Finance for Strategic Managers: Comprehensive Analysis Report

VerifiedAdded on 2023/01/06

|22

|5820

|50

Report

AI Summary

This report provides a comprehensive analysis of finance for strategic managers, focusing on the importance of financial information, business risks, and financial statements. It delves into the significance of financial data for business decisions, including investment and lending. The report explores business risks such as market risk and credit risk, and examines the purpose, structure, and content of published accounts, using Tesco plc as an example. It covers the interpretation of financial accounts, including income statements and balance sheets, and calculates financial ratios for strategic decision-making. The report distinguishes between long and short-term financial requirements, compares sources of finance, and examines cash flow management techniques. Finally, it explores different ownership structures and methods for appraising strategic capital or investment projects, providing a complete overview of the financial aspects relevant to strategic management.

Finance for Strategic

Managers

Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

ACTIVITY 1...............................................................................................................................................3

1. Why financial information is needed in business.................................................................................3

2. Business risks related to financial decisions........................................................................................4

3. Summary of the financial information for business decisions..............................................................5

ACTIVITY 2...............................................................................................................................................6

1. Explanation of the purpose, structure and content of published accounts............................................6

2. Interpretation of the financial accounts in these accounts....................................................................7

3. Calculation of financial ratios and how support strategic decision making........................................12

ACTIVITY 3.............................................................................................................................................13

Distinguishes between long and short-term financial requirements for businesses................................13

Comparing the sources of long and short term finance for businesses...................................................15

Examination of cash flow management techniques and an assessment of why the management of cash

flow is so important...............................................................................................................................16

ACTIVITY 4.............................................................................................................................................17

Different ownership structure and compare and contrast of roles & accountability of owners and

managers in making decision.................................................................................................................17

Evaluation of methods for appraising strategic capital or investment projects......................................19

CONCLUSION.........................................................................................................................................20

REFERENCES..........................................................................................................................................21

INTRODUCTION.......................................................................................................................................3

ACTIVITY 1...............................................................................................................................................3

1. Why financial information is needed in business.................................................................................3

2. Business risks related to financial decisions........................................................................................4

3. Summary of the financial information for business decisions..............................................................5

ACTIVITY 2...............................................................................................................................................6

1. Explanation of the purpose, structure and content of published accounts............................................6

2. Interpretation of the financial accounts in these accounts....................................................................7

3. Calculation of financial ratios and how support strategic decision making........................................12

ACTIVITY 3.............................................................................................................................................13

Distinguishes between long and short-term financial requirements for businesses................................13

Comparing the sources of long and short term finance for businesses...................................................15

Examination of cash flow management techniques and an assessment of why the management of cash

flow is so important...............................................................................................................................16

ACTIVITY 4.............................................................................................................................................17

Different ownership structure and compare and contrast of roles & accountability of owners and

managers in making decision.................................................................................................................17

Evaluation of methods for appraising strategic capital or investment projects......................................19

CONCLUSION.........................................................................................................................................20

REFERENCES..........................................................................................................................................21

INTRODUCTION

Finance is major aspects for business managers in attempt to take effective and corrective

actions. There are number of approaches and strategies such as ratio analysis, financial statement

interpretation and many others in attempt to take reasonable decisions. Essentially, the key

aspect that must be recognized by executives is in each form of organization is finance (Bentley,

Omer and Sharp, 2013). The project study is focused on family company that has been

established by a fresh member and needs to acquire crucial financial skills knowledge such that

resources could be employed most effectively. The study is divided into four major activities; the

first one contains detailed information regarding importance of business's financial data; while

second activity focuses on analyzing of company's financial statements. The third one activity is

concerned with analysis of longer- and shorter-term finance for a corporation or business.

In later part of study, appropriate strategies have been applied towards investment projects.

ACTIVITY 1

1. Why financial information is needed in business.

Using different forms of statements like income statements, cash-flows, financial position

etc., and financial information are received. For managers, these financial information are very

critical to take corrective measures. Following, the significance of fiscal information are stated as

follows:

In attempt to determine the financial performance of businesses, financial information

is advantageous.

These types of data could be considered as a foundation for taking longer-term decisions, such as

taking large investment opportunities by using accessible threat and returns corporate financial

data (Collins, Pasewark and Riley, 2012).

Financial information is important as it offers significant information regarding the sustainability

of business accounting and reporting.

Financial data helps companies make better financial decisions as they highlight the major ROI

(return on investment) components of the company.

Finance is major aspects for business managers in attempt to take effective and corrective

actions. There are number of approaches and strategies such as ratio analysis, financial statement

interpretation and many others in attempt to take reasonable decisions. Essentially, the key

aspect that must be recognized by executives is in each form of organization is finance (Bentley,

Omer and Sharp, 2013). The project study is focused on family company that has been

established by a fresh member and needs to acquire crucial financial skills knowledge such that

resources could be employed most effectively. The study is divided into four major activities; the

first one contains detailed information regarding importance of business's financial data; while

second activity focuses on analyzing of company's financial statements. The third one activity is

concerned with analysis of longer- and shorter-term finance for a corporation or business.

In later part of study, appropriate strategies have been applied towards investment projects.

ACTIVITY 1

1. Why financial information is needed in business.

Using different forms of statements like income statements, cash-flows, financial position

etc., and financial information are received. For managers, these financial information are very

critical to take corrective measures. Following, the significance of fiscal information are stated as

follows:

In attempt to determine the financial performance of businesses, financial information

is advantageous.

