Strategic Financial Management: Investment Appraisal Report

VerifiedAdded on 2022/12/27

|12

|4010

|87

Report

AI Summary

This report delves into strategic financial management, focusing on investment appraisal techniques and financing strategies. It begins with an introduction to strategic financial management, emphasizing its role in achieving business goals and increasing shareholder equity. The core of the report involves the calculation and analysis of investment appraisal techniques, including payback period, internal rate of return (IRR), and net present value (NPV), applied to two example projects (Aspire and Wolf). Detailed calculations for each technique are presented, followed by an analysis and evaluation of the projects, recommending the adoption of Project Wolf due to its shorter payback period. The report justifies the use of NPV and payback period, highlighting their advantages and disadvantages. Finally, the report discusses two key sources of financing: equity, and their implications. This comprehensive analysis provides insights into making sound investment decisions and securing financial resources for business growth.

Strategic financial

management

management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Calculation of investment appraisal techniques..........................................................................3

Analysis and evaluation of Investment projects..........................................................................6

Two sources of financing.............................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Calculation of investment appraisal techniques..........................................................................3

Analysis and evaluation of Investment projects..........................................................................6

Two sources of financing.............................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Strategic financial management entails not just to controlling a business earnings, but doing so

with the aim of achieving the business's mission and vision and also increasing shareholder

equity over period (Bouzon, Govindan and Rodriguez, 2018). It aids in the establishment of

business goals, it also provides a framework for developing and implementing strategies to

address problems that arise during the process. It also entails setting out a plan to help the

company achieve its goals. In this report, calculation of different investment appraisal techniques

is shown which help company to determine the best suitable option for investments. In addition,

report also discuss the analysis and evaluation of most important investment method and the

source of funding which is implemented by company to meet the requirement of investment.

TASK

Calculation of investment appraisal techniques

Investment evaluation is a process through which a company evaluates the feasibility of potential

acquisitions or schemes depending on the results of various working capital as well as funding

techniques. This is a type of fundamental research for investors and it can assist in identifying

long-term patterns and also a corporation's potential profitability. These methods have excellent

answers to this issue. Each approach looks at the design from with a particular perspective and

offers a unique perspective. The most command methods which are used in the context of AYR

Co. to calculate the profitability of both project which is more beneficial are discussed below

with detail calculation (Chow, Greatbatch and Bracci, 2019).

Payback period: The payback time is amongst the most basic investment valuation strategies.

The payback strategy describes how long it takes for a venture to produce enough working

capital to offset its initial costs. The payback period seems to be the interval between when you

make an expenditure and when you break even on the transaction Take the expense of the project

and split it by the revealing how much profit to determine the payback date. Short repayment

times are preferable since it requires less time for such an individual to recoup their investment

resources.

Internal rate of return: The undervaluing rate, or internal rate of return, takes discounted

profitability to the same level as the original investment. To put it another way, it's really the

undervaluing pace during which the business won't lose money or earn a profit. This is achieved

Strategic financial management entails not just to controlling a business earnings, but doing so

with the aim of achieving the business's mission and vision and also increasing shareholder

equity over period (Bouzon, Govindan and Rodriguez, 2018). It aids in the establishment of

business goals, it also provides a framework for developing and implementing strategies to

address problems that arise during the process. It also entails setting out a plan to help the

company achieve its goals. In this report, calculation of different investment appraisal techniques

is shown which help company to determine the best suitable option for investments. In addition,

report also discuss the analysis and evaluation of most important investment method and the

source of funding which is implemented by company to meet the requirement of investment.

TASK

Calculation of investment appraisal techniques

Investment evaluation is a process through which a company evaluates the feasibility of potential

acquisitions or schemes depending on the results of various working capital as well as funding

techniques. This is a type of fundamental research for investors and it can assist in identifying

long-term patterns and also a corporation's potential profitability. These methods have excellent

answers to this issue. Each approach looks at the design from with a particular perspective and

offers a unique perspective. The most command methods which are used in the context of AYR

Co. to calculate the profitability of both project which is more beneficial are discussed below

with detail calculation (Chow, Greatbatch and Bracci, 2019).

Payback period: The payback time is amongst the most basic investment valuation strategies.

The payback strategy describes how long it takes for a venture to produce enough working

capital to offset its initial costs. The payback period seems to be the interval between when you

make an expenditure and when you break even on the transaction Take the expense of the project

and split it by the revealing how much profit to determine the payback date. Short repayment

times are preferable since it requires less time for such an individual to recoup their investment

resources.

Internal rate of return: The undervaluing rate, or internal rate of return, takes discounted

profitability to the same level as the original investment. To put it another way, it's really the

undervaluing pace during which the business won't lose money or earn a profit. This is achieved

