Strategic Corporate Finance Report: Axiata and Maxis Analysis

VerifiedAdded on 2023/06/11

|19

|4335

|127

Report

AI Summary

This report provides a strategic corporate finance analysis of Axiata Group Berhad and Maxis Berhad, two companies in the communication industry, focusing on a five-year performance review. Part A analyzes the companies' financial performance using various ratios, including liquidity, profitability, working capital, and capital structure ratios, to assess their financial health and efficiency. It also examines strategic investments and corporate governance practices. Part B delves into the calculation of the Weighted Average Cost of Capital (WACC) for J&J, Net Present Value (NPV) calculations, and explores different alternatives to cash dividends for returning value to shareholders, providing a comprehensive financial overview and strategic insights for decision-making.

Strategic Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Part A..............................................................................................................................................3

Analysing the performance of the companies on the basis of Ratios..........................................3

Strategic Investment....................................................................................................................7

Corporate Governance.................................................................................................................7

CONCLUSION................................................................................................................................8

Part B.............................................................................................................................................8

1. Calculating the Weighted Average Cost of Capital (WACC) for J & J..................................8

2. Calculating the net present value and recommendations.......................................................10

3. Explaining the four different alternatives to cash dividend as the way of returning value to

the shareholders.........................................................................................................................11

REFERENCES................................................................................................................................1

APPENDICES.................................................................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Part A..............................................................................................................................................3

Analysing the performance of the companies on the basis of Ratios..........................................3

Strategic Investment....................................................................................................................7

Corporate Governance.................................................................................................................7

CONCLUSION................................................................................................................................8

Part B.............................................................................................................................................8

1. Calculating the Weighted Average Cost of Capital (WACC) for J & J..................................8

2. Calculating the net present value and recommendations.......................................................10

3. Explaining the four different alternatives to cash dividend as the way of returning value to

the shareholders.........................................................................................................................11

REFERENCES................................................................................................................................1

APPENDICES.................................................................................................................................3

INTRODUCTION

Strategic corporate finance is concerned with managing the finances of the company with

the view to succeed by achieving the long term goals and objectives of the company and

maximization of the funds of the shareholders. This report will investigate the financial

performance of two companies namely, Axiata Group Berhad and Maxis Berhad operating in the

communication industry. Both the companies are listed companies on the FTSE Bursa Malaysia

KLCI Index. On the basis of ratio analysis, corporate governance and investment strategy a

report will be prepared for the Board of Directors through analysis and evaluation of the five-

year performance of both the companies.

Axiata Group Berhad is popularly known as Axiata. The former name of company is TM

International Berhad. It is a Malaysia based MNC operating largely in Asia as

telecommunications conglomerate. One of the largest wireless carriers in Malaysia. Maxis

Berhad or Maxis Communications is a Malaysian service provider of communication services.

The company is one of the biggest and oldest company in telecommunications sector in

Malaysia.

MAIN BODY

Part A

Analysing the performance of the companies on the basis of Ratios

Liquidity Ratio

Liquidity Ratio calculates the ability of the company to make the payment for its debt

when they become due (Haralayya, 2022). This ratio tells the quickness of a company in

converting its current assets into cash so that the short term liabilities can be paid off on timely

basis.

2021 2020 2019 2018 2017

current ratio Axiata Group Berhad 0.61 0.69 0.39 0.67 0.65

MAXIS BERHAD 0.48 0.63 0.53 0.59 0.57

Quick Ratio Axiata Group Berhad 0.60 0.68 0.39 0.66 0.64

MAXIS BERHAD 0.43 0.57 0.50 0.55 0.37

Strategic corporate finance is concerned with managing the finances of the company with

the view to succeed by achieving the long term goals and objectives of the company and

maximization of the funds of the shareholders. This report will investigate the financial

performance of two companies namely, Axiata Group Berhad and Maxis Berhad operating in the

communication industry. Both the companies are listed companies on the FTSE Bursa Malaysia

KLCI Index. On the basis of ratio analysis, corporate governance and investment strategy a

report will be prepared for the Board of Directors through analysis and evaluation of the five-

year performance of both the companies.

Axiata Group Berhad is popularly known as Axiata. The former name of company is TM

International Berhad. It is a Malaysia based MNC operating largely in Asia as

telecommunications conglomerate. One of the largest wireless carriers in Malaysia. Maxis

Berhad or Maxis Communications is a Malaysian service provider of communication services.

The company is one of the biggest and oldest company in telecommunications sector in

Malaysia.

MAIN BODY

Part A

Analysing the performance of the companies on the basis of Ratios

Liquidity Ratio

Liquidity Ratio calculates the ability of the company to make the payment for its debt

when they become due (Haralayya, 2022). This ratio tells the quickness of a company in

converting its current assets into cash so that the short term liabilities can be paid off on timely

basis.

2021 2020 2019 2018 2017

current ratio Axiata Group Berhad 0.61 0.69 0.39 0.67 0.65

MAXIS BERHAD 0.48 0.63 0.53 0.59 0.57

Quick Ratio Axiata Group Berhad 0.60 0.68 0.39 0.66 0.64

MAXIS BERHAD 0.43 0.57 0.50 0.55 0.37

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The two liquidity ratios calculated are current ratio and quick ratio. The current ratio of

Axiata Group Berhad is 0.61 for the year 2021. The company had the lowest current ratio in the

year 2019. Expect year 2019 other four years shows little variations in the current ratio. The

company’s current ratio rises in year 2018 slightly as compared to the year 2017. The reason

behind weak current ratio in the year 2019 is low current assets with the company against the

comparatively high current liabilities as compared to the other years. On an average the current

ratio of the company indicates that the company has 0.6 current asset against each of its short

term liability (INTEGRATED ANNUAL REPORTS. 2022). Liquidity ratios shows the cash

available with the company to pay for its current liabilities. Quick assets are calculated by

subtracting the inventories from the current assets. The immediate cash available with the

company to pay for its 1RM of short term liabilities is 0.60RM in the current year.

The current and quick ratios of Maxis Berhad fell in the year 2021 in comparison to

2020. Company has RM0.63 and RM0.57 worth of current and quick assets respectively against

1RM of its current liabilities in the year 2020 that declined to 0.48RM of current and 0.43RM of

quick assets in the year 2021. On an average the company has RM0.5 of current assets against

each of its liabilities.

The liquidity of Axiata Group Berhad is better in comparison to Maxis Berhad. This

indicates the better availability of short term assets with the company Axiata as compared to

Maxis to pay for its current liabilities when they arise.

