Project Report: Strategic Financial Management Analysis

VerifiedAdded on 2020/04/21

|51

|9741

|218

Project

AI Summary

This project report delves into strategic financial management, examining critical aspects such as cost accounting, financial statement analysis, and investment appraisal. The report begins by outlining the tools and techniques of cost accounting, including its concepts, features, and importance, as well as the design and system of costing. It then moves on to analyze financial performance through financial statement analysis, evaluating statements and offering recommendations. The budgetary process of an organization is also explored, including the evaluation of budgetary targets and the development of a master budget. Further, the report discusses long-term and short-term funding sources, investment appraisal methods, and strategic investment decisions. The analysis incorporates financial ratios and comparative studies of companies like Ford Motors to assess performance and make recommendations for improvement. The report concludes with a detailed examination of the strategic investment decisions and the importance of financial information in shaping future strategies.

Running Head: Strategic Financial Management

Project Report: Strategic Financial Management

1

Project Report: Strategic Financial Management

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Financial Management

Contents

Tools and techniques of cost accounting..........................................................................4

Concepts, features and importance of cost accounting.................................................4

Tools of costing design and system..............................................................................5

Recommendation..........................................................................................................6

Analysis of the financial performance..............................................................................8

Financial statement analysis.........................................................................................8

Financial statement evaluation...................................................................................11

Recommendation........................................................................................................15

Budgetary process of organization.................................................................................16

Evaluation of budgetary targets..................................................................................16

Development of master budget...................................................................................17

Evaluation of the budget and its process....................................................................18

Long term and short term sources..................................................................................21

Need for short term working capital and long term funds..........................................21

Appropriate source of short term funds......................................................................21

Choice of sources........................................................................................................22

Investment appraisal.......................................................................................................25

Financial appraisal methods.......................................................................................25

Strategic investment decision.....................................................................................27

Analysis over strategic investment decisions.............................................................30

References.......................................................................................................................32

Appendix.........................................................................................................................35

2

Contents

Tools and techniques of cost accounting..........................................................................4

Concepts, features and importance of cost accounting.................................................4

Tools of costing design and system..............................................................................5

Recommendation..........................................................................................................6

Analysis of the financial performance..............................................................................8

Financial statement analysis.........................................................................................8

Financial statement evaluation...................................................................................11

Recommendation........................................................................................................15

Budgetary process of organization.................................................................................16

Evaluation of budgetary targets..................................................................................16

Development of master budget...................................................................................17

Evaluation of the budget and its process....................................................................18

Long term and short term sources..................................................................................21

Need for short term working capital and long term funds..........................................21

Appropriate source of short term funds......................................................................21

Choice of sources........................................................................................................22

Investment appraisal.......................................................................................................25

Financial appraisal methods.......................................................................................25

Strategic investment decision.....................................................................................27

Analysis over strategic investment decisions.............................................................30

References.......................................................................................................................32

Appendix.........................................................................................................................35

2

Strategic Financial Management

3

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Financial Management

Que 1)

Tools and techniques of cost accounting:

1.1)

Concepts, features and importance of cost accounting:

Cost accounting is the concept of accounting which assists the manufacturing

companies to identify the total cost of the company to make various decisions about the

production, sales etc of the company. It helps the company to analyze various new strategies

for the betterment of the company and for managing the entire activities of the company. Cost

accounting is a process of classifying, recording, analyzing, allocating and evaluating various

alternative actions to control and evaluate the total cost of the company1.

The main purpose of cost accounting is to offer information for various decisions

making in a good manner. Cost accounting assist the company to analyze all the information

related to the total cost of the company and it evaluates the information and presents them in

an understandable state so that a better decision could be done2. Cost accounting uses the

internal as well as external sources to manage and maintain the business in a proper manner.

Cost accounting evaluates the internal operations and the activities of the company in order to

enhance the overall performance and the business management of the company.

Cost accounting is important for every business to manage the cost and activities of

the company. The main importance of the cost accounting is its capability to put a light over

the entire profitability position and the performance of the company. It depict about the

financial position and workings of the business. Cost accounting permits the manager to

manage the cash flows of the company. it also assist the manager to identify that whether the

1 Don, Hansen, Mowen Maryanne, and Guan Liming. Cost management: accounting and

control. Cengage Learning, 2007.

2 Richard Lambert, Leuz Christian, and Verrecchia Robert E. "Accounting information,

disclosure, and the cost of capital." Journal of accounting research 45.2 (2007): 385-420.

