Strategic Management Project: Buckisthan Auto Performance Analysis

VerifiedAdded on 2023/01/11

|18

|6124

|96

Project

AI Summary

This project provides a detailed analysis of Buckisthan Auto, a European car manufacturer, focusing on its strategic management and competitive advantage. The project examines the company's performance across four rounds of operation, comparing key performance measures (KPMs) with actual results to assess financial health, operational efficiency, and market strategies. The analysis includes sales income, gross profit, operating profit, material costs, and bank balance trends. The project also explores the company's learning in financial, operational, marketing, and human resource aspects. It assesses the impact of decisions, such as launching new car models and automation investments, on overall performance. The report highlights the company's successes, such as increasing sales and maintaining a strong bank balance, and identifies areas for improvement, such as controlling fixed overheads and labor costs to enhance profitability and shareholder value. The project concludes with an overview of team performance and references.

Strategic

Management for

Competitive

Advantage

(Project B)

1

Management for

Competitive

Advantage

(Project B)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................... 3

COMPANY PERFORMANCE......................................................................................................3

Round 1: Comparison of KPMs with actual results..................................................................3

Round 2: Comparison of KPMs with actual results..................................................................5

Round 3: Comparison of KPMs with actual results..................................................................7

Round 4: Comparison of KPMs with actual results..................................................................8

Trends in KPMs..................................................................................................................... 10

LEARNING................................................................................................................................ 10

Financial................................................................................................................................ 10

Operations............................................................................................................................. 11

Marketing............................................................................................................................... 12

Human resources.................................................................................................................. 14

CONCLUSION........................................................................................................................... 15

TEAM PERFORMANCE............................................................................................................ 15

REFERENCES.......................................................................................................................... 18

2

INTRODUCTION......................................................................................................................... 3

COMPANY PERFORMANCE......................................................................................................3

Round 1: Comparison of KPMs with actual results..................................................................3

Round 2: Comparison of KPMs with actual results..................................................................5

Round 3: Comparison of KPMs with actual results..................................................................7

Round 4: Comparison of KPMs with actual results..................................................................8

Trends in KPMs..................................................................................................................... 10

LEARNING................................................................................................................................ 10

Financial................................................................................................................................ 10

Operations............................................................................................................................. 11

Marketing............................................................................................................................... 12

Human resources.................................................................................................................. 14

CONCLUSION........................................................................................................................... 15

TEAM PERFORMANCE............................................................................................................ 15

REFERENCES.......................................................................................................................... 18

2

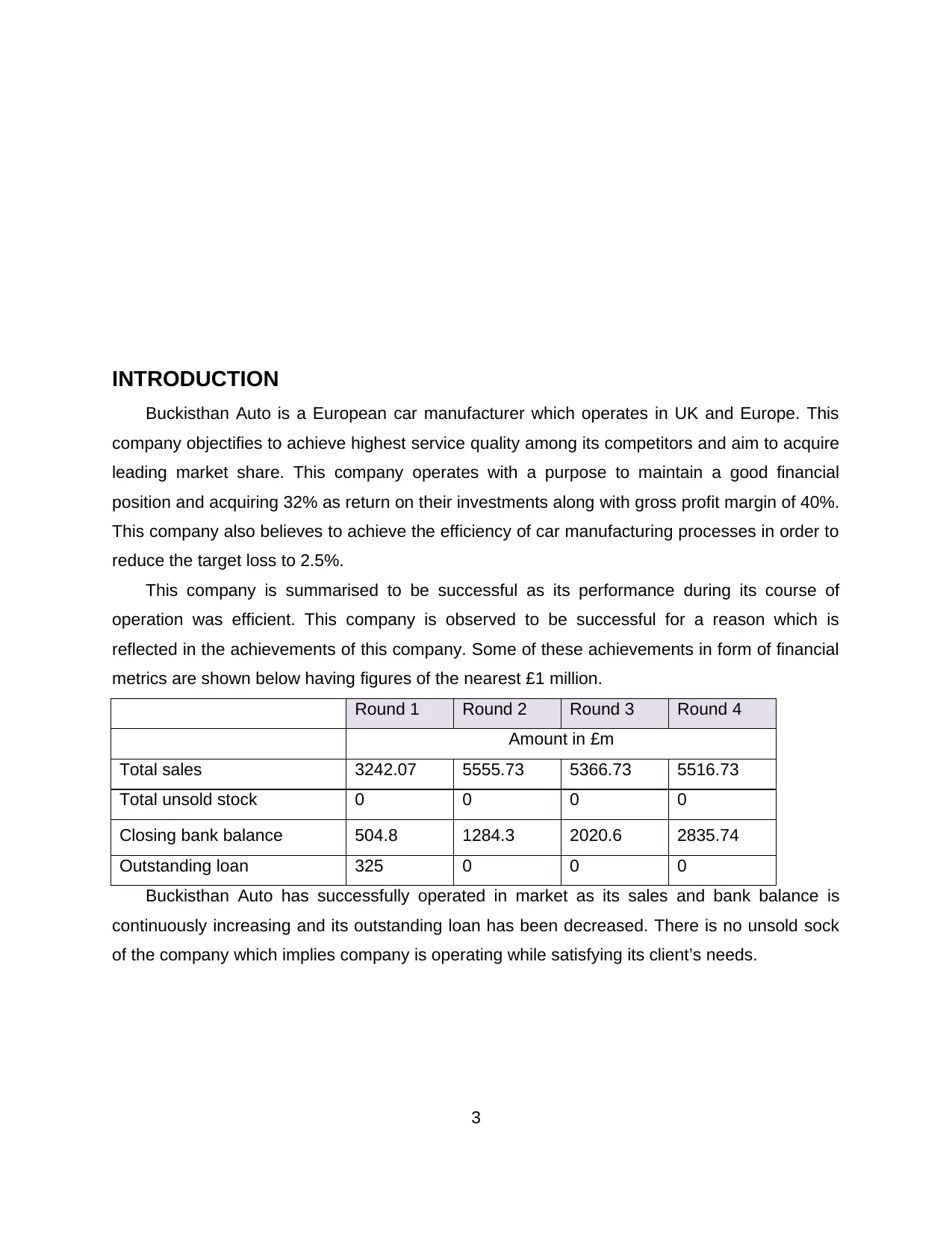

INTRODUCTION

Buckisthan Auto is a European car manufacturer which operates in UK and Europe. This

company objectifies to achieve highest service quality among its competitors and aim to acquire

leading market share. This company operates with a purpose to maintain a good financial

position and acquiring 32% as return on their investments along with gross profit margin of 40%.

