Strategic Financial Analysis Report: Booker and Tate & Lyle

VerifiedAdded on 2022/10/18

|35

|8266

|26

Report

AI Summary

This report provides a comprehensive strategic financial analysis of Booker and Tate & Lyle, focusing on the principal methods of analyzing company accounts from an external perspective. It begins with an introduction to financial analysis, explaining how financial statements like the Balance Sheet, Income Statement, and Cash flow statements are used to assess a company's financial position, profitability, efficiency, liquidity, and leverage. The report then delves into ratio calculation, covering profitability ratios (Gross Profit Margin, Net Profit Margin, Return on Capital Employed), liquidity ratios (Current Ratio, Quick Ratio), efficiency ratios (Days of Sales Outstanding, Days of Inventory on Hand, Days of Payables, Cash Conversion Cycle), leverage ratios (Debt-to-Equity Ratio, Gearing), cash flow ratios (Operating Cash Flow to Sales, Operating Cash Flow to Net Income, Cash Flow to Total Debt), and investor ratios (Earnings per Share, Dividend Pay-out, Price-Earnings Ratio). Furthermore, it includes common size analysis (vertical and horizontal analysis), DuPont analysis, and segmental analysis. The report evaluates the financial performance of Booker and Tate & Lyle using these techniques, highlighting trends and providing insights into their financial health, while also critically assessing the shortcomings of these methods and proposing contemporary analysis methods to limit those shortcomings.

Running Head: Strategic Financial Analysis

Strategic Financial Analysis

Strategic Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Financial Analysis

Contents

2.0 Ratio Calculation.......................................................................................................................1

2.0 Introduction to Financial Analysis...............................................................................................1

2.1 Profitability..................................................................................................................................1

2.1.1 Gross Profit Margin (GPM)..................................................................................................4

2.1.2 Net Profit Margin..................................................................................................................5

2.1.3 Return on Capital Employed (ROCE)...................................................................................6

2.2 Liquidity......................................................................................................................................7

2.2.1 Current Ratio........................................................................................................................7

2.2.2 Quick Ratio...........................................................................................................................8

2.3 Efficiency....................................................................................................................................8

2.3.1 Days of Sales Outstanding (DSO).........................................................................................9

2.3.2 Days of Inventory on Hand (DOI)........................................................................................9

2.3.3 Days of Payables (DOP).....................................................................................................10

2.3.4 Cash Conversion Cycle (CCC)...........................................................................................10

2.4 Leverage....................................................................................................................................11

2.4.1 Debt-to-Equity Ratio...........................................................................................................11

2.4.2 Gearing...............................................................................................................................12

2.5 Cash Flow Ratios.......................................................................................................................12

2.5.1 Operating Cash Flow to Sales.............................................................................................13

2.5.2 Operating Cash Flow to Net Income...................................................................................13

2.5.3 Cash Flow to Total Debt.....................................................................................................14

2.6 Investor’s Ratio.........................................................................................................................14

2.6.1 Earnings per Share (EPS)....................................................................................................15

2.6.2 Dividend Pay-out................................................................................................................15

2.6.3 Price- Earnings Ratio (P/E Ratio).......................................................................................16

2.7 Common Size............................................................................................................................16

2.7.1 Vertical Analysis................................................................................................................17

2.7.2 Horizontal Analysis............................................................................................................21

2.8 DuPont Analysis........................................................................................................................25

2.8.1 DuPont - 3 factor ROE........................................................................................................25

2.8.1 DuPont - 2 factor ROA.......................................................................................................26

2.9 Segmental Analysis...................................................................................................................27

1

Contents

2.0 Ratio Calculation.......................................................................................................................1

2.0 Introduction to Financial Analysis...............................................................................................1

2.1 Profitability..................................................................................................................................1

2.1.1 Gross Profit Margin (GPM)..................................................................................................4

2.1.2 Net Profit Margin..................................................................................................................5

2.1.3 Return on Capital Employed (ROCE)...................................................................................6

2.2 Liquidity......................................................................................................................................7

2.2.1 Current Ratio........................................................................................................................7

2.2.2 Quick Ratio...........................................................................................................................8

2.3 Efficiency....................................................................................................................................8

2.3.1 Days of Sales Outstanding (DSO).........................................................................................9

2.3.2 Days of Inventory on Hand (DOI)........................................................................................9

2.3.3 Days of Payables (DOP).....................................................................................................10

2.3.4 Cash Conversion Cycle (CCC)...........................................................................................10

2.4 Leverage....................................................................................................................................11

2.4.1 Debt-to-Equity Ratio...........................................................................................................11

2.4.2 Gearing...............................................................................................................................12

2.5 Cash Flow Ratios.......................................................................................................................12

2.5.1 Operating Cash Flow to Sales.............................................................................................13

2.5.2 Operating Cash Flow to Net Income...................................................................................13

2.5.3 Cash Flow to Total Debt.....................................................................................................14

2.6 Investor’s Ratio.........................................................................................................................14

2.6.1 Earnings per Share (EPS)....................................................................................................15

2.6.2 Dividend Pay-out................................................................................................................15

2.6.3 Price- Earnings Ratio (P/E Ratio).......................................................................................16

2.7 Common Size............................................................................................................................16

2.7.1 Vertical Analysis................................................................................................................17

2.7.2 Horizontal Analysis............................................................................................................21

2.8 DuPont Analysis........................................................................................................................25

2.8.1 DuPont - 3 factor ROE........................................................................................................25

2.8.1 DuPont - 2 factor ROA.......................................................................................................26

2.9 Segmental Analysis...................................................................................................................27

1

Strategic Financial Analysis

References...........................................................................................................................................28

2.0 Ratio Calculation

2.0 Introduction to Financial Analysis

Financial analyses are done for measuring the companies’ performance over a specific time

period. It is the process through which financial position are assessed by doing analysis on

stability, profitability and viability of the companies. Various financial statements like

Balance Sheet, Income Statement and Cash flow statements are used for the purpose of

analysis. Income statement of the company talks about its operational efficiency and balance

sheet talks about its net worth (Sultan, 2014).

The measures like financial ratios give the idea about the organisation’s profitability,

efficiency, liquidity, leverage etc. There are other analysis like vertical analysis and

horizontal analysis which are done over financial statements of the company.

We would study the financial performance and position of Booker and Tate and Lyle using

ratio analysis, horizontal analysis, vertical analysis, DuPont analysis and segmental analysis.

2.1 Profitability

2

Profitability ratios are preferred for measuring the ability of a company to generate revenue in relation to

the balance sheet, cost of operations, revenue and shareholders’ equity during the given financial year.

These ratios are able to reflect on number of business conditions. These ratios even depict the efficiency

level of an entity. The sales profitability and investments profitability can also be accessed through these

ratios (Fardiansyah, Achsani and Juanda, 2016).

References...........................................................................................................................................28

2.0 Ratio Calculation

2.0 Introduction to Financial Analysis

Financial analyses are done for measuring the companies’ performance over a specific time

period. It is the process through which financial position are assessed by doing analysis on

stability, profitability and viability of the companies. Various financial statements like

Balance Sheet, Income Statement and Cash flow statements are used for the purpose of

analysis. Income statement of the company talks about its operational efficiency and balance

sheet talks about its net worth (Sultan, 2014).

