Strategic Financial Analysis Report: Booker and Tate & Lyle Comparison

VerifiedAdded on 2020/02/03

|22

|5476

|180

Report

AI Summary

This report presents a strategic financial analysis (SFA) of Booker and Tate & Lyle, two companies in the food and beverage sector. The analysis employs various financial techniques, including ratio analysis (profitability, liquidity, efficiency, and leverage), common size analysis (vertical and horizontal), and Du Pont analysis, to assess their financial performance over a five-year period (2012-2016). The report delves into the companies' backgrounds, the techniques used, and the merits and demerits of each analytical method. The core of the report involves calculating and interpreting key financial ratios to evaluate profitability, liquidity, efficiency, and leverage. It also includes an overview of contemporary methods like CAPM, EMH, and EVA. The report concludes with recommendations based on the findings, offering insights into the financial strengths and weaknesses of each company, and highlighting areas for improvement. The goal is to clarify the role of strategic financial analysis by determining their importance in the current business.

STRATEGIC FINANCIAL

ANALYSIS

ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. INTRODUCTION.......................................................................................................................4

1.1 Define SFA and importance of financial analysis............................................................4

1.2 Assignment objectives......................................................................................................4

1.3 Background of selected companies..................................................................................4

1.4 Techniques used throughout the report............................................................................5

2. RATIO ANALYSIS.....................................................................................................................5

2.1 Profitability.......................................................................................................................5

2.2 Liquidity...........................................................................................................................6

2.3 Efficiency.........................................................................................................................8

2.4 Leverage...........................................................................................................................9

2.5 Investors.........................................................................................................................10

3.0 Common size analysis..............................................................................................................11

3.1 Vertical analysis.............................................................................................................11

3.2 Horizontal analysis.........................................................................................................11

3.3 Du Pont analysis.............................................................................................................11

3.4 Segment analysis............................................................................................................11

4.0 MERITS AND DEMERITS....................................................................................................12

4.1 Ratio analysis..................................................................................................................12

4.2 Common size..................................................................................................................12

4.3 Du Pont...........................................................................................................................13

4.4 Segment analysis............................................................................................................13

5.0 CONCLUSIONS AND RECOMMENDATIONS..................................................................13

5.1 Conclusions....................................................................................................................13

5.2 Recommendations..........................................................................................................14

6.0 CONTEMPORARY METHODS ANALYSIS.......................................................................14

6.1 CAPM.............................................................................................................................14

6.2 EMH...............................................................................................................................14

6.3 EVA................................................................................................................................15

REFERENCES..............................................................................................................................16

APPENDICES.................................................................................................................................1

1. INTRODUCTION.......................................................................................................................4

1.1 Define SFA and importance of financial analysis............................................................4

1.2 Assignment objectives......................................................................................................4

1.3 Background of selected companies..................................................................................4

1.4 Techniques used throughout the report............................................................................5

2. RATIO ANALYSIS.....................................................................................................................5

2.1 Profitability.......................................................................................................................5

2.2 Liquidity...........................................................................................................................6

2.3 Efficiency.........................................................................................................................8

2.4 Leverage...........................................................................................................................9

2.5 Investors.........................................................................................................................10

3.0 Common size analysis..............................................................................................................11

3.1 Vertical analysis.............................................................................................................11

3.2 Horizontal analysis.........................................................................................................11

3.3 Du Pont analysis.............................................................................................................11

3.4 Segment analysis............................................................................................................11

4.0 MERITS AND DEMERITS....................................................................................................12

4.1 Ratio analysis..................................................................................................................12

4.2 Common size..................................................................................................................12

4.3 Du Pont...........................................................................................................................13

4.4 Segment analysis............................................................................................................13

5.0 CONCLUSIONS AND RECOMMENDATIONS..................................................................13

5.1 Conclusions....................................................................................................................13

5.2 Recommendations..........................................................................................................14

6.0 CONTEMPORARY METHODS ANALYSIS.......................................................................14

6.1 CAPM.............................................................................................................................14

6.2 EMH...............................................................................................................................14

6.3 EVA................................................................................................................................15

REFERENCES..............................................................................................................................16

APPENDICES.................................................................................................................................1

1. INTRODUCTION

1.1 Define SFA and importance of financial analysis

Strategic financial analysis is that approach commonly used by an entity which consists

of setting end goals and then analysing all the ways of completing the goals. It is that analysis in

which different tools and techniques are used as personnel of this entity will use specific tactics

to reach their specific goals (Braveman, 2016). There are some importance of this analysis which

will assists an enterprise in uplifting their existing situations. It is helpful for an entity in

preparing budgets which is basic form of financial analysis in SFA. The future upcoming cash

flows are forecasted by ascertaining the present the facts and figures. This analysis is also

responsible for conducting price analysis in which external market forces are identified in order

to determine price of an enterprise. In the price analysis the main aim of the owner is to generate

high sales volume at higher prices by determining the external elasticity of demand in the overall

market. The primary objective of this assignment is to clarify the role of strategic financial

analysis by determining their importance in the current business.

1.2 Assignment objectives

Two companies has been selected for this project report such as Booker and Tate&Lyle

among which financial comparison has been done by applying various techniques of strategic

financial analysis. Financial ratios has been calculated by commenting upon the business

efficiency of 5 years in order to take further step in the business in order to select or reject the

current project or expanding with another business.

1.3 Background of selected companies

Booker is one of the company selected for assessing its internal business functioning for

the given project (Agarwal and Green, 2016). It is one of the famous food and beverage entity

operated their business in the United Kingdom which provides their products or services as a

wholesaler. It deals in variety of products such as macro, booker direct, classic drinks, Ritter

courivaud, chef direct, premier, family shopper in order to cater the needs of customers. It is the

biggest strengths is that current it is serving about 1.5 million customers. It is regarded as the

largest cash and carry operator in the UK which are privileged to served around 18000 product

lines ranging from different price and brand ranges according to the budget of an individual. It

1.1 Define SFA and importance of financial analysis

Strategic financial analysis is that approach commonly used by an entity which consists

of setting end goals and then analysing all the ways of completing the goals. It is that analysis in

which different tools and techniques are used as personnel of this entity will use specific tactics

to reach their specific goals (Braveman, 2016). There are some importance of this analysis which

will assists an enterprise in uplifting their existing situations. It is helpful for an entity in

preparing budgets which is basic form of financial analysis in SFA. The future upcoming cash

flows are forecasted by ascertaining the present the facts and figures. This analysis is also

responsible for conducting price analysis in which external market forces are identified in order

to determine price of an enterprise. In the price analysis the main aim of the owner is to generate

high sales volume at higher prices by determining the external elasticity of demand in the overall

market. The primary objective of this assignment is to clarify the role of strategic financial

analysis by determining their importance in the current business.

