 -7.137761723

-3.376557884 3.139396445 -2.153690564

5.364566372 12.69692207 4.604499042

4.18876711 -5.524992562 -1.549423835

-8.466052979 3.37273044 -0.313163335

7. CAPM calculation by linear regression method:

The Capital Asset Pricing Model (CAPM) is known as CAPM, which is one of the fundamental models in the financial field. The

CAPM elaborates variability in the rate of return (rt) as a function of the rate of return on a market portfolio (rM,t) consisting all

publicly traded price returns. Usually, the rate of return of any price return can be measured using opportunity cost that is the return on

a risk free asset (rf,t). The difference between the return and risk free rate is known as “risk premium” as it is the reward or punishment

-7.476620558 -7.839109711 -8.064750175

-11.90322884 -0.216829519 -9.370710096

6.190925872 3.256103736 8.055659186

2.245579104 -0.259188666 -2.575155381

4.692881998 -4.08685647 -1.021343431

-0.673790526 2.834213239 2.4670044

-0.944338754 0.144667944 2.001734502

-2.992850947 3.666596833 0.869147563

1.300200416 -2.670297659 -2.667569988

-11.41064297 -8.674331288 -8.050930807

4.861274255 -0.27923757 2.220271978

-2.018280118 -1.287692031 -0.240111514

-5.017029356 -2.140253022 0.395060987

-4.190335875 4.629026974 0.757711887

-0.486322658 -8.116394465 -3.684784252

3.7020411 -3.925392548 -1.321732721

-0.312507948 -0.980357538 -1.051663239

-3.981981139 3.855189485 2.934779205

2.131907037 -2.997199265 -0.788007245

9.157566153 4.172085053 1.683529388

4.600336138 -6.85122762 0.117416591

5.832689421 0.505688481 -0.108979758

0.917546122 -10.95650644 -3.989292881

-0.0295022 -0.557455389 2.234772796

-3.878090574 -9.520550366 -5.928826758

9.666698047 -1.031083896 0.316559129

7.951489318 -5.81899456 1.820997098

0.092050663 -2.479088958 0.025329003

-1.371234489 1.271469436 -0.697052593

-11.25397954 -8.649199928 -6.291140749

0.222044837 2.035416414 1.563337488

-5.419598325 1.153991905 -2.032175138

0.126140392 -0.601447731 -2.029835682

2.258745562 -8.818937971 -0.375780405

-8.628842199 -4.206271874 -0.628100338

-8.007270678 3.022747831 -4.075468737

2.769727671 -2.014846465 1.353364432

-2.051634427 -3.800772286 -4.071543608

-4.293121139 -16.71764992 -0.041360105

5.098926219 -3.559729073 0.229747367

-5.484221049 -3.242510203 -2.589738458

9.515162035 -6.220805109 -4.828277922

1.698382334 3.474390633 3.341887644

-2.44575068 -2.827196604 -3.688919723

-6.640909592 4.460404307 -1.197527755

-4.08195468 -3.057052978 -1.051327024

-3.624233562 -6.542529853 -4.458555928

1.648562471 -2.617752153 -0.250031675

-12.02416118 -11.30658884 -8.66247309

-1.853598512 -4.054191606 -4.739873126

10.13596342 -5.582312911 5.82093795

-4.003281788 -2.690275654 -2.167525814

-2.862024094 -3.568471827 -4.037565854

-20.46376586 -11.71738949 -7.137761723

-3.376557884 3.139396445 -2.153690564

5.364566372 12.69692207 4.604499042

4.18876711 -5.524992562 -1.549423835

-8.466052979 3.37273044 -0.313163335

7. CAPM calculation by linear regression method:

The Capital Asset Pricing Model (CAPM) is known as CAPM, which is one of the fundamental models in the financial field. The

CAPM elaborates variability in the rate of return (rt) as a function of the rate of return on a market portfolio (rM,t) consisting all

publicly traded price returns. Usually, the rate of return of any price return can be measured using opportunity cost that is the return on

a risk free asset (rf,t). The difference between the return and risk free rate is known as “risk premium” as it is the reward or punishment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9STATISTICS FOR BUSINESS AND FINANCE

for performing a risky investment (Peirson et al. 2014). In accordance to CAPM, the risk premium on a security (rt –rf,t) is proportional

to the risk premium on the market portfolio (rM,t – rf,t). According to CAPM,

(rt –rf,t) = βM*(rM,t – rf,t) ……………….(1)

Equation (1) is called economic model as it describes association between excess price returns and excess market return.

