Strategic Financial Management: Stakeholder & Financial Analysis

VerifiedAdded on 2023/04/10

|13

|3343

|51

Report

AI Summary

This report provides an analysis of strategic financial management, focusing on Tesco plc and Benedict Corporation. Task 1 involves a stakeholder analysis of Tesco, identifying key stakeholders like customers, government, and employees, and analyzing the role of environmental and social reviews in demonstrating performance and CSR. Task 2 focuses on the financial performance of Benedict Corporation, employing ratios such as current ratio, quick ratio, receivable turnover ratio, trade payable ratio, and inventory turnover ratio to assess the company's liquidity and efficiency. The report includes calculations and explanations of the movements in these ratios between two years, providing insights into the company's financial health and areas for improvement. This document is available on Desklib, a platform offering a wealth of study resources for students.

Strategic Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

Task 1......................................................................................................................................................3

Task 2......................................................................................................................................................6

CONCLUSION........................................................................................................................................12

REFRENCES...........................................................................................................................................13

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

Task 1......................................................................................................................................................3

Task 2......................................................................................................................................................6

CONCLUSION........................................................................................................................................12

REFRENCES...........................................................................................................................................13

INTRODUCTION

The term strategic financial management can be understood as a form of study which involves

not only controlling the value of a firm, but also managing them with the aim of meeting the

aims and objectives of the organizations and price stabilization value over time (Delkhosh and

Mousavi, 2016). This is about producing market profit and achieving an adequate return on

investment (ROI). Financial control is characterized by company financial strategies, the

development of accounting policies and the making of financial decisions. The report is based on

two companies named Tesco plc and Benedict Corporation. Under the report stakeholder

analysis of Tesco plc has been done while in second part of report financial performance of

Benedict Corporation is done by help of various kinds of ratios.

MAIN BODY

Task 1

a) Explains the term ‘stakeholder’ and identifies three types of stakeholder of Tesco

Stakeholder: A stakeholder is an entity who has a stake in a corporation and may either control

the company or be influenced by it (Kumar, 2017). Its owners, personnel, clients, and vendors

are the key stakeholders of a particular company. However, the term has been expanded to cover

societies, states, and labor associations, with growing commitment to corporate social

responsibility.

Stakeholders may be intrinsic to an entity or extrinsic to it. Individuals whose participation in a

business comes from a direct interaction, such as work, ownership, or expenditure, are internal

stakeholders. External partners are people that do not deal for a firm directly but somehow are

influenced by the company's actions and performance. All external parties are known to be

vendors, creditors, and civic groups.

In accordance of annual report of Tesco plc, this can be inferred that there is both types of

stakeholders including internal and external. Tesco's key stakeholders are consumers, vendors,

creditors, opponents, parties, local governments, and the government. Tesco works with

hundreds of manufacturers and producers in order to serve consumers with high quality,

The term strategic financial management can be understood as a form of study which involves

not only controlling the value of a firm, but also managing them with the aim of meeting the

aims and objectives of the organizations and price stabilization value over time (Delkhosh and

Mousavi, 2016). This is about producing market profit and achieving an adequate return on

investment (ROI). Financial control is characterized by company financial strategies, the

development of accounting policies and the making of financial decisions. The report is based on

two companies named Tesco plc and Benedict Corporation. Under the report stakeholder

analysis of Tesco plc has been done while in second part of report financial performance of

Benedict Corporation is done by help of various kinds of ratios.

MAIN BODY

Task 1

a) Explains the term ‘stakeholder’ and identifies three types of stakeholder of Tesco

Stakeholder: A stakeholder is an entity who has a stake in a corporation and may either control

the company or be influenced by it (Kumar, 2017). Its owners, personnel, clients, and vendors

are the key stakeholders of a particular company. However, the term has been expanded to cover

societies, states, and labor associations, with growing commitment to corporate social

responsibility.