Profitability Ratio

Profitability ratio are used as a tool to determine the ability of business in generating

earnings (Choi and et.al., 2018). Various types of expenses are compared with the sales by the

company to determine the profitability of the company.

2021 2020 2019 2018 2017

Operating Profit

Ratio Axiata Group Berhad 14.74% 10.31% 17.59% -9.99% 12.29%

MAXIS BERHAD 41.55% 41.62% 40.60% 40.25% 48.63%

Net Profit Ratio Axiata Group Berhad 4.93% 2.58% 7.38% -20.83% 4.76%

MAXIS BERHAD 14.21% 15.41% 16.31% 19.36% 25.20%

Axiata Group Berhad is 0.61 for the year 2021. The company had the lowest current ratio in the

year 2019. Expect year 2019 other four years shows little variations in the current ratio. The

company’s current ratio rises in year 2018 slightly as compared to the year 2017. The reason

behind weak current ratio in the year 2019 is low current assets with the company against the

comparatively high current liabilities as compared to the other years. On an average the current

ratio of the company indicates that the company has 0.6 current asset against each of its short

term liability (INTEGRATED ANNUAL REPORTS. 2022). Liquidity ratios shows the cash

available with the company to pay for its current liabilities. Quick assets are calculated by

subtracting the inventories from the current assets. The immediate cash available with the

company to pay for its 1RM of short term liabilities is 0.60RM in the current year.

The current and quick ratios of Maxis Berhad fell in the year 2021 in comparison to

2020. Company has RM0.63 and RM0.57 worth of current and quick assets respectively against

1RM of its current liabilities in the year 2020 that declined to 0.48RM of current and 0.43RM of

quick assets in the year 2021. On an average the company has RM0.5 of current assets against

each of its liabilities.

The liquidity of Axiata Group Berhad is better in comparison to Maxis Berhad. This

indicates the better availability of short term assets with the company Axiata as compared to

Maxis to pay for its current liabilities when they arise.

Profitability Ratio

Profitability ratio are used as a tool to determine the ability of business in generating

earnings (Choi and et.al., 2018). Various types of expenses are compared with the sales by the

company to determine the profitability of the company.

2021 2020 2019 2018 2017

Operating Profit

Ratio Axiata Group Berhad 14.74% 10.31% 17.59% -9.99% 12.29%

MAXIS BERHAD 41.55% 41.62% 40.60% 40.25% 48.63%

Net Profit Ratio Axiata Group Berhad 4.93% 2.58% 7.38% -20.83% 4.76%

MAXIS BERHAD 14.21% 15.41% 16.31% 19.36% 25.20%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating profit ratio is calculated by dividing the profit generated by the company from

its operations or the revenue left with the company after providing for its operating expenses

with the sales by the company. The ratio for the operations of the Axiata Group Berhad show an

increasing trend for the year 2021 as compared to the year 2020. The company has operating loss

for the year 2018 and the computed ratio is -10% approximately. The operating profit ratio of the

company hiked in the year 2019. Net profit ratio for the year 2021 is nearly 5% showing an

approx. rise of 2.5% from the previous year.

Operating profit ratio of the Maxis communication is stable from the last four years after

a decline of nearly 8% in the year 2018. The net profit ratio of the company shows gradual

declining trend over the past five years (Annual Report. 2022).

In terms of the profitability the Maxis communications is ahead and better from the

Axiata Group Berhad. Both the operating profit and net profit ratios are promising for the later

company in comparison to former.

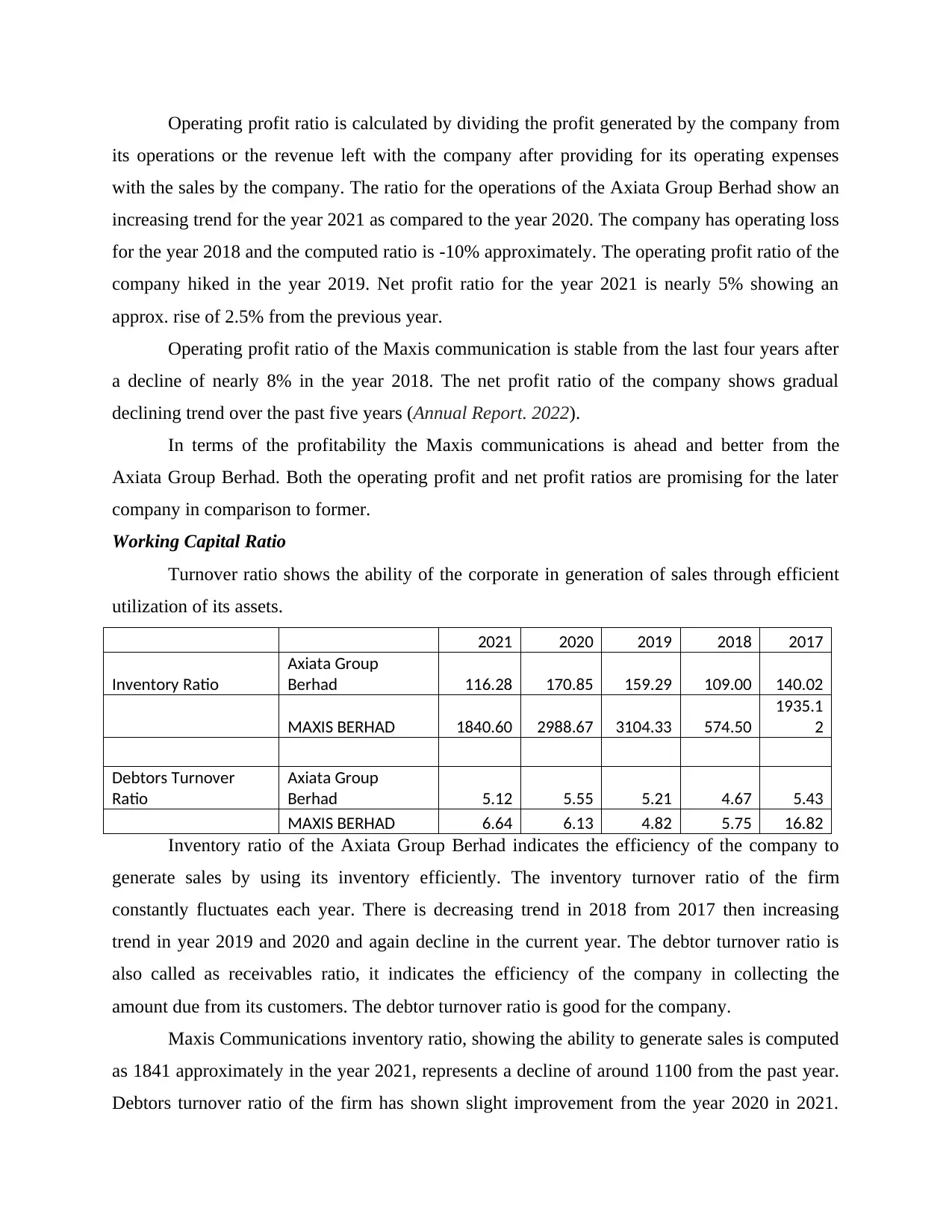

Working Capital Ratio

Turnover ratio shows the ability of the corporate in generation of sales through efficient

utilization of its assets.

