Stock Performance Analysis: Holding Period Returns and CAPM

VerifiedAdded on 2023/05/28

|8

|699

|264

Homework Assignment

AI Summary

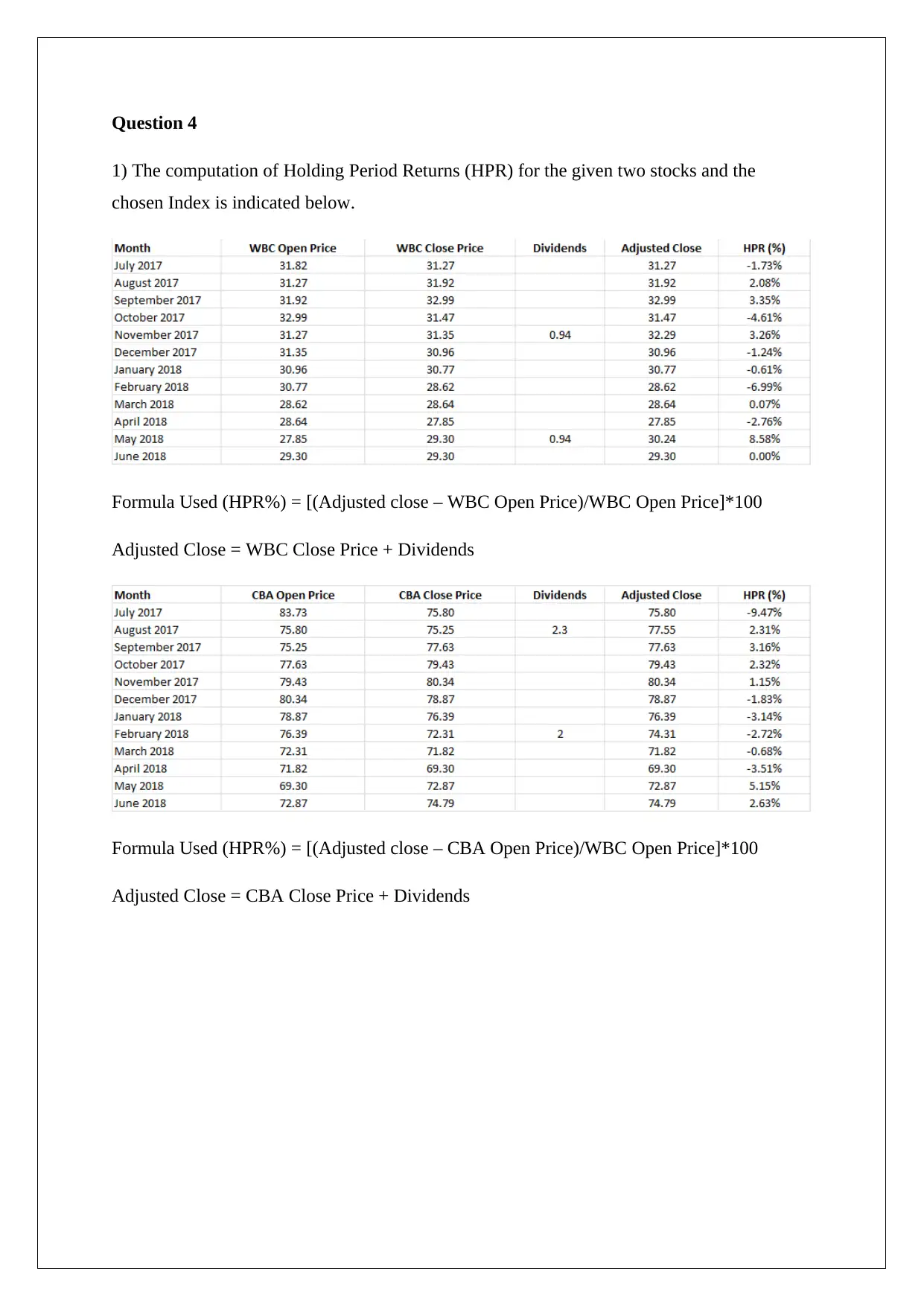

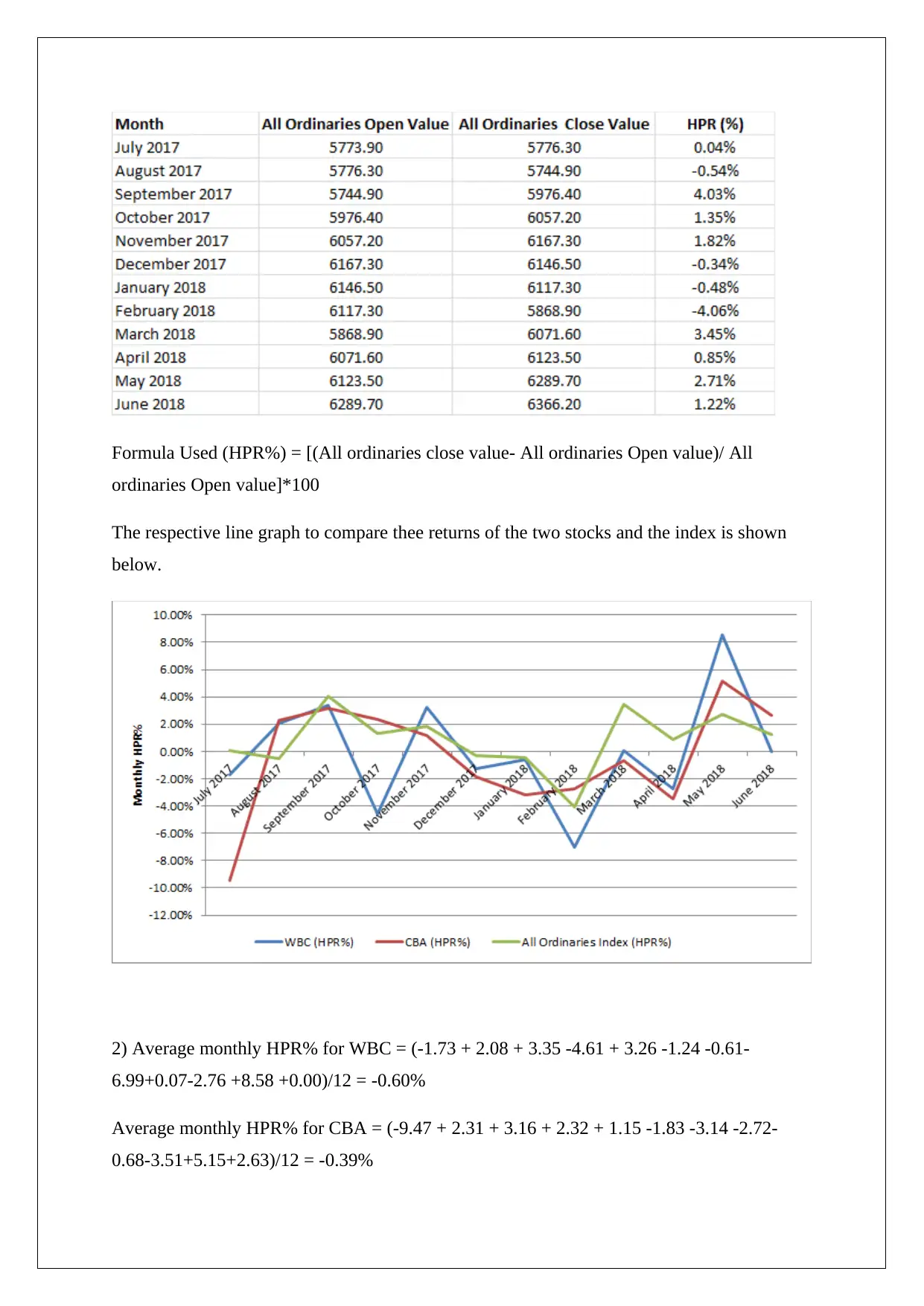

