Strategic Financial Management Report: Financial Analysis of Sainsbury

VerifiedAdded on 2020/06/06

|26

|7068

|146

Report

AI Summary

This report provides a comprehensive analysis of strategic financial management, focusing on the case of Sainsbury, a major UK supermarket chain. It begins by evaluating the risks associated with inadequate financial resources and explores various planning tools like budgeting and capital budgeting to mitigate these risks. The report then delves into an analysis of Sainsbury's financial statements, using ratio analysis to assess its financial viability and compare its performance to that of its competitor, Tesco. Key financial ratios such as profitability, liquidity, solvency, and efficiency ratios are examined. The report also assesses strategies for monitoring both tangible and intangible resources, and it explains the importance of cost in pricing strategies, suggesting improvements to existing costing systems. Finally, the report explores investment appraisal techniques and analyzes the viability of expansion plans through these techniques, alongside strategies for minimizing different types of financial risks. The report provides a detailed overview of Sainsbury's financial position, performance, and management strategies.

Strategic Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1. Evaluating the risks that can occur from inadequate resources along with the planning tools

for the same..................................................................................................................................3

2. Analyzing financial statements of Sainsbury to determine its financial viability...................5

3. Assessing strategies and tools that can be employed for monitoring both tangible and

intangible resources...................................................................................................................12

4. Explaining the importance of cost in pricing strategies and recommending improvements

for the exiting costing system....................................................................................................14

TASK 2..........................................................................................................................................14

1. Investment appraisal techniques............................................................................................14

2. Analyzing viability of expansion plan through investment appraisal techniques.................17

3. Different types of risk and strategies to minimise risks........................................................20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................24

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1. Evaluating the risks that can occur from inadequate resources along with the planning tools

for the same..................................................................................................................................3

2. Analyzing financial statements of Sainsbury to determine its financial viability...................5

3. Assessing strategies and tools that can be employed for monitoring both tangible and

intangible resources...................................................................................................................12

4. Explaining the importance of cost in pricing strategies and recommending improvements

for the exiting costing system....................................................................................................14

TASK 2..........................................................................................................................................14

1. Investment appraisal techniques............................................................................................14

2. Analyzing viability of expansion plan through investment appraisal techniques.................17

3. Different types of risk and strategies to minimise risks........................................................20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................24

INTRODUCTION

Strategic financial management is the process that lays high level of emphasis on the

attainment of long term organizational goals. In the present era, firms make focus on employing

the tool of strategic financial management which in turn facilitates specific planning pertaining

to the usage and management of organizational financial resources. Moreover, strategic planning

assists firm in making allocation of monetary resources according to goals and thereby helps in

generating high return as well as maximizing shareholder’s return. Such field of finance also

helps in assessing potential investment opportunities that available to business and thereby

ensures smooth functioning of business operations and functions.

For this project, Sainsbury, largest chain of supermarket in UK, has been selected. It

offers wide range of products or services to the customers at suitable prices. In this, the present

report will shed light on the tools & techniques that can be undertaken for the purpose of

planning and allocation of financial resources. Further, report also highlights the extent to which

financial position and performance of Sainsbury is good. It also depicts the manner in which

organization can monitor both tangible and intangible resources. Report will also provide deeper

insight about the way in which capital budgeting tools & techniques aid in decision making.

TASK 1

1. Evaluating the risks that can occur from inadequate resources along with the planning tools for

the same

Financial decisions that are undertaken by manager have significant impact on both

internal and external performance of an organization.

1. Strategic decision -

The strategic decision is taken to formulate future of the business in effective way so that

it may be able to beat competitors in effectual way. This is required so that organisation may

flourish in the best possible way. The strategic decision is taken and is really difficult to ascertain

and is affected by internal and external factors and as such, it is basically formulated with

objective of the capital expenditures, plant layout and many more which are examples of

Strategic financial management is the process that lays high level of emphasis on the

attainment of long term organizational goals. In the present era, firms make focus on employing

the tool of strategic financial management which in turn facilitates specific planning pertaining

to the usage and management of organizational financial resources. Moreover, strategic planning

assists firm in making allocation of monetary resources according to goals and thereby helps in

generating high return as well as maximizing shareholder’s return. Such field of finance also

helps in assessing potential investment opportunities that available to business and thereby

ensures smooth functioning of business operations and functions.

For this project, Sainsbury, largest chain of supermarket in UK, has been selected. It

offers wide range of products or services to the customers at suitable prices. In this, the present

report will shed light on the tools & techniques that can be undertaken for the purpose of

planning and allocation of financial resources. Further, report also highlights the extent to which

financial position and performance of Sainsbury is good. It also depicts the manner in which

organization can monitor both tangible and intangible resources. Report will also provide deeper

insight about the way in which capital budgeting tools & techniques aid in decision making.

TASK 1

1. Evaluating the risks that can occur from inadequate resources along with the planning tools for

the same

Financial decisions that are undertaken by manager have significant impact on both

internal and external performance of an organization.

1. Strategic decision -

The strategic decision is taken to formulate future of the business in effective way so that

it may be able to beat competitors in effectual way. This is required so that organisation may

flourish in the best possible way. The strategic decision is taken and is really difficult to ascertain

and is affected by internal and external factors and as such, it is basically formulated with

objective of the capital expenditures, plant layout and many more which are examples of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

strategic decision taken by organisation (Sofat and Hiro, 2015).

2. Basic decision -

The basic decisions are required to be taken by organisation which are much vital for it.

These are to be taken deliberately by organisation so that it may move ahead of the rivals quite

effectively. Thus, it involves plant location, channels of distribution and other basic decisions

which affect organisation's performance in the positive way. These decisions are taken by

organisation so that it may perform well in the market and as such, it may earn profit with

implementation of structured policies.

3. Policy decision -

Policy decision are taken by upper management or top management of the organisation to

take better and effective decisions. It affects entire organisation and as a result, it is able to

perform well by implementing well-structured policy decisions. It affects internal and external

factors as well. The policy decisions are taken which consists of financial structure, policies

related to marketing and maintaining effective organisation structure as well (Chandra, 2011).

These policy decisions form the basis of effective performance of the organisation and as such,

goals are achieved by taking enhanced decisions. The above three key resource decisions are to

be taken effectively by management so that organisation may flourish in the market with much

ease.

