Stockland Units Auditing and Ethics Report: 2019 Analysis & Review

VerifiedAdded on 2023/04/21

|15

|2750

|222

Report

AI Summary

This report provides an in-depth analysis of the auditing and ethics of Stockland Units, focusing on the 2018 financial year. The report begins with an executive summary, followed by an introduction that outlines the scope of the analysis, which includes an assessment of the level of materiality, a preliminary review of the company's financial position, and an interpretation of its cash flow statements. The analysis of materiality considers both quantitative and qualitative factors, including financial risks and the impact of estimations on the company's financial statements. The preliminary review examines the current and quick ratios, as well as the debt-to-equity ratio. Finally, the cash flow interpretation assesses the company's cash inflows and outflows from operating, investing, and financing activities. The report concludes with a summary of findings and references to support the analysis.

Auditing and Ethics

2019

2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stockland units

Executive Summary

It is important for the organization to adhere to the disclosures pattern so that it helps in

creating a positive image for the organization. To cement the footstep in the industry it is

essential that the company will operate in a diligent manner. Stockland units are considered

for the course of study and the report stress upon the materiality level of the company

together with the preliminary review. Further, the cash flow of the organization has been

discussed and the opinion of the auditor has been provided.

2

Executive Summary

It is important for the organization to adhere to the disclosures pattern so that it helps in

creating a positive image for the organization. To cement the footstep in the industry it is

essential that the company will operate in a diligent manner. Stockland units are considered

for the course of study and the report stress upon the materiality level of the company

together with the preliminary review. Further, the cash flow of the organization has been

discussed and the opinion of the auditor has been provided.

2

Stockland units

Contents

Introduction.......................................................................................................................................3

1. Level of the materiality of Stockland.........................................................................................3

2. Preliminary Review.......................................................................................................................5

3. Cash flow interpretation................................................................................................................6

Conclusion.........................................................................................................................................8

References.........................................................................................................................................9

3

Contents

Introduction.......................................................................................................................................3

1. Level of the materiality of Stockland.........................................................................................3

2. Preliminary Review.......................................................................................................................5

3. Cash flow interpretation................................................................................................................6

Conclusion.........................................................................................................................................8

References.........................................................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stockland units

Introduction

Stockland units are engaged in the business of managing and developing shopping centers,

logistic centers, buildings, communities, etc. In this report, Stockland units are selected in

relation to the concept of materiality, analytical review and framing an opinion on the same.

In short, the company is analyzed under various parameters that enable to answer where the

company comprises of materiality or the auditor has provided a clean report. It is essential

for an organization to have an annual report that is free from any unclear statement that will

help in the conduct of the audit.

1. Level of the materiality of Stockland

Materiality holds a lot of significance for an organization with respect to its financials.

Quantitative Considerations and Qualitative Considerations are the two aspects of

considering materiality. The accounts prepared and presented by the management of an

organization may have a lot of misstatements but only those qualify as material that has the

tendency to impact the investment related decisions of an investor (Mock et. al, 2013). There

are various aspects that determine the materiality of specific information such as its nature,

usefulness, size and etc. It is the responsibility of an auditor to trace the presence of material

misstatements in the financial statements of the company and accordingly take necessary

measures so as to reduce or eliminate the same (Baldwin, 2010). Detecting the presence of

material misstatements in the financials of an organization is a task in itself and therefore, it

is an essential part of auditing. This is why the auditors chose to determine the significant

impact of material misstatements on the overall financial statements of an organization by

means of applying the materiality concept during the time of planning and the execution of

the same. It is important for the managers to keep a strong assessment of the annual report

because the details regarding any mistake can be traced (Blay, Geiger, & North, 2013)

Materiality can be quantitative as well as qualitative terms. Following are the few steps that

are required to be followed so as to deal with quantitative considerations-

A preliminary judgment is chosen initially for materiality during the planning stage of the

audit by means of assuming 0.5% of total assets or 5-10% of normalized net income. The

normalized net income must not be comprised of incomes from discounted operations and

one-time loss or income (Carcello, 2012). In the next step, the performance materiality is

taken into consideration. Thereafter, in the third step, the estimation of material

misstatements with respect to specific accounts must be done. By following all these steps, an

4

Introduction

Stockland units are engaged in the business of managing and developing shopping centers,

logistic centers, buildings, communities, etc. In this report, Stockland units are selected in

relation to the concept of materiality, analytical review and framing an opinion on the same.