2021 2020 2019 2018 2017

Inventory Ratio

Axiata Group

Berhad 116.28 170.85 159.29 109.00 140.02

MAXIS BERHAD 1840.60 2988.67 3104.33 574.50

1935.1

2

Debtors Turnover

Ratio

Axiata Group

Berhad 5.12 5.55 5.21 4.67 5.43

MAXIS BERHAD 6.64 6.13 4.82 5.75 16.82

Inventory ratio of the Axiata Group Berhad indicates the efficiency of the company to

generate sales by using its inventory efficiently. The inventory turnover ratio of the firm

constantly fluctuates each year. There is decreasing trend in 2018 from 2017 then increasing

trend in year 2019 and 2020 and again decline in the current year. The debtor turnover ratio is

also called as receivables ratio, it indicates the efficiency of the company in collecting the

amount due from its customers. The debtor turnover ratio is good for the company.

Maxis Communications inventory ratio, showing the ability to generate sales is computed

as 1841 approximately in the year 2021, represents a decline of around 1100 from the past year.

Debtors turnover ratio of the firm has shown slight improvement from the year 2020 in 2021.

its operations or the revenue left with the company after providing for its operating expenses

with the sales by the company. The ratio for the operations of the Axiata Group Berhad show an

increasing trend for the year 2021 as compared to the year 2020. The company has operating loss

for the year 2018 and the computed ratio is -10% approximately. The operating profit ratio of the

company hiked in the year 2019. Net profit ratio for the year 2021 is nearly 5% showing an

approx. rise of 2.5% from the previous year.

Operating profit ratio of the Maxis communication is stable from the last four years after

a decline of nearly 8% in the year 2018. The net profit ratio of the company shows gradual

declining trend over the past five years (Annual Report. 2022).

In terms of the profitability the Maxis communications is ahead and better from the

Axiata Group Berhad. Both the operating profit and net profit ratios are promising for the later

company in comparison to former.

Working Capital Ratio

Turnover ratio shows the ability of the corporate in generation of sales through efficient

utilization of its assets.

2021 2020 2019 2018 2017

Inventory Ratio

Axiata Group

Berhad 116.28 170.85 159.29 109.00 140.02

MAXIS BERHAD 1840.60 2988.67 3104.33 574.50

1935.1

2

Debtors Turnover

Ratio

Axiata Group

Berhad 5.12 5.55 5.21 4.67 5.43

MAXIS BERHAD 6.64 6.13 4.82 5.75 16.82

Inventory ratio of the Axiata Group Berhad indicates the efficiency of the company to

generate sales by using its inventory efficiently. The inventory turnover ratio of the firm

constantly fluctuates each year. There is decreasing trend in 2018 from 2017 then increasing

trend in year 2019 and 2020 and again decline in the current year. The debtor turnover ratio is

also called as receivables ratio, it indicates the efficiency of the company in collecting the

amount due from its customers. The debtor turnover ratio is good for the company.

Maxis Communications inventory ratio, showing the ability to generate sales is computed

as 1841 approximately in the year 2021, represents a decline of around 1100 from the past year.

Debtors turnover ratio of the firm has shown slight improvement from the year 2020 in 2021.

There is an increasing trend over the last three years reflecting the increasing efficiency of the

firm.

On the basis of the working capital ratio the efficiency of Maxis Berhad is higher than the

other company Axiata Group Berhad. Maxis communication uses its assets more efficiently than

the Axiata leading to comparatively higher sales of the company.

