Financial Performance Evaluation of Samsung PLC for Strategic Managers

VerifiedAdded on 2020/10/22

|11

|2503

|364

Report

AI Summary

This report provides a comprehensive financial analysis of Samsung PLC. It begins with an introduction to strategic financial management and its application to the company. The report examines Samsung's financial statements, including the income statement and balance sheet, interpreting key data points. It then performs a comparative analysis using various financial ratios, such as liquidity, leverage, and profitability ratios, comparing 2016 and 2017 data to assess trends and performance. The report further delves into strategic decision-making, specifically focusing on the Net Present Value (NPV) of replacing an old machine with a new one, providing calculations and recommendations. Finally, the report concludes with a summary of findings and recommendations for the strategic management of Samsung's finances.

Finance for strategic

manager

manager

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Covered in PPT...........................................................................................................................1

TASK 2 ...........................................................................................................................................1

2.1 Interpretation of financial statements of Samsung PLC.......................................................1

2.2 Comparative analysis of financial data using Ratio analysis for Samsung PLC..................2

TASK 3 ...........................................................................................................................................4

Covered in leaflet........................................................................................................................4

TASK 4 ...........................................................................................................................................4

3.2 Providing advice for the best course of action......................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Covered in PPT...........................................................................................................................1

TASK 2 ...........................................................................................................................................1

2.1 Interpretation of financial statements of Samsung PLC.......................................................1

2.2 Comparative analysis of financial data using Ratio analysis for Samsung PLC..................2

TASK 3 ...........................................................................................................................................4

Covered in leaflet........................................................................................................................4

TASK 4 ...........................................................................................................................................4

3.2 Providing advice for the best course of action......................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

INTRODUCTION

Finance is the life blood of any organisation without finance no organisation can survive

in the market. Strategic managers use strategic financial management system to form best

strategies to utilize finance within the organisation. Strategic financial management refers to the

planning and controlling the usage of financial resources of the organisation. Samsung PLC is a

manufacturing company, it needs to properly maintain the financial resources.

In this project report, sources of financial data, formulation of business strategy, analysis

of financial statements, strategic decision making, cash flows etc. are discussed to analyse the

financial position of Samsung PLC. Ratio analysis is used to determine the profitability of the

organisation. Financial statements show the actual financial condition of the company, that helps

the managers to form best business strategy (Basak and Makarov, 2014).

TASK 1

Covered in PPT

TASK 2

2.1 Interpretation of financial statements of Samsung PLC

Interpretation of financial statements refers to analysis and determination of the

importance of the financial statement data which helps in forecasting for future earnings, debt

maturities, ability to pay interest, profitability of current and long term etc. It also includes many

processes like analysis, arrangement, establishing relationship between present facts and give

conclusion on the basis of that facts. The company involves first three steps in growth and

summarisation of financial and operating information as well as in the preparation of financial

statements. These steps are analysis of each and every transaction for determination of accounts

which is to be debited or credited and their measurement and variation of amount involved in

these transactions, recording of those transaction in the journals, summarised in ledgers and

preparation of an account and last in preparation of financial statements (Gorbenko and Malenko,

2014).

