Tesco's Financial Analysis: Finance for Strategic Managers Report

VerifiedAdded on 2021/02/20

|17

|5944

|31

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco, a major multinational retailer. It begins by outlining the financial information needs of a business and the associated risks in decision-making. The report then delves into the structure and content of published accounts, using Tesco as a case study to interpret financial information and calculate key financial ratios such as current ratio, acid test ratio, debtor days, and creditor days. The analysis extends to differentiating between short and long-term finance requirements, comparing financing sources, and assessing cash flow management techniques. Furthermore, the report evaluates methods for appraising strategic capital or investment projects and examines the corporate governance and regulatory aspects of different business ownership structures. The report incorporates Tesco's financial data to illustrate key concepts and support strategic business decision-making processes.

Finance for Strategic Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

LO 1......................................................................................................................................................3

1.1 Assessing the financial information needs of the business........................................................3

1.2 Identifying risks associated with the financial and business decision making process.............4

1.3. Summarising financial information as required in the process of strategic business decision

making.............................................................................................................................................5

LO 2......................................................................................................................................................6

2.1 Explaining the structure and content of the published accounts................................................6

2.2 Interpreting financial information in published accounts of Tesco...........................................6

2.3 Calculate financial ratios from published accounts to support strategic business decision-

making.............................................................................................................................................7

LO 3......................................................................................................................................................9

3.1 Differentiating between long and short term finance requirements for business.....................9

3.2 Compare the sources of long and short-term finance for businesses.......................................10

3.3 Assessing importance of managing cash flow and techniques................................................11

3.4 Evaluating methods for appraising strategic capital or investment projects...........................11

LO 4....................................................................................................................................................12

4.1 Analyse the corporate governance, legal and regulatory requirements of different business

ownership structures......................................................................................................................12

4.2 Capital investment appraisal ...................................................................................................13

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................16

INTRODUCTION................................................................................................................................3

LO 1......................................................................................................................................................3

1.1 Assessing the financial information needs of the business........................................................3

1.2 Identifying risks associated with the financial and business decision making process.............4

1.3. Summarising financial information as required in the process of strategic business decision

making.............................................................................................................................................5

LO 2......................................................................................................................................................6

2.1 Explaining the structure and content of the published accounts................................................6

2.2 Interpreting financial information in published accounts of Tesco...........................................6

2.3 Calculate financial ratios from published accounts to support strategic business decision-

making.............................................................................................................................................7

LO 3......................................................................................................................................................9

3.1 Differentiating between long and short term finance requirements for business.....................9

3.2 Compare the sources of long and short-term finance for businesses.......................................10

3.3 Assessing importance of managing cash flow and techniques................................................11

3.4 Evaluating methods for appraising strategic capital or investment projects...........................11

LO 4....................................................................................................................................................12

4.1 Analyse the corporate governance, legal and regulatory requirements of different business

ownership structures......................................................................................................................12

4.2 Capital investment appraisal ...................................................................................................13

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................16

INTRODUCTION

Financial management is concerned with the effective as well as efficient allocation of available

business funds and resources in business operations. With the help of strategies, plans and policies

every business organization can make proper utilization of its limited business and financial

resources. By formulating budget and financial plans, a company can achieve its business goals in a

cost effective manner easily. The present report is based on Tesco plc, which is a British

multinational groceries and merchandise retail store having its headquarters in England, United

Kingdom. Tesco is engaged in business chains in form of Super market, Super store and

Convenience shop across different places. The report will discuss about different types of financial

information which are required for making strategic business decision. It will also define risk

associated with the financial as well as business decision. Further the report will explain the concept

of published accounts along with its structure base. Also, it will explain the point of difference

between long and short term finance requirements for business and aspect related to the cash flow

management techniques. At last, the report will streamline about the basic requirement related to the

corporate governance, legal and regulatory framework of different business ownership structures. It

will also depict how it assists the managers in their decision making process.

MAIN BODY

LO 1

1.1 Assessing the financial information needs of the business.

Financial information plays crucial role in every business organization as it is the base on

which all the decisions are made by the management of the company. Managers requires high

quality and reliable financial information so as to assign the resources of the company as per the

needs of its business operations efficiently for meeting all the strategic objectives. By making

correct and accurate use of available financial information and its assignment in number of financial

management techniques can help Tesco in successful decision making. By making correct analysis

of the financial statements, meaningful as well as useful information can be evaluated from it.

With the help of financial information, both the owner and managers can have better

understanding regarding the overall business health, liquidity as well as solvency position for a

specific period of time (Attig and El Ghoul, 2018). It depicts about the current position of business

assets, capital, its net worth and the amount of liabilities due at a particular time period. It also

assists stakeholders and investors of Tesco in assessing their own wealth creation made by profit

earned by the company. Financial statements thus provides several types of financial information by

Financial management is concerned with the effective as well as efficient allocation of available

business funds and resources in business operations. With the help of strategies, plans and policies

every business organization can make proper utilization of its limited business and financial

resources. By formulating budget and financial plans, a company can achieve its business goals in a

cost effective manner easily. The present report is based on Tesco plc, which is a British

multinational groceries and merchandise retail store having its headquarters in England, United

Kingdom. Tesco is engaged in business chains in form of Super market, Super store and

Convenience shop across different places. The report will discuss about different types of financial

information which are required for making strategic business decision. It will also define risk

associated with the financial as well as business decision. Further the report will explain the concept

of published accounts along with its structure base. Also, it will explain the point of difference

between long and short term finance requirements for business and aspect related to the cash flow

management techniques. At last, the report will streamline about the basic requirement related to the

corporate governance, legal and regulatory framework of different business ownership structures. It

will also depict how it assists the managers in their decision making process.