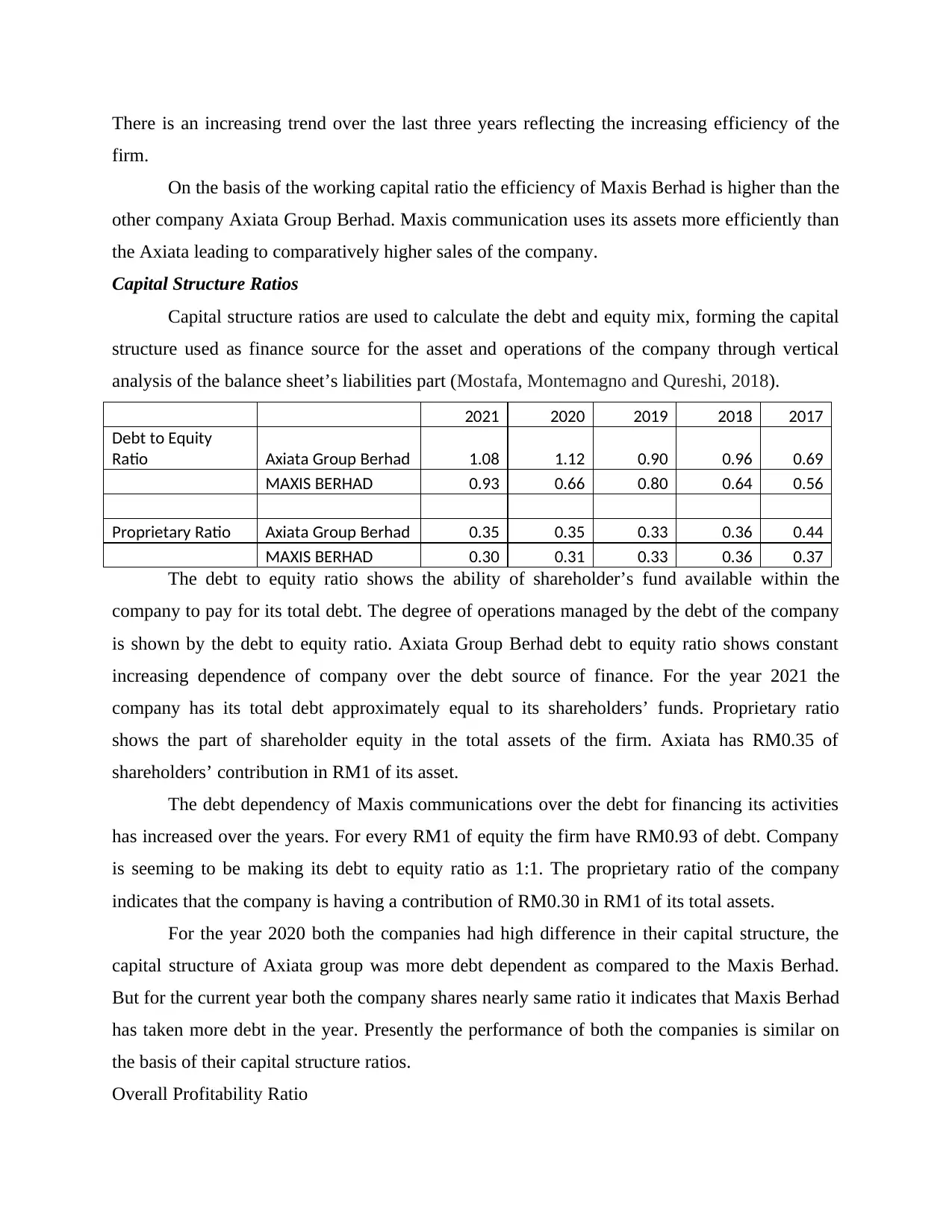

Capital Structure Ratios

Capital structure ratios are used to calculate the debt and equity mix, forming the capital

structure used as finance source for the asset and operations of the company through vertical

analysis of the balance sheet’s liabilities part (Mostafa, Montemagno and Qureshi, 2018).

2021 2020 2019 2018 2017

Debt to Equity

Ratio Axiata Group Berhad 1.08 1.12 0.90 0.96 0.69

MAXIS BERHAD 0.93 0.66 0.80 0.64 0.56

Proprietary Ratio Axiata Group Berhad 0.35 0.35 0.33 0.36 0.44

MAXIS BERHAD 0.30 0.31 0.33 0.36 0.37

The debt to equity ratio shows the ability of shareholder’s fund available within the

company to pay for its total debt. The degree of operations managed by the debt of the company

is shown by the debt to equity ratio. Axiata Group Berhad debt to equity ratio shows constant

increasing dependence of company over the debt source of finance. For the year 2021 the

company has its total debt approximately equal to its shareholders’ funds. Proprietary ratio

shows the part of shareholder equity in the total assets of the firm. Axiata has RM0.35 of

shareholders’ contribution in RM1 of its asset.

The debt dependency of Maxis communications over the debt for financing its activities

has increased over the years. For every RM1 of equity the firm have RM0.93 of debt. Company

is seeming to be making its debt to equity ratio as 1:1. The proprietary ratio of the company

indicates that the company is having a contribution of RM0.30 in RM1 of its total assets.

For the year 2020 both the companies had high difference in their capital structure, the

capital structure of Axiata group was more debt dependent as compared to the Maxis Berhad.

But for the current year both the company shares nearly same ratio it indicates that Maxis Berhad

has taken more debt in the year. Presently the performance of both the companies is similar on

the basis of their capital structure ratios.

Overall Profitability Ratio

firm.

On the basis of the working capital ratio the efficiency of Maxis Berhad is higher than the

other company Axiata Group Berhad. Maxis communication uses its assets more efficiently than

the Axiata leading to comparatively higher sales of the company.

Capital Structure Ratios

Capital structure ratios are used to calculate the debt and equity mix, forming the capital

structure used as finance source for the asset and operations of the company through vertical

analysis of the balance sheet’s liabilities part (Mostafa, Montemagno and Qureshi, 2018).

2021 2020 2019 2018 2017

Debt to Equity

Ratio Axiata Group Berhad 1.08 1.12 0.90 0.96 0.69

MAXIS BERHAD 0.93 0.66 0.80 0.64 0.56

Proprietary Ratio Axiata Group Berhad 0.35 0.35 0.33 0.36 0.44

MAXIS BERHAD 0.30 0.31 0.33 0.36 0.37

The debt to equity ratio shows the ability of shareholder’s fund available within the

company to pay for its total debt. The degree of operations managed by the debt of the company

is shown by the debt to equity ratio. Axiata Group Berhad debt to equity ratio shows constant

increasing dependence of company over the debt source of finance. For the year 2021 the

company has its total debt approximately equal to its shareholders’ funds. Proprietary ratio

shows the part of shareholder equity in the total assets of the firm. Axiata has RM0.35 of

shareholders’ contribution in RM1 of its asset.

The debt dependency of Maxis communications over the debt for financing its activities

has increased over the years. For every RM1 of equity the firm have RM0.93 of debt. Company

is seeming to be making its debt to equity ratio as 1:1. The proprietary ratio of the company

indicates that the company is having a contribution of RM0.30 in RM1 of its total assets.

For the year 2020 both the companies had high difference in their capital structure, the

capital structure of Axiata group was more debt dependent as compared to the Maxis Berhad.

But for the current year both the company shares nearly same ratio it indicates that Maxis Berhad

has taken more debt in the year. Presently the performance of both the companies is similar on

the basis of their capital structure ratios.