4

Que 1)

Tools and techniques of cost accounting:

1.1)

Concepts, features and importance of cost accounting:

Cost accounting is the concept of accounting which assists the manufacturing

companies to identify the total cost of the company to make various decisions about the

production, sales etc of the company. It helps the company to analyze various new strategies

for the betterment of the company and for managing the entire activities of the company. Cost

accounting is a process of classifying, recording, analyzing, allocating and evaluating various

alternative actions to control and evaluate the total cost of the company1.

The main purpose of cost accounting is to offer information for various decisions

making in a good manner. Cost accounting assist the company to analyze all the information

related to the total cost of the company and it evaluates the information and presents them in

an understandable state so that a better decision could be done2. Cost accounting uses the

internal as well as external sources to manage and maintain the business in a proper manner.

Cost accounting evaluates the internal operations and the activities of the company in order to

enhance the overall performance and the business management of the company.

Cost accounting is important for every business to manage the cost and activities of

the company. The main importance of the cost accounting is its capability to put a light over

the entire profitability position and the performance of the company. It depict about the

financial position and workings of the business. Cost accounting permits the manager to

manage the cash flows of the company. it also assist the manager to identify that whether the

1 Don, Hansen, Mowen Maryanne, and Guan Liming. Cost management: accounting and

control. Cengage Learning, 2007.

2 Richard Lambert, Leuz Christian, and Verrecchia Robert E. "Accounting information,

disclosure, and the cost of capital." Journal of accounting research 45.2 (2007): 385-420.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Financial Management

company is making profits or not, whether the organization need some tighten system and

some priorities must be reassessed according to the current performance and the position.

Thus according to the above evaluation, it has been found that the cost accounting is

very significant for the organization.

1.2)

Tools of costing design and system:

Costing design and system of an organization depicts that an organization is always

required to look over various factors and aspects while taking a decision about the costing

design system. The costing design system is a tool which helps the organization to make the

costing reports in order to make better decisions about the performance and the position of

the company3.

A cost design system helps the manager of the company to collect the information and

arrange them in such a manner that the good decision could be taken from the company and

the manufacturing process of the company could also be managed. Overhead or indirect cost

is calculated through it which assists the company to make various new decisions. The tools

of costing design system are as follows:

a. external cost design system control

b. internal cost design system control

External cost design system control:

External cost design control system applied for analyzing the performance and the

position of the company4. These standards are used by the companies to shape the firm in a

proper way and the cost ratios are also calculated through it. Ratio analysis and the

3 Arik Azoulay, et al. "The use of the transition cost accounting system in health services

research." Cost Effectiveness and Resource Allocation 5.1 (2007): 11.

4 Charles T. Horngren, Cost accounting: A managerial emphasis, 13/e. Pearson Education

India, 2009.

5

company is making profits or not, whether the organization need some tighten system and

some priorities must be reassessed according to the current performance and the position.

Thus according to the above evaluation, it has been found that the cost accounting is

very significant for the organization.

1.2)

Tools of costing design and system:

Costing design and system of an organization depicts that an organization is always

required to look over various factors and aspects while taking a decision about the costing

design system. The costing design system is a tool which helps the organization to make the

costing reports in order to make better decisions about the performance and the position of

the company3.

A cost design system helps the manager of the company to collect the information and

arrange them in such a manner that the good decision could be taken from the company and

the manufacturing process of the company could also be managed. Overhead or indirect cost

is calculated through it which assists the company to make various new decisions. The tools

of costing design system are as follows:

a. external cost design system control

b. internal cost design system control

External cost design system control:

External cost design control system applied for analyzing the performance and the

position of the company4. These standards are used by the companies to shape the firm in a

proper way and the cost ratios are also calculated through it. Ratio analysis and the

3 Arik Azoulay, et al. "The use of the transition cost accounting system in health services

research." Cost Effectiveness and Resource Allocation 5.1 (2007): 11.

4 Charles T. Horngren, Cost accounting: A managerial emphasis, 13/e. Pearson Education

India, 2009.

5

Strategic Financial Management

controlling power of the government and the stakeholders are the external cost design system

which is managed by the companies through external sources to analyze and evaluate the

position of the company as well as it also helps the company to make various better and new

decisions about the position and the performance of the company.

Internal cost design system control:

Internal cost design control system applied for analyzing the performance and the

position of the company through internal factors. These standards are used by the companies

to shape the firm in a proper way and the cost ratios are also calculated through it5.

Budgeting, capital budget, revenue budget, standard costing and variance analysis are the

internal cost design system which is managed by the companies through internal sources to

analyze and evaluate the position of the company as well as it also helps the company to

make various better and new decisions about the position and the performance of the

company.