In short, the company is analyzed under various parameters that enable to answer where the

company comprises of materiality or the auditor has provided a clean report. It is essential

for an organization to have an annual report that is free from any unclear statement that will

help in the conduct of the audit.

1. Level of the materiality of Stockland

Materiality holds a lot of significance for an organization with respect to its financials.

Quantitative Considerations and Qualitative Considerations are the two aspects of

considering materiality. The accounts prepared and presented by the management of an

organization may have a lot of misstatements but only those qualify as material that has the

tendency to impact the investment related decisions of an investor (Mock et. al, 2013). There

are various aspects that determine the materiality of specific information such as its nature,

usefulness, size and etc. It is the responsibility of an auditor to trace the presence of material

misstatements in the financial statements of the company and accordingly take necessary

measures so as to reduce or eliminate the same (Baldwin, 2010). Detecting the presence of

material misstatements in the financials of an organization is a task in itself and therefore, it

is an essential part of auditing. This is why the auditors chose to determine the significant

impact of material misstatements on the overall financial statements of an organization by

means of applying the materiality concept during the time of planning and the execution of

the same. It is important for the managers to keep a strong assessment of the annual report

because the details regarding any mistake can be traced (Blay, Geiger, & North, 2013)

Materiality can be quantitative as well as qualitative terms. Following are the few steps that

are required to be followed so as to deal with quantitative considerations-

A preliminary judgment is chosen initially for materiality during the planning stage of the

audit by means of assuming 0.5% of total assets or 5-10% of normalized net income. The

normalized net income must not be comprised of incomes from discounted operations and

one-time loss or income (Carcello, 2012). In the next step, the performance materiality is

taken into consideration. Thereafter, in the third step, the estimation of material

misstatements with respect to specific accounts must be done. By following all these steps, an

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stockland units

auditor will be able to estimate overall misstatements and draw comparisons with prior

estimated misstatements in order to ascertain if at all the financials are manipulated.

Qualitative considerations are concerned with the material misstatements that do not fall in

the domain of quantitative considerations. Absence of adequate disclosures in the final

reports of an organization such as contingent liabilities, consolidated statements, and so on is

a fine example of qualitative considerations (Niemi & Sundgren, 2012). The exit of a senior

manager from the organization must also be deemed as material information and therefore,

the same must be disclosed in the auditors’ report. It is the right of the investors to know

about the sudden alterations in the senior management and what the organization has to say

upon the same.

The quantitative considerations of materiality for Stockland can be done either by means of

having 0.5% of total assets or 5-10% of normalized net income. The total assets of Stockland

are amounting at $19291 million which means the estimated materiality of the same is the

expression of 0.5% of $19221 million. In the second scenario, the net income represents the

NPBT which is $966 million in the year 2018. Therefore, the estimated materiality of

Stockland is either 5% or 10% of $966 million.

Stockland takes several methods and assumptions so as to determine the FV fewer costs of

disposal. The company evaluates the same on the basis of past experiences, assumptions,

policies, and plans. The company makes such assumptions that are achievable in the real

world for if the same didn’t work out as what was expected then the profitability of the

organization shall be severely impacted. Therefore, it is the responsibility of an auditor to

evaluate all such estimations and the impacts of the same on the business activities of an

organization

5

auditor will be able to estimate overall misstatements and draw comparisons with prior

estimated misstatements in order to ascertain if at all the financials are manipulated.