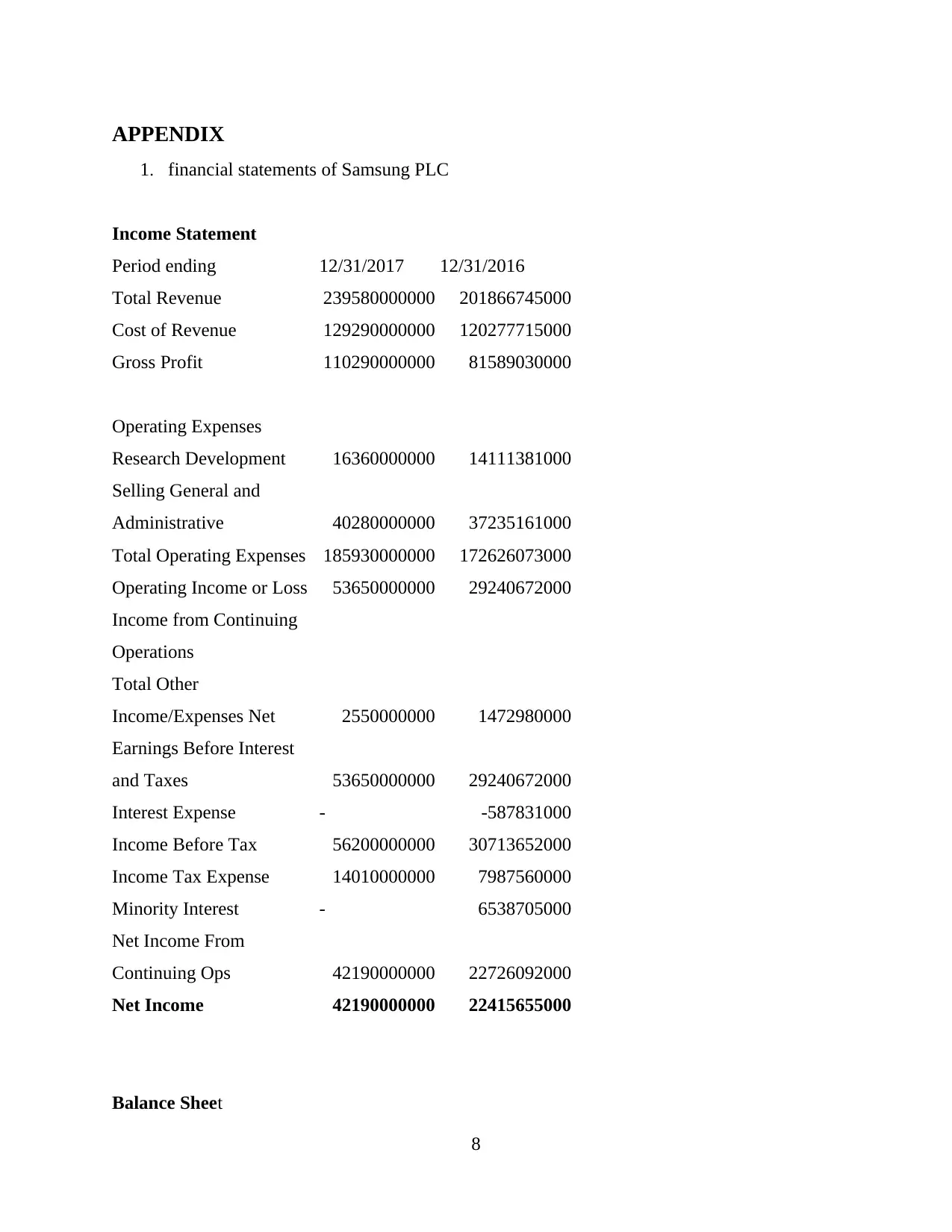

Income statement: It is one out of three financial statement which investors need to

understand in order to analysis profitability and company's future growth which plays a

important role in deciding whether to invest or not. As per appendix 1. Samsung's total revenue

1

Finance is the life blood of any organisation without finance no organisation can survive

in the market. Strategic managers use strategic financial management system to form best

strategies to utilize finance within the organisation. Strategic financial management refers to the

planning and controlling the usage of financial resources of the organisation. Samsung PLC is a

manufacturing company, it needs to properly maintain the financial resources.

In this project report, sources of financial data, formulation of business strategy, analysis

of financial statements, strategic decision making, cash flows etc. are discussed to analyse the

financial position of Samsung PLC. Ratio analysis is used to determine the profitability of the

organisation. Financial statements show the actual financial condition of the company, that helps

the managers to form best business strategy (Basak and Makarov, 2014).

TASK 1

Covered in PPT

TASK 2

2.1 Interpretation of financial statements of Samsung PLC

Interpretation of financial statements refers to analysis and determination of the

importance of the financial statement data which helps in forecasting for future earnings, debt

maturities, ability to pay interest, profitability of current and long term etc. It also includes many

processes like analysis, arrangement, establishing relationship between present facts and give

conclusion on the basis of that facts. The company involves first three steps in growth and

summarisation of financial and operating information as well as in the preparation of financial

statements. These steps are analysis of each and every transaction for determination of accounts

which is to be debited or credited and their measurement and variation of amount involved in

these transactions, recording of those transaction in the journals, summarised in ledgers and

preparation of an account and last in preparation of financial statements (Gorbenko and Malenko,

2014).

Income statement: It is one out of three financial statement which investors need to

understand in order to analysis profitability and company's future growth which plays a

important role in deciding whether to invest or not. As per appendix 1. Samsung's total revenue

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is 239580000000 in 2017 which refers to company's sales of goods and services to its customers

and its Gross Profit is 110290000000 that represents the difference between it's net sales and cost

of sales which represents the resources to cover company's expenses. Greater and stable gross

profits positively impact on its Net income which is 42190000000 in 2017 and it is more than

previous financial year which helps in examine the earning capacity and efficiency of different

business activities. This income statement determines the profitability and investigate the future

prospective of Samsung PLC (Wuttke, and et. al., 2013).

