Stock Risk Analysis & Portfolio Diversification in Corporate Finance

VerifiedAdded on 2023/06/03

|4

|727

|498

Homework Assignment

AI Summary

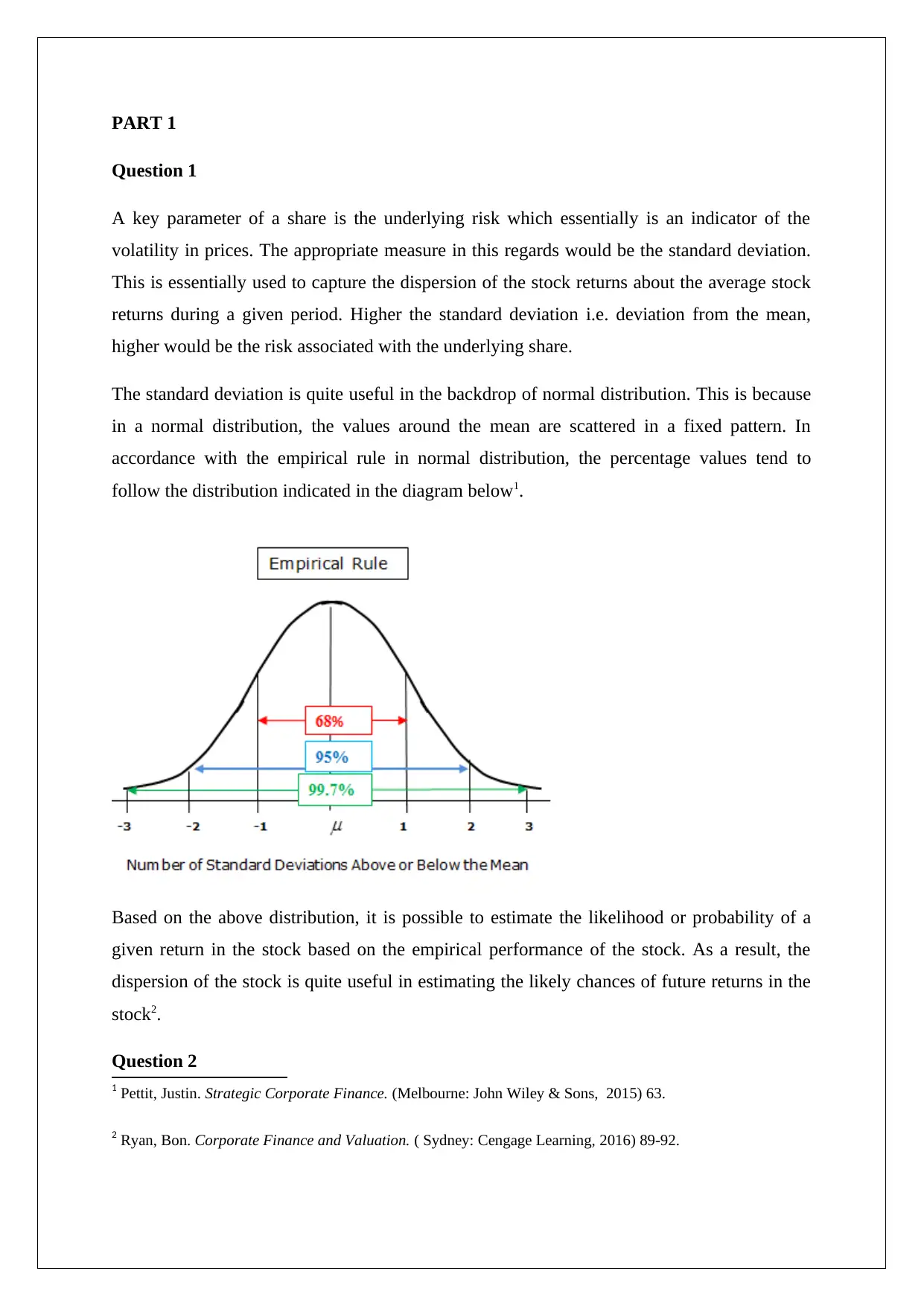

This corporate finance assignment delves into the analysis of stock risk, focusing on standard deviation as a key measure of volatility. It explains how standard deviation helps estimate the likelihood of future stock returns within a normal distribution. The assignment further explores portfolio theory, emphasizing the importance of negative correlation between stock returns to achieve risk reduction through diversification. It also examines the impact of incorporating a risk-free asset into a portfolio, demonstrating that diversification benefits are negated when one asset has zero standard deviation. Desklib provides access to this and many other solved assignments to support student learning.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.