These types of data could be considered as a foundation for taking longer-term decisions, such as

taking large investment opportunities by using accessible threat and returns corporate financial

data (Collins, Pasewark and Riley, 2012).

Financial information is important as it offers significant information regarding the sustainability

of business accounting and reporting.

Financial data helps companies make better financial decisions as they highlight the major ROI

(return on investment) components of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial information important for organizations to comprehend the areas where changes are

deemed necessary.

These are therefore several main significance of business's financial information as well as, in

the sense of family business stated above, they need to comprehend this significance in business.

When they are conscious of the significance of business's financial information, effective use

of financial assets and other resources available would be conceivable for them.

2. Business risks related to financial decisions.

Risk is present in any commercial operation, and successful risk management is integral

part of the operation of a sustainable firm. Business management includes varying levels of risk

mitigation. Any risks could be managed explicitly by careful monitoring. In the scenario of

finance feild, there are distinct types of risks that have a massive effect on the functioning of the

present state of businesses. These types of risks are evolving in businesses due to inaccurate

financial choices. Some typical financial risks in business context are described below:

Market risk-: These risk involves a detrimental change in the conditions of the setting

wherein the organisation works. One example of competitive market risk is increasing trend of

clients to purchase online. This component of market risk posed the most serious hurdles to

traditional retail businesses. Firms which have been prepared to make the necessary adjustments

to encourage the online shopping populace have been functioning and seen a significant rise in

revenues, while businesses which have been late to respond or have made lacklustre choices in

their response to evolving market have declined enormously. In the scenario of respective family

firms, this sort of risk may arise if they spend in project and market conditions vary considerably

owing to any global epidemic or natural catastrophe (Council and Britain, 2015).

Credit risk- By increasing customer credits, organisational credit risk could inflict. It can

also refer to credit risk of enterprise itself on its vendors. A business accepts credit risk by

providing its customers the means to buy financing, due to possibility that the customer can fail

to obtain reimbursement. A company must uphold its own loan obligations by ensuring that it

currently has adequate working capital to repay its overdue debts. Alternatively, the suppliers

could either avoid giving loan payments to business enterprise or even completely resist doing

deemed necessary.

These are therefore several main significance of business's financial information as well as, in

the sense of family business stated above, they need to comprehend this significance in business.

When they are conscious of the significance of business's financial information, effective use

of financial assets and other resources available would be conceivable for them.

2. Business risks related to financial decisions.

Risk is present in any commercial operation, and successful risk management is integral

part of the operation of a sustainable firm. Business management includes varying levels of risk

mitigation. Any risks could be managed explicitly by careful monitoring. In the scenario of

finance feild, there are distinct types of risks that have a massive effect on the functioning of the

present state of businesses. These types of risks are evolving in businesses due to inaccurate

financial choices. Some typical financial risks in business context are described below:

Market risk-: These risk involves a detrimental change in the conditions of the setting

wherein the organisation works. One example of competitive market risk is increasing trend of

clients to purchase online. This component of market risk posed the most serious hurdles to

traditional retail businesses. Firms which have been prepared to make the necessary adjustments

to encourage the online shopping populace have been functioning and seen a significant rise in

revenues, while businesses which have been late to respond or have made lacklustre choices in

their response to evolving market have declined enormously. In the scenario of respective family

firms, this sort of risk may arise if they spend in project and market conditions vary considerably

owing to any global epidemic or natural catastrophe (Council and Britain, 2015).

Credit risk- By increasing customer credits, organisational credit risk could inflict. It can

also refer to credit risk of enterprise itself on its vendors. A business accepts credit risk by

providing its customers the means to buy financing, due to possibility that the customer can fail

to obtain reimbursement. A company must uphold its own loan obligations by ensuring that it

currently has adequate working capital to repay its overdue debts. Alternatively, the suppliers

could either avoid giving loan payments to business enterprise or even completely resist doing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

enterprise with the entity. For example, when the respective family firm sells products on

credits to clients as well as their buyers fails to meet payments, they can experience such risk.

3. Summary of the financial information for business decisions.

Financial data serves a critical function in getting it simpler for companies to monitor

all financial outcomes. It is a system wherein the business records and discloses the parts of

financial data which go through and outs of its organisational processes, enabling both

organisational executives and external stakeholders and investors to evaluate the success of the

organisation and make knowledgeable decisions. Financial information serves to make strategic

decisions in the following way:

It provides investors with a structure for determining and analyzing the fiscal sustainability of

securities offering firms.

It helps lenders to assess the financial health, viability and credit risk of firms.

It helps companies to make decisions about how to allocate scarce resources, together with its

related, financial reporting (Fu, Kraft and Zhang, 2012).

In addition to these features, financial information adds to the decision-making of these kinds as:

Investing decisions- Different investors as well as potential investors employ fiscal information

to construct presumptions on a company's sustainability and financial creditworthiness. It allows

them to establish trade goals to determine not whether market value is fairly priced. Stockholders

do not even have information regarding the historical, current and future fiscal sustainability of

stocks and bonds, but through financial information this is possible to carry out a number of

analyses (Council, 2014).

Lending decisions – While making lending sum, the lenders simply wants to determine how

much risk is involved which can be generated by evaluating the fiscal information of company.

When this magnitude of threat is determined through financial information, lenders would also

be allowed to evaluate how much it will be lent and with what cost to leverage.

credits to clients as well as their buyers fails to meet payments, they can experience such risk.