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

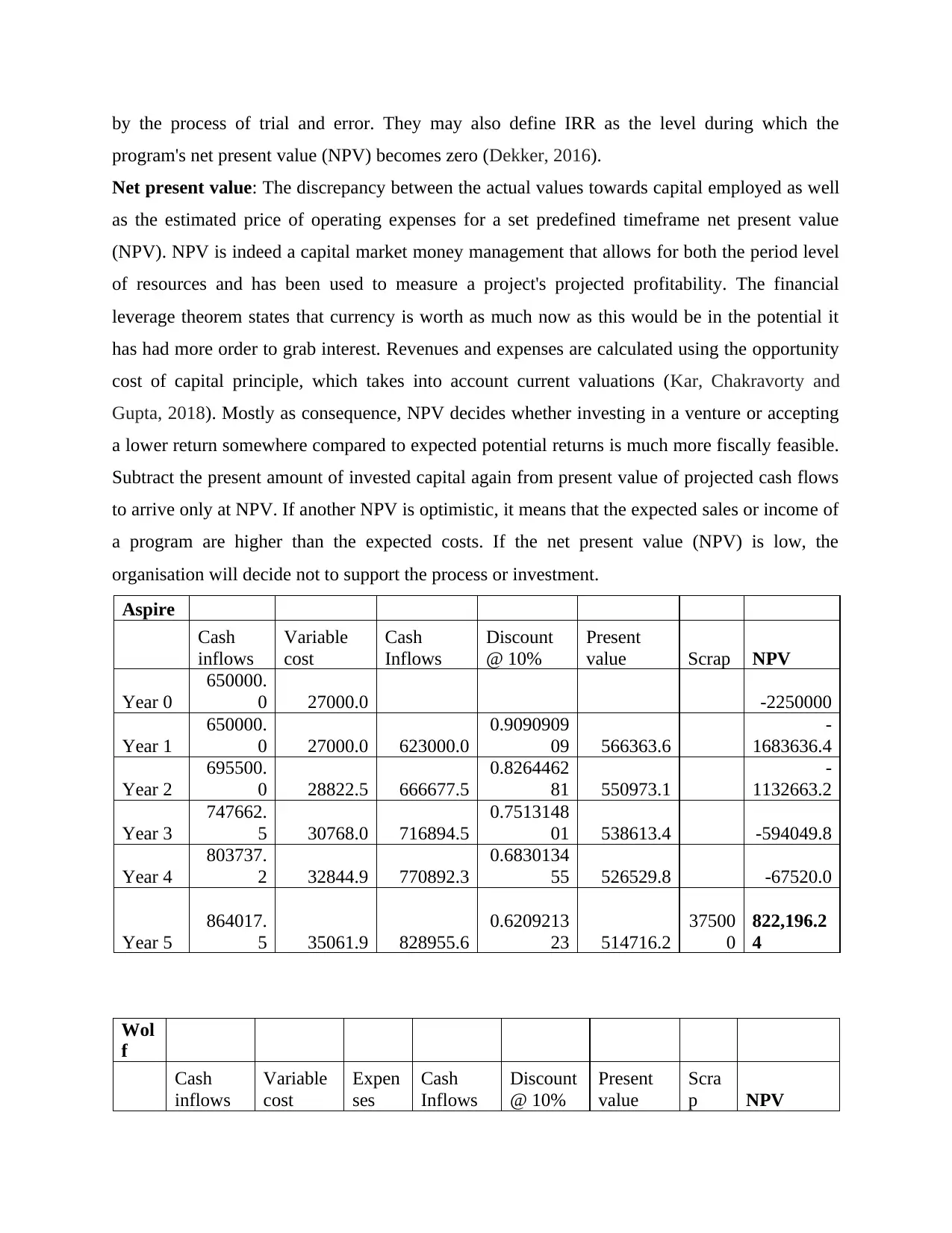

by the process of trial and error. They may also define IRR as the level during which the

program's net present value (NPV) becomes zero (Dekker, 2016).

Net present value: The discrepancy between the actual values towards capital employed as well

as the estimated price of operating expenses for a set predefined timeframe net present value

(NPV). NPV is indeed a capital market money management that allows for both the period level

of resources and has been used to measure a project's projected profitability. The financial

leverage theorem states that currency is worth as much now as this would be in the potential it

has had more order to grab interest. Revenues and expenses are calculated using the opportunity

cost of capital principle, which takes into account current valuations (Kar, Chakravorty and

Gupta, 2018). Mostly as consequence, NPV decides whether investing in a venture or accepting

a lower return somewhere compared to expected potential returns is much more fiscally feasible.

Subtract the present amount of invested capital again from present value of projected cash flows

to arrive only at NPV. If another NPV is optimistic, it means that the expected sales or income of

a program are higher than the expected costs. If the net present value (NPV) is low, the

organisation will decide not to support the process or investment.

Aspire

Cash

inflows

Variable

cost

Cash

Inflows

Discount

@ 10%

Present

value Scrap NPV

Year 0

650000.

0 27000.0 -2250000

Year 1

650000.

0 27000.0 623000.0

0.9090909

09 566363.6

-

1683636.4

Year 2

695500.

0 28822.5 666677.5

0.8264462

81 550973.1

-

1132663.2

Year 3

747662.

5 30768.0 716894.5

0.7513148

01 538613.4 -594049.8

Year 4

803737.

2 32844.9 770892.3

0.6830134

55 526529.8 -67520.0

Year 5

864017.

5 35061.9 828955.6

0.6209213

23 514716.2

37500

0

822,196.2

4

Wol

f

Cash

inflows

Variable

cost

Expen

ses

Cash

Inflows

Discount

@ 10%

Present

value

Scra

p NPV

program's net present value (NPV) becomes zero (Dekker, 2016).

Net present value: The discrepancy between the actual values towards capital employed as well

as the estimated price of operating expenses for a set predefined timeframe net present value

(NPV). NPV is indeed a capital market money management that allows for both the period level

of resources and has been used to measure a project's projected profitability. The financial

leverage theorem states that currency is worth as much now as this would be in the potential it

has had more order to grab interest. Revenues and expenses are calculated using the opportunity

cost of capital principle, which takes into account current valuations (Kar, Chakravorty and

Gupta, 2018). Mostly as consequence, NPV decides whether investing in a venture or accepting

a lower return somewhere compared to expected potential returns is much more fiscally feasible.

Subtract the present amount of invested capital again from present value of projected cash flows

to arrive only at NPV. If another NPV is optimistic, it means that the expected sales or income of

a program are higher than the expected costs. If the net present value (NPV) is low, the

organisation will decide not to support the process or investment.

Aspire

Cash

inflows

Variable

cost

Cash

Inflows

Discount

@ 10%

Present

value Scrap NPV

Year 0

650000.

0 27000.0 -2250000

Year 1

650000.

0 27000.0 623000.0

0.9090909

09 566363.6

-

1683636.4

Year 2

695500.

0 28822.5 666677.5

0.8264462

81 550973.1

-

1132663.2

Year 3

747662.

5 30768.0 716894.5

0.7513148

01 538613.4 -594049.8

Year 4

803737.

2 32844.9 770892.3

0.6830134

55 526529.8 -67520.0

Year 5

864017.