This company also believes to achieve the efficiency of car manufacturing processes in order to

reduce the target loss to 2.5%.

This company is summarised to be successful as its performance during its course of

operation was efficient. This company is observed to be successful for a reason which is

reflected in the achievements of this company. Some of these achievements in form of financial

metrics are shown below having figures of the nearest £1 million.

Round 1 Round 2 Round 3 Round 4

Amount in £m

Total sales 3242.07 5555.73 5366.73 5516.73

Total unsold stock 0 0 0 0

Closing bank balance 504.8 1284.3 2020.6 2835.74

Outstanding loan 325 0 0 0

Buckisthan Auto has successfully operated in market as its sales and bank balance is

continuously increasing and its outstanding loan has been decreased. There is no unsold sock

of the company which implies company is operating while satisfying its client’s needs.

3

Buckisthan Auto is a European car manufacturer which operates in UK and Europe. This

company objectifies to achieve highest service quality among its competitors and aim to acquire

leading market share. This company operates with a purpose to maintain a good financial

position and acquiring 32% as return on their investments along with gross profit margin of 40%.

This company also believes to achieve the efficiency of car manufacturing processes in order to

reduce the target loss to 2.5%.

This company is summarised to be successful as its performance during its course of

operation was efficient. This company is observed to be successful for a reason which is

reflected in the achievements of this company. Some of these achievements in form of financial

metrics are shown below having figures of the nearest £1 million.

Round 1 Round 2 Round 3 Round 4

Amount in £m

Total sales 3242.07 5555.73 5366.73 5516.73

Total unsold stock 0 0 0 0

Closing bank balance 504.8 1284.3 2020.6 2835.74

Outstanding loan 325 0 0 0

Buckisthan Auto has successfully operated in market as its sales and bank balance is

continuously increasing and its outstanding loan has been decreased. There is no unsold sock

of the company which implies company is operating while satisfying its client’s needs.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

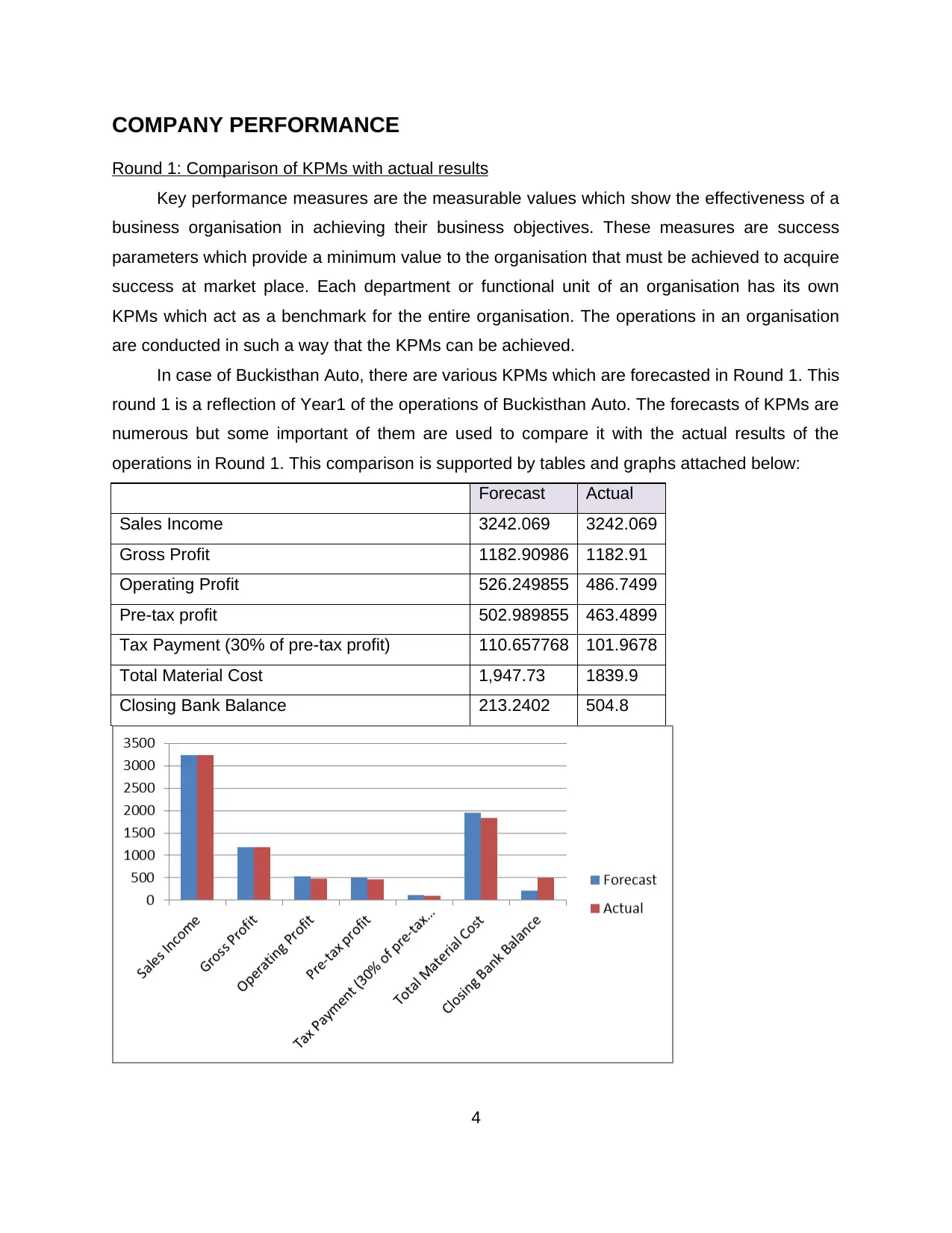

COMPANY PERFORMANCE

Round 1: Comparison of KPMs with actual results

Key performance measures are the measurable values which show the effectiveness of a

business organisation in achieving their business objectives. These measures are success

parameters which provide a minimum value to the organisation that must be achieved to acquire

success at market place. Each department or functional unit of an organisation has its own

KPMs which act as a benchmark for the entire organisation. The operations in an organisation

are conducted in such a way that the KPMs can be achieved.

