Stock Price Analysis: British Petroleum P.L.C. (2018) - Module X

VerifiedAdded on 2021/12/16

|8

|264

|137

Report

AI Summary

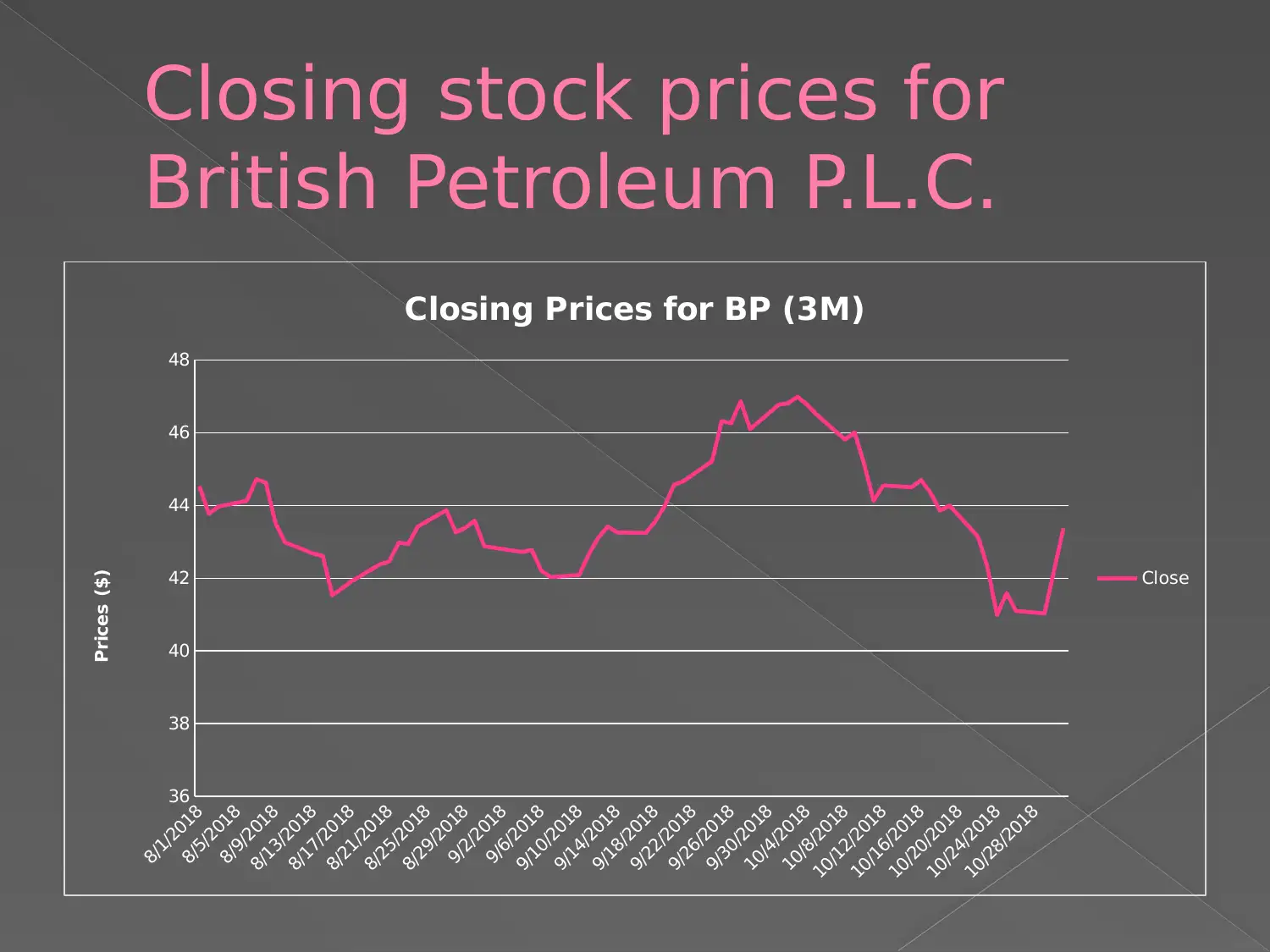

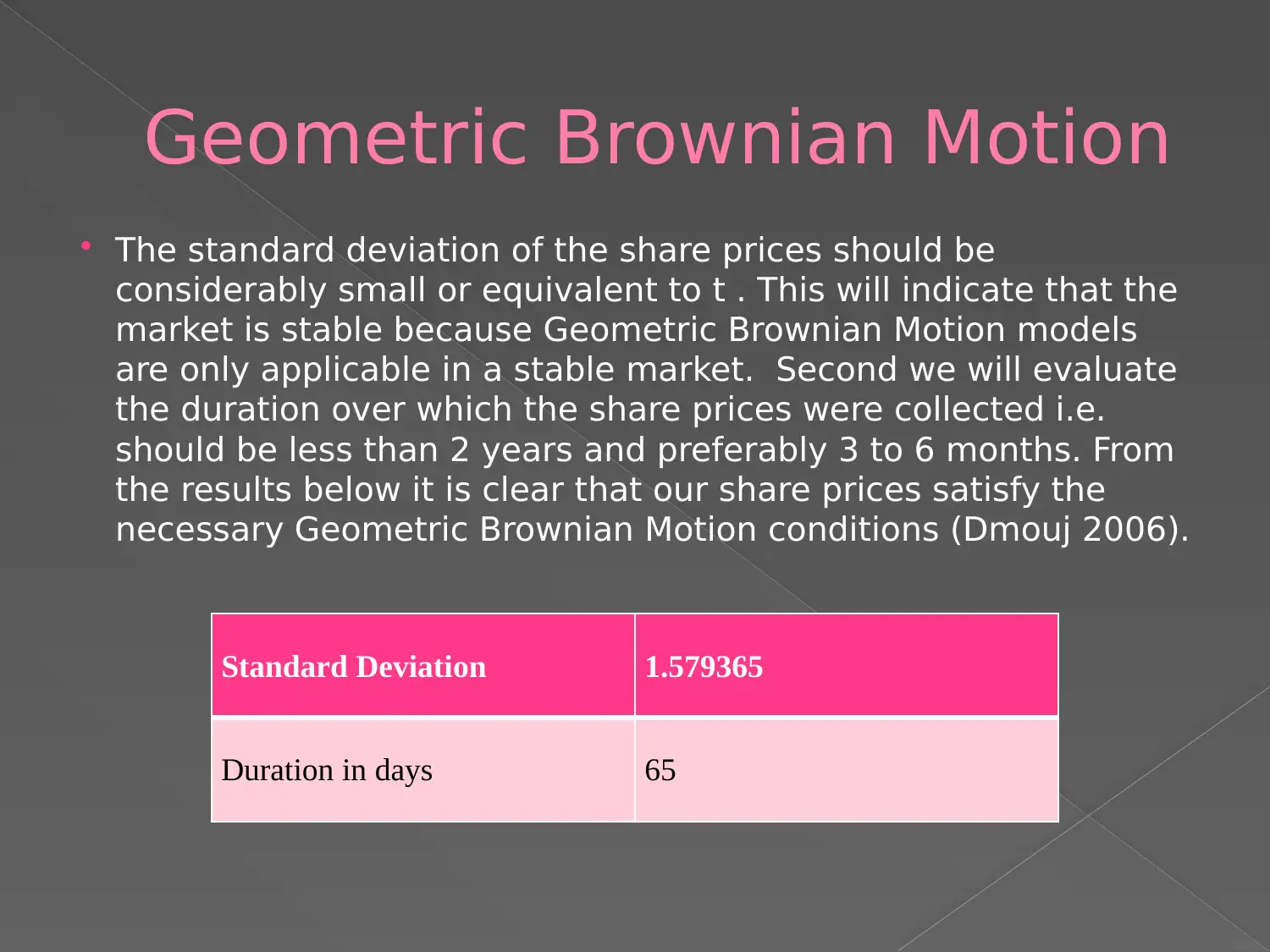

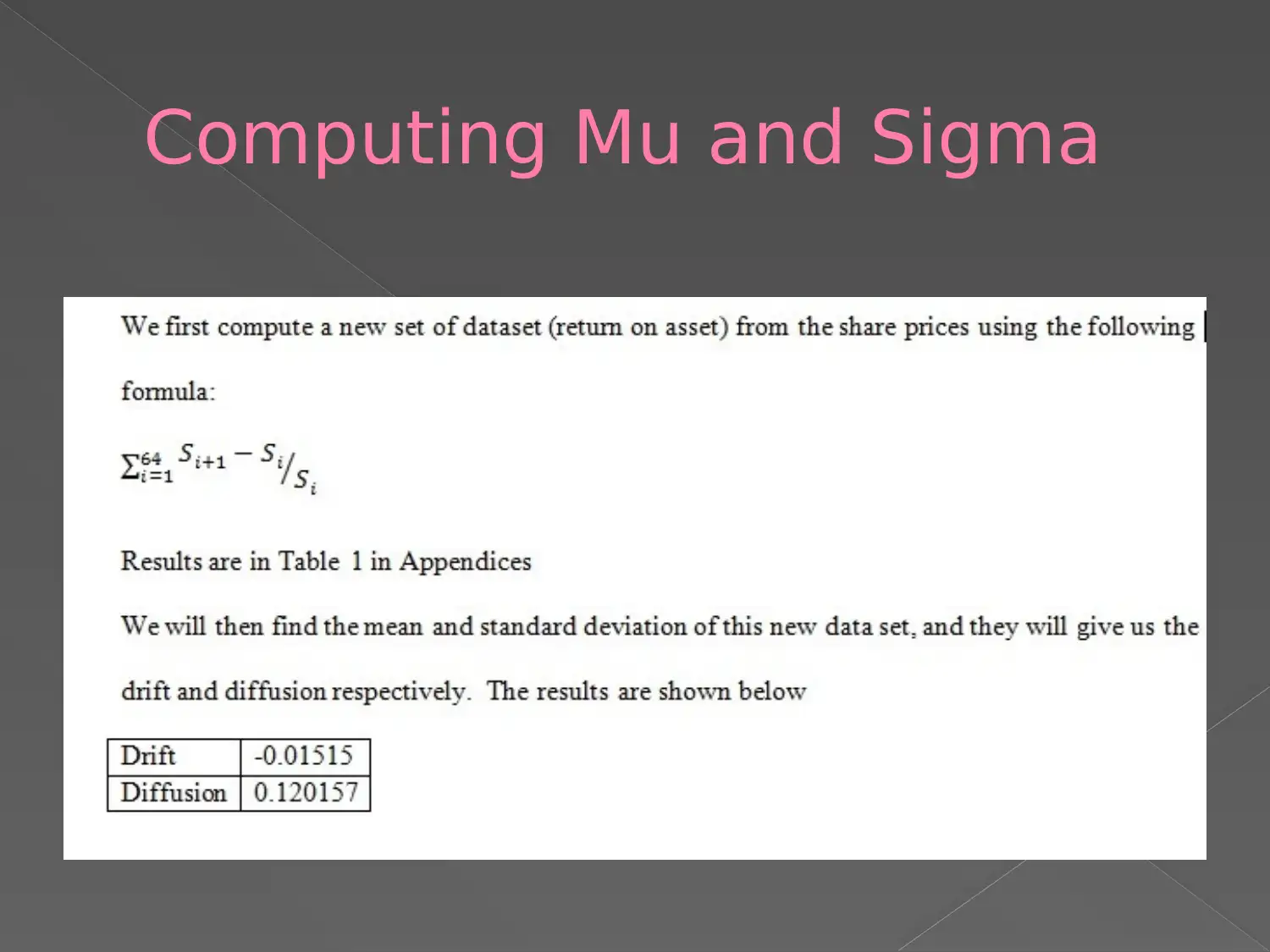