Qualitative considerations are concerned with the material misstatements that do not fall in

the domain of quantitative considerations. Absence of adequate disclosures in the final

reports of an organization such as contingent liabilities, consolidated statements, and so on is

a fine example of qualitative considerations (Niemi & Sundgren, 2012). The exit of a senior

manager from the organization must also be deemed as material information and therefore,

the same must be disclosed in the auditors’ report. It is the right of the investors to know

about the sudden alterations in the senior management and what the organization has to say

upon the same.

The quantitative considerations of materiality for Stockland can be done either by means of

having 0.5% of total assets or 5-10% of normalized net income. The total assets of Stockland

are amounting at $19291 million which means the estimated materiality of the same is the

expression of 0.5% of $19221 million. In the second scenario, the net income represents the

NPBT which is $966 million in the year 2018. Therefore, the estimated materiality of

Stockland is either 5% or 10% of $966 million.

Stockland takes several methods and assumptions so as to determine the FV fewer costs of

disposal. The company evaluates the same on the basis of past experiences, assumptions,

policies, and plans. The company makes such assumptions that are achievable in the real

world for if the same didn’t work out as what was expected then the profitability of the

organization shall be severely impacted. Therefore, it is the responsibility of an auditor to

evaluate all such estimations and the impacts of the same on the business activities of an