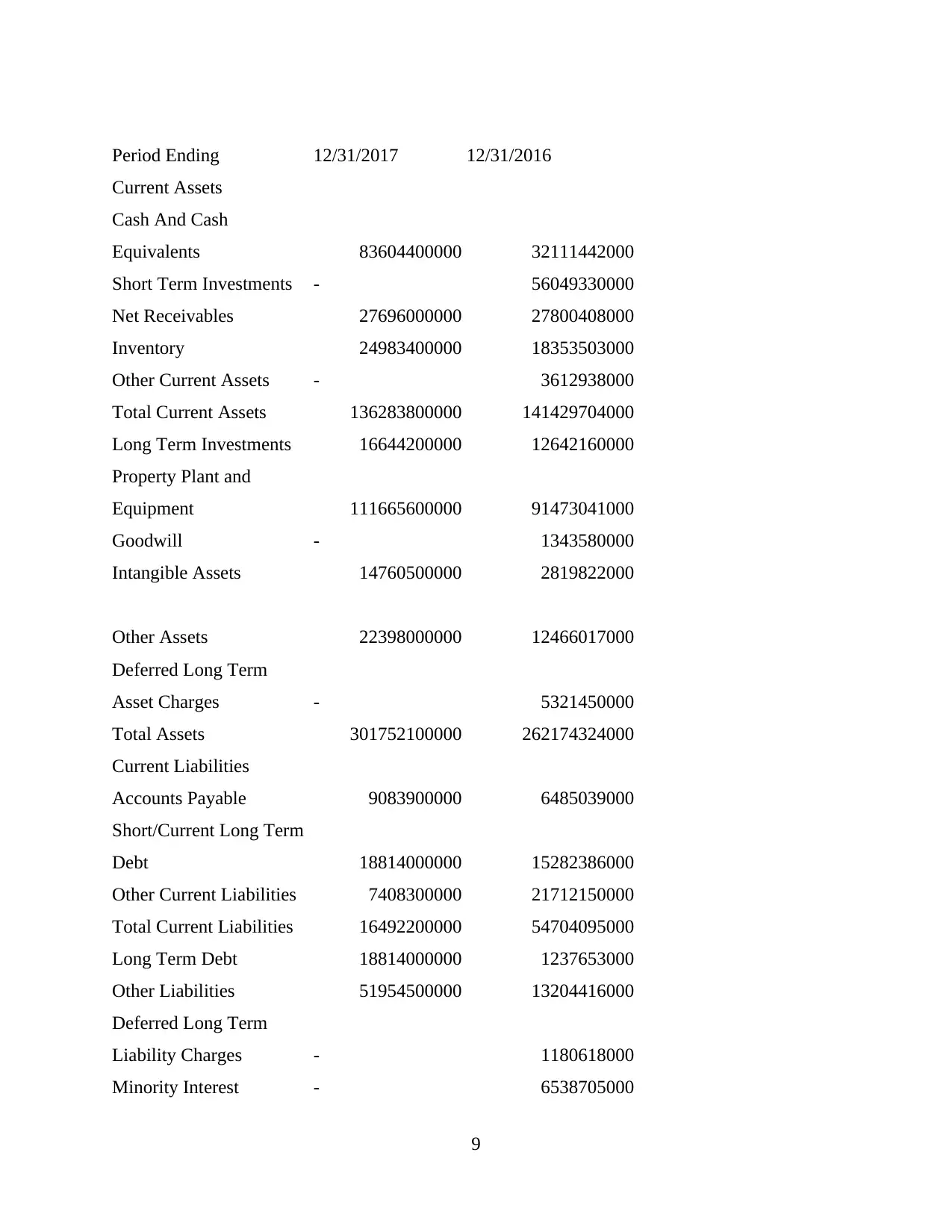

Balance Sheet: It shows the business solvency, assets liquidity, finance sources and

utilisation of capital (Smit and Trigeorgis, 2012). Balance Sheet divided into two parts i.e. assets

which is equal to liabilities plus shareholders equity which interpreted company's financial

position at the end of financial year. As per appendix 2. Samsung's total assets is 301752100000

which is used to operates business is equals to its liabilities 87260700000 plus stockholder equity

214491400000 combines the amount that is initially invested in the company. Liabilities and

stockholders equity are two sources that assist these assets .

2.2 Comparative analysis of financial data using Ratio analysis for Samsung PLC

Comparative statement analysis refers to comparison between company's last year

financial statements with prior year. Horizontal, Vertical and Ratio analysis are the three

important methods of comparative financial statement analysis.

Ratio Analysis is the method in which the ratio between two or more variables of the

organisation is compared. Liquidity, profitability, activity, short and long term solvency ratio and

many more are the ratios used to analysis Samsung PLC (Ratio Analysis, 2018). Following are

mentioned below:

Liquidity Ratio: It is defined as company's ability to meet its short term debts.

a) Current ratio = Current Assets/ Current liabilities

Current ratio (2017) = 136283800000 / 16492200000

= 8.12 : 1

Current ratio (2016) = 141429704000 / 54704095000

= 2.59 : 1

When interpreting Samsung's current ratio which is 8.12 :1 it means for every 1 in current

liabilities, the company has 8.12 in current assets, which is considered good because it is higher

than last year current ratio i.e. 2.59 means better financial position.

2

and its Gross Profit is 110290000000 that represents the difference between it's net sales and cost

of sales which represents the resources to cover company's expenses. Greater and stable gross

profits positively impact on its Net income which is 42190000000 in 2017 and it is more than

previous financial year which helps in examine the earning capacity and efficiency of different

business activities. This income statement determines the profitability and investigate the future

prospective of Samsung PLC (Wuttke, and et. al., 2013).

Balance Sheet: It shows the business solvency, assets liquidity, finance sources and

utilisation of capital (Smit and Trigeorgis, 2012). Balance Sheet divided into two parts i.e. assets

which is equal to liabilities plus shareholders equity which interpreted company's financial

position at the end of financial year. As per appendix 2. Samsung's total assets is 301752100000

which is used to operates business is equals to its liabilities 87260700000 plus stockholder equity

214491400000 combines the amount that is initially invested in the company. Liabilities and

stockholders equity are two sources that assist these assets .

2.2 Comparative analysis of financial data using Ratio analysis for Samsung PLC

Comparative statement analysis refers to comparison between company's last year

financial statements with prior year. Horizontal, Vertical and Ratio analysis are the three

important methods of comparative financial statement analysis.

Ratio Analysis is the method in which the ratio between two or more variables of the

organisation is compared. Liquidity, profitability, activity, short and long term solvency ratio and

many more are the ratios used to analysis Samsung PLC (Ratio Analysis, 2018). Following are

mentioned below:

Liquidity Ratio: It is defined as company's ability to meet its short term debts.

a) Current ratio = Current Assets/ Current liabilities

Current ratio (2017) = 136283800000 / 16492200000

= 8.12 : 1

Current ratio (2016) = 141429704000 / 54704095000

= 2.59 : 1

When interpreting Samsung's current ratio which is 8.12 :1 it means for every 1 in current

liabilities, the company has 8.12 in current assets, which is considered good because it is higher

than last year current ratio i.e. 2.59 means better financial position.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