MAIN BODY

LO 1

1.1 Assessing the financial information needs of the business.

Financial information plays crucial role in every business organization as it is the base on

which all the decisions are made by the management of the company. Managers requires high

quality and reliable financial information so as to assign the resources of the company as per the

needs of its business operations efficiently for meeting all the strategic objectives. By making

correct and accurate use of available financial information and its assignment in number of financial

management techniques can help Tesco in successful decision making. By making correct analysis

of the financial statements, meaningful as well as useful information can be evaluated from it.

With the help of financial information, both the owner and managers can have better

understanding regarding the overall business health, liquidity as well as solvency position for a

specific period of time (Attig and El Ghoul, 2018). It depicts about the current position of business

assets, capital, its net worth and the amount of liabilities due at a particular time period. It also

assists stakeholders and investors of Tesco in assessing their own wealth creation made by profit

earned by the company. Financial statements thus provides several types of financial information by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

use of which both the investors and creditors can easily evaluates the current financial performance

and position of Tesco. On the basis of financial information, the management of Tesco can

formulate sound business policies, plans and strategies for the betterment of its business, improving

overall efficiency of its business operations, maximization profit level etc. With these statements,

investors can evaluates past performance of Tesco and also can determine the future cash flows for

a specific time period. Also, the amount of cash inflow and outflow can be monitored for a time

period and measures can be taken for reducing cost expenses associated with unproductive and

unnecessary business department thereby increasing the overall profitability and performance level.

1.2 Identifying risks associated with the financial and business decision making process.

The term financial management is associated with the process of managing, controlling and

monitoring of business assets, liabilities, resources in an effective and efficient manner with the aim

of betterment of business operations and performance. While carrying on business, company has to

face many types of risk which creates direct impact on the profitability aspect. For mitigating risk

associated, proper risk management plan has to be made by the management of Tesco. Risk

management process is a technique related to the process of internal monitoring and controlling

business operations thereby ensuring system efficiency. It also focuses on making proper

compliance with set defined business standards, norms for achieving business goals and objectives.

It also facilitates achievement of business targets of Tesco by identifying and analysing cost and risk

factors and thus controlling it for overcoming unnecessary business losses. Different types of

financial risk are there which has to be minimized by formulating sound business policies such as:

1. Market Risk – It is the type of risk associated with the business which is being exposed to

the adverse market movements. It is a type of systematic risk which cannot be eliminated

and is related with bad performance of the financial markets factors such as interest rates,

recessions etc.

2. Interest Rate Risk – It arises as a result of fluctuations in the interest rates from time to

time because of financial market and share market fluctuations.

3. Purchasing power Risk – Also known as Inflation risk, it is the possibility of having an

adverse effect on the value of money created by inflationary pressures prevailing in the

economy of the country (DeBoeuf and et.al., 2018).

4. Credit Risk – Is a risk in which borrower’s has fail to meet its contract obligations resulting

investors as well as lenders of Tesco in a position to lose out in the collection process of

costs, interest and cash flow.

5. Liquidity Risk – Is a type of risk in which company is having inability to realise its own

current and liquid assets such as investment etc. within a required time frame for minimizing

and position of Tesco. On the basis of financial information, the management of Tesco can

formulate sound business policies, plans and strategies for the betterment of its business, improving

overall efficiency of its business operations, maximization profit level etc. With these statements,

investors can evaluates past performance of Tesco and also can determine the future cash flows for

a specific time period. Also, the amount of cash inflow and outflow can be monitored for a time

period and measures can be taken for reducing cost expenses associated with unproductive and

unnecessary business department thereby increasing the overall profitability and performance level.

1.2 Identifying risks associated with the financial and business decision making process.

The term financial management is associated with the process of managing, controlling and

monitoring of business assets, liabilities, resources in an effective and efficient manner with the aim

of betterment of business operations and performance. While carrying on business, company has to

face many types of risk which creates direct impact on the profitability aspect. For mitigating risk

associated, proper risk management plan has to be made by the management of Tesco. Risk

management process is a technique related to the process of internal monitoring and controlling

business operations thereby ensuring system efficiency. It also focuses on making proper

compliance with set defined business standards, norms for achieving business goals and objectives.

It also facilitates achievement of business targets of Tesco by identifying and analysing cost and risk

factors and thus controlling it for overcoming unnecessary business losses. Different types of

financial risk are there which has to be minimized by formulating sound business policies such as:

1. Market Risk – It is the type of risk associated with the business which is being exposed to

the adverse market movements. It is a type of systematic risk which cannot be eliminated

and is related with bad performance of the financial markets factors such as interest rates,

recessions etc.