Occurrence of risk from inadequate resources

In the case of having inadequate resources Sainsbury plc would not become able to grab

profitable opportunities which will arise in near future. This in turn places direct impact

on organizational profitability and overall position.

Sainsbury plc will also face difficulty in investing money in R&D activity when the

situation of financial inadequacy exists. Now, innovative offering become key for success

which in turn assists in gaining competitive edge over others. Thus, if firm does not have

enough resources for research activity then there are no innovative and lack of

competitive edge (Hill, 2007).

Along with this, financial inadequacy also impacts expansion plan of business to a great

extent. Now, with the motive to widen customer base leading companies like Sainsbury

makes more focus on doing business at global level. Hence, in the absence of having

2. Basic decision -

The basic decisions are required to be taken by organisation which are much vital for it.

These are to be taken deliberately by organisation so that it may move ahead of the rivals quite

effectively. Thus, it involves plant location, channels of distribution and other basic decisions

which affect organisation's performance in the positive way. These decisions are taken by

organisation so that it may perform well in the market and as such, it may earn profit with

implementation of structured policies.

3. Policy decision -

Policy decision are taken by upper management or top management of the organisation to

take better and effective decisions. It affects entire organisation and as a result, it is able to

perform well by implementing well-structured policy decisions. It affects internal and external

factors as well. The policy decisions are taken which consists of financial structure, policies

related to marketing and maintaining effective organisation structure as well (Chandra, 2011).

These policy decisions form the basis of effective performance of the organisation and as such,

goals are achieved by taking enhanced decisions. The above three key resource decisions are to

be taken effectively by management so that organisation may flourish in the market with much

ease.

Occurrence of risk from inadequate resources

In the case of having inadequate resources Sainsbury plc would not become able to grab

profitable opportunities which will arise in near future. This in turn places direct impact

on organizational profitability and overall position.

Sainsbury plc will also face difficulty in investing money in R&D activity when the

situation of financial inadequacy exists. Now, innovative offering become key for success

which in turn assists in gaining competitive edge over others. Thus, if firm does not have

enough resources for research activity then there are no innovative and lack of

competitive edge (Hill, 2007).

Along with this, financial inadequacy also impacts expansion plan of business to a great

extent. Now, with the motive to widen customer base leading companies like Sainsbury

makes more focus on doing business at global level. Hence, in the absence of having

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

adequate financial resources Sainsbury would not become able to execute plan in relation

to expanding operations globally.

There are several tools and techniques which can be used for financial planning and

allocation of resources:

Budgeting: By undertaking budgeting tools and techniques such as incremental, ZBB,

ABB etc Sainsbury Plc can make optimum allocation of financial resources in different

business activities. Traditional technique such as ZBB lays high level of emphasis on

resource allocation as per the needs or requirement. According to zero base budgeting,

every list of item is clearly justified which in turn gives indication regarding optimal

financial allocation (Hofstede, 2013). Further, budgeting tool also helps in ascertaining

the position of surplus / deficit and helps in finding suitable ways that contributes in goal

attainment.

Budgetary control: For planning purpose, budgetary control tool is considered as good

which also helps in making suitable allocation of financial resources. Hence, by doing

comparison of actual results with standards firm can assess both deviations and

associated causes (Curry, 2013). Thus, by taking into account the outcome or analysis of

budgetary control business unit can develop competent plan for the upcoming time

period.

Capital budgeting: By employing capital budgeting tools such as payback, NPV, ARR

and IRR Tesco plc can do effectual planning. Moreover, methods of investment appraisal

help in determining project which prove to be more beneficial for them (Dada, Azim and

Ullah, 2014). In this way, by selecting suitable project firm can do suitable planning.

2. Analyzing financial statements of Sainsbury to determine its financial viability

Ratio analysis may be served as a financial tool that provides high level of assistance in

summarizing and evaluating financial statements of the firm. By using such tool firm can assess

the extent to which its performance is improved over the time frame (Benedict and Elliott, 2008).

Further, such technique also helps firm in evaluating its position over rival. In this, to ascertain

monetary position of Sainsbury in against to the rival firm Tesco, leading retail chain of UK, has

been considered. Hence, such technique is highly significant which in turn assist firm in

evaluating its performance and helps in developing competent framework.

to expanding operations globally.

There are several tools and techniques which can be used for financial planning and

allocation of resources:

Budgeting: By undertaking budgeting tools and techniques such as incremental, ZBB,

ABB etc Sainsbury Plc can make optimum allocation of financial resources in different

business activities. Traditional technique such as ZBB lays high level of emphasis on

resource allocation as per the needs or requirement. According to zero base budgeting,

every list of item is clearly justified which in turn gives indication regarding optimal

financial allocation (Hofstede, 2013). Further, budgeting tool also helps in ascertaining

the position of surplus / deficit and helps in finding suitable ways that contributes in goal

attainment.

Budgetary control: For planning purpose, budgetary control tool is considered as good

which also helps in making suitable allocation of financial resources. Hence, by doing

comparison of actual results with standards firm can assess both deviations and

associated causes (Curry, 2013). Thus, by taking into account the outcome or analysis of

budgetary control business unit can develop competent plan for the upcoming time

period.

Capital budgeting: By employing capital budgeting tools such as payback, NPV, ARR

and IRR Tesco plc can do effectual planning. Moreover, methods of investment appraisal

help in determining project which prove to be more beneficial for them (Dada, Azim and

Ullah, 2014). In this way, by selecting suitable project firm can do suitable planning.

2. Analyzing financial statements of Sainsbury to determine its financial viability

Ratio analysis may be served as a financial tool that provides high level of assistance in

summarizing and evaluating financial statements of the firm. By using such tool firm can assess

the extent to which its performance is improved over the time frame (Benedict and Elliott, 2008).

Further, such technique also helps firm in evaluating its position over rival. In this, to ascertain

monetary position of Sainsbury in against to the rival firm Tesco, leading retail chain of UK, has

been considered. Hence, such technique is highly significant which in turn assist firm in

evaluating its performance and helps in developing competent framework.

