Holmes Institute - HI5019: Case Study of Paradise Industry Analysis

VerifiedAdded on 2023/01/11

|14

|2841

|86

Case Study

AI Summary

This case study analyzes Paradise Industry, focusing on the expenditure and cash conversion cycles. The report begins with an introduction to these concepts, followed by a detailed examination of the system flow chart of expenditure, highlighting internal control weaknesses within the purchasing and receiving departments. The analysis covers structural weaknesses, documentation issues, and organizational control deficiencies, proposing internal control suggestions for both the revenue and expenditure cycle frameworks. The study then explores the cash conversion cycle, presenting a system flow chart and analyzing various risks involved, such as payment delays, liquidity decline, and inventory issues. The report concludes with recommendations for risk management, emphasizing the importance of simplifying inventory, increasing the buying cycle, and improving the order-to-money cycle to mitigate potential risks within the organization. The document offers valuable insights into financial systems and risk management.

Case study- Paradise Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

Conclusion.................................................................................................................................................12

REFERENCES..........................................................................................................................................13

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

Conclusion.................................................................................................................................................12

REFERENCES..........................................................................................................................................13

INTRODUCTION

The report is based on two concepts: the spending cycle and the cash conversion cycle.

The graph demonstrates how and when the documents are posted, how many copies need to be

produced for distribution, and how the research under way is managed (Phillips, 2018). Faults

also are discussed and recommendations were provided for the proposed selection phase. The

other word, that is the cash conversion period, refers to the time, the possibility and also to the

entire process.

