Exploring Variance Analysis: A Comprehensive Study on Fixed Overheads

VerifiedAdded on 2020/06/06

|20

|5716

|41

AI Summary

The assignment examines significant facets of management accounting, emphasizing absorption and marginal costing methodologies. It explores how these approaches affect financial decisions and operational strategies through detailed variance analysis, particularly concerning fixed production overhead variances. Additionally, it assesses managerial accounting practices including inventory, capital expenditure control, and their strategic implications on businesses. The document provides insights into effective cost control mechanisms, highlighting the integral role of management accountants in guiding organizational objectives. Furthermore, it references authoritative studies to underpin the analysis with contemporary academic perspectives.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

An area of study where financial plans are prepared, implemented, monitored and

evaluated within an enterprise is referred as management accounting (MA). This is basically

used by firms for making several kinds of business decisions of internal environment. Further, it

not focuses on external business environment and not supports to make decisions related to the

same (Nørreklit, 2014). In the present study, Harrods Limited Company is taken into

consideration. This firm is a small business enterprise and has market presence in retail industry

of UK. Throughout the project, systems of MA and methods involved under its reporting

procedure are explained. Apart from this, income statements are formulated for selected firm

using two MA techniques i.e. marginal and absorption. Besides this, planning methods which are

considered by Harrods Limited in order to control over the budgetary are evaluated in the

project. Moreover, the current assignment focuses on systems of MA which support the retailer

for making effective solutions for several financial issues.

TASK 1

P1 Explaining MA and its systems along with key requirements, applied by Harrods Limited

within business

Business Report

From: Management accounting Officer

To: General Manager

Harrods Limited

Subject: Systems of management accounting

Date: 24th November 2017

Introduction

1

An area of study where financial plans are prepared, implemented, monitored and

evaluated within an enterprise is referred as management accounting (MA). This is basically

used by firms for making several kinds of business decisions of internal environment. Further, it

not focuses on external business environment and not supports to make decisions related to the

same (Nørreklit, 2014). In the present study, Harrods Limited Company is taken into

consideration. This firm is a small business enterprise and has market presence in retail industry

of UK. Throughout the project, systems of MA and methods involved under its reporting

procedure are explained. Apart from this, income statements are formulated for selected firm

using two MA techniques i.e. marginal and absorption. Besides this, planning methods which are

considered by Harrods Limited in order to control over the budgetary are evaluated in the

project. Moreover, the current assignment focuses on systems of MA which support the retailer

for making effective solutions for several financial issues.

TASK 1

P1 Explaining MA and its systems along with key requirements, applied by Harrods Limited

within business

Business Report

From: Management accounting Officer

To: General Manager

Harrods Limited

Subject: Systems of management accounting

Date: 24th November 2017

Introduction

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

At the workplace of each firm, wide range of decisions and judgements are needed to take in

proper manner. For this, some methods are applied by it which support to determine required

information in adequate manner. The present business report reflects some systems of MA used

by Harrods Limited. Apart from this, essential needs of these all the approaches are also

described under this stated report.

Systems

Cost accounting: Expenses are one of very essential and sensitive part for every organisation

which must be lower. If level of total cost is high in the firm then it will create negative impact

on the financial performance directly. The cost accounting system is a procedure in order to

record, segregate, analyse, summarise as well as allocate courses of actions for controlling

expenses. It consists of different types like activity based, target, throughput, environmental,

standard cost accounting etc. Basic components included under this system are like raw

materials, labour and overheads (Bruynseels and Cardinaels, 2013). Essential needs of this for

Harrods Limited is to determine level of total expenses associated at the workplace. Further, it

is supportive for ascertaining cost incurred to produce and sale one unit up to consumers. For

segregating total expenditures in the firm also this method is used by the retailer. Apart from

this, for presenting as well as interpreting information for management planning, evaluating

performance and controlling cost accounting is significant. The company invests in various

capital projects and expansion also where this stated system of MA is highly supportive. Hence,

essential requirement of cost accounting in Harrods Limited is to assess expenditures incurred

within firm.

Stock management: Inventory is also very significant part for the firms which must be lower at

the end of every financial year. The basic issue behind this is that, higher the stock create

negative impact on company for generating revenue. On the basis of this system management of

Harrods Limited able to manage and reduce stock within enterprise. So that, inventory turnover

ratio will be improved along with financial performance. Moreover, it majorly deals with time

that when to order the stock and how much. When these both the aspects clearly known by the

management then it can improve performance. Further, objective of inventory management is to

reduce total cost of stock and gain higher returns (Inventory Management, 2013). For this

particular situation, economic order quantity and just-in-time, theses two tools used. While

2

proper manner. For this, some methods are applied by it which support to determine required

information in adequate manner. The present business report reflects some systems of MA used

by Harrods Limited. Apart from this, essential needs of these all the approaches are also

described under this stated report.