3. Summary of the financial information for business decisions.

Financial data serves a critical function in getting it simpler for companies to monitor

all financial outcomes. It is a system wherein the business records and discloses the parts of

financial data which go through and outs of its organisational processes, enabling both

organisational executives and external stakeholders and investors to evaluate the success of the

organisation and make knowledgeable decisions. Financial information serves to make strategic

decisions in the following way:

It provides investors with a structure for determining and analyzing the fiscal sustainability of

securities offering firms.

It helps lenders to assess the financial health, viability and credit risk of firms.

It helps companies to make decisions about how to allocate scarce resources, together with its

related, financial reporting (Fu, Kraft and Zhang, 2012).

In addition to these features, financial information adds to the decision-making of these kinds as:

Investing decisions- Different investors as well as potential investors employ fiscal information

to construct presumptions on a company's sustainability and financial creditworthiness. It allows

them to establish trade goals to determine not whether market value is fairly priced. Stockholders

do not even have information regarding the historical, current and future fiscal sustainability of

stocks and bonds, but through financial information this is possible to carry out a number of

analyses (Council, 2014).

Lending decisions – While making lending sum, the lenders simply wants to determine how

much risk is involved which can be generated by evaluating the fiscal information of company.

When this magnitude of threat is determined through financial information, lenders would also

be allowed to evaluate how much it will be lent and with what cost to leverage.

ACTIVITY 2

1. Explanation of the purpose, structure and content of published accounts

In this portion of the project study, the financial statements and other relevant reports of

company Tesco plc have been considered as an illustration.

1. Purpose, structure and content of published accounts

In corporations, three types of accounts/reports are compiled, which are the income

statement, company's balance sheet and the cash flows statement. All these hasva a basic

purpose as well as structure as outlined below in following manner:

Purpose of compiling income statement: The predominant intent of

framing income statement is to providing stakeholders with details on the

company's profit results and operating results, as well as to offer detailed insights

into company's internal evaluations between various businesses and sectors. The

purpose of a company is to produce profits. Business income statement indicates

whether or not corporation is making a profit. It pays for half of the company's

sales and deducts all its expenditures. What's taken is profit or losses.

Management must understand how their company works and whether it is

sustainable. Managers employ this to assess the gain and cost results

of businesses.

Purpose of framing a balance sheet-The aim of framing balance sheet is to report

the financial state of the corporation from a specific point in period. Along with

the amounts invested in the business (common stock), the declaration shows

whatever the entity has (equity) or even how much they owes (capital).

When balance sheets are combined together over a number of previous years, this

information is more essential such that trends could be seen in various items

listed.

Purpose of preparing Cash Flows Statement- The main intention

of preparing Cash Flows Statement is to include information of all cash in-flows,

cash payouts and net monetary variation resulting from the activities, acquisitions

and funding of a company during the year. The cash flow statement employs

1. Explanation of the purpose, structure and content of published accounts

In this portion of the project study, the financial statements and other relevant reports of

company Tesco plc have been considered as an illustration.

1. Purpose, structure and content of published accounts

In corporations, three types of accounts/reports are compiled, which are the income

statement, company's balance sheet and the cash flows statement. All these hasva a basic

purpose as well as structure as outlined below in following manner:

Purpose of compiling income statement: The predominant intent of

framing income statement is to providing stakeholders with details on the

company's profit results and operating results, as well as to offer detailed insights

into company's internal evaluations between various businesses and sectors. The

purpose of a company is to produce profits. Business income statement indicates

whether or not corporation is making a profit. It pays for half of the company's

sales and deducts all its expenditures. What's taken is profit or losses.

Management must understand how their company works and whether it is

sustainable. Managers employ this to assess the gain and cost results

of businesses.

Purpose of framing a balance sheet-The aim of framing balance sheet is to report

the financial state of the corporation from a specific point in period. Along with

the amounts invested in the business (common stock), the declaration shows

whatever the entity has (equity) or even how much they owes (capital).

When balance sheets are combined together over a number of previous years, this

information is more essential such that trends could be seen in various items

listed.

Purpose of preparing Cash Flows Statement- The main intention

of preparing Cash Flows Statement is to include information of all cash in-flows,

cash payouts and net monetary variation resulting from the activities, acquisitions

and funding of a company during the year. The cash flow statement employs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cash-based accounting rather than accrual-based accounting that is being used by

other businesses on balance sheet and income statements. That's also critical

because a corporation may accumulate accounting profits but may not necessarily

collect cash. It might result in gains and taxes owed but would not have the means

to remain solvent. Cash inflows as well as cash outflows stated in cash

flows statement are subdivided into money outflows through operations,

investments and funding. These information offer insights into liquidity with

solvency, and also the capacity of companies to fulfill potential capital and

development requirements.

2. Interpretation of the financial accounts in these accounts

In finance and economics, a financial account is a part of the balance of trade of a

business that covers company charges or liabilities, especially with respect to financial assets.

Capital expenditure, investment spending and productive resources, divided by industry, are

elements of the financial account. As reported in the balance of payments of a corporation, non-

residents' complaints made on the financial resources of citizens are liabilities, while residents'

complaints levied towards non-residents are assets (Kunhibava, Ling and Ruslan, 2018).