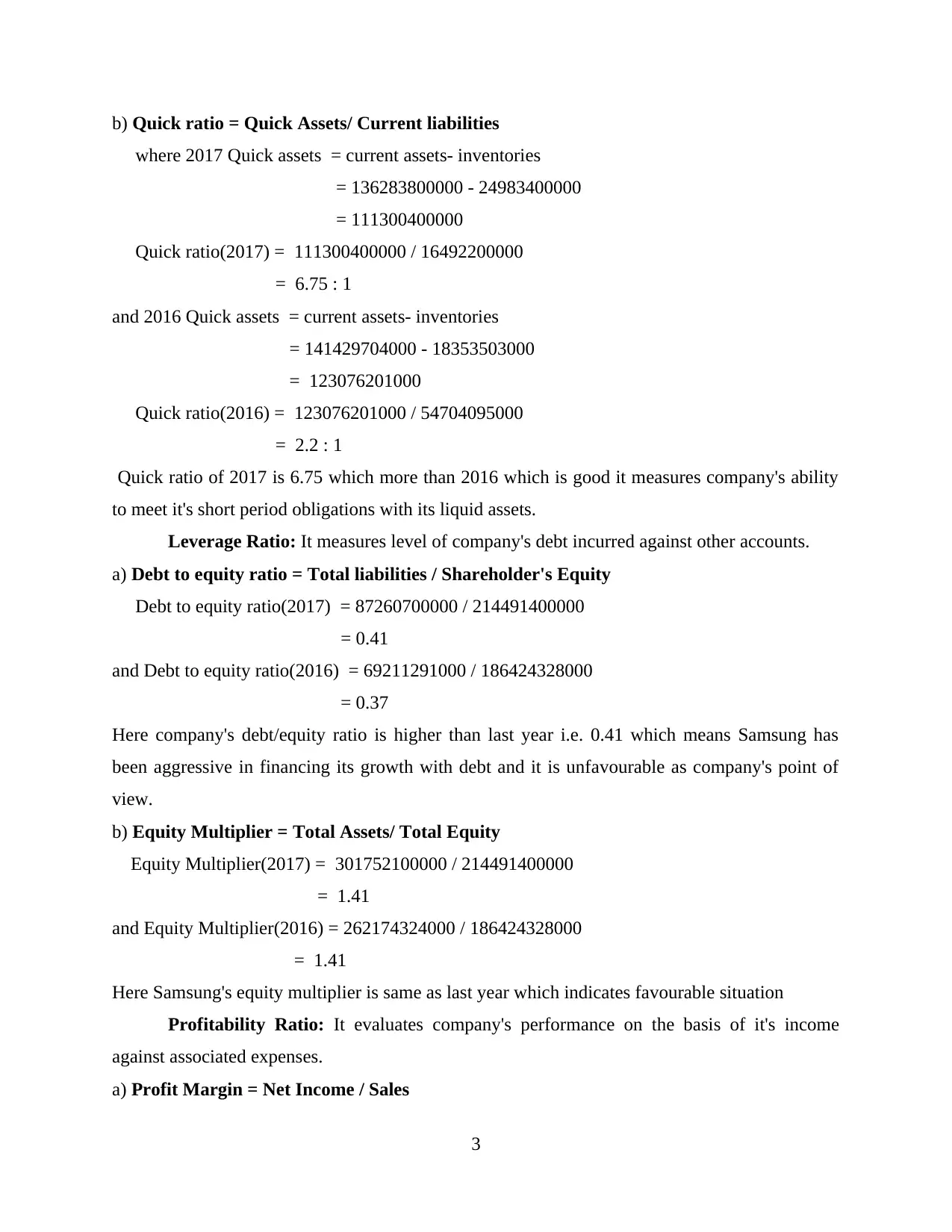

b) Quick ratio = Quick Assets/ Current liabilities

where 2017 Quick assets = current assets- inventories

= 136283800000 - 24983400000

= 111300400000

Quick ratio(2017) = 111300400000 / 16492200000

= 6.75 : 1

and 2016 Quick assets = current assets- inventories

= 141429704000 - 18353503000

= 123076201000

Quick ratio(2016) = 123076201000 / 54704095000

= 2.2 : 1

Quick ratio of 2017 is 6.75 which more than 2016 which is good it measures company's ability

to meet it's short period obligations with its liquid assets.

Leverage Ratio: It measures level of company's debt incurred against other accounts.

a) Debt to equity ratio = Total liabilities / Shareholder's Equity

Debt to equity ratio(2017) = 87260700000 / 214491400000

= 0.41

and Debt to equity ratio(2016) = 69211291000 / 186424328000

= 0.37

Here company's debt/equity ratio is higher than last year i.e. 0.41 which means Samsung has

been aggressive in financing its growth with debt and it is unfavourable as company's point of

view.

b) Equity Multiplier = Total Assets/ Total Equity

Equity Multiplier(2017) = 301752100000 / 214491400000

= 1.41

and Equity Multiplier(2016) = 262174324000 / 186424328000

= 1.41

Here Samsung's equity multiplier is same as last year which indicates favourable situation

Profitability Ratio: It evaluates company's performance on the basis of it's income

against associated expenses.

a) Profit Margin = Net Income / Sales

3

where 2017 Quick assets = current assets- inventories

= 136283800000 - 24983400000

= 111300400000

Quick ratio(2017) = 111300400000 / 16492200000

= 6.75 : 1

and 2016 Quick assets = current assets- inventories

= 141429704000 - 18353503000

= 123076201000

Quick ratio(2016) = 123076201000 / 54704095000

= 2.2 : 1

Quick ratio of 2017 is 6.75 which more than 2016 which is good it measures company's ability

to meet it's short period obligations with its liquid assets.

Leverage Ratio: It measures level of company's debt incurred against other accounts.

a) Debt to equity ratio = Total liabilities / Shareholder's Equity

Debt to equity ratio(2017) = 87260700000 / 214491400000

= 0.41

and Debt to equity ratio(2016) = 69211291000 / 186424328000

= 0.37

Here company's debt/equity ratio is higher than last year i.e. 0.41 which means Samsung has

been aggressive in financing its growth with debt and it is unfavourable as company's point of

view.

b) Equity Multiplier = Total Assets/ Total Equity

Equity Multiplier(2017) = 301752100000 / 214491400000

= 1.41

and Equity Multiplier(2016) = 262174324000 / 186424328000

= 1.41

Here Samsung's equity multiplier is same as last year which indicates favourable situation

Profitability Ratio: It evaluates company's performance on the basis of it's income

against associated expenses.