Systems

Cost accounting: Expenses are one of very essential and sensitive part for every organisation

which must be lower. If level of total cost is high in the firm then it will create negative impact

on the financial performance directly. The cost accounting system is a procedure in order to

record, segregate, analyse, summarise as well as allocate courses of actions for controlling

expenses. It consists of different types like activity based, target, throughput, environmental,

standard cost accounting etc. Basic components included under this system are like raw

materials, labour and overheads (Bruynseels and Cardinaels, 2013). Essential needs of this for

Harrods Limited is to determine level of total expenses associated at the workplace. Further, it

is supportive for ascertaining cost incurred to produce and sale one unit up to consumers. For

segregating total expenditures in the firm also this method is used by the retailer. Apart from

this, for presenting as well as interpreting information for management planning, evaluating

performance and controlling cost accounting is significant. The company invests in various

capital projects and expansion also where this stated system of MA is highly supportive. Hence,

essential requirement of cost accounting in Harrods Limited is to assess expenditures incurred

within firm.

Stock management: Inventory is also very significant part for the firms which must be lower at

the end of every financial year. The basic issue behind this is that, higher the stock create

negative impact on company for generating revenue. On the basis of this system management of

Harrods Limited able to manage and reduce stock within enterprise. So that, inventory turnover

ratio will be improved along with financial performance. Moreover, it majorly deals with time

that when to order the stock and how much. When these both the aspects clearly known by the

management then it can improve performance. Further, objective of inventory management is to

reduce total cost of stock and gain higher returns (Inventory Management, 2013). For this

particular situation, economic order quantity and just-in-time, theses two tools used. While

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

managing this aspect valuation is also mandatory to do. To make stock valuation, LIFO, FIFO

and Weighted average methods are implemented in Harrods.

Job costing: Another approach of MA is the job costing which has key purpose is to analyse

expenses incurred to manufacture each product unit. Further, revenue generated by the firm are

also assessed on the basis of each job of the company. It is one kind of cost monitoring process

which are assigned to produce every product in the business environment. Further, it keeps

proper record of every expense comes into consideration at the workplace of Harrods Limited.

Being a retailer, this job costing system is considered to know that to purchase goods, complete

packaging and sale in the market how much level of expenses incurred. It includes basically

three kinds of accounting activities for deriving total cost of each job product. Such activities

are like purchase of raw materials, labour or wages as well as overhead expenditures (Cooper,

Ezzamel and Qu, 2017). Therefore, it will become to set effective price of per unit using

suitable pricing strategies.

Price optimisation: At the end, last system used by selected firm of MA is price optimisation

which works for pricing aspects only. Herein, any other kind of financial information as well as

data not taken into consideration. It is a method which helps to Harrods Limited for analysing

behaviour of buyers or customers at different price levels. It is used to derive structure of three

prices which are like initial, promotional as well as discount pricing in the firm. One particular

price at which major customers give positive response that is to be determined by the retailer.

On the basis of this particular system, management able to make fruitful pricing decisions so

that it able to gain huge incomes.

Conclusion

It can be analysed from the current business report that, using several systems fallen under

management accounting the firm makes effective decisions. These systems are like job costing,

stock management, price optimisation and cost accounting. The job costing and cost accounting

support to determine expenses incurred to produce batch products and total production

respectively. Apart from this, inventory management and price optimisation considered by

Harrods for managing stock and opt profitable price for selling retail products in market.

3

and Weighted average methods are implemented in Harrods.

Job costing: Another approach of MA is the job costing which has key purpose is to analyse

expenses incurred to manufacture each product unit. Further, revenue generated by the firm are

also assessed on the basis of each job of the company. It is one kind of cost monitoring process

which are assigned to produce every product in the business environment. Further, it keeps

proper record of every expense comes into consideration at the workplace of Harrods Limited.

Being a retailer, this job costing system is considered to know that to purchase goods, complete

packaging and sale in the market how much level of expenses incurred. It includes basically

three kinds of accounting activities for deriving total cost of each job product. Such activities

are like purchase of raw materials, labour or wages as well as overhead expenditures (Cooper,

Ezzamel and Qu, 2017). Therefore, it will become to set effective price of per unit using

suitable pricing strategies.

Price optimisation: At the end, last system used by selected firm of MA is price optimisation

which works for pricing aspects only. Herein, any other kind of financial information as well as

data not taken into consideration. It is a method which helps to Harrods Limited for analysing

behaviour of buyers or customers at different price levels. It is used to derive structure of three

prices which are like initial, promotional as well as discount pricing in the firm. One particular

price at which major customers give positive response that is to be determined by the retailer.

On the basis of this particular system, management able to make fruitful pricing decisions so

that it able to gain huge incomes.

Conclusion

It can be analysed from the current business report that, using several systems fallen under

management accounting the firm makes effective decisions. These systems are like job costing,

stock management, price optimisation and cost accounting. The job costing and cost accounting

support to determine expenses incurred to produce batch products and total production

respectively. Apart from this, inventory management and price optimisation considered by

Harrods for managing stock and opt profitable price for selling retail products in market.