5 35061.9 828955.6

0.6209213

23 514716.2

37500

0

822,196.2

4

Wol

f

Cash

inflows

Variable

cost

Expen

ses

Cash

Inflows

Discount

@ 10%

Present

value

Scra

p NPV

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Year

0 955000.0 14400.0

18000.

0 -2250000

Year

1 955000.0 14400.0

18000.

0 922600.0

0.909090

909 838727.3

-

1411272.7

Year

2 955000.0 15480.0

16650.

0 922870.0

0.826446

281 762702.5 -648570.2

Year

3 955000.0 16641.0

15401.

3 922957.8

0.751314

801 693431.8 44861.6

Year

4 955000.0 17889.1

14246.

2 922864.8

0.683013

455 630329.1 675190.6

Year

5 955000.0 19230.8

13177.

7 922591.5

0.620921

323 572856.8

3750

00

1,623,047.

39

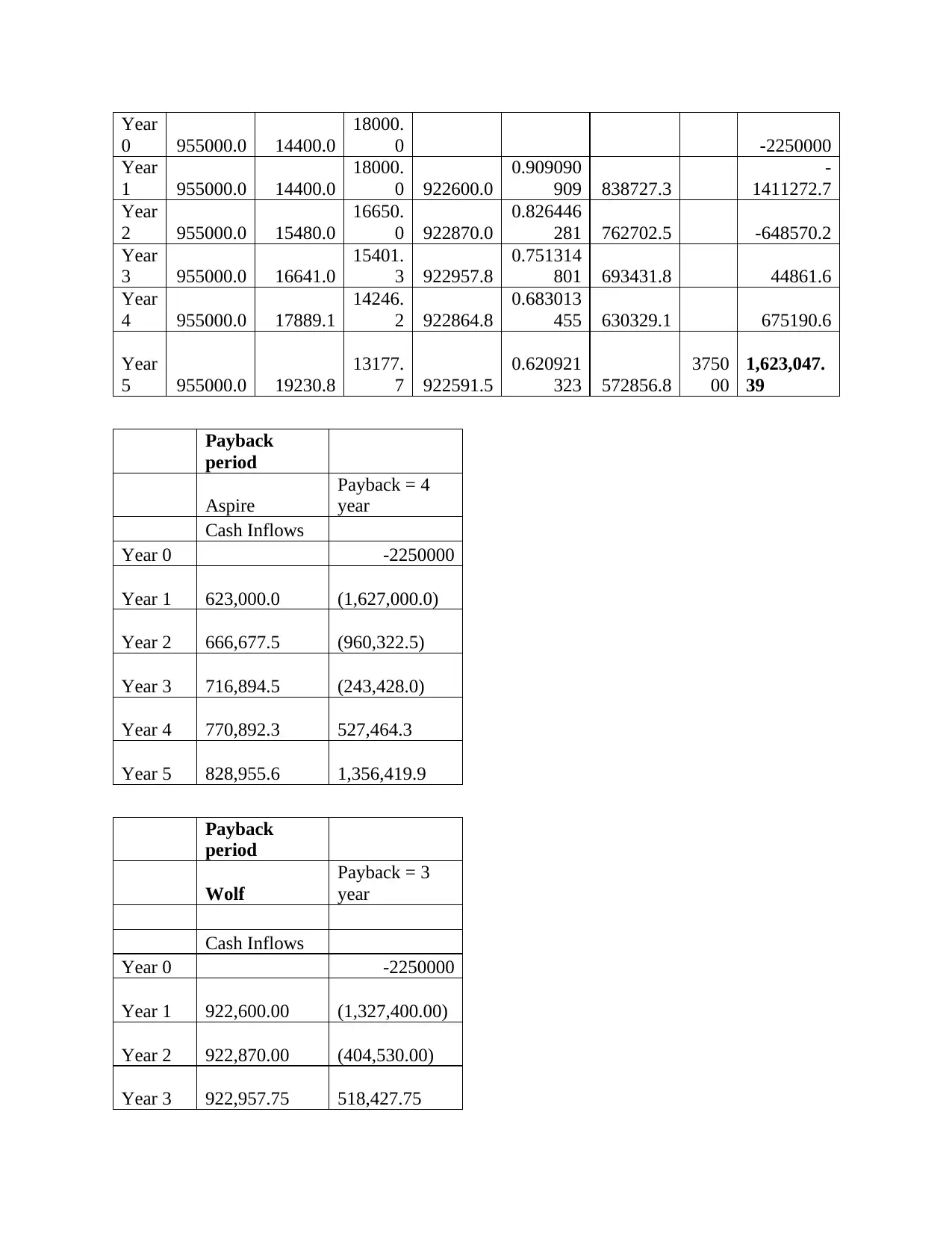

Payback

period

Aspire

Payback = 4

year

Cash Inflows

Year 0 -2250000

Year 1 623,000.0 (1,627,000.0)

Year 2 666,677.5 (960,322.5)

Year 3 716,894.5 (243,428.0)

Year 4 770,892.3 527,464.3

Year 5 828,955.6 1,356,419.9

Payback

period

Wolf

Payback = 3

year

Cash Inflows

Year 0 -2250000

Year 1 922,600.00 (1,327,400.00)

Year 2 922,870.00 (404,530.00)

Year 3 922,957.75 518,427.75

0 955000.0 14400.0

18000.

0 -2250000

Year

1 955000.0 14400.0

18000.

0 922600.0

0.909090

909 838727.3

-

1411272.7

Year

2 955000.0 15480.0

16650.

0 922870.0

0.826446

281 762702.5 -648570.2

Year

3 955000.0 16641.0

15401.

3 922957.8

0.751314

801 693431.8 44861.6

Year

4 955000.0 17889.1

14246.

2 922864.8

0.683013

455 630329.1 675190.6

Year

5 955000.0 19230.8

13177.

7 922591.5

0.620921

323 572856.8

3750

00

1,623,047.