In case of Buckisthan Auto, there are various KPMs which are forecasted in Round 1. This

round 1 is a reflection of Year1 of the operations of Buckisthan Auto. The forecasts of KPMs are

numerous but some important of them are used to compare it with the actual results of the

operations in Round 1. This comparison is supported by tables and graphs attached below:

Forecast Actual

Sales Income 3242.069 3242.069

Gross Profit 1182.90986 1182.91

Operating Profit 526.249855 486.7499

Pre-tax profit 502.989855 463.4899

Tax Payment (30% of pre-tax profit) 110.657768 101.9678

Total Material Cost 1,947.73 1839.9

Closing Bank Balance 213.2402 504.8

4

Round 1: Comparison of KPMs with actual results

Key performance measures are the measurable values which show the effectiveness of a

business organisation in achieving their business objectives. These measures are success

parameters which provide a minimum value to the organisation that must be achieved to acquire

success at market place. Each department or functional unit of an organisation has its own

KPMs which act as a benchmark for the entire organisation. The operations in an organisation

are conducted in such a way that the KPMs can be achieved.

In case of Buckisthan Auto, there are various KPMs which are forecasted in Round 1. This

round 1 is a reflection of Year1 of the operations of Buckisthan Auto. The forecasts of KPMs are

numerous but some important of them are used to compare it with the actual results of the

operations in Round 1. This comparison is supported by tables and graphs attached below:

Forecast Actual

Sales Income 3242.069 3242.069

Gross Profit 1182.90986 1182.91

Operating Profit 526.249855 486.7499

Pre-tax profit 502.989855 463.4899

Tax Payment (30% of pre-tax profit) 110.657768 101.9678

Total Material Cost 1,947.73 1839.9

Closing Bank Balance 213.2402 504.8

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above table is the representation of forecasted KPMs and actual results of the

operations of Buckisthan Auto in Round 1. The above analysis has only considered few KPMs

which are considered as important at our discretion in this Round. These KPMs are in some

cases similar to the actual results but in few cases these are different from the actual results as

well; this table is then represented using a bar graph which is providing a clear picture of the

differences between standard and actual results.

Sales income – The actual sales of Buckisthan Auto in Round 1 are similar to the KPM

which implies this company successfully operated in market and generated revenue which was

planned.

Gross Profit – Similar to sales, actual gross profit of this company for Round 1 is also

similar to their KPM. This similarity is the result of unchanged material and labour costs rate in

the market.

Operating Profit – This type of profit is the income which an organisation gains from

operating in the market. The forecasted operating income of this company is higher than its

actual, this situation implies that company was unable to earn what it suspected that it will earn.

This difference in KPM and actual value of operating income raises an issue that in future

company will unable to control its operating expenses specially fixed expenses. Due to this

difference, the pre taxation income of this company is also different.

Tax Payment (30% of pre-tax profit) – The tax which is paid by this company is different

from its forecasted taxation. This dissimilarity will result into the issue of uneven tax deductions.

Total Material Cost – Total material cost which is incurred by this company is lower than

what was forecasted. This implies that the company is not ordering adequate material which can

result in lower satisfaction of the clients.

The above analysis is a base or a rationale for Round 2 decisions; the differences in

actual and forecasted values provide yearly objectives for this company which will help in

controlling the position of this company.

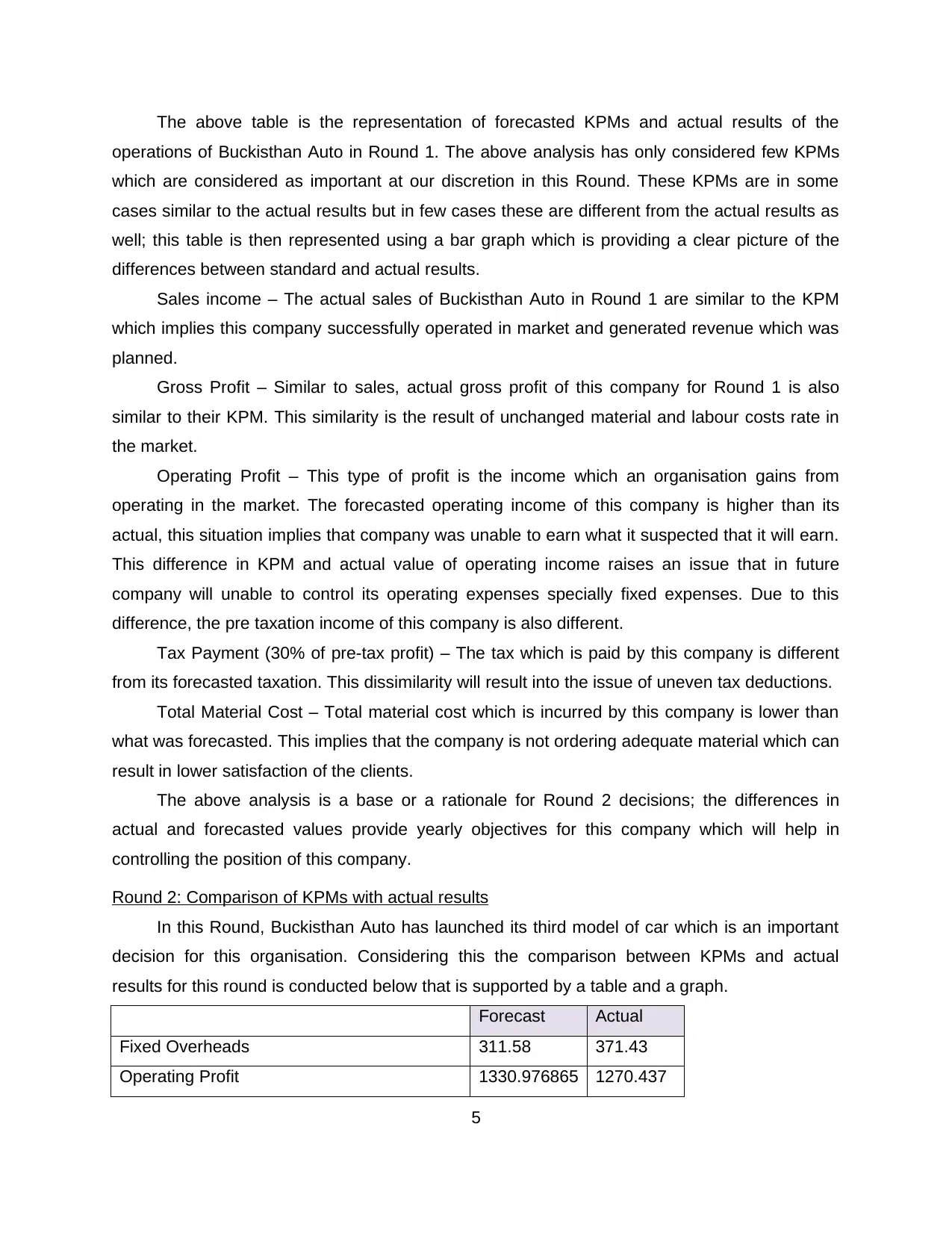

Round 2: Comparison of KPMs with actual results

In this Round, Buckisthan Auto has launched its third model of car which is an important

decision for this organisation. Considering this the comparison between KPMs and actual

results for this round is conducted below that is supported by a table and a graph.

