Financial Analysis of Bank of Valletta and APS Bank: Report

VerifiedAdded on 2022/08/26

|26

|3929

|17

Report

AI Summary

This report presents a financial analysis of two Maltese banks, Bank of Valletta (BOV) and APS Bank, examining their performance using financial ratios and market indicators from 2017 and 2018. The analysis includes profitability ratios (operating income to total assets, return on equity, and return on total assets) and capital structure ratios (interest coverage ratio, loan to assets ratio, and capital adequacy ratio). The report also incorporates vertical analysis to assess the banks' income statements and balance sheets, along with a discussion of key performance indicators (KPIs) such as customer retention and market performance. The report highlights the risks and opportunities facing these banks, offering insights into their strategic financial management practices. The analysis is based on the data of 2017 and 2018, and it also includes a discussion of the industry's performance in Malta.

Strategic financial

managment

managment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................3

Interpretation and evaluation.................................................................................................................3

Ratio Analysis.......................................................................................................................................3

Profitability ratios..............................................................................................................................4

Capital structure ratios.......................................................................................................................7

Vertical analysis....................................................................................................................................8

Market performance and KPIs.........................................................................................................10

Risks and opportunities.......................................................................................................................13

Conclusion...........................................................................................................................................16

References...........................................................................................................................................17

Introduction...........................................................................................................................................3

Interpretation and evaluation.................................................................................................................3

Ratio Analysis.......................................................................................................................................3

Profitability ratios..............................................................................................................................4

Capital structure ratios.......................................................................................................................7

Vertical analysis....................................................................................................................................8

Market performance and KPIs.........................................................................................................10

Risks and opportunities.......................................................................................................................13

Conclusion...........................................................................................................................................16

References...........................................................................................................................................17

Introduction

The report brings out a discussion on financial analysis of company registered in Malta Stock

Exchange. Financial analysis is conducted with the help of ratio analysis and commonsize

horizontal analysis with the data of 2017 and 2018. For non-financial analysis, KPIs and

market performance has been examined of Bank of Valletta and APS bank. Ratio analysis is

to examine several aspects of the organisation’s operation and performance. It can improve

the understanding of financial statements and reports. There are several risks and

opportunities in the banking industry.

Bank of Valletta is a Maltese banking service organisation, which is headquartered in Santa

Venera. This bank is one of the oldest and established service provider in the nation. The

organisation has 44 branches, a head office, wealth management, and regional business

centres located near Maltese islands (Bank of Valletta, 2018). The bank was founded in 1974,

which is headquartered in BOV centre, Santa Venera, and Triq il kanun. Products offered

include commercial and retail banking with number of employees (1843). APS is a private

bank, which is founded in 1910 and it was incorporated in 1970 (Bank of Valletta, 2018). It

includes and employs 300 staff members across Gozo and Malta. The products offered

include commercial banking, asset management, and private banking. Number of employees

include 300. The subsidiaries include APS Funds Sicav plc (Bank of Valletta, 2018).

Interpretation and evaluation

Ratio Analysis

Ratio analysis is to examine different aspects of the organisation’s financial situations. While

analysing the bank`s performance, it is seen that measurement indicates capital, assets, and

liabilities with the help of organisation`s balance sheet (Srinivasan, & Thevaranjan, 2016).

The report brings out a discussion on financial analysis of company registered in Malta Stock

Exchange. Financial analysis is conducted with the help of ratio analysis and commonsize

horizontal analysis with the data of 2017 and 2018. For non-financial analysis, KPIs and

market performance has been examined of Bank of Valletta and APS bank. Ratio analysis is

to examine several aspects of the organisation’s operation and performance. It can improve

the understanding of financial statements and reports. There are several risks and

opportunities in the banking industry.

Bank of Valletta is a Maltese banking service organisation, which is headquartered in Santa

Venera. This bank is one of the oldest and established service provider in the nation. The

organisation has 44 branches, a head office, wealth management, and regional business

centres located near Maltese islands (Bank of Valletta, 2018). The bank was founded in 1974,

which is headquartered in BOV centre, Santa Venera, and Triq il kanun. Products offered

include commercial and retail banking with number of employees (1843). APS is a private

bank, which is founded in 1910 and it was incorporated in 1970 (Bank of Valletta, 2018). It

includes and employs 300 staff members across Gozo and Malta. The products offered

include commercial banking, asset management, and private banking. Number of employees

include 300. The subsidiaries include APS Funds Sicav plc (Bank of Valletta, 2018).

Interpretation and evaluation

Ratio Analysis

Ratio analysis is to examine different aspects of the organisation’s financial situations. While

analysing the bank`s performance, it is seen that measurement indicates capital, assets, and

liabilities with the help of organisation`s balance sheet (Srinivasan, & Thevaranjan, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

These ratios will ensure the financial stability of banks through profitability ratios, and capital

structural ratios. Financial reporting in banking sector, which is different from other

industries. The main objective of banking organisation is to attract funds at acceptable cost

and finally invest to earn higher returns. For profitability analysis, return on capital

employed, return on equity, return on total assets, and operating income to the total assets.

For capital structure ratios, interest coverage ratio, loan to assets ratio and capital adequacy

ratio (APS bank, 2018).