MAIN BODY

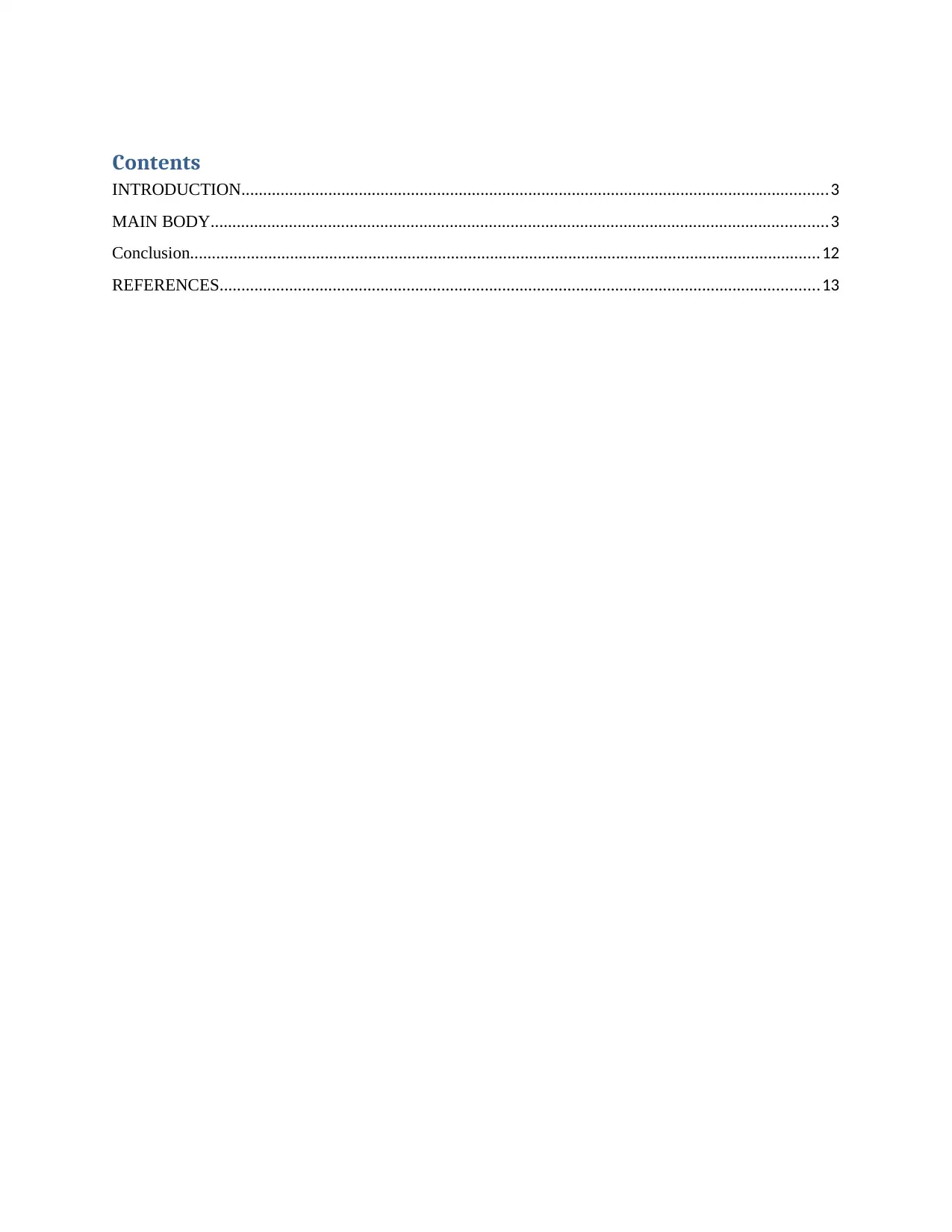

1. System flow chart of expenditure cycle

The report is based on two concepts: the spending cycle and the cash conversion cycle.

The graph demonstrates how and when the documents are posted, how many copies need to be

produced for distribution, and how the research under way is managed (Phillips, 2018). Faults

also are discussed and recommendations were provided for the proposed selection phase. The

other word, that is the cash conversion period, refers to the time, the possibility and also to the

entire process.