3

P2 Scribe different method acting which are considered for MA reporting at the workplace of

Harrods Limited

Business Report

From: Management accounting Officer

To: General Manager

Harrods Limited

Subject: Management activity reports

Date: 24th November 2017

Introduction

A system in which small reports prepared on the basis of various financial transactions and after

clubbing them financial statements are formulated for an organisation is known as reporting

system. The current business report shows about various methods involved in MA reporting.

Considering to such systems Harrods Limited easily able to prepare financial statements analyse

performance in the market.

Significance of management activity reports

Basic importance of management activity reports is to know day-to-day financial transactions

recorded of the firm. Further, managers able to assess that incomes are outcomes in form of

cash are whether in proper proportion or not. On the basis of such reports firm can easily make

final accounts and publish in the market (Grabner and Moers, 2013). Moreover, various reports

of MA reporting are stated below:

Performance report: This method is used for measuring as well as analysing performance of the

company where two data compared with each another. In accordance with this method,

managers assess that firm performs well or poor in the market. By making comparison between

budgeted and actual figures at the end of year, performance is to be analysed. When budgeted

data higher as compared to actual in the financial period ending then poor performance will be

considered. Under this condition, Harrods Limited will make strategies for managing and

declining costs and enhancing revenue. So that, it easily able to meet budgeted data and boost

up performance in retail segment of UK. This is generally applied by the businesses because it

4

Harrods Limited

Business Report

From: Management accounting Officer

To: General Manager

Harrods Limited

Subject: Management activity reports

Date: 24th November 2017

Introduction

A system in which small reports prepared on the basis of various financial transactions and after

clubbing them financial statements are formulated for an organisation is known as reporting

system. The current business report shows about various methods involved in MA reporting.

Considering to such systems Harrods Limited easily able to prepare financial statements analyse

performance in the market.

Significance of management activity reports

Basic importance of management activity reports is to know day-to-day financial transactions

recorded of the firm. Further, managers able to assess that incomes are outcomes in form of

cash are whether in proper proportion or not. On the basis of such reports firm can easily make

final accounts and publish in the market (Grabner and Moers, 2013). Moreover, various reports

of MA reporting are stated below:

Performance report: This method is used for measuring as well as analysing performance of the

company where two data compared with each another. In accordance with this method,

managers assess that firm performs well or poor in the market. By making comparison between

budgeted and actual figures at the end of year, performance is to be analysed. When budgeted

data higher as compared to actual in the financial period ending then poor performance will be

considered. Under this condition, Harrods Limited will make strategies for managing and

declining costs and enhancing revenue. So that, it easily able to meet budgeted data and boost

up performance in retail segment of UK. This is generally applied by the businesses because it

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps to become more financially sound and meet financial goals.

Accounts receivables ageing: Another method of MA reporting is accounts receivables ageing

which keeps record of credit sales made within one fiscal year. It is not necessary that the firm

sale its products and services in cash always (Cadez and Guilding, 2012). Rather than cash,

many times managers sale goods and services on credit as well. This amount is to be received

after sometimes or many be in upcoming business year from customers. Sum of money of total

credit sales is recorded in this particular report on day-to-day basis. Transactions recorded on

the basis of chronological order where initial date recorded on top and so on. Herein, Harrods

Limited can determine that up to which amount, products are sold on credit within one year.

Total of this report is recorded in balance sheet of the firm as debtors in assets side.

Departmental report: As per this, every financial transactions occurred in each function of the

company are recorded. Incomes and expenses come into consideration in HR, marketing,

production, research and development etc. departments are included in this method. Central

manager of Harrods Limited can determine that which particular segment of company gives

more profit. In addition to this, efficiency and productivity both terms are also easily defined of

the department. On the basis of this, proper and attractive strategies for boosting performance

can be made and applied at the workplace. Herein, final accounts or descriptions of receipts and

payments can be properly evaluated (Groot and Selto, 2013). Therefore, decisions for allocating

resources and implementing tactics can be made appropriately.

Operation budget report: This kind of particular method of reporting used by Harrods Limited

to prepare operational budget. On the basis of this, incomes as well as payments for the

upcoming financial year are forecasted. During this process, if management finds that cash

position in next year will be in negative manner then strategies will be prepared. When next

year will come then the formulated tactics will be applied in the business. Due to this, it can

enhance sales and decline payments where cash position will improve ultimately. Once total

expenses made and recorded in this report then used as operating costs in the firm.

Conclusion

It can be summarised from the present report that, with the help of various reports a company

able to accomplish MA reporting process in proper and effective manner. It includes major

5

Accounts receivables ageing: Another method of MA reporting is accounts receivables ageing

which keeps record of credit sales made within one fiscal year. It is not necessary that the firm

sale its products and services in cash always (Cadez and Guilding, 2012). Rather than cash,

many times managers sale goods and services on credit as well. This amount is to be received

after sometimes or many be in upcoming business year from customers. Sum of money of total

credit sales is recorded in this particular report on day-to-day basis. Transactions recorded on

the basis of chronological order where initial date recorded on top and so on. Herein, Harrods

Limited can determine that up to which amount, products are sold on credit within one year.