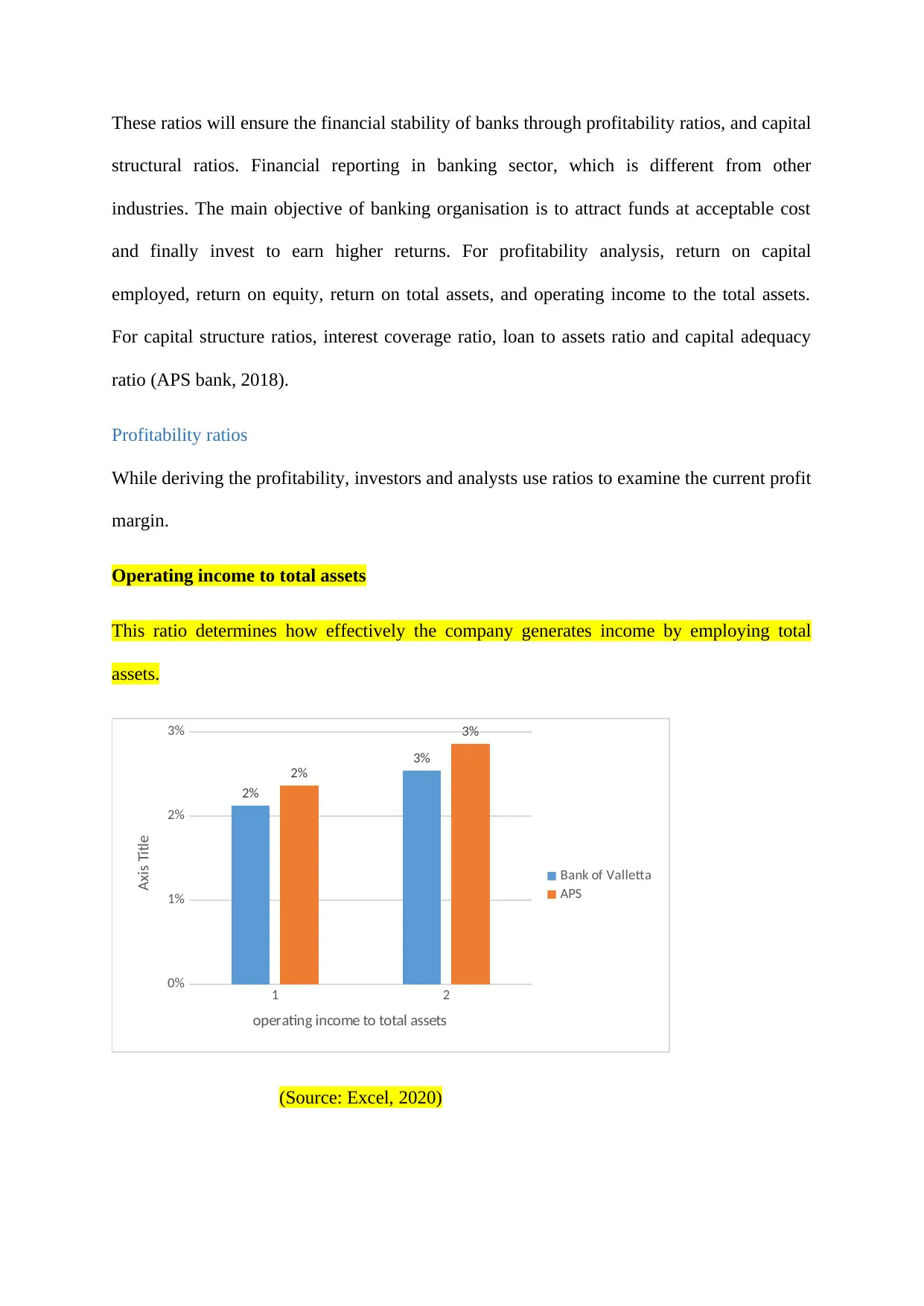

Profitability ratios

While deriving the profitability, investors and analysts use ratios to examine the current profit

margin.

Operating income to total assets

This ratio determines how effectively the company generates income by employing total

assets.

1 2

0%

1%

2%

3%

2%

3%

2%

3%

Bank of Valletta

APS

operating income to total assets

Axis Title

(Source: Excel, 2020)

structural ratios. Financial reporting in banking sector, which is different from other

industries. The main objective of banking organisation is to attract funds at acceptable cost

and finally invest to earn higher returns. For profitability analysis, return on capital

employed, return on equity, return on total assets, and operating income to the total assets.

For capital structure ratios, interest coverage ratio, loan to assets ratio and capital adequacy

ratio (APS bank, 2018).

Profitability ratios

While deriving the profitability, investors and analysts use ratios to examine the current profit

margin.

Operating income to total assets

This ratio determines how effectively the company generates income by employing total

assets.

1 2

0%

1%

2%

3%

2%

3%

2%

3%

Bank of Valletta

APS

operating income to total assets

Axis Title

(Source: Excel, 2020)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

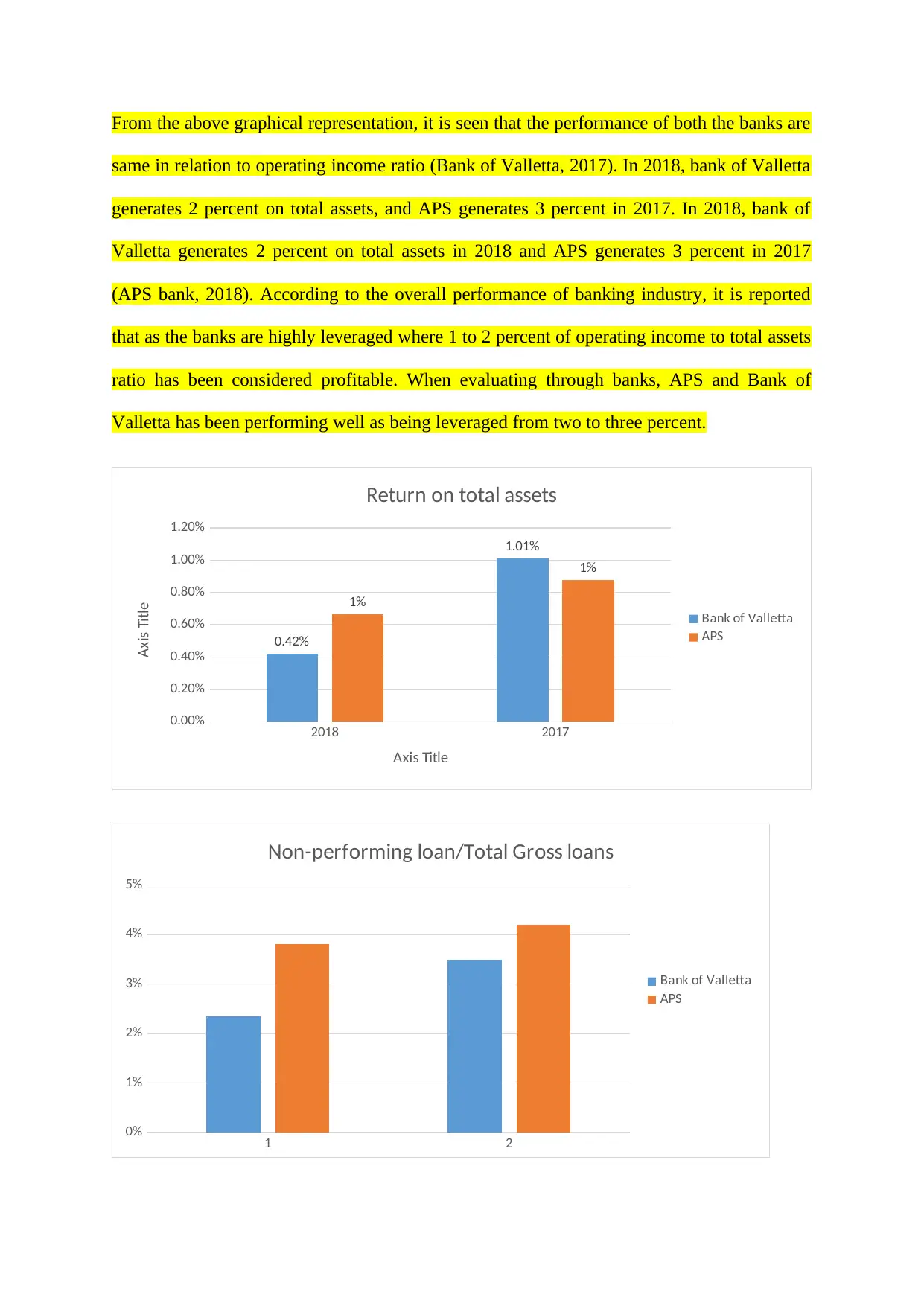

From the above graphical representation, it is seen that the performance of both the banks are