1.2 Assignment objectives

Two companies has been selected for this project report such as Booker and Tate&Lyle

among which financial comparison has been done by applying various techniques of strategic

financial analysis. Financial ratios has been calculated by commenting upon the business

efficiency of 5 years in order to take further step in the business in order to select or reject the

current project or expanding with another business.

1.3 Background of selected companies

Booker is one of the company selected for assessing its internal business functioning for

the given project (Agarwal and Green, 2016). It is one of the famous food and beverage entity

operated their business in the United Kingdom which provides their products or services as a

wholesaler. It deals in variety of products such as macro, booker direct, classic drinks, Ritter

courivaud, chef direct, premier, family shopper in order to cater the needs of customers. It is the

biggest strengths is that current it is serving about 1.5 million customers. It is regarded as the

largest cash and carry operator in the UK which are privileged to served around 18000 product

lines ranging from different price and brand ranges according to the budget of an individual. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

also works as retailer business but major sales and the revenue comes from the wholesaling

business.

Tate&Lyle is multinational business entity which is based in the British agribusiness

which deals in the food and beverage sectors. This enterprise has also listed in the London stock

exchange with a constituent of FTSE 250 indexes. This enterprise specialises in the innovative

technology which is applied in providing all kinds of products (Hasan and Kobeissi, 2016). The

technology has used to transform different raw materials into finished products without affecting

their nutrients. These materials whose nutritional level will enhance by using these methods such

as corn, tapioca and oats. The main emphasises of this entity is on using all kinds of organic

materials by avoiding chemicals and artificial in the food as health is the key to keep fit and

health is the basic motto of this firm It operated with round 25 manufacture facilities and good

network of research and development centres all across the world. The income and financial

conditions has raised due to several good decisions taken by this enterprise such as

diversification approach in which entering into another markets will be beneficial for an entity.

1.4 Techniques used throughout the report

This assignment gives greater importance to all the techniques used by an entity by using

different methods of analysis in assessing the business efficiency of both the selected entities.

The profitability of this entity will be ascertained by applying profitability ratios. The liquidity

has been ascertained by calculating current ratios which will determine available cash balance

held with an enterprise (Braveman, 2016). The business efficiency are determined by calculating

asset turnover and inventory turnover. Leverage can be found out which reflects financial health

of both the enterprise. These ratios will be helpful for all the investors in order accept or reject

the decision of investing in the business. Du-pont analysis which will break ROCE in three

different parts. Cash flow analysis has been used to know the movement of cash flow and cash

outflow from the business. Common size balance sheet are prepared which is a comparative

analysis of a previous year.