The financial account is a reporting tool for company asset change of ownership and is

made up of two sub-accounts. Household ownership of foreign properties, including such

international deposit accounts and shares in foreign firms, is included in the first subaccount. The

following sub-account involves foreign ownership of domestic properties, such as the acquisition

by foreign interests of treasury securities or loans issued by foreign entities to financial

institutions. There are mentioned three types of financial accounts which are prepare every type

of company to analysis the profitability and financial performance of the business such as:

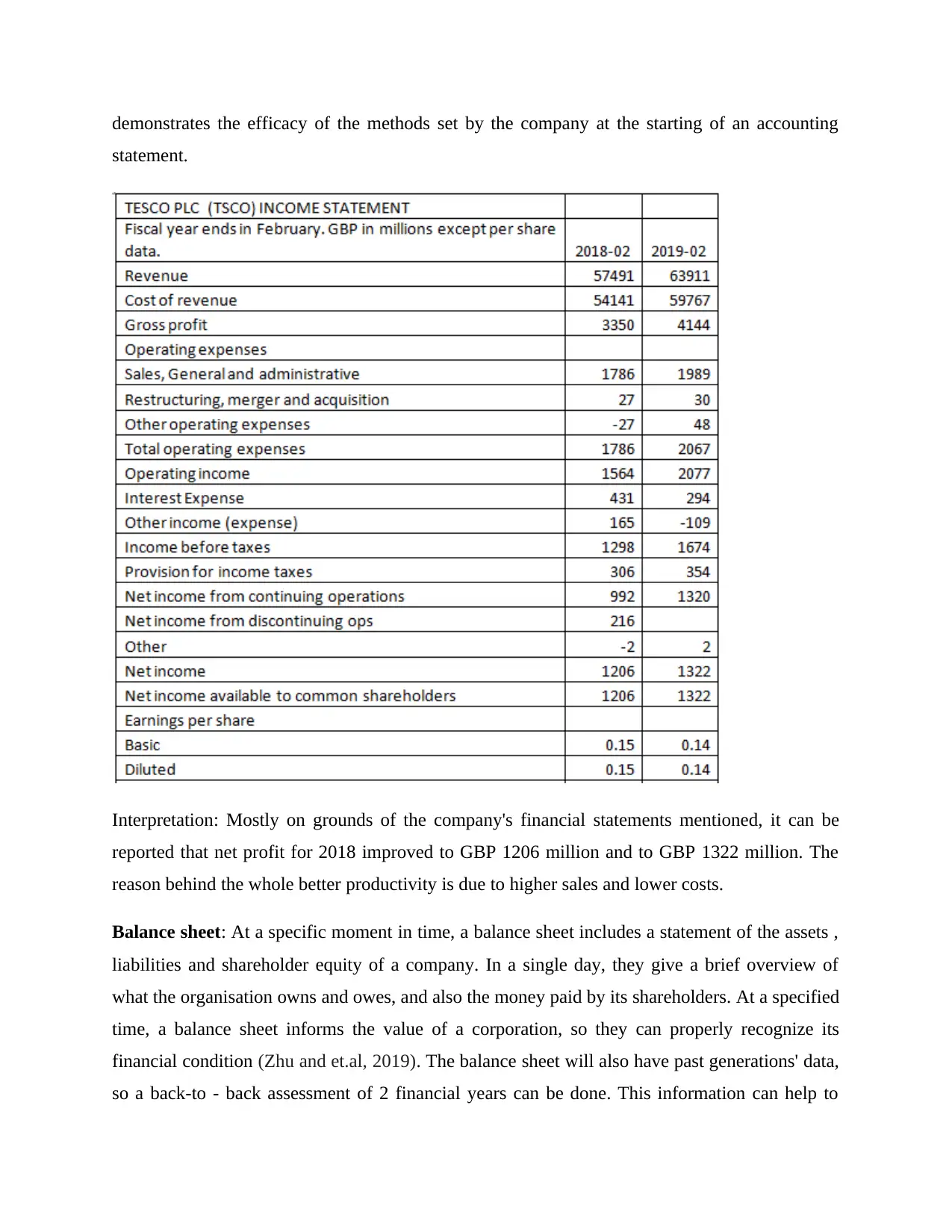

Income statement: One of three main financial statements used only to evaluate the profitability

and financial efficiency of a business is the income statement. The revenue statement

summarizes the revenues and expenditures produced out over life of the agreement by the

business. The income statement is often referred to as a statement of profit and loss (P&L),

statement of profits, statement of operations or statement of sales (Berns, Figueroa-Armijos, da

Motta Veiga and Dunne, 2020). An income statement helps enterprises make the decision either

through creating value, significantly reducing, or even both, they can create income. It also

other businesses on balance sheet and income statements. That's also critical

because a corporation may accumulate accounting profits but may not necessarily

collect cash. It might result in gains and taxes owed but would not have the means

to remain solvent. Cash inflows as well as cash outflows stated in cash

flows statement are subdivided into money outflows through operations,

investments and funding. These information offer insights into liquidity with

solvency, and also the capacity of companies to fulfill potential capital and

development requirements.

2. Interpretation of the financial accounts in these accounts

In finance and economics, a financial account is a part of the balance of trade of a

business that covers company charges or liabilities, especially with respect to financial assets.

Capital expenditure, investment spending and productive resources, divided by industry, are

elements of the financial account. As reported in the balance of payments of a corporation, non-

residents' complaints made on the financial resources of citizens are liabilities, while residents'

complaints levied towards non-residents are assets (Kunhibava, Ling and Ruslan, 2018).