same in relation to operating income ratio (Bank of Valletta, 2017). In 2018, bank of Valletta

generates 2 percent on total assets, and APS generates 3 percent in 2017. In 2018, bank of

Valletta generates 2 percent on total assets in 2018 and APS generates 3 percent in 2017

(APS bank, 2018). According to the overall performance of banking industry, it is reported

that as the banks are highly leveraged where 1 to 2 percent of operating income to total assets

ratio has been considered profitable. When evaluating through banks, APS and Bank of

Valletta has been performing well as being leveraged from two to three percent.

2018 2017

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

0.42%

1.01%

1%

1%

Return on total assets

Bank of Valletta

APS

Axis Title

Axis Title

1 2

0%

1%

2%

3%

4%

5%

Non-performing loan/Total Gross loans

Bank of Valletta

APS

same in relation to operating income ratio (Bank of Valletta, 2017). In 2018, bank of Valletta

generates 2 percent on total assets, and APS generates 3 percent in 2017. In 2018, bank of

Valletta generates 2 percent on total assets in 2018 and APS generates 3 percent in 2017

(APS bank, 2018). According to the overall performance of banking industry, it is reported

that as the banks are highly leveraged where 1 to 2 percent of operating income to total assets

ratio has been considered profitable. When evaluating through banks, APS and Bank of

Valletta has been performing well as being leveraged from two to three percent.

2018 2017

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

0.42%

1.01%

1%

1%

Return on total assets

Bank of Valletta

APS

Axis Title

Axis Title

1 2

0%

1%

2%

3%

4%

5%

Non-performing loan/Total Gross loans

Bank of Valletta

APS

According the banking industry of Malta, standard non-performing loan to total gross loan is

estimated at 4.099 percent in 2017 and 5 percent in 2018. Reduced non-performing loan ratio

means more secure loans to customers. APS Bank`s has 3.8 and 4.2 percent, which indicates

that it performs well in regards to the industry. Bank of Valletta is able to maintain much

lower ratio, which is a good indication of recovery the loans.

Increasing net interest income ratio is quite helpful. Bank of Valletta generates 7 percent in

2017, and 8 percent interest income in 2018. There is a need to improve interest income ratio

by enhancing and increasing net operating income, decreasing operating expense, pay off

existing debt, and decreasing the borrowing amount. Expense to income ratio has been one of

the important criteria through which banks can evaluate how much expense it has occurred to

have operating income. Bank of Valletta generates 43 percent in 2017 and 55 percent in

2018. On the other hand, decreasing expense to income ratio indicates that the company has

been incurring less and generating more, which signifies that resources are being used in an

efficient way.