The measures like financial ratios give the idea about the organisation’s profitability,

efficiency, liquidity, leverage etc. There are other analysis like vertical analysis and

horizontal analysis which are done over financial statements of the company.

We would study the financial performance and position of Booker and Tate and Lyle using

ratio analysis, horizontal analysis, vertical analysis, DuPont analysis and segmental analysis.

2.1 Profitability

2

Profitability ratios are preferred for measuring the ability of a company to generate revenue in relation to

the balance sheet, cost of operations, revenue and shareholders’ equity during the given financial year.

These ratios are able to reflect on number of business conditions. These ratios even depict the efficiency

level of an entity. The sales profitability and investments profitability can also be accessed through these

ratios (Fardiansyah, Achsani and Juanda, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Financial Analysis

Table 1: Explanations to Important Ratios

Ratio Analysis

Profitability

Gross

Profit

Margin

(GPM)

This ratio shows the relationship established between the gross profit and net

sales wherein both cash and credit sales are considered. This ratio is often

referred as gross profit Ratio. Higher the ratio better is the management of the

company in managing the cost of sales (Tulsian, 2014).

Net Profit

Margin

(NPM)

The ratio tells about those earnings which the company has generated after

meeting its all types of expenses such as cost of sales, operational cost, taxes

etc. it gives us the idea about the company's profitability (The Motley Fool,

n.d.).

Return on

Capital

Employed

(ROCE)

This ratio helps to know the ability of the company to effectively allocate the

capital and indicates the profitability of the company. Thisratio carries out the

comparison between the the operational earnings and the capital invested in the

business. Overall, it shows the corporate performance (Das, 2017).

Liquidity

Current

Ratio

This ratio shows the level of current assets as compared to the current

liabilities of the company. The company with higher current ratio is in a better

liquidity position as compared to the ones with lower current ratio. This ratio

considers inventories and account receivables as liquid assets (Warrad, 2014).

Quick Ratio This ratio displays the level of highly liquid assets as compared to the current

liabilities of the company. This ratio does not consider inventory as the current

assets (Atieh, 2014).

Efficiency

3

Table 1: Explanations to Important Ratios

Ratio Analysis

Profitability

Gross

Profit

Margin

(GPM)

This ratio shows the relationship established between the gross profit and net

sales wherein both cash and credit sales are considered. This ratio is often

referred as gross profit Ratio. Higher the ratio better is the management of the

company in managing the cost of sales (Tulsian, 2014).

Net Profit

Margin

(NPM)

The ratio tells about those earnings which the company has generated after

meeting its all types of expenses such as cost of sales, operational cost, taxes

etc. it gives us the idea about the company's profitability (The Motley Fool,

n.d.).

Return on

Capital

Employed

(ROCE)

This ratio helps to know the ability of the company to effectively allocate the

capital and indicates the profitability of the company. Thisratio carries out the

comparison between the the operational earnings and the capital invested in the

business. Overall, it shows the corporate performance (Das, 2017).

Liquidity

Current

Ratio

This ratio shows the level of current assets as compared to the current

liabilities of the company. The company with higher current ratio is in a better

liquidity position as compared to the ones with lower current ratio. This ratio

considers inventories and account receivables as liquid assets (Warrad, 2014).

Quick Ratio This ratio displays the level of highly liquid assets as compared to the current

liabilities of the company. This ratio does not consider inventory as the current

assets (Atieh, 2014).

Efficiency

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Financial Analysis

Days of

Sales

Outstandin

g (DSO)

It helps to calculate the average days the company is taking for the cash

collection on the credit sales. It is estimated on a monthly, quarterly or yearly

basis (The Business Professor, n.d.).

Days of

Inventory

on Hand

(DOI)

The ratio speaks about average days taken by the business to convert the

inventory into sales. Also, it tells us about the inventory management of

company (bdc, n.d.).

Days of

Payables

(DOP)

This ratio tells about the average number of days taken by the company to

make payments on their account payables which includes, vendors, suppliers,

creditors etc. (WallstreetMojo, n.d.).

Cash

Conversion

Cycle

(CCC)

This tells us about how much days are taken by the company to collect cash

from the accounts receivables and how much days is it taking to convert raw

material into finished goods after subtracting the number of days taken by the

company to pay its short-term obligations (Yasir, Majid and Yousaf, 2014).

Leverage

Debt-to-

Equity

Ratio (D/E)

It displays how much of company's operations are being financed using debt

over equity (Morningstar, n.d.).

Gearing Gearing ratio measures the level of debt company has used in its capital

structure which includes both debt and equity (Thompson, 2018).

Cash Flow Ratios

Operating

Cash flow

to Sales

Operating cash flow to sales depicts that sales amount which has been

converted to cash flow from operating activities.

Operating

Cash Flow

to Net

This ratio represents the amount of net income converted to the cash flow from

operations

4

Days of

Sales

Outstandin

g (DSO)

It helps to calculate the average days the company is taking for the cash

collection on the credit sales. It is estimated on a monthly, quarterly or yearly

basis (The Business Professor, n.d.).

Days of

Inventory

on Hand

(DOI)

The ratio speaks about average days taken by the business to convert the

inventory into sales. Also, it tells us about the inventory management of

company (bdc, n.d.).

Days of

Payables

(DOP)

This ratio tells about the average number of days taken by the company to

make payments on their account payables which includes, vendors, suppliers,

creditors etc. (WallstreetMojo, n.d.).

Cash

Conversion

Cycle

(CCC)

This tells us about how much days are taken by the company to collect cash

from the accounts receivables and how much days is it taking to convert raw

material into finished goods after subtracting the number of days taken by the

company to pay its short-term obligations (Yasir, Majid and Yousaf, 2014).

Leverage

Debt-to-

Equity

Ratio (D/E)

It displays how much of company's operations are being financed using debt

over equity (Morningstar, n.d.).

Gearing Gearing ratio measures the level of debt company has used in its capital

structure which includes both debt and equity (Thompson, 2018).

Cash Flow Ratios

Operating

Cash flow

to Sales

Operating cash flow to sales depicts that sales amount which has been

converted to cash flow from operating activities.

Operating

Cash Flow

to Net

This ratio represents the amount of net income converted to the cash flow from

operations

4

Strategic Financial Analysis

Income

Cash Flow

to Total

Debt

This ratio shows the cash flow generated by the organisation through its

operations for each dollar of debt it used. It is an important measure solvency

and liquidity (Garcia, 2017).

Investor's Ratio

Earnings

Per Share

(EPS)

EPS is an important indicator of risk, company's success and its performance.

It is even used to forecast the future price of company's shares because the

change in the value of EPS often impacts the share price of that company

(Robbetze, Villiers and Harmse, 2017).

Dividend

Pay-out

(DPO)

Dividend pay-out refers to that portion of company's net income which is

distributed as dividend to the shareholders. Higher dividend pay-out ratio of a

company reflects its liberal dividend policy and low dividend pay-out reflects

the conservative dividend policy (Nwabuisi, Aseoluwa and Tolulope, 2017).

Price-

Earnings

Ratio (P/E)

This ratio is used to calculate the value of a firm for which it considers the

current price of the company's shares and earnings received on per share of the

company (Ghaeli, 2016).

