A Comparative Analysis of Straddle and Strangle Strategies on Indexes

VerifiedAdded on 2023/04/23

|7

|729

|248

Case Study

AI Summary

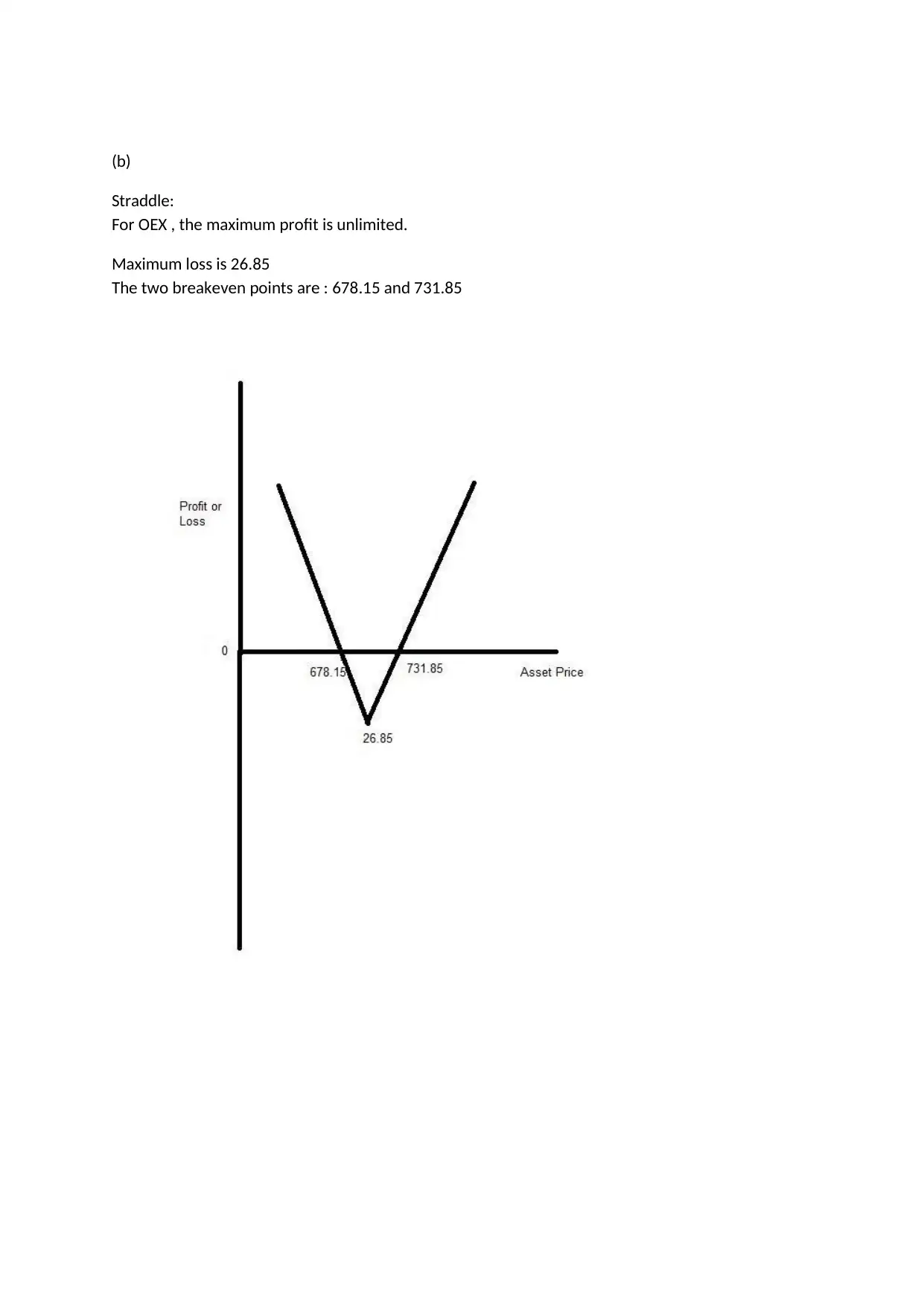

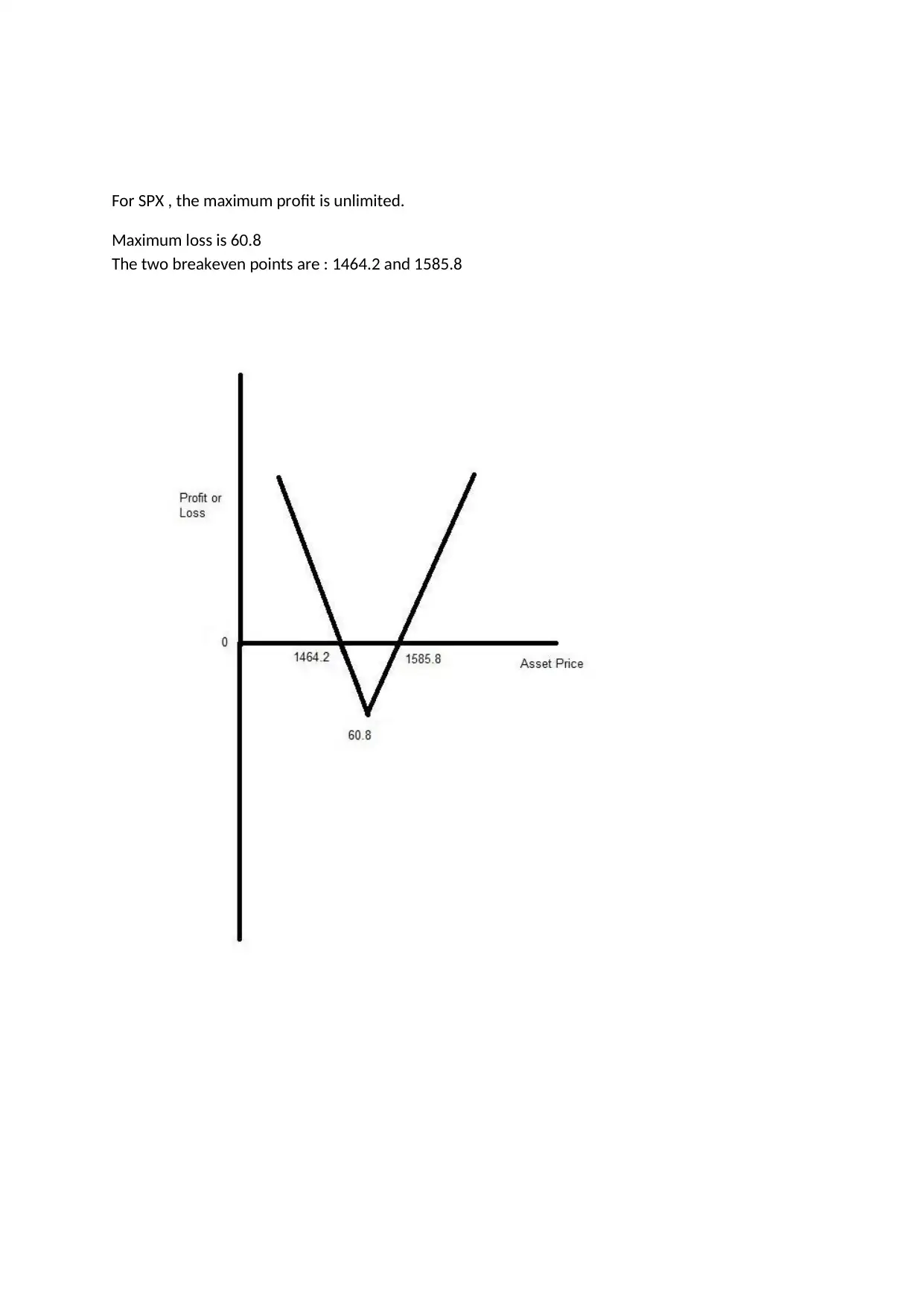

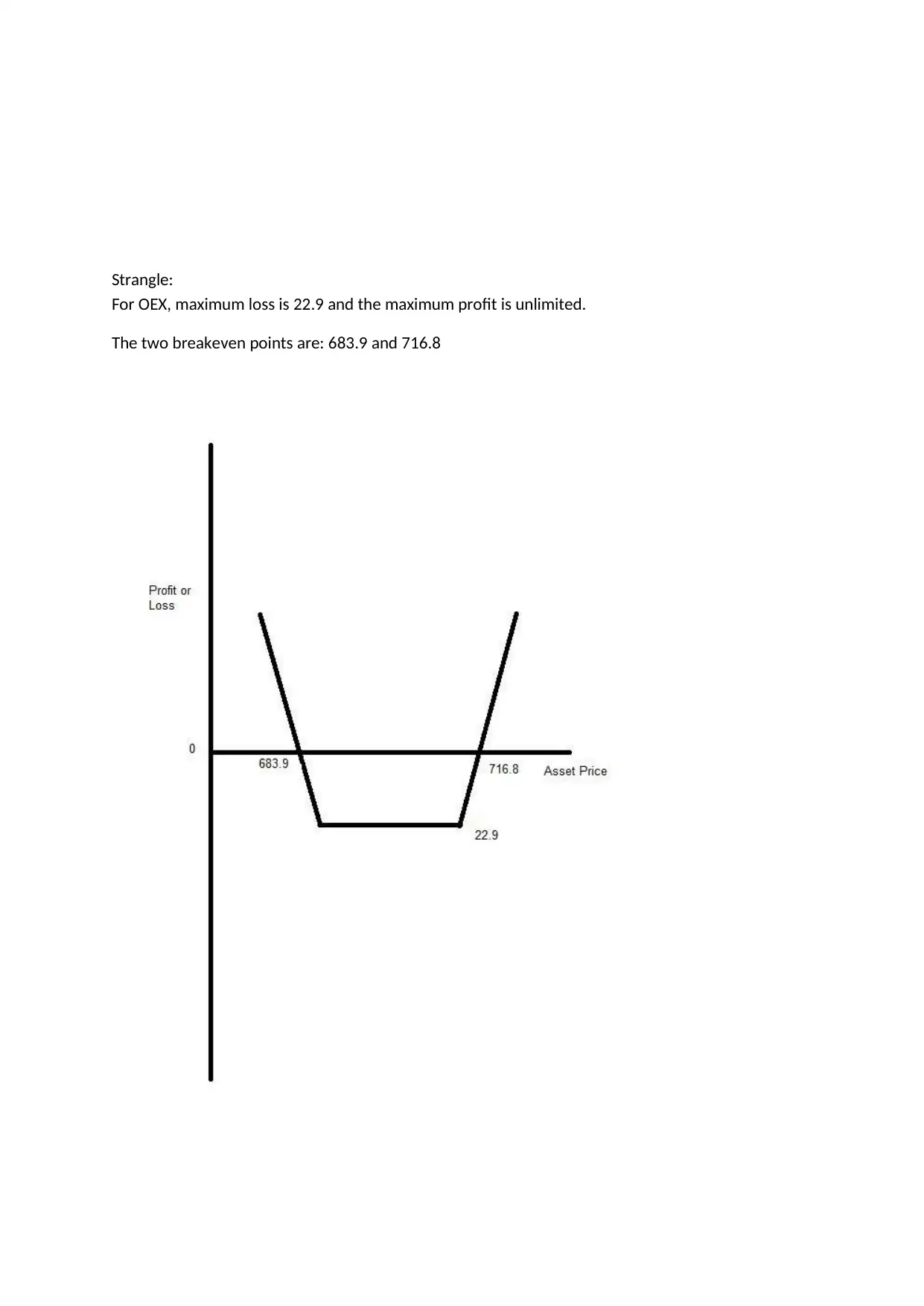