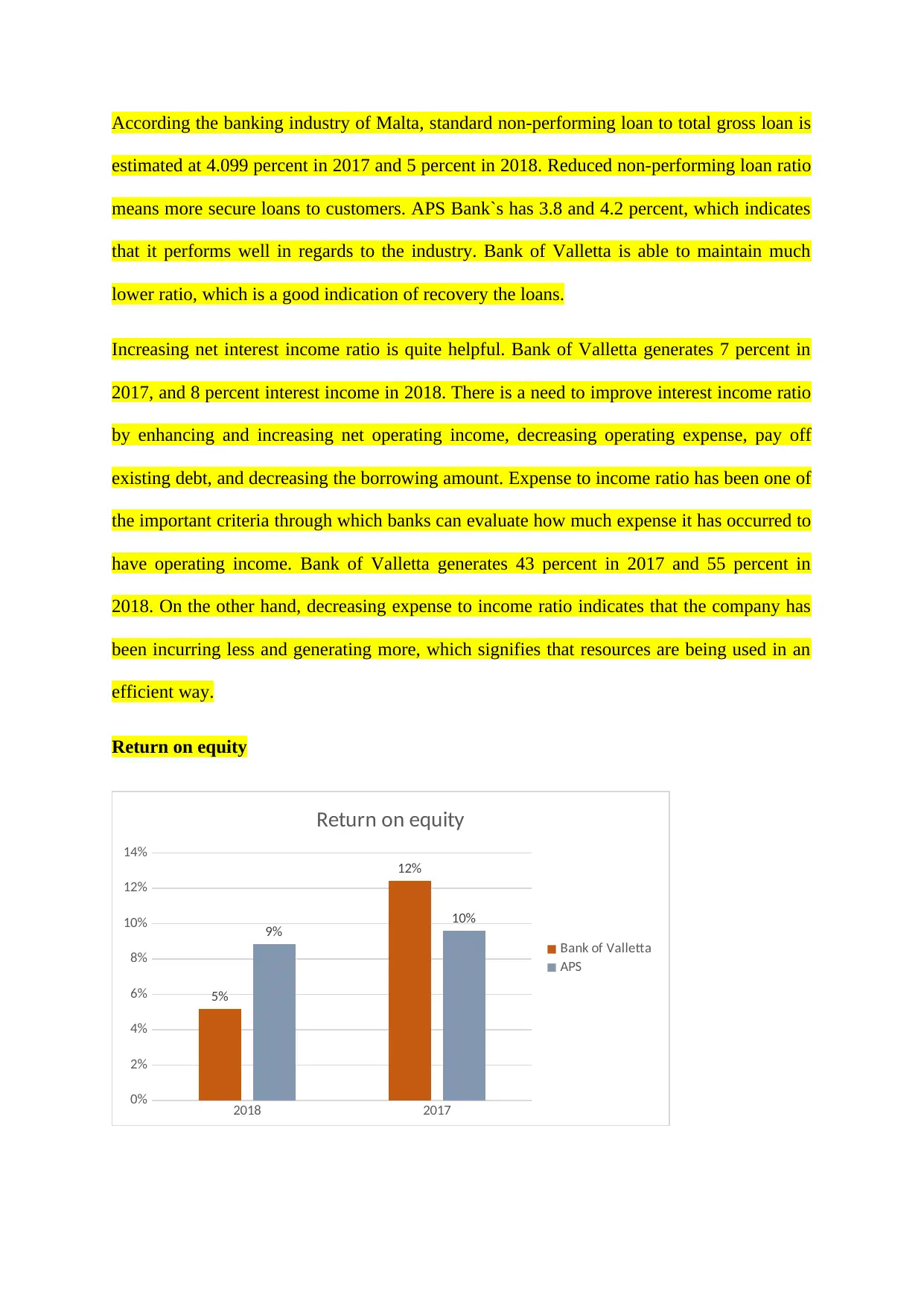

Return on equity

2018 2017

0%

2%

4%

6%

8%

10%

12%

14%

5%

12%

9% 10%

Return on equity

Bank of Valletta

APS

estimated at 4.099 percent in 2017 and 5 percent in 2018. Reduced non-performing loan ratio

means more secure loans to customers. APS Bank`s has 3.8 and 4.2 percent, which indicates

that it performs well in regards to the industry. Bank of Valletta is able to maintain much

lower ratio, which is a good indication of recovery the loans.

Increasing net interest income ratio is quite helpful. Bank of Valletta generates 7 percent in

2017, and 8 percent interest income in 2018. There is a need to improve interest income ratio

by enhancing and increasing net operating income, decreasing operating expense, pay off

existing debt, and decreasing the borrowing amount. Expense to income ratio has been one of

the important criteria through which banks can evaluate how much expense it has occurred to

have operating income. Bank of Valletta generates 43 percent in 2017 and 55 percent in

2018. On the other hand, decreasing expense to income ratio indicates that the company has

been incurring less and generating more, which signifies that resources are being used in an

efficient way.

Return on equity

2018 2017

0%

2%

4%

6%

8%

10%

12%

14%

5%

12%

9% 10%

Return on equity

Bank of Valletta

APS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This indicates the response of net profit in relation to equity. APS is consistent for both the

years 2017 and 2018. On the other hand, Bank of Valletta earns 5 percent in 2017 and 12

percent in 2018.

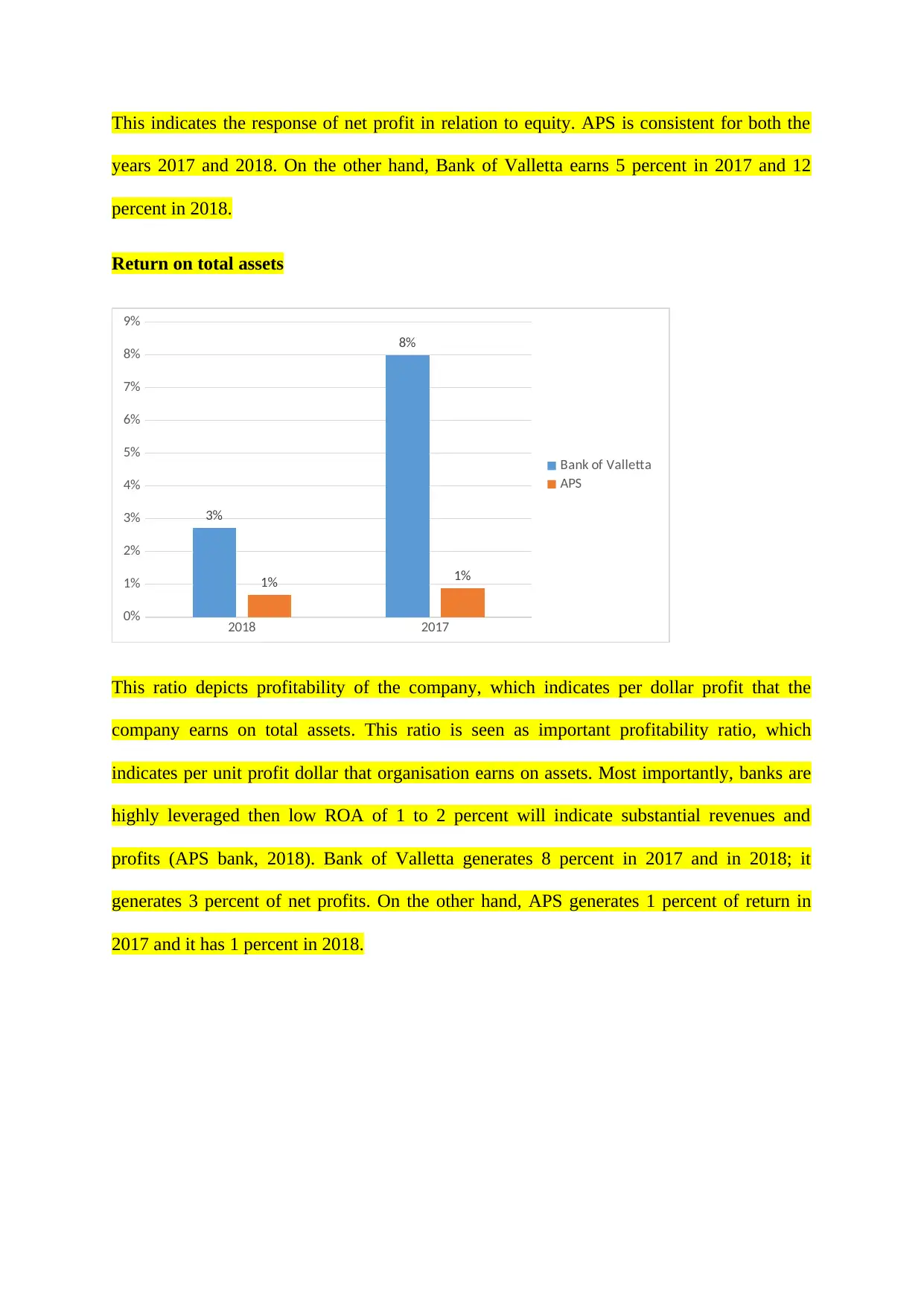

Return on total assets

2018 2017

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

3%

8%

1% 1%

Bank of Valletta

APS

This ratio depicts profitability of the company, which indicates per dollar profit that the

company earns on total assets. This ratio is seen as important profitability ratio, which

indicates per unit profit dollar that organisation earns on assets. Most importantly, banks are

highly leveraged then low ROA of 1 to 2 percent will indicate substantial revenues and

profits (APS bank, 2018). Bank of Valletta generates 8 percent in 2017 and in 2018; it

generates 3 percent of net profits. On the other hand, APS generates 1 percent of return in

2017 and it has 1 percent in 2018.

years 2017 and 2018. On the other hand, Bank of Valletta earns 5 percent in 2017 and 12

percent in 2018.