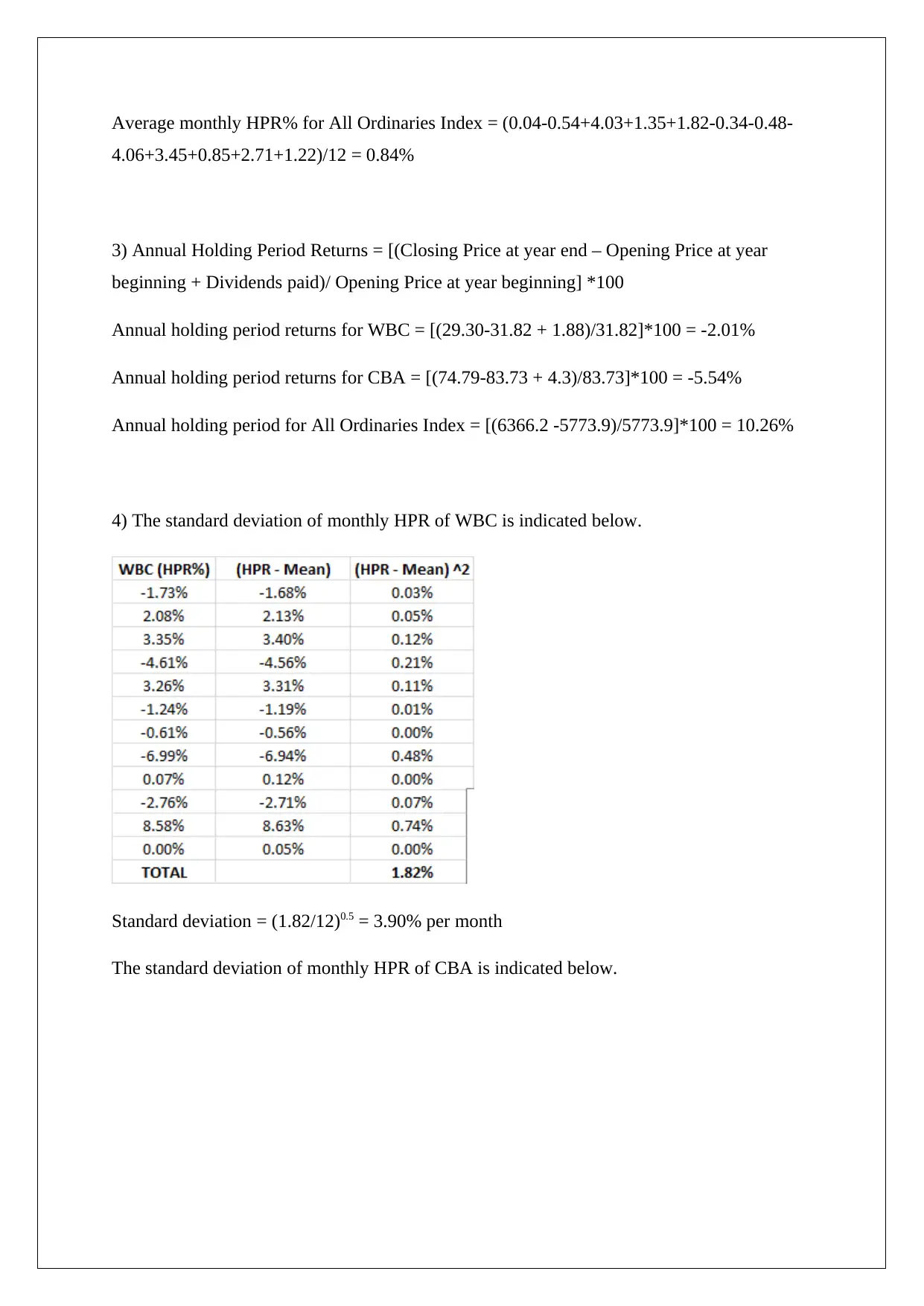

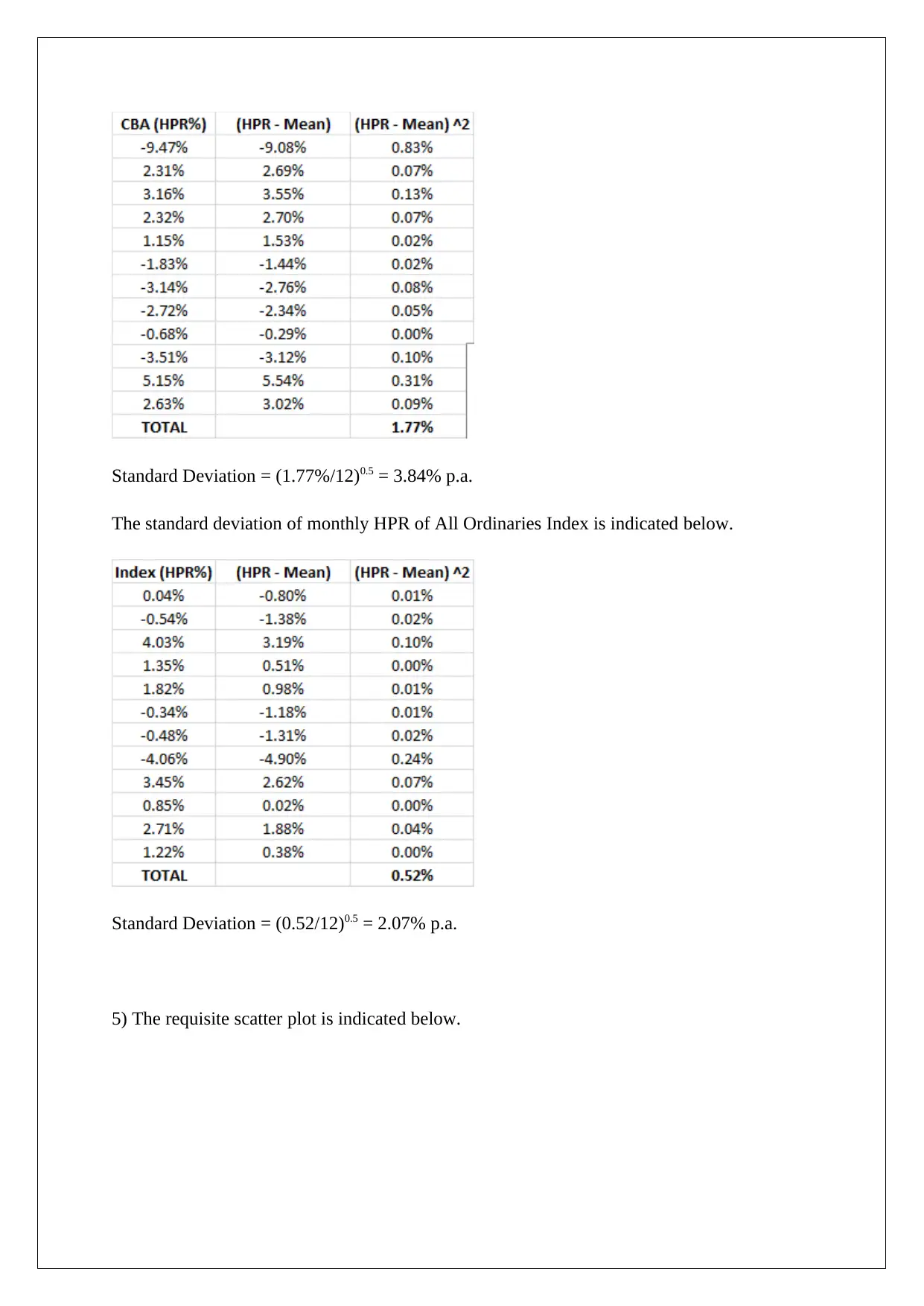

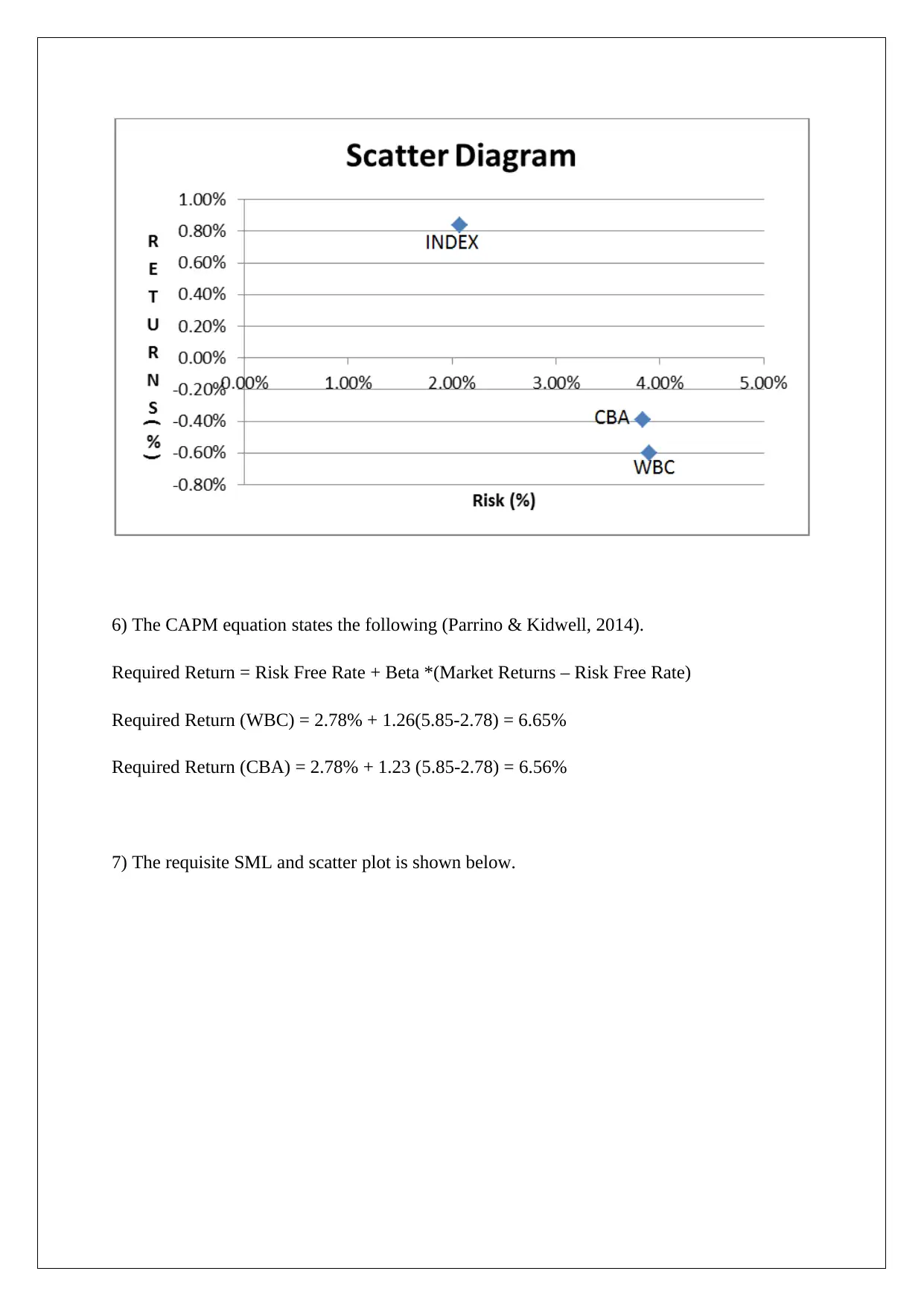

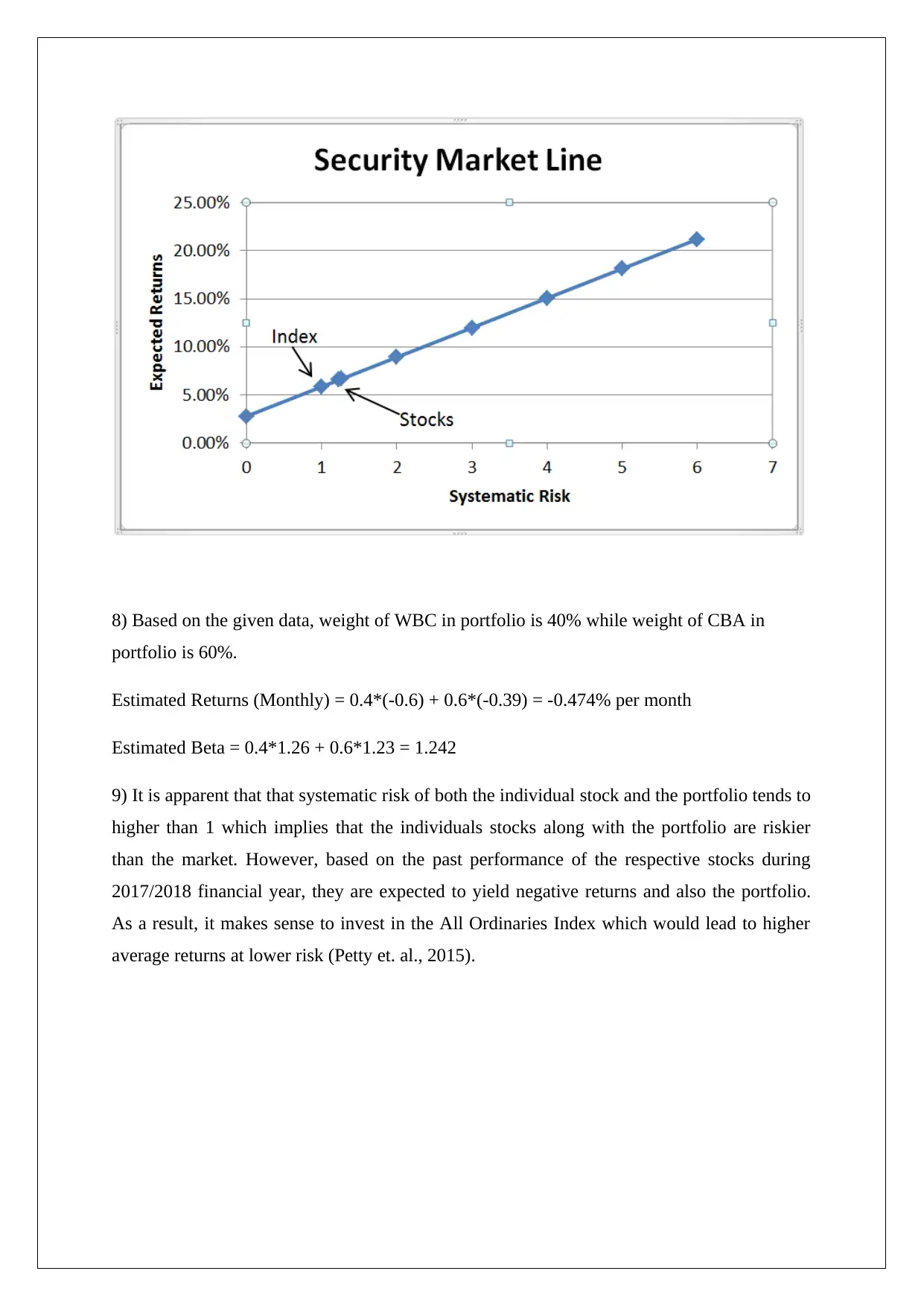

This assignment provides a comprehensive analysis of the holding period returns (HPR) for Westpac Banking Corporation (WBC), Commonwealth Bank of Australia (CBA), and the All Ordinaries Index for a specific financial year. The analysis includes calculations of monthly and annual HPR, average monthly HPR, and standard deviation of monthly HPR for each investment. A line graph is used to compare the monthly returns of the two stocks and the index. The assignment also involves creating a scatter plot and applying the Capital Asset Pricing Model (CAPM) to determine the required return for each stock, followed by constructing the Security Market Line (SML). Furthermore, the assignment calculates the estimated returns and beta for a portfolio consisting of WBC and CBA, with specified weights. The conclusion recommends investing in the All Ordinaries Index due to its higher average returns and lower risk compared to individual stocks and the constructed portfolio, based on their past performance.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.