a) Profit Margin = Net Income / Sales

3

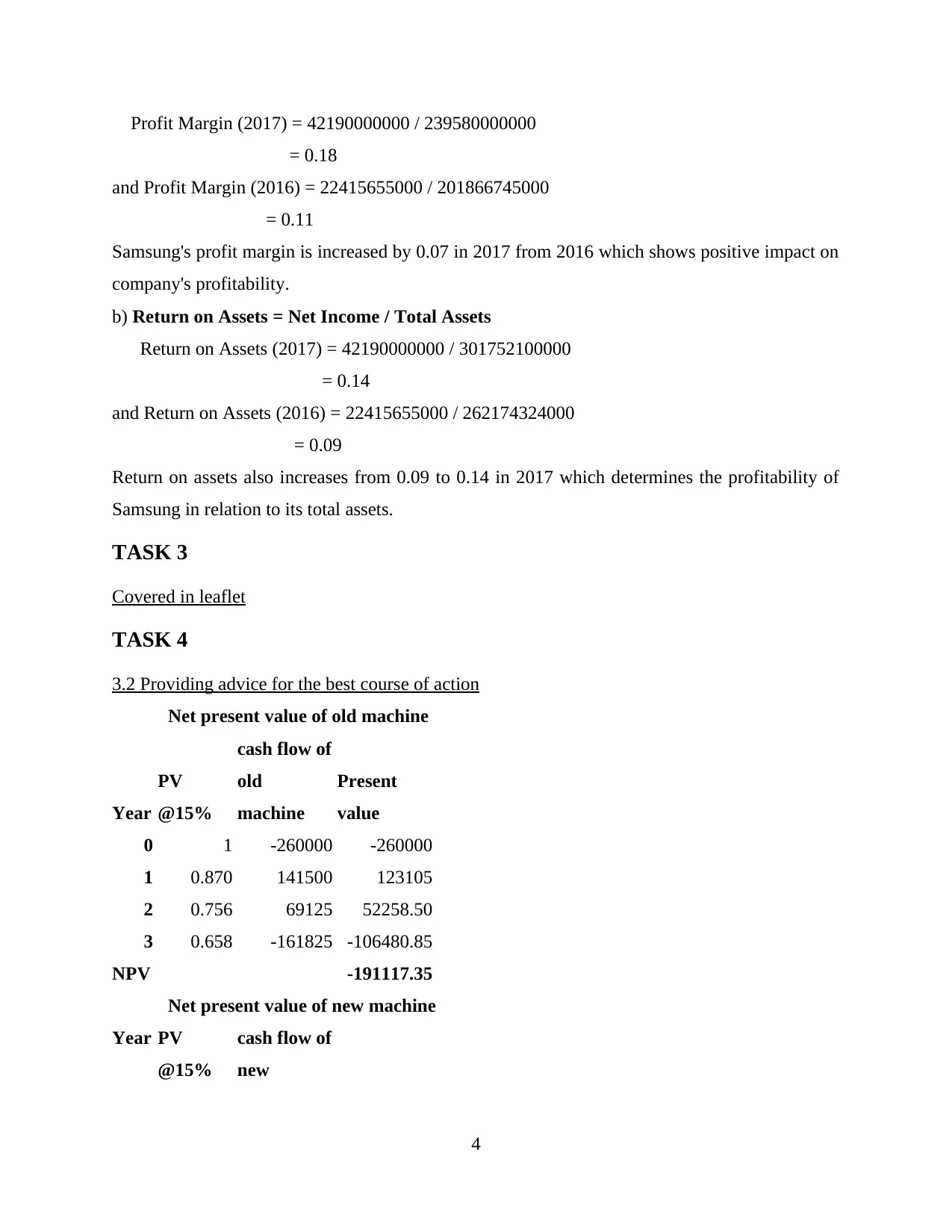

Profit Margin (2017) = 42190000000 / 239580000000

= 0.18

and Profit Margin (2016) = 22415655000 / 201866745000

= 0.11

Samsung's profit margin is increased by 0.07 in 2017 from 2016 which shows positive impact on

company's profitability.

b) Return on Assets = Net Income / Total Assets

Return on Assets (2017) = 42190000000 / 301752100000

= 0.14

and Return on Assets (2016) = 22415655000 / 262174324000

= 0.09

Return on assets also increases from 0.09 to 0.14 in 2017 which determines the profitability of

Samsung in relation to its total assets.

TASK 3

Covered in leaflet

TASK 4

3.2 Providing advice for the best course of action

Net present value of old machine

Year

PV

@15%

cash flow of

old

machine

Present

value

0 1 -260000 -260000

1 0.870 141500 123105

2 0.756 69125 52258.50

3 0.658 -161825 -106480.85

NPV -191117.35

Net present value of new machine

Year PV

@15%

cash flow of

new

4

= 0.18

and Profit Margin (2016) = 22415655000 / 201866745000

= 0.11

Samsung's profit margin is increased by 0.07 in 2017 from 2016 which shows positive impact on

company's profitability.

b) Return on Assets = Net Income / Total Assets

Return on Assets (2017) = 42190000000 / 301752100000

= 0.14

and Return on Assets (2016) = 22415655000 / 262174324000

= 0.09

Return on assets also increases from 0.09 to 0.14 in 2017 which determines the profitability of

Samsung in relation to its total assets.