Total of this report is recorded in balance sheet of the firm as debtors in assets side.

Departmental report: As per this, every financial transactions occurred in each function of the

company are recorded. Incomes and expenses come into consideration in HR, marketing,

production, research and development etc. departments are included in this method. Central

manager of Harrods Limited can determine that which particular segment of company gives

more profit. In addition to this, efficiency and productivity both terms are also easily defined of

the department. On the basis of this, proper and attractive strategies for boosting performance

can be made and applied at the workplace. Herein, final accounts or descriptions of receipts and

payments can be properly evaluated (Groot and Selto, 2013). Therefore, decisions for allocating

resources and implementing tactics can be made appropriately.

Operation budget report: This kind of particular method of reporting used by Harrods Limited

to prepare operational budget. On the basis of this, incomes as well as payments for the

upcoming financial year are forecasted. During this process, if management finds that cash

position in next year will be in negative manner then strategies will be prepared. When next

year will come then the formulated tactics will be applied in the business. Due to this, it can

enhance sales and decline payments where cash position will improve ultimately. Once total

expenses made and recorded in this report then used as operating costs in the firm.

Conclusion

It can be summarised from the present report that, with the help of various reports a company

able to accomplish MA reporting process in proper and effective manner. It includes major

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

three methods which are such as operation budget, departmental, performance and debtors or

accounts receivables ageing. When these all the small reports formulated properly then total

amount of these recorded in respective final accounts. Further, every firm including Harrods

Limited use this process for taking internal judgements at the workplace.

TASK 2

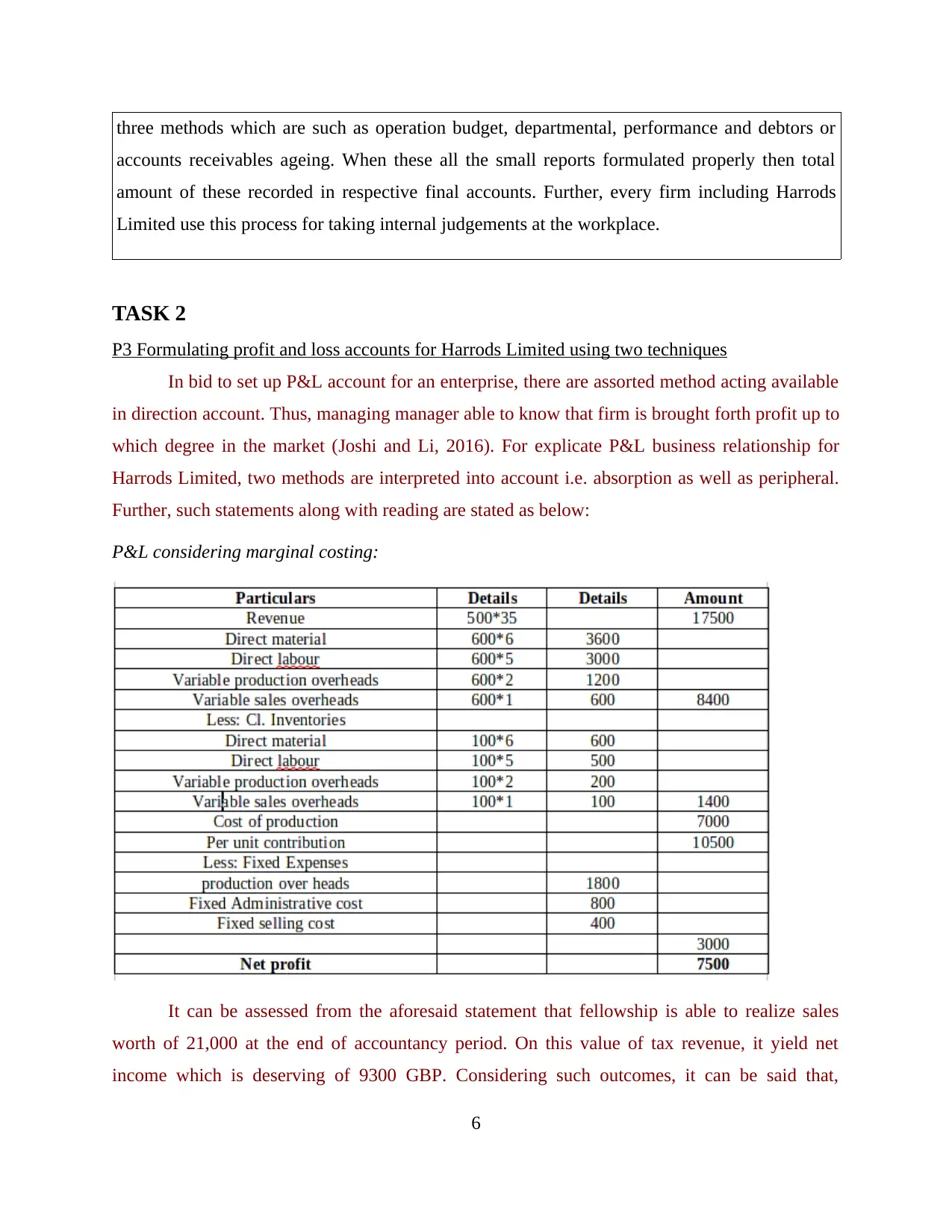

P3 Formulating profit and loss accounts for Harrods Limited using two techniques

In bid to set up P&L account for an enterprise, there are assorted method acting available

in direction account. Thus, managing manager able to know that firm is brought forth profit up to

which degree in the market (Joshi and Li, 2016). For explicate P&L business relationship for

Harrods Limited, two methods are interpreted into account i.e. absorption as well as peripheral.