MAIN BODY

1. System flow chart of expenditure cycle

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

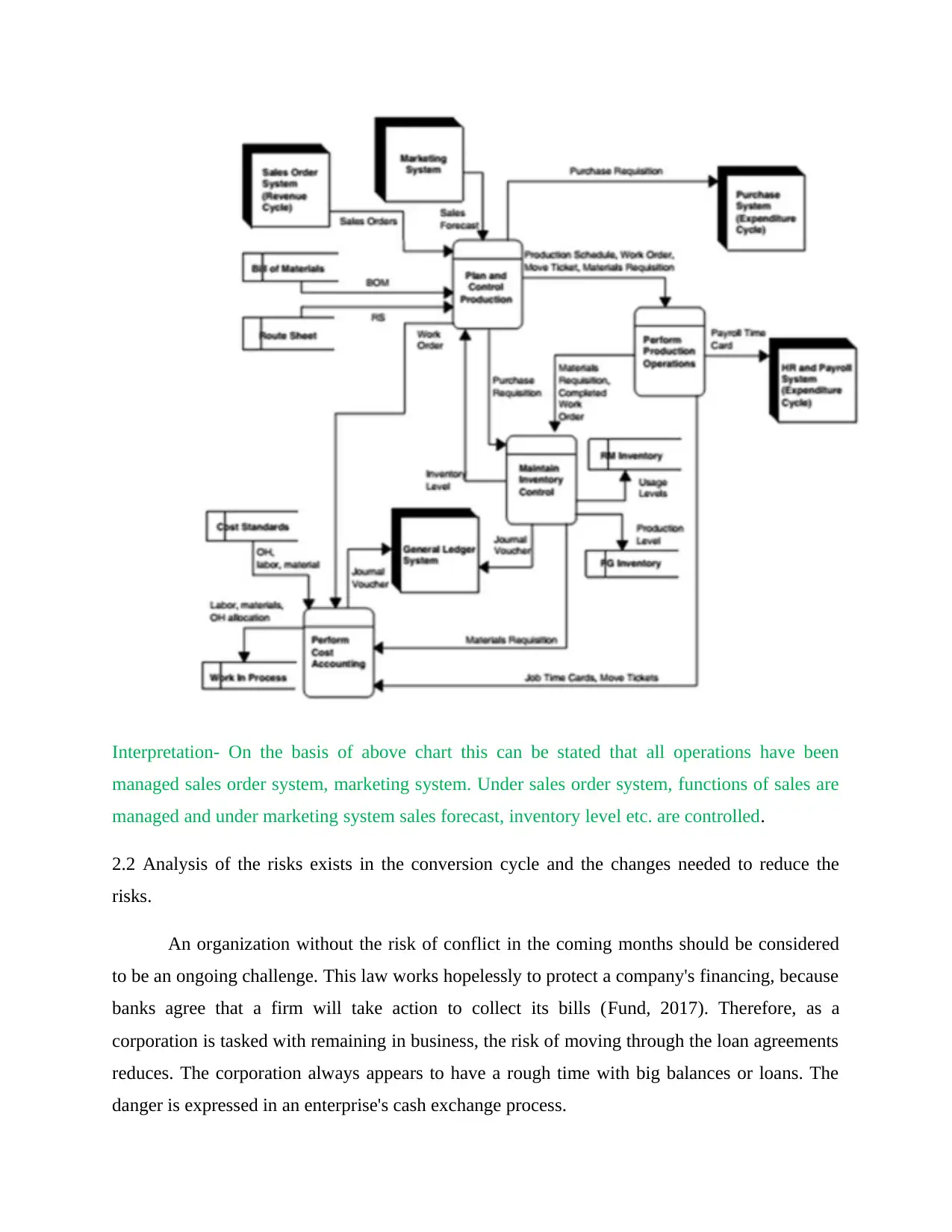

Analysis- the system flow chart of expenditure indicates that under this chart, there are

two departments purchasing and receiving department. In the receiving department, all types

of inventory functions are managed such as warehouses, computer inventory system etc.

while purchasing department all types of buying activities are included.

1.1 Analysis of physical internal control weaknesses in the expenditure cycle

1. Possible weaknesses Structural weaknesses

The income cycle system: Most RC activities are carried out the over-charged by the investment

advisor (AC), in particular the RC, transactions and processes. The consumer's request is

received and acknowledged, generates files for RC sources, like slips and tender packing, but

also retains the particular stock and receipts for the cash deposits. False intentions can happen

right here. The CA may be inaccurate with the purchaser of the product lines and may

misinterpret the user. The customer may still have more cost, but he keeps track of and assures

about the sale at the very same price.

Expenditure cycle system- In one division, the Group combines identification, approval and care;

distribution, sourcing and stock management (R, P & IC). It is an violation of the division of

responsibilities (Banerjee, 2018). Most EC operations are carried out by R, P and IC in certain

organizational responsibilities, in particular EC, transactions or procedures. This makes

payments, collects structured refunds, evaluates and maintains inventories, and provides a

statistical repository on accounts payable. False behavior could happen here. For example, R, P

and IC staff may have conflicting positions on the seller and may annoy the president / owner;

they may even take unkempt soup (except hard food) and no one will take charge of it.

2. Weaknesses of documentation and commercial actions (methods)

The identification and economic operations of giant eggplants can be at risk throughout

the purchasing cycle:

two departments purchasing and receiving department. In the receiving department, all types

of inventory functions are managed such as warehouses, computer inventory system etc.

while purchasing department all types of buying activities are included.

1.1 Analysis of physical internal control weaknesses in the expenditure cycle

1. Possible weaknesses Structural weaknesses

The income cycle system: Most RC activities are carried out the over-charged by the investment

advisor (AC), in particular the RC, transactions and processes. The consumer's request is

received and acknowledged, generates files for RC sources, like slips and tender packing, but

also retains the particular stock and receipts for the cash deposits. False intentions can happen

right here. The CA may be inaccurate with the purchaser of the product lines and may

misinterpret the user. The customer may still have more cost, but he keeps track of and assures

about the sale at the very same price.

Expenditure cycle system- In one division, the Group combines identification, approval and care;

distribution, sourcing and stock management (R, P & IC). It is an violation of the division of

responsibilities (Banerjee, 2018). Most EC operations are carried out by R, P and IC in certain

organizational responsibilities, in particular EC, transactions or procedures. This makes

payments, collects structured refunds, evaluates and maintains inventories, and provides a

statistical repository on accounts payable. False behavior could happen here. For example, R, P

and IC staff may have conflicting positions on the seller and may annoy the president / owner;

they may even take unkempt soup (except hard food) and no one will take charge of it.

2. Weaknesses of documentation and commercial actions (methods)

The identification and economic operations of giant eggplants can be at risk throughout

the purchasing cycle:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Successful figures in the CE files, for example, do not interfere with the number of records.

The creation and differentiation of performance / reporting may be difficult, particularly when

the business is beginning to implement a new accounting method.