2. Interest Rate Risk – It arises as a result of fluctuations in the interest rates from time to

time because of financial market and share market fluctuations.

3. Purchasing power Risk – Also known as Inflation risk, it is the possibility of having an

adverse effect on the value of money created by inflationary pressures prevailing in the

economy of the country (DeBoeuf and et.al., 2018).

4. Credit Risk – Is a risk in which borrower’s has fail to meet its contract obligations resulting

investors as well as lenders of Tesco in a position to lose out in the collection process of

costs, interest and cash flow.

5. Liquidity Risk – Is a type of risk in which company is having inability to realise its own

current and liquid assets such as investment etc. within a required time frame for minimizing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business loss. It is position in which the company is not able to meet its short term financial

demands.

6. Operational Risk – Is associated with the profitability and performance aspects of the

business which is getting affected by the negative rumours, bad quality services and

products, continuous legal proceedings and non compliances made by the company. It thus

affects the overall profitability, performance and customer base of the company resulting in

business loss.

1.3. Summarising financial information as required in the process of strategic business decision

making.

For business organization either of small size or big size, profitability, growth, success and

customer satisfaction are considered as one of the most important factors which has to be taken into

consideration while formulating any new business plans. At the time of preparation of financial

plans or budget all the relevant and crucial information of statistical, accounting as well as financial

nature has to be consider for the betterment of business goals and objectives. Following information

has to be considered at time of making strategic business decision viz.:

1. Projection of operational cost – Forecasting has to be done in context of business cost

which are going to be incurred for carrying on different business operations and activities.

Every financial statement has to depict about estimated cost and the actual cost incurred

during a specific period of time. The cost projection feature helps Tesco in making estimates

about current and capital assets level, amount of expenses to be incurred for starting any

new business operation. By making proper estimates related to cost expenditure, Tesco can

make high profit margins and makes improvement in its business activities.

2. Balance Sheet & Statement of Income – With the help of these financials, one can

ascertain deep information related to the financial health and current position of the

company on the basis of which future as well as present decision can be made effectively

(Coleman, Cotei and Farhat, 2016). Also, the statement of income depicts figure related to

sales, revenue, loss and cost expenses made during a specific time period.

3. Cash flow statement – It provides details related to inflow and outflow activities of cash

and fund resources of the business for definite time. It also assists in making projections

related to the process of allocation of cash amount for minimizing unnecessary cost

expenses and for maximizing profit level as well.

demands.

6. Operational Risk – Is associated with the profitability and performance aspects of the

business which is getting affected by the negative rumours, bad quality services and

products, continuous legal proceedings and non compliances made by the company. It thus

affects the overall profitability, performance and customer base of the company resulting in

business loss.

1.3. Summarising financial information as required in the process of strategic business decision

making.

For business organization either of small size or big size, profitability, growth, success and

customer satisfaction are considered as one of the most important factors which has to be taken into

consideration while formulating any new business plans. At the time of preparation of financial

plans or budget all the relevant and crucial information of statistical, accounting as well as financial

nature has to be consider for the betterment of business goals and objectives. Following information

has to be considered at time of making strategic business decision viz.:

1. Projection of operational cost – Forecasting has to be done in context of business cost

which are going to be incurred for carrying on different business operations and activities.

Every financial statement has to depict about estimated cost and the actual cost incurred

during a specific period of time. The cost projection feature helps Tesco in making estimates

about current and capital assets level, amount of expenses to be incurred for starting any

new business operation. By making proper estimates related to cost expenditure, Tesco can

make high profit margins and makes improvement in its business activities.

2. Balance Sheet & Statement of Income – With the help of these financials, one can

ascertain deep information related to the financial health and current position of the

company on the basis of which future as well as present decision can be made effectively

(Coleman, Cotei and Farhat, 2016). Also, the statement of income depicts figure related to

sales, revenue, loss and cost expenses made during a specific time period.

3. Cash flow statement – It provides details related to inflow and outflow activities of cash

and fund resources of the business for definite time. It also assists in making projections

related to the process of allocation of cash amount for minimizing unnecessary cost

expenses and for maximizing profit level as well.

LO 2

2.1 Explaining the structure and content of the published accounts.

Published accounts are those accounts of company which are published with the purpose of

providing greater publicity to the business. It also enables its members, stakeholders, investors and

public on the large basis for providing better understanding about the aspects related to profitability

and financial positions of the business (Drover and et.al., 2017). These are those accounts or

statements which has to be published as per the relevant applicable rules, regulation, provisions and

laws for providing clear and true picture about the financial position of the company.

The objective behind preparation of published accounts is to provide accurate information

about performance level for a particular financial year related to different business aspects such as

production, sales, profit and cost expenses. It also facilitates comparison between present and past

financials and variances depicted are overcome by formulating effective strategies.

The main contents of published accounts of any business organization are as follows:

1. The Chairman and CEO Statement

2. Priorities of company

3. Business model use

4. Financial review

5. Environmental and social review

6. Risk and uncertainites faced

7. Corporate governance

8. Directors Report

9. Auditors Report

10. Statement of Income

11. Statement of Changes in Financial Position

12. The annotated version of the balance sheet of the company

13. Statement of Cash flow for the period ended

14. Annexures

2.2 Interpreting financial information in published accounts of Tesco.

As per the market segmentation performance level, Tesco has been growing with rapid rate

across the globe. The net income of the company for the financial year 2019 is £1,320 million with

450,000 number of employees presently working for its. Also, the revenue made by the company

for the year 2019 is £63,911 million and operating income of £2,206 million for the same

accounting year.