1.3)

Recommendation:

Lastly, the study has been performed over the costing and pricing system of the

comapny to analyze the best policies and strategies for improving the position of the pricing

system and costing system of the company. An organization is always suggested to look over

various factors and aspects while making a decision about the costing system and the pricing

policies of the company.

Costing and pricing decision of the organization could be taken through analyzing all

the internal and external cost factors of the company. These would help the comapny to make

a better decision about reducing the level of the cost and enhancing the level of the price. The

internal aspect which must be considered by the comapny while making a decision about the

costing and pricing is capital budgeting, budget evaluation, variance analysis and standard

costing whereas the external costing system are the cost ratios6. All of these technologies and

5 Glen, Arnold. Corporate financial management. Pearson Education, 2008.

6 Horne Van, James and Wachowicz John Martin. Fundamentals of financial management.

Pearson Education, 2008.

6

controlling power of the government and the stakeholders are the external cost design system

which is managed by the companies through external sources to analyze and evaluate the

position of the company as well as it also helps the company to make various better and new

decisions about the position and the performance of the company.

Internal cost design system control:

Internal cost design control system applied for analyzing the performance and the

position of the company through internal factors. These standards are used by the companies

to shape the firm in a proper way and the cost ratios are also calculated through it5.

Budgeting, capital budget, revenue budget, standard costing and variance analysis are the

internal cost design system which is managed by the companies through internal sources to

analyze and evaluate the position of the company as well as it also helps the company to

make various better and new decisions about the position and the performance of the

company.

1.3)

Recommendation:

Lastly, the study has been performed over the costing and pricing system of the

comapny to analyze the best policies and strategies for improving the position of the pricing

system and costing system of the company. An organization is always suggested to look over

various factors and aspects while making a decision about the costing system and the pricing

policies of the company.

Costing and pricing decision of the organization could be taken through analyzing all

the internal and external cost factors of the company. These would help the comapny to make

a better decision about reducing the level of the cost and enhancing the level of the price. The

internal aspect which must be considered by the comapny while making a decision about the

costing and pricing is capital budgeting, budget evaluation, variance analysis and standard

costing whereas the external costing system are the cost ratios6. All of these technologies and

5 Glen, Arnold. Corporate financial management. Pearson Education, 2008.

6 Horne Van, James and Wachowicz John Martin. Fundamentals of financial management.

Pearson Education, 2008.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Financial Management

the aspect are the method to evaluate the total cost of the comapny and predict the future on

the basis of financial information so that a better policy and strategy could be made by the

company for managing the cost and pricing of the company.

7

the aspect are the method to evaluate the total cost of the comapny and predict the future on

the basis of financial information so that a better policy and strategy could be made by the

company for managing the cost and pricing of the company.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Financial Management

Que 2)

Analysis of the financial performance:

2.1)

Financial statement analysis:

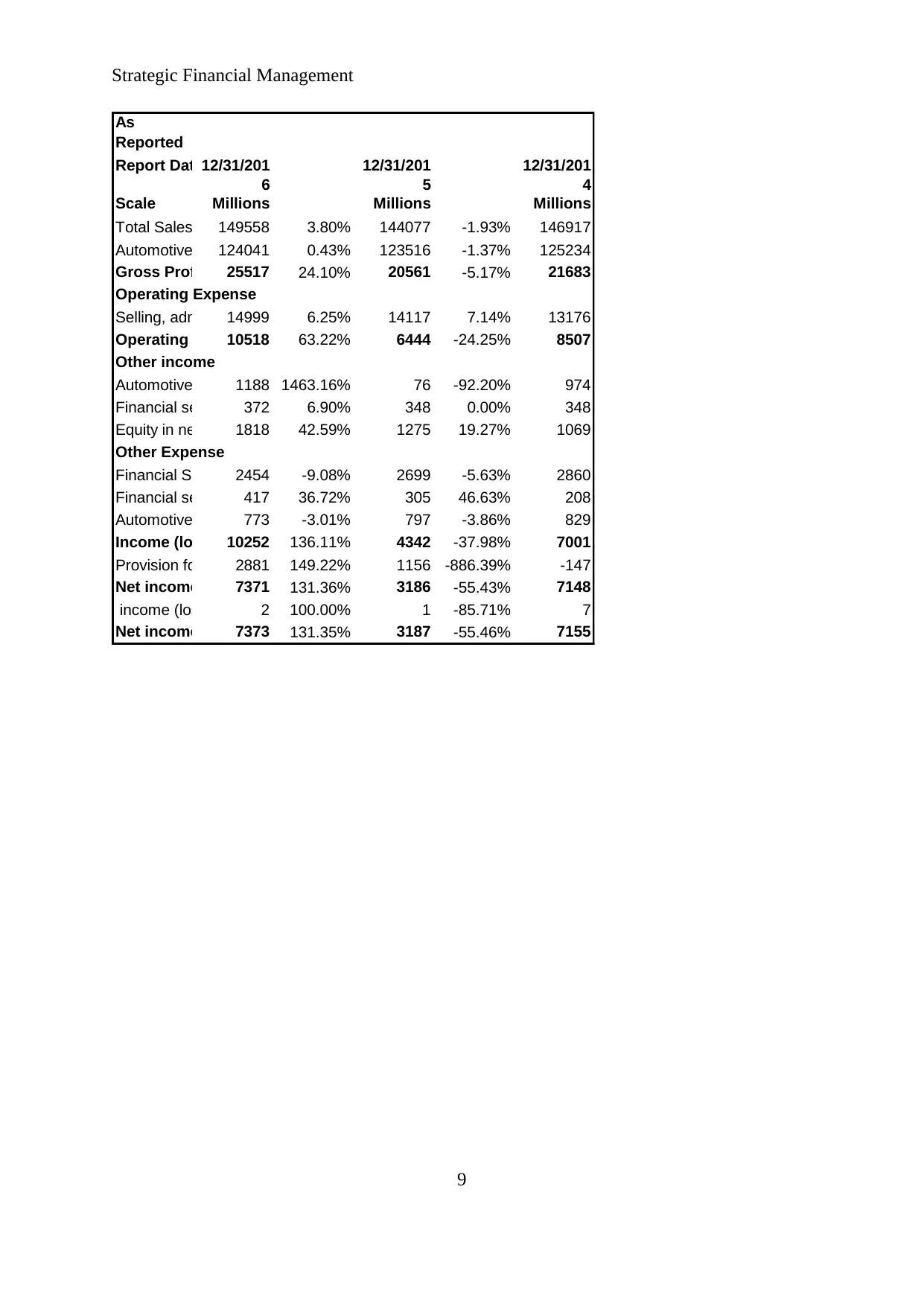

Financial statement analysis is the accounting method which is used by the companies

to analyze the financial position of the company. The financial position of the company is

analyzed on various bases. Mainly, the analyst and the financial manager of a company

analyze the financial position and the performance of the company through analyzing the

financial statement of a company7. For this analysis, ford motors have been analyzed and the

study has been done over the financial statement of ford motors.

The financial statement of Ford Motors could be analyzed by the financial analyst and

financial manager of a company on various bases such as through analyzing the last 3 year

statement, through analyzing some key financial figures from the financial statement of the

company, by conducting the study of the trend analysis of the company, by analyzing the

study of horizontal analysis of the company and by conducting the study of ratio analysis

over the company and through comparing these figures from the financial statement8. The

analysis study over the financial statement of ford motors is as follows:

7 Robert Higgins, Analysis for financial management. McGraw-Hill/Irwin, 2012.

8 Alan Shapiro, Multinational financial management. John Wiley & Sons, 2008.

8

Que 2)

Analysis of the financial performance:

2.1)

Financial statement analysis:

Financial statement analysis is the accounting method which is used by the companies

to analyze the financial position of the company. The financial position of the company is

analyzed on various bases. Mainly, the analyst and the financial manager of a company

analyze the financial position and the performance of the company through analyzing the

financial statement of a company7. For this analysis, ford motors have been analyzed and the

study has been done over the financial statement of ford motors.

The financial statement of Ford Motors could be analyzed by the financial analyst and

financial manager of a company on various bases such as through analyzing the last 3 year

statement, through analyzing some key financial figures from the financial statement of the

company, by conducting the study of the trend analysis of the company, by analyzing the

study of horizontal analysis of the company and by conducting the study of ratio analysis

over the company and through comparing these figures from the financial statement8. The

analysis study over the financial statement of ford motors is as follows:

7 Robert Higgins, Analysis for financial management. McGraw-Hill/Irwin, 2012.

8 Alan Shapiro, Multinational financial management. John Wiley & Sons, 2008.

8

Strategic Financial Management

As

Reported

AnnualReport Date12/31/201

6

12/31/201

5

12/31/201

4

Scale Millions Millions Millions

Total Sales revenues149558 3.80% 144077 -1.93% 146917

Automotive cost of sales124041 0.43% 123516 -1.37% 125234

Gross Profit 25517 24.10% 20561 -5.17% 21683

Operating Expense

Selling, administrative & other expenses14999 6.25% 14117 7.14% 13176

Operating Income10518 63.22% 6444 -24.25% 8507

Other income

Automotive interest income & other income net1188 1463.16% 76 -92.20% 974

Financial services other income, net372 6.90% 348 0.00% 348

Equity in net income of affiliated companies1818 42.59% 1275 19.27% 1069

Other Expense

Financial Services interest expense2454 -9.08% 2699 -5.63% 2860

Financial services provision for credit & insurance losses417 36.72% 305 46.63% 208