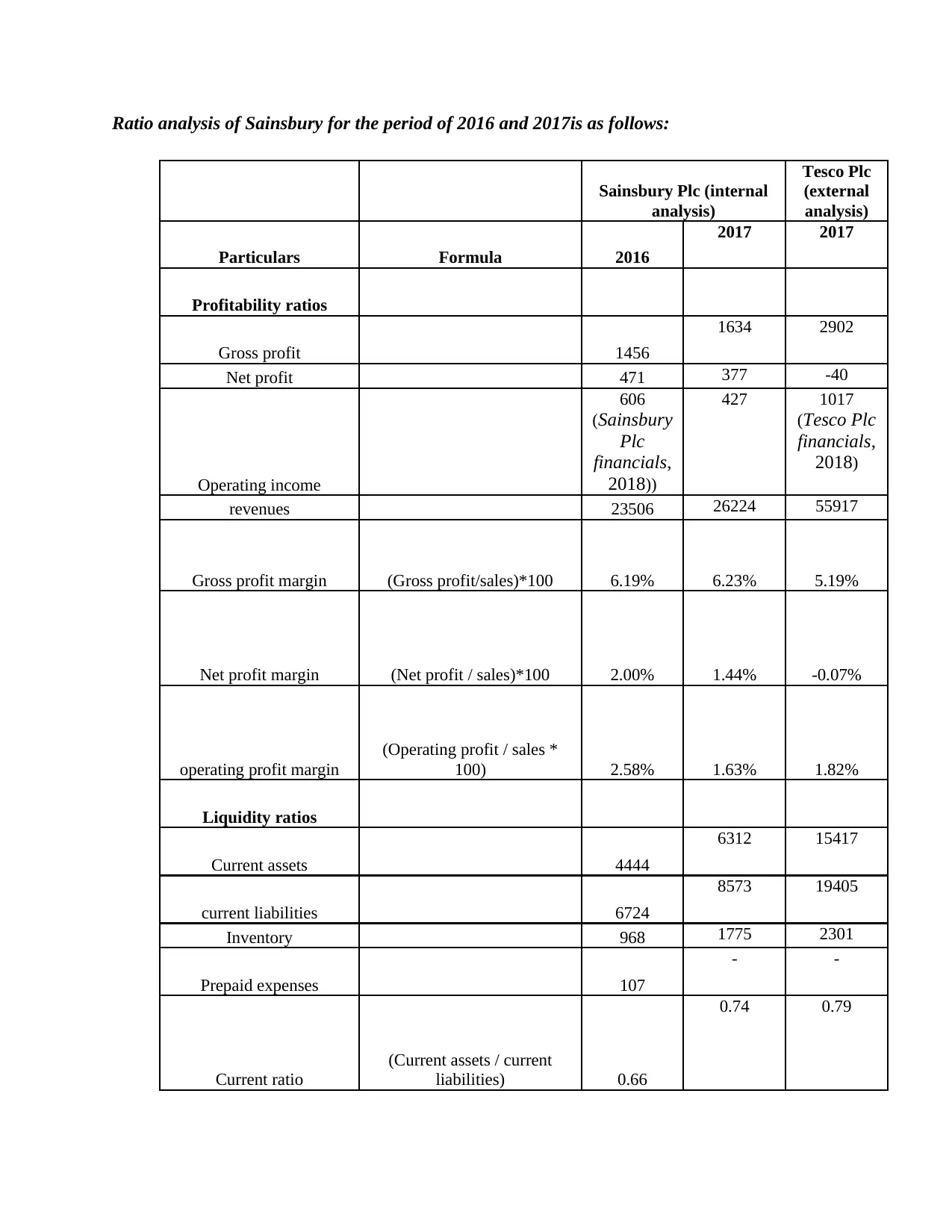

Ratio analysis of Sainsbury for the period of 2016 and 2017is as follows:

Sainsbury Plc (internal

analysis)

Tesco Plc

(external

analysis)

Particulars Formula 2016

2017 2017

Profitability ratios

Gross profit 1456

1634 2902

Net profit 471 377 -40

Operating income

606

(Sainsbury

Plc

financials,

2018))

427 1017

(Tesco Plc

financials,

2018)

revenues 23506 26224 55917

Gross profit margin (Gross profit/sales)*100 6.19% 6.23% 5.19%

Net profit margin (Net profit / sales)*100 2.00% 1.44% -0.07%

operating profit margin

(Operating profit / sales *

100) 2.58% 1.63% 1.82%

Liquidity ratios

Current assets 4444

6312 15417

current liabilities 6724

8573 19405

Inventory 968 1775 2301

Prepaid expenses 107

- -

Current ratio

(Current assets / current

liabilities) 0.66

0.74 0.79

Sainsbury Plc (internal

analysis)

Tesco Plc

(external

analysis)

Particulars Formula 2016

2017 2017

Profitability ratios

Gross profit 1456

1634 2902

Net profit 471 377 -40

Operating income

606

(Sainsbury

Plc

financials,

2018))

427 1017

(Tesco Plc

financials,

2018)