39

Payback

period

Aspire

Payback = 4

year

Cash Inflows

Year 0 -2250000

Year 1 623,000.0 (1,627,000.0)

Year 2 666,677.5 (960,322.5)

Year 3 716,894.5 (243,428.0)

Year 4 770,892.3 527,464.3

Year 5 828,955.6 1,356,419.9

Payback

period

Wolf

Payback = 3

year

Cash Inflows

Year 0 -2250000

Year 1 922,600.00 (1,327,400.00)

Year 2 922,870.00 (404,530.00)

Year 3 922,957.75 518,427.75

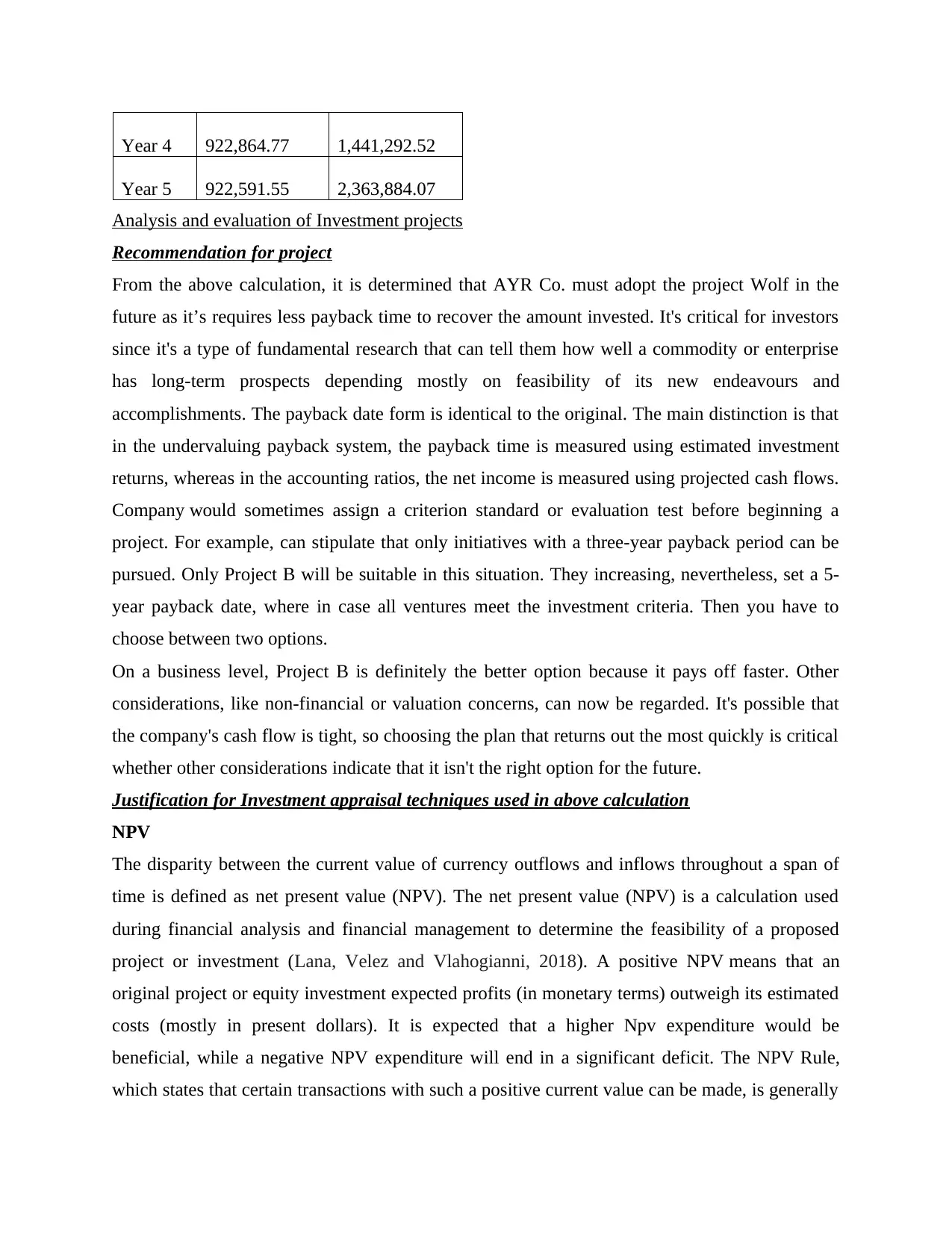

Year 4 922,864.77 1,441,292.52

Year 5 922,591.55 2,363,884.07

Analysis and evaluation of Investment projects

Recommendation for project

From the above calculation, it is determined that AYR Co. must adopt the project Wolf in the

future as it’s requires less payback time to recover the amount invested. It's critical for investors

since it's a type of fundamental research that can tell them how well a commodity or enterprise

has long-term prospects depending mostly on feasibility of its new endeavours and

accomplishments. The payback date form is identical to the original. The main distinction is that

in the undervaluing payback system, the payback time is measured using estimated investment

returns, whereas in the accounting ratios, the net income is measured using projected cash flows.

Company would sometimes assign a criterion standard or evaluation test before beginning a

project. For example, can stipulate that only initiatives with a three-year payback period can be

pursued. Only Project B will be suitable in this situation. They increasing, nevertheless, set a 5-

year payback date, where in case all ventures meet the investment criteria. Then you have to

choose between two options.

On a business level, Project B is definitely the better option because it pays off faster. Other

considerations, like non-financial or valuation concerns, can now be regarded. It's possible that

the company's cash flow is tight, so choosing the plan that returns out the most quickly is critical

whether other considerations indicate that it isn't the right option for the future.

Justification for Investment appraisal techniques used in above calculation

NPV

The disparity between the current value of currency outflows and inflows throughout a span of

time is defined as net present value (NPV). The net present value (NPV) is a calculation used

during financial analysis and financial management to determine the feasibility of a proposed

project or investment (Lana, Velez and Vlahogianni, 2018). A positive NPV means that an

original project or equity investment expected profits (in monetary terms) outweigh its estimated

costs (mostly in present dollars). It is expected that a higher Npv expenditure would be

beneficial, while a negative NPV expenditure will end in a significant deficit. The NPV Rule,

which states that certain transactions with such a positive current value can be made, is generally

Year 5 922,591.55 2,363,884.07

Analysis and evaluation of Investment projects

Recommendation for project

From the above calculation, it is determined that AYR Co. must adopt the project Wolf in the

future as it’s requires less payback time to recover the amount invested. It's critical for investors

since it's a type of fundamental research that can tell them how well a commodity or enterprise

has long-term prospects depending mostly on feasibility of its new endeavours and

accomplishments. The payback date form is identical to the original. The main distinction is that

in the undervaluing payback system, the payback time is measured using estimated investment

returns, whereas in the accounting ratios, the net income is measured using projected cash flows.