2. RATIO ANALYSIS

2.1 Profitability

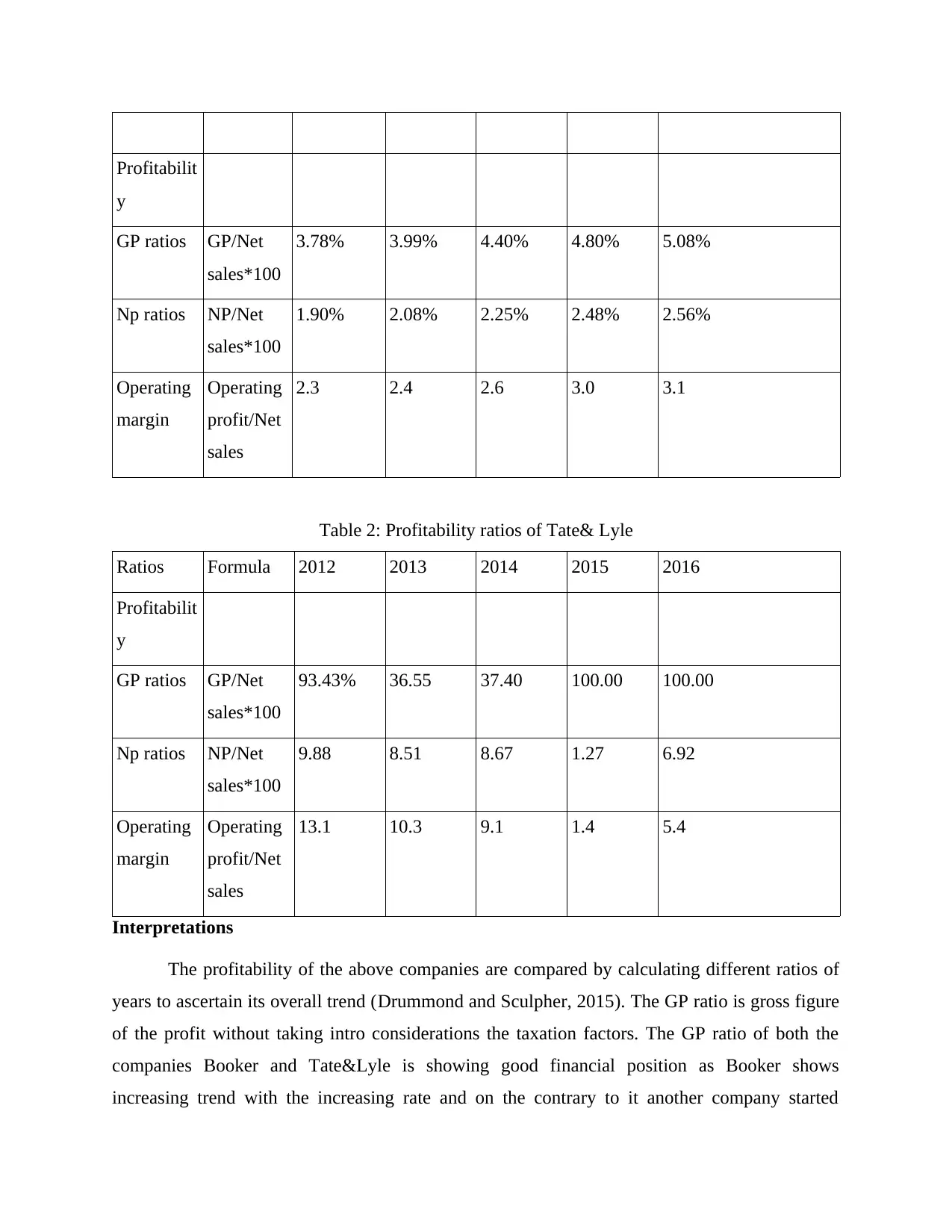

Table 1: Profitability ratios of Booker

Ratios Formula 2012 2013 2014 2015 2016

business.

Tate&Lyle is multinational business entity which is based in the British agribusiness

which deals in the food and beverage sectors. This enterprise has also listed in the London stock

exchange with a constituent of FTSE 250 indexes. This enterprise specialises in the innovative

technology which is applied in providing all kinds of products (Hasan and Kobeissi, 2016). The

technology has used to transform different raw materials into finished products without affecting

their nutrients. These materials whose nutritional level will enhance by using these methods such

as corn, tapioca and oats. The main emphasises of this entity is on using all kinds of organic

materials by avoiding chemicals and artificial in the food as health is the key to keep fit and

health is the basic motto of this firm It operated with round 25 manufacture facilities and good

network of research and development centres all across the world. The income and financial

conditions has raised due to several good decisions taken by this enterprise such as

diversification approach in which entering into another markets will be beneficial for an entity.

1.4 Techniques used throughout the report

This assignment gives greater importance to all the techniques used by an entity by using

different methods of analysis in assessing the business efficiency of both the selected entities.

The profitability of this entity will be ascertained by applying profitability ratios. The liquidity

has been ascertained by calculating current ratios which will determine available cash balance

held with an enterprise (Braveman, 2016). The business efficiency are determined by calculating

asset turnover and inventory turnover. Leverage can be found out which reflects financial health

of both the enterprise. These ratios will be helpful for all the investors in order accept or reject

the decision of investing in the business. Du-pont analysis which will break ROCE in three

different parts. Cash flow analysis has been used to know the movement of cash flow and cash

outflow from the business. Common size balance sheet are prepared which is a comparative

analysis of a previous year.

2. RATIO ANALYSIS

2.1 Profitability

Table 1: Profitability ratios of Booker

Ratios Formula 2012 2013 2014 2015 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profitabilit

y

GP ratios GP/Net

sales*100

3.78% 3.99% 4.40% 4.80% 5.08%

Np ratios NP/Net

sales*100

1.90% 2.08% 2.25% 2.48% 2.56%

Operating

margin

Operating

profit/Net

sales

2.3 2.4 2.6 3.0 3.1

Table 2: Profitability ratios of Tate& Lyle

Ratios Formula 2012 2013 2014 2015 2016

Profitabilit

y

GP ratios GP/Net

sales*100

93.43% 36.55 37.40 100.00 100.00

Np ratios NP/Net

sales*100

9.88 8.51 8.67 1.27 6.92

Operating

margin

Operating

profit/Net

sales

13.1 10.3 9.1 1.4 5.4

Interpretations

The profitability of the above companies are compared by calculating different ratios of

years to ascertain its overall trend (Drummond and Sculpher, 2015). The GP ratio is gross figure

of the profit without taking intro considerations the taxation factors. The GP ratio of both the

companies Booker and Tate&Lyle is showing good financial position as Booker shows

increasing trend with the increasing rate and on the contrary to it another company started

y

GP ratios GP/Net

sales*100

3.78% 3.99% 4.40% 4.80% 5.08%

Np ratios NP/Net

sales*100

1.90% 2.08% 2.25% 2.48% 2.56%

Operating

margin

Operating

profit/Net

sales

2.3 2.4 2.6 3.0 3.1

Table 2: Profitability ratios of Tate& Lyle

Ratios Formula 2012 2013 2014 2015 2016

Profitabilit

y

GP ratios GP/Net

sales*100

93.43% 36.55 37.40 100.00 100.00

Np ratios NP/Net

sales*100

9.88 8.51 8.67 1.27 6.92

Operating

margin

Operating

profit/Net

sales

13.1 10.3 9.1 1.4 5.4

Interpretations

The profitability of the above companies are compared by calculating different ratios of

years to ascertain its overall trend (Drummond and Sculpher, 2015). The GP ratio is gross figure

of the profit without taking intro considerations the taxation factors. The GP ratio of both the

companies Booker and Tate&Lyle is showing good financial position as Booker shows

increasing trend with the increasing rate and on the contrary to it another company started

initially with higher and in end two years shows 100% efficiency and in middle shows lack of

progress. Again the NP ratios are increasing again and Tate&Lyle shows fewer efforts. The slow

steady approach again proves to be beneficial as their operating profit are shown good profit

trends as compared to the other companies.