Forecast Actual

Fixed Overheads 311.58 371.43

Operating Profit 1330.976865 1270.437

5

operations of Buckisthan Auto in Round 1. The above analysis has only considered few KPMs

which are considered as important at our discretion in this Round. These KPMs are in some

cases similar to the actual results but in few cases these are different from the actual results as

well; this table is then represented using a bar graph which is providing a clear picture of the

differences between standard and actual results.

Sales income – The actual sales of Buckisthan Auto in Round 1 are similar to the KPM

which implies this company successfully operated in market and generated revenue which was

planned.

Gross Profit – Similar to sales, actual gross profit of this company for Round 1 is also

similar to their KPM. This similarity is the result of unchanged material and labour costs rate in

the market.

Operating Profit – This type of profit is the income which an organisation gains from

operating in the market. The forecasted operating income of this company is higher than its

actual, this situation implies that company was unable to earn what it suspected that it will earn.

This difference in KPM and actual value of operating income raises an issue that in future

company will unable to control its operating expenses specially fixed expenses. Due to this

difference, the pre taxation income of this company is also different.

Tax Payment (30% of pre-tax profit) – The tax which is paid by this company is different

from its forecasted taxation. This dissimilarity will result into the issue of uneven tax deductions.

Total Material Cost – Total material cost which is incurred by this company is lower than

what was forecasted. This implies that the company is not ordering adequate material which can

result in lower satisfaction of the clients.

The above analysis is a base or a rationale for Round 2 decisions; the differences in

actual and forecasted values provide yearly objectives for this company which will help in

controlling the position of this company.

Round 2: Comparison of KPMs with actual results

In this Round, Buckisthan Auto has launched its third model of car which is an important

decision for this organisation. Considering this the comparison between KPMs and actual

results for this round is conducted below that is supported by a table and a graph.

Forecast Actual

Fixed Overheads 311.58 371.43

Operating Profit 1330.976865 1270.437

5

Net Interest Payment 0 -2.57

Post-tax profit 1038.161955 992.94546

Sales Income 5092.747917 5365.56

Total Labour Cost 102.375 103.06487

Closing Bank Balance 931.1967697 1284.2951

Fixed Overheads – These overheads are the expenses which Buckisthan Auto incurs

every year to manufacture their goods and operate effectively. These expenses are higher than

it was anticipated. This difference in KPM and actual result will raise an issue of lower

profitability and shareholder value of the company.

Operating Profit – As mentioned above, the operating profit which is earned by

Buckisthan Auto is not able to even cross its minimum value which was set in KPM. This

difference will result into the issue of low profit and the funds for next year will also decrease.

Net Interest Payment – Interest is the value which an organisation pays for the loan

acquired from them. Due to loan gained in Round 1, the interest amount of this round has been

increased. This interest has now been paid from profit of this company due to which post tax

profit of this is also reduced.

Sales Income – The sales income and closing bank balance of Buckisthan Auto in

Round 2 is higher than its KPM which is a good indicator. This difference will result in

opportunity of enhancing liquidity position of this company.

Total Labour Cost – Due to launching new model, the labour cost of this organisation has

been increased to an extend which was not even expected. This difference has been occur due

6

Post-tax profit 1038.161955 992.94546

Sales Income 5092.747917 5365.56

Total Labour Cost 102.375 103.06487

Closing Bank Balance 931.1967697 1284.2951

Fixed Overheads – These overheads are the expenses which Buckisthan Auto incurs

every year to manufacture their goods and operate effectively. These expenses are higher than

it was anticipated. This difference in KPM and actual result will raise an issue of lower

profitability and shareholder value of the company.

Operating Profit – As mentioned above, the operating profit which is earned by

Buckisthan Auto is not able to even cross its minimum value which was set in KPM. This

difference will result into the issue of low profit and the funds for next year will also decrease.

Net Interest Payment – Interest is the value which an organisation pays for the loan

acquired from them. Due to loan gained in Round 1, the interest amount of this round has been

increased. This interest has now been paid from profit of this company due to which post tax

profit of this is also reduced.

Sales Income – The sales income and closing bank balance of Buckisthan Auto in

Round 2 is higher than its KPM which is a good indicator. This difference will result in

opportunity of enhancing liquidity position of this company.

Total Labour Cost – Due to launching new model, the labour cost of this organisation has

been increased to an extend which was not even expected. This difference has been occur due

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to high labour costs that will result into the issue of higher cost of sales which will again reduce

the net profit and shareholder value.

The decisions which were made in this Round are the rationale for Round 3 decisions.

The points which will impact the Round 3 decisions are enhancing liquidity position, reducing

profitability and introduction of another car model with high labour rate.