Company would sometimes assign a criterion standard or evaluation test before beginning a

project. For example, can stipulate that only initiatives with a three-year payback period can be

pursued. Only Project B will be suitable in this situation. They increasing, nevertheless, set a 5-

year payback date, where in case all ventures meet the investment criteria. Then you have to

choose between two options.

On a business level, Project B is definitely the better option because it pays off faster. Other

considerations, like non-financial or valuation concerns, can now be regarded. It's possible that

the company's cash flow is tight, so choosing the plan that returns out the most quickly is critical

whether other considerations indicate that it isn't the right option for the future.

Justification for Investment appraisal techniques used in above calculation

NPV

The disparity between the current value of currency outflows and inflows throughout a span of

time is defined as net present value (NPV). The net present value (NPV) is a calculation used

during financial analysis and financial management to determine the feasibility of a proposed

project or investment (Lana, Velez and Vlahogianni, 2018). A positive NPV means that an

original project or equity investment expected profits (in monetary terms) outweigh its estimated

costs (mostly in present dollars). It is expected that a higher Npv expenditure would be

beneficial, while a negative NPV expenditure will end in a significant deficit. The NPV Rule,

which states that certain transactions with such a positive current value can be made, is generally

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

considered acceptable. The NPV Rule, which states that certain securities with positive Net

present values returns can be accepted, is based on this principle. Adjusted for inflation as well

as earnings through new profits generated during the interim, cash throughout the current is

worth as much as the identical significant value. In other terms, a dollar generated by the

investment would be equal to the present value earned currently.

Advantages of using NPV.

Time value of money: This approach is a technique for determining the project viability. It took

a long time worth of capital into account. The valuation of potential cash flows would be lower

than the amount of modern cash flows. As a result, the greater the cash balance, the lower the

valuation. It really is a critical factor that should be taken into account when using the NPV

form. When a Project A with such a life of three years have higher revenue throughout the early

incident as well as a Project B with such a lifespan of three years have higher revenues during

the latter time, so using NPV, the company would be capable of picking Project A wisely

because inflows now are more valuable than inflows further on (Lu and Xiao-qiang, 2017).

The investment's valued: The Net Present Value equation not only determines not whether a

project can be viable, it also determines the gross benefit value. After undervaluing the

investment returns, the project would benefit $1,623,047.39, as seen in the example above. The

tool calculates the profit or loss on an investment.

Payback period

The payback approach aids in determining an investment portfolio payback time. The payback

period (PBP) seems to be the duration of information (in years) it requires again for retained

earnings from some kind of proposal's profits to offset the original investment. Once given the

option, a CFO will choose the plan with both the shorter payback time. Since it is simple to

measure and comprehend, the repayment way to measure capital spending programs is quite

common. That being said, it has several flaws and overlooks certain critical considerations that

really should be weighed when assessing the commercial feasibility of programs. The benefits of

the repayment method have made it a common option among executives. However, the

drawbacks of the repayment cycle, like those of any other system, prohibit managers about

relying entirely on it to make decisions. Throughout this post, we'll go through the benefits and

drawbacks including its repayment method in order to assist you form an opinion about this

capital budgeting technique.

present values returns can be accepted, is based on this principle. Adjusted for inflation as well

as earnings through new profits generated during the interim, cash throughout the current is

worth as much as the identical significant value. In other terms, a dollar generated by the

investment would be equal to the present value earned currently.

Advantages of using NPV.

Time value of money: This approach is a technique for determining the project viability. It took

a long time worth of capital into account. The valuation of potential cash flows would be lower

than the amount of modern cash flows. As a result, the greater the cash balance, the lower the

valuation. It really is a critical factor that should be taken into account when using the NPV

form. When a Project A with such a life of three years have higher revenue throughout the early

incident as well as a Project B with such a lifespan of three years have higher revenues during

the latter time, so using NPV, the company would be capable of picking Project A wisely

because inflows now are more valuable than inflows further on (Lu and Xiao-qiang, 2017).

The investment's valued: The Net Present Value equation not only determines not whether a

project can be viable, it also determines the gross benefit value. After undervaluing the

investment returns, the project would benefit $1,623,047.39, as seen in the example above. The

tool calculates the profit or loss on an investment.

Payback period

The payback approach aids in determining an investment portfolio payback time. The payback

period (PBP) seems to be the duration of information (in years) it requires again for retained

earnings from some kind of proposal's profits to offset the original investment. Once given the

option, a CFO will choose the plan with both the shorter payback time. Since it is simple to

measure and comprehend, the repayment way to measure capital spending programs is quite

common. That being said, it has several flaws and overlooks certain critical considerations that

really should be weighed when assessing the commercial feasibility of programs. The benefits of

the repayment method have made it a common option among executives. However, the

drawbacks of the repayment cycle, like those of any other system, prohibit managers about

relying entirely on it to make decisions. Throughout this post, we'll go through the benefits and

drawbacks including its repayment method in order to assist you form an opinion about this

capital budgeting technique.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages of Payback period

Simple to Manage and Comprehend: This is one of the most important benefits including its

payback era. The approach has a small number of inputs and is simpler to quantify than most

financial analysis. To measure the payback time, all they need are the preliminary project

expense and estimated cash flows. Other strategies were using the same inputs too though, but

they require more conclusions. For example, the quantity of investment, which is used by most

approaches, necessitates managers making some judgments (McLeod, Payne and Evert, 2016).