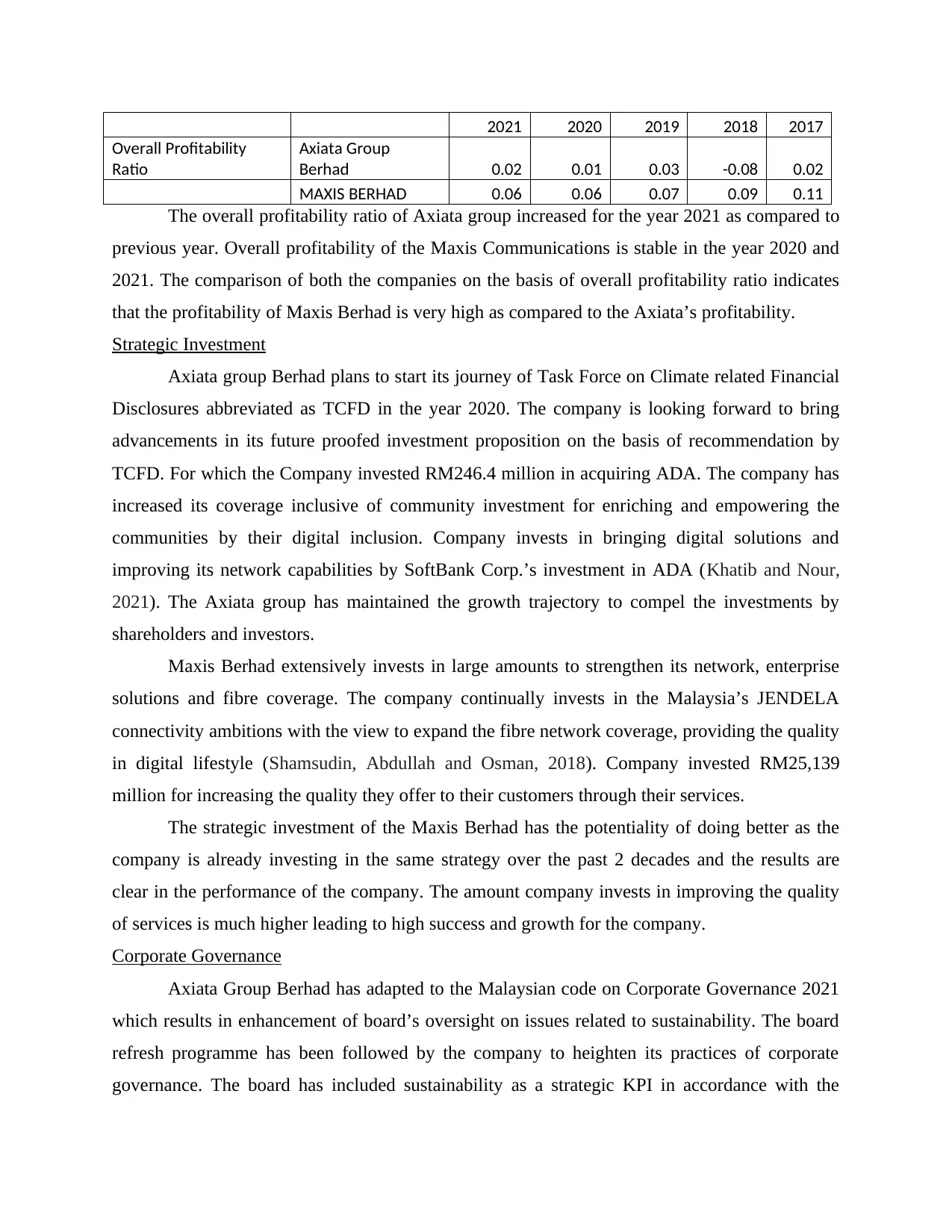

Overall Profitability Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2021 2020 2019 2018 2017

Overall Profitability

Ratio

Axiata Group

Berhad 0.02 0.01 0.03 -0.08 0.02

MAXIS BERHAD 0.06 0.06 0.07 0.09 0.11

The overall profitability ratio of Axiata group increased for the year 2021 as compared to

previous year. Overall profitability of the Maxis Communications is stable in the year 2020 and

2021. The comparison of both the companies on the basis of overall profitability ratio indicates

that the profitability of Maxis Berhad is very high as compared to the Axiata’s profitability.

Strategic Investment

Axiata group Berhad plans to start its journey of Task Force on Climate related Financial

Disclosures abbreviated as TCFD in the year 2020. The company is looking forward to bring

advancements in its future proofed investment proposition on the basis of recommendation by

TCFD. For which the Company invested RM246.4 million in acquiring ADA. The company has

increased its coverage inclusive of community investment for enriching and empowering the

communities by their digital inclusion. Company invests in bringing digital solutions and

improving its network capabilities by SoftBank Corp.’s investment in ADA (Khatib and Nour,

2021). The Axiata group has maintained the growth trajectory to compel the investments by

shareholders and investors.

Maxis Berhad extensively invests in large amounts to strengthen its network, enterprise

solutions and fibre coverage. The company continually invests in the Malaysia’s JENDELA

connectivity ambitions with the view to expand the fibre network coverage, providing the quality

in digital lifestyle (Shamsudin, Abdullah and Osman, 2018). Company invested RM25,139

million for increasing the quality they offer to their customers through their services.

The strategic investment of the Maxis Berhad has the potentiality of doing better as the

company is already investing in the same strategy over the past 2 decades and the results are

clear in the performance of the company. The amount company invests in improving the quality

of services is much higher leading to high success and growth for the company.

Corporate Governance

Axiata Group Berhad has adapted to the Malaysian code on Corporate Governance 2021

which results in enhancement of board’s oversight on issues related to sustainability. The board

refresh programme has been followed by the company to heighten its practices of corporate

governance. The board has included sustainability as a strategic KPI in accordance with the

Overall Profitability

Ratio

Axiata Group

Berhad 0.02 0.01 0.03 -0.08 0.02

MAXIS BERHAD 0.06 0.06 0.07 0.09 0.11

The overall profitability ratio of Axiata group increased for the year 2021 as compared to

previous year. Overall profitability of the Maxis Communications is stable in the year 2020 and

2021. The comparison of both the companies on the basis of overall profitability ratio indicates

that the profitability of Maxis Berhad is very high as compared to the Axiata’s profitability.

Strategic Investment

Axiata group Berhad plans to start its journey of Task Force on Climate related Financial

Disclosures abbreviated as TCFD in the year 2020. The company is looking forward to bring

advancements in its future proofed investment proposition on the basis of recommendation by

TCFD. For which the Company invested RM246.4 million in acquiring ADA. The company has

increased its coverage inclusive of community investment for enriching and empowering the

communities by their digital inclusion. Company invests in bringing digital solutions and

improving its network capabilities by SoftBank Corp.’s investment in ADA (Khatib and Nour,

2021). The Axiata group has maintained the growth trajectory to compel the investments by

shareholders and investors.

Maxis Berhad extensively invests in large amounts to strengthen its network, enterprise

solutions and fibre coverage. The company continually invests in the Malaysia’s JENDELA

connectivity ambitions with the view to expand the fibre network coverage, providing the quality

in digital lifestyle (Shamsudin, Abdullah and Osman, 2018). Company invested RM25,139

million for increasing the quality they offer to their customers through their services.

The strategic investment of the Maxis Berhad has the potentiality of doing better as the

company is already investing in the same strategy over the past 2 decades and the results are

clear in the performance of the company. The amount company invests in improving the quality

of services is much higher leading to high success and growth for the company.