Automotive interest expense773 -3.01% 797 -3.86% 829

Income (loss) before income taxes10252 136.11% 4342 -37.98% 7001

Provision for (benefit from) income taxes2881 149.22% 1156 -886.39% -147

Net income 7371 131.36% 3186 -55.43% 7148

income (loss) attributable to noncontrolling interests2 100.00% 1 -85.71% 7

Net income (loss) attributable to Ford Motor Company7373 131.35% 3187 -55.46% 7155

9

As

Reported

AnnualReport Date12/31/201

6

12/31/201

5

12/31/201

4

Scale Millions Millions Millions

Total Sales revenues149558 3.80% 144077 -1.93% 146917

Automotive cost of sales124041 0.43% 123516 -1.37% 125234

Gross Profit 25517 24.10% 20561 -5.17% 21683

Operating Expense

Selling, administrative & other expenses14999 6.25% 14117 7.14% 13176

Operating Income10518 63.22% 6444 -24.25% 8507

Other income

Automotive interest income & other income net1188 1463.16% 76 -92.20% 974

Financial services other income, net372 6.90% 348 0.00% 348

Equity in net income of affiliated companies1818 42.59% 1275 19.27% 1069

Other Expense

Financial Services interest expense2454 -9.08% 2699 -5.63% 2860

Financial services provision for credit & insurance losses417 36.72% 305 46.63% 208

Automotive interest expense773 -3.01% 797 -3.86% 829

Income (loss) before income taxes10252 136.11% 4342 -37.98% 7001

Provision for (benefit from) income taxes2881 149.22% 1156 -886.39% -147

Net income 7371 131.36% 3186 -55.43% 7148

income (loss) attributable to noncontrolling interests2 100.00% 1 -85.71% 7

Net income (loss) attributable to Ford Motor Company7373 131.35% 3187 -55.46% 7155

