Strategic Dynamics in the Banking Industry: A Comprehensive Review

VerifiedAdded on 2020/05/28

|16

|4410

|61

AI Summary

The banking industry has been a focal point for strategic analysis due to its complex nature and significant role in global economies. This assignment explores these complexities using Porter’s Five Forces as the primary analytical tool, supplemented by contemporary studies on efficiency, regulation, and competition dynamics. The analysis begins with an overview of the current state of the banking sector, highlighting key players and market trends. It then proceeds to apply each of Porter's Five Forces—threat of new entrants, bargaining power of suppliers, bargaining power of buyers, threat of substitute products or services, and industry rivalry—to understand competitive pressures within the industry.

The study also incorporates insights from recent research on banking efficiency, emphasizing how technological advancements and regulatory changes influence operational effectiveness. Additionally, it considers international perspectives by examining case studies such as the impact of global financial crises on Korean banks and regulatory effects in other regions like Australia and Kenya. The conclusion synthesizes these findings to offer strategic recommendations for stakeholders aiming to navigate the evolving landscape of the banking industry.

Running Head: International & Global Business

National Australian Bank

International and Global Business

National Australian Bank

International and Global Business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International and global business 1

Table of Content

Introduction................................................................................................................................3

Banking Industry in France........................................................................................................4

The Present Situation..............................................................................................................4

Porter’s Five Force Model......................................................................................................5

Threat of New Entrant........................................................................................................5

The Bargaining power of suppliers.....................................................................................5

Bargaining power of customers..........................................................................................6

Threat of Substitutes...........................................................................................................6

Competitive Rivalry............................................................................................................6

France’s Trade Union.............................................................................................................6

Recommendation for France..................................................................................................7

Banking Industry in Korea.........................................................................................................7

Present Situation in Korea..........................................................................................................7

Porter 5 Force Model- Banking in Korea...............................................................................8

Threat of New Entrant........................................................................................................8

Threat of Substitute Products..............................................................................................9

Bargaining power of customers..........................................................................................9

Bargaining power of suppliers............................................................................................9

Competitive Rivalry............................................................................................................9

Final Words on South Korea Banking Sector........................................................................9

Table of Content

Introduction................................................................................................................................3

Banking Industry in France........................................................................................................4

The Present Situation..............................................................................................................4

Porter’s Five Force Model......................................................................................................5

Threat of New Entrant........................................................................................................5

The Bargaining power of suppliers.....................................................................................5

Bargaining power of customers..........................................................................................6

Threat of Substitutes...........................................................................................................6

Competitive Rivalry............................................................................................................6

France’s Trade Union.............................................................................................................6

Recommendation for France..................................................................................................7

Banking Industry in Korea.........................................................................................................7

Present Situation in Korea..........................................................................................................7

Porter 5 Force Model- Banking in Korea...............................................................................8

Threat of New Entrant........................................................................................................8

Threat of Substitute Products..............................................................................................9

Bargaining power of customers..........................................................................................9

Bargaining power of suppliers............................................................................................9

Competitive Rivalry............................................................................................................9

Final Words on South Korea Banking Sector........................................................................9

International and global business 2

Banking Sector in Brazil..........................................................................................................10

Present Situation of Banking Sector........................................................................................10

Porter 5 Forces Model for Brazil..........................................................................................11

Barriers to Entry................................................................................................................11

Threat of Substitutes.........................................................................................................11

Bargaining power of consumers.......................................................................................11

Bargaining power of Suppliers.........................................................................................11

Competitive Rivalry..........................................................................................................12

Recommendation & Conclusion..............................................................................................12

Banking Sector in Brazil..........................................................................................................10

Present Situation of Banking Sector........................................................................................10

Porter 5 Forces Model for Brazil..........................................................................................11

Barriers to Entry................................................................................................................11

Threat of Substitutes.........................................................................................................11

Bargaining power of consumers.......................................................................................11

Bargaining power of Suppliers.........................................................................................11

Competitive Rivalry..........................................................................................................12

Recommendation & Conclusion..............................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International and global business 3

Introduction

Banking sector in Australia is dominated by the Big 4’s, namely; Commonwealth Bank of

Australia, Westpac Banking Corporation, Australian and New Zealand Banking Group &

National Australia Bank (Moradi-Motlagh & Babacan, 2015). Apart from the Big 4, the

industry has a number of small to medium scale banks serving the population, financial

institutions, credit unions and mutual banks fill up the rest of the banking ecosystem. Other

foreign banks are also present but they have a retail presence.