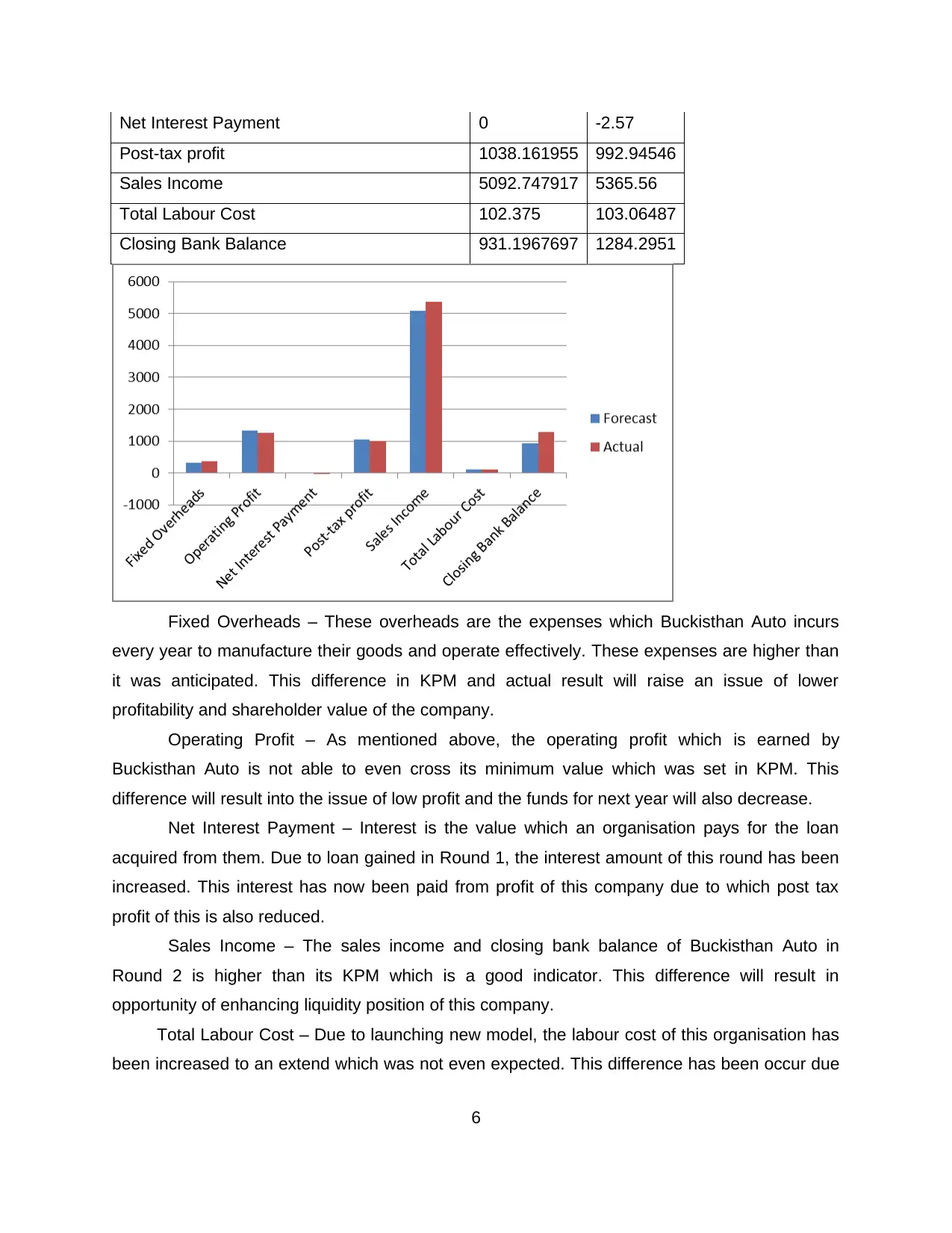

Round 3: Comparison of KPMs with actual results

In this round, Buckisthan Auto decided to continue their Automation investment as 50%

for model 2 even after experiencing high requirement in Round 2. Few kPMs are selected and

then compared with actual results by using table and graphical tools below:

Forecast Actual

Automation investment and allocation for

model 2 50% 60%

Units of Automation [A] for model 2 125 150

Fixed Overheads 309.58 363.31

Operating Profit 1132.14932 1077.68258

Post-tax profit 922.0764696 900.551012

Opening Bank Balance 324 1285.11

Sales Income 4919.50617 5308.75

Automation investment and allocation and Units of Automation - Buckisthan Auto

manufactures three models of cars and for each model they have allocated automation

investment and units of automation. For model 2 car, the automation investment was 60% in

7

the net profit and shareholder value.

The decisions which were made in this Round are the rationale for Round 3 decisions.

The points which will impact the Round 3 decisions are enhancing liquidity position, reducing

profitability and introduction of another car model with high labour rate.

Round 3: Comparison of KPMs with actual results

In this round, Buckisthan Auto decided to continue their Automation investment as 50%

for model 2 even after experiencing high requirement in Round 2. Few kPMs are selected and

then compared with actual results by using table and graphical tools below:

Forecast Actual

Automation investment and allocation for

model 2 50% 60%

Units of Automation [A] for model 2 125 150

Fixed Overheads 309.58 363.31

Operating Profit 1132.14932 1077.68258

Post-tax profit 922.0764696 900.551012

Opening Bank Balance 324 1285.11

Sales Income 4919.50617 5308.75

Automation investment and allocation and Units of Automation - Buckisthan Auto

manufactures three models of cars and for each model they have allocated automation

investment and units of automation. For model 2 car, the automation investment was 60% in

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Round 1, but after introduction of Model 3 car, this percentage reduced to 50%. Even after

facing the high requirement of automation investment for Model 2 in Round 2, decisions were

not changed in Round 3. This has resultant in 150 units of automation where these were

forecasted at 125. This unchanged decision has raised an issue of higher workforce

consumption and wages. This issue can even impact the production of other two car models.

Fixed Overheads – Like every other Round, this round as well fixed expense of the year

are increasing its minimum Key performance measure. The fixed expenses which were

predicted to be acquired are less than the expenses which are actually incurred. This difference

will not only result in decreasing profitability but will also impact the shareholder value of this

company.

Operating Profit and Post-tax profit – As discussed above, the fixed overheads are the

reason behind lower operating profit and post tax profit of this company. The company is

experiencing the situation where company set a minimum value of profit and company was

unable to acquire that minimum KPM as well. This difference in KPM and actual results will

imply the issue of low credibility of the company due to which company will not be able to

acquire loan easily in future.

Opening Bank Balance and Sales Income – The management of Buckisthan Auto has

successfully satisfied KPM of opening bank balance and sales income. This situation is not an

issue but an opportunity for this company as by higher sales income and bank balance,

company will not require loan in future and can also provide credit to their clients in order to

satisfy their needs.

The decisions taken in Round 3 were crucial as they were impacted by the two previous

rounds. The decision of maintaining high liquidity in company and not expanding the automation

investment are the rationale for Round 4 as by considering these only the decisions of next

round will be undertaken.