The CAPM beta is crucial from the viewpoints of investors as it discloses the volatility of market price returns. Particularly, the

bête (slope) measures the sensitivity of variation of given return of security in the whole price market. Value of beta defines whether

the price return is a defensive, a neutral price index or an aggressive price index. Including an intercept (β 0) and an error term (ut) in

the model, we have a simple linear regression model –

(rt - rf,t) = β0 + βM (rM,t - rf,t) +ut ………………..(2)

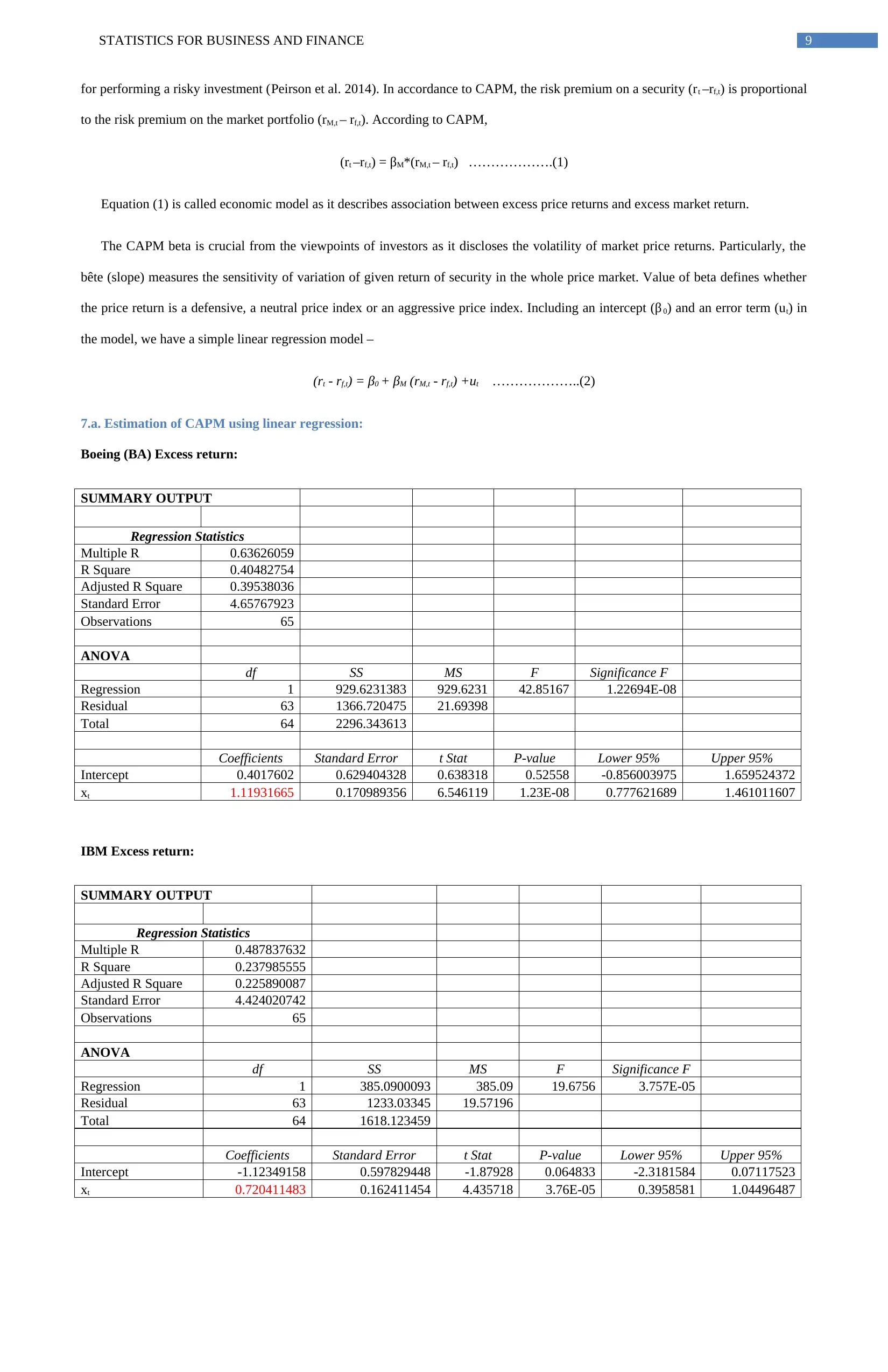

7.a. Estimation of CAPM using linear regression:

Boeing (BA) Excess return:

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.63626059

R Square 0.40482754

Adjusted R Square 0.39538036

Standard Error 4.65767923

Observations 65

ANOVA

df SS MS F Significance F

Regression 1 929.6231383 929.6231 42.85167 1.22694E-08

Residual 63 1366.720475 21.69398

Total 64 2296.343613

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.4017602 0.629404328 0.638318 0.52558 -0.856003975 1.659524372

xt 1.11931665 0.170989356 6.546119 1.23E-08 0.777621689 1.461011607

IBM Excess return:

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.487837632

R Square 0.237985555

Adjusted R Square 0.225890087

Standard Error 4.424020742

Observations 65

ANOVA

df SS MS F Significance F

Regression 1 385.0900093 385.09 19.6756 3.757E-05

Residual 63 1233.03345 19.57196

Total 64 1618.123459

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -1.12349158 0.597829448 -1.87928 0.064833 -2.3181584 0.07117523

xt 0.720411483 0.162411454 4.435718 3.76E-05 0.3958581 1.04496487

for performing a risky investment (Peirson et al. 2014). In accordance to CAPM, the risk premium on a security (rt –rf,t) is proportional

to the risk premium on the market portfolio (rM,t – rf,t). According to CAPM,

(rt –rf,t) = βM*(rM,t – rf,t) ……………….(1)

Equation (1) is called economic model as it describes association between excess price returns and excess market return.

The CAPM beta is crucial from the viewpoints of investors as it discloses the volatility of market price returns. Particularly, the