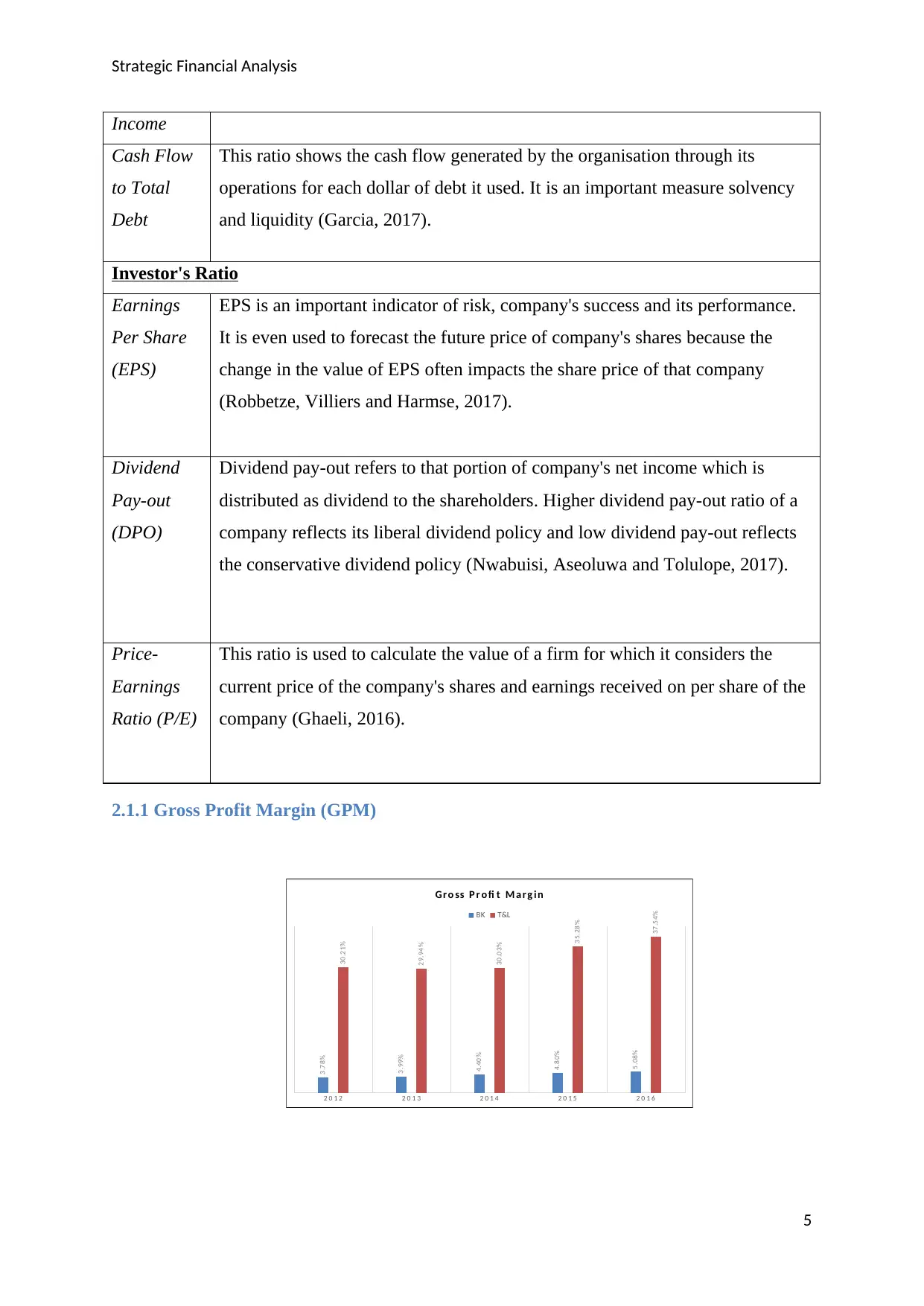

2.1.1 Gross Profit Margin (GPM)

2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6

3.78%

3.99%

4.40%

4.80%

5.08%

30.21%

29.94%

30.03%

35.28%

37.54%

Gr o ss P r o fi t M a r g i n

BK T&L

5

Income

Cash Flow

to Total

Debt

This ratio shows the cash flow generated by the organisation through its

operations for each dollar of debt it used. It is an important measure solvency

and liquidity (Garcia, 2017).

Investor's Ratio

Earnings

Per Share

(EPS)

EPS is an important indicator of risk, company's success and its performance.

It is even used to forecast the future price of company's shares because the

change in the value of EPS often impacts the share price of that company

(Robbetze, Villiers and Harmse, 2017).

Dividend

Pay-out

(DPO)

Dividend pay-out refers to that portion of company's net income which is

distributed as dividend to the shareholders. Higher dividend pay-out ratio of a

company reflects its liberal dividend policy and low dividend pay-out reflects

the conservative dividend policy (Nwabuisi, Aseoluwa and Tolulope, 2017).

Price-

Earnings

Ratio (P/E)

This ratio is used to calculate the value of a firm for which it considers the

current price of the company's shares and earnings received on per share of the

company (Ghaeli, 2016).

2.1.1 Gross Profit Margin (GPM)

2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6

3.78%

3.99%

4.40%

4.80%

5.08%

30.21%

29.94%

30.03%

35.28%

37.54%

Gr o ss P r o fi t M a r g i n

BK T&L

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Financial Analysis

The gross profit margin of Booker is showing an upward trend over five year period. The

gross profit margin has gone up because of increased revenue over the five years period. Over

the five years, the major part of the Booker’s revenue is coming from the non-tobacco

segment whose revenue increased by 44% (£2.39bn in 2012; £3.43bn in 2016), however the

revenue from the tobacco segment has just increased by 6.12% (£1.47bn in 2012; £1.56bn in

2016) (Booker Annual Report, 2016).

Gross profit margin of Tate & Lyle came down during 2013 as compared to 2012 therefore;

the gross profit margin of the company did not show a constant increasing trend. In 2014,

T&L acquired the assets and complete business of Winway Biotechnology Nantong Co. This

acquisition was done with the plan to enhance the capacity of Winway Biotechnology

Nantong for increasing the sale of speciality fibre products food. This increased the revenue

of T&L and also the improved capacity reduced T&L’s cost of production. As a result, the

gross profit margin increased by 7.5% from 2014(30%) to 2016 (37.5%) (Tate and Lyle,

2014).