2.1 Explaining the structure and content of the published accounts.

Published accounts are those accounts of company which are published with the purpose of

providing greater publicity to the business. It also enables its members, stakeholders, investors and

public on the large basis for providing better understanding about the aspects related to profitability

and financial positions of the business (Drover and et.al., 2017). These are those accounts or

statements which has to be published as per the relevant applicable rules, regulation, provisions and

laws for providing clear and true picture about the financial position of the company.

The objective behind preparation of published accounts is to provide accurate information

about performance level for a particular financial year related to different business aspects such as

production, sales, profit and cost expenses. It also facilitates comparison between present and past

financials and variances depicted are overcome by formulating effective strategies.

The main contents of published accounts of any business organization are as follows:

1. The Chairman and CEO Statement

2. Priorities of company

3. Business model use

4. Financial review

5. Environmental and social review

6. Risk and uncertainites faced

7. Corporate governance

8. Directors Report

9. Auditors Report

10. Statement of Income

11. Statement of Changes in Financial Position

12. The annotated version of the balance sheet of the company

13. Statement of Cash flow for the period ended

14. Annexures

2.2 Interpreting financial information in published accounts of Tesco.

As per the market segmentation performance level, Tesco has been growing with rapid rate

across the globe. The net income of the company for the financial year 2019 is £1,320 million with

450,000 number of employees presently working for its. Also, the revenue made by the company

for the year 2019 is £63,911 million and operating income of £2,206 million for the same

accounting year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tesco has been operating in different part of the world with around 6800 number of shops.

Also, it has become the third largest retailer across the globe in term of gross revenues till the year

2019. When it is measured in terms of revenues factor, Tesco has been the ninth largest retail store

in the world having its operational business and shops in approximately seven different countries. It

has also become market leader in the business of groceries in the United Kingdom having market

share of around 28.4% (Tesco plc, 2019).

2.3 Calculate financial ratios from published accounts to support strategic business decision-making

Particulars 2018 (in £m) 2019 (in £m)

1. Current Ratio

Current Assets 13600 12570

Current Liabilities 19233 20680

Current Ratio = Current

Assets/ Current Liabilities 0.71 0.61

2. Acid Test Ratio

Quick Asset 11336 9953

Current Liabilities 19233 20680

Acid Test Ratio = Current

Assets/ Current Liabilities 0.589 0.481

3. Debtor days

Trade Debtors 1504 1640

Revenue Sales 57493 63911

Debtor days = (Trade

Debtors/Revenue Sales) *

365

9.55 9.37

4. Creditor days

Trade Payables 8994 9354

Cost of Sales 54141 59767

Creditor days = (Trade

Payables/Cost of

Sales)*365

60.63 57.13

5. Gross profit margin

Gross Margin 3352 4144

Total Revenue 57493 63911

Gross Margin Ratio =

Gross Margin/ Total

Revenue

0.06 0.06

6. Operating Profit

Margin

Operating Profit 1839 2153

Total Revenue 57493 63911

Also, it has become the third largest retailer across the globe in term of gross revenues till the year

2019. When it is measured in terms of revenues factor, Tesco has been the ninth largest retail store

in the world having its operational business and shops in approximately seven different countries. It

has also become market leader in the business of groceries in the United Kingdom having market

share of around 28.4% (Tesco plc, 2019).

2.3 Calculate financial ratios from published accounts to support strategic business decision-making

Particulars 2018 (in £m) 2019 (in £m)

1. Current Ratio

Current Assets 13600 12570

Current Liabilities 19233 20680

Current Ratio = Current

Assets/ Current Liabilities 0.71 0.61

2. Acid Test Ratio

Quick Asset 11336 9953

Current Liabilities 19233 20680

Acid Test Ratio = Current

Assets/ Current Liabilities 0.589 0.481

3. Debtor days

Trade Debtors 1504 1640

Revenue Sales 57493 63911

Debtor days = (Trade

Debtors/Revenue Sales) *

365

9.55 9.37

4. Creditor days

Trade Payables 8994 9354

Cost of Sales 54141 59767

Creditor days = (Trade

Payables/Cost of

Sales)*365

60.63 57.13

5. Gross profit margin

Gross Margin 3352 4144

Total Revenue 57493 63911

Gross Margin Ratio =

Gross Margin/ Total

Revenue

0.06 0.06

6. Operating Profit

Margin

Operating Profit 1839 2153

Total Revenue 57493 63911

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating Profit Margin =

Operating Profit /Total

Revenue

0.03 0.03

7. Working capital

Current Assets 13600 12570

Current Liabilities 19233 20680

Working capital = Current

Assets – Current Liabilities -5633.00 -8110.00

8. Debt to equity

Total liabilities 34404 34213

Total Stockholders’ Equity 10480 14834

Debt to equity = Total

liabilities / Total

Stockholders’ Equity

3.28 2.31

(Annual report of Tesco plc, 2019)

Interpretation

1. Current Ratio – It defines the overall liquidity position of the business along with the

financial health and position. It helps in determining whether Tesco has made use of its

available current assets of the business for meeting its short term business obligations. The

ratio determines for the year are 0.71 and 0.61 for 2018 & 2019 respectively. It depicts that

it is matter of concern for the company as it will not able to meet its upcoming business

obligation in near future.