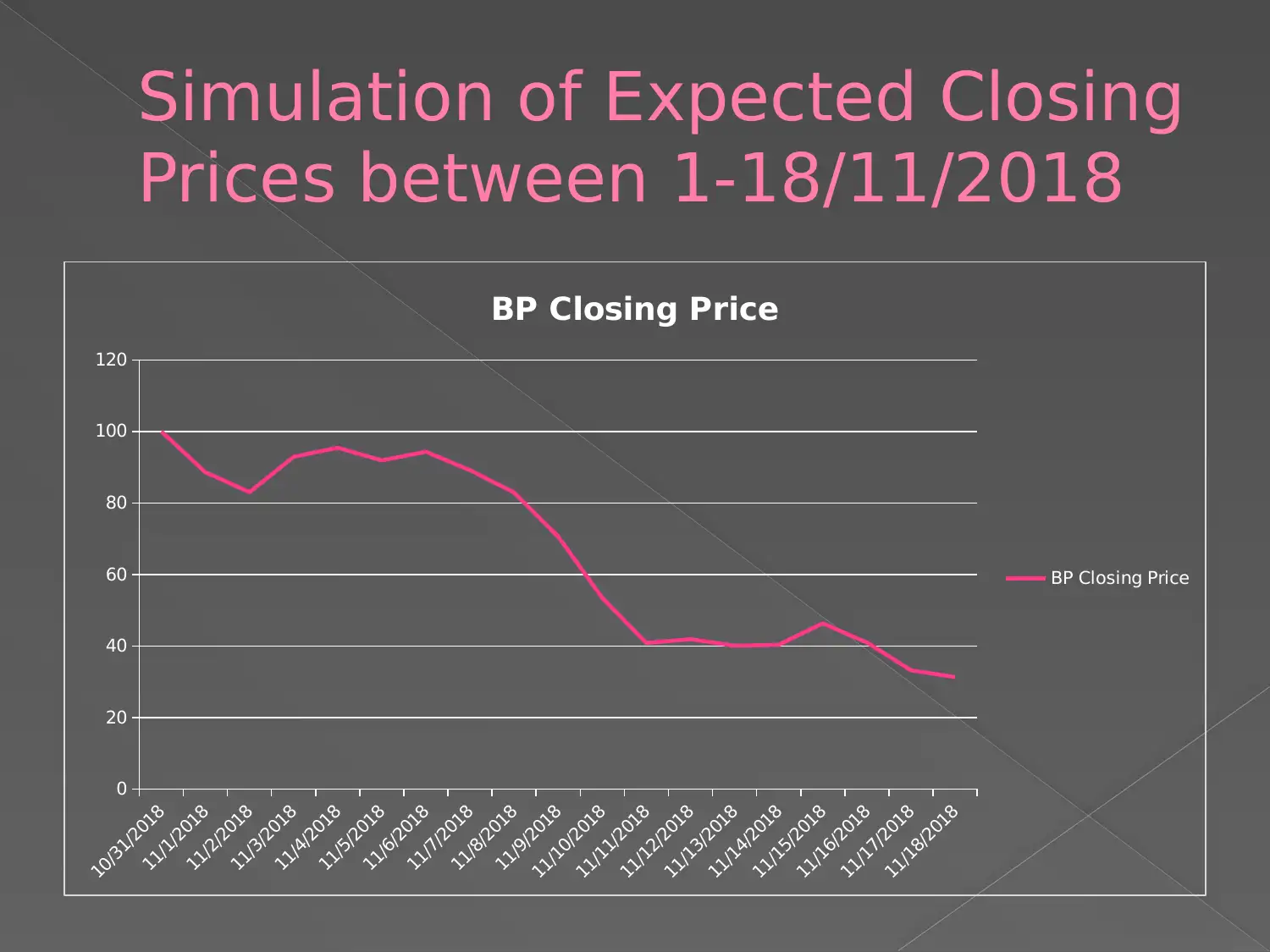

This report presents an analysis of British Petroleum's (BP) stock prices, focusing on the application of Geometric Brownian Motion (GBM). The report discusses the concepts of drift (Mu) and volatility (Sigma) and their relationship to time, emphasizing that these parameters are not constant. The report explains the significance of a small standard deviation in share prices, indicating market stability, which is a prerequisite for GBM models. The analysis covers a time frame of less than two years, meeting the conditions for GBM. The report references relevant literature and includes appendices. The primary focus is to analyze the behavior of the share prices of British Petroleum and to apply a financial model to it.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.