TASK 3

Covered in leaflet

TASK 4

3.2 Providing advice for the best course of action

Net present value of old machine

Year

PV

@15%

cash flow of

old

machine

Present

value

0 1 -260000 -260000

1 0.870 141500 123105

2 0.756 69125 52258.50

3 0.658 -161825 -106480.85

NPV -191117.35

Net present value of new machine

Year PV

@15%

cash flow of

new

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

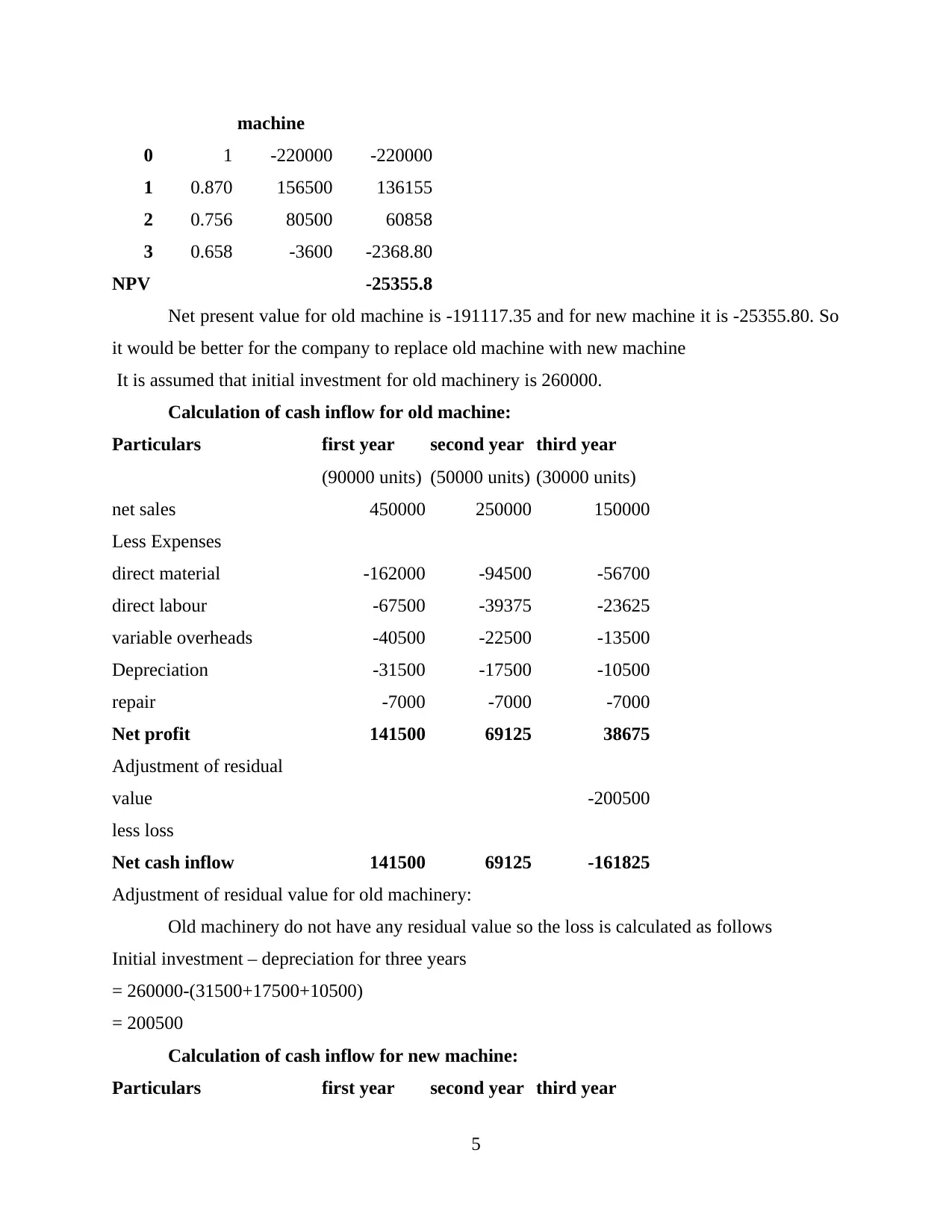

machine

0 1 -220000 -220000

1 0.870 156500 136155

2 0.756 80500 60858

3 0.658 -3600 -2368.80

NPV -25355.8

Net present value for old machine is -191117.35 and for new machine it is -25355.80. So

it would be better for the company to replace old machine with new machine

It is assumed that initial investment for old machinery is 260000.

Calculation of cash inflow for old machine:

Particulars first year second year third year

(90000 units) (50000 units) (30000 units)

net sales 450000 250000 150000

Less Expenses

direct material -162000 -94500 -56700

direct labour -67500 -39375 -23625

variable overheads -40500 -22500 -13500

Depreciation -31500 -17500 -10500

repair -7000 -7000 -7000

Net profit 141500 69125 38675

Adjustment of residual

value -200500

less loss

Net cash inflow 141500 69125 -161825

Adjustment of residual value for old machinery:

Old machinery do not have any residual value so the loss is calculated as follows

Initial investment – depreciation for three years

= 260000-(31500+17500+10500)

= 200500

Calculation of cash inflow for new machine:

Particulars first year second year third year

5

0 1 -220000 -220000

1 0.870 156500 136155

2 0.756 80500 60858

3 0.658 -3600 -2368.80

NPV -25355.8

Net present value for old machine is -191117.35 and for new machine it is -25355.80. So

it would be better for the company to replace old machine with new machine

It is assumed that initial investment for old machinery is 260000.

Calculation of cash inflow for old machine:

Particulars first year second year third year

(90000 units) (50000 units) (30000 units)

net sales 450000 250000 150000

Less Expenses

direct material -162000 -94500 -56700

direct labour -67500 -39375 -23625

variable overheads -40500 -22500 -13500

Depreciation -31500 -17500 -10500

repair -7000 -7000 -7000

Net profit 141500 69125 38675

Adjustment of residual

value -200500

less loss

Net cash inflow 141500 69125 -161825

Adjustment of residual value for old machinery:

Old machinery do not have any residual value so the loss is calculated as follows

Initial investment – depreciation for three years

= 260000-(31500+17500+10500)

= 200500

Calculation of cash inflow for new machine:

Particulars first year second year third year

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

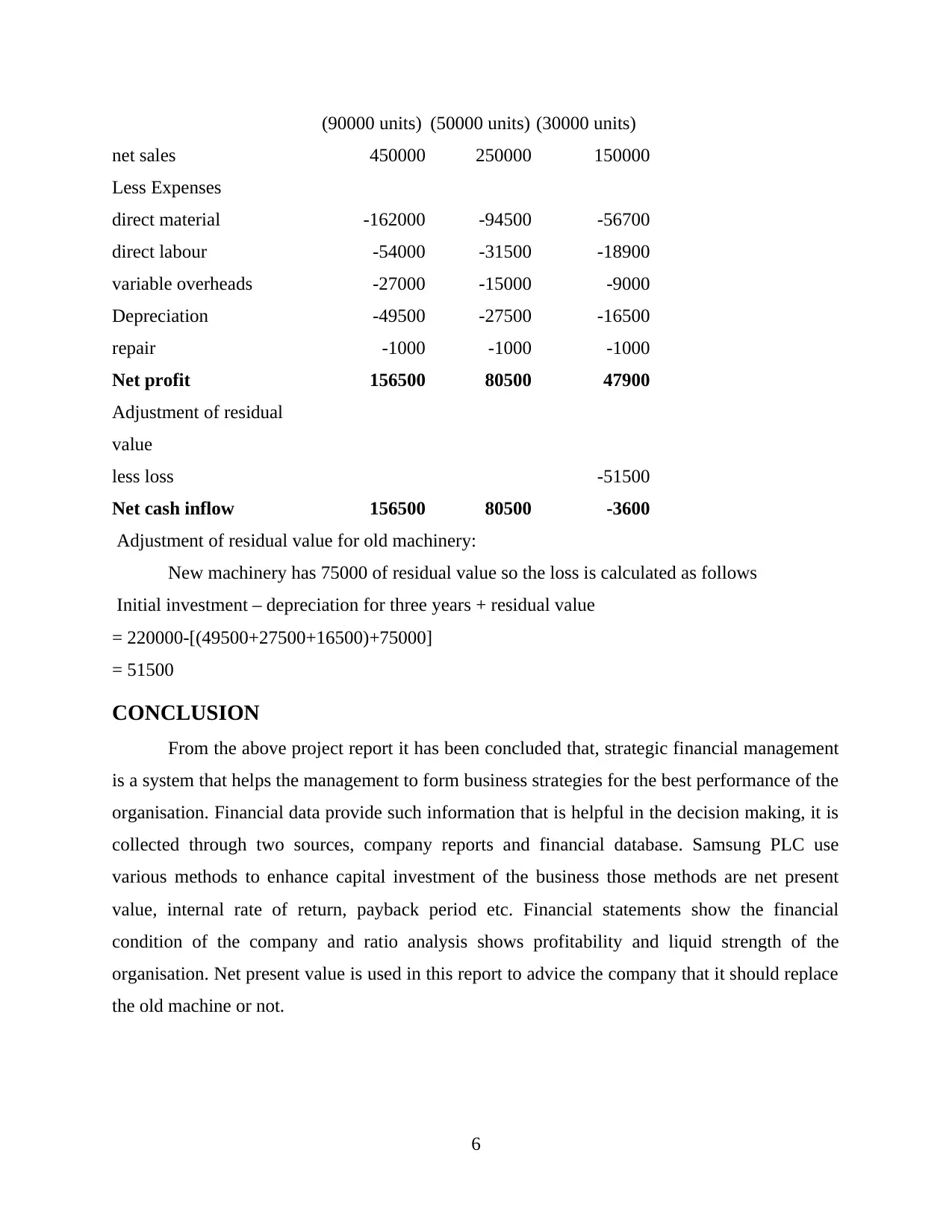

(90000 units) (50000 units) (30000 units)

net sales 450000 250000 150000

Less Expenses

direct material -162000 -94500 -56700

direct labour -54000 -31500 -18900

variable overheads -27000 -15000 -9000

Depreciation -49500 -27500 -16500

repair -1000 -1000 -1000

Net profit 156500 80500 47900

Adjustment of residual

value

less loss -51500

Net cash inflow 156500 80500 -3600

Adjustment of residual value for old machinery:

New machinery has 75000 of residual value so the loss is calculated as follows

Initial investment – depreciation for three years + residual value

= 220000-[(49500+27500+16500)+75000]

= 51500

CONCLUSION

From the above project report it has been concluded that, strategic financial management

is a system that helps the management to form business strategies for the best performance of the

organisation. Financial data provide such information that is helpful in the decision making, it is

collected through two sources, company reports and financial database. Samsung PLC use

various methods to enhance capital investment of the business those methods are net present

value, internal rate of return, payback period etc. Financial statements show the financial

condition of the company and ratio analysis shows profitability and liquid strength of the

organisation. Net present value is used in this report to advice the company that it should replace

the old machine or not.

6

net sales 450000 250000 150000

Less Expenses

direct material -162000 -94500 -56700

direct labour -54000 -31500 -18900

variable overheads -27000 -15000 -9000

Depreciation -49500 -27500 -16500

repair -1000 -1000 -1000

Net profit 156500 80500 47900

Adjustment of residual

value

less loss -51500

Net cash inflow 156500 80500 -3600

Adjustment of residual value for old machinery:

New machinery has 75000 of residual value so the loss is calculated as follows

Initial investment – depreciation for three years + residual value

= 220000-[(49500+27500+16500)+75000]

= 51500

CONCLUSION

From the above project report it has been concluded that, strategic financial management

is a system that helps the management to form business strategies for the best performance of the

organisation. Financial data provide such information that is helpful in the decision making, it is

collected through two sources, company reports and financial database. Samsung PLC use

various methods to enhance capital investment of the business those methods are net present

value, internal rate of return, payback period etc. Financial statements show the financial

condition of the company and ratio analysis shows profitability and liquid strength of the

organisation. Net present value is used in this report to advice the company that it should replace

the old machine or not.

6

REFERENCES

Books and Journals:

Basak, S. and Makarov, D., 2014. Strategic asset allocation in money management. The Journal

of Finance. 69(1). pp.179-217.

Boonstra, A., 2013. How do top managers support strategic information system projects and why

do they sometimes withhold this support?. International Journal of Project

Management. 31(4). pp.498-512.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic management journal. 35(1). pp.1-23.

Cheng, M. M. and Humphreys, K. A., 2012. The differential improvement effects of the strategy

map and scorecard perspectives on managers' strategic judgments. The Accounting

Review. 87(3). pp.899-924.

Dewulf, G., Blanken, A. and Bult-Spiering, M., 2012. Strategic issues in public-private

partnerships. London, England: Wiley-Blackwell.

Gorbenko, A. S. and Malenko, A., 2014. Strategic and financial bidders in takeover auctions. The

Journal of Finance. 69(6). pp.2513-2555.