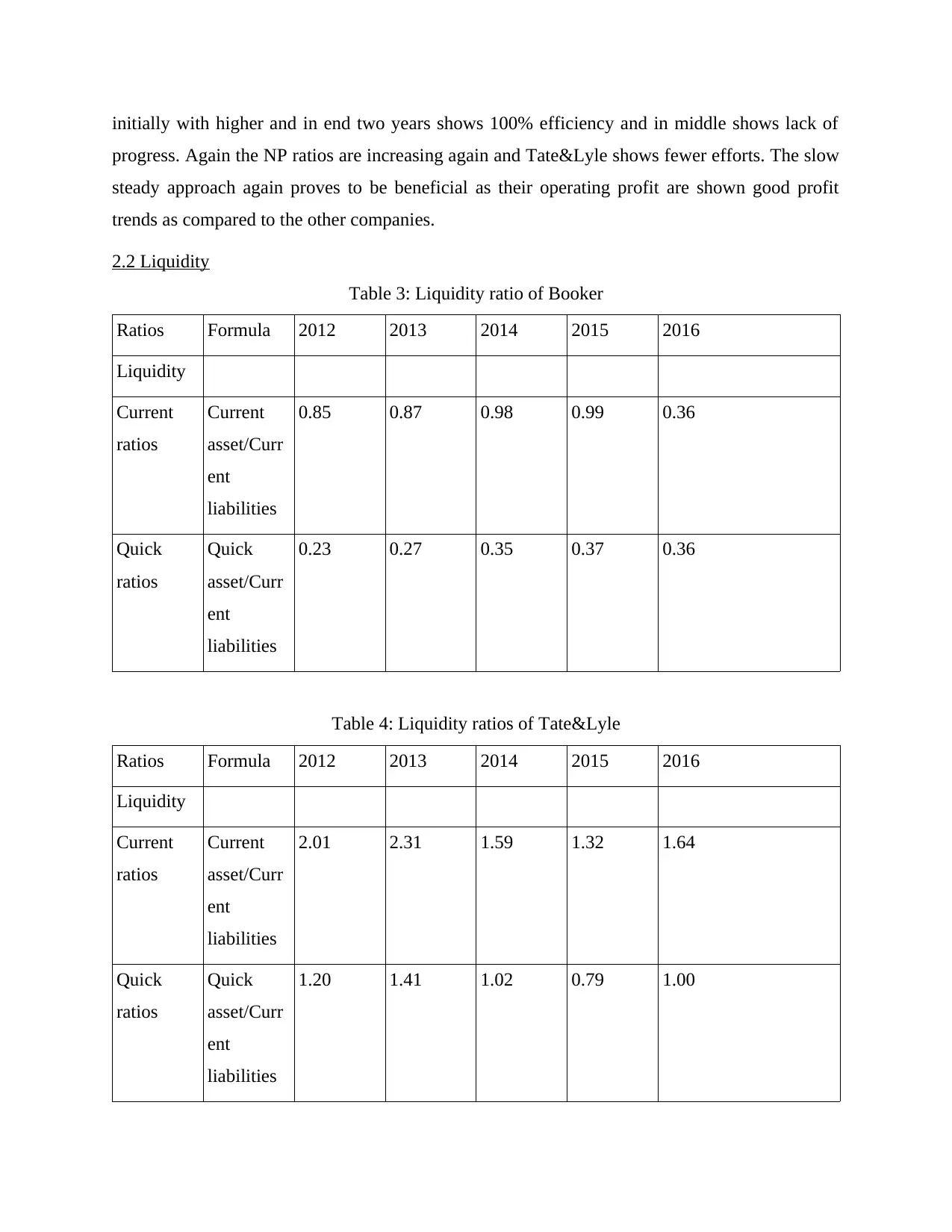

2.2 Liquidity

Table 3: Liquidity ratio of Booker

Ratios Formula 2012 2013 2014 2015 2016

Liquidity

Current

ratios

Current

asset/Curr

ent

liabilities

0.85 0.87 0.98 0.99 0.36

Quick

ratios

Quick

asset/Curr

ent

liabilities

0.23 0.27 0.35 0.37 0.36

Table 4: Liquidity ratios of Tate&Lyle

Ratios Formula 2012 2013 2014 2015 2016

Liquidity

Current

ratios

Current

asset/Curr

ent

liabilities

2.01 2.31 1.59 1.32 1.64

Quick

ratios

Quick

asset/Curr

ent

liabilities

1.20 1.41 1.02 0.79 1.00

progress. Again the NP ratios are increasing again and Tate&Lyle shows fewer efforts. The slow

steady approach again proves to be beneficial as their operating profit are shown good profit

trends as compared to the other companies.

2.2 Liquidity

Table 3: Liquidity ratio of Booker

Ratios Formula 2012 2013 2014 2015 2016

Liquidity

Current

ratios

Current

asset/Curr

ent

liabilities

0.85 0.87 0.98 0.99 0.36

Quick

ratios

Quick

asset/Curr

ent

liabilities

0.23 0.27 0.35 0.37 0.36

Table 4: Liquidity ratios of Tate&Lyle

Ratios Formula 2012 2013 2014 2015 2016

Liquidity

Current

ratios

Current

asset/Curr

ent

liabilities

2.01 2.31 1.59 1.32 1.64

Quick

ratios

Quick

asset/Curr

ent

liabilities

1.20 1.41 1.02 0.79 1.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretations

Liquidity ratios of the business enterprise will show available cash balance held with an

enterprise in order to meet their short term obligations (Agarwal and Green, 2016). When the

current ratios are constant trend has been identified then in that situation Booker has generated

good ratios but less than one. On the other hand, another entity has higher ratio greater than one

but not in a systematic way. Other ratio is quick assets which ascertained the business efficiency

by excluding the inventory from the current assets. Booker shows upward with increasing rate

and Tate&Lyle generates lower ratios towards the downward position.

2.3 Efficiency

Table 5: Efficiency ratios of Booker

Ratios Formula 2012 2013 2014 2015 2016

Efficiency

Asset

turnover

Total

assets/Net

sales4.37

4.37 3.90 3.96 3.76 3.75

Inventory

turnover

COGS/

Average

inventory

15.48 14.31 15.05 13.80 13.89

Receivabl

es

turnover

Receivabl

es/Net

credit

sales

82.23 73.79 79.08 70.57 50.93

Table 6: Efficiency ratios of Tate&Lyle

Ratios Formula 2012 2013 2014 2015 2016

Efficiency

Asset

turnover

Total

assets/Net

1.04 1.14 1.18 0.95 0.95

Liquidity ratios of the business enterprise will show available cash balance held with an

enterprise in order to meet their short term obligations (Agarwal and Green, 2016). When the

current ratios are constant trend has been identified then in that situation Booker has generated

good ratios but less than one. On the other hand, another entity has higher ratio greater than one

but not in a systematic way. Other ratio is quick assets which ascertained the business efficiency

by excluding the inventory from the current assets. Booker shows upward with increasing rate

and Tate&Lyle generates lower ratios towards the downward position.