Corporate Governance

Axiata Group Berhad has adapted to the Malaysian code on Corporate Governance 2021

which results in enhancement of board’s oversight on issues related to sustainability. The board

refresh programme has been followed by the company to heighten its practices of corporate

governance. The board has included sustainability as a strategic KPI in accordance with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Malaysian code (Dixon, 2022). High ethical and good corporate governance standards are

followed by the company. The effectivity of the governance is recognized by the Indonesian

Institute for corporate directorship corporate governance award 2021. All the principles of good

corporate governance like integrity, ethics, respect to rights and balanced disclosure are

followed.

The board of the Maxis Communication is committed towards upholding the highest

standards of corporate governance. The company hols integrity at all levels, regulatory duties

and commercial objectives are duly undertaken (Ab, Rahaman and Haron, 2021). Malaysian

Code on Corporate Governance 2021 recommendations are followed by the company.

The Corporate Governance of Axiata Group Berhad is better in comparison to Maxis.

Through effective corporate governance the company ensures the sustainability in its processes

and is highly integrated and transparent.

CONCLUSION

Based on the report the importance of strategic corporate finance in evaluating the

performance has been highlighted. The report has calculated the ratios of Axiata Group Berhad

and Maxis Berhad to analyse the performance of the two companies. Maxis Berhad is the higher

performing company based on the liquidity, profitability, solvency and efficiency of the

company being better. The corporate governance of the Axiata Group Berhad is better than

Maxis communications. The strategic investment of Maxis Communications in more reliable.

Part B

1. Calculating the Weighted Average Cost of Capital (WACC) for J & J

The WACC is a concept which outlines the average cost of capital from the different

sources though which company generates money. These different sources include common

stock, bonds, debenture, preferred stock and other different forms of debt (Budhathoki and Rai,

2020). This tool is assistive for the investors to determine that whether investment within the

company is beneficial and profitable or not. This WACC is being calculated by multiplying the

cost of every capital source with the related weight and then totalling all the sources together

gives the WACC.

WACC=(VE×Re) + (VD×Rd×(1−Tc))

Here

E- market value of equity

followed by the company. The effectivity of the governance is recognized by the Indonesian

Institute for corporate directorship corporate governance award 2021. All the principles of good

corporate governance like integrity, ethics, respect to rights and balanced disclosure are

followed.

The board of the Maxis Communication is committed towards upholding the highest

standards of corporate governance. The company hols integrity at all levels, regulatory duties

and commercial objectives are duly undertaken (Ab, Rahaman and Haron, 2021). Malaysian

Code on Corporate Governance 2021 recommendations are followed by the company.

The Corporate Governance of Axiata Group Berhad is better in comparison to Maxis.

Through effective corporate governance the company ensures the sustainability in its processes

and is highly integrated and transparent.

CONCLUSION

Based on the report the importance of strategic corporate finance in evaluating the

performance has been highlighted. The report has calculated the ratios of Axiata Group Berhad

and Maxis Berhad to analyse the performance of the two companies. Maxis Berhad is the higher

performing company based on the liquidity, profitability, solvency and efficiency of the

company being better. The corporate governance of the Axiata Group Berhad is better than

Maxis communications. The strategic investment of Maxis Communications in more reliable.

Part B

1. Calculating the Weighted Average Cost of Capital (WACC) for J & J

The WACC is a concept which outlines the average cost of capital from the different

sources though which company generates money. These different sources include common

stock, bonds, debenture, preferred stock and other different forms of debt (Budhathoki and Rai,

2020). This tool is assistive for the investors to determine that whether investment within the

company is beneficial and profitable or not. This WACC is being calculated by multiplying the

cost of every capital source with the related weight and then totalling all the sources together

gives the WACC.

WACC=(VE×Re) + (VD×Rd×(1−Tc))