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Financial Management

As

Reported

AnnualReport Date12/31/201

6

12/31/201

5

12/31/201

4

Scale Millions Millions Millions

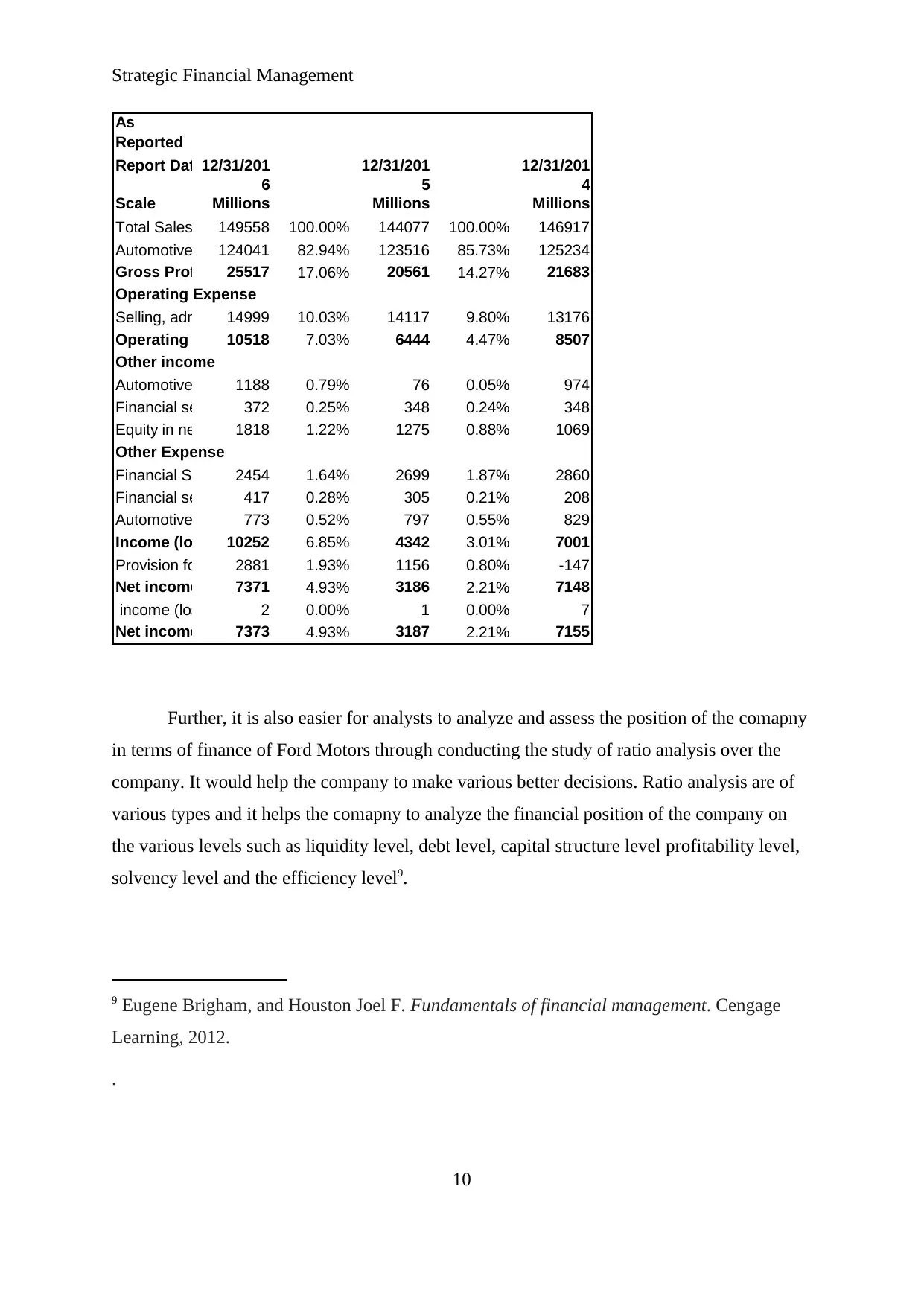

Total Sales revenues149558 100.00% 144077 100.00% 146917

Automotive cost of sales124041 82.94% 123516 85.73% 125234

Gross Profit 25517 17.06% 20561 14.27% 21683

Operating Expense

Selling, administrative & other expenses14999 10.03% 14117 9.80% 13176

Operating Income10518 7.03% 6444 4.47% 8507

Other income

Automotive interest income & other income net1188 0.79% 76 0.05% 974

Financial services other income, net372 0.25% 348 0.24% 348

Equity in net income of affiliated companies1818 1.22% 1275 0.88% 1069

Other Expense

Financial Services interest expense2454 1.64% 2699 1.87% 2860

Financial services provision for credit & insurance losses417 0.28% 305 0.21% 208

Automotive interest expense773 0.52% 797 0.55% 829

Income (loss) before income taxes10252 6.85% 4342 3.01% 7001

Provision for (benefit from) income taxes2881 1.93% 1156 0.80% -147

Net income 7371 4.93% 3186 2.21% 7148

income (loss) attributable to noncontrolling interests2 0.00% 1 0.00% 7

Net income (loss) attributable to Ford Motor Company7373 4.93% 3187 2.21% 7155

Further, it is also easier for analysts to analyze and assess the position of the comapny

in terms of finance of Ford Motors through conducting the study of ratio analysis over the

company. It would help the company to make various better decisions. Ratio analysis are of

various types and it helps the comapny to analyze the financial position of the company on

the various levels such as liquidity level, debt level, capital structure level profitability level,

solvency level and the efficiency level9.

9 Eugene Brigham, and Houston Joel F. Fundamentals of financial management. Cengage

Learning, 2012.

.

10

As

Reported

AnnualReport Date12/31/201

6

12/31/201

5

12/31/201

4

Scale Millions Millions Millions

Total Sales revenues149558 100.00% 144077 100.00% 146917

Automotive cost of sales124041 82.94% 123516 85.73% 125234

Gross Profit 25517 17.06% 20561 14.27% 21683

Operating Expense

Selling, administrative & other expenses14999 10.03% 14117 9.80% 13176

Operating Income10518 7.03% 6444 4.47% 8507

Other income

Automotive interest income & other income net1188 0.79% 76 0.05% 974

Financial services other income, net372 0.25% 348 0.24% 348

Equity in net income of affiliated companies1818 1.22% 1275 0.88% 1069

Other Expense

Financial Services interest expense2454 1.64% 2699 1.87% 2860

Financial services provision for credit & insurance losses417 0.28% 305 0.21% 208

Automotive interest expense773 0.52% 797 0.55% 829

Income (loss) before income taxes10252 6.85% 4342 3.01% 7001

Provision for (benefit from) income taxes2881 1.93% 1156 0.80% -147

Net income 7371 4.93% 3186 2.21% 7148

income (loss) attributable to noncontrolling interests2 0.00% 1 0.00% 7

Net income (loss) attributable to Ford Motor Company7373 4.93% 3187 2.21% 7155

Further, it is also easier for analysts to analyze and assess the position of the comapny

in terms of finance of Ford Motors through conducting the study of ratio analysis over the

company. It would help the company to make various better decisions. Ratio analysis are of

various types and it helps the comapny to analyze the financial position of the company on

the various levels such as liquidity level, debt level, capital structure level profitability level,

solvency level and the efficiency level9.