2.3 Efficiency

Table 5: Efficiency ratios of Booker

Ratios Formula 2012 2013 2014 2015 2016

Efficiency

Asset

turnover

Total

assets/Net

sales4.37

4.37 3.90 3.96 3.76 3.75

Inventory

turnover

COGS/

Average

inventory

15.48 14.31 15.05 13.80 13.89

Receivabl

es

turnover

Receivabl

es/Net

credit

sales

82.23 73.79 79.08 70.57 50.93

Table 6: Efficiency ratios of Tate&Lyle

Ratios Formula 2012 2013 2014 2015 2016

Efficiency

Asset

turnover

Total

assets/Net

1.04 1.14 1.18 0.95 0.95

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales

Inventory

turnover

COGS/

Average

inventory

4.77 0.45 4.23 3.38 -

Receivabl

es

turnover

Receivabl

es/Net

credit

sales

12.16 10.96 10.53 9.13 9.69

Interpretations

The ratio of asset turnover in both the companies are decreasing but the less impact of the

declining performance on the overall market is less in Tate&Lyle as compared to the Booker.

The decrease in the asset turnover ratio can be decreases due to the less amount of the sales and

the re revenue generated by an enterprise (Bellostas and López-Arceiz, 2016). The inventory

turnover ratio will reveal the proportion of cost of goods as compared to the average inventory

stored in an enterprise. It is decreasing in both the companies due to the higher expenses

involved in the entity. Receivables turnover ratios are calculated to determine the firm's ability in

order to receive the money from all its debtors. The deficiency of both the entities are reflected

with the help of this ratio as it is showing decreasing ratios.

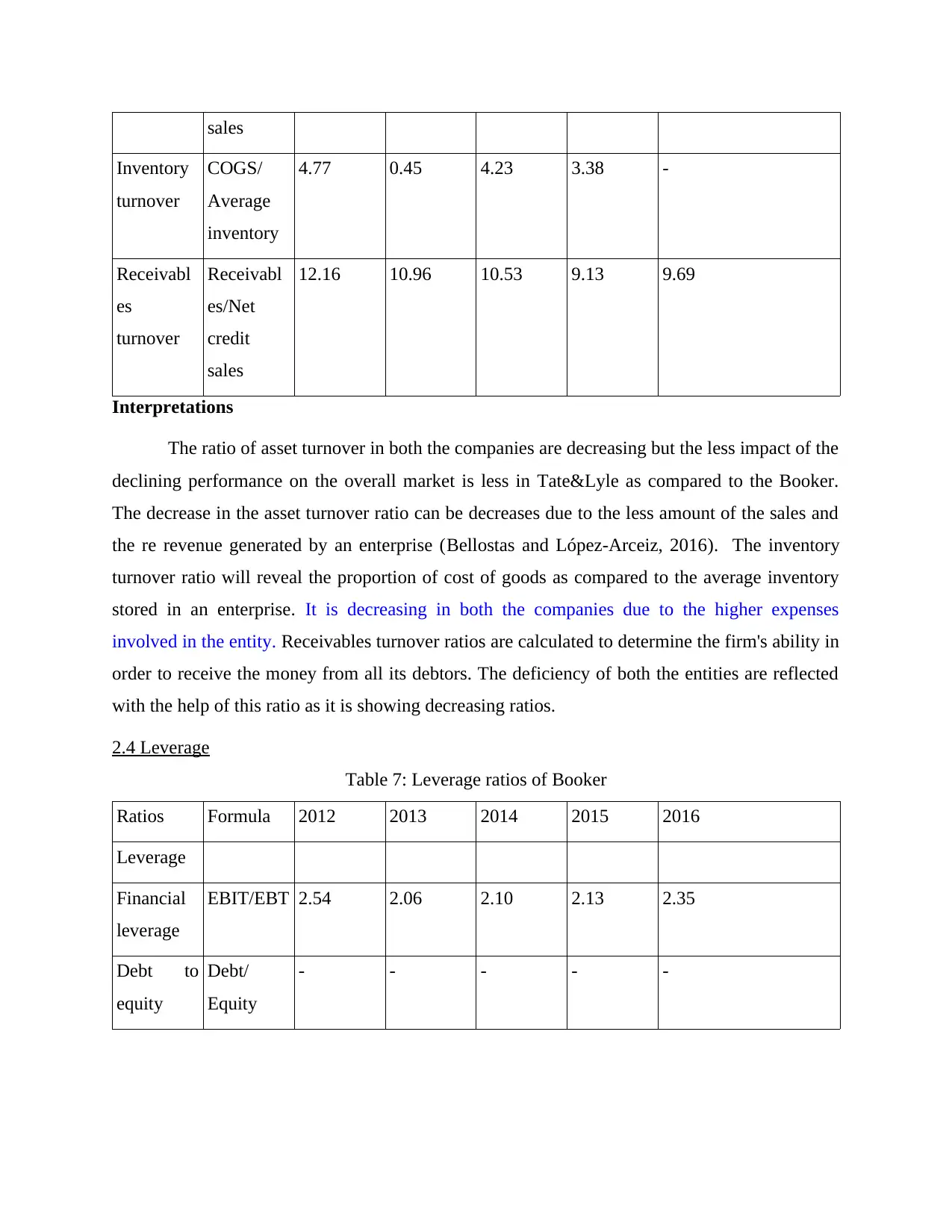

2.4 Leverage

Table 7: Leverage ratios of Booker

Ratios Formula 2012 2013 2014 2015 2016

Leverage

Financial

leverage

EBIT/EBT 2.54 2.06 2.10 2.13 2.35

Debt to

equity

Debt/

Equity

- - - - -

Inventory

turnover

COGS/

Average

inventory

4.77 0.45 4.23 3.38 -

Receivabl

es

turnover

Receivabl

es/Net

credit

sales

12.16 10.96 10.53 9.13 9.69

Interpretations

The ratio of asset turnover in both the companies are decreasing but the less impact of the

declining performance on the overall market is less in Tate&Lyle as compared to the Booker.