organization

5

Stockland units

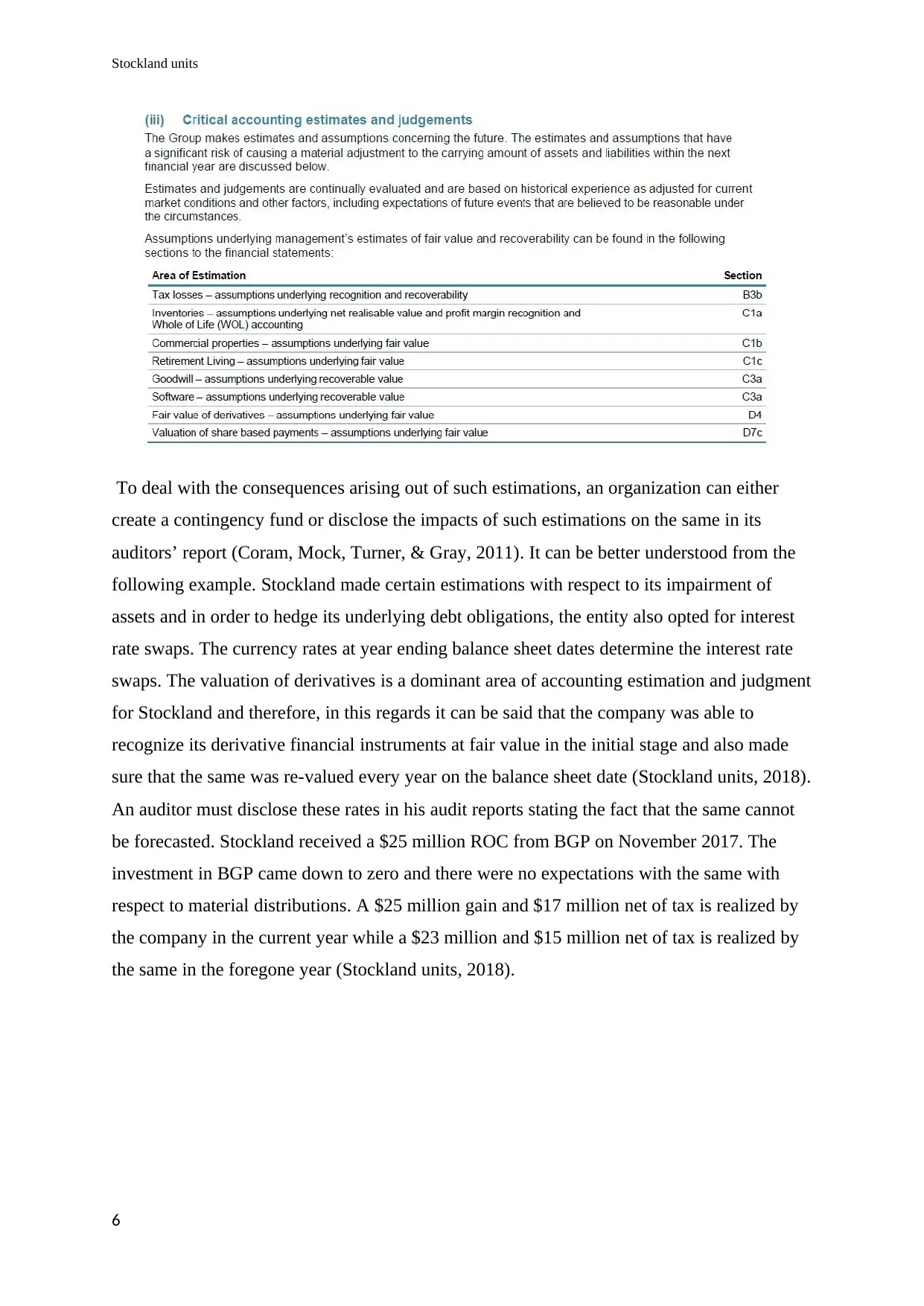

To deal with the consequences arising out of such estimations, an organization can either

create a contingency fund or disclose the impacts of such estimations on the same in its

auditors’ report (Coram, Mock, Turner, & Gray, 2011). It can be better understood from the

following example. Stockland made certain estimations with respect to its impairment of

assets and in order to hedge its underlying debt obligations, the entity also opted for interest

rate swaps. The currency rates at year ending balance sheet dates determine the interest rate

swaps. The valuation of derivatives is a dominant area of accounting estimation and judgment

for Stockland and therefore, in this regards it can be said that the company was able to

recognize its derivative financial instruments at fair value in the initial stage and also made

sure that the same was re-valued every year on the balance sheet date (Stockland units, 2018).

An auditor must disclose these rates in his audit reports stating the fact that the same cannot