Return on total assets

2018 2017

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

3%

8%

1% 1%

Bank of Valletta

APS

This ratio depicts profitability of the company, which indicates per dollar profit that the

company earns on total assets. This ratio is seen as important profitability ratio, which

indicates per unit profit dollar that organisation earns on assets. Most importantly, banks are

highly leveraged then low ROA of 1 to 2 percent will indicate substantial revenues and

profits (APS bank, 2018). Bank of Valletta generates 8 percent in 2017 and in 2018; it

generates 3 percent of net profits. On the other hand, APS generates 1 percent of return in

2017 and it has 1 percent in 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

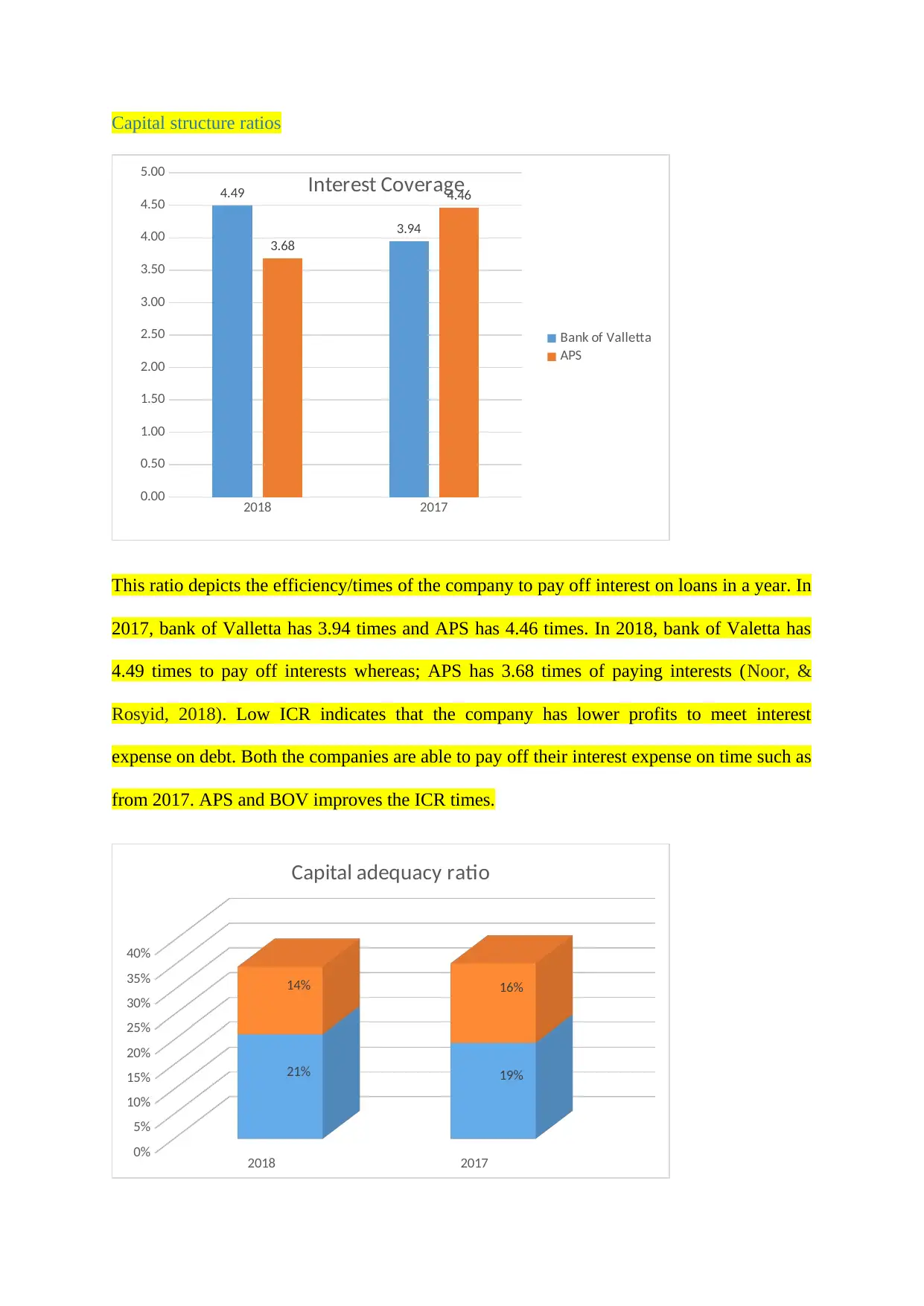

Capital structure ratios

2018 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

4.49

3.94

3.68

4.46

Interest Coverage

Bank of Valletta

APS

This ratio depicts the efficiency/times of the company to pay off interest on loans in a year. In

2017, bank of Valletta has 3.94 times and APS has 4.46 times. In 2018, bank of Valetta has

4.49 times to pay off interests whereas; APS has 3.68 times of paying interests (Noor, &

Rosyid, 2018). Low ICR indicates that the company has lower profits to meet interest

expense on debt. Both the companies are able to pay off their interest expense on time such as

from 2017. APS and BOV improves the ICR times.

2018 2017

0%

5%

10%

15%

20%

25%

30%

35%

40%

21% 19%

14% 16%

Capital adequacy ratio

2018 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

4.49

3.94

3.68

4.46

Interest Coverage

Bank of Valletta

APS

This ratio depicts the efficiency/times of the company to pay off interest on loans in a year. In

2017, bank of Valletta has 3.94 times and APS has 4.46 times. In 2018, bank of Valetta has

4.49 times to pay off interests whereas; APS has 3.68 times of paying interests (Noor, &

Rosyid, 2018). Low ICR indicates that the company has lower profits to meet interest

expense on debt. Both the companies are able to pay off their interest expense on time such as

from 2017. APS and BOV improves the ICR times.