National Australia Bank was formed in the year 1982 as National commercial Banking

Corporation of Australia Limited, later the name got changed to NAB. The bank has its

headquarters in Melbourne and is serving the Markets of Australia, New Zealand and certain

parts of Asia. The bank is flourishing under the leadership of Andrew Thorburn (CEO) and

Mike Baird (Chairman). The market offering of the bank are Business banking, consumer

banking, wholesale banking, wealth management & Insurance as some of its major products.

National Bank of Australia is one of the highest respected banks of the Australian continent

and people turn up to the bank for fulfilment of their financial needs with impeccable

customer service. The bank employs over 35,000 employees in all its location and the

workforce is highly diverse in nature (Salim, Arjomandi & Seufert, 2016). The people

working at the bank take joint ownership and responsibility towards helping people and

providing them with best banking services. The Bank made a whopping cash profit of $ 6.48

Billion in the year 2016, which was net up by 4.2% from the preceding year, the results of FY

2017 are also better than the expected. Hence it can be said that National Bank of Australia

within a short duration for over than 3 decade has made a mark in the Australian Banking

Industry.

Every organization is in business to make profits and expand its business operations; same is

the case with National Australia Bank. NAB is looking forward to expand in the markets of

France, Brazil and Korea (Graham & Anderson, 2015). The decision for the expansion will

be based on the market attractiveness and the present banking scenario in these countries and

accordingly strategies will be recommended to NAB for the expansion.

Introduction

Banking sector in Australia is dominated by the Big 4’s, namely; Commonwealth Bank of

Australia, Westpac Banking Corporation, Australian and New Zealand Banking Group &

National Australia Bank (Moradi-Motlagh & Babacan, 2015). Apart from the Big 4, the

industry has a number of small to medium scale banks serving the population, financial

institutions, credit unions and mutual banks fill up the rest of the banking ecosystem. Other

foreign banks are also present but they have a retail presence.

National Australia Bank was formed in the year 1982 as National commercial Banking

Corporation of Australia Limited, later the name got changed to NAB. The bank has its

headquarters in Melbourne and is serving the Markets of Australia, New Zealand and certain

parts of Asia. The bank is flourishing under the leadership of Andrew Thorburn (CEO) and

Mike Baird (Chairman). The market offering of the bank are Business banking, consumer

banking, wholesale banking, wealth management & Insurance as some of its major products.

National Bank of Australia is one of the highest respected banks of the Australian continent

and people turn up to the bank for fulfilment of their financial needs with impeccable

customer service. The bank employs over 35,000 employees in all its location and the

workforce is highly diverse in nature (Salim, Arjomandi & Seufert, 2016). The people

working at the bank take joint ownership and responsibility towards helping people and

providing them with best banking services. The Bank made a whopping cash profit of $ 6.48

Billion in the year 2016, which was net up by 4.2% from the preceding year, the results of FY

2017 are also better than the expected. Hence it can be said that National Bank of Australia

within a short duration for over than 3 decade has made a mark in the Australian Banking

Industry.

Every organization is in business to make profits and expand its business operations; same is

the case with National Australia Bank. NAB is looking forward to expand in the markets of

France, Brazil and Korea (Graham & Anderson, 2015). The decision for the expansion will

be based on the market attractiveness and the present banking scenario in these countries and

accordingly strategies will be recommended to NAB for the expansion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International and global business 4

Banking Industry in France

A major structural reform in happened in the year 1984 in the French Banking industry, a

noteworthy fundamental change was removing the distinction between commercial and

merchant banks and clubbed them all together under one supervisory system. Credit Agricole

(CA), BNP Paribas, Societe Generale, Caisse d’Epargne, LCL and Credit Mutuel are some of

the largest France banks across the globe (Schwienbacher, 2016). The commercial banks

perform all the functions of regular banks like providing short and long term credits,

overdrafts, assisting in public offerings of shares and corporate debt et.al. Overall, France

has a total of 132 foreign banks with most of them having sizeable branch networks.

European central bank is the supervisory authority which controls all the financial

instruments and is responsible for printing of money.

The Present Situation

There is improvement in the economic situation of France; GDP grew by 1.2 % in the

year 2016.

France has in total 364 banks (January 2017)

European banking authority has said that the top 6 banks are amongst the Global

systematically important banks.