Quick Mitigate: Managers can easily measure the payback time of programmes because it is

easier to compute and has less inputs. This enables management to make swift decisions, which

is critical in businesses with scarce capital.

Liquidity is preferred: Almost no capital budgeting approach shows the payback date, which is

critical detail. A proposal with a smaller payback time is usually less risky. For small enterprises

with scarce funding, such knowledge is critical. Small companies must rapidly recoup their costs

in order to expand in new ventures. In markets where there is uncertainty or rapid technical

development, the payback approach is very useful. Since of this volatility, forecasting projected

annual cash inflows is challenging. As a result, doing that and completing tasks with fast PBP

decreases the potential of a failure due to fragmentation. The payback technique's most important

benefit has been its flexibility. It was a simple method of comparing many proposals just choose

the one with the quickest payback period. The payback, on the other hand, has a number of

realistic and conceptual disadvantages.

Two sources of financing

Equity, also known as investors' equity (or investors' equitable throughout the context of

privately owned companies), is the sum of capital that would be returning to a minority

employees because all of the corporation's properties are repossessed but all of the liabilities was

paying off during the event of an insolvency. That is the amount of the business sale without any

authority given by the firm that were not exchanged with the transaction throughout the terms of

payment. Furthermore, shareholder equity may be used to reflect a business's market valuation

(Passetti and Tenucci, 2016). Equity should be used as a method of money. It also reflects a

corporation's pro-rata holding of its shares. Among the most popular types of capital is equity

that can be placed on a firm's balance sheet. It is consider to be most popular pieces of evidence

used by investors to measure a corporate accounting stability, so it is seen on the accounting

Simple to Manage and Comprehend: This is one of the most important benefits including its

payback era. The approach has a small number of inputs and is simpler to quantify than most

financial analysis. To measure the payback time, all they need are the preliminary project

expense and estimated cash flows. Other strategies were using the same inputs too though, but

they require more conclusions. For example, the quantity of investment, which is used by most

approaches, necessitates managers making some judgments (McLeod, Payne and Evert, 2016).

Quick Mitigate: Managers can easily measure the payback time of programmes because it is

easier to compute and has less inputs. This enables management to make swift decisions, which

is critical in businesses with scarce capital.

Liquidity is preferred: Almost no capital budgeting approach shows the payback date, which is

critical detail. A proposal with a smaller payback time is usually less risky. For small enterprises

with scarce funding, such knowledge is critical. Small companies must rapidly recoup their costs

in order to expand in new ventures. In markets where there is uncertainty or rapid technical

development, the payback approach is very useful. Since of this volatility, forecasting projected

annual cash inflows is challenging. As a result, doing that and completing tasks with fast PBP

decreases the potential of a failure due to fragmentation. The payback technique's most important

benefit has been its flexibility. It was a simple method of comparing many proposals just choose

the one with the quickest payback period. The payback, on the other hand, has a number of

realistic and conceptual disadvantages.

Two sources of financing

Equity, also known as investors' equity (or investors' equitable throughout the context of

privately owned companies), is the sum of capital that would be returning to a minority

employees because all of the corporation's properties are repossessed but all of the liabilities was

paying off during the event of an insolvency. That is the amount of the business sale without any

authority given by the firm that were not exchanged with the transaction throughout the terms of

payment. Furthermore, shareholder equity may be used to reflect a business's market valuation

(Passetti and Tenucci, 2016). Equity should be used as a method of money. It also reflects a

corporation's pro-rata holding of its shares. Among the most popular types of capital is equity

that can be placed on a firm's balance sheet. It is consider to be most popular pieces of evidence

used by investors to measure a corporate accounting stability, so it is seen on the accounting

records. The "assets-minus-liabilities" share price formula creates a straightforward image of a

company's wealth, and thus can be widely accessed by financial analysts, by contrasting specific

figures representing what the corporation controls and what it holds. The funds earned by a firm

is known as equity, but is used to buy properties, invest in ventures, and finance operations. A

company may make investments by raising debt (throughout the form of grants or securities) or

equity (throughout the securities of the company) (by selling stock). Equity investments become

preferred by investors because they allow them to participate more fully in a company's earnings

and progress. The company is focused on Angle investors for case of equity financing which

normally call businesses with negative stock value to be expensive or dangerous investments.

Market value is also not a reliable measure of a corporate accounting stability on its own; but,

when combined with other resources and indicators, an individual can correctly assess a firm's

performance. It's significant because it reflects the worth of an investor's interest in a firm, as

measured by another ownership of the preferred equity. Stockholders who own shares in a

company will benefit from both capital gains income. Shareholders who own stock will be able

to vote on company decisions as well as operations of a company appointments. These stock

ownership advantages encourage shareholders to remain committed to the organization. The

value of a company's stockholders may be rational or irrational. If the result is satisfactory, the

total profitability are sufficient to support its liabilities. When the capital structure is

unfavourable, the corporation's liabilities outweigh its funds; this is known as financial statement

bankruptcy (Quattrone, 2016).

A debt would be a chunk of cash lent by another person. Many companies and individuals

employ debt to finance major transactions that they would not be able to make under normal

conditions. A loan agreement allows the investing party to make payments mostly on assumption

that this be repaid at a future stage, normally with interest. Loans, such as deposits and vehicle

loans, as well as unsecured loans as well as consumer debt, seem to be the most prevalent types

of debt. The creditor is expected to repay the total debt before a certain date, usually several

months in the future, according to the borrower to the lender. The amount of inflation that even

the creditor will pay is also specified throughout the loan agreements. In order to make the

investment AYR co. is planning to take a bank loan for a certified bank on reliable interest rate

including the time period which is not a burden over company. The rate of interest which the

applicant must pay monthly, calculated as a proportion including its amount borrowed, also is

company's wealth, and thus can be widely accessed by financial analysts, by contrasting specific

figures representing what the corporation controls and what it holds. The funds earned by a firm

is known as equity, but is used to buy properties, invest in ventures, and finance operations. A

company may make investments by raising debt (throughout the form of grants or securities) or

equity (throughout the securities of the company) (by selling stock). Equity investments become

preferred by investors because they allow them to participate more fully in a company's earnings

and progress. The company is focused on Angle investors for case of equity financing which

normally call businesses with negative stock value to be expensive or dangerous investments.