Further, such statements along with reading are stated as below:

P&L considering marginal costing:

It can be assessed from the aforesaid statement that fellowship is able to realize sales

worth of 21,000 at the end of accountancy period. On this value of tax revenue, it yield net

income which is deserving of 9300 GBP. Considering such outcomes, it can be said that,

6

accounts receivables ageing. When these all the small reports formulated properly then total

amount of these recorded in respective final accounts. Further, every firm including Harrods

Limited use this process for taking internal judgements at the workplace.

TASK 2

P3 Formulating profit and loss accounts for Harrods Limited using two techniques

In bid to set up P&L account for an enterprise, there are assorted method acting available

in direction account. Thus, managing manager able to know that firm is brought forth profit up to

which degree in the market (Joshi and Li, 2016). For explicate P&L business relationship for

Harrods Limited, two methods are interpreted into account i.e. absorption as well as peripheral.

Further, such statements along with reading are stated as below:

P&L considering marginal costing:

It can be assessed from the aforesaid statement that fellowship is able to realize sales

worth of 21,000 at the end of accountancy period. On this value of tax revenue, it yield net

income which is deserving of 9300 GBP. Considering such outcomes, it can be said that,

6

management of Harrods can reduce total changeable outgo in the year. As it Further, in the future

when managers manage such expenses then can enhance net profits of business organization in

approaching year.