Almost 370,000 people comprise the workforce of the banking industry.

The six largest banks of France made a total income of €145.7 Billion

French banking industry is currently dealing with many International and European

regulatory requirements along with heavy tax burdens.

Outstanding business loans until 2017 were to the tune of €920 Billion.

SME’s are the prime beneficiaries of the bank lending activities.

The French Banks have decided to come up with an API in order to propose a much

stronger, secure, resilient and a standardised solution to connect the third party

providers.

Hence, the statistics and the figures of French banking industry says that the economy and the

banks are still struggling to recover from the Failure of the economy and banking system in

Banking Industry in France

A major structural reform in happened in the year 1984 in the French Banking industry, a

noteworthy fundamental change was removing the distinction between commercial and

merchant banks and clubbed them all together under one supervisory system. Credit Agricole

(CA), BNP Paribas, Societe Generale, Caisse d’Epargne, LCL and Credit Mutuel are some of

the largest France banks across the globe (Schwienbacher, 2016). The commercial banks

perform all the functions of regular banks like providing short and long term credits,

overdrafts, assisting in public offerings of shares and corporate debt et.al. Overall, France

has a total of 132 foreign banks with most of them having sizeable branch networks.

European central bank is the supervisory authority which controls all the financial

instruments and is responsible for printing of money.

The Present Situation

There is improvement in the economic situation of France; GDP grew by 1.2 % in the

year 2016.

France has in total 364 banks (January 2017)

European banking authority has said that the top 6 banks are amongst the Global

systematically important banks.

Almost 370,000 people comprise the workforce of the banking industry.

The six largest banks of France made a total income of €145.7 Billion

French banking industry is currently dealing with many International and European

regulatory requirements along with heavy tax burdens.

Outstanding business loans until 2017 were to the tune of €920 Billion.

SME’s are the prime beneficiaries of the bank lending activities.

The French Banks have decided to come up with an API in order to propose a much

stronger, secure, resilient and a standardised solution to connect the third party

providers.

Hence, the statistics and the figures of French banking industry says that the economy and the

banks are still struggling to recover from the Failure of the economy and banking system in

International and global business 5

some countries of EU, and the aftermath of the same is still being felt by the banking industry

(Riasi, 2015). Thus it can be said that, in the future the market condition will improve for

certain, but it is actually a tough call to get dragged in the prevailing condition of France.

In order to further determine the market attractiveness of the French banking industry,

Porter’s 5 force model will be used to analyse the profitability and the attractiveness of the

market.