Market value is also not a reliable measure of a corporate accounting stability on its own; but,

when combined with other resources and indicators, an individual can correctly assess a firm's

performance. It's significant because it reflects the worth of an investor's interest in a firm, as

measured by another ownership of the preferred equity. Stockholders who own shares in a

company will benefit from both capital gains income. Shareholders who own stock will be able

to vote on company decisions as well as operations of a company appointments. These stock

ownership advantages encourage shareholders to remain committed to the organization. The

value of a company's stockholders may be rational or irrational. If the result is satisfactory, the

total profitability are sufficient to support its liabilities. When the capital structure is

unfavourable, the corporation's liabilities outweigh its funds; this is known as financial statement

bankruptcy (Quattrone, 2016).

A debt would be a chunk of cash lent by another person. Many companies and individuals

employ debt to finance major transactions that they would not be able to make under normal

conditions. A loan agreement allows the investing party to make payments mostly on assumption

that this be repaid at a future stage, normally with interest. Loans, such as deposits and vehicle

loans, as well as unsecured loans as well as consumer debt, seem to be the most prevalent types

of debt. The creditor is expected to repay the total debt before a certain date, usually several

months in the future, according to the borrower to the lender. The amount of inflation that even

the creditor will pay is also specified throughout the loan agreements. In order to make the

investment AYR co. is planning to take a bank loan for a certified bank on reliable interest rate

including the time period which is not a burden over company. The rate of interest which the

applicant must pay monthly, calculated as a proportion including its amount borrowed, also is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

specified throughout the existing loans. Interest has been used to reimburse the investor for

carrying on the burden of the debt and also allowing the applicant to pay back the loan rapidly in

attempt to lessen his net interest cost. Firms that really need funding have other lending solutions

than loans as well as consumer debt. Individuals cannot make investments or corporate bonds,

which are popular forms of commercial paper. Securities are a form of debt product that helps a

business to raise money by offering shareholders the guarantee of redemption (Sledgianowski,

Gomaa and Tan, 2017).

Impact on average cost of capital

As a company receives money from debt borrowing, the financing portion of the income

statement shows a favourable item, and also a rise in current liabilities. Principal, that must be

lent to lenders and shareholders, and interest are all part of debt servicing. Interest payments on

loans lower net profits and cash flow, even though debt doesn't really magnify ownership. This

decrease in net profit also results in a tax advantage since the gross income is smaller. Liquidity

ratios like debt-to-equity as well as debt-to-total capital increase as debt levels rise. Covenants

are also attached to loan funding, requiring a company to fulfil some term debt as well as debt-

level conditions. Debt creditors have priority over shareholders throughout the case of a

company's insolvency.

While equity funding has little effect on a company's earnings, it will dilute current shareholders'

investments when the firm's total income is distributed over a greater amount of securities. As a

business raises money from equity funding, the capital structure from financing operations

column shows a favourable item, as well as a rise in common shares at par net realizable value.

Impact of bank loan on shareholder and lenders

Certain contract terms, known as agreements, will apply to higher payments, including the

availability of budget allocations details. Loans aren't really versatile, and you might end up

spending interest on money they don't need. If your clients don't reimburse them on time, they

might have difficulty making mortgage repayments, triggering cash flow issues. In certain

situations, loans are backed by the business's properties or your personal belongings, such as

your house. Lending institutions can have cheaper rates that unsecured loans, however if they

can't afford the mortgage, the savings or property could be at threat. If they wish to repay the

money until the expiry of the agreement, they will have to pay a small fee (Zyoud and Fuchs-

Hanusch, 2017). If they wish to pay back the loan even before expiry of the agreement, you will

carrying on the burden of the debt and also allowing the applicant to pay back the loan rapidly in

attempt to lessen his net interest cost. Firms that really need funding have other lending solutions

than loans as well as consumer debt. Individuals cannot make investments or corporate bonds,

which are popular forms of commercial paper. Securities are a form of debt product that helps a

business to raise money by offering shareholders the guarantee of redemption (Sledgianowski,

Gomaa and Tan, 2017).

Impact on average cost of capital

As a company receives money from debt borrowing, the financing portion of the income

statement shows a favourable item, and also a rise in current liabilities. Principal, that must be

lent to lenders and shareholders, and interest are all part of debt servicing. Interest payments on

loans lower net profits and cash flow, even though debt doesn't really magnify ownership. This

decrease in net profit also results in a tax advantage since the gross income is smaller. Liquidity

ratios like debt-to-equity as well as debt-to-total capital increase as debt levels rise. Covenants

are also attached to loan funding, requiring a company to fulfil some term debt as well as debt-

level conditions. Debt creditors have priority over shareholders throughout the case of a

company's insolvency.

While equity funding has little effect on a company's earnings, it will dilute current shareholders'

investments when the firm's total income is distributed over a greater amount of securities. As a

business raises money from equity funding, the capital structure from financing operations

column shows a favourable item, as well as a rise in common shares at par net realizable value.

Impact of bank loan on shareholder and lenders

Certain contract terms, known as agreements, will apply to higher payments, including the

availability of budget allocations details. Loans aren't really versatile, and you might end up

spending interest on money they don't need. If your clients don't reimburse them on time, they

might have difficulty making mortgage repayments, triggering cash flow issues. In certain

situations, loans are backed by the business's properties or your personal belongings, such as

your house. Lending institutions can have cheaper rates that unsecured loans, however if they

can't afford the mortgage, the savings or property could be at threat. If they wish to repay the

money until the expiry of the agreement, they will have to pay a small fee (Zyoud and Fuchs-

Hanusch, 2017). If they wish to pay back the loan even before expiry of the agreement, you will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

have to pay a fee, especially if the interest’s rate is set. Refinance for recurring costs is not a

smart option and it will be impossible to keep up with repayments. Rather, ongoing costs can be

supported through cash from purchases, likely with an outstanding balance as a buffer. If you are

unable to secure a loan or any form of financing from the bank, people have other financing

opportunities. See Business Lending Options - An Outline for more detail. Prepare the company

for bank lending if they think a line of credit is a feasible choice for the company.