bête (slope) measures the sensitivity of variation of given return of security in the whole price market. Value of beta defines whether

the price return is a defensive, a neutral price index or an aggressive price index. Including an intercept (β 0) and an error term (ut) in

the model, we have a simple linear regression model –

(rt - rf,t) = β0 + βM (rM,t - rf,t) +ut ………………..(2)

7.a. Estimation of CAPM using linear regression:

Boeing (BA) Excess return:

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.63626059

R Square 0.40482754

Adjusted R Square 0.39538036

Standard Error 4.65767923

Observations 65

ANOVA

df SS MS F Significance F

Regression 1 929.6231383 929.6231 42.85167 1.22694E-08

Residual 63 1366.720475 21.69398

Total 64 2296.343613

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.4017602 0.629404328 0.638318 0.52558 -0.856003975 1.659524372

xt 1.11931665 0.170989356 6.546119 1.23E-08 0.777621689 1.461011607

IBM Excess return:

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.487837632

R Square 0.237985555

Adjusted R Square 0.225890087

Standard Error 4.424020742

Observations 65

ANOVA

df SS MS F Significance F

Regression 1 385.0900093 385.09 19.6756 3.757E-05

Residual 63 1233.03345 19.57196

Total 64 1618.123459

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -1.12349158 0.597829448 -1.87928 0.064833 -2.3181584 0.07117523

xt 0.720411483 0.162411454 4.435718 3.76E-05 0.3958581 1.04496487

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10STATISTICS FOR BUSINESS AND FINANCE

7.b. Interpretation of Coefficients:

The calculated β-value for Boeing excess return and Excess market return is 1.11931665. The calculated β-value for IBM excess

return and Excess market return is 0.720411483. The calculated β-values define that BA price indexes are 111.93% less volatile than

the market, whereas the volatility level of IBM compared to the market is 72.04%. Therefore, it can be stated that Boeing (BA) is

highly volatile than IBM. Therefore, Boeing (BA) is considered to be more profitable than IBM price returns.