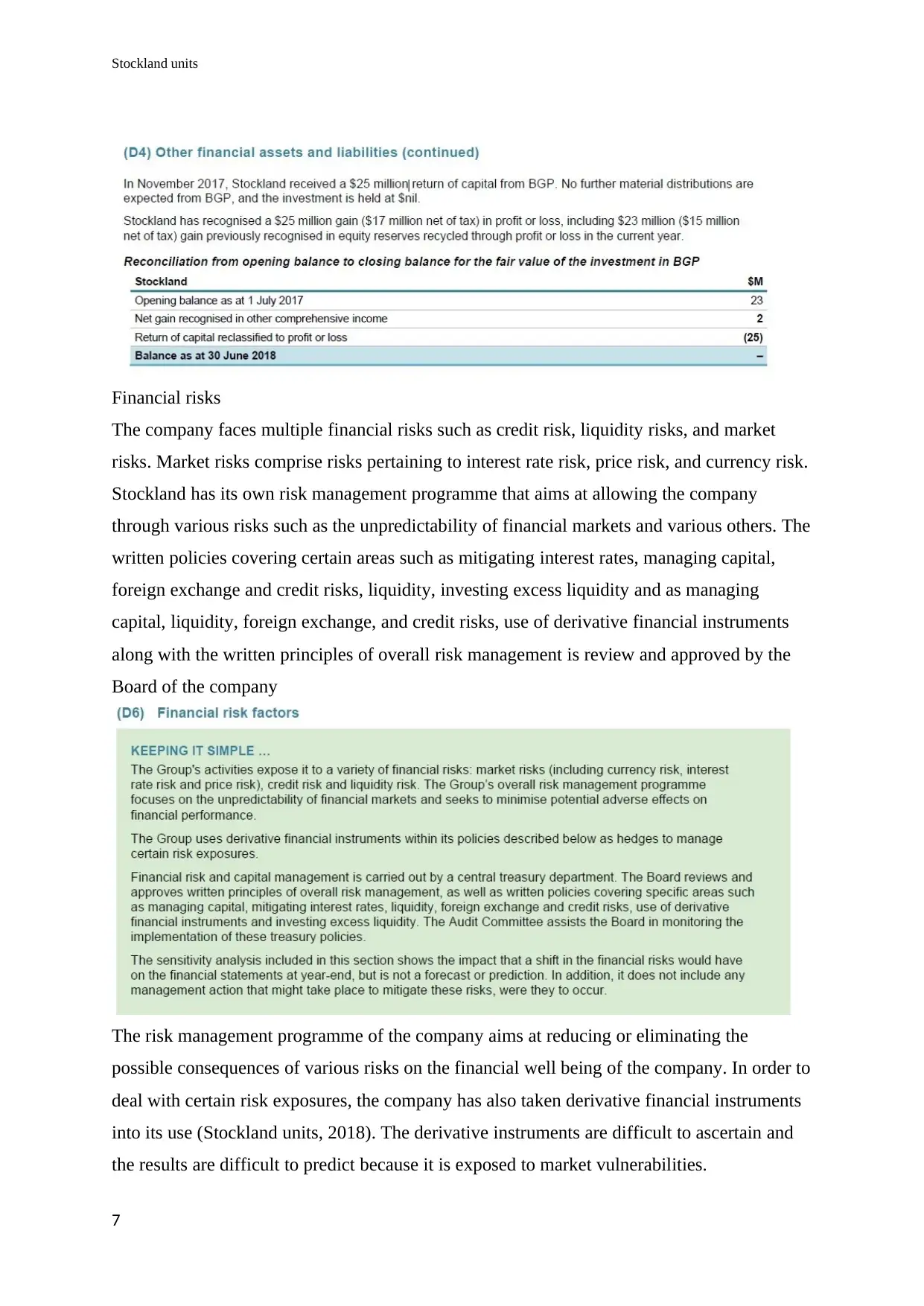

be forecasted. Stockland received a $25 million ROC from BGP on November 2017. The

investment in BGP came down to zero and there were no expectations with the same with

respect to material distributions. A $25 million gain and $17 million net of tax is realized by

the company in the current year while a $23 million and $15 million net of tax is realized by

the same in the foregone year (Stockland units, 2018).

6

To deal with the consequences arising out of such estimations, an organization can either

create a contingency fund or disclose the impacts of such estimations on the same in its

auditors’ report (Coram, Mock, Turner, & Gray, 2011). It can be better understood from the

following example. Stockland made certain estimations with respect to its impairment of

assets and in order to hedge its underlying debt obligations, the entity also opted for interest

rate swaps. The currency rates at year ending balance sheet dates determine the interest rate

swaps. The valuation of derivatives is a dominant area of accounting estimation and judgment

for Stockland and therefore, in this regards it can be said that the company was able to

recognize its derivative financial instruments at fair value in the initial stage and also made

sure that the same was re-valued every year on the balance sheet date (Stockland units, 2018).

An auditor must disclose these rates in his audit reports stating the fact that the same cannot

be forecasted. Stockland received a $25 million ROC from BGP on November 2017. The

investment in BGP came down to zero and there were no expectations with the same with

respect to material distributions. A $25 million gain and $17 million net of tax is realized by

the company in the current year while a $23 million and $15 million net of tax is realized by

the same in the foregone year (Stockland units, 2018).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stockland units

Financial risks

The company faces multiple financial risks such as credit risk, liquidity risks, and market

risks. Market risks comprise risks pertaining to interest rate risk, price risk, and currency risk.

Stockland has its own risk management programme that aims at allowing the company

through various risks such as the unpredictability of financial markets and various others. The

written policies covering certain areas such as mitigating interest rates, managing capital,

foreign exchange and credit risks, liquidity, investing excess liquidity and as managing

capital, liquidity, foreign exchange, and credit risks, use of derivative financial instruments

along with the written principles of overall risk management is review and approved by the

Board of the company

The risk management programme of the company aims at reducing or eliminating the

possible consequences of various risks on the financial well being of the company. In order to

deal with certain risk exposures, the company has also taken derivative financial instruments

into its use (Stockland units, 2018). The derivative instruments are difficult to ascertain and

the results are difficult to predict because it is exposed to market vulnerabilities.