• The Accountant directly promotes the plan by evaluating the client's financial background

(company management framework or consumer accounting source) during the contract

negotiation process. It seems like the consumer has not yet done a ton of work to the product.

Internal control weaknesses (IC)

The possible shortcomings of the general control of the body's RC structure are:

Organizational Controls

Accounts of staff; a wide range of tasks, like expenditure, revenue account holders,

substantial inventory and learn better, may be exempted (Tanvejsilp, Dushoff and Xie,

2018). This can activate the inconsistency of the AC-client. In addition, the President /

Owner will not assess the currency findings.

Documentation checks

The RC documents are not complete:

Description several duplicates of the sales order (CO) documents are required as one is

not sufficient. If the accounting firm actually sends CO information on the line, it appears

that the marketing director may insert incorrect data that may make a significant

contribution to incredulity.

There is no straightforward CO for telephone calls collected in the customer and the

publicized Order of acknowledgement (OA) and that there is no high strength or lack of

facts in the return.

Resource responsibility checks

The creation and differentiation of performance / reporting may be difficult, particularly when

the business is beginning to implement a new accounting method.

• The Accountant directly promotes the plan by evaluating the client's financial background

(company management framework or consumer accounting source) during the contract

negotiation process. It seems like the consumer has not yet done a ton of work to the product.

Internal control weaknesses (IC)

The possible shortcomings of the general control of the body's RC structure are:

Organizational Controls

Accounts of staff; a wide range of tasks, like expenditure, revenue account holders,

substantial inventory and learn better, may be exempted (Tanvejsilp, Dushoff and Xie,

2018). This can activate the inconsistency of the AC-client. In addition, the President /

Owner will not assess the currency findings.

Documentation checks

The RC documents are not complete:

Description several duplicates of the sales order (CO) documents are required as one is

not sufficient. If the accounting firm actually sends CO information on the line, it appears

that the marketing director may insert incorrect data that may make a significant

contribution to incredulity.

There is no straightforward CO for telephone calls collected in the customer and the

publicized Order of acknowledgement (OA) and that there is no high strength or lack of

facts in the return.

Resource responsibility checks

The workers assert that goods from the growth of storage facilities be coordinated by

transporting to make sure, at least even when they're not verified, that the oral request by

the AC or the president or owner, that the shipping staff members (report) are recognized

at the time of listing. This is problematic because it will achieve results, but there is no

evidence left.

Executives exercise controls

No marketing goals have been formed for the RC, such as credit authorization, account

liberties, agreements and collection procedure; this can cause discomfort as the group

keeps developing and utilizes the most staff to control the RC workouts (Lecue and Wu,

2017). RC processes may be enacted under conditions of ambiguity and inconsistency

due to a lack of manufacturing processes. In addition, it is difficult for an institution to

start preparing for its replacement when the accounting firm leaves.

The possible shortcomings of the general control of the body's EC framework are:

Organizational Controls

There are many responsibilities for staff involved in the invoice, buy and tracking of an

account, such as inventory control, credit debt obligations and information management. The

employees of R, P and IC finish most of the CE modules. This may make a contribution to an

immoral role.

Document checks

CE documents are not complete as there are no adequate documents of:

Represent the purchase basic assumption that the device setup is not allowed.

Rendered an order for reimbursement, which does not imply a formal exchange officer.

Upon receipt of the reassessment paper. This is critical for stock exchanges and

additional analysis.

transporting to make sure, at least even when they're not verified, that the oral request by

the AC or the president or owner, that the shipping staff members (report) are recognized

at the time of listing. This is problematic because it will achieve results, but there is no

evidence left.

Executives exercise controls

No marketing goals have been formed for the RC, such as credit authorization, account

liberties, agreements and collection procedure; this can cause discomfort as the group

keeps developing and utilizes the most staff to control the RC workouts (Lecue and Wu,

2017). RC processes may be enacted under conditions of ambiguity and inconsistency

due to a lack of manufacturing processes. In addition, it is difficult for an institution to

start preparing for its replacement when the accounting firm leaves.

The possible shortcomings of the general control of the body's EC framework are:

Organizational Controls

There are many responsibilities for staff involved in the invoice, buy and tracking of an

account, such as inventory control, credit debt obligations and information management. The

employees of R, P and IC finish most of the CE modules. This may make a contribution to an

immoral role.