revenues 23506 26224 55917

Gross profit margin (Gross profit/sales)*100 6.19% 6.23% 5.19%

Net profit margin (Net profit / sales)*100 2.00% 1.44% -0.07%

operating profit margin

(Operating profit / sales *

100) 2.58% 1.63% 1.82%

Liquidity ratios

Current assets 4444

6312 15417

current liabilities 6724

8573 19405

Inventory 968 1775 2301

Prepaid expenses 107

- -

Current ratio

(Current assets / current

liabilities) 0.66

0.74 0.79

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

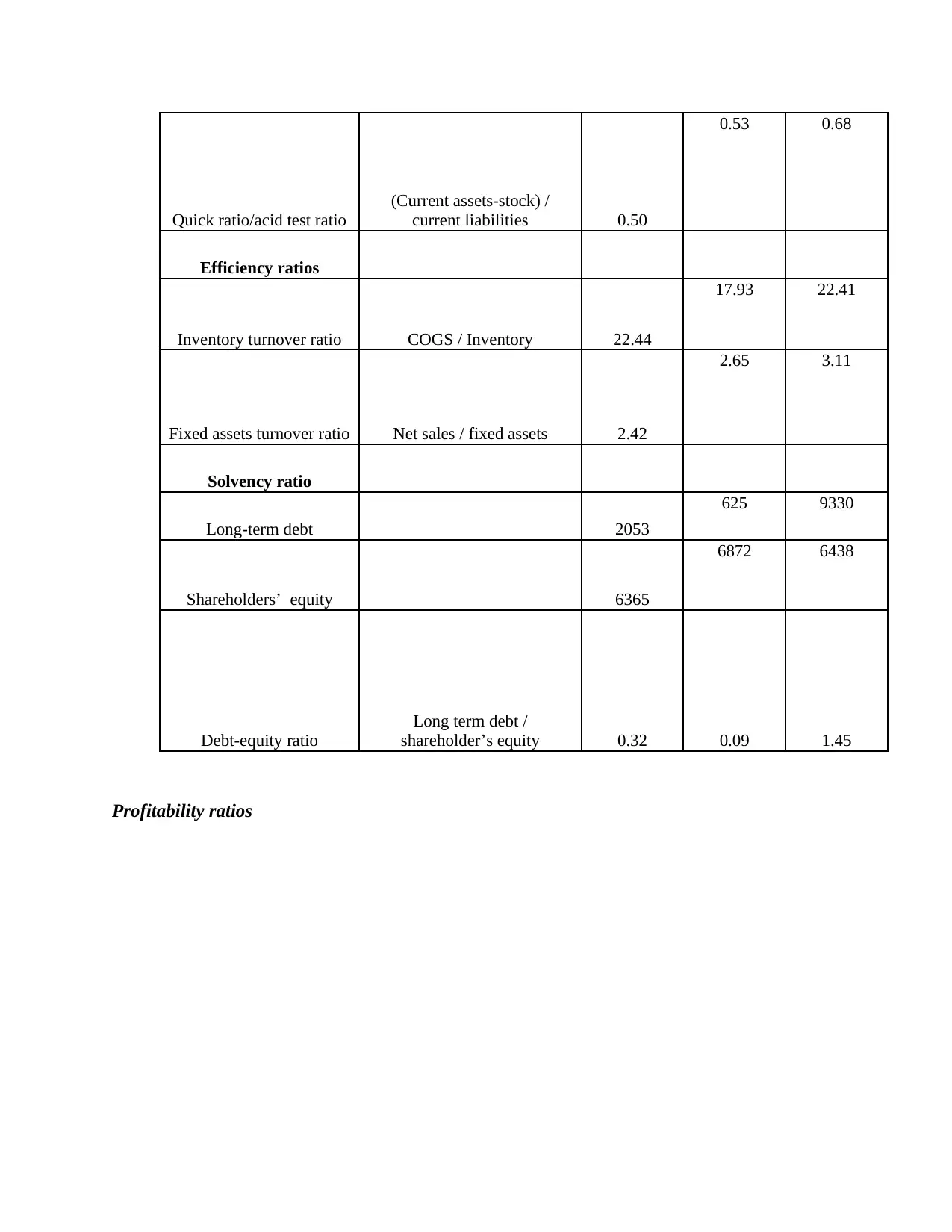

Quick ratio/acid test ratio

(Current assets-stock) /

current liabilities 0.50

0.53 0.68

Efficiency ratios

Inventory turnover ratio COGS / Inventory 22.44

17.93 22.41

Fixed assets turnover ratio Net sales / fixed assets 2.42

2.65 3.11

Solvency ratio

Long-term debt 2053

625 9330

Shareholders’ equity 6365

6872 6438

Debt-equity ratio

Long term debt /

shareholder’s equity 0.32 0.09 1.45

Profitability ratios

(Current assets-stock) /

current liabilities 0.50

0.53 0.68

Efficiency ratios

Inventory turnover ratio COGS / Inventory 22.44

17.93 22.41

Fixed assets turnover ratio Net sales / fixed assets 2.42

2.65 3.11

Solvency ratio

Long-term debt 2053

625 9330

Shareholders’ equity 6365

6872 6438

Debt-equity ratio

Long term debt /

shareholder’s equity 0.32 0.09 1.45

Profitability ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross profit

margin Net profit margin operating profit

margin-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Sainsbury Plc 2016

Sainsbury Plc 2017

Tesco Plc 2017

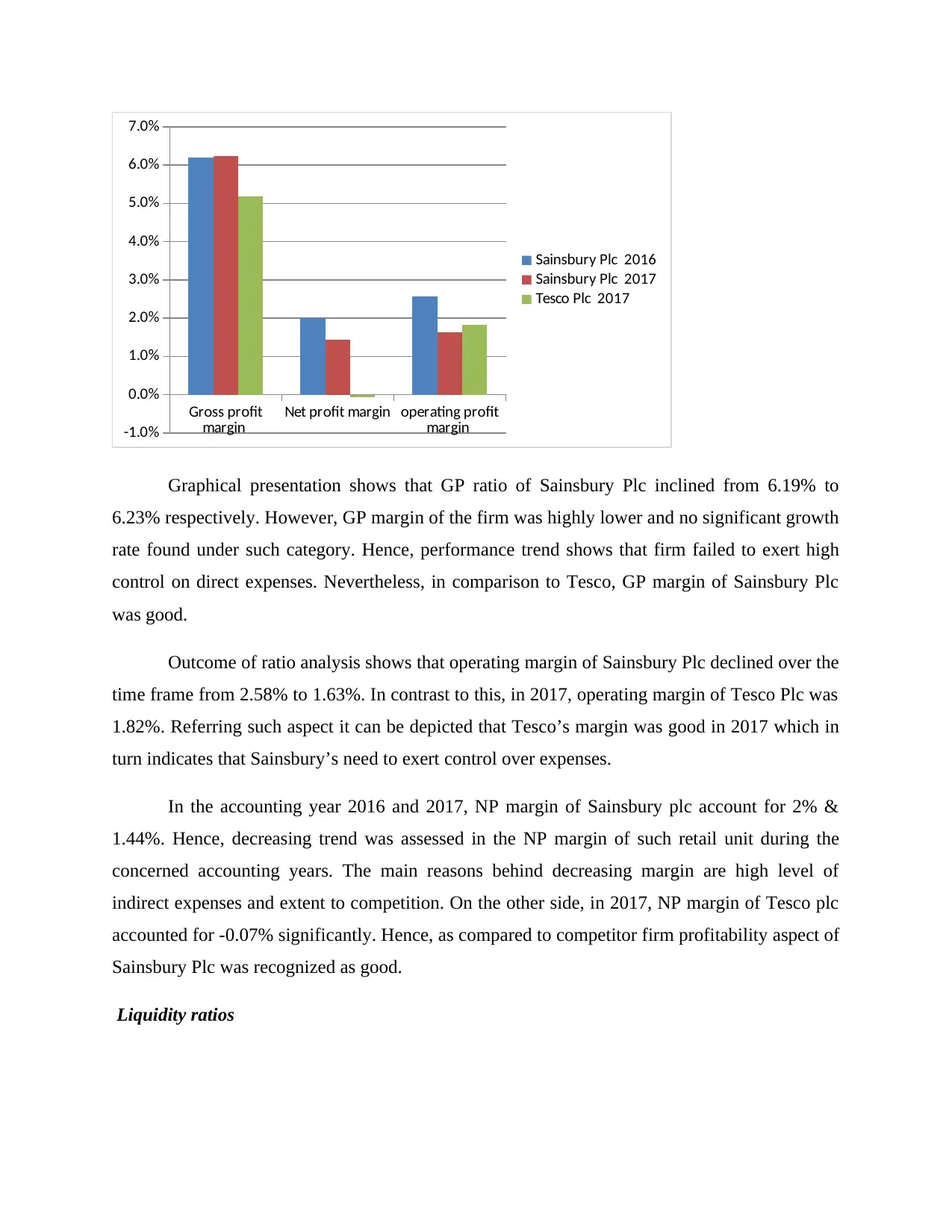

Graphical presentation shows that GP ratio of Sainsbury Plc inclined from 6.19% to

6.23% respectively. However, GP margin of the firm was highly lower and no significant growth

rate found under such category. Hence, performance trend shows that firm failed to exert high

control on direct expenses. Nevertheless, in comparison to Tesco, GP margin of Sainsbury Plc

was good.

Outcome of ratio analysis shows that operating margin of Sainsbury Plc declined over the