Round 4: Comparison of KPMs with actual results

In this year, Buckisthan Auto decided to increase their operational efficiency so that units

of their manufactured cars can be increased. This year decisions are most crucial and analysis

of these decisions has been conducted below supported by a bar graph and a comparison

table.

Forecast Actual

Material Cost 3818.51301 3814.95301

Gross Profit 1595.83899 1599.3989

8

facing the high requirement of automation investment for Model 2 in Round 2, decisions were

not changed in Round 3. This has resultant in 150 units of automation where these were

forecasted at 125. This unchanged decision has raised an issue of higher workforce

consumption and wages. This issue can even impact the production of other two car models.

Fixed Overheads – Like every other Round, this round as well fixed expense of the year

are increasing its minimum Key performance measure. The fixed expenses which were

predicted to be acquired are less than the expenses which are actually incurred. This difference

will not only result in decreasing profitability but will also impact the shareholder value of this

company.

Operating Profit and Post-tax profit – As discussed above, the fixed overheads are the

reason behind lower operating profit and post tax profit of this company. The company is

experiencing the situation where company set a minimum value of profit and company was

unable to acquire that minimum KPM as well. This difference in KPM and actual results will

imply the issue of low credibility of the company due to which company will not be able to

acquire loan easily in future.

Opening Bank Balance and Sales Income – The management of Buckisthan Auto has

successfully satisfied KPM of opening bank balance and sales income. This situation is not an

issue but an opportunity for this company as by higher sales income and bank balance,

company will not require loan in future and can also provide credit to their clients in order to

satisfy their needs.

The decisions taken in Round 3 were crucial as they were impacted by the two previous

rounds. The decision of maintaining high liquidity in company and not expanding the automation

investment are the rationale for Round 4 as by considering these only the decisions of next

round will be undertaken.

Round 4: Comparison of KPMs with actual results

In this year, Buckisthan Auto decided to increase their operational efficiency so that units

of their manufactured cars can be increased. This year decisions are most crucial and analysis

of these decisions has been conducted below supported by a bar graph and a comparison

table.

Forecast Actual

Material Cost 3818.51301 3814.95301

Gross Profit 1595.83899 1599.3989

8

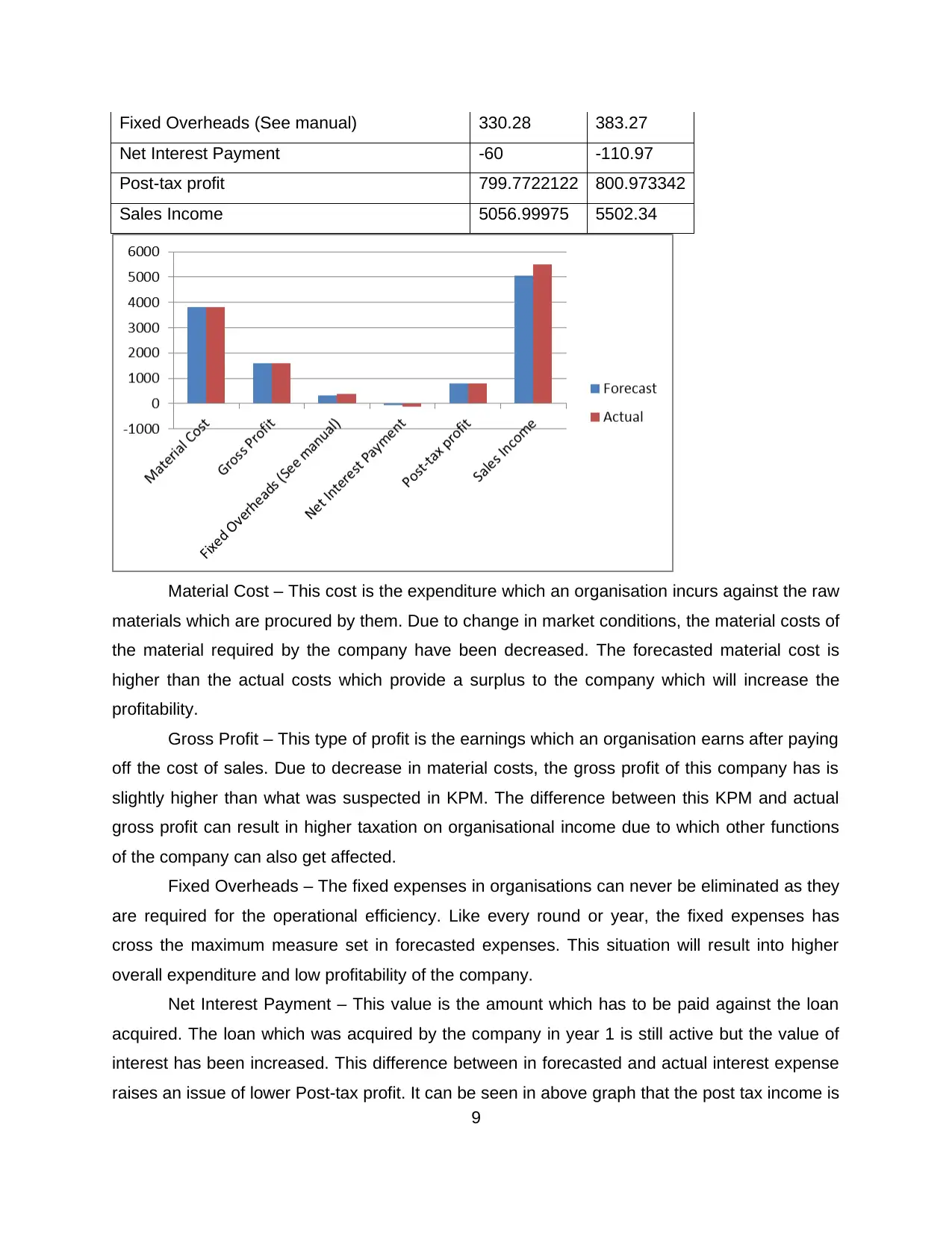

Fixed Overheads (See manual) 330.28 383.27

Net Interest Payment -60 -110.97

Post-tax profit 799.7722122 800.973342

Sales Income 5056.99975 5502.34

Material Cost – This cost is the expenditure which an organisation incurs against the raw

materials which are procured by them. Due to change in market conditions, the material costs of

the material required by the company have been decreased. The forecasted material cost is

higher than the actual costs which provide a surplus to the company which will increase the

profitability.