The financial account is a reporting tool for company asset change of ownership and is

made up of two sub-accounts. Household ownership of foreign properties, including such

international deposit accounts and shares in foreign firms, is included in the first subaccount. The

following sub-account involves foreign ownership of domestic properties, such as the acquisition

by foreign interests of treasury securities or loans issued by foreign entities to financial

institutions. There are mentioned three types of financial accounts which are prepare every type

of company to analysis the profitability and financial performance of the business such as:

Income statement: One of three main financial statements used only to evaluate the profitability

and financial efficiency of a business is the income statement. The revenue statement

summarizes the revenues and expenditures produced out over life of the agreement by the

business. The income statement is often referred to as a statement of profit and loss (P&L),

statement of profits, statement of operations or statement of sales (Berns, Figueroa-Armijos, da

Motta Veiga and Dunne, 2020). An income statement helps enterprises make the decision either

through creating value, significantly reducing, or even both, they can create income. It also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

demonstrates the efficacy of the methods set by the company at the starting of an accounting

statement.

Interpretation: Mostly on grounds of the company's financial statements mentioned, it can be

reported that net profit for 2018 improved to GBP 1206 million and to GBP 1322 million. The

reason behind the whole better productivity is due to higher sales and lower costs.

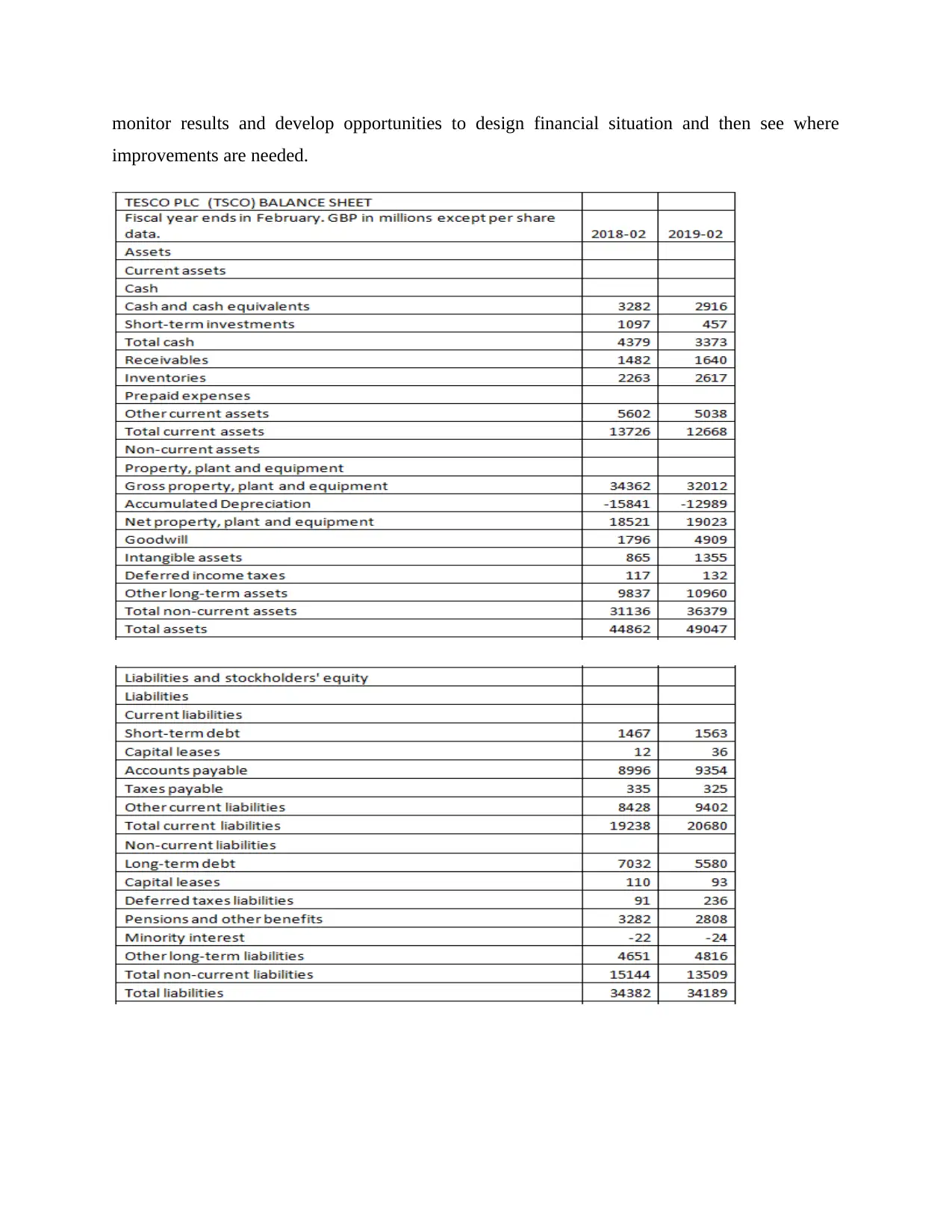

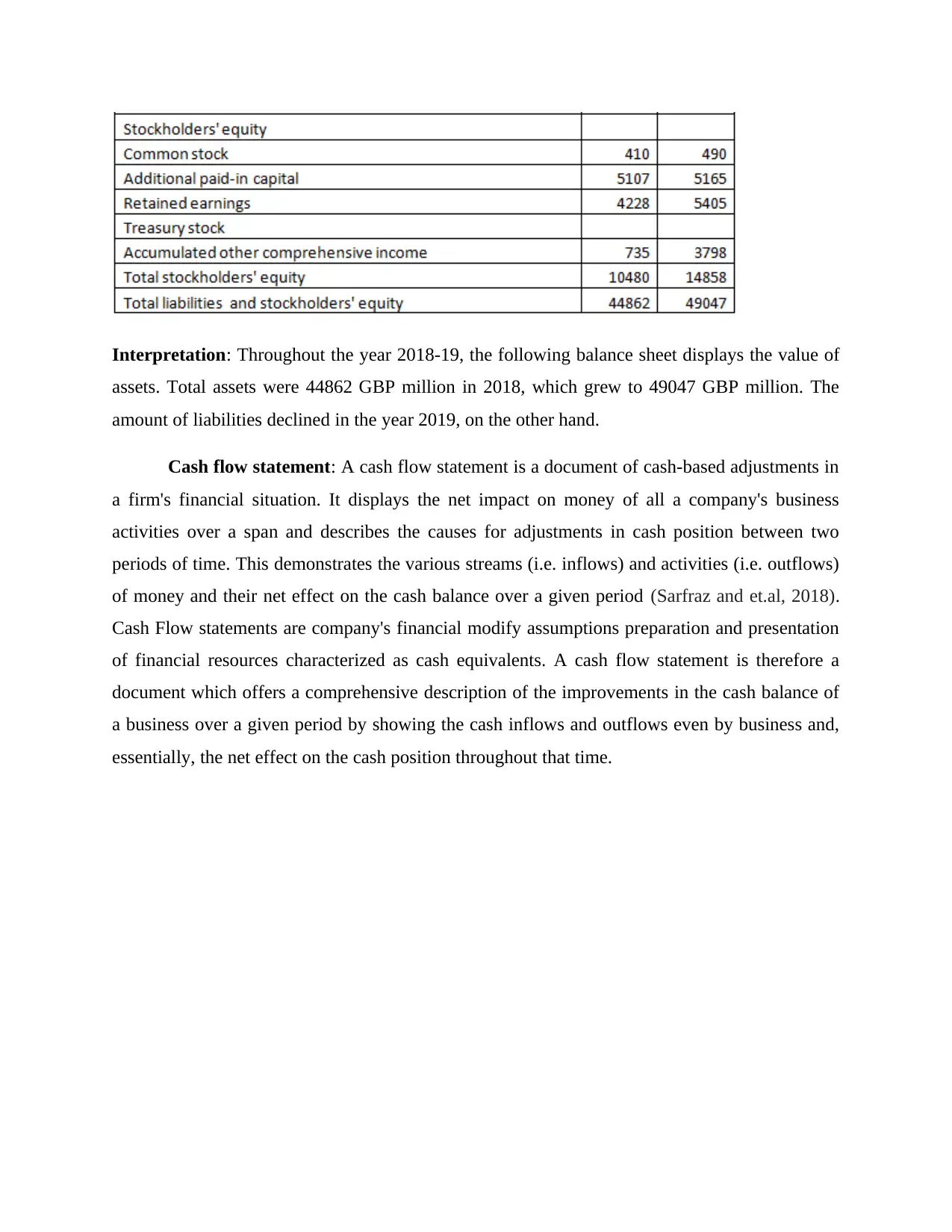