2018 2017

0%

5%

10%

15%

20%

25%

30%

35%

40%

21% 19%

14% 16%

Capital adequacy ratio

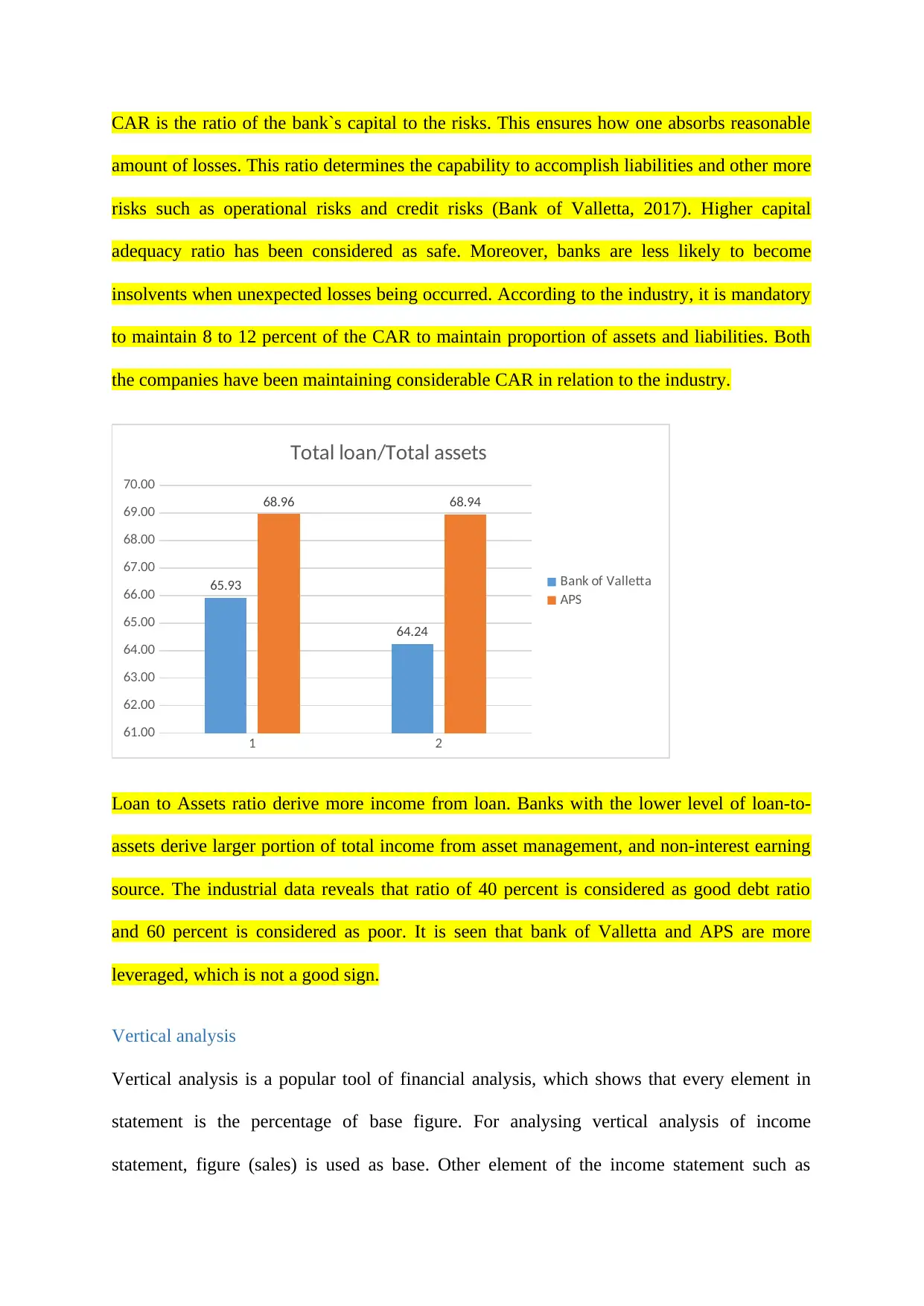

CAR is the ratio of the bank`s capital to the risks. This ensures how one absorbs reasonable

amount of losses. This ratio determines the capability to accomplish liabilities and other more

risks such as operational risks and credit risks (Bank of Valletta, 2017). Higher capital

adequacy ratio has been considered as safe. Moreover, banks are less likely to become

insolvents when unexpected losses being occurred. According to the industry, it is mandatory

to maintain 8 to 12 percent of the CAR to maintain proportion of assets and liabilities. Both

the companies have been maintaining considerable CAR in relation to the industry.

1 2

61.00

62.00

63.00

64.00

65.00

66.00

67.00

68.00

69.00

70.00

65.93

64.24

68.96 68.94

Total loan/Total assets

Bank of Valletta

APS

Loan to Assets ratio derive more income from loan. Banks with the lower level of loan-to-

assets derive larger portion of total income from asset management, and non-interest earning

source. The industrial data reveals that ratio of 40 percent is considered as good debt ratio

and 60 percent is considered as poor. It is seen that bank of Valletta and APS are more

leveraged, which is not a good sign.

Vertical analysis

Vertical analysis is a popular tool of financial analysis, which shows that every element in

statement is the percentage of base figure. For analysing vertical analysis of income

statement, figure (sales) is used as base. Other element of the income statement such as

amount of losses. This ratio determines the capability to accomplish liabilities and other more

risks such as operational risks and credit risks (Bank of Valletta, 2017). Higher capital

adequacy ratio has been considered as safe. Moreover, banks are less likely to become

insolvents when unexpected losses being occurred. According to the industry, it is mandatory

to maintain 8 to 12 percent of the CAR to maintain proportion of assets and liabilities. Both

the companies have been maintaining considerable CAR in relation to the industry.

1 2

61.00

62.00

63.00

64.00

65.00

66.00

67.00

68.00

69.00

70.00

65.93

64.24

68.96 68.94

Total loan/Total assets

Bank of Valletta

APS

Loan to Assets ratio derive more income from loan. Banks with the lower level of loan-to-

assets derive larger portion of total income from asset management, and non-interest earning

source. The industrial data reveals that ratio of 40 percent is considered as good debt ratio

and 60 percent is considered as poor. It is seen that bank of Valletta and APS are more

leveraged, which is not a good sign.

Vertical analysis

Vertical analysis is a popular tool of financial analysis, which shows that every element in

statement is the percentage of base figure. For analysing vertical analysis of income

statement, figure (sales) is used as base. Other element of the income statement such as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

income tax, gross profit, and cost of goods sold and net income shown as percentage of sales

(Srinivasan, & Thevaranjan, 2016). To analyse the balance sheet, total asset is used as base

figure. All current assets, fixed assets and current liabilities, total liabilities, stockholder`s

equity, and long term debt are shown as percentage of total assets.