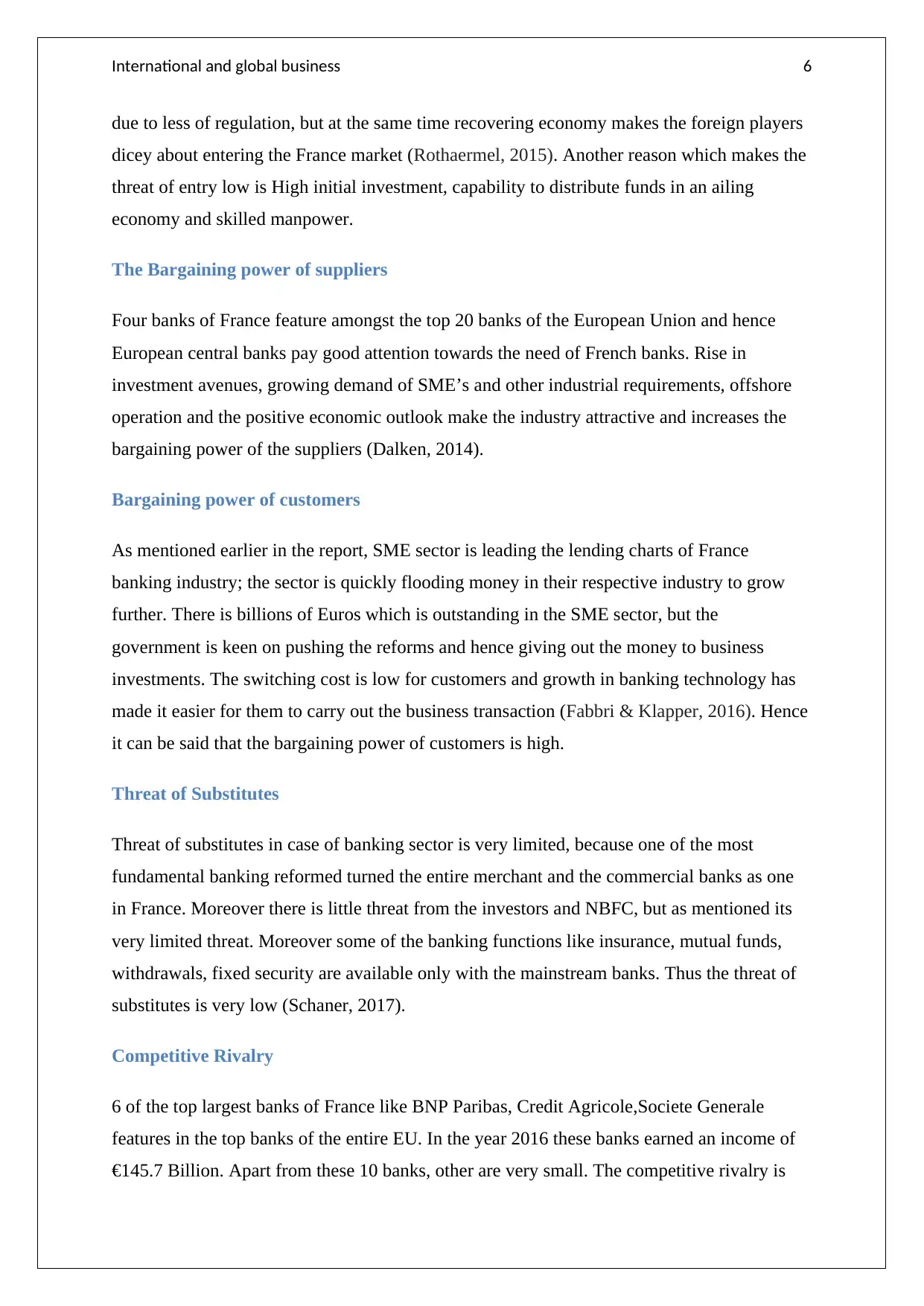

Porter’s Five Force Model

Porter’s 5 force model is extremely useful when it comes to finding the attractiveness and

profitability in the market (Dobbs, 2014). Porter uses the 5 force as the attribute to determine

the industry attractiveness. Following the guidelines of the model will understand the France

banking industry

Threat of New Entrant

France had undergone a fundamental regulatory change which got commercial and merchant

bank together under one roof of European central bank. France is still recovering from the

crisis faced by the European Union. The threat of entry seemed to be moderate in the industry

some countries of EU, and the aftermath of the same is still being felt by the banking industry

(Riasi, 2015). Thus it can be said that, in the future the market condition will improve for

certain, but it is actually a tough call to get dragged in the prevailing condition of France.

In order to further determine the market attractiveness of the French banking industry,

Porter’s 5 force model will be used to analyse the profitability and the attractiveness of the

market.

Porter’s Five Force Model

Porter’s 5 force model is extremely useful when it comes to finding the attractiveness and

profitability in the market (Dobbs, 2014). Porter uses the 5 force as the attribute to determine

the industry attractiveness. Following the guidelines of the model will understand the France

banking industry

Threat of New Entrant

France had undergone a fundamental regulatory change which got commercial and merchant

bank together under one roof of European central bank. France is still recovering from the

crisis faced by the European Union. The threat of entry seemed to be moderate in the industry

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International and global business 6

due to less of regulation, but at the same time recovering economy makes the foreign players

dicey about entering the France market (Rothaermel, 2015). Another reason which makes the

threat of entry low is High initial investment, capability to distribute funds in an ailing

economy and skilled manpower.

The Bargaining power of suppliers

Four banks of France feature amongst the top 20 banks of the European Union and hence

European central banks pay good attention towards the need of French banks. Rise in

investment avenues, growing demand of SME’s and other industrial requirements, offshore

operation and the positive economic outlook make the industry attractive and increases the

bargaining power of the suppliers (Dalken, 2014).

Bargaining power of customers

As mentioned earlier in the report, SME sector is leading the lending charts of France

banking industry; the sector is quickly flooding money in their respective industry to grow

further. There is billions of Euros which is outstanding in the SME sector, but the

government is keen on pushing the reforms and hence giving out the money to business

investments. The switching cost is low for customers and growth in banking technology has

made it easier for them to carry out the business transaction (Fabbri & Klapper, 2016). Hence

it can be said that the bargaining power of customers is high.