7.c. Interpretation of R2:

The linear regression tables describe that the values of R2 of BA and IBM are 0.40482754 and 0.237985555. The R2 indicates

the relationship of the dependent variable with the independent variable. Hence, from the values of multiple R2 of the two price returns

it could be stated that Boeing (BA) excess return (40.48%) is more associated than the association of IBM (23.80%).

7.d. Construction of 95% confidence interval for Slope Efficient:

Confidence Interval of IBM Price Return:

A. For Boeing (BA) price return, slope (β1) = 1.11931665, Standard Error = 0.170989356, d.f. = 64, t-value = 6.546119. Hence,

the 95% confidence interval for the slope coefficient would be (0.777621689, 1.461011607).

B. For IBM price return, slope (β1) = 0.720411483, Standard Error = 0.162411454, d.f. = 64, t-value = 4.435718. Hence, the 95%

confidence interval for the slope coefficient would be (0.3958581, 1.04496487).

8. Preferable neutral Price Return:

The testing of aggressiveness of the excess price returns needs the following hypothesis:

Null hypothesis (H0): β1 = 1

Alternative hypothesis (H1): β1 < 1

For BA price returns, β1 is 1.11931665 along with the standard error (SE) 0.170989356. The “residual degrees of freedom” is

63 and calculated p-value is 0.0. Hence, t = β1/ SE = 6.546119.

For IBM price indexes, β1 is 0.720411483 along with the standard error (SE) 0.162411454. The “residual degrees of freedom”

is 63 and calculated p-value is 0.0. Hence, t = β1/ SE = 4.435718.

For both the excess price returns, the p-values are positive t-value and equal degrees of freedom 64. The 95% confidence intervals

for beta values of both BA and IBM price returns are (0.777621689, 1.461011607) and (0.3958581, 1.04496487). The confidence

intervals near to 0 refers more neutral nature for price excess return. The confidence intervals of t-statistics indicate that IBM price

return is more neutral (Moffett, Stonehill and Eiteman 2014).

9. Normal Probability Plot in OLS:

IBM Ecess Price return residual plot:

7.b. Interpretation of Coefficients:

The calculated β-value for Boeing excess return and Excess market return is 1.11931665. The calculated β-value for IBM excess

return and Excess market return is 0.720411483. The calculated β-values define that BA price indexes are 111.93% less volatile than

the market, whereas the volatility level of IBM compared to the market is 72.04%. Therefore, it can be stated that Boeing (BA) is

highly volatile than IBM. Therefore, Boeing (BA) is considered to be more profitable than IBM price returns.

7.c. Interpretation of R2:

The linear regression tables describe that the values of R2 of BA and IBM are 0.40482754 and 0.237985555. The R2 indicates

the relationship of the dependent variable with the independent variable. Hence, from the values of multiple R2 of the two price returns

it could be stated that Boeing (BA) excess return (40.48%) is more associated than the association of IBM (23.80%).

7.d. Construction of 95% confidence interval for Slope Efficient:

Confidence Interval of IBM Price Return:

A. For Boeing (BA) price return, slope (β1) = 1.11931665, Standard Error = 0.170989356, d.f. = 64, t-value = 6.546119. Hence,

the 95% confidence interval for the slope coefficient would be (0.777621689, 1.461011607).

B. For IBM price return, slope (β1) = 0.720411483, Standard Error = 0.162411454, d.f. = 64, t-value = 4.435718. Hence, the 95%

confidence interval for the slope coefficient would be (0.3958581, 1.04496487).