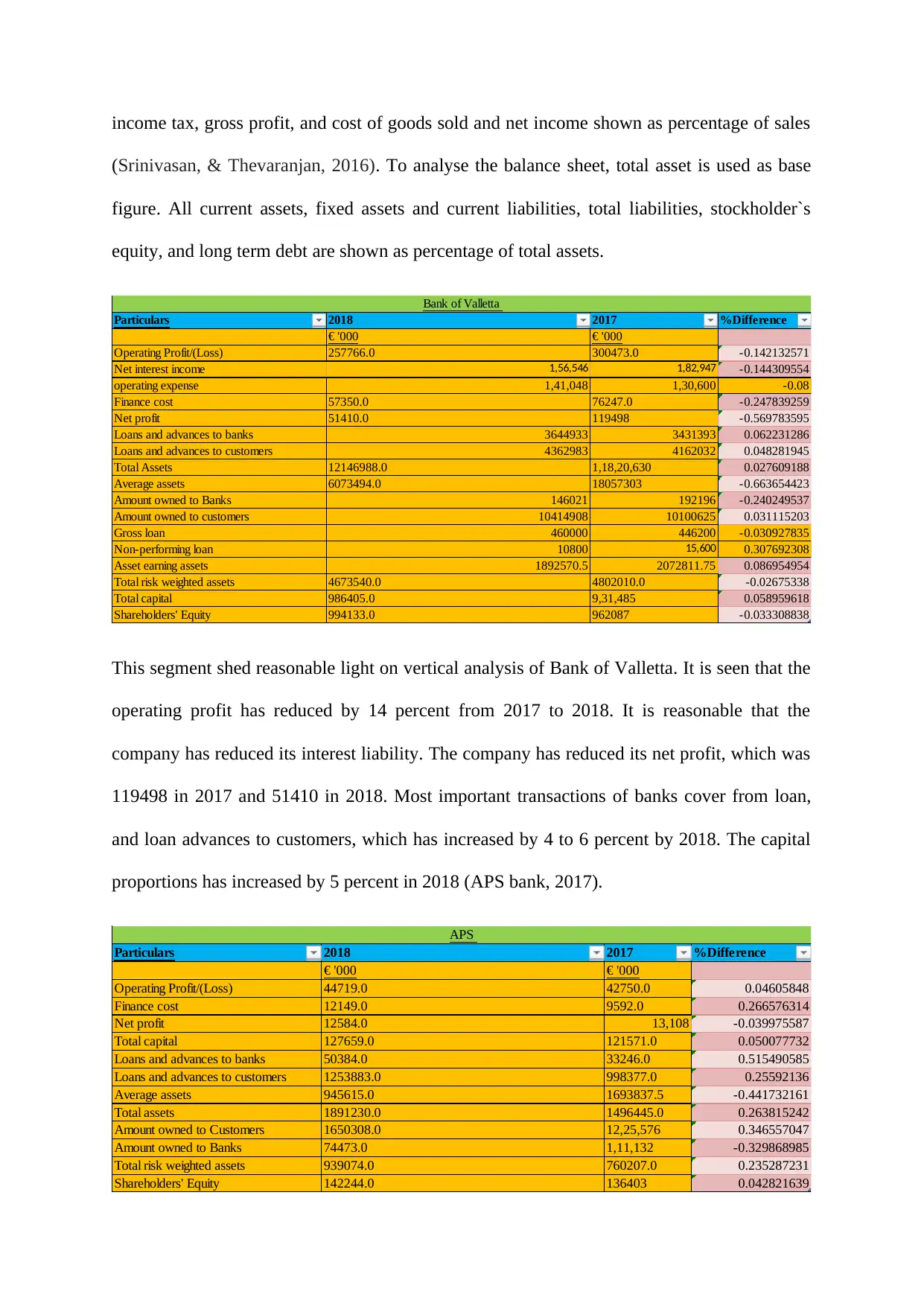

Particulars 2018 2017 %Difference

€ '000 € '000

Operating Profit/(Loss) 257766.0 300473.0 -0.142132571

Net interest income 1,56,546 1,82,947 -0.144309554

operating expense 1,41,048 1,30,600 -0.08

Finance cost 57350.0 76247.0 -0.247839259

Net profit 51410.0 119498 -0.569783595

Loans and advances to banks 3644933 3431393 0.062231286

Loans and advances to customers 4362983 4162032 0.048281945

Total Assets 12146988.0 1,18,20,630 0.027609188

Average assets 6073494.0 18057303 -0.663654423

Amount owned to Banks 146021 192196 -0.240249537

Amount owned to customers 10414908 10100625 0.031115203

Gross loan 460000 446200 -0.030927835

Non-performing loan 10800 15,600 0.307692308

Asset earning assets 1892570.5 2072811.75 0.086954954

Total risk weighted assets 4673540.0 4802010.0 -0.02675338

Total capital 986405.0 9,31,485 0.058959618

Shareholders' Equity 994133.0 962087 -0.033308838

Bank of Valletta

This segment shed reasonable light on vertical analysis of Bank of Valletta. It is seen that the

operating profit has reduced by 14 percent from 2017 to 2018. It is reasonable that the

company has reduced its interest liability. The company has reduced its net profit, which was

119498 in 2017 and 51410 in 2018. Most important transactions of banks cover from loan,

and loan advances to customers, which has increased by 4 to 6 percent by 2018. The capital

proportions has increased by 5 percent in 2018 (APS bank, 2017).

Particulars 2018 2017 %Difference

€ '000 € '000

Operating Profit/(Loss) 44719.0 42750.0 0.04605848

Finance cost 12149.0 9592.0 0.266576314

Net profit 12584.0 13,108 -0.039975587

Total capital 127659.0 121571.0 0.050077732

Loans and advances to banks 50384.0 33246.0 0.515490585

Loans and advances to customers 1253883.0 998377.0 0.25592136

Average assets 945615.0 1693837.5 -0.441732161

Total assets 1891230.0 1496445.0 0.263815242

Amount owned to Customers 1650308.0 12,25,576 0.346557047

Amount owned to Banks 74473.0 1,11,132 -0.329868985

Total risk weighted assets 939074.0 760207.0 0.235287231

Shareholders' Equity 142244.0 136403 0.042821639

APS

(Srinivasan, & Thevaranjan, 2016). To analyse the balance sheet, total asset is used as base

figure. All current assets, fixed assets and current liabilities, total liabilities, stockholder`s

equity, and long term debt are shown as percentage of total assets.