Threat of Substitutes

Threat of substitutes in case of banking sector is very limited, because one of the most

fundamental banking reformed turned the entire merchant and the commercial banks as one

in France. Moreover there is little threat from the investors and NBFC, but as mentioned its

very limited threat. Moreover some of the banking functions like insurance, mutual funds,

withdrawals, fixed security are available only with the mainstream banks. Thus the threat of

substitutes is very low (Schaner, 2017).

Competitive Rivalry

6 of the top largest banks of France like BNP Paribas, Credit Agricole,Societe Generale

features in the top banks of the entire EU. In the year 2016 these banks earned an income of

€145.7 Billion. Apart from these 10 banks, other are very small. The competitive rivalry is

due to less of regulation, but at the same time recovering economy makes the foreign players

dicey about entering the France market (Rothaermel, 2015). Another reason which makes the

threat of entry low is High initial investment, capability to distribute funds in an ailing

economy and skilled manpower.

The Bargaining power of suppliers

Four banks of France feature amongst the top 20 banks of the European Union and hence

European central banks pay good attention towards the need of French banks. Rise in

investment avenues, growing demand of SME’s and other industrial requirements, offshore

operation and the positive economic outlook make the industry attractive and increases the

bargaining power of the suppliers (Dalken, 2014).

Bargaining power of customers

As mentioned earlier in the report, SME sector is leading the lending charts of France

banking industry; the sector is quickly flooding money in their respective industry to grow

further. There is billions of Euros which is outstanding in the SME sector, but the

government is keen on pushing the reforms and hence giving out the money to business

investments. The switching cost is low for customers and growth in banking technology has

made it easier for them to carry out the business transaction (Fabbri & Klapper, 2016). Hence

it can be said that the bargaining power of customers is high.

Threat of Substitutes

Threat of substitutes in case of banking sector is very limited, because one of the most

fundamental banking reformed turned the entire merchant and the commercial banks as one

in France. Moreover there is little threat from the investors and NBFC, but as mentioned its

very limited threat. Moreover some of the banking functions like insurance, mutual funds,

withdrawals, fixed security are available only with the mainstream banks. Thus the threat of

substitutes is very low (Schaner, 2017).

Competitive Rivalry

6 of the top largest banks of France like BNP Paribas, Credit Agricole,Societe Generale

features in the top banks of the entire EU. In the year 2016 these banks earned an income of

€145.7 Billion. Apart from these 10 banks, other are very small. The competitive rivalry is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International and global business 7

moderate as there is no cut throat competition, but every player competes on providing better

services and products (Piercy, 2014).

France’s Trade Union

There are in all 5 trade unions in the banking sector, namely

Federation of workers in Banks & Assurance (FSBPA)

French Democratic Confederation of Labour

Work force in banks, affiliated to General confederation of Labour

Federation of Christian workers in banks

The trade unions in the sector compete for the members and look for their support in the

workplace to get a seat in the council. The rivalry as of now is not much but in couple of

years, it will surely get fierce (Lange, Ross & Vannicelli, 2016). A strong point of

competition among the union is in terms of the rights to be consulted on the formulation of

public policy and its implementation.

Recommendation for France

France with a GDP of 2.465 Trillion is fifth largest economy of the world. Despite the fact

that economy is growing back from its slow down a couple of years back, the NPA,

unsecured loans, outstanding loans et.al are excessively high in France. Moreover the sector

is dominated by the 6 major banks which have been in the industry for decades. Hence, in all

light of the evidence, France will not be a better market for expansion owing to the sluggish

growth in the economy and tendency of people to default on their loans. For NAB, the

expansion in France is not a feasible option considering the growth of the bank

Banking Industry in Korea

South Korean economy is showing some good resistance to the political and geopolitical

turmoil, the GDP grew by 2.2% year on year following a gain of 2.4% in the last quarter of

the year 2016.Further the sector is having a positive outlook owing to the rise in domestic

demand and rise in the investment are positive signs of growth (Kanagaretnam, Lobo &

Wang, 2015). Consumer spending is bound to increase, but high household debt burden will

moderate as there is no cut throat competition, but every player competes on providing better

services and products (Piercy, 2014).