Document checks

CE documents are not complete as there are no adequate documents of:

Represent the purchase basic assumption that the device setup is not allowed.

Rendered an order for reimbursement, which does not imply a formal exchange officer.

Upon receipt of the reassessment paper. This is critical for stock exchanges and

additional analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal controls suggested

For the RC framework:

Complex business frameworks, namely credit agreements, account privileges and sharing

and programs written should be established for RC.

The procedures and practices for mediation and receipt should be carried out in

compliance with (willingly established).

Exchange correspondence such as percent return papers and compensation papers shall

be published annually for the external inquiry and the audit process.

CE Framework:

The method of purchasing and managing cash should be established for purchase limits,

returns on buying and method of purchases (Sturny, 2019).

The procurement strategies should be tested with cash transfer and negotiation

agreements (in the case of negotiations).

The Mobile Account Checks, Breaches and Complaints review by managers periodically.

Assistance should be regulated to deter retail theft and avoid staffing, such as unusual

incidents in retail. The rules for internal controls conform to COSO monitoring and audit

capabilities of the internal control program.

System flow chart of conversion cycle

Flow chart of cash conversion cycle- This can be described as a type of chart consisting

of detailed details on activities linked to the conversion of current assets to cash. Below is a flow

chart showing the importance of every time for the turn of the current assets into cash:

For the RC framework:

Complex business frameworks, namely credit agreements, account privileges and sharing

and programs written should be established for RC.

The procedures and practices for mediation and receipt should be carried out in

compliance with (willingly established).

Exchange correspondence such as percent return papers and compensation papers shall

be published annually for the external inquiry and the audit process.

CE Framework:

The method of purchasing and managing cash should be established for purchase limits,

returns on buying and method of purchases (Sturny, 2019).

The procurement strategies should be tested with cash transfer and negotiation

agreements (in the case of negotiations).

The Mobile Account Checks, Breaches and Complaints review by managers periodically.

Assistance should be regulated to deter retail theft and avoid staffing, such as unusual

incidents in retail. The rules for internal controls conform to COSO monitoring and audit

capabilities of the internal control program.

System flow chart of conversion cycle

Flow chart of cash conversion cycle- This can be described as a type of chart consisting

of detailed details on activities linked to the conversion of current assets to cash. Below is a flow

chart showing the importance of every time for the turn of the current assets into cash:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- On the basis of above chart this can be stated that all operations have been

managed sales order system, marketing system. Under sales order system, functions of sales are

managed and under marketing system sales forecast, inventory level etc. are controlled.

2.2 Analysis of the risks exists in the conversion cycle and the changes needed to reduce the

risks.

An organization without the risk of conflict in the coming months should be considered

to be an ongoing challenge. This law works hopelessly to protect a company's financing, because

banks agree that a firm will take action to collect its bills (Fund, 2017). Therefore, as a

corporation is tasked with remaining in business, the risk of moving through the loan agreements

reduces. The corporation always appears to have a rough time with big balances or loans. The

danger is expressed in an enterprise's cash exchange process.

managed sales order system, marketing system. Under sales order system, functions of sales are

managed and under marketing system sales forecast, inventory level etc. are controlled.

2.2 Analysis of the risks exists in the conversion cycle and the changes needed to reduce the

risks.

An organization without the risk of conflict in the coming months should be considered

to be an ongoing challenge. This law works hopelessly to protect a company's financing, because

banks agree that a firm will take action to collect its bills (Fund, 2017). Therefore, as a

corporation is tasked with remaining in business, the risk of moving through the loan agreements

reduces. The corporation always appears to have a rough time with big balances or loans. The

danger is expressed in an enterprise's cash exchange process.

Types of risks involved in cash conversion cycle:

1. Delay in Payment- If longer customers invest and AR also increases dramatically, the real

issue begins. The toughest solution is potentially that the corporation covers the banks' shortfall.

This is risky since the present situation is not a corporation or a financial body but a resident

concern. Speaking to the business owner and maximizing the AP DO would be a wise phase in

the management of DO production. The consequence is a variety of businesses that raise capital

and operate solely to support their workers.

2. Decline in Liquidity- A wise estimation of community capital resources is important, because

lower fund balance raises the liquidity risk. Business experts and advisors contribute to

producing income and to having adequate capital to meet a company's normal needs, so

consumers agree whether an organization is typically willing to cover the acquisition supplies.