Here

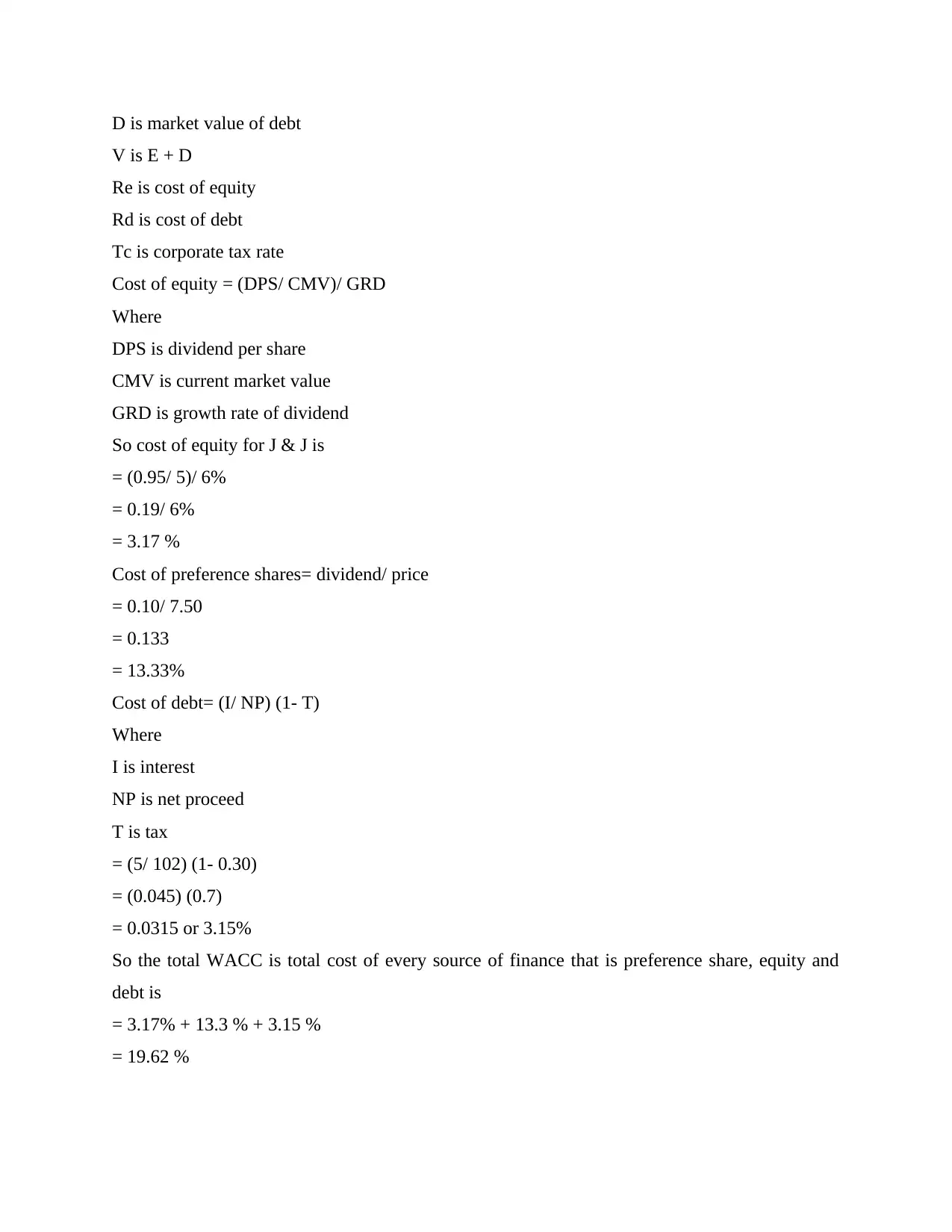

E- market value of equity

D is market value of debt

V is E + D

Re is cost of equity

Rd is cost of debt

Tc is corporate tax rate

Cost of equity = (DPS/ CMV)/ GRD

Where

DPS is dividend per share

CMV is current market value

GRD is growth rate of dividend

So cost of equity for J & J is

= (0.95/ 5)/ 6%

= 0.19/ 6%

= 3.17 %

Cost of preference shares= dividend/ price

= 0.10/ 7.50

= 0.133

= 13.33%

Cost of debt= (I/ NP) (1- T)

Where

I is interest

NP is net proceed

T is tax

= (5/ 102) (1- 0.30)

= (0.045) (0.7)

= 0.0315 or 3.15%

So the total WACC is total cost of every source of finance that is preference share, equity and

debt is

= 3.17% + 13.3 % + 3.15 %

= 19.62 %

V is E + D

Re is cost of equity

Rd is cost of debt

Tc is corporate tax rate

Cost of equity = (DPS/ CMV)/ GRD

Where

DPS is dividend per share

CMV is current market value

GRD is growth rate of dividend

So cost of equity for J & J is

= (0.95/ 5)/ 6%

= 0.19/ 6%

= 3.17 %

Cost of preference shares= dividend/ price

= 0.10/ 7.50

= 0.133

= 13.33%

Cost of debt= (I/ NP) (1- T)

Where

I is interest

NP is net proceed

T is tax

= (5/ 102) (1- 0.30)

= (0.045) (0.7)

= 0.0315 or 3.15%

So the total WACC is total cost of every source of finance that is preference share, equity and

debt is

= 3.17% + 13.3 % + 3.15 %

= 19.62 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

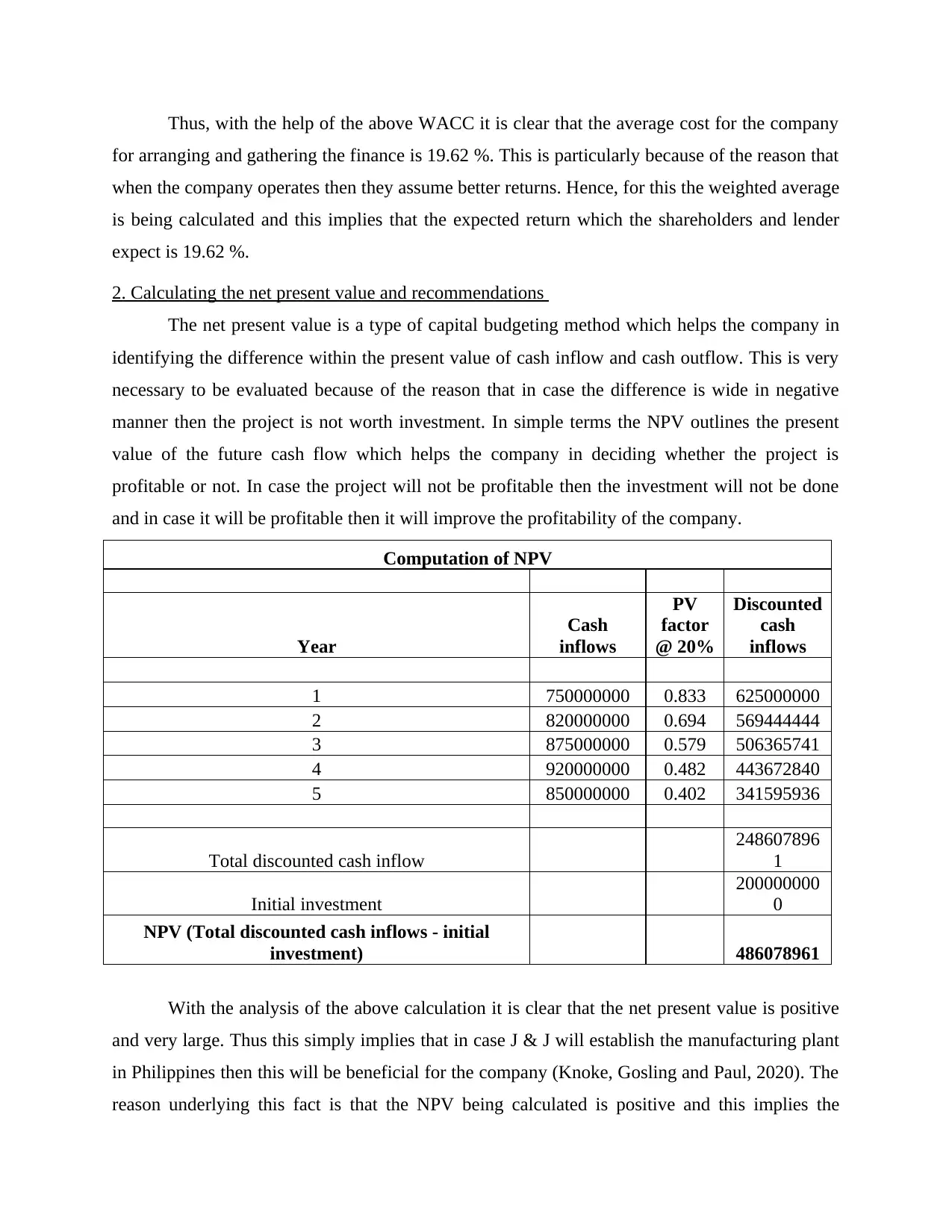

Thus, with the help of the above WACC it is clear that the average cost for the company

for arranging and gathering the finance is 19.62 %. This is particularly because of the reason that

when the company operates then they assume better returns. Hence, for this the weighted average

is being calculated and this implies that the expected return which the shareholders and lender

expect is 19.62 %.