2. Acid Test Ratio – Also known as Quick Ratio which helps in determining the overall

business strength and solvency position of the business. The ratio calculated for Tesco are

0.589 and 0.481 for year 2018 and 2019. It helps in assessing how quickly the assets of

business will turn into liquid or cash for meeting its business obligation as and when arises.

3. Debtor days – It helps in determining the average time period in which the company will be

able to recover its debt amount due from its customer and other vendors against the amount

of credit sales made. Tesco will be able to get its amount back in 9.55 & 9.37 days which is

good for company as it will help company in remaining liquid and meeting cash

requirements.

4. Creditor days – Defines time in which company will repay all its business obligations due

against credit purchase made from its suppliers, lenders etc. The company should always

focus on increasing its creditors period as it will help the company in remaining liquid and

ensures proper availability of cash. Ratio calculated is 60.63 & 57.13 which is good for

Tesco.

Operating Profit /Total

Revenue

0.03 0.03

7. Working capital

Current Assets 13600 12570

Current Liabilities 19233 20680

Working capital = Current

Assets – Current Liabilities -5633.00 -8110.00

8. Debt to equity

Total liabilities 34404 34213

Total Stockholders’ Equity 10480 14834

Debt to equity = Total

liabilities / Total

Stockholders’ Equity

3.28 2.31

(Annual report of Tesco plc, 2019)

Interpretation

1. Current Ratio – It defines the overall liquidity position of the business along with the

financial health and position. It helps in determining whether Tesco has made use of its

available current assets of the business for meeting its short term business obligations. The

ratio determines for the year are 0.71 and 0.61 for 2018 & 2019 respectively. It depicts that

it is matter of concern for the company as it will not able to meet its upcoming business

obligation in near future.

2. Acid Test Ratio – Also known as Quick Ratio which helps in determining the overall

business strength and solvency position of the business. The ratio calculated for Tesco are

0.589 and 0.481 for year 2018 and 2019. It helps in assessing how quickly the assets of

business will turn into liquid or cash for meeting its business obligation as and when arises.

3. Debtor days – It helps in determining the average time period in which the company will be

able to recover its debt amount due from its customer and other vendors against the amount

of credit sales made. Tesco will be able to get its amount back in 9.55 & 9.37 days which is

good for company as it will help company in remaining liquid and meeting cash

requirements.

4. Creditor days – Defines time in which company will repay all its business obligations due

against credit purchase made from its suppliers, lenders etc. The company should always

focus on increasing its creditors period as it will help the company in remaining liquid and

ensures proper availability of cash. Ratio calculated is 60.63 & 57.13 which is good for

Tesco.

5. Gross profit margin – Is amount of revenue which has been received after making all the

business related expenses from the sales amount. 0.06 is the profit margin remaining for

Tesco after deducting all the business expenses.

6. Operating Profit Margin – It determines the efficiency level of its business operations. Is

amount which is left after paying all business expenses including variable expenses too. 0.03

is operating profit margin for Tesco for year 2018 & 2019.

7. Working capital – Is a concept which measures liquidity of business & assess the capability

for paying its obligations due. For Tesco working capital available is -5633 & -8110 for the

year 2018 & 2019.

8. Debt to equity – It determines the part of creditors, shareholders & owners in the capital

employed part of the business. It helps in assessing how better Tesco has used its available

business capital resources for making profit. Ratio calculated is 3.28 & 2.31 for 2018 &

2019 respectively.