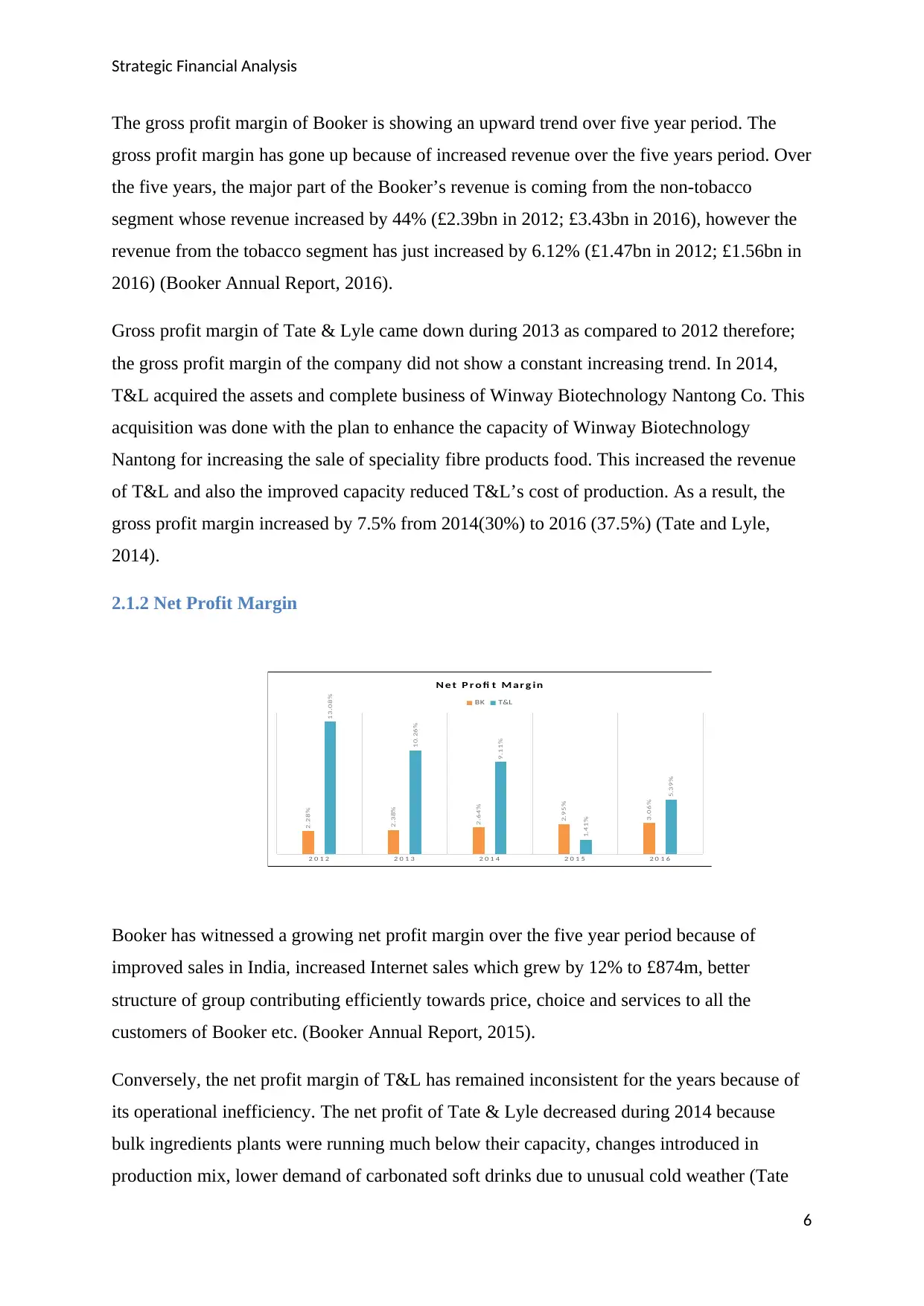

2.1.2 Net Profit Margin

2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6

2.28%

2.38%

2.64%

2.95%

3.06%

13.08%

10.26%

9.11%

1.41%

5.39%

N e t P r o fi t M ar g in

BK T&L

Booker has witnessed a growing net profit margin over the five year period because of

improved sales in India, increased Internet sales which grew by 12% to £874m, better

structure of group contributing efficiently towards price, choice and services to all the

customers of Booker etc. (Booker Annual Report, 2015).

Conversely, the net profit margin of T&L has remained inconsistent for the years because of

its operational inefficiency. The net profit of Tate & Lyle decreased during 2014 because

bulk ingredients plants were running much below their capacity, changes introduced in

production mix, lower demand of carbonated soft drinks due to unusual cold weather (Tate

6

The gross profit margin of Booker is showing an upward trend over five year period. The

gross profit margin has gone up because of increased revenue over the five years period. Over

the five years, the major part of the Booker’s revenue is coming from the non-tobacco

segment whose revenue increased by 44% (£2.39bn in 2012; £3.43bn in 2016), however the

revenue from the tobacco segment has just increased by 6.12% (£1.47bn in 2012; £1.56bn in

2016) (Booker Annual Report, 2016).

Gross profit margin of Tate & Lyle came down during 2013 as compared to 2012 therefore;

the gross profit margin of the company did not show a constant increasing trend. In 2014,

T&L acquired the assets and complete business of Winway Biotechnology Nantong Co. This

acquisition was done with the plan to enhance the capacity of Winway Biotechnology

Nantong for increasing the sale of speciality fibre products food. This increased the revenue

of T&L and also the improved capacity reduced T&L’s cost of production. As a result, the

gross profit margin increased by 7.5% from 2014(30%) to 2016 (37.5%) (Tate and Lyle,

2014).

2.1.2 Net Profit Margin

2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6

2.28%

2.38%

2.64%

2.95%

3.06%

13.08%

10.26%

9.11%

1.41%

5.39%

N e t P r o fi t M ar g in

BK T&L

Booker has witnessed a growing net profit margin over the five year period because of

improved sales in India, increased Internet sales which grew by 12% to £874m, better

structure of group contributing efficiently towards price, choice and services to all the

customers of Booker etc. (Booker Annual Report, 2015).

Conversely, the net profit margin of T&L has remained inconsistent for the years because of

its operational inefficiency. The net profit of Tate & Lyle decreased during 2014 because

bulk ingredients plants were running much below their capacity, changes introduced in

production mix, lower demand of carbonated soft drinks due to unusual cold weather (Tate

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Financial Analysis

and Lyle Annual Report, 2014). The major factor which impacted the net profit of T&L

during the year were the extended shutdown of SPLENDA Sucralose facility in Singapore

because of industrial accident, unusual and prolonged winter in US during 2013/14 caused

operations related difficulties in US plant and made the company enter with little inventory

during the year 2015 (Tate and Lyle Final Results, 2015).

No doubt, in most of the years out of five, net profit margin of Tate & Lyle has always been

more than that of Booker. It is because the production cost incurred by Tate & Lyle is much

lower as compared with that of Bookers’. The higher cost of production lowers the net profit

margin of Booker in spite of witnessing higher sales than T&L.