8. Preferable neutral Price Return:

The testing of aggressiveness of the excess price returns needs the following hypothesis:

Null hypothesis (H0): β1 = 1

Alternative hypothesis (H1): β1 < 1

For BA price returns, β1 is 1.11931665 along with the standard error (SE) 0.170989356. The “residual degrees of freedom” is

63 and calculated p-value is 0.0. Hence, t = β1/ SE = 6.546119.

For IBM price indexes, β1 is 0.720411483 along with the standard error (SE) 0.162411454. The “residual degrees of freedom”

is 63 and calculated p-value is 0.0. Hence, t = β1/ SE = 4.435718.

For both the excess price returns, the p-values are positive t-value and equal degrees of freedom 64. The 95% confidence intervals

for beta values of both BA and IBM price returns are (0.777621689, 1.461011607) and (0.3958581, 1.04496487). The confidence

intervals near to 0 refers more neutral nature for price excess return. The confidence intervals of t-statistics indicate that IBM price

return is more neutral (Moffett, Stonehill and Eiteman 2014).

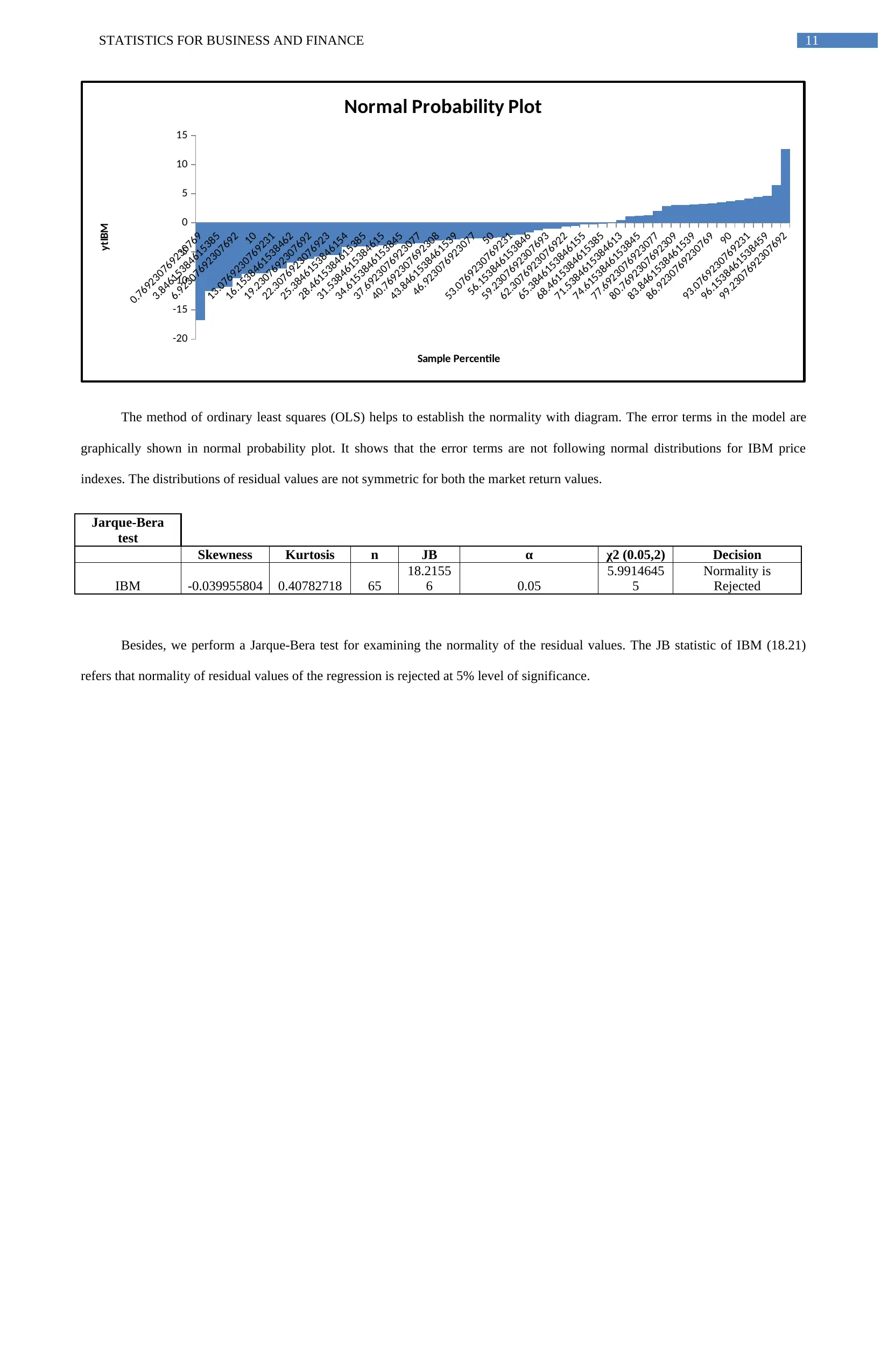

9. Normal Probability Plot in OLS:

IBM Ecess Price return residual plot:

11STATISTICS FOR BUSINESS AND FINANCE

0.769230769230769

3.84615384615385

6.92307692307692

10

13.0769230769231

16.1538461538462

19.2307692307692

22.3076923076923

25.3846153846154

28.4615384615385

31.5384615384615

34.6153846153845

37.6923076923077

40.7692307692308

43.8461538461539

46.923076923077

50

53.0769230769231

56.153846153846

59.2307692307693

62.3076923076922

65.3846153846155

68.4615384615385

71.5384615384613

74.6153846153845

77.6923076923077

80.7692307692309

83.8461538461539

86.9230769230769

90

93.0769230769231

96.1538461538459

99.2307692307692

-20

-15

-10

-5

0

5

10

15

Normal Probability Plot

Sample Percentile

ytIBM

The method of ordinary least squares (OLS) helps to establish the normality with diagram. The error terms in the model are