LO 3

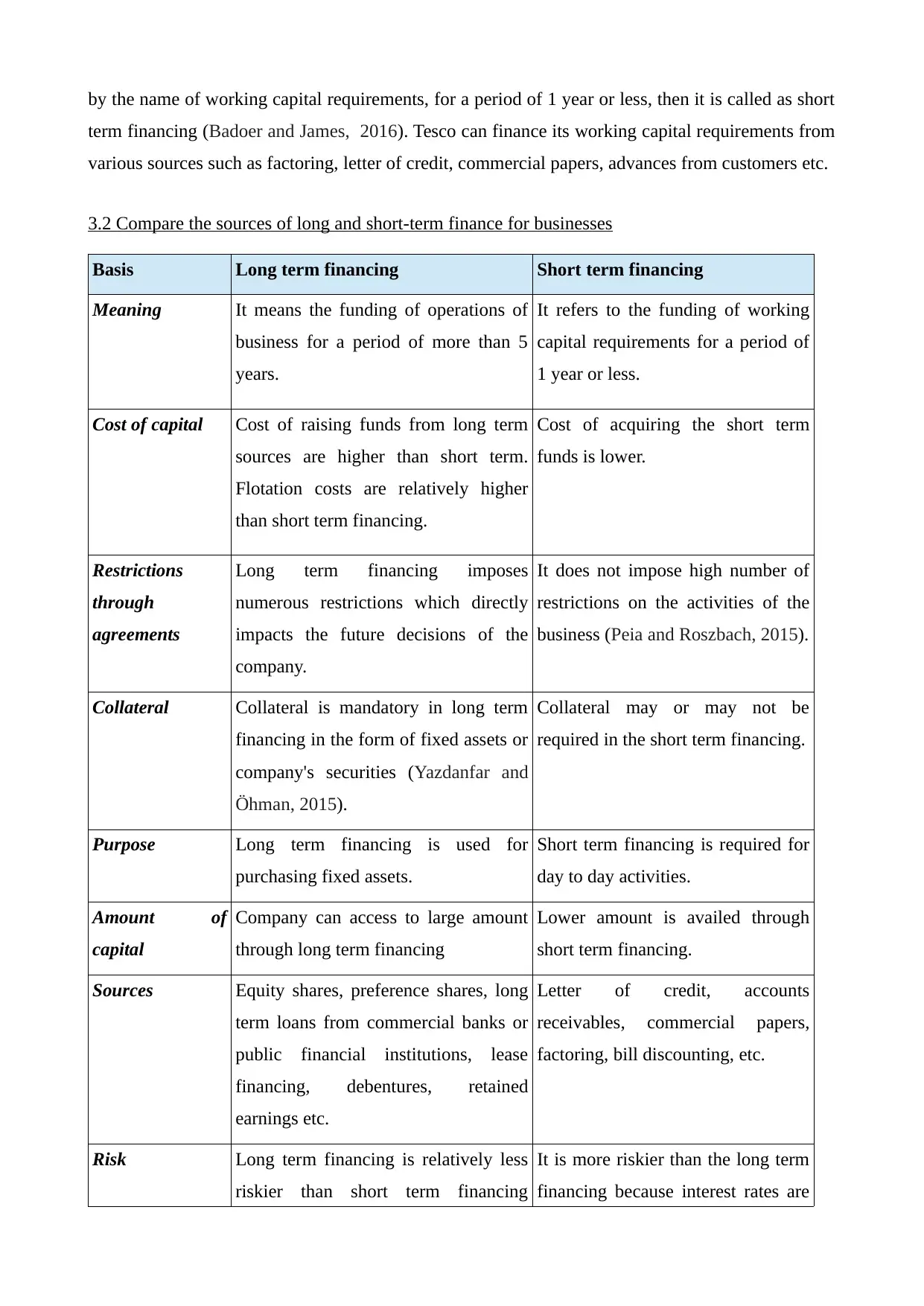

3.1 Differentiating between long and short term finance requirements for business

An organisation needs funds for operating and running its business both for shorter and

longer duration. There are different sources through a company generate its funds which are

categorised on the basis of ownership, time duration, internal or external etc.

Long term finance :

A business requires long term for the purpose of acquiring fixed assets such as land,

building, plant & machinery. Long term finance signifies the funds which is required for more than

5 years for financing the long term expenditure of the company (Véron and Wolff, 2016). Tesco can

finance its long fixed capital by the way of preference share, equity share, long term loans, lease,

retained earnings, financing from international institutions.

Medium term finance :

When the funds are required for a period of more than 1 to 5 years, then its known as

medium term financing of the operations of the company. It is usually raised for financing the

deferred revenue expenditures such as advertisements expenses (Pilbeam, 2018). There are various

sources through which Tesco can avail medium funds such as accruals, bill financing, installment

credit, hire purchasing etc.

Short term finance :

Funds when are needed for financing the routine operations of the company usually known

business related expenses from the sales amount. 0.06 is the profit margin remaining for

Tesco after deducting all the business expenses.

6. Operating Profit Margin – It determines the efficiency level of its business operations. Is

amount which is left after paying all business expenses including variable expenses too. 0.03

is operating profit margin for Tesco for year 2018 & 2019.

7. Working capital – Is a concept which measures liquidity of business & assess the capability

for paying its obligations due. For Tesco working capital available is -5633 & -8110 for the

year 2018 & 2019.

8. Debt to equity – It determines the part of creditors, shareholders & owners in the capital

employed part of the business. It helps in assessing how better Tesco has used its available

business capital resources for making profit. Ratio calculated is 3.28 & 2.31 for 2018 &

2019 respectively.

LO 3

3.1 Differentiating between long and short term finance requirements for business

An organisation needs funds for operating and running its business both for shorter and

longer duration. There are different sources through a company generate its funds which are

categorised on the basis of ownership, time duration, internal or external etc.

Long term finance :

A business requires long term for the purpose of acquiring fixed assets such as land,

building, plant & machinery. Long term finance signifies the funds which is required for more than

5 years for financing the long term expenditure of the company (Véron and Wolff, 2016). Tesco can

finance its long fixed capital by the way of preference share, equity share, long term loans, lease,

retained earnings, financing from international institutions.

Medium term finance :

When the funds are required for a period of more than 1 to 5 years, then its known as

medium term financing of the operations of the company. It is usually raised for financing the

deferred revenue expenditures such as advertisements expenses (Pilbeam, 2018). There are various

sources through which Tesco can avail medium funds such as accruals, bill financing, installment

credit, hire purchasing etc.