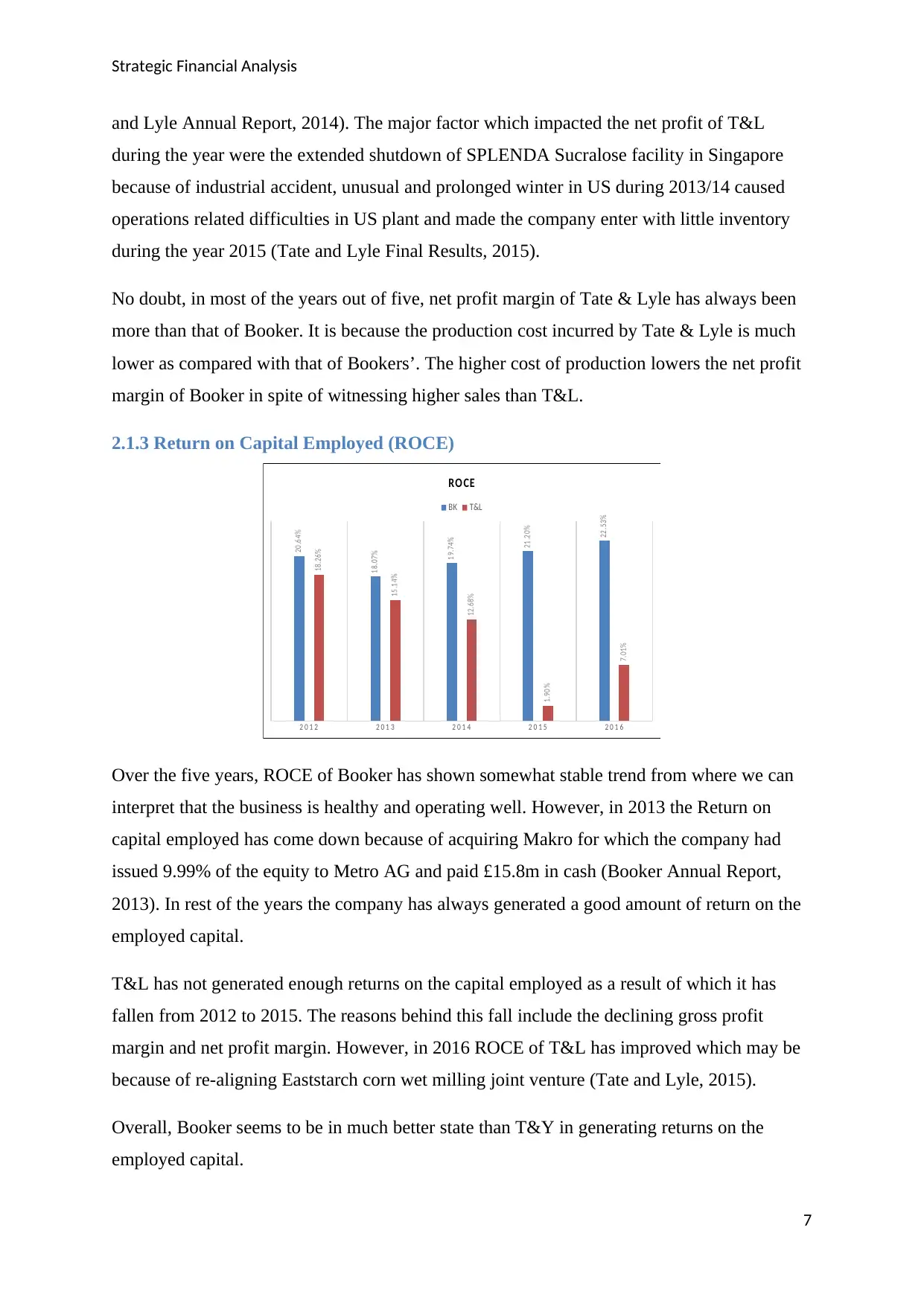

2.1.3 Return on Capital Employed (ROCE)

2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6

20.64%

18.07%

19.74%

21.20%

22.53%

18.26%

15.14%

12.68%

1.90%

7.01%

RO CE

BK T&L

Over the five years, ROCE of Booker has shown somewhat stable trend from where we can

interpret that the business is healthy and operating well. However, in 2013 the Return on

capital employed has come down because of acquiring Makro for which the company had

issued 9.99% of the equity to Metro AG and paid £15.8m in cash (Booker Annual Report,

2013). In rest of the years the company has always generated a good amount of return on the

employed capital.

T&L has not generated enough returns on the capital employed as a result of which it has

fallen from 2012 to 2015. The reasons behind this fall include the declining gross profit

margin and net profit margin. However, in 2016 ROCE of T&L has improved which may be

because of re-aligning Eaststarch corn wet milling joint venture (Tate and Lyle, 2015).

Overall, Booker seems to be in much better state than T&Y in generating returns on the

employed capital.

7

and Lyle Annual Report, 2014). The major factor which impacted the net profit of T&L

during the year were the extended shutdown of SPLENDA Sucralose facility in Singapore

because of industrial accident, unusual and prolonged winter in US during 2013/14 caused

operations related difficulties in US plant and made the company enter with little inventory

during the year 2015 (Tate and Lyle Final Results, 2015).

No doubt, in most of the years out of five, net profit margin of Tate & Lyle has always been

more than that of Booker. It is because the production cost incurred by Tate & Lyle is much

lower as compared with that of Bookers’. The higher cost of production lowers the net profit

margin of Booker in spite of witnessing higher sales than T&L.

2.1.3 Return on Capital Employed (ROCE)

2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6

20.64%

18.07%

19.74%

21.20%

22.53%

18.26%

15.14%

12.68%

1.90%

7.01%

RO CE

BK T&L

Over the five years, ROCE of Booker has shown somewhat stable trend from where we can

interpret that the business is healthy and operating well. However, in 2013 the Return on

capital employed has come down because of acquiring Makro for which the company had

issued 9.99% of the equity to Metro AG and paid £15.8m in cash (Booker Annual Report,

2013). In rest of the years the company has always generated a good amount of return on the

employed capital.

T&L has not generated enough returns on the capital employed as a result of which it has

fallen from 2012 to 2015. The reasons behind this fall include the declining gross profit

margin and net profit margin. However, in 2016 ROCE of T&L has improved which may be

because of re-aligning Eaststarch corn wet milling joint venture (Tate and Lyle, 2015).

Overall, Booker seems to be in much better state than T&Y in generating returns on the

employed capital.