graphically shown in normal probability plot. It shows that the error terms are not following normal distributions for IBM price

indexes. The distributions of residual values are not symmetric for both the market return values.

Jarque-Bera

test

Skewness Kurtosis n JB α χ2 (0.05,2) Decision

IBM -0.039955804 0.40782718 65

18.2155

6 0.05

5.9914645

5

Normality is

Rejected

Besides, we perform a Jarque-Bera test for examining the normality of the residual values. The JB statistic of IBM (18.21)

refers that normality of residual values of the regression is rejected at 5% level of significance.

0.769230769230769

3.84615384615385

6.92307692307692

10

13.0769230769231

16.1538461538462

19.2307692307692

22.3076923076923

25.3846153846154

28.4615384615385

31.5384615384615

34.6153846153845

37.6923076923077

40.7692307692308

43.8461538461539

46.923076923077

50

53.0769230769231

56.153846153846

59.2307692307693

62.3076923076922

65.3846153846155

68.4615384615385

71.5384615384613

74.6153846153845

77.6923076923077

80.7692307692309

83.8461538461539

86.9230769230769

90

93.0769230769231

96.1538461538459

99.2307692307692

-20

-15

-10

-5

0

5

10

15

Normal Probability Plot

Sample Percentile

ytIBM

The method of ordinary least squares (OLS) helps to establish the normality with diagram. The error terms in the model are

graphically shown in normal probability plot. It shows that the error terms are not following normal distributions for IBM price

indexes. The distributions of residual values are not symmetric for both the market return values.

Jarque-Bera

test

Skewness Kurtosis n JB α χ2 (0.05,2) Decision

IBM -0.039955804 0.40782718 65

18.2155

6 0.05

5.9914645

5

Normality is

Rejected

Besides, we perform a Jarque-Bera test for examining the normality of the residual values. The JB statistic of IBM (18.21)

refers that normality of residual values of the regression is rejected at 5% level of significance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.