Short term finance :

Funds when are needed for financing the routine operations of the company usually known

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by the name of working capital requirements, for a period of 1 year or less, then it is called as short

term financing (Badoer and James, 2016). Tesco can finance its working capital requirements from

various sources such as factoring, letter of credit, commercial papers, advances from customers etc.

3.2 Compare the sources of long and short-term finance for businesses

Basis Long term financing Short term financing

Meaning It means the funding of operations of

business for a period of more than 5

years.

It refers to the funding of working

capital requirements for a period of

1 year or less.

Cost of capital Cost of raising funds from long term

sources are higher than short term.

Flotation costs are relatively higher

than short term financing.

Cost of acquiring the short term

funds is lower.

Restrictions

through

agreements

Long term financing imposes

numerous restrictions which directly

impacts the future decisions of the

company.

It does not impose high number of

restrictions on the activities of the

business (Peia and Roszbach, 2015).

Collateral Collateral is mandatory in long term

financing in the form of fixed assets or

company's securities (Yazdanfar and

Öhman, 2015).

Collateral may or may not be

required in the short term financing.

Purpose Long term financing is used for

purchasing fixed assets.

Short term financing is required for

day to day activities.

Amount of

capital

Company can access to large amount

through long term financing

Lower amount is availed through

short term financing.

Sources Equity shares, preference shares, long

term loans from commercial banks or

public financial institutions, lease

financing, debentures, retained

earnings etc.

Letter of credit, accounts

receivables, commercial papers,

factoring, bill discounting, etc.

Risk Long term financing is relatively less

riskier than short term financing

It is more riskier than the long term

financing because interest rates are

term financing (Badoer and James, 2016). Tesco can finance its working capital requirements from

various sources such as factoring, letter of credit, commercial papers, advances from customers etc.

3.2 Compare the sources of long and short-term finance for businesses

Basis Long term financing Short term financing

Meaning It means the funding of operations of

business for a period of more than 5

years.

It refers to the funding of working

capital requirements for a period of

1 year or less.

Cost of capital Cost of raising funds from long term

sources are higher than short term.

Flotation costs are relatively higher

than short term financing.

Cost of acquiring the short term

funds is lower.

Restrictions

through

agreements

Long term financing imposes

numerous restrictions which directly

impacts the future decisions of the

company.

It does not impose high number of

restrictions on the activities of the

business (Peia and Roszbach, 2015).

Collateral Collateral is mandatory in long term

financing in the form of fixed assets or

company's securities (Yazdanfar and

Öhman, 2015).

Collateral may or may not be

required in the short term financing.

Purpose Long term financing is used for

purchasing fixed assets.

Short term financing is required for

day to day activities.

Amount of

capital

Company can access to large amount

through long term financing

Lower amount is availed through

short term financing.

Sources Equity shares, preference shares, long

term loans from commercial banks or

public financial institutions, lease

financing, debentures, retained

earnings etc.

Letter of credit, accounts

receivables, commercial papers,

factoring, bill discounting, etc.

Risk Long term financing is relatively less

riskier than short term financing

It is more riskier than the long term

financing because interest rates are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

because of the fact that interest rate is

stable and temporary rescission does

not greatly impacts the interest rates.

highly subject to market forces.

3.3 Assessing importance of managing cash flow and techniques.

Cash flow management is a technique of monitoring, evaluating, controlling and assessing

the amount of cash and funds resources taking place in the business for a specific period of time.

With the help of cash flow management process, a company can have full information about the

amount of cash revenue made and expenses done for a particular time period. Importance of cash

flow management are:

1. It helps in formulation sound financial plans and budget for the next or specific time frame.

2. It also helps in identification and minimising unnecessary cost expenses associated with

unproductive business operations.

3. Also, it assist in making proper allocation of cash amount for a particular business operation

and for department too (Häcker and Ernst, 2017).

Cash flow management techniques are as follows:

1. Monitoring properly each business transaction of the company for having full knowledge

about cash inflow and outflow.

2. Keeping a track of customer account or accounts receivables for timely recovery of amount

due and for minimising default risk.

3. By properly monitoring cost expenses and formulating sound business policies and

strategies related to allocation of cost and cash amount.

3.4 Evaluating methods for appraising strategic capital or investment projects.

Net Present Value (NPV): The net present value of the company take into consideration

various cash flows occurred at different period. This method take into account time value of money.

The positive cash inflows indicates that the cash inflows exceeds cash outflows. The negative cash

flows indicates that the cash outflows are more than the cash inflows and leads to higher losses.

When NPV is zero it states that the cash inflows is equal to the cash outflows. The company will

neither make profit nor loss.

Internal Rate of Return (IRR): The IRR is an effective metrics which evaluates the

amount of profits earned from the potential investment (Patrick and French, 2016). Higher the IRR

stable and temporary rescission does

not greatly impacts the interest rates.

highly subject to market forces.

3.3 Assessing importance of managing cash flow and techniques.

Cash flow management is a technique of monitoring, evaluating, controlling and assessing

the amount of cash and funds resources taking place in the business for a specific period of time.