7

Financial risks

The company faces multiple financial risks such as credit risk, liquidity risks, and market

risks. Market risks comprise risks pertaining to interest rate risk, price risk, and currency risk.

Stockland has its own risk management programme that aims at allowing the company

through various risks such as the unpredictability of financial markets and various others. The

written policies covering certain areas such as mitigating interest rates, managing capital,

foreign exchange and credit risks, liquidity, investing excess liquidity and as managing

capital, liquidity, foreign exchange, and credit risks, use of derivative financial instruments

along with the written principles of overall risk management is review and approved by the

Board of the company

The risk management programme of the company aims at reducing or eliminating the

possible consequences of various risks on the financial well being of the company. In order to

deal with certain risk exposures, the company has also taken derivative financial instruments

into its use (Stockland units, 2018). The derivative instruments are difficult to ascertain and

the results are difficult to predict because it is exposed to market vulnerabilities.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stockland units

2. Preliminary Review

The current ratio is also known as the liquidity ratio. It is the comparison between the current

assets and current liabilities of an organization. The ratio is used in order to ascertain the

ability of an entity to tackle its short term debt obligations. Stockland has lower trade

receivables and a higher volume of sales (Matthew, 2015). This means that the company must

work on its current ratio by means of uplifting the same so as to enhance its cash flows which

will eventually bring about a rise in its sales as well. Enhancing the cash flow position of a

company not only aids in the rise of sales but also allows the debts to lower down. An entity

can be free from the pressure of debts if it is able to generate higher revenues. Stockland’s

current ratio could not meet the industry’s standards for the year 2018 as the same drop down

to 0.37 from 0.51. It indicates a high level of risk for the financial well-being of the company.

The auditor must work as per analytical procedures so as to enhance the current ratio of the

company and must continue to do so unless the same is not achieved (Kaplan, 2011).

Quick asset ratio is also termed as an acid test ratio. It is the ratio between the liquid assets

and liquid liabilities of an organization. The results of Stockland quick asset ratio was just

like that of its current ratio for the year 2018. The quick asset ratio of the Stockland depicted

that the liquid assets held by the company were sufficient enough of repaying the liquid

liabilities of the same . This means that the liquid liabilities of the Stockland are enhancing

slowly as compared to the progress of its liquid assets. The investors must always look out

8

2. Preliminary Review

The current ratio is also known as the liquidity ratio. It is the comparison between the current

assets and current liabilities of an organization. The ratio is used in order to ascertain the

ability of an entity to tackle its short term debt obligations. Stockland has lower trade

receivables and a higher volume of sales (Matthew, 2015). This means that the company must

work on its current ratio by means of uplifting the same so as to enhance its cash flows which

will eventually bring about a rise in its sales as well. Enhancing the cash flow position of a

company not only aids in the rise of sales but also allows the debts to lower down. An entity

can be free from the pressure of debts if it is able to generate higher revenues. Stockland’s

current ratio could not meet the industry’s standards for the year 2018 as the same drop down

to 0.37 from 0.51. It indicates a high level of risk for the financial well-being of the company.

The auditor must work as per analytical procedures so as to enhance the current ratio of the

company and must continue to do so unless the same is not achieved (Kaplan, 2011).

Quick asset ratio is also termed as an acid test ratio. It is the ratio between the liquid assets

and liquid liabilities of an organization. The results of Stockland quick asset ratio was just

like that of its current ratio for the year 2018. The quick asset ratio of the Stockland depicted

that the liquid assets held by the company were sufficient enough of repaying the liquid

liabilities of the same . This means that the liquid liabilities of the Stockland are enhancing

slowly as compared to the progress of its liquid assets. The investors must always look out

8

Stockland units

for both quick asset ratio and a current ratio of a particular organization so as to make

appropriate investment related decisions (Merchant, 2012).