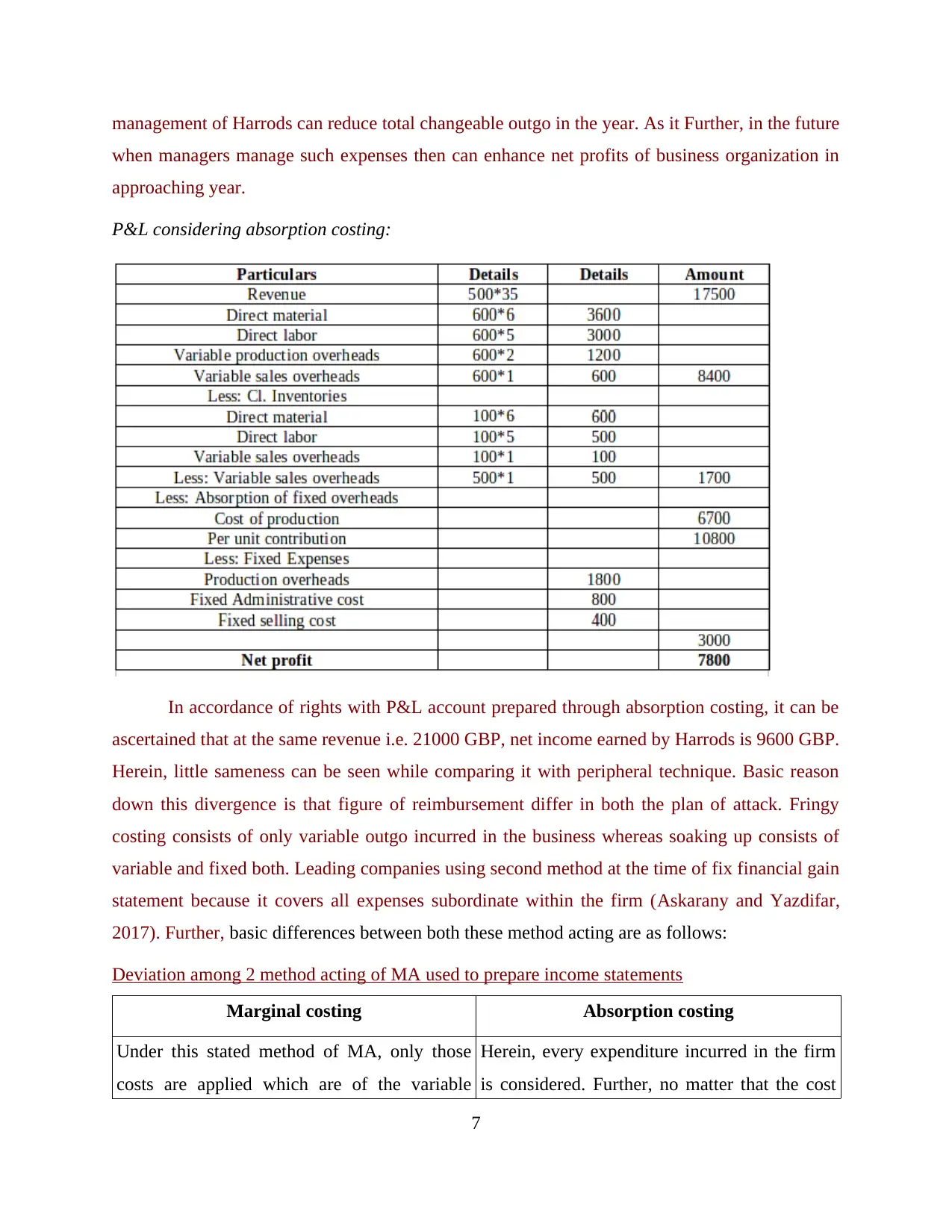

P&L considering absorption costing:

In accordance of rights with P&L account prepared through absorption costing, it can be

ascertained that at the same revenue i.e. 21000 GBP, net income earned by Harrods is 9600 GBP.

Herein, little sameness can be seen while comparing it with peripheral technique. Basic reason

down this divergence is that figure of reimbursement differ in both the plan of attack. Fringy

costing consists of only variable outgo incurred in the business whereas soaking up consists of

variable and fixed both. Leading companies using second method at the time of fix financial gain

statement because it covers all expenses subordinate within the firm (Askarany and Yazdifar,

2017). Further, basic differences between both these method acting are as follows:

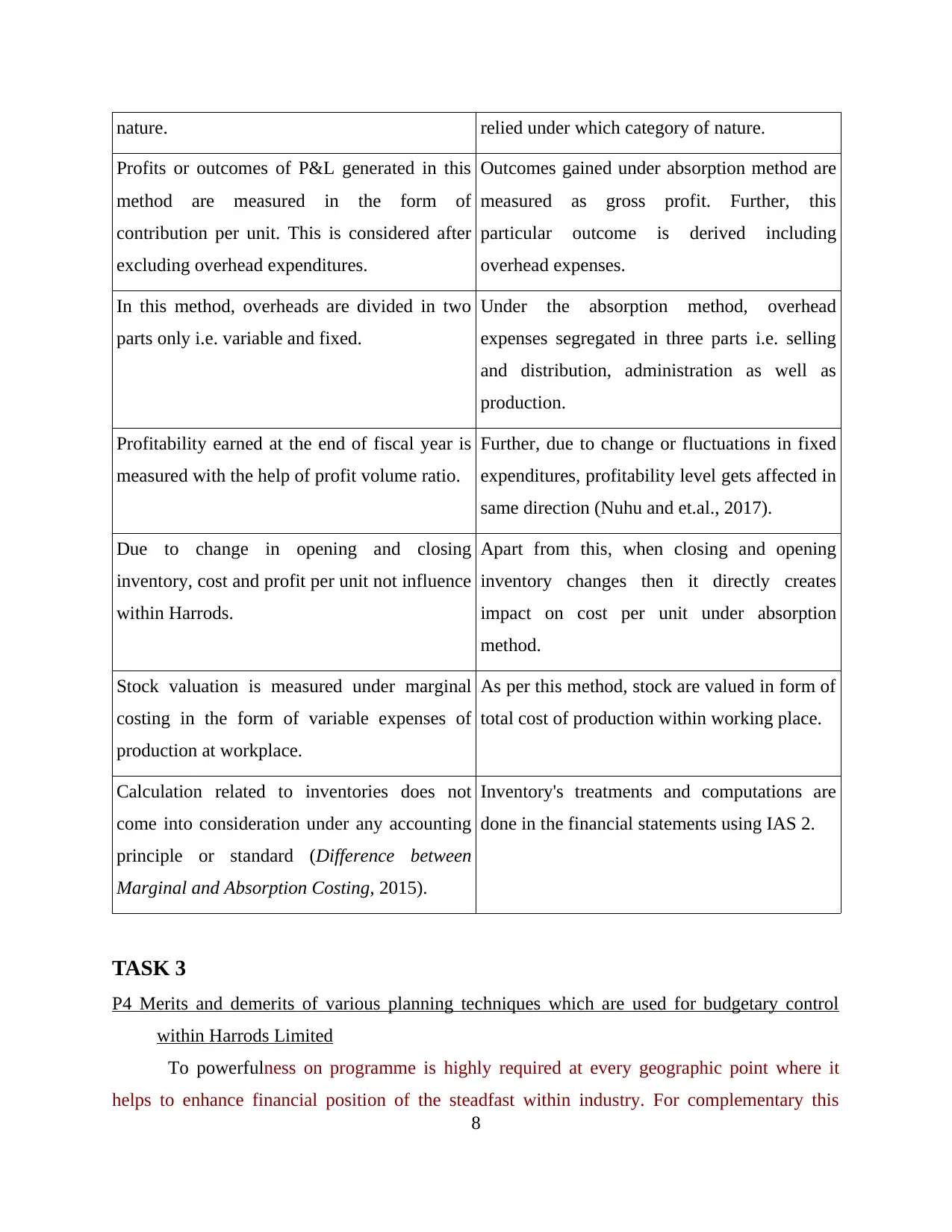

Deviation among 2 method acting of MA used to prepare income statements

Marginal costing Absorption costing

Under this stated method of MA, only those

costs are applied which are of the variable

Herein, every expenditure incurred in the firm

is considered. Further, no matter that the cost

7

when managers manage such expenses then can enhance net profits of business organization in

approaching year.