7

Strategic Financial Analysis

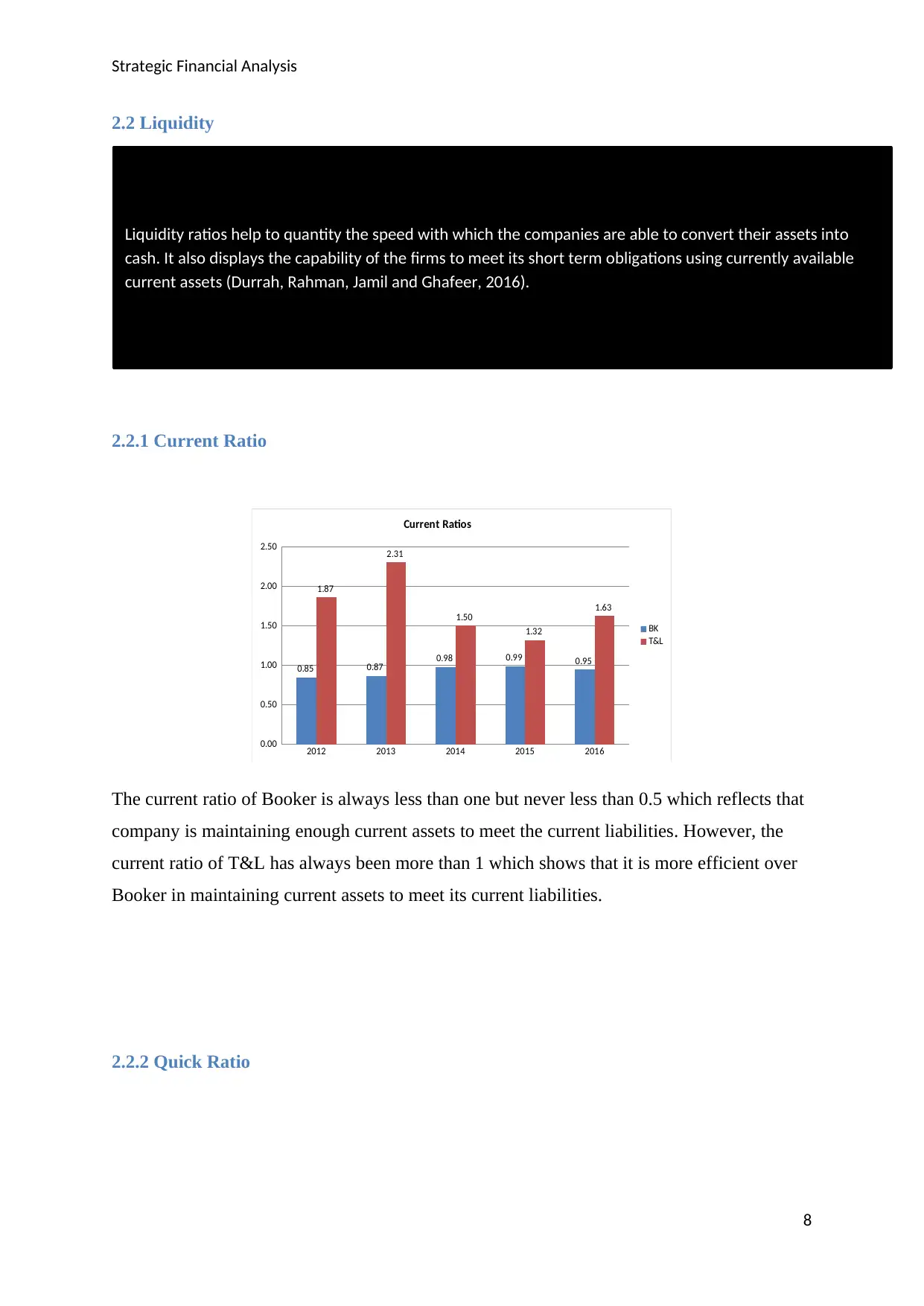

2.2 Liquidity

2.2.1 Current Ratio

2012 2013 2014 2015 2016

0.00

0.50

1.00

1.50

2.00

2.50

0.85 0.87 0.98 0.99 0.95

1.87

2.31

1.50

1.32

1.63

Current Ratios

BK

T&L

The current ratio of Booker is always less than one but never less than 0.5 which reflects that

company is maintaining enough current assets to meet the current liabilities. However, the

current ratio of T&L has always been more than 1 which shows that it is more efficient over

Booker in maintaining current assets to meet its current liabilities.

2.2.2 Quick Ratio

8

Liquidity ratios help to quantity the speed with which the companies are able to convert their assets into

cash. It also displays the capability of the firms to meet its short term obligations using currently available

current assets (Durrah, Rahman, Jamil and Ghafeer, 2016).

2.2 Liquidity

2.2.1 Current Ratio

2012 2013 2014 2015 2016

0.00

0.50

1.00

1.50

2.00

2.50

0.85 0.87 0.98 0.99 0.95

1.87

2.31

1.50

1.32

1.63

Current Ratios

BK

T&L

The current ratio of Booker is always less than one but never less than 0.5 which reflects that

company is maintaining enough current assets to meet the current liabilities. However, the

current ratio of T&L has always been more than 1 which shows that it is more efficient over

Booker in maintaining current assets to meet its current liabilities.

2.2.2 Quick Ratio

8

Liquidity ratios help to quantity the speed with which the companies are able to convert their assets into

cash. It also displays the capability of the firms to meet its short term obligations using currently available

current assets (Durrah, Rahman, Jamil and Ghafeer, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Financial Analysis

2012 2013 2014 2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.30 0.34

0.44 0.45 0.44

1.21

1.44

0.98

0.81

1.03

Quick Ratios

BK

T&L

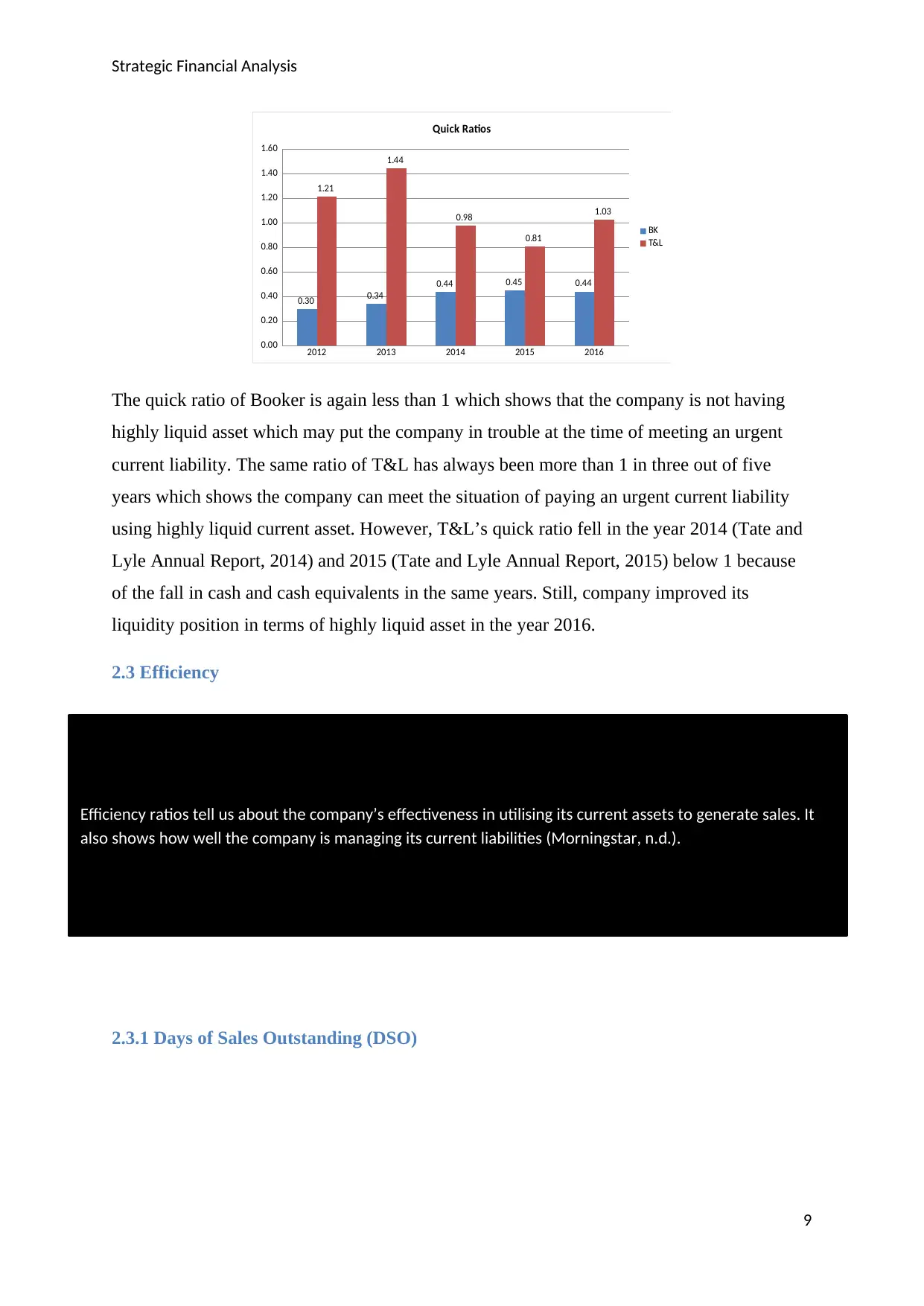

The quick ratio of Booker is again less than 1 which shows that the company is not having

highly liquid asset which may put the company in trouble at the time of meeting an urgent

current liability. The same ratio of T&L has always been more than 1 in three out of five

years which shows the company can meet the situation of paying an urgent current liability

using highly liquid current asset. However, T&L’s quick ratio fell in the year 2014 (Tate and

Lyle Annual Report, 2014) and 2015 (Tate and Lyle Annual Report, 2015) below 1 because

of the fall in cash and cash equivalents in the same years. Still, company improved its

liquidity position in terms of highly liquid asset in the year 2016.