Balance sheet: At a specific moment in time, a balance sheet includes a statement of the assets ,

liabilities and shareholder equity of a company. In a single day, they give a brief overview of

what the organisation owns and owes, and also the money paid by its shareholders. At a specified

time, a balance sheet informs the value of a corporation, so they can properly recognize its

financial condition (Zhu and et.al, 2019). The balance sheet will also have past generations' data,

so a back-to - back assessment of 2 financial years can be done. This information can help to

statement.

Interpretation: Mostly on grounds of the company's financial statements mentioned, it can be

reported that net profit for 2018 improved to GBP 1206 million and to GBP 1322 million. The

reason behind the whole better productivity is due to higher sales and lower costs.

Balance sheet: At a specific moment in time, a balance sheet includes a statement of the assets ,

liabilities and shareholder equity of a company. In a single day, they give a brief overview of

what the organisation owns and owes, and also the money paid by its shareholders. At a specified

time, a balance sheet informs the value of a corporation, so they can properly recognize its

financial condition (Zhu and et.al, 2019). The balance sheet will also have past generations' data,

so a back-to - back assessment of 2 financial years can be done. This information can help to

monitor results and develop opportunities to design financial situation and then see where

improvements are needed.

improvements are needed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: Throughout the year 2018-19, the following balance sheet displays the value of

assets. Total assets were 44862 GBP million in 2018, which grew to 49047 GBP million. The

amount of liabilities declined in the year 2019, on the other hand.