Liquidity is also a prerequisite for foreign regulators to determine commitments, for example

while addressing queries (Zou and Qian, 2018).

3. Void Invoices- Someone who intends to lead the manufacturer, the service provider and the

borrower can contact the company. Communicating by phone, by mail, by fax or by e-mail might

be required. The scammer wants the name of the bank Modified with the following receipts. The

scammer is actually running the expected new account.

4. Lack of inputs- Absence of running systems including production lines , for example linked

production methods.

5. Deficiency inventory- Anxious stock markets may cause problems, poor corporate forecasts

and misleading stocks, it should have limited production ferocity on a daily basis. A design

brand, for example, offers a 3-shaped model shoe. The reflections don't often sell one month

after the start of this season and will only be canceled for the next show.

6. Acutely sharpened- The essay generates greater competition than anticipated and becomes

sold out fast. When the transaction window is low, that can talk of missed sales. For examples, in

January a popular Christmas toy might cause a sensation.

1. Delay in Payment- If longer customers invest and AR also increases dramatically, the real

issue begins. The toughest solution is potentially that the corporation covers the banks' shortfall.

This is risky since the present situation is not a corporation or a financial body but a resident

concern. Speaking to the business owner and maximizing the AP DO would be a wise phase in

the management of DO production. The consequence is a variety of businesses that raise capital

and operate solely to support their workers.

2. Decline in Liquidity- A wise estimation of community capital resources is important, because

lower fund balance raises the liquidity risk. Business experts and advisors contribute to

producing income and to having adequate capital to meet a company's normal needs, so

consumers agree whether an organization is typically willing to cover the acquisition supplies.

Liquidity is also a prerequisite for foreign regulators to determine commitments, for example

while addressing queries (Zou and Qian, 2018).

3. Void Invoices- Someone who intends to lead the manufacturer, the service provider and the

borrower can contact the company. Communicating by phone, by mail, by fax or by e-mail might

be required. The scammer wants the name of the bank Modified with the following receipts. The

scammer is actually running the expected new account.

4. Lack of inputs- Absence of running systems including production lines , for example linked

production methods.

5. Deficiency inventory- Anxious stock markets may cause problems, poor corporate forecasts

and misleading stocks, it should have limited production ferocity on a daily basis. A design

brand, for example, offers a 3-shaped model shoe. The reflections don't often sell one month

after the start of this season and will only be canceled for the next show.

6. Acutely sharpened- The essay generates greater competition than anticipated and becomes

sold out fast. When the transaction window is low, that can talk of missed sales. For examples, in

January a popular Christmas toy might cause a sensation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7. A worthy loss- An object, component or material is on the rack every day and it's cheap to

find. Value may decline significantly due to other competing product inputs or indefinite

transport costs (Neyestani, 2017).

8. Natural hazards- Every day on the store there is an object, part or material that is

inexpensive. The value will decline easily, since it is difficult to measure certain rival inputs or

transportation costs.

9. Channel index- Stocks transferred to transportation services result in an unusual form of

inventory hazard. Backers often have the option of redeeming unsold bonds and growing profits

if they don't sell. In addition, inadequate inventory in a channel may damage financial activity if

users stop applying.

Changes needed to reduce the risks/ Risk management:

Focus on seeing the end-to-end supply chain:

The challenging aspect of adaptable chains is that the only impact they have is

manufacturer, organization and consumer exercises. This is when the condition of suppliers,

customers etc. is immediately ignored.

1. Simplify the inventory- One of the most convincing businesses of agile chain startups is

potentially to adjust inventory scale, while responding quickly and reducing resources (Hassan

and Mahinderjit-Singh, 2016). To charge shop and stock while still being sufficiently loaded to

satisfy the needs of customers, continue with the following methods:

Reducing the intergovernmental nature of the Plan section as a whole

Appropriately managing shipping times for the supplier

Appropriate collaboration processes (for example, JIT and VMI)

Limit thing’s redundant streams

Approximately boost the governance of tender process and subordination.

2. Increase the buying cycle- Flexible (and inevitable) risk-taking risks that present a significant

concern for payment suppliers. If they seek to expand time to half the sending of money (for

find. Value may decline significantly due to other competing product inputs or indefinite

transport costs (Neyestani, 2017).