Gross Profit – This type of profit is the earnings which an organisation earns after paying

off the cost of sales. Due to decrease in material costs, the gross profit of this company has is

slightly higher than what was suspected in KPM. The difference between this KPM and actual

gross profit can result in higher taxation on organisational income due to which other functions

of the company can also get affected.

Fixed Overheads – The fixed expenses in organisations can never be eliminated as they

are required for the operational efficiency. Like every round or year, the fixed expenses has

cross the maximum measure set in forecasted expenses. This situation will result into higher

overall expenditure and low profitability of the company.

Net Interest Payment – This value is the amount which has to be paid against the loan

acquired. The loan which was acquired by the company in year 1 is still active but the value of

interest has been increased. This difference between in forecasted and actual interest expense

raises an issue of lower Post-tax profit. It can be seen in above graph that the post tax income is

9

Net Interest Payment -60 -110.97

Post-tax profit 799.7722122 800.973342

Sales Income 5056.99975 5502.34

Material Cost – This cost is the expenditure which an organisation incurs against the raw

materials which are procured by them. Due to change in market conditions, the material costs of

the material required by the company have been decreased. The forecasted material cost is

higher than the actual costs which provide a surplus to the company which will increase the

profitability.

Gross Profit – This type of profit is the earnings which an organisation earns after paying

off the cost of sales. Due to decrease in material costs, the gross profit of this company has is

slightly higher than what was suspected in KPM. The difference between this KPM and actual

gross profit can result in higher taxation on organisational income due to which other functions

of the company can also get affected.

Fixed Overheads – The fixed expenses in organisations can never be eliminated as they

are required for the operational efficiency. Like every round or year, the fixed expenses has

cross the maximum measure set in forecasted expenses. This situation will result into higher

overall expenditure and low profitability of the company.

Net Interest Payment – This value is the amount which has to be paid against the loan

acquired. The loan which was acquired by the company in year 1 is still active but the value of

interest has been increased. This difference between in forecasted and actual interest expense

raises an issue of lower Post-tax profit. It can be seen in above graph that the post tax income is

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

slightly higher than it was predicted even after increase in fixed and interest expense. This

slightly higher profit is the result of low material costs.

All the decisions taken in this year are the base for performance indicators for next few

years.

Trends in KPMs

KPMs or the Key performance measures which are set for Buckisthan Auto are observed

effectively and are showing few trends and patterns. These trends are identified below:

The sales KPM are revised every year due to which in every round the value of

forecasted sales is different. The KPM for sales is set effectively by analysing each and

every aspect of the business due to which in every round the actual sales is exactly

similar to predicted sales.

Even after knowing the required automation investment percentage for model 2 car, the

automation percentage has been decreased. This trend was the result of high availability

of investment for automation which could have been used in case of any adverse

condition.

The loan amount was only requested in first year of the operation so that viable

monetary funds can be procured and the operations can be conducted effectively in

consequent years.

The pattern of KPM of bank balance of was to increase it gradually so that liquidity

position of the company could have been enhanced.

The KPM of material and labour cost was set by analysing the current cost of material

and labour in market. This KPM ignored all other market forces due to which actual

material and labour costs were higher in few rounds than the predicted costs.

LEARNING

There are certain functions in organisations which are controlled by making effective and

responsible decisions. These functions are financial, marketing, operations and human

resources.

Financial

Finance department is a functional unit which manages the flow of money in an

organisation. The functions or activities of this department include preparation of financial

reports, internal auditing, accounting and many more. As the financial director of this company,

few decisions are made which include minimising the unnecessary costs and achieve the lowest

10

slightly higher profit is the result of low material costs.

All the decisions taken in this year are the base for performance indicators for next few

years.

Trends in KPMs

KPMs or the Key performance measures which are set for Buckisthan Auto are observed

effectively and are showing few trends and patterns. These trends are identified below:

The sales KPM are revised every year due to which in every round the value of

forecasted sales is different. The KPM for sales is set effectively by analysing each and

every aspect of the business due to which in every round the actual sales is exactly

similar to predicted sales.

Even after knowing the required automation investment percentage for model 2 car, the

automation percentage has been decreased. This trend was the result of high availability

of investment for automation which could have been used in case of any adverse

condition.

The loan amount was only requested in first year of the operation so that viable

monetary funds can be procured and the operations can be conducted effectively in

consequent years.

The pattern of KPM of bank balance of was to increase it gradually so that liquidity

position of the company could have been enhanced.

The KPM of material and labour cost was set by analysing the current cost of material

and labour in market. This KPM ignored all other market forces due to which actual

material and labour costs were higher in few rounds than the predicted costs.

LEARNING

There are certain functions in organisations which are controlled by making effective and

responsible decisions. These functions are financial, marketing, operations and human

resources.

Financial

Finance department is a functional unit which manages the flow of money in an

organisation. The functions or activities of this department include preparation of financial

reports, internal auditing, accounting and many more. As the financial director of this company,

few decisions are made which include minimising the unnecessary costs and achieve the lowest

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

excess of inventory. There were few more financial decisions as well which were undertaken.

These decisions included eliminating cash shortage and fixing the pricing strategy for each

model of car.

The 4 decision which are stated and analysed below could have been taken more

effectively if all the financial concepts that were taught were applied thoroughly in all the rounds.

The first financial decision was to eliminate the unnecessary variable costs but due to this

decision fixed costs were higher than the predicted costs in every round. This decision could

have been made better if the financial concept of balance of payments was used (Cuervo‐

Cazurra, 2011); this decision impacted internal stakeholder group of employees as their wages

are also a part of fixed costs. If this concept was considered then it would be known that

eliminating one expense will result in increment of another expense. Second decision was to

eliminate the excess of inventory but due to this, excess of inventory in every year (round) was

0. This 0 inventory at the end of every year also presents the lack of material. This decision

could also been made better if the inventory control strategies of FIFO and LIFO were used

(Haddock-Millar and Rigby, 2015). By using FIFO method, first purchased units would have

been used first and if any excess would have been result then it could be waved off easily (De

Jonge, 2011). This decision impacted the external stakeholder group of suppliers.

The third and fourth decisions were to maintain adequate cash balance and fixating the

pricing strategy. This decision resulted into high liquidity of the company but also stresses the

financial position of this company. If the concept of solvency was used along with liquidity then

this decision would have been made better (Harrison, 2013).