The decrease in the asset turnover ratio can be decreases due to the less amount of the sales and

the re revenue generated by an enterprise (Bellostas and López-Arceiz, 2016). The inventory

turnover ratio will reveal the proportion of cost of goods as compared to the average inventory

stored in an enterprise. It is decreasing in both the companies due to the higher expenses

involved in the entity. Receivables turnover ratios are calculated to determine the firm's ability in

order to receive the money from all its debtors. The deficiency of both the entities are reflected

with the help of this ratio as it is showing decreasing ratios.

2.4 Leverage

Table 7: Leverage ratios of Booker

Ratios Formula 2012 2013 2014 2015 2016

Leverage

Financial

leverage

EBIT/EBT 2.54 2.06 2.10 2.13 2.35

Debt to

equity

Debt/

Equity

- - - - -

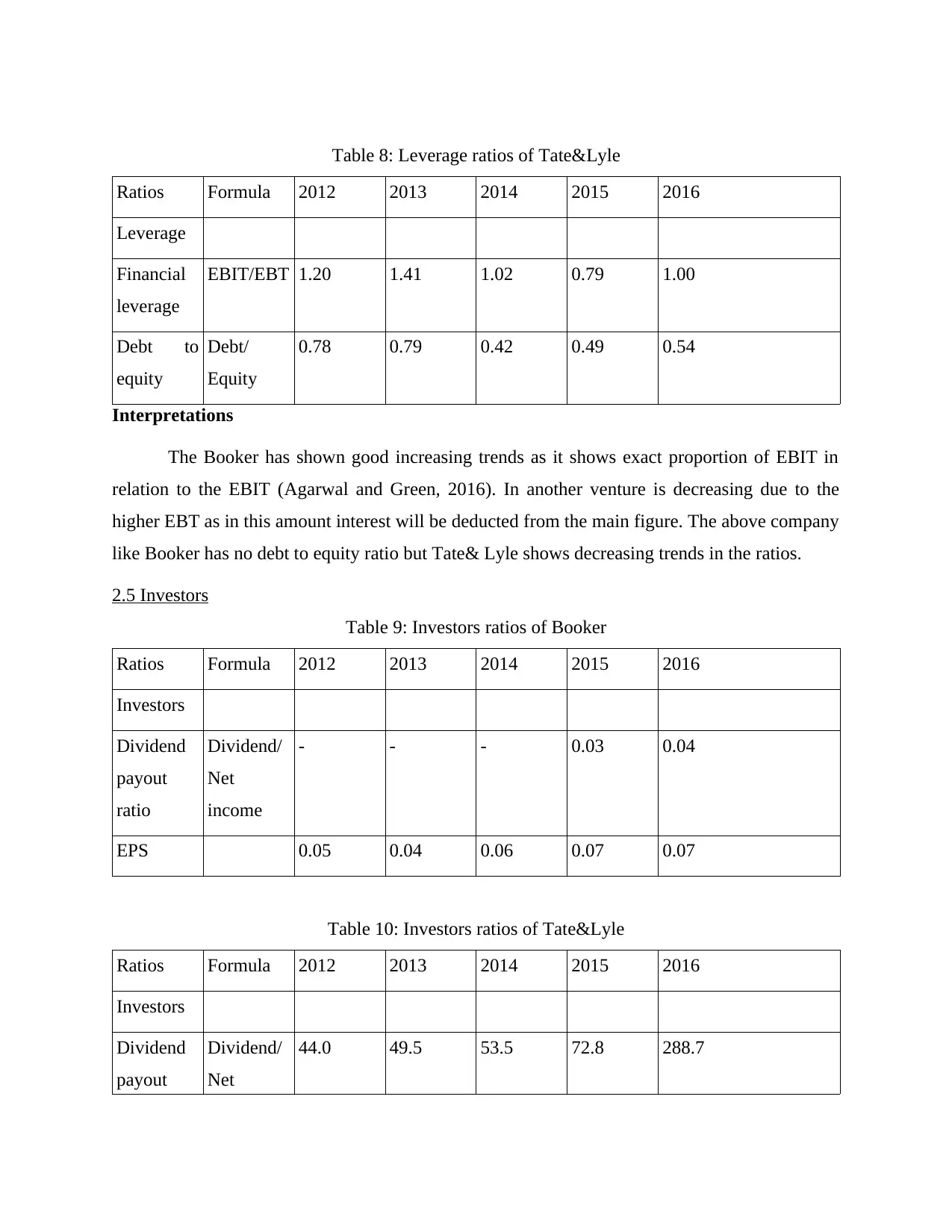

Table 8: Leverage ratios of Tate&Lyle

Ratios Formula 2012 2013 2014 2015 2016

Leverage

Financial

leverage

EBIT/EBT 1.20 1.41 1.02 0.79 1.00

Debt to

equity

Debt/

Equity

0.78 0.79 0.42 0.49 0.54

Interpretations

The Booker has shown good increasing trends as it shows exact proportion of EBIT in

relation to the EBIT (Agarwal and Green, 2016). In another venture is decreasing due to the

higher EBT as in this amount interest will be deducted from the main figure. The above company

like Booker has no debt to equity ratio but Tate& Lyle shows decreasing trends in the ratios.

2.5 Investors

Table 9: Investors ratios of Booker

Ratios Formula 2012 2013 2014 2015 2016

Investors

Dividend

payout

ratio

Dividend/

Net

income

- - - 0.03 0.04

EPS 0.05 0.04 0.06 0.07 0.07

Table 10: Investors ratios of Tate&Lyle

Ratios Formula 2012 2013 2014 2015 2016

Investors

Dividend

payout

Dividend/

Net

44.0 49.5 53.5 72.8 288.7

Ratios Formula 2012 2013 2014 2015 2016

Leverage

Financial

leverage

EBIT/EBT 1.20 1.41 1.02 0.79 1.00

Debt to

equity

Debt/

Equity

0.78 0.79 0.42 0.49 0.54

Interpretations

The Booker has shown good increasing trends as it shows exact proportion of EBIT in

relation to the EBIT (Agarwal and Green, 2016). In another venture is decreasing due to the

higher EBT as in this amount interest will be deducted from the main figure. The above company

like Booker has no debt to equity ratio but Tate& Lyle shows decreasing trends in the ratios.