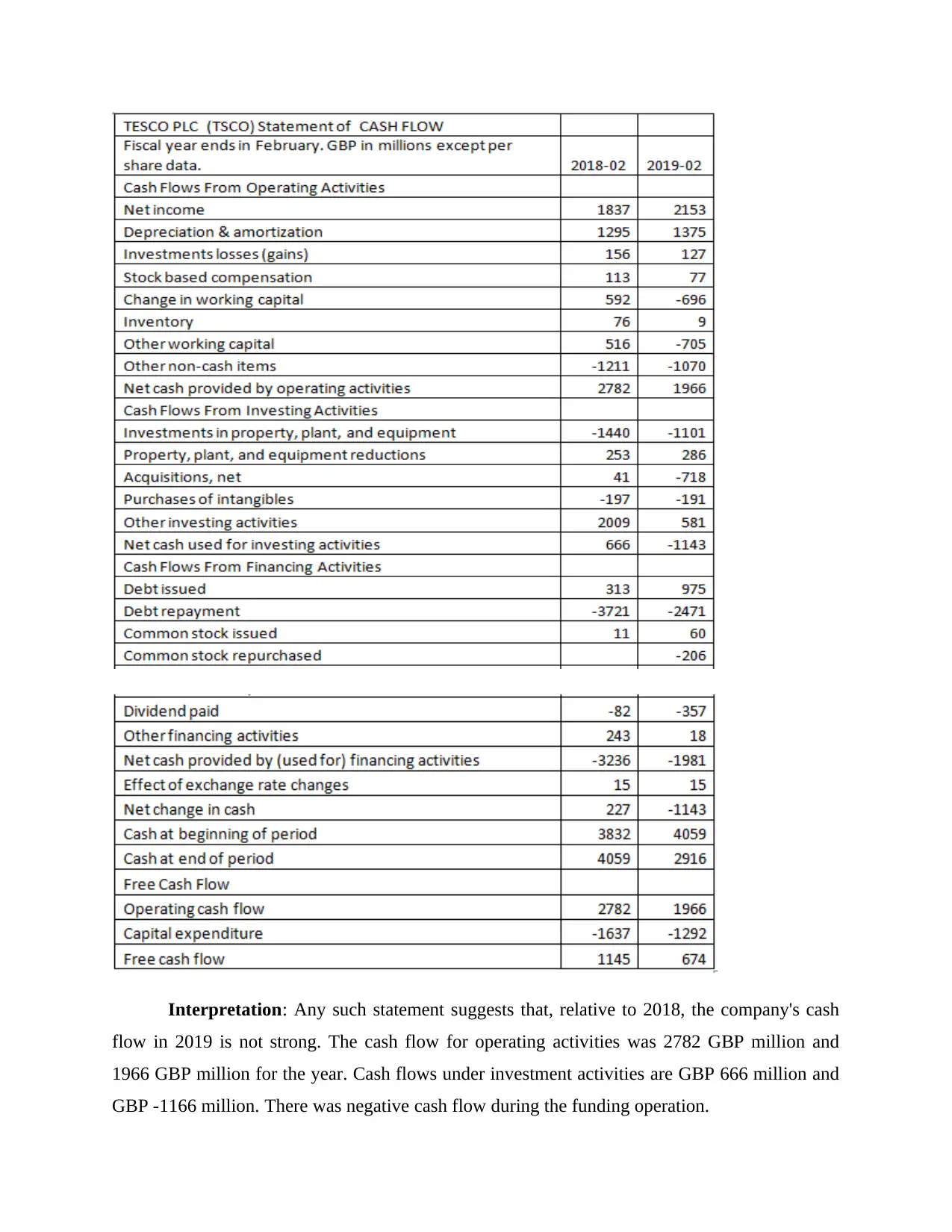

Cash flow statement: A cash flow statement is a document of cash-based adjustments in

a firm's financial situation. It displays the net impact on money of all a company's business

activities over a span and describes the causes for adjustments in cash position between two

periods of time. This demonstrates the various streams (i.e. inflows) and activities (i.e. outflows)

of money and their net effect on the cash balance over a given period (Sarfraz and et.al, 2018).

Cash Flow statements are company's financial modify assumptions preparation and presentation

of financial resources characterized as cash equivalents. A cash flow statement is therefore a

document which offers a comprehensive description of the improvements in the cash balance of

a business over a given period by showing the cash inflows and outflows even by business and,

essentially, the net effect on the cash position throughout that time.

assets. Total assets were 44862 GBP million in 2018, which grew to 49047 GBP million. The

amount of liabilities declined in the year 2019, on the other hand.

Cash flow statement: A cash flow statement is a document of cash-based adjustments in

a firm's financial situation. It displays the net impact on money of all a company's business

activities over a span and describes the causes for adjustments in cash position between two

periods of time. This demonstrates the various streams (i.e. inflows) and activities (i.e. outflows)

of money and their net effect on the cash balance over a given period (Sarfraz and et.al, 2018).

Cash Flow statements are company's financial modify assumptions preparation and presentation

of financial resources characterized as cash equivalents. A cash flow statement is therefore a

document which offers a comprehensive description of the improvements in the cash balance of

a business over a given period by showing the cash inflows and outflows even by business and,

essentially, the net effect on the cash position throughout that time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: Any such statement suggests that, relative to 2018, the company's cash

flow in 2019 is not strong. The cash flow for operating activities was 2782 GBP million and

1966 GBP million for the year. Cash flows under investment activities are GBP 666 million and

GBP -1166 million. There was negative cash flow during the funding operation.

flow in 2019 is not strong. The cash flow for operating activities was 2782 GBP million and

1966 GBP million for the year. Cash flows under investment activities are GBP 666 million and

GBP -1166 million. There was negative cash flow during the funding operation.