time frame from 2.58% to 1.63%. In contrast to this, in 2017, operating margin of Tesco Plc was

1.82%. Referring such aspect it can be depicted that Tesco’s margin was good in 2017 which in

turn indicates that Sainsbury’s need to exert control over expenses.

In the accounting year 2016 and 2017, NP margin of Sainsbury plc account for 2% &

1.44%. Hence, decreasing trend was assessed in the NP margin of such retail unit during the

concerned accounting years. The main reasons behind decreasing margin are high level of

indirect expenses and extent to competition. On the other side, in 2017, NP margin of Tesco plc

accounted for -0.07% significantly. Hence, as compared to competitor firm profitability aspect of

Sainsbury Plc was recognized as good.

Liquidity ratios

margin Net profit margin operating profit

margin-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Sainsbury Plc 2016

Sainsbury Plc 2017

Tesco Plc 2017

Graphical presentation shows that GP ratio of Sainsbury Plc inclined from 6.19% to

6.23% respectively. However, GP margin of the firm was highly lower and no significant growth

rate found under such category. Hence, performance trend shows that firm failed to exert high

control on direct expenses. Nevertheless, in comparison to Tesco, GP margin of Sainsbury Plc

was good.

Outcome of ratio analysis shows that operating margin of Sainsbury Plc declined over the

time frame from 2.58% to 1.63%. In contrast to this, in 2017, operating margin of Tesco Plc was

1.82%. Referring such aspect it can be depicted that Tesco’s margin was good in 2017 which in

turn indicates that Sainsbury’s need to exert control over expenses.

In the accounting year 2016 and 2017, NP margin of Sainsbury plc account for 2% &

1.44%. Hence, decreasing trend was assessed in the NP margin of such retail unit during the

concerned accounting years. The main reasons behind decreasing margin are high level of

indirect expenses and extent to competition. On the other side, in 2017, NP margin of Tesco plc

accounted for -0.07% significantly. Hence, as compared to competitor firm profitability aspect of

Sainsbury Plc was recognized as good.