P&L considering absorption costing:

In accordance of rights with P&L account prepared through absorption costing, it can be

ascertained that at the same revenue i.e. 21000 GBP, net income earned by Harrods is 9600 GBP.

Herein, little sameness can be seen while comparing it with peripheral technique. Basic reason

down this divergence is that figure of reimbursement differ in both the plan of attack. Fringy

costing consists of only variable outgo incurred in the business whereas soaking up consists of

variable and fixed both. Leading companies using second method at the time of fix financial gain

statement because it covers all expenses subordinate within the firm (Askarany and Yazdifar,

2017). Further, basic differences between both these method acting are as follows:

Deviation among 2 method acting of MA used to prepare income statements

Marginal costing Absorption costing

Under this stated method of MA, only those

costs are applied which are of the variable

Herein, every expenditure incurred in the firm

is considered. Further, no matter that the cost

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

nature. relied under which category of nature.

Profits or outcomes of P&L generated in this

method are measured in the form of

contribution per unit. This is considered after

excluding overhead expenditures.

Outcomes gained under absorption method are

measured as gross profit. Further, this

particular outcome is derived including

overhead expenses.

In this method, overheads are divided in two

parts only i.e. variable and fixed.

Under the absorption method, overhead

expenses segregated in three parts i.e. selling

and distribution, administration as well as

production.

Profitability earned at the end of fiscal year is

measured with the help of profit volume ratio.

Further, due to change or fluctuations in fixed

expenditures, profitability level gets affected in

same direction (Nuhu and et.al., 2017).

Due to change in opening and closing

inventory, cost and profit per unit not influence

within Harrods.

Apart from this, when closing and opening

inventory changes then it directly creates

impact on cost per unit under absorption

method.

Stock valuation is measured under marginal

costing in the form of variable expenses of

production at workplace.

As per this method, stock are valued in form of

total cost of production within working place.

Calculation related to inventories does not

come into consideration under any accounting

principle or standard (Difference between

Marginal and Absorption Costing, 2015).

Inventory's treatments and computations are

done in the financial statements using IAS 2.

TASK 3

P4 Merits and demerits of various planning techniques which are used for budgetary control

within Harrods Limited

To powerfulness on programme is highly required at every geographic point where it

helps to enhance financial position of the steadfast within industry. For complementary this

8

Profits or outcomes of P&L generated in this

method are measured in the form of

contribution per unit. This is considered after

excluding overhead expenditures.

Outcomes gained under absorption method are

measured as gross profit. Further, this

particular outcome is derived including

overhead expenses.

In this method, overheads are divided in two

parts only i.e. variable and fixed.

Under the absorption method, overhead

expenses segregated in three parts i.e. selling

and distribution, administration as well as

production.

Profitability earned at the end of fiscal year is

measured with the help of profit volume ratio.

Further, due to change or fluctuations in fixed

expenditures, profitability level gets affected in

same direction (Nuhu and et.al., 2017).

Due to change in opening and closing

inventory, cost and profit per unit not influence

within Harrods.

Apart from this, when closing and opening

inventory changes then it directly creates

impact on cost per unit under absorption

method.

Stock valuation is measured under marginal

costing in the form of variable expenses of

production at workplace.

As per this method, stock are valued in form of

total cost of production within working place.

Calculation related to inventories does not

come into consideration under any accounting

principle or standard (Difference between

Marginal and Absorption Costing, 2015).

Inventory's treatments and computations are

done in the financial statements using IAS 2.

TASK 3

P4 Merits and demerits of various planning techniques which are used for budgetary control

within Harrods Limited

To powerfulness on programme is highly required at every geographic point where it

helps to enhance financial position of the steadfast within industry. For complementary this

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

specific task some effective readying know-how are taken into business relationship by the pull

off. Harrods limited institution is a retailer company which is located in UK. It was incorporated

in the year 1889. The company necessarily to know about its fund. So it can use zero based or

determinate or incremental monetary fund method acting for fund devising. Zero based

programme method uses the technique of re evaluation of each and every cost that are enclosed

in unexpected expenditure. Fixed budgeting play-acting uses a set amount of cost for calculating

time unit or yearly monetary fund. Further, additive monetary fund used when institution wants

to enhance the budgets on accordant basis over the periods. Rating of these all the formulation

methods is stated below:

Zero based budgeting

It is management accounting that involves preparing budget from zero based or re-

evaluation of every item and justify all the expense incurred by department. Zero based

budgeting is a method of budgeting in which all the expenditures are calculated for new period.