8. Natural hazards- Every day on the store there is an object, part or material that is

inexpensive. The value will decline easily, since it is difficult to measure certain rival inputs or

transportation costs.

9. Channel index- Stocks transferred to transportation services result in an unusual form of

inventory hazard. Backers often have the option of redeeming unsold bonds and growing profits

if they don't sell. In addition, inadequate inventory in a channel may damage financial activity if

users stop applying.

Changes needed to reduce the risks/ Risk management:

Focus on seeing the end-to-end supply chain:

The challenging aspect of adaptable chains is that the only impact they have is

manufacturer, organization and consumer exercises. This is when the condition of suppliers,

customers etc. is immediately ignored.

1. Simplify the inventory- One of the most convincing businesses of agile chain startups is

potentially to adjust inventory scale, while responding quickly and reducing resources (Hassan

and Mahinderjit-Singh, 2016). To charge shop and stock while still being sufficiently loaded to

satisfy the needs of customers, continue with the following methods:

Reducing the intergovernmental nature of the Plan section as a whole

Appropriately managing shipping times for the supplier

Appropriate collaboration processes (for example, JIT and VMI)

Limit thing’s redundant streams

Approximately boost the governance of tender process and subordination.

2. Increase the buying cycle- Flexible (and inevitable) risk-taking risks that present a significant

concern for payment suppliers. If they seek to expand time to half the sending of money (for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

keeping it as available as expected) the impact on the income of remittance companies will be

capricious.

In every event, the amount of individuals in the pocket may be rearranged with the downside,

corporate experience and possible cap on the first betting. Find a role in these areas of the

multifaceted chain:

Applicable to monitor the sustainable development agreement in order to reduce iteration

quicker than the conditions stipulated.

No Ways of registering and getting paid workflow allowances.

LEAP Creation of a provider base to make the exchange of contracts more financially

viable.

3. Advance Order to Money Circle- the payment method is variable, based on the period,

dependency and accuracy (Bobade and Patil, 2016). In addition, some have adopted the tradition

of providing effective and productive treatment until the client plans pursue counseling for a

sport.

It is difficult to restrict this restriction to collection times while maintaining a fast , reliable

schedule and reliable volume of output. Attempt to split the process in certain specific areas and

see if the period will be shortened:

Send immediately (speed and accuracy) payment forms.

Active in pursuit of adaptive and fundamental inventions.

Benefit and the extent to which merchant accounts are given to the various customers

(Salman, and Hashim, 2016).

Conclusion

The described portion of the report concludes that documents of the company should be

updated so as to make better checks feasible and to increase the quality of customer contact. In

addition to the article, each flow chart allows organizations to make correct decisions. Efficient

distribution of duties within a business is often to be updated such that resentment and theft at

capricious.

In every event, the amount of individuals in the pocket may be rearranged with the downside,

corporate experience and possible cap on the first betting. Find a role in these areas of the

multifaceted chain:

Applicable to monitor the sustainable development agreement in order to reduce iteration

quicker than the conditions stipulated.

No Ways of registering and getting paid workflow allowances.

LEAP Creation of a provider base to make the exchange of contracts more financially

viable.

3. Advance Order to Money Circle- the payment method is variable, based on the period,

dependency and accuracy (Bobade and Patil, 2016). In addition, some have adopted the tradition

of providing effective and productive treatment until the client plans pursue counseling for a

sport.

It is difficult to restrict this restriction to collection times while maintaining a fast , reliable

schedule and reliable volume of output. Attempt to split the process in certain specific areas and

see if the period will be shortened:

Send immediately (speed and accuracy) payment forms.

Active in pursuit of adaptive and fundamental inventions.

Benefit and the extent to which merchant accounts are given to the various customers

(Salman, and Hashim, 2016).

Conclusion

The described portion of the report concludes that documents of the company should be

updated so as to make better checks feasible and to increase the quality of customer contact. In

addition to the article, each flow chart allows organizations to make correct decisions. Efficient

distribution of duties within a business is often to be updated such that resentment and theft at

work are avoided. Consequently, make specific recommendations that rely on the integrated

COSO control scheme of the author.

COSO control scheme of the author.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.