Liquidity ratios

2016 2017 2017

Sainsbury Plc Tesco Plc

0.55

0.6

0.65

0.7

0.75

0.8

Current ratio

Current ratio

2016 2017 2017

Sainsbury Plc Tesco Plc

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Quick ratio/acid test ratio

Quick ratio/acid test ratio

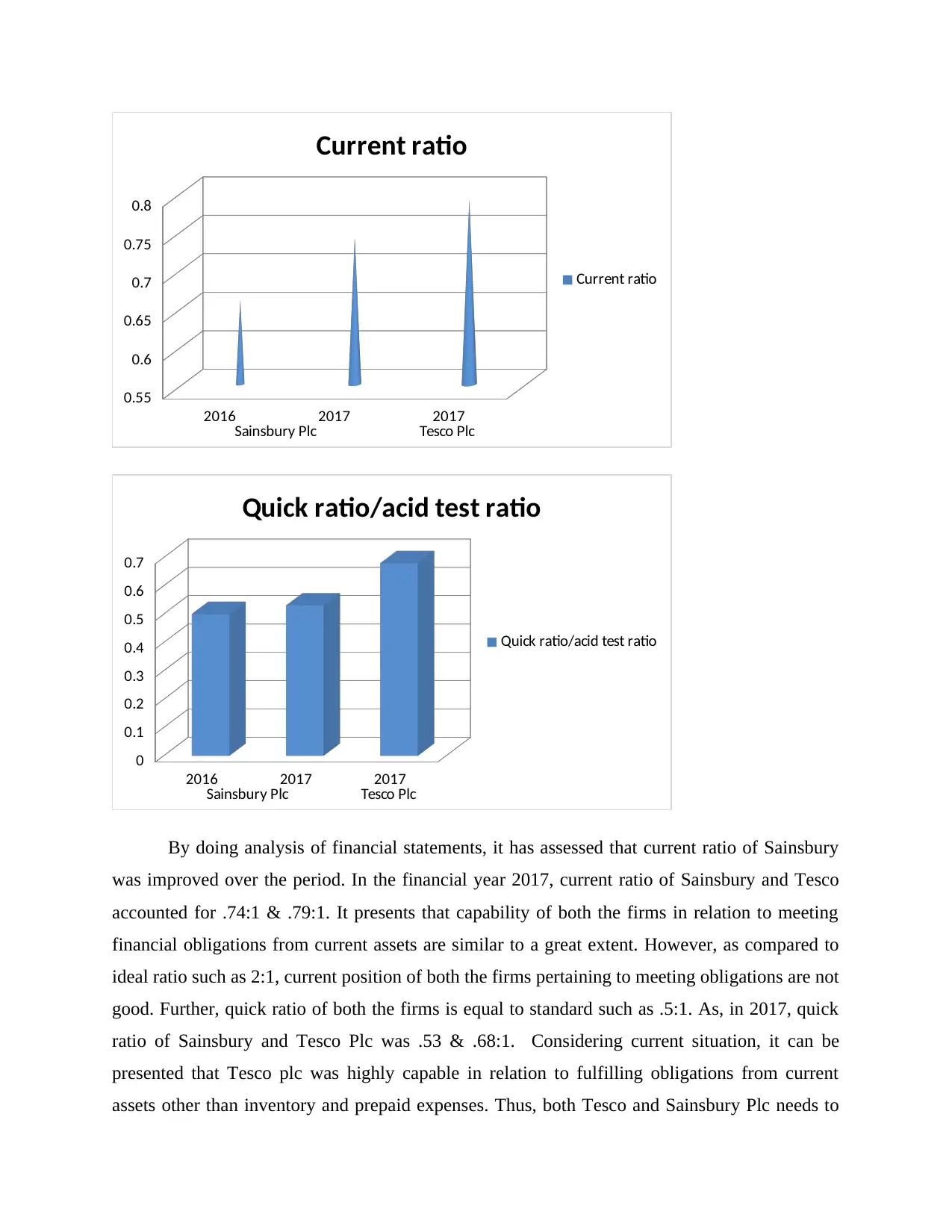

By doing analysis of financial statements, it has assessed that current ratio of Sainsbury

was improved over the period. In the financial year 2017, current ratio of Sainsbury and Tesco

accounted for .74:1 & .79:1. It presents that capability of both the firms in relation to meeting

financial obligations from current assets are similar to a great extent. However, as compared to

ideal ratio such as 2:1, current position of both the firms pertaining to meeting obligations are not

good. Further, quick ratio of both the firms is equal to standard such as .5:1. As, in 2017, quick

ratio of Sainsbury and Tesco Plc was .53 & .68:1. Considering current situation, it can be

presented that Tesco plc was highly capable in relation to fulfilling obligations from current

assets other than inventory and prepaid expenses. Thus, both Tesco and Sainsbury Plc needs to

Sainsbury Plc Tesco Plc

0.55

0.6

0.65

0.7

0.75

0.8

Current ratio

Current ratio

2016 2017 2017

Sainsbury Plc Tesco Plc

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Quick ratio/acid test ratio

Quick ratio/acid test ratio

By doing analysis of financial statements, it has assessed that current ratio of Sainsbury

was improved over the period. In the financial year 2017, current ratio of Sainsbury and Tesco

accounted for .74:1 & .79:1. It presents that capability of both the firms in relation to meeting

financial obligations from current assets are similar to a great extent. However, as compared to

ideal ratio such as 2:1, current position of both the firms pertaining to meeting obligations are not

good. Further, quick ratio of both the firms is equal to standard such as .5:1. As, in 2017, quick

ratio of Sainsbury and Tesco Plc was .53 & .68:1. Considering current situation, it can be

presented that Tesco plc was highly capable in relation to fulfilling obligations from current

assets other than inventory and prepaid expenses. Thus, both Tesco and Sainsbury Plc needs to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

undertake strategic measure for maintaining enough assets within the firm and strengthening

liquidity position (Thomas, 2009).