2.3 Efficiency

2.3.1 Days of Sales Outstanding (DSO)

9

Efficiency ratios tell us about the company’s effectiveness in utilising its current assets to generate sales. It

also shows how well the company is managing its current liabilities (Morningstar, n.d.).

2012 2013 2014 2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.30 0.34

0.44 0.45 0.44

1.21

1.44

0.98

0.81

1.03

Quick Ratios

BK

T&L

The quick ratio of Booker is again less than 1 which shows that the company is not having

highly liquid asset which may put the company in trouble at the time of meeting an urgent

current liability. The same ratio of T&L has always been more than 1 in three out of five

years which shows the company can meet the situation of paying an urgent current liability

using highly liquid current asset. However, T&L’s quick ratio fell in the year 2014 (Tate and

Lyle Annual Report, 2014) and 2015 (Tate and Lyle Annual Report, 2015) below 1 because

of the fall in cash and cash equivalents in the same years. Still, company improved its

liquidity position in terms of highly liquid asset in the year 2016.

2.3 Efficiency

2.3.1 Days of Sales Outstanding (DSO)

9

Efficiency ratios tell us about the company’s effectiveness in utilising its current assets to generate sales. It

also shows how well the company is managing its current liabilities (Morningstar, n.d.).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Financial Analysis

2012 2013 2014 2015 2016

0

5

10

15

20

25

30

35

40

4 5 5 5 7

31

33

37 37 38

Days of Sales Outstanding

BK

T&L

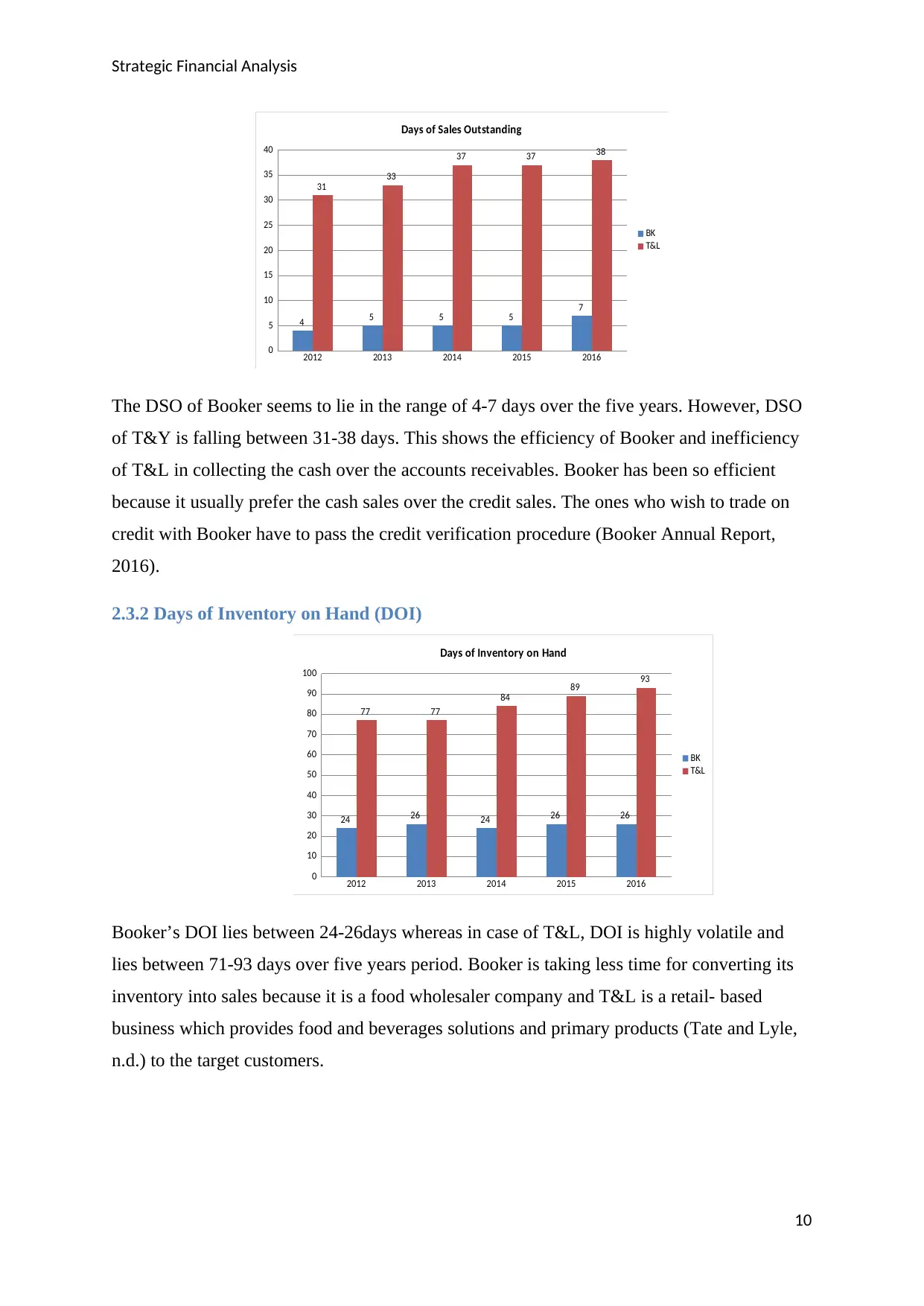

The DSO of Booker seems to lie in the range of 4-7 days over the five years. However, DSO

of T&Y is falling between 31-38 days. This shows the efficiency of Booker and inefficiency

of T&L in collecting the cash over the accounts receivables. Booker has been so efficient

because it usually prefer the cash sales over the credit sales. The ones who wish to trade on

credit with Booker have to pass the credit verification procedure (Booker Annual Report,

2016).

2.3.2 Days of Inventory on Hand (DOI)

2012 2013 2014 2015 2016

0

10

20

30

40

50

60

70

80

90

100

24 26 24 26 26

77 77

84 89 93

Days of Inventory on Hand

BK

T&L

Booker’s DOI lies between 24-26days whereas in case of T&L, DOI is highly volatile and

lies between 71-93 days over five years period. Booker is taking less time for converting its

inventory into sales because it is a food wholesaler company and T&L is a retail- based

business which provides food and beverages solutions and primary products (Tate and Lyle,

n.d.) to the target customers.