With the help of cash flow management process, a company can have full information about the

amount of cash revenue made and expenses done for a particular time period. Importance of cash

flow management are:

1. It helps in formulation sound financial plans and budget for the next or specific time frame.

2. It also helps in identification and minimising unnecessary cost expenses associated with

unproductive business operations.

3. Also, it assist in making proper allocation of cash amount for a particular business operation

and for department too (Häcker and Ernst, 2017).

Cash flow management techniques are as follows:

1. Monitoring properly each business transaction of the company for having full knowledge

about cash inflow and outflow.

2. Keeping a track of customer account or accounts receivables for timely recovery of amount

due and for minimising default risk.

3. By properly monitoring cost expenses and formulating sound business policies and

strategies related to allocation of cost and cash amount.

3.4 Evaluating methods for appraising strategic capital or investment projects.

Net Present Value (NPV): The net present value of the company take into consideration

various cash flows occurred at different period. This method take into account time value of money.

The positive cash inflows indicates that the cash inflows exceeds cash outflows. The negative cash

flows indicates that the cash outflows are more than the cash inflows and leads to higher losses.

When NPV is zero it states that the cash inflows is equal to the cash outflows. The company will

neither make profit nor loss.

Internal Rate of Return (IRR): The IRR is an effective metrics which evaluates the

amount of profits earned from the potential investment (Patrick and French, 2016). Higher the IRR

the better the project and helps in evaluating that the project will generate higher returns.

Payback period: It is an effective tool which helps in evaluating the time required to

recover the funds invested (Al Ani, 2015. ). It helps in effectively evaluate the risk associated with

various project to re-cope the initial amount of investment (Payback period – Meaning, Usage &

Illustrations, 2019). The lower the payback period of the project higher is the benefit of the project.

LO 4

4.1 Analyse the corporate governance, legal and regulatory requirements of different business

ownership structures.

Sole trader: It is also referred to as sole proprietorship firm which is owned by the one

individual person. Owners have complete control on the business and therefore the owner of the

business is solely responsible for the debt obligations and profit of the company (Bakar and et.al.,

2016). There is no legal separation between the business entity and the owner. The owner of the

company can solely operate the business in an effective manner. The owner of the company pay tax

on the profit earned by the business.

The key advantage of the sole proprietorship company is that it is easy to set up as it does

not require to be registered and one can run the business with minimal formalities. Another major

advantage of this company is that there are very few legal regulations are there which makes it

easier for sole trader to run the business smoothly. The major disadvantage of this business is that it

has limited findings and resources. The owner of the business is solely responsible for debt

obligations.

Partnership: The partnership firm is formed when two or more than two person come

together in order to run a specific business (Rana, Allen and Liu, 2018). All the partners n the

company are responsible for the profit and loss sharing according to the particular ratios held by

them in the company. All the owners in the company are referred to as partners and collectively it is

famed as partnership firm.

Limited liability corporation: LLC is a type of organizational structure where the owners of

the company are not individually liable for the debt and liabilities of the company. The limited

liability corporation is a mixture of both partnership and corporation.

Non- profit corporation: This organization is carried out for educational, religious and

charitable purpose. This organization raises funds from public, private and public institutions, etc.

This company is run for the purpose of serving people and not for making profit.

Cooperative: It is a private business organizational structure. The profits earned by the

Payback period: It is an effective tool which helps in evaluating the time required to

recover the funds invested (Al Ani, 2015. ). It helps in effectively evaluate the risk associated with

various project to re-cope the initial amount of investment (Payback period – Meaning, Usage &

Illustrations, 2019). The lower the payback period of the project higher is the benefit of the project.

LO 4

4.1 Analyse the corporate governance, legal and regulatory requirements of different business

ownership structures.

Sole trader: It is also referred to as sole proprietorship firm which is owned by the one

individual person. Owners have complete control on the business and therefore the owner of the

business is solely responsible for the debt obligations and profit of the company (Bakar and et.al.,

2016). There is no legal separation between the business entity and the owner. The owner of the

company can solely operate the business in an effective manner. The owner of the company pay tax

on the profit earned by the business.

The key advantage of the sole proprietorship company is that it is easy to set up as it does

not require to be registered and one can run the business with minimal formalities. Another major

advantage of this company is that there are very few legal regulations are there which makes it

easier for sole trader to run the business smoothly. The major disadvantage of this business is that it

has limited findings and resources. The owner of the business is solely responsible for debt

obligations.

Partnership: The partnership firm is formed when two or more than two person come

together in order to run a specific business (Rana, Allen and Liu, 2018). All the partners n the

company are responsible for the profit and loss sharing according to the particular ratios held by

them in the company. All the owners in the company are referred to as partners and collectively it is

famed as partnership firm.

Limited liability corporation: LLC is a type of organizational structure where the owners of

the company are not individually liable for the debt and liabilities of the company. The limited

liability corporation is a mixture of both partnership and corporation.

Non- profit corporation: This organization is carried out for educational, religious and

charitable purpose. This organization raises funds from public, private and public institutions, etc.

This company is run for the purpose of serving people and not for making profit.

Cooperative: It is a private business organizational structure. The profits earned by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.