Operations

Buckisthan Auto is a European car manufacturing company and manufacturing car

models are the operations of this company. There are total of four important operational

decisions which were taken by the company which could have been taken more effectively if

material concepts were considered. The first out of these decisions is to use JIT as an

operational management strategy in order to minimise the set up costs. This decision could

have been better if the concept of TQM was considered as by considering this strategy the set

up costs would have been lower along with acquiring quality products (Ivanov, Tsipoulanidis and

Schönberger, 2017). This decision has impacted the internal stakeholder group of board of

director as their developed strategies will be questioned by shareholders.

Another decision made against operational functions of this company is to prioritising

quantity over quality. The car models of this company have various features but some of these

11

These decisions included eliminating cash shortage and fixing the pricing strategy for each

model of car.

The 4 decision which are stated and analysed below could have been taken more

effectively if all the financial concepts that were taught were applied thoroughly in all the rounds.

The first financial decision was to eliminate the unnecessary variable costs but due to this

decision fixed costs were higher than the predicted costs in every round. This decision could

have been made better if the financial concept of balance of payments was used (Cuervo‐

Cazurra, 2011); this decision impacted internal stakeholder group of employees as their wages

are also a part of fixed costs. If this concept was considered then it would be known that

eliminating one expense will result in increment of another expense. Second decision was to

eliminate the excess of inventory but due to this, excess of inventory in every year (round) was

0. This 0 inventory at the end of every year also presents the lack of material. This decision

could also been made better if the inventory control strategies of FIFO and LIFO were used

(Haddock-Millar and Rigby, 2015). By using FIFO method, first purchased units would have

been used first and if any excess would have been result then it could be waved off easily (De

Jonge, 2011). This decision impacted the external stakeholder group of suppliers.

The third and fourth decisions were to maintain adequate cash balance and fixating the

pricing strategy. This decision resulted into high liquidity of the company but also stresses the

financial position of this company. If the concept of solvency was used along with liquidity then

this decision would have been made better (Harrison, 2013).

Operations

Buckisthan Auto is a European car manufacturing company and manufacturing car

models are the operations of this company. There are total of four important operational

decisions which were taken by the company which could have been taken more effectively if

material concepts were considered. The first out of these decisions is to use JIT as an

operational management strategy in order to minimise the set up costs. This decision could

have been better if the concept of TQM was considered as by considering this strategy the set

up costs would have been lower along with acquiring quality products (Ivanov, Tsipoulanidis and

Schönberger, 2017). This decision has impacted the internal stakeholder group of board of

director as their developed strategies will be questioned by shareholders.

Another decision made against operational functions of this company is to prioritising

quantity over quality. The car models of this company have various features but some of these

11

features may lack in quality. This decision would have been made better if concept of quality

management was considered while making this decision (Krajewski, Ritzman and Malhotra,

2013). The third decision made by this company was to launch their third model car in round 2.

This decision resulted in higher labour costs, this decision could have been made better if the

concept of process management was considered. By considering this concept, the third model

car could have been launched after few years as by then company would have gain viable

experience and brand image in market.

The last and fourth decision made for operations of this company was to prioritising the

model 2 car the most. This decision could have been better if the concept of lean production

was considered (Larson and Gray, 2013). Due to prioritising the 2nd model car, the sales of other

two models was low, in future this can even result in low sales of entire organisation. This

decision has impacted the external stakeholder group of investors.

Marketing

Marketing is an activity that focuses over presenting the goods and services prospective

organization into the market in the most efficient way to provide information to the targeted

audience about the offerings of the organization which are established according to the needs

and preferences of people. Marketing is became a very important and essential function of a

company as it includes activities related to buying, selling, transportation, storage,

standardization and grading financial risk along with circulating marketing market information.

Buckisthan Auto was initially dealing in manufacturing auto but which changing market condition

and decreasing demand of auto rickshaw now the company showcase is over developing

quality car according to the demand of the market (Lasserre, 2017). The marketing activity is

very important for organization in order to develop awareness in the public about their new

offerings. Buckisthan is initially focusing and introduce into models to their respective customers

that are a compact City cars and a medium size car. Marketing strategy is developed with to

appropriate models that is the STP model and the marketing mix model. The in segment and

targeted audience of Buckisthan for there to car models are youngsters who have recently

started their careers and not have enough cash to invest in cars and water luxury motor vehicle.

The first model that is s hundred is perfectly suitable for individuals under the age of 25 as they

are just beginning their careers. The second model is focusing and targeting towards individuals

is grouping belonging to 25 to 40 years as majority of these people are settled in their lives and

have family.

12

management was considered while making this decision (Krajewski, Ritzman and Malhotra,

2013). The third decision made by this company was to launch their third model car in round 2.

This decision resulted in higher labour costs, this decision could have been made better if the

concept of process management was considered. By considering this concept, the third model

car could have been launched after few years as by then company would have gain viable

experience and brand image in market.

The last and fourth decision made for operations of this company was to prioritising the

model 2 car the most. This decision could have been better if the concept of lean production

was considered (Larson and Gray, 2013). Due to prioritising the 2nd model car, the sales of other

two models was low, in future this can even result in low sales of entire organisation. This

decision has impacted the external stakeholder group of investors.

Marketing

Marketing is an activity that focuses over presenting the goods and services prospective

organization into the market in the most efficient way to provide information to the targeted

audience about the offerings of the organization which are established according to the needs

and preferences of people. Marketing is became a very important and essential function of a

company as it includes activities related to buying, selling, transportation, storage,

standardization and grading financial risk along with circulating marketing market information.

Buckisthan Auto was initially dealing in manufacturing auto but which changing market condition

and decreasing demand of auto rickshaw now the company showcase is over developing

quality car according to the demand of the market (Lasserre, 2017). The marketing activity is

very important for organization in order to develop awareness in the public about their new

offerings. Buckisthan is initially focusing and introduce into models to their respective customers

that are a compact City cars and a medium size car. Marketing strategy is developed with to

appropriate models that is the STP model and the marketing mix model. The in segment and

targeted audience of Buckisthan for there to car models are youngsters who have recently

started their careers and not have enough cash to invest in cars and water luxury motor vehicle.

The first model that is s hundred is perfectly suitable for individuals under the age of 25 as they

are just beginning their careers. The second model is focusing and targeting towards individuals

is grouping belonging to 25 to 40 years as majority of these people are settled in their lives and

have family.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.