Solvency ratio analysis

2016 2017 2017

Sainsbury Plc Tesco Plc

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Debt-equity ratio

Debt-equity ratio

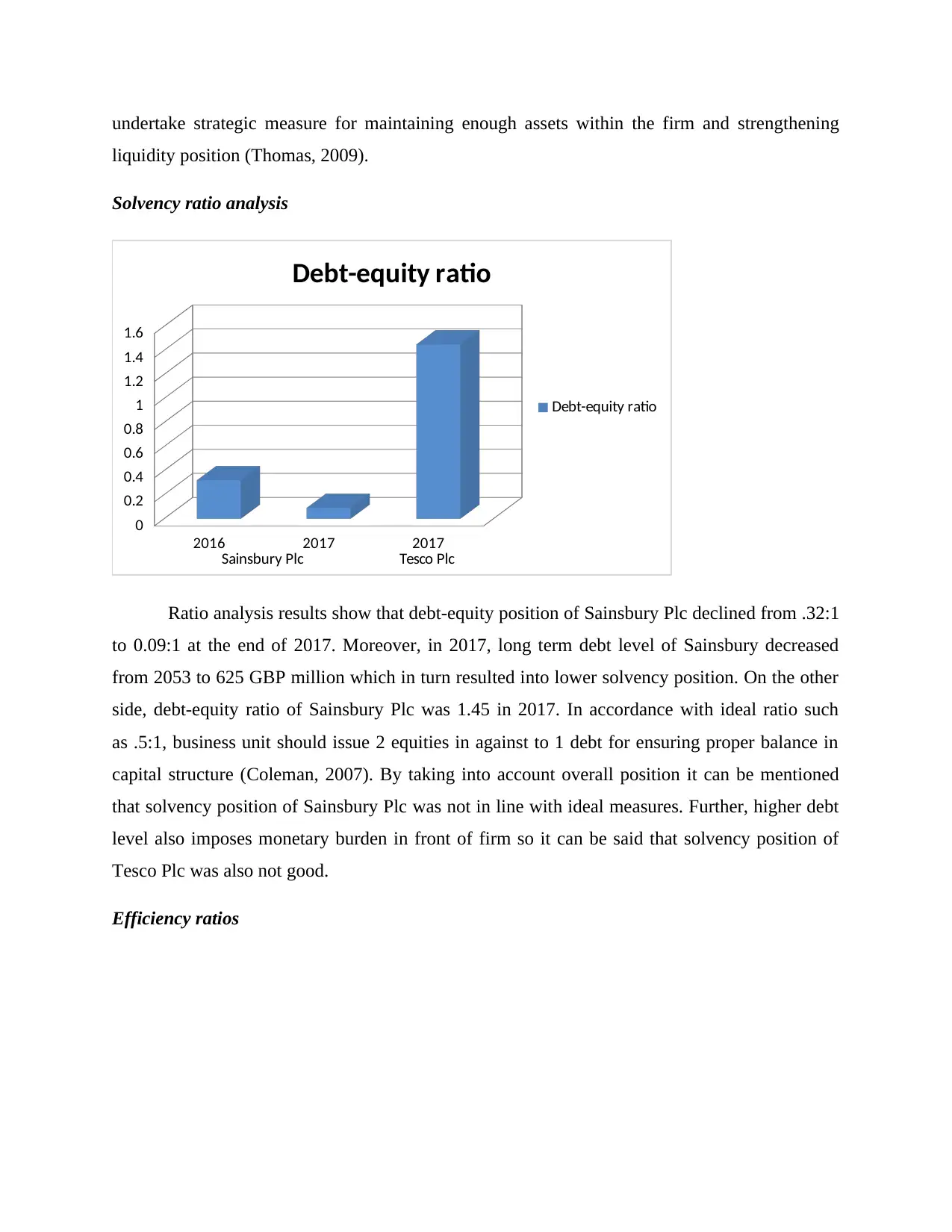

Ratio analysis results show that debt-equity position of Sainsbury Plc declined from .32:1

to 0.09:1 at the end of 2017. Moreover, in 2017, long term debt level of Sainsbury decreased

from 2053 to 625 GBP million which in turn resulted into lower solvency position. On the other

side, debt-equity ratio of Sainsbury Plc was 1.45 in 2017. In accordance with ideal ratio such

as .5:1, business unit should issue 2 equities in against to 1 debt for ensuring proper balance in

capital structure (Coleman, 2007). By taking into account overall position it can be mentioned

that solvency position of Sainsbury Plc was not in line with ideal measures. Further, higher debt

level also imposes monetary burden in front of firm so it can be said that solvency position of

Tesco Plc was also not good.

Efficiency ratios

liquidity position (Thomas, 2009).

Solvency ratio analysis

2016 2017 2017

Sainsbury Plc Tesco Plc

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Debt-equity ratio

Debt-equity ratio

Ratio analysis results show that debt-equity position of Sainsbury Plc declined from .32:1

to 0.09:1 at the end of 2017. Moreover, in 2017, long term debt level of Sainsbury decreased

from 2053 to 625 GBP million which in turn resulted into lower solvency position. On the other

side, debt-equity ratio of Sainsbury Plc was 1.45 in 2017. In accordance with ideal ratio such

as .5:1, business unit should issue 2 equities in against to 1 debt for ensuring proper balance in

capital structure (Coleman, 2007). By taking into account overall position it can be mentioned

that solvency position of Sainsbury Plc was not in line with ideal measures. Further, higher debt

level also imposes monetary burden in front of firm so it can be said that solvency position of

Tesco Plc was also not good.

Efficiency ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2016 2017 2017

Sainsbury Plc Tesco Plc

0

5

10

15

20

25

Inventory turnover ratio

Fixed assets turnover ratio

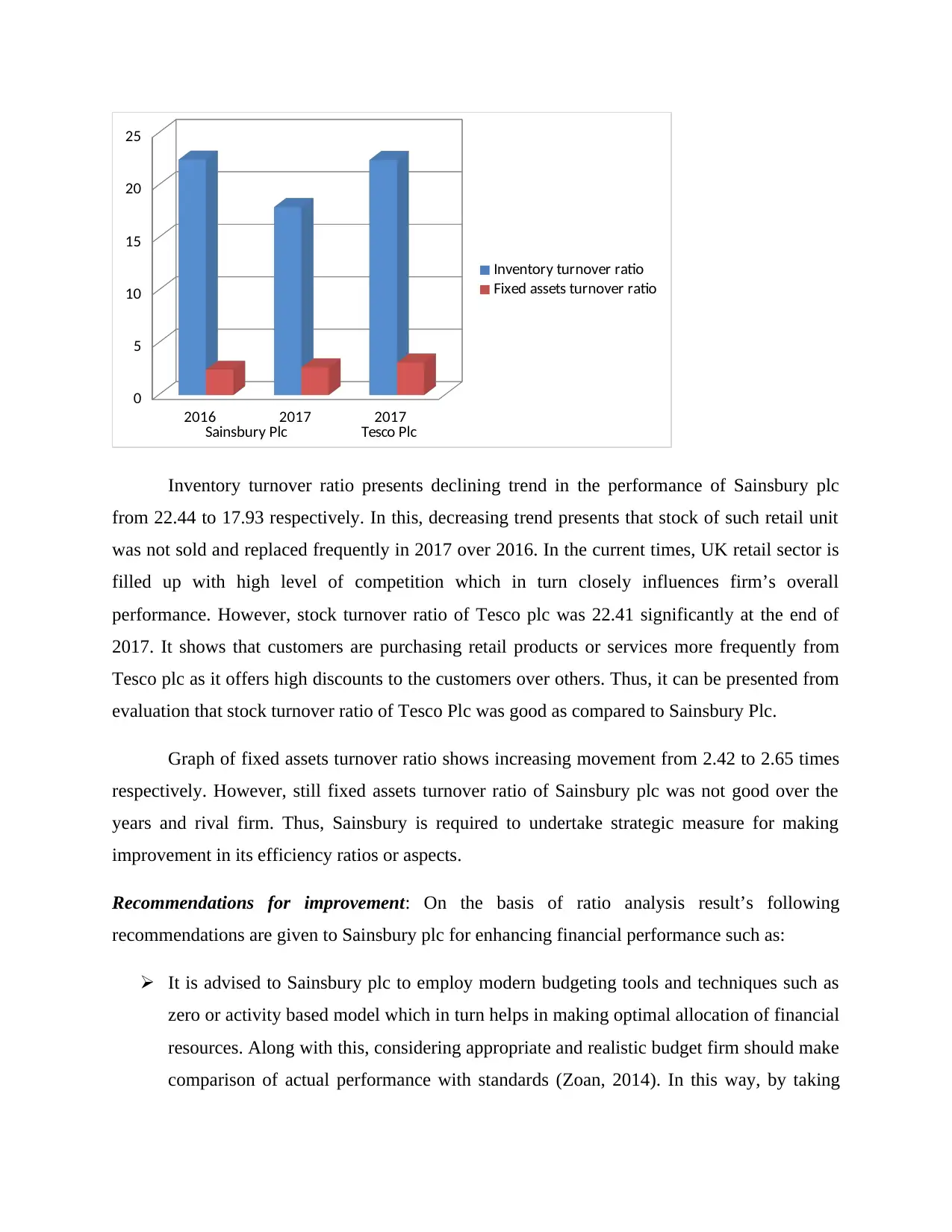

Inventory turnover ratio presents declining trend in the performance of Sainsbury plc

from 22.44 to 17.93 respectively. In this, decreasing trend presents that stock of such retail unit

was not sold and replaced frequently in 2017 over 2016. In the current times, UK retail sector is

filled up with high level of competition which in turn closely influences firm’s overall

performance. However, stock turnover ratio of Tesco plc was 22.41 significantly at the end of

2017. It shows that customers are purchasing retail products or services more frequently from

Tesco plc as it offers high discounts to the customers over others. Thus, it can be presented from

evaluation that stock turnover ratio of Tesco Plc was good as compared to Sainsbury Plc.