2.5 Investors

Table 9: Investors ratios of Booker

Ratios Formula 2012 2013 2014 2015 2016

Investors

Dividend

payout

ratio

Dividend/

Net

income

- - - 0.03 0.04

EPS 0.05 0.04 0.06 0.07 0.07

Table 10: Investors ratios of Tate&Lyle

Ratios Formula 2012 2013 2014 2015 2016

Investors

Dividend

payout

Dividend/

Net

44.0 49.5 53.5 72.8 288.7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

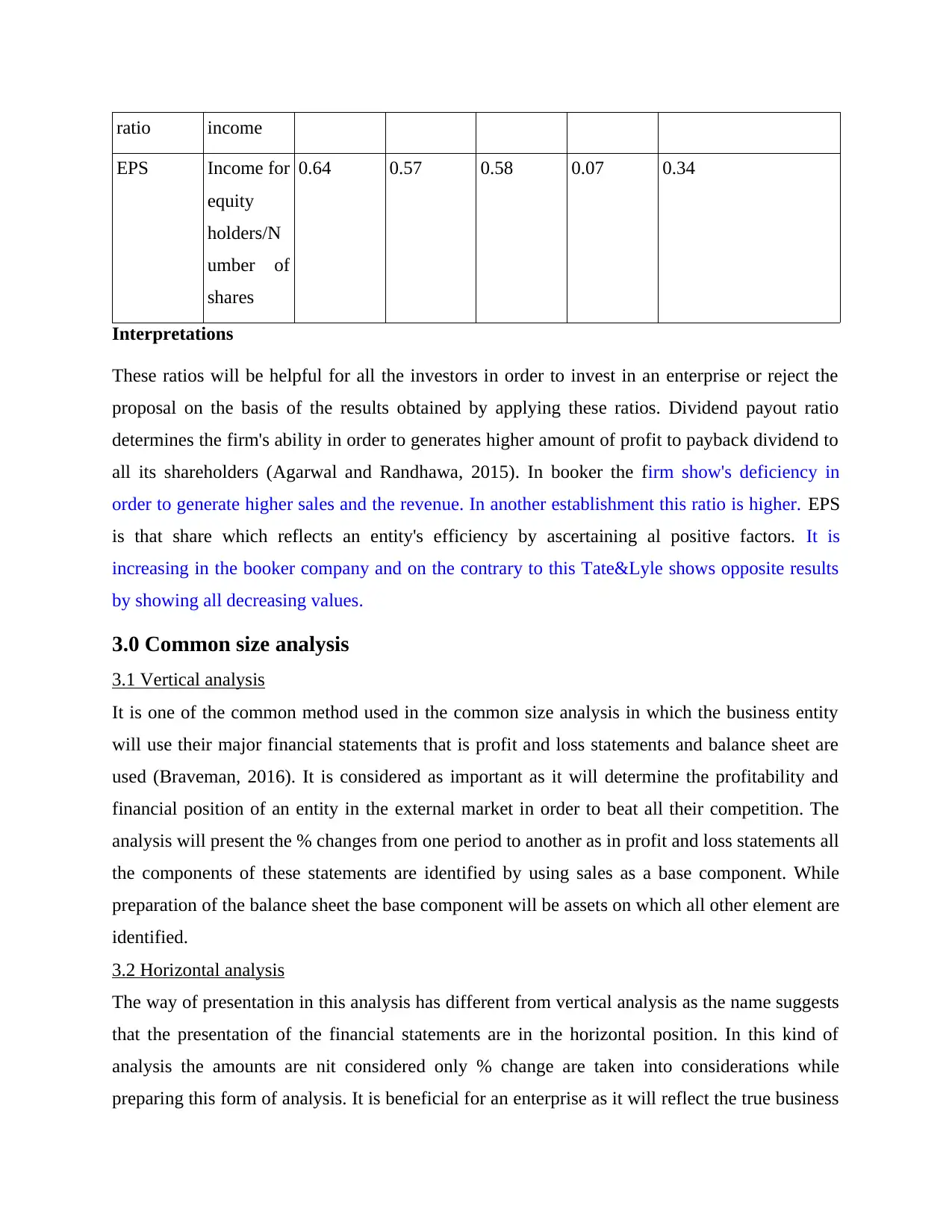

ratio income

EPS Income for

equity

holders/N

umber of

shares

0.64 0.57 0.58 0.07 0.34

Interpretations

These ratios will be helpful for all the investors in order to invest in an enterprise or reject the

proposal on the basis of the results obtained by applying these ratios. Dividend payout ratio

determines the firm's ability in order to generates higher amount of profit to payback dividend to

all its shareholders (Agarwal and Randhawa, 2015). In booker the firm show's deficiency in

order to generate higher sales and the revenue. In another establishment this ratio is higher. EPS

is that share which reflects an entity's efficiency by ascertaining al positive factors. It is

increasing in the booker company and on the contrary to this Tate&Lyle shows opposite results

by showing all decreasing values.

3.0 Common size analysis

3.1 Vertical analysis

It is one of the common method used in the common size analysis in which the business entity

will use their major financial statements that is profit and loss statements and balance sheet are

used (Braveman, 2016). It is considered as important as it will determine the profitability and

financial position of an entity in the external market in order to beat all their competition. The

analysis will present the % changes from one period to another as in profit and loss statements all

the components of these statements are identified by using sales as a base component. While

preparation of the balance sheet the base component will be assets on which all other element are

identified.

3.2 Horizontal analysis

The way of presentation in this analysis has different from vertical analysis as the name suggests

that the presentation of the financial statements are in the horizontal position. In this kind of

analysis the amounts are nit considered only % change are taken into considerations while

preparing this form of analysis. It is beneficial for an enterprise as it will reflect the true business

EPS Income for

equity

holders/N

umber of

shares

0.64 0.57 0.58 0.07 0.34

Interpretations

These ratios will be helpful for all the investors in order to invest in an enterprise or reject the

proposal on the basis of the results obtained by applying these ratios. Dividend payout ratio

determines the firm's ability in order to generates higher amount of profit to payback dividend to

all its shareholders (Agarwal and Randhawa, 2015). In booker the firm show's deficiency in

order to generate higher sales and the revenue. In another establishment this ratio is higher. EPS

is that share which reflects an entity's efficiency by ascertaining al positive factors. It is

increasing in the booker company and on the contrary to this Tate&Lyle shows opposite results

by showing all decreasing values.