In this method it is assumes that there are no pre committed expenditure and no carried forward

balance (Steed and Gu, 2009). Harrods limited can use this method of budgeting because it has

accuracy and efficiency in its performance.

Advantages: Accuracy- Harrods limited can use zero based budgeting method because it is very

accurate technique against the regular method. It involves making budgeting for the

company with re evaluate each item of cash flow. Efficiency- It is a process that helps for allocation of resources with efficiently. It assures

that numbers taken by department for budgeting is actual number.

Coordination and communication- Zero based budgeting improves communication and

coordination within the organisation. It also motivates employees because this method

involves them in the process of decision making.

Disadvantages: Time consuming- Zero based budgeting method is a time intensive process of Harrods

Limited because in this method every item re-evaluated for calculation (DRURY, 2013).

9

off. Harrods limited institution is a retailer company which is located in UK. It was incorporated

in the year 1889. The company necessarily to know about its fund. So it can use zero based or

determinate or incremental monetary fund method acting for fund devising. Zero based

programme method uses the technique of re evaluation of each and every cost that are enclosed

in unexpected expenditure. Fixed budgeting play-acting uses a set amount of cost for calculating

time unit or yearly monetary fund. Further, additive monetary fund used when institution wants

to enhance the budgets on accordant basis over the periods. Rating of these all the formulation

methods is stated below:

Zero based budgeting

It is management accounting that involves preparing budget from zero based or re-

evaluation of every item and justify all the expense incurred by department. Zero based

budgeting is a method of budgeting in which all the expenditures are calculated for new period.

In this method it is assumes that there are no pre committed expenditure and no carried forward

balance (Steed and Gu, 2009). Harrods limited can use this method of budgeting because it has

accuracy and efficiency in its performance.

Advantages: Accuracy- Harrods limited can use zero based budgeting method because it is very

accurate technique against the regular method. It involves making budgeting for the

company with re evaluate each item of cash flow. Efficiency- It is a process that helps for allocation of resources with efficiently. It assures

that numbers taken by department for budgeting is actual number.

Coordination and communication- Zero based budgeting improves communication and

coordination within the organisation. It also motivates employees because this method

involves them in the process of decision making.

Disadvantages: Time consuming- Zero based budgeting method is a time intensive process of Harrods

Limited because in this method every item re-evaluated for calculation (DRURY, 2013).

9

Requirement of high manpower- This budget making method requires large number of

employees because it involves budgeting from scratch. The company can not use

adequate human resource for this method.

Lack of expertise- In this method every item and cost explained by the department which

is very difficult task and requires more training.

Fixed budgeting

This method acting allows the fellowship to criterion long term as well as short term

budget. It apportions set amount of cost towards essentials from which territorial division can

compare monthly budget and yearly budget. Furthermore, as per this special method Harrows

Limited can enhance its commercial enterprise public presentation with same percentages over

the accounting periods.

Advantages: Measure performance- It is method that allots each month same amount of money from

which the company can compare monthly budget to measure long term success. When

the firm able to know level of performance then can implement required strategies to

improve (Miriam, 2011). Conformation cost down- This method acting helps to live the business to kind same

position at all business enterprise levels. As costs go down in the firm then Harrods

Limited will become to make more net income at the end of year.

Changes within a limit- This process only works when the business can survive. It allows

small businesses to cover unexpected cost.

Disadvantages: Inaccurate- This method of budgeting is not accurate as compared to zero budgeting

method. It is based on a set amount of cost which is not calculated by the Harrods

Limited.

Inefficient- In this process there are lack of communication and coordination techniques

therefore this method uses more time and cost (Hiebl, 2014). This method does not use

actual data or expenditure which makes it inefficient.

10

employees because it involves budgeting from scratch. The company can not use

adequate human resource for this method.

Lack of expertise- In this method every item and cost explained by the department which

is very difficult task and requires more training.

Fixed budgeting

This method acting allows the fellowship to criterion long term as well as short term

budget. It apportions set amount of cost towards essentials from which territorial division can

compare monthly budget and yearly budget. Furthermore, as per this special method Harrows

Limited can enhance its commercial enterprise public presentation with same percentages over

the accounting periods.

Advantages: Measure performance- It is method that allots each month same amount of money from

which the company can compare monthly budget to measure long term success. When

the firm able to know level of performance then can implement required strategies to

improve (Miriam, 2011). Conformation cost down- This method acting helps to live the business to kind same

position at all business enterprise levels. As costs go down in the firm then Harrods

Limited will become to make more net income at the end of year.

Changes within a limit- This process only works when the business can survive. It allows

small businesses to cover unexpected cost.

Disadvantages: Inaccurate- This method of budgeting is not accurate as compared to zero budgeting

method. It is based on a set amount of cost which is not calculated by the Harrods

Limited.

Inefficient- In this process there are lack of communication and coordination techniques

therefore this method uses more time and cost (Hiebl, 2014). This method does not use

actual data or expenditure which makes it inefficient.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.