10

2012 2013 2014 2015 2016

0

5

10

15

20

25

30

35

40

4 5 5 5 7

31

33

37 37 38

Days of Sales Outstanding

BK

T&L

The DSO of Booker seems to lie in the range of 4-7 days over the five years. However, DSO

of T&Y is falling between 31-38 days. This shows the efficiency of Booker and inefficiency

of T&L in collecting the cash over the accounts receivables. Booker has been so efficient

because it usually prefer the cash sales over the credit sales. The ones who wish to trade on

credit with Booker have to pass the credit verification procedure (Booker Annual Report,

2016).

2.3.2 Days of Inventory on Hand (DOI)

2012 2013 2014 2015 2016

0

10

20

30

40

50

60

70

80

90

100

24 26 24 26 26

77 77

84 89 93

Days of Inventory on Hand

BK

T&L

Booker’s DOI lies between 24-26days whereas in case of T&L, DOI is highly volatile and

lies between 71-93 days over five years period. Booker is taking less time for converting its

inventory into sales because it is a food wholesaler company and T&L is a retail- based

business which provides food and beverages solutions and primary products (Tate and Lyle,

n.d.) to the target customers.

10

Strategic Financial Analysis

2.3.3 Days of Payables (DOP)

2012 2013 2014 2015 2016

0

10

20

30

40

50

60

38 40 38 40 4242 42 44

51

55

Days of Payables

BK

T&L

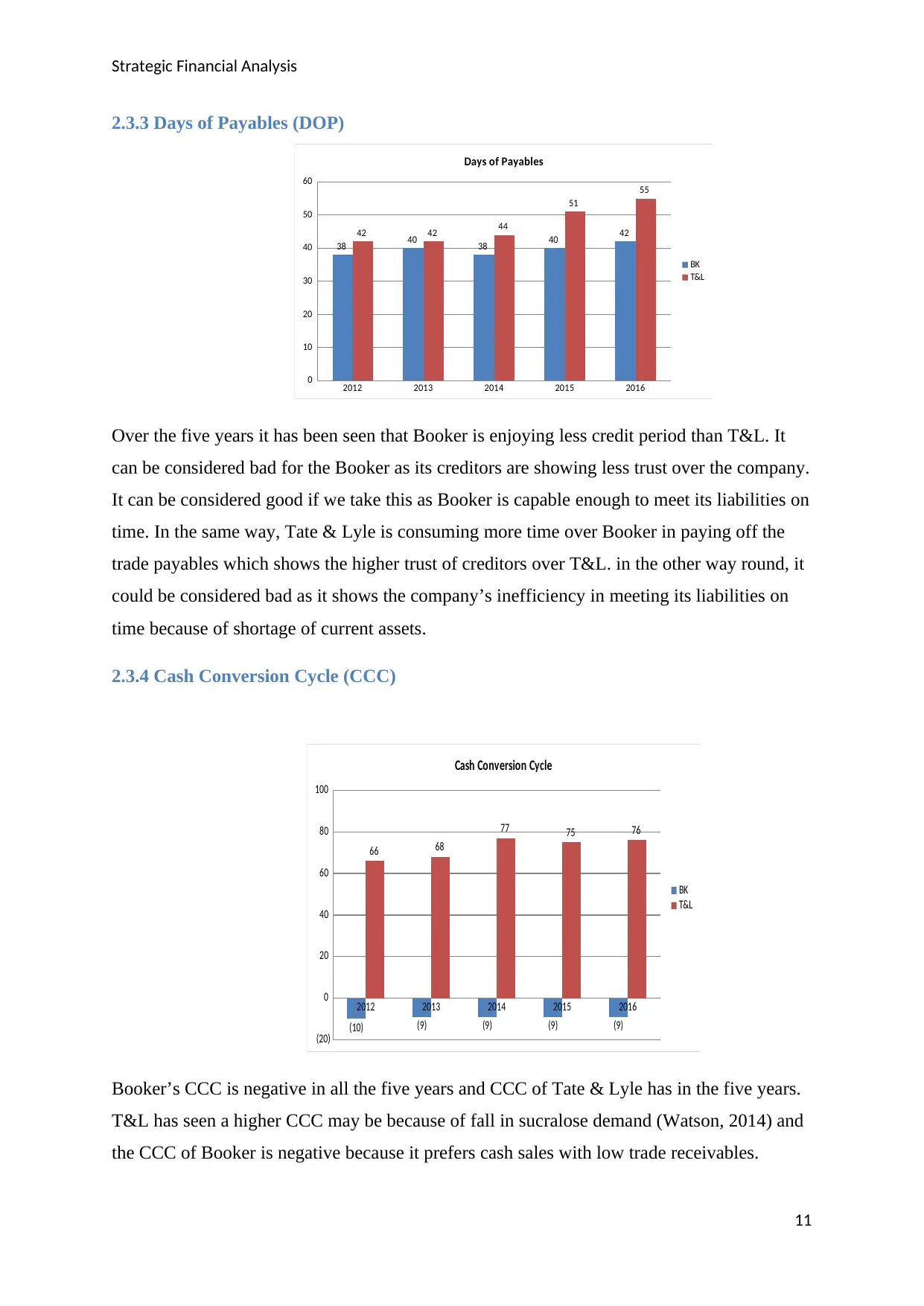

Over the five years it has been seen that Booker is enjoying less credit period than T&L. It

can be considered bad for the Booker as its creditors are showing less trust over the company.

It can be considered good if we take this as Booker is capable enough to meet its liabilities on

time. In the same way, Tate & Lyle is consuming more time over Booker in paying off the

trade payables which shows the higher trust of creditors over T&L. in the other way round, it

could be considered bad as it shows the company’s inefficiency in meeting its liabilities on

time because of shortage of current assets.

2.3.4 Cash Conversion Cycle (CCC)

2012 2013 2014 2015 2016

(20)

0

20

40

60

80

100

(10) (9) (9) (9) (9)

66 68

77 75 76

Cash Conversion Cycle

BK

T&L

Booker’s CCC is negative in all the five years and CCC of Tate & Lyle has in the five years.

T&L has seen a higher CCC may be because of fall in sucralose demand (Watson, 2014) and

the CCC of Booker is negative because it prefers cash sales with low trade receivables.

11

2.3.3 Days of Payables (DOP)

2012 2013 2014 2015 2016

0

10

20

30

40

50

60

38 40 38 40 4242 42 44

51

55

Days of Payables

BK

T&L

Over the five years it has been seen that Booker is enjoying less credit period than T&L. It

can be considered bad for the Booker as its creditors are showing less trust over the company.

It can be considered good if we take this as Booker is capable enough to meet its liabilities on

time. In the same way, Tate & Lyle is consuming more time over Booker in paying off the

trade payables which shows the higher trust of creditors over T&L. in the other way round, it

could be considered bad as it shows the company’s inefficiency in meeting its liabilities on

time because of shortage of current assets.

2.3.4 Cash Conversion Cycle (CCC)

2012 2013 2014 2015 2016

(20)

0

20

40

60

80

100

(10) (9) (9) (9) (9)

66 68

77 75 76

Cash Conversion Cycle

BK

T&L

Booker’s CCC is negative in all the five years and CCC of Tate & Lyle has in the five years.

T&L has seen a higher CCC may be because of fall in sucralose demand (Watson, 2014) and

the CCC of Booker is negative because it prefers cash sales with low trade receivables.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 35

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.