Smit, H. T. and Trigeorgis, L., 2012. Strategic investment: Real options and games. Princeton

University Press.

Ward, K., 2012. Strategic management accounting. Routledge.

Wheelen, T. L. and Hunger, J. D., 2011. Concepts in strategic management and business policy.

Pearson Education India.

Wuttke, D. A., and et. al., 2013. Managing the innovation adoption of supply chain finance—

Empirical evidence from six European case studies. Journal of Business Logistics.

34(2). pp.148-166.

Online

Ratio Analysis, 2018. [Online]. Available through: <www.accountingtools.com/articles/ratio-

analysis.html>

7

Books and Journals:

Basak, S. and Makarov, D., 2014. Strategic asset allocation in money management. The Journal

of Finance. 69(1). pp.179-217.

Boonstra, A., 2013. How do top managers support strategic information system projects and why

do they sometimes withhold this support?. International Journal of Project

Management. 31(4). pp.498-512.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic management journal. 35(1). pp.1-23.

Cheng, M. M. and Humphreys, K. A., 2012. The differential improvement effects of the strategy

map and scorecard perspectives on managers' strategic judgments. The Accounting

Review. 87(3). pp.899-924.

Dewulf, G., Blanken, A. and Bult-Spiering, M., 2012. Strategic issues in public-private

partnerships. London, England: Wiley-Blackwell.

Gorbenko, A. S. and Malenko, A., 2014. Strategic and financial bidders in takeover auctions. The

Journal of Finance. 69(6). pp.2513-2555.

Smit, H. T. and Trigeorgis, L., 2012. Strategic investment: Real options and games. Princeton

University Press.

Ward, K., 2012. Strategic management accounting. Routledge.

Wheelen, T. L. and Hunger, J. D., 2011. Concepts in strategic management and business policy.

Pearson Education India.

Wuttke, D. A., and et. al., 2013. Managing the innovation adoption of supply chain finance—

Empirical evidence from six European case studies. Journal of Business Logistics.

34(2). pp.148-166.

Online

Ratio Analysis, 2018. [Online]. Available through: <www.accountingtools.com/articles/ratio-

analysis.html>

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

1. financial statements of Samsung PLC

Income Statement

Period ending 12/31/2017 12/31/2016

Total Revenue 239580000000 201866745000

Cost of Revenue 129290000000 120277715000

Gross Profit 110290000000 81589030000

Operating Expenses

Research Development 16360000000 14111381000

Selling General and

Administrative 40280000000 37235161000

Total Operating Expenses 185930000000 172626073000

Operating Income or Loss 53650000000 29240672000

Income from Continuing

Operations

Total Other

Income/Expenses Net 2550000000 1472980000

Earnings Before Interest

and Taxes 53650000000 29240672000

Interest Expense - -587831000

Income Before Tax 56200000000 30713652000

Income Tax Expense 14010000000 7987560000

Minority Interest - 6538705000

Net Income From

Continuing Ops 42190000000 22726092000

Net Income 42190000000 22415655000

Balance Sheet

8

1. financial statements of Samsung PLC

Income Statement

Period ending 12/31/2017 12/31/2016

Total Revenue 239580000000 201866745000

Cost of Revenue 129290000000 120277715000

Gross Profit 110290000000 81589030000

Operating Expenses

Research Development 16360000000 14111381000

Selling General and

Administrative 40280000000 37235161000

Total Operating Expenses 185930000000 172626073000

Operating Income or Loss 53650000000 29240672000

Income from Continuing

Operations

Total Other

Income/Expenses Net 2550000000 1472980000

Earnings Before Interest

and Taxes 53650000000 29240672000

Interest Expense - -587831000

Income Before Tax 56200000000 30713652000

Income Tax Expense 14010000000 7987560000

Minority Interest - 6538705000

Net Income From

Continuing Ops 42190000000 22726092000

Net Income 42190000000 22415655000

Balance Sheet

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Period Ending 12/31/2017 12/31/2016

Current Assets

Cash And Cash

Equivalents 83604400000 32111442000

Short Term Investments - 56049330000

Net Receivables 27696000000 27800408000

Inventory 24983400000 18353503000

Other Current Assets - 3612938000

Total Current Assets 136283800000 141429704000

Long Term Investments 16644200000 12642160000

Property Plant and

Equipment 111665600000 91473041000

Goodwill - 1343580000

Intangible Assets 14760500000 2819822000

Other Assets 22398000000 12466017000

Deferred Long Term

Asset Charges - 5321450000

Total Assets 301752100000 262174324000

Current Liabilities

Accounts Payable 9083900000 6485039000

Short/Current Long Term

Debt 18814000000 15282386000

Other Current Liabilities 7408300000 21712150000

Total Current Liabilities 16492200000 54704095000

Long Term Debt 18814000000 1237653000

Other Liabilities 51954500000 13204416000

Deferred Long Term

Liability Charges - 1180618000

Minority Interest - 6538705000

9

Current Assets

Cash And Cash

Equivalents 83604400000 32111442000

Short Term Investments - 56049330000

Net Receivables 27696000000 27800408000

Inventory 24983400000 18353503000

Other Current Assets - 3612938000

Total Current Assets 136283800000 141429704000

Long Term Investments 16644200000 12642160000

Property Plant and

Equipment 111665600000 91473041000

Goodwill - 1343580000

Intangible Assets 14760500000 2819822000

Other Assets 22398000000 12466017000

Deferred Long Term

Asset Charges - 5321450000

Total Assets 301752100000 262174324000

Current Liabilities

Accounts Payable 9083900000 6485039000

Short/Current Long Term

Debt 18814000000 15282386000

Other Current Liabilities 7408300000 21712150000

Total Current Liabilities 16492200000 54704095000

Long Term Debt 18814000000 1237653000

Other Liabilities 51954500000 13204416000

Deferred Long Term

Liability Charges - 1180618000

Minority Interest - 6538705000

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.