9 Eugene Brigham, and Houston Joel F. Fundamentals of financial management. Cengage

Learning, 2012.

.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Financial Management

Thus it is easy for the company to analyze and investigate the financial statement of

the company through conducting the horizontal analysis, vertical analysis, analysis over the

key financial terms, ratio analysis etc.

2.2)

Financial statement evaluation:

Financial statement evaluation is crucial or every organization to identify and analyze

the position as well as analyzing the performance of the company in a specific year. For

instance, it is easier for analysts to analyze and assess the position of the finance of a

company through conducting the study of ratio analysis over the company10. It would help the

company to make various better decisions. Ratio analysis are of various types and it helps the

comapny to analyze the financial position of the company on the various levels such as

liquidity level, debt level, capital structure level profitability level, solvency level and the

efficiency level11.

Ratio analysis study depict about the profitability position which helps the comapny

to analyze that gross profit, net profit and the return on equity of the company. Further, the

liquidity position of the company is analyzing through identifying the current and quick

position of the company. More, the efficiency position of the company is analyzing through

identifying the receivable collection period, payable collection period and asset turnover ratio

position of the company12. Lastly, the solvency position of the company is analyzing through

identifying the debt equity and debt asset position of the company

10 Glen Arnold. Corporate financial management. Pearson Higher Ed, 2013.

11 Evert Wipplinger. "Philippe Jorion: Value at Risk-The New Benchmark for Managing

Financial Risk." Financial Markets and Portfolio Management 21.3 (2007): 397.

12 Söhnke M. Bartram, Brown Gregory W, and Fehle Frank R. "International evidence on

financial derivatives usage." Financial management 38.1 (2009): 185-206.

11

Thus it is easy for the company to analyze and investigate the financial statement of

the company through conducting the horizontal analysis, vertical analysis, analysis over the

key financial terms, ratio analysis etc.

2.2)

Financial statement evaluation:

Financial statement evaluation is crucial or every organization to identify and analyze

the position as well as analyzing the performance of the company in a specific year. For

instance, it is easier for analysts to analyze and assess the position of the finance of a

company through conducting the study of ratio analysis over the company10. It would help the

company to make various better decisions. Ratio analysis are of various types and it helps the

comapny to analyze the financial position of the company on the various levels such as

liquidity level, debt level, capital structure level profitability level, solvency level and the

efficiency level11.

Ratio analysis study depict about the profitability position which helps the comapny

to analyze that gross profit, net profit and the return on equity of the company. Further, the

liquidity position of the company is analyzing through identifying the current and quick

position of the company. More, the efficiency position of the company is analyzing through

identifying the receivable collection period, payable collection period and asset turnover ratio

position of the company12. Lastly, the solvency position of the company is analyzing through

identifying the debt equity and debt asset position of the company

10 Glen Arnold. Corporate financial management. Pearson Higher Ed, 2013.

11 Evert Wipplinger. "Philippe Jorion: Value at Risk-The New Benchmark for Managing

Financial Risk." Financial Markets and Portfolio Management 21.3 (2007): 397.

12 Söhnke M. Bartram, Brown Gregory W, and Fehle Frank R. "International evidence on

financial derivatives usage." Financial management 38.1 (2009): 185-206.