Particulars 2018 2017 %Difference

€ '000 € '000

Operating Profit/(Loss) 257766.0 300473.0 -0.142132571

Net interest income 1,56,546 1,82,947 -0.144309554

operating expense 1,41,048 1,30,600 -0.08

Finance cost 57350.0 76247.0 -0.247839259

Net profit 51410.0 119498 -0.569783595

Loans and advances to banks 3644933 3431393 0.062231286

Loans and advances to customers 4362983 4162032 0.048281945

Total Assets 12146988.0 1,18,20,630 0.027609188

Average assets 6073494.0 18057303 -0.663654423

Amount owned to Banks 146021 192196 -0.240249537

Amount owned to customers 10414908 10100625 0.031115203

Gross loan 460000 446200 -0.030927835

Non-performing loan 10800 15,600 0.307692308

Asset earning assets 1892570.5 2072811.75 0.086954954

Total risk weighted assets 4673540.0 4802010.0 -0.02675338

Total capital 986405.0 9,31,485 0.058959618

Shareholders' Equity 994133.0 962087 -0.033308838

Bank of Valletta

This segment shed reasonable light on vertical analysis of Bank of Valletta. It is seen that the

operating profit has reduced by 14 percent from 2017 to 2018. It is reasonable that the

company has reduced its interest liability. The company has reduced its net profit, which was

119498 in 2017 and 51410 in 2018. Most important transactions of banks cover from loan,

and loan advances to customers, which has increased by 4 to 6 percent by 2018. The capital

proportions has increased by 5 percent in 2018 (APS bank, 2017).

Particulars 2018 2017 %Difference

€ '000 € '000

Operating Profit/(Loss) 44719.0 42750.0 0.04605848

Finance cost 12149.0 9592.0 0.266576314

Net profit 12584.0 13,108 -0.039975587

Total capital 127659.0 121571.0 0.050077732

Loans and advances to banks 50384.0 33246.0 0.515490585

Loans and advances to customers 1253883.0 998377.0 0.25592136

Average assets 945615.0 1693837.5 -0.441732161

Total assets 1891230.0 1496445.0 0.263815242

Amount owned to Customers 1650308.0 12,25,576 0.346557047

Amount owned to Banks 74473.0 1,11,132 -0.329868985

Total risk weighted assets 939074.0 760207.0 0.235287231

Shareholders' Equity 142244.0 136403 0.042821639

APS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating profit has increased by 4 percent in 2018. Finance cost has increased by 26 percent

in 2018. Total capital has increased by 5 percent in 2018. The important element and

transaction include loans and advances to banks and customers by 51 percent and 25 percent.

Total asset has increased by 26 percent in 2018. Net profit has been decreased by 3 percent

by 2018. Total risk weighted assets has increased by 26 percent in 2018 (Srinivasan, &

Thevaranjan, 2016).

Market performance and KPIs

KPIs

Customer retention

Certain KPIs listed for the banking industry include asset quality, customer penetration,

assets under management, and customer retention. Bank of Valletta pertains to perform the

esteemed customers coming over the last few months by updating the documentation by

ensuring all customer data is complete and up to date (Blanchard et al., 2018). Bank has been

requesting the customer for kind cooperation in respect to deadlines and provisions of

complete data, which they have received from banks. Bank will understand certain

inconvenience and striving in making the procedure simple and concise (APS bank, 2017).

As far as employee retention is concerned, APS has been working on small scale while

comparing it to the bank of Valletta.

in 2018. Total capital has increased by 5 percent in 2018. The important element and

transaction include loans and advances to banks and customers by 51 percent and 25 percent.

Total asset has increased by 26 percent in 2018. Net profit has been decreased by 3 percent

by 2018. Total risk weighted assets has increased by 26 percent in 2018 (Srinivasan, &

Thevaranjan, 2016).

Market performance and KPIs

KPIs

Customer retention

Certain KPIs listed for the banking industry include asset quality, customer penetration,

assets under management, and customer retention. Bank of Valletta pertains to perform the

esteemed customers coming over the last few months by updating the documentation by

ensuring all customer data is complete and up to date (Blanchard et al., 2018). Bank has been

requesting the customer for kind cooperation in respect to deadlines and provisions of

complete data, which they have received from banks. Bank will understand certain

inconvenience and striving in making the procedure simple and concise (APS bank, 2017).

As far as employee retention is concerned, APS has been working on small scale while

comparing it to the bank of Valletta.

With total of employee count, it is seen that employees have decreased by 0.8 percent.

Further, in the first year, it has increased by 6.9 percent and then it has increased 16.9 percent

in last two years. Opening of new branch of APS is marked new standard in local retail

banking. Branch has traditional retail point, which connects with customers. New

technologies include “bricks and mortar” is under the pressure from the digital technologies.

Real estate has been expensive with cost of technology, which has been decreasing. Rate of

adoption and new technologies by the customers leading the banks to look at tow

segmentation strategies. Convention branch remain vital for the business in helping customer

retention.

Customer penetration

The bank is able to attract shareholders, which has approached 1 billion Euros in 2017. While

handling and delegating BOV complaints, it is seen that bank strives to create long-term

relationship with customers by supporting and feeling special. Banks avail professional,

caring and customer experience. Complimenting customers and encouraging for being honest

and genuine and submitting their documents on time.

Market performance

Bank of Valletta has been providing financial, investment and banking services in Malta.

Currently, the company has been trading 59.4 percent below fair value. The earnings have

been growing by 25.1 percent for the last few years (Aidoo, & Mensah, 2018). Bank of

Valletta has forecasted annual growth of 7.6 percent in 1 to 3 years where projection is based

on consensus estimations of professional analysts helping the investors to understand the

organisational ability to generate profits. There have been criteria for risk checks-

Further, in the first year, it has increased by 6.9 percent and then it has increased 16.9 percent

in last two years. Opening of new branch of APS is marked new standard in local retail

banking. Branch has traditional retail point, which connects with customers. New

technologies include “bricks and mortar” is under the pressure from the digital technologies.

Real estate has been expensive with cost of technology, which has been decreasing. Rate of

adoption and new technologies by the customers leading the banks to look at tow

segmentation strategies. Convention branch remain vital for the business in helping customer

retention.

Customer penetration

The bank is able to attract shareholders, which has approached 1 billion Euros in 2017. While

handling and delegating BOV complaints, it is seen that bank strives to create long-term

relationship with customers by supporting and feeling special. Banks avail professional,

caring and customer experience. Complimenting customers and encouraging for being honest

and genuine and submitting their documents on time.

Market performance

Bank of Valletta has been providing financial, investment and banking services in Malta.

Currently, the company has been trading 59.4 percent below fair value. The earnings have

been growing by 25.1 percent for the last few years (Aidoo, & Mensah, 2018). Bank of

Valletta has forecasted annual growth of 7.6 percent in 1 to 3 years where projection is based

on consensus estimations of professional analysts helping the investors to understand the

organisational ability to generate profits. There have been criteria for risk checks-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.