3.0 Common size analysis

3.1 Vertical analysis

It is one of the common method used in the common size analysis in which the business entity

will use their major financial statements that is profit and loss statements and balance sheet are

used (Braveman, 2016). It is considered as important as it will determine the profitability and

financial position of an entity in the external market in order to beat all their competition. The

analysis will present the % changes from one period to another as in profit and loss statements all

the components of these statements are identified by using sales as a base component. While

preparation of the balance sheet the base component will be assets on which all other element are

identified.

3.2 Horizontal analysis

The way of presentation in this analysis has different from vertical analysis as the name suggests

that the presentation of the financial statements are in the horizontal position. In this kind of

analysis the amounts are nit considered only % change are taken into considerations while

preparing this form of analysis. It is beneficial for an enterprise as it will reflect the true business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance of an entity in which internal performance are compared in order to make corrective

actions in order to remove their internal weaknesses.

3.3 Du Pont analysis

Return on Equity= Total assets/Shareholder's equity*Return on assets

Return on equity= Total assets/Shareholder's equity*Net income/Total assets

Return on equity= Total assets/shareholder's equity*Revenues/total assets*Net income/Revenues

Return on Equity= Total assets/shareholder's equity*Revenues/total assets* Operating

income/Revenues* EBIT/operating income*(1-tax/EBIT)

3.4 Segment analysis

The segments are integral part of an enterprise whose main motive is to complete the overall

work on time by allotting all work into different departments (Drummond and Sculpher 2015).

The segmentation in the above food and beverage industries includes groceries, shelf space

allocation, monitoring of all the items, drinks, raw groceries, food processing, finished product's

cell. These standard segmentation will be same in the both organisation as both falls in the same

industry. The variations in the segments may due to the changes in the needs and expectations of

an enterprise.

4.0 MERITS AND DEMERITS

4.1 Ratio analysis

It refers to comparative analysis of the business performance of two organisations among which

this comparison has been established by categorising all the variables of the business into

different categories.

Advantages

It helps in forecasting and plaining as it will reveal the costs involved in the business of

Booker and tate& lyle which helps them in order to determine their sales level.

Comparison of the current figures of both the company in relation to their previous years

The operational efficiency has been measured by calculating different kinds of ratios

Disadvantages

Ratios will be provide wrong results due to errors in the financial statements

The ratios based on the financial information will only provides historical information

and no real information.

actions in order to remove their internal weaknesses.

3.3 Du Pont analysis

Return on Equity= Total assets/Shareholder's equity*Return on assets

Return on equity= Total assets/Shareholder's equity*Net income/Total assets

Return on equity= Total assets/shareholder's equity*Revenues/total assets*Net income/Revenues

Return on Equity= Total assets/shareholder's equity*Revenues/total assets* Operating

income/Revenues* EBIT/operating income*(1-tax/EBIT)

3.4 Segment analysis

The segments are integral part of an enterprise whose main motive is to complete the overall

work on time by allotting all work into different departments (Drummond and Sculpher 2015).

The segmentation in the above food and beverage industries includes groceries, shelf space

allocation, monitoring of all the items, drinks, raw groceries, food processing, finished product's

cell. These standard segmentation will be same in the both organisation as both falls in the same

industry. The variations in the segments may due to the changes in the needs and expectations of

an enterprise.

4.0 MERITS AND DEMERITS

4.1 Ratio analysis

It refers to comparative analysis of the business performance of two organisations among which

this comparison has been established by categorising all the variables of the business into

different categories.

Advantages

It helps in forecasting and plaining as it will reveal the costs involved in the business of

Booker and tate& lyle which helps them in order to determine their sales level.

Comparison of the current figures of both the company in relation to their previous years

The operational efficiency has been measured by calculating different kinds of ratios

Disadvantages

Ratios will be provide wrong results due to errors in the financial statements

The ratios based on the financial information will only provides historical information

and no real information.

4.2 Common size

Advantages

The simplified structure of common size statements is easy to understanding in order to

interpret the results of booker and tate& lyle.

The booker and tate&lyle can predict their future cash flows by using time series analysis

over one period to another period.

The different components which is to be covered in the different financial statements are

compared easily.

Disadvantages

The information may get misleading to the users of the business as external changes like

inflationary rate will change the prices level.

These statements failed to reveal true positions of sales and all other components covered

in the business due to widow dressing of financial statements.

4.3 Du Pont

Advantages

It will assist all the investors in order to make business decisions equally by taking into

considerations all the external factors

This will reveal the complete picture regarding financial health of an enterprise and their

business performance.

It uses financial and leverage resources in order to remove the minute deficiency remains

in the factors.

Disadvantages

It heavily relies on the accounting data from the company's financial statements which is

not good as slight changes in the data may lead to complete transformation.

This analysis is based on other ratios so in case of lack fop information it is not proved to

be beneficial for an enterprise.

4.4 Segment analysis

Advantages

Advantages

The simplified structure of common size statements is easy to understanding in order to

interpret the results of booker and tate& lyle.

The booker and tate&lyle can predict their future cash flows by using time series analysis

over one period to another period.

The different components which is to be covered in the different financial statements are

compared easily.

Disadvantages

The information may get misleading to the users of the business as external changes like

inflationary rate will change the prices level.

These statements failed to reveal true positions of sales and all other components covered

in the business due to widow dressing of financial statements.

4.3 Du Pont

Advantages

It will assist all the investors in order to make business decisions equally by taking into

considerations all the external factors

This will reveal the complete picture regarding financial health of an enterprise and their

business performance.

It uses financial and leverage resources in order to remove the minute deficiency remains

in the factors.

Disadvantages

It heavily relies on the accounting data from the company's financial statements which is

not good as slight changes in the data may lead to complete transformation.

This analysis is based on other ratios so in case of lack fop information it is not proved to

be beneficial for an enterprise.

4.4 Segment analysis

Advantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.