11

Strategic Financial Management

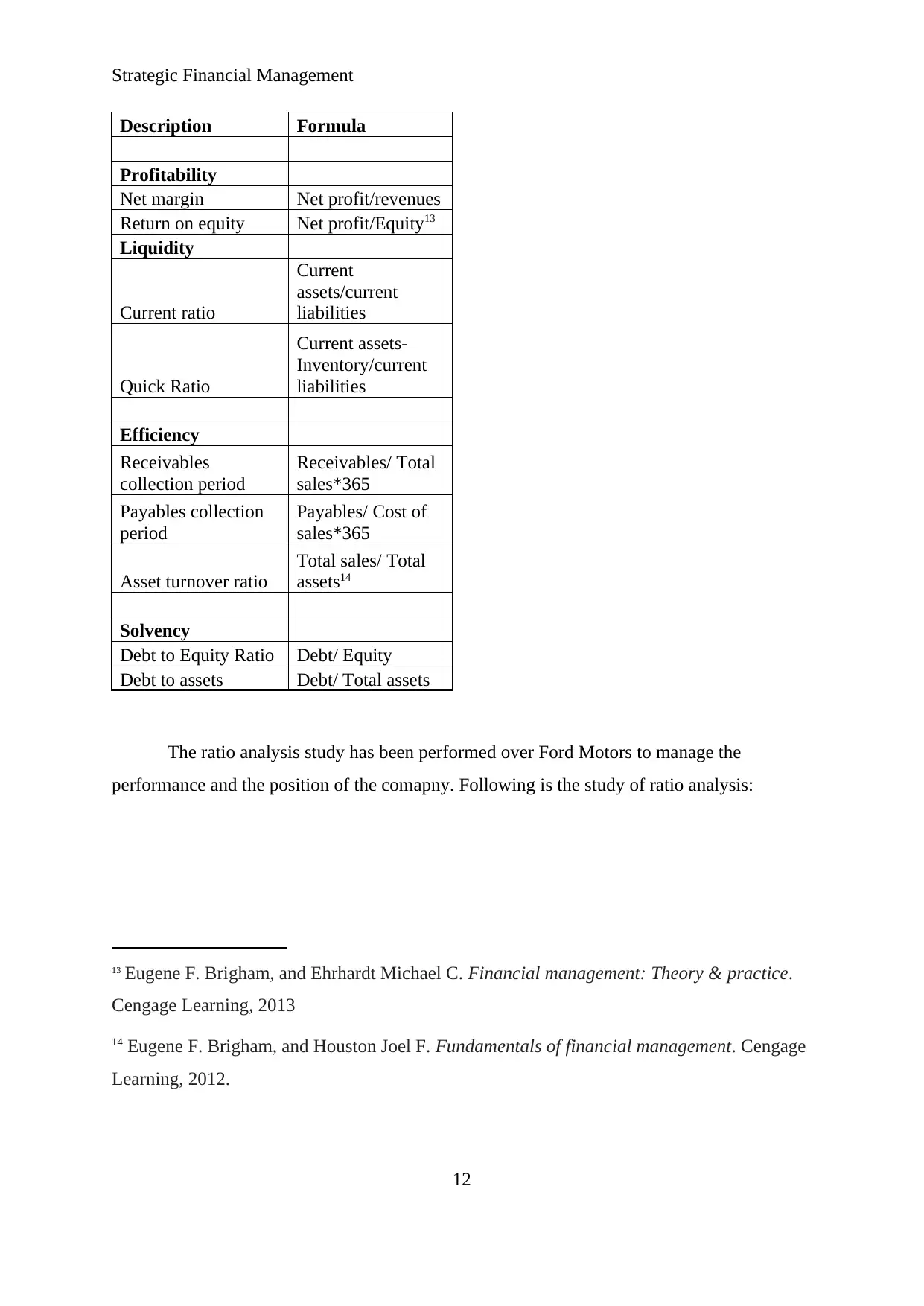

Description Formula

Profitability

Net margin Net profit/revenues

Return on equity Net profit/Equity13

Liquidity

Current ratio

Current

assets/current

liabilities

Quick Ratio

Current assets-

Inventory/current

liabilities

Efficiency

Receivables

collection period

Receivables/ Total

sales*365

Payables collection

period

Payables/ Cost of

sales*365

Asset turnover ratio

Total sales/ Total

assets14

Solvency

Debt to Equity Ratio Debt/ Equity

Debt to assets Debt/ Total assets

The ratio analysis study has been performed over Ford Motors to manage the

performance and the position of the comapny. Following is the study of ratio analysis:

13 Eugene F. Brigham, and Ehrhardt Michael C. Financial management: Theory & practice.

Cengage Learning, 2013

14 Eugene F. Brigham, and Houston Joel F. Fundamentals of financial management. Cengage

Learning, 2012.

12

Description Formula

Profitability

Net margin Net profit/revenues

Return on equity Net profit/Equity13

Liquidity

Current ratio

Current

assets/current

liabilities

Quick Ratio

Current assets-

Inventory/current

liabilities

Efficiency

Receivables

collection period

Receivables/ Total

sales*365

Payables collection

period

Payables/ Cost of

sales*365

Asset turnover ratio

Total sales/ Total

assets14

Solvency

Debt to Equity Ratio Debt/ Equity

Debt to assets Debt/ Total assets

The ratio analysis study has been performed over Ford Motors to manage the

performance and the position of the comapny. Following is the study of ratio analysis:

13 Eugene F. Brigham, and Ehrhardt Michael C. Financial management: Theory & practice.

Cengage Learning, 2013

14 Eugene F. Brigham, and Houston Joel F. Fundamentals of financial management. Cengage

Learning, 2012.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 51

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.