France’s Trade Union

There are in all 5 trade unions in the banking sector, namely

Federation of workers in Banks & Assurance (FSBPA)

French Democratic Confederation of Labour

Work force in banks, affiliated to General confederation of Labour

Federation of Christian workers in banks

The trade unions in the sector compete for the members and look for their support in the

workplace to get a seat in the council. The rivalry as of now is not much but in couple of

years, it will surely get fierce (Lange, Ross & Vannicelli, 2016). A strong point of

competition among the union is in terms of the rights to be consulted on the formulation of

public policy and its implementation.

Recommendation for France

France with a GDP of 2.465 Trillion is fifth largest economy of the world. Despite the fact

that economy is growing back from its slow down a couple of years back, the NPA,

unsecured loans, outstanding loans et.al are excessively high in France. Moreover the sector

is dominated by the 6 major banks which have been in the industry for decades. Hence, in all

light of the evidence, France will not be a better market for expansion owing to the sluggish

growth in the economy and tendency of people to default on their loans. For NAB, the

expansion in France is not a feasible option considering the growth of the bank

Banking Industry in Korea

South Korean economy is showing some good resistance to the political and geopolitical

turmoil, the GDP grew by 2.2% year on year following a gain of 2.4% in the last quarter of

the year 2016.Further the sector is having a positive outlook owing to the rise in domestic

demand and rise in the investment are positive signs of growth (Kanagaretnam, Lobo &

Wang, 2015). Consumer spending is bound to increase, but high household debt burden will

International and global business 8

inhibit the growth. US & China are the biggest export destinations for Korea, and the export

outlook looks positive just opening up opportunities for the Korean banks. South Korean

industrial products and exports are on an upward trend and even the business sentiment n the

manufacturing sector is showing signs of improvement, a very promising outlook for the

South Korean Banking sector. Service sector in South Korea plays an important role and

provides for 60% of the GDP and 70% of the workforce employed.

Korea’s banking system consists of banking and non-banking financial institutions. Financial

services commission and the Financial Supervisory Service are the bodies responsible for

supervision and examination of all banks, including both the specialized, government owned

banks, securities and the insurance companies.

Present Situation in Korea

Since 2014, the banking sector’s net foreign asset turned positive and since then it is

on an upward trend of improvement. It rose from US $100m in 2014 to US

$47.2billion in 2018.

The profitability of the South Korean banks has improved in recent times despite a

low interest rate and a mature market, though the banks have been facing growing

competition and regulatory pressures in the domestic market.

Arrival of 2 internet bank is creating a disruption and stir in the market, as mobile-

savvy consumers are smart and quickly adopting to smartphone banking.

Housing debt level is rising.

The earning of South Korean banks grew sharply in the first half of 2017 (US$ 7.1

Bn), 171% rise from the previous year.

The increase in the pure-play internet banks is posing a threat to the brick and mortar

banks.

K Bank & Kakao banks launched their commercial operations in the year 2017 and

have been making a splash ever since.

South Korean Banks are themselves looking for globalization in the emerging

markets; they are rapidly expanding into the Asian markets, due to increase from

domestic competition and the rise of internet banks (Park & Lee, 2017).

inhibit the growth. US & China are the biggest export destinations for Korea, and the export

outlook looks positive just opening up opportunities for the Korean banks. South Korean

industrial products and exports are on an upward trend and even the business sentiment n the

manufacturing sector is showing signs of improvement, a very promising outlook for the

South Korean Banking sector. Service sector in South Korea plays an important role and

provides for 60% of the GDP and 70% of the workforce employed.

Korea’s banking system consists of banking and non-banking financial institutions. Financial

services commission and the Financial Supervisory Service are the bodies responsible for

supervision and examination of all banks, including both the specialized, government owned

banks, securities and the insurance companies.

Present Situation in Korea

Since 2014, the banking sector’s net foreign asset turned positive and since then it is

on an upward trend of improvement. It rose from US $100m in 2014 to US

$47.2billion in 2018.

The profitability of the South Korean banks has improved in recent times despite a

low interest rate and a mature market, though the banks have been facing growing

competition and regulatory pressures in the domestic market.

Arrival of 2 internet bank is creating a disruption and stir in the market, as mobile-

savvy consumers are smart and quickly adopting to smartphone banking.

Housing debt level is rising.

The earning of South Korean banks grew sharply in the first half of 2017 (US$ 7.1

Bn), 171% rise from the previous year.

The increase in the pure-play internet banks is posing a threat to the brick and mortar

banks.