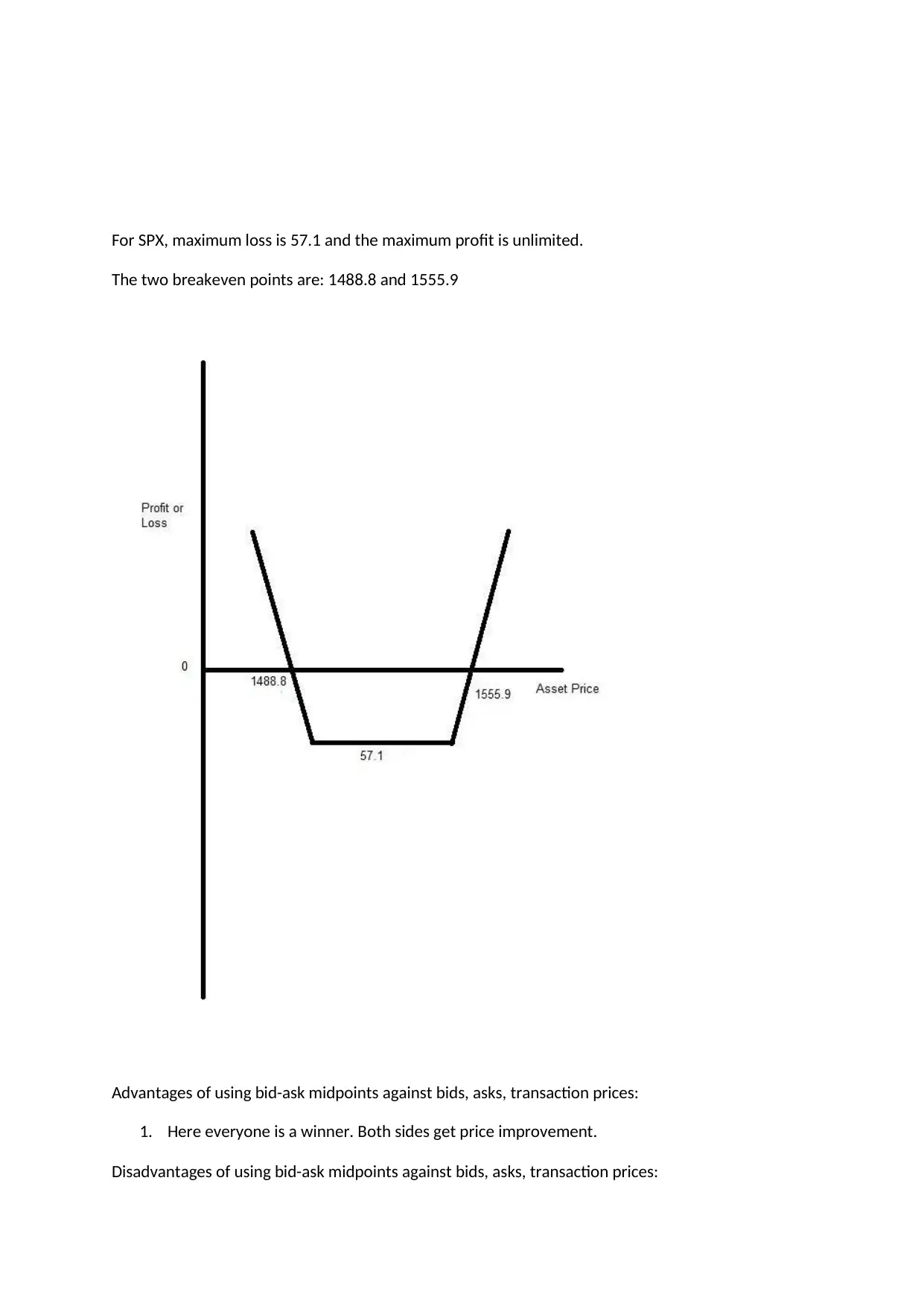

This case study analyzes straddle and strangle strategies for index options trading, using data from July 2, 2007, focusing on the OEX and SPX indices. It details the construction of long straddle and long strangle positions, comparing their advantages and disadvantages, including cost, break-even points, and sensitivity to time decay. The analysis includes calculations of maximum profit, maximum loss, and break-even points for both strategies on both indices. Additionally, it discusses the pros and cons of using bid-ask midpoints for trading, highlighting issues like reduced market transparency and reliance on data feeds. Desklib offers a platform for students to access similar solved assignments and past papers.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.