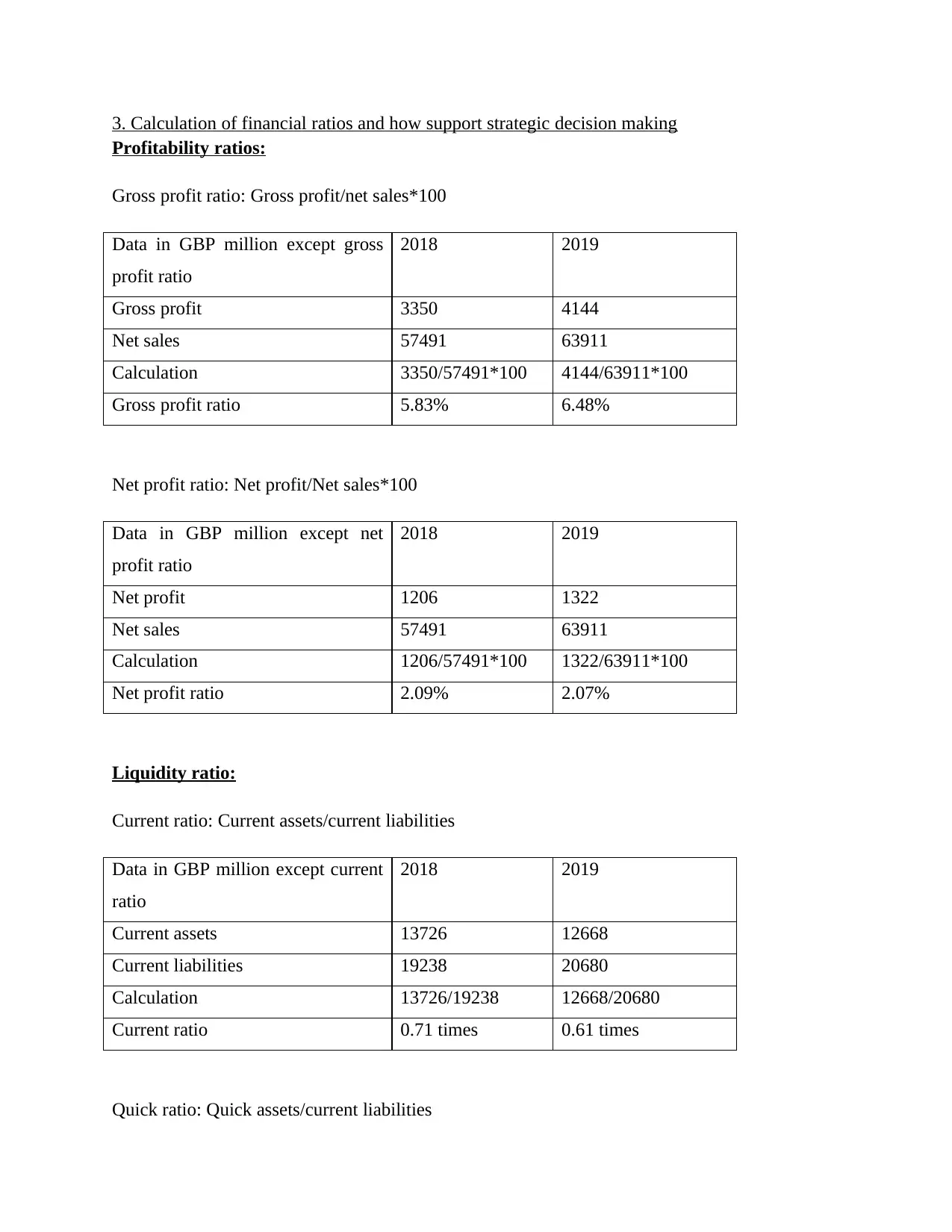

3. Calculation of financial ratios and how support strategic decision making

Profitability ratios:

Gross profit ratio: Gross profit/net sales*100

Data in GBP million except gross

profit ratio

2018 2019

Gross profit 3350 4144

Net sales 57491 63911

Calculation 3350/57491*100 4144/63911*100

Gross profit ratio 5.83% 6.48%

Net profit ratio: Net profit/Net sales*100

Data in GBP million except net

profit ratio

2018 2019

Net profit 1206 1322

Net sales 57491 63911

Calculation 1206/57491*100 1322/63911*100

Net profit ratio 2.09% 2.07%

Liquidity ratio:

Current ratio: Current assets/current liabilities

Data in GBP million except current

ratio

2018 2019

Current assets 13726 12668

Current liabilities 19238 20680

Calculation 13726/19238 12668/20680

Current ratio 0.71 times 0.61 times

Quick ratio: Quick assets/current liabilities

Profitability ratios:

Gross profit ratio: Gross profit/net sales*100

Data in GBP million except gross

profit ratio

2018 2019

Gross profit 3350 4144

Net sales 57491 63911

Calculation 3350/57491*100 4144/63911*100

Gross profit ratio 5.83% 6.48%

Net profit ratio: Net profit/Net sales*100

Data in GBP million except net

profit ratio

2018 2019

Net profit 1206 1322

Net sales 57491 63911

Calculation 1206/57491*100 1322/63911*100

Net profit ratio 2.09% 2.07%

Liquidity ratio:

Current ratio: Current assets/current liabilities

Data in GBP million except current

ratio

2018 2019

Current assets 13726 12668

Current liabilities 19238 20680

Calculation 13726/19238 12668/20680

Current ratio 0.71 times 0.61 times

Quick ratio: Quick assets/current liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.