The auditor must work as per analytical procedures so as to ascertain the value of liquid

assets and liquid liabilities of the company and must also draw comparisons with the previous

year numbers.

Stockland’s debt to equity ratio is at 14 which depicts that the assets owned by the company

are much lower than the debts of the same (Stockland units, 2018). The auditor must trace the

possible reasons which ultimately allowed the debt of the company to rise over its assets and

must opt for trend analysis of the bad debt expenses.

3. Cash flow interpretation

2018 2017

Cash inflow from operating activities 728 921

Net cash outflow from investing activities -426 -380

Net cash inflow from financing activities -207 -511

The major composition of cash flow happens from the cash flow from operating activities

that is $728 in 2018. However, the cash flow from operating activities declined from $921 in

2017 to $728 (Stockland units, 2018).

The major cash receipts happened from the business operations. The primary cash receipts

happened from cash receipts from operations, proceeds from the sale of investments, and

proceedings from borrowings. On the contrary, cash payments happened from cash payments

for the operations, payment for land, payments for investment properties.

Moreover, there has been a sale of investment and derived $278 million in 2018. On the

other hand, the major outflow happened from the cash payments ($1785m) and payment for

investing properties ($463m). Further, payment was made for PPE amounting $58 million 9

Stockland units, 2018).

The cash flow statement depicts a clear view that the business is performing efficiently and

there is no reason that the business will go under liquidation or there is a danger of the going

9

for both quick asset ratio and a current ratio of a particular organization so as to make

appropriate investment related decisions (Merchant, 2012).

The auditor must work as per analytical procedures so as to ascertain the value of liquid

assets and liquid liabilities of the company and must also draw comparisons with the previous

year numbers.

Stockland’s debt to equity ratio is at 14 which depicts that the assets owned by the company

are much lower than the debts of the same (Stockland units, 2018). The auditor must trace the

possible reasons which ultimately allowed the debt of the company to rise over its assets and

must opt for trend analysis of the bad debt expenses.

3. Cash flow interpretation

2018 2017

Cash inflow from operating activities 728 921

Net cash outflow from investing activities -426 -380

Net cash inflow from financing activities -207 -511

The major composition of cash flow happens from the cash flow from operating activities

that is $728 in 2018. However, the cash flow from operating activities declined from $921 in

2017 to $728 (Stockland units, 2018).

The major cash receipts happened from the business operations. The primary cash receipts

happened from cash receipts from operations, proceeds from the sale of investments, and

proceedings from borrowings. On the contrary, cash payments happened from cash payments

for the operations, payment for land, payments for investment properties.

Moreover, there has been a sale of investment and derived $278 million in 2018. On the

other hand, the major outflow happened from the cash payments ($1785m) and payment for

investing properties ($463m). Further, payment was made for PPE amounting $58 million 9

Stockland units, 2018).

The cash flow statement depicts a clear view that the business is performing efficiently and

there is no reason that the business will go under liquidation or there is a danger of the going

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stockland units

concern. As there is no risk, hence the auditor provides no recommendation in relation to the

same (Stockland units, 2018).

As per the annual report of the company, it is stated by the annual report that the audit is done

in accordance to the Australian Auditing Standards. The Auditor responsibility is clearly

reflected in the financial report of the section. Further, it is clear from the statement of the

auditor that the evidence obtained was sufficient and appropriate and hence an unqualified

opinion was provided by the auditors. The opinion has been provided entirely on the basis of

the annual report that means the annual report is free from the material defects.

10

concern. As there is no risk, hence the auditor provides no recommendation in relation to the

same (Stockland units, 2018).

As per the annual report of the company, it is stated by the annual report that the audit is done

in accordance to the Australian Auditing Standards. The Auditor responsibility is clearly

reflected in the financial report of the section. Further, it is clear from the statement of the

auditor that the evidence obtained was sufficient and appropriate and hence an unqualified

opinion was provided by the auditors. The opinion has been provided entirely on the basis of

the annual report that means the annual report is free from the material defects.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stockland units

Conclusion

As per the overall study, it can be commented that the organization Stockland units has

ensured a proper utilization of resources and maintained strong disclosures. The audit has

been done effectively and hence, adhered to all rules and regulations. The company has

ensured that Australian Accounting Standard has been followed and there were no intentional

risks. The auditors has performed their duty and provided an unqualified opinion stating

meaning that the company has neither funds issues nor the going concern is under danger.