2. Calculating the net present value and recommendations

The net present value is a type of capital budgeting method which helps the company in

identifying the difference within the present value of cash inflow and cash outflow. This is very

necessary to be evaluated because of the reason that in case the difference is wide in negative

manner then the project is not worth investment. In simple terms the NPV outlines the present

value of the future cash flow which helps the company in deciding whether the project is

profitable or not. In case the project will not be profitable then the investment will not be done

and in case it will be profitable then it will improve the profitability of the company.

Computation of NPV

Year

Cash

inflows

PV

factor

@ 20%

Discounted

cash

inflows

1 750000000 0.833 625000000

2 820000000 0.694 569444444

3 875000000 0.579 506365741

4 920000000 0.482 443672840

5 850000000 0.402 341595936

Total discounted cash inflow

248607896

1

Initial investment

200000000

0

NPV (Total discounted cash inflows - initial

investment) 486078961

With the analysis of the above calculation it is clear that the net present value is positive

and very large. Thus this simply implies that in case J & J will establish the manufacturing plant

in Philippines then this will be beneficial for the company (Knoke, Gosling and Paul, 2020). The

reason underlying this fact is that the NPV being calculated is positive and this implies the

for arranging and gathering the finance is 19.62 %. This is particularly because of the reason that

when the company operates then they assume better returns. Hence, for this the weighted average

is being calculated and this implies that the expected return which the shareholders and lender

expect is 19.62 %.

2. Calculating the net present value and recommendations

The net present value is a type of capital budgeting method which helps the company in

identifying the difference within the present value of cash inflow and cash outflow. This is very

necessary to be evaluated because of the reason that in case the difference is wide in negative

manner then the project is not worth investment. In simple terms the NPV outlines the present

value of the future cash flow which helps the company in deciding whether the project is

profitable or not. In case the project will not be profitable then the investment will not be done

and in case it will be profitable then it will improve the profitability of the company.

Computation of NPV

Year

Cash

inflows

PV

factor

@ 20%

Discounted

cash

inflows

1 750000000 0.833 625000000

2 820000000 0.694 569444444

3 875000000 0.579 506365741

4 920000000 0.482 443672840

5 850000000 0.402 341595936

Total discounted cash inflow

248607896

1

Initial investment

200000000

0

NPV (Total discounted cash inflows - initial

investment) 486078961

With the analysis of the above calculation it is clear that the net present value is positive

and very large. Thus this simply implies that in case J & J will establish the manufacturing plant

in Philippines then this will be beneficial for the company (Knoke, Gosling and Paul, 2020). The

reason underlying this fact is that the NPV being calculated is positive and this implies the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

project is worth investment. This is also beneficial for the company as the project is beneficial

and highly profitable. Thus, for J & J it is beneficial that they open the establishment in

Philippines.

The recommendation of the use of NPV is that company and potential investor can

analyse that whether they should invest within the project or not. Also, it is recommended to the

company to not invest in the project which is having negative NPV. This is pertaining to the fact

that when the NPV is negative then it implies that in future the project will be providing loss and

this will be affecting the profitability of the business to a great extent.

3. Explaining the four different alternatives to cash dividend as the way of returning value to the

shareholders

The cash dividend is being referred to as the distribution of the funds and the money paid

to the shareholders from the current earning. There are different alternatives for the cash

dividend which company can pay against the cash dividend. These alternatives include the

following-

The first alternative involves share repurchases and within this method the company

purchase its own shares and this results in reduction of the numbers of outstanding

shares. With this company can either retire the shares or even can hold them like a

treasury stock. Thus, the reduction in the shares outstanding outlines that even the profits

will be same the earnings per share will be increasing.

Another alternative to cash dividend is stock split which is a way to issue stock dividend.

Many a times the company can split the shares and this can be treated as an alternate to

the cash dividend. This stock split is being executed with help of issuing new shares in

exchange of the old shares. This splitting of stock does not change the market

capitalisation of the company but only changes the number of shared outstanding.

In addition to this another alternative to cash dividend is the stock dividend. Within this

method, the company provides for an additional shares of stock in exchange of the cash

dividend (What Are the Alternatives to Cash Dividends for Shareholders? 2022). In this

method the company gives more stake to the shareholders other than the existing stake in

order to avoid the cash dividend.

and highly profitable. Thus, for J & J it is beneficial that they open the establishment in

Philippines.

The recommendation of the use of NPV is that company and potential investor can

analyse that whether they should invest within the project or not. Also, it is recommended to the

company to not invest in the project which is having negative NPV. This is pertaining to the fact

that when the NPV is negative then it implies that in future the project will be providing loss and

this will be affecting the profitability of the business to a great extent.

3. Explaining the four different alternatives to cash dividend as the way of returning value to the

shareholders

The cash dividend is being referred to as the distribution of the funds and the money paid

to the shareholders from the current earning. There are different alternatives for the cash

dividend which company can pay against the cash dividend. These alternatives include the

following-

The first alternative involves share repurchases and within this method the company

purchase its own shares and this results in reduction of the numbers of outstanding

shares. With this company can either retire the shares or even can hold them like a

treasury stock. Thus, the reduction in the shares outstanding outlines that even the profits

will be same the earnings per share will be increasing.

Another alternative to cash dividend is stock split which is a way to issue stock dividend.

Many a times the company can split the shares and this can be treated as an alternate to

the cash dividend. This stock split is being executed with help of issuing new shares in

exchange of the old shares. This splitting of stock does not change the market

capitalisation of the company but only changes the number of shared outstanding.

In addition to this another alternative to cash dividend is the stock dividend. Within this

method, the company provides for an additional shares of stock in exchange of the cash

dividend (What Are the Alternatives to Cash Dividends for Shareholders? 2022). In this

method the company gives more stake to the shareholders other than the existing stake in

order to avoid the cash dividend.

Moreover, another method for avoiding the cash dividend is the qualified dividend. These

qualified dividends are being paid in cash to the shareholders but these are taxed at the

same rate as compared to the long term capital gains.

Hence, with this it can be stated that instead of using the cash dividend the company can

undertake the use of the different alternatives listed above.

qualified dividends are being paid in cash to the shareholders but these are taxed at the

same rate as compared to the long term capital gains.

Hence, with this it can be stated that instead of using the cash dividend the company can

undertake the use of the different alternatives listed above.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.