K Bank & Kakao banks launched their commercial operations in the year 2017 and

have been making a splash ever since.

South Korean Banks are themselves looking for globalization in the emerging

markets; they are rapidly expanding into the Asian markets, due to increase from

domestic competition and the rise of internet banks (Park & Lee, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International and global business 9

Porter 5 Force Model- Banking in Korea

Threat of New Entrant

As South Korean banks are looking for a way out for global expansion into developing or the

emerging economies around Asia, it leaves a fair chunk of market open to any new Entrant.

The cost of entry is particularly high, but South Korea as a banking sector has good scope for

growth. With the expansion if Internet banks like Kakao, the market looks more attractive

(Porter & Heppelmann, 2014). Government regulation and policies are strong; hence there is

moderate threat to entry.

Threat of Substitute Products

As long as people need money, insurance, financial products, fixed deposit security et al, the

threat of substitute products remain very low. Institution can lend money but they still don’t

have power to function like a regular bank thus reducing the threat of substitute products to

low.

Bargaining power of customers

South Korea is one nation whose population can be clearly identified with the service class.

The service class looks for faster services and solution in comparison to the business or

Porter 5 Force Model- Banking in Korea

Threat of New Entrant

As South Korean banks are looking for a way out for global expansion into developing or the

emerging economies around Asia, it leaves a fair chunk of market open to any new Entrant.

The cost of entry is particularly high, but South Korea as a banking sector has good scope for

growth. With the expansion if Internet banks like Kakao, the market looks more attractive

(Porter & Heppelmann, 2014). Government regulation and policies are strong; hence there is

moderate threat to entry.

Threat of Substitute Products

As long as people need money, insurance, financial products, fixed deposit security et al, the

threat of substitute products remain very low. Institution can lend money but they still don’t

have power to function like a regular bank thus reducing the threat of substitute products to

low.

Bargaining power of customers

South Korea is one nation whose population can be clearly identified with the service class.

The service class looks for faster services and solution in comparison to the business or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International and global business 10

agriculture class. Penetration of internet banking happened due to the need of speedy

services. The switching cost is relatively lower and the loyalty of customers towards the bank

is moderate, thus making the bargaining power of customers range from medium to high.

Bargaining power of suppliers

Bank of Korea is the central bank of South Korea and it has recently mentioned that it will

leave Won to operate according to the market forces and will not respond until Won gets too

big a currency and price destabilization happens. Bank has raised interest rate for the first

time in 6 years and is hopeful of solid advance growth due to controlled inflationary pressure

and a strong rising demand. It can be said that the bargaining power of suppliers is moderate

due to less intervention.

Competitive Rivalry

The competitive rivalry seems to be divided into click and mortar and the newly emerged

internet banks, this is leading the red blood competition in South Korea. K bank & Kakao are

making a splash in the market, kind of what happened when Apple launched iPhones. Also,

the new future is internet only banks because of a new legislation were pending. Hence, the

rivalry is high (Lee & Ryu, 2014).

Final Words on South Korea Banking Sector

The year 2014 saw struggle in South Korean Banking sector, with big names like HSBC and

Standard chartered withdrawing from the retail market, banking scandals and excess liquidity

were the times of troubled waters. Both the private and public sector banks were looking for

growth in the outside markets. Regional banks of Korea have shown some strong promise in

comparison to nationwide banks, experts believe that the regional firms are the ones who will

dominate the banking sector of Korea (Wee, 2017). Hence, NAB has an excellent opportunity

here, to merge with the regional bank of South Korea, get into the depth of internet banking

and make it easier for people to bank. South Korea despite all the scandals, issues, problems

it faced in the market still seems to be a profitable market. And NAB can go with the

acquisition growth strategy to expand its base, first in Korea and then to the neighbouring

parts of Asia.

agriculture class. Penetration of internet banking happened due to the need of speedy

services. The switching cost is relatively lower and the loyalty of customers towards the bank

is moderate, thus making the bargaining power of customers range from medium to high.

Bargaining power of suppliers

Bank of Korea is the central bank of South Korea and it has recently mentioned that it will

leave Won to operate according to the market forces and will not respond until Won gets too

big a currency and price destabilization happens. Bank has raised interest rate for the first

time in 6 years and is hopeful of solid advance growth due to controlled inflationary pressure

and a strong rising demand. It can be said that the bargaining power of suppliers is moderate

due to less intervention.