Graph of fixed assets turnover ratio shows increasing movement from 2.42 to 2.65 times

respectively. However, still fixed assets turnover ratio of Sainsbury plc was not good over the

years and rival firm. Thus, Sainsbury is required to undertake strategic measure for making

improvement in its efficiency ratios or aspects.

Recommendations for improvement: On the basis of ratio analysis result’s following

recommendations are given to Sainsbury plc for enhancing financial performance such as:

It is advised to Sainsbury plc to employ modern budgeting tools and techniques such as

zero or activity based model which in turn helps in making optimal allocation of financial

resources. Along with this, considering appropriate and realistic budget firm should make

comparison of actual performance with standards (Zoan, 2014). In this way, by taking

Sainsbury Plc Tesco Plc

0

5

10

15

20

25

Inventory turnover ratio

Fixed assets turnover ratio

Inventory turnover ratio presents declining trend in the performance of Sainsbury plc

from 22.44 to 17.93 respectively. In this, decreasing trend presents that stock of such retail unit

was not sold and replaced frequently in 2017 over 2016. In the current times, UK retail sector is

filled up with high level of competition which in turn closely influences firm’s overall

performance. However, stock turnover ratio of Tesco plc was 22.41 significantly at the end of

2017. It shows that customers are purchasing retail products or services more frequently from

Tesco plc as it offers high discounts to the customers over others. Thus, it can be presented from

evaluation that stock turnover ratio of Tesco Plc was good as compared to Sainsbury Plc.

Graph of fixed assets turnover ratio shows increasing movement from 2.42 to 2.65 times

respectively. However, still fixed assets turnover ratio of Sainsbury plc was not good over the

years and rival firm. Thus, Sainsbury is required to undertake strategic measure for making

improvement in its efficiency ratios or aspects.

Recommendations for improvement: On the basis of ratio analysis result’s following

recommendations are given to Sainsbury plc for enhancing financial performance such as:

It is advised to Sainsbury plc to employ modern budgeting tools and techniques such as

zero or activity based model which in turn helps in making optimal allocation of financial

resources. Along with this, considering appropriate and realistic budget firm should make

comparison of actual performance with standards (Zoan, 2014). In this way, by taking

effectual measure on time business organization can control expenses and enhance profit

margin.

Further, it is recommended to Sainsbury Plc that in the near future emphasis should be

placed on issuing debt for the development of suitable financial structure. Thus, firm

should keep in mind ideal ratio while taking decision in relation to fulfilling monetary

needs from varied sources.

Sainsbury Plc also needs to make focus on maintaining enough current assets such as

inventory, cash etc within the firm for enhancing liquidity position. This in turn makes

improvement in firm’s capability regarding meeting of current liabilities such as bank

overdraft, creditors etc (Brown and Petersen, 2011).

For enhancing inventory turnover ratio and sales firm needs to highlight both price as

well as quality in promotional campaign. Moreover, now customers are highly concerned

toward both pricing and quality of products or services. Thus, through the means of

promotional plan or campaign firm can attract more customers (Chavis, Klapper and

Love, 2011). Along with this, for increasing the level of fixed assets turnover ratio

Sainsbury Plc needs to lay emphasis on maintenance and conducting training &

development session for personnel.

3. Assessing strategies and tools that can be employed for monitoring both tangible and

intangible resources

Tangible resources

1. Physical resources -

This tangible resources include assets which consists of buildings and plant and

machinery. It is essential that business should take effective steps to maintain physical resources

so that it may yield adequate revenue in effectual way. For effective maintenance, reduction in

life cycle costs should be made, make effective maintenance of monitoring system so that assets

may provide better results in effectual manner (Renz and Herman, 2016).

2. Material resources -

The material resources are need to be effectively managed by company so that it may

yield benefits to organisation in effective way. This includes strategies to effectively maintain

resources by reusing, recycle material resources. The material resources are required to be

margin.

Further, it is recommended to Sainsbury Plc that in the near future emphasis should be

placed on issuing debt for the development of suitable financial structure. Thus, firm

should keep in mind ideal ratio while taking decision in relation to fulfilling monetary

needs from varied sources.

Sainsbury Plc also needs to make focus on maintaining enough current assets such as

inventory, cash etc within the firm for enhancing liquidity position. This in turn makes

improvement in firm’s capability regarding meeting of current liabilities such as bank

overdraft, creditors etc (Brown and Petersen, 2011).

For enhancing inventory turnover ratio and sales firm needs to highlight both price as

well as quality in promotional campaign. Moreover, now customers are highly concerned

toward both pricing and quality of products or services. Thus, through the means of

promotional plan or campaign firm can attract more customers (Chavis, Klapper and

Love, 2011). Along with this, for increasing the level of fixed assets turnover ratio

Sainsbury Plc needs to lay emphasis on maintenance and conducting training &

development session for personnel.

3. Assessing strategies and tools that can be employed for monitoring both tangible and

intangible resources

Tangible resources

1. Physical resources -

This tangible resources include assets which consists of buildings and plant and

machinery. It is essential that business should take effective steps to maintain physical resources

so that it may yield adequate revenue in effectual way. For effective maintenance, reduction in

life cycle costs should be made, make effective maintenance of monitoring system so that assets

may provide better results in effectual manner (Renz and Herman, 2016).

2. Material resources -

The material resources are need to be effectively managed by company so that it may

yield benefits to organisation in effective way. This includes strategies to effectively maintain

resources by reusing, recycle material resources. The material resources are required to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.