CONCLUSION

In the last of report, it is founded that the funding is moderately risky, falling in between

low-risk debt and high-risk financing decision. The borrower creates a mortgage, but if all looks

perfectly, the corporation repays the loan on agreed-upon terms. The "best" sum of debt differs

from one company to the next. Various criteria are being used to decide whether the amount of

debt, or interest, that a business uses to finance activities is within a proper range while

determining its financial status.

smart option and it will be impossible to keep up with repayments. Rather, ongoing costs can be

supported through cash from purchases, likely with an outstanding balance as a buffer. If you are

unable to secure a loan or any form of financing from the bank, people have other financing

opportunities. See Business Lending Options - An Outline for more detail. Prepare the company

for bank lending if they think a line of credit is a feasible choice for the company.

CONCLUSION

In the last of report, it is founded that the funding is moderately risky, falling in between

low-risk debt and high-risk financing decision. The borrower creates a mortgage, but if all looks

perfectly, the corporation repays the loan on agreed-upon terms. The "best" sum of debt differs

from one company to the next. Various criteria are being used to decide whether the amount of

debt, or interest, that a business uses to finance activities is within a proper range while

determining its financial status.

REFERENCES

Books and Journals

Bouzon, M., Govindan, K. and Rodriguez, C .M. T., 2018. Evaluating barriers for reverse

logistics implementation under a multiple stakeholders’ perspective analysis using grey

decision making approach. Resources, conservation and recycling, 128, pp.315-335.

Chow, D.S., Greatbatch, D. and Bracci, E., 2019. Financial responsibilisation and the role of

accounting in social work: challenges and possibilities. The British Journal of Social

Work, 49(6), pp.1582-1600.

Dekker, H.C., 2016. On the boundaries between intrafirm and interfirm management accounting

research. Management Accounting Research, 31, pp.86-99.

Du, L., Feng, Y., Lu, W., Kong, L. and Yang, Z., 2020. Evolutionary game analysis of

stakeholders' decision-making behaviours in construction and demolition waste

management. Environmental Impact Assessment Review, 84, p.106408.

Kar, S., Chakravorty, B., Sinha, S. and Gupta, M. P., 2018. Analysis of stakeholders within IoT

ecosystem. In Digital India (pp. 251-276). Springer, Cham.

Lana, I., Del Ser, J., Velez, M. and Vlahogianni, E.I., 2018. Road traffic forecasting: Recent

advances and new challenges. IEEE Intelligent Transportation Systems Magazine, 10(2),

pp.93-109.

Lu, D. A. I. and Xiao-qiang, Z .H. I., 2017. How the Westernized Management Accounting

Techniques are Transferred to China's SOEs? A Case Study. Finance Research, (1), p.3.

McLeod, M.S., Payne, G.T. and Evert, R.E., 2016. Organizational ethics research: A systematic

review of methods and analytical techniques. Journal of Business Ethics, 134(3), pp.429-

443.

Passetti, E. and Tenucci, A., 2016. Eco-efficiency measurement and the influence of

organisational factors: evidence from large Italian companies. Journal of Cleaner

production, 122, pp.228-239.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Sledgianowski, D., Gomaa, M. and Tan, C., 2017. Toward integration of Big Data, technology

and information systems competencies into the accounting curriculum. Journal of

Accounting Education, 38, pp.81-93.

Zyoud, S.H. and Fuchs-Hanusch, D., 2017. A bibliometric-based survey on AHP and TOPSIS

techniques. Expert systems with applications, 78, pp.158-181.

Books and Journals

Bouzon, M., Govindan, K. and Rodriguez, C .M. T., 2018. Evaluating barriers for reverse

logistics implementation under a multiple stakeholders’ perspective analysis using grey

decision making approach. Resources, conservation and recycling, 128, pp.315-335.

Chow, D.S., Greatbatch, D. and Bracci, E., 2019. Financial responsibilisation and the role of

accounting in social work: challenges and possibilities. The British Journal of Social

Work, 49(6), pp.1582-1600.

Dekker, H.C., 2016. On the boundaries between intrafirm and interfirm management accounting

research. Management Accounting Research, 31, pp.86-99.

Du, L., Feng, Y., Lu, W., Kong, L. and Yang, Z., 2020. Evolutionary game analysis of

stakeholders' decision-making behaviours in construction and demolition waste

management. Environmental Impact Assessment Review, 84, p.106408.

Kar, S., Chakravorty, B., Sinha, S. and Gupta, M. P., 2018. Analysis of stakeholders within IoT

ecosystem. In Digital India (pp. 251-276). Springer, Cham.

Lana, I., Del Ser, J., Velez, M. and Vlahogianni, E.I., 2018. Road traffic forecasting: Recent

advances and new challenges. IEEE Intelligent Transportation Systems Magazine, 10(2),

pp.93-109.

Lu, D. A. I. and Xiao-qiang, Z .H. I., 2017. How the Westernized Management Accounting

Techniques are Transferred to China's SOEs? A Case Study. Finance Research, (1), p.3.

McLeod, M.S., Payne, G.T. and Evert, R.E., 2016. Organizational ethics research: A systematic

review of methods and analytical techniques. Journal of Business Ethics, 134(3), pp.429-

443.

Passetti, E. and Tenucci, A., 2016. Eco-efficiency measurement and the influence of

organisational factors: evidence from large Italian companies. Journal of Cleaner

production, 122, pp.228-239.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Sledgianowski, D., Gomaa, M. and Tan, C., 2017. Toward integration of Big Data, technology

and information systems competencies into the accounting curriculum. Journal of

Accounting Education, 38, pp.81-93.

Zyoud, S.H. and Fuchs-Hanusch, D., 2017. A bibliometric-based survey on AHP and TOPSIS

techniques. Expert systems with applications, 78, pp.158-181.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.