Competitive Rivalry

The competitive rivalry seems to be divided into click and mortar and the newly emerged

internet banks, this is leading the red blood competition in South Korea. K bank & Kakao are

making a splash in the market, kind of what happened when Apple launched iPhones. Also,

the new future is internet only banks because of a new legislation were pending. Hence, the

rivalry is high (Lee & Ryu, 2014).

Final Words on South Korea Banking Sector

The year 2014 saw struggle in South Korean Banking sector, with big names like HSBC and

Standard chartered withdrawing from the retail market, banking scandals and excess liquidity

were the times of troubled waters. Both the private and public sector banks were looking for

growth in the outside markets. Regional banks of Korea have shown some strong promise in

comparison to nationwide banks, experts believe that the regional firms are the ones who will

dominate the banking sector of Korea (Wee, 2017). Hence, NAB has an excellent opportunity

here, to merge with the regional bank of South Korea, get into the depth of internet banking

and make it easier for people to bank. South Korea despite all the scandals, issues, problems

it faced in the market still seems to be a profitable market. And NAB can go with the

acquisition growth strategy to expand its base, first in Korea and then to the neighbouring

parts of Asia.

International and global business 11

Banking Sector in Brazil

Presently the banking system in Brazil looks promising and is extremely efficient. Almost all

the banks have internet sites which are offering most to its entire product and services on

web, hence at technology front the banks seems to be doing good. There are numerous bank

branches all over the cities with at least one major bank in the entire city (Barbosa, Rocha &

Salazar, 2015). The five largest banks have almost 15000 branches spread through Brazil,

while the international operations are centralized at the bank’s headquarters either in Sao

Paolo or Rio de Janeiro. Overall, in the top 10 banks of Brazil, 3 are state owned( Banco do

Brasil, Caixa Economical Federal & Banrisul) five being private Brazilian bank’s (Bradesco,

BTG Pactul ) and two being foreign banks( Banco Santender from Spain and Citibank)

Present Situation of Banking Sector

Moody has recently revised Brazil banking sector outlook to stable owing to the

improvement in the economy.

The condition seems to have improved after 3 years of continuous recession, relieving

the pressure on both the bankers and the borrowers.

The economy is forecasted to grow by 1.5% in 2018 (Kanagaretnam, Lobo & Wang,

2017)

Bank profitability will improve as lenders will benefit from lower cost of funding and

having to provision for bank losses.

Credit demand to increase in the year 2018 due to falling lending rates.

Selic –the central bank of Brazil was predicted to be at 8% in 2018 owing to good

credit growth.

Banks seem to profit due to less of political noise.

Forecast for credit growth, -1.1% in 2017, 6.7 % in 2018 and 9.8% in 2019.

The banks are looking to increase their credit growth and take advantage of lower net

interest margins.

Banking Sector in Brazil

Presently the banking system in Brazil looks promising and is extremely efficient. Almost all

the banks have internet sites which are offering most to its entire product and services on

web, hence at technology front the banks seems to be doing good. There are numerous bank

branches all over the cities with at least one major bank in the entire city (Barbosa, Rocha &

Salazar, 2015). The five largest banks have almost 15000 branches spread through Brazil,

while the international operations are centralized at the bank’s headquarters either in Sao

Paolo or Rio de Janeiro. Overall, in the top 10 banks of Brazil, 3 are state owned( Banco do

Brasil, Caixa Economical Federal & Banrisul) five being private Brazilian bank’s (Bradesco,

BTG Pactul ) and two being foreign banks( Banco Santender from Spain and Citibank)

Present Situation of Banking Sector

Moody has recently revised Brazil banking sector outlook to stable owing to the

improvement in the economy.

The condition seems to have improved after 3 years of continuous recession, relieving

the pressure on both the bankers and the borrowers.

The economy is forecasted to grow by 1.5% in 2018 (Kanagaretnam, Lobo & Wang,

2017)

Bank profitability will improve as lenders will benefit from lower cost of funding and

having to provision for bank losses.

Credit demand to increase in the year 2018 due to falling lending rates.

Selic –the central bank of Brazil was predicted to be at 8% in 2018 owing to good

credit growth.

Banks seem to profit due to less of political noise.

Forecast for credit growth, -1.1% in 2017, 6.7 % in 2018 and 9.8% in 2019.

The banks are looking to increase their credit growth and take advantage of lower net

interest margins.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.