11

Conclusion

As per the overall study, it can be commented that the organization Stockland units has

ensured a proper utilization of resources and maintained strong disclosures. The audit has

been done effectively and hence, adhered to all rules and regulations. The company has

ensured that Australian Accounting Standard has been followed and there were no intentional

risks. The auditors has performed their duty and provided an unqualified opinion stating

meaning that the company has neither funds issues nor the going concern is under danger.

11

Stockland units

References

Baldwin, S. (2010). Doing a content audit or inventory. Pearson Press.

Blay, A. D., Geiger, M. A. & North, D. S. (2011). The Auditor's Going-Concern Opinion as a

Communication of Risk. Auditing: A Journal of Practice & Theory, 30 (2): 77- 102. Doi:

https://doi.org/10.2308/ajpt-50002

Carcello, J. (2012). What do investors want from the standard audit report? CPA Journal 82

Retrieved from https://www.questia.com/magazine/1P3-2594765681/what-do-investors-

want-from-the-standard-audit-report

Coram, P., Mock, T. J., Turner, J. & Gray, G. (2011). The communicative value of the

auditor’s report. Australian Accounting Review 21(3): 235-252. Doi:

https://doi.org/10.1111/j.1835-2561.2011.00140.x

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383. https://doi.org/10.2308/accr.00000031

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management Misconduct?.

The Accounting Review, 90(2), 495-527. Doi: https://doi.org/10.2308/accr-50871

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. Doi: https://doi.org/10.1108/01140581211283904

Mock, T. J., Bédard, J., Coram, P., Davis, S., Espahbodi, R. and Warne, R. (2013). The audit

reporting model: Current research synthesis and implications. Auditing: A Journal of

Practice and Theory, 32, 323-351. Doi: https://doi.org/10.2308/ajpt-50294

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796. Doi:

https://doi.org/10.1080/09638180.2012.671465

Stockland units. (2018). Stockland units annual report & accounts 2018. Retrieved from

https://www.stockland.com.au/investor-centre/interactive-annual-review/downloads

12

References

Baldwin, S. (2010). Doing a content audit or inventory. Pearson Press.

Blay, A. D., Geiger, M. A. & North, D. S. (2011). The Auditor's Going-Concern Opinion as a

Communication of Risk. Auditing: A Journal of Practice & Theory, 30 (2): 77- 102. Doi:

https://doi.org/10.2308/ajpt-50002

Carcello, J. (2012). What do investors want from the standard audit report? CPA Journal 82

Retrieved from https://www.questia.com/magazine/1P3-2594765681/what-do-investors-

want-from-the-standard-audit-report

Coram, P., Mock, T. J., Turner, J. & Gray, G. (2011). The communicative value of the

auditor’s report. Australian Accounting Review 21(3): 235-252. Doi:

https://doi.org/10.1111/j.1835-2561.2011.00140.x

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383. https://doi.org/10.2308/accr.00000031

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management Misconduct?.

The Accounting Review, 90(2), 495-527. Doi: https://doi.org/10.2308/accr-50871

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. Doi: https://doi.org/10.1108/01140581211283904

Mock, T. J., Bédard, J., Coram, P., Davis, S., Espahbodi, R. and Warne, R. (2013). The audit

reporting model: Current research synthesis and implications. Auditing: A Journal of

Practice and Theory, 32, 323-351. Doi: https://doi.org/10.2308/ajpt-50294

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796. Doi:

https://doi.org/10.1080/09638180.2012.671465

Stockland units. (2018). Stockland units annual report & accounts 2018. Retrieved from

https://www.stockland.com.au/investor-centre/interactive-annual-review/downloads

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.