Stakeholders may be intrinsic to an entity or extrinsic to it. Individuals whose participation in a

business comes from a direct interaction, such as work, ownership, or expenditure, are internal

stakeholders. External partners are people that do not deal for a firm directly but somehow are

influenced by the company's actions and performance. All external parties are known to be

vendors, creditors, and civic groups.

In accordance of annual report of Tesco plc, this can be inferred that there is both types of

stakeholders including internal and external. Tesco's key stakeholders are consumers, vendors,

creditors, opponents, parties, local governments, and the government. Tesco works with

hundreds of manufacturers and producers in order to serve consumers with high quality,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

nutritious and organic goods. These producers and distributors not only provide Tesco with the

quality goods needed, but they also help the business minimize food waste. Below some key

stakeholders are explained which are as follows:

Customers: These are the main stakeholders of a company as they have an ability to affect their

performance. Customers are considered as external stakeholders because they do not have their

own interest in company’s policies and plans (Trinh and Thao, 2017). Though, customers can be

affected due to change in company’s strategies and plans. This is so because if a company makes

change in their prices than customers can be affected can change their purchasing habits. In the

context of Tesco company, this can be inferred that their sales in year 2016 has been dropped by

few volumes which indicates that customers might shifted their interest towards other company.

As well as Tesco might have changed their policies and plans which may lead to lower sales and

customer diversion.

Government: The government is also a main stakeholder as they can affect to company’s

performance by changing own policies and plans. It is essential for companies to follow

regulations and guidelines of government. In addition to this government collects tax from the

companies on a regular basis. The government of United Kingdom is a key stakeholder of Tesco

plc. This is so because they have ability to impact financial performance of such company. The

effect of government can be measured by help of amount of tax paid during an accounting

period. From annual report this can be stated that they have paid tax on profit after tax but in year

2016 they paid less amount of tax due to lack of income in such year.

Employee- Workers are important internal stakeholders. Employees have substantial financial

and time commitments in the company and play a specific role in the organization's policy,

tactics, and activities. These stakeholders are key person of many firms, also recognized as

lenders, and have a monetary stake in a business's performance. They offer the business

resources and the capacity to perform and even expand by their stake in the company. So, the

stake of a shareholder in a corporation is financial, but not all investors are involved. In the

context of above Tesco plc this can be inferred that there are a range of employees in their

operations and activities which play a significant role.

quality goods needed, but they also help the business minimize food waste. Below some key

stakeholders are explained which are as follows:

Customers: These are the main stakeholders of a company as they have an ability to affect their

performance. Customers are considered as external stakeholders because they do not have their

own interest in company’s policies and plans (Trinh and Thao, 2017). Though, customers can be

affected due to change in company’s strategies and plans. This is so because if a company makes

change in their prices than customers can be affected can change their purchasing habits. In the

context of Tesco company, this can be inferred that their sales in year 2016 has been dropped by

few volumes which indicates that customers might shifted their interest towards other company.

As well as Tesco might have changed their policies and plans which may lead to lower sales and

customer diversion.

Government: The government is also a main stakeholder as they can affect to company’s

performance by changing own policies and plans. It is essential for companies to follow

regulations and guidelines of government. In addition to this government collects tax from the

companies on a regular basis. The government of United Kingdom is a key stakeholder of Tesco

plc. This is so because they have ability to impact financial performance of such company. The

effect of government can be measured by help of amount of tax paid during an accounting

period. From annual report this can be stated that they have paid tax on profit after tax but in year

2016 they paid less amount of tax due to lack of income in such year.

Employee- Workers are important internal stakeholders. Employees have substantial financial

and time commitments in the company and play a specific role in the organization's policy,

tactics, and activities. These stakeholders are key person of many firms, also recognized as

lenders, and have a monetary stake in a business's performance. They offer the business

resources and the capacity to perform and even expand by their stake in the company. So, the

stake of a shareholder in a corporation is financial, but not all investors are involved. In the

context of above Tesco plc this can be inferred that there are a range of employees in their

operations and activities which play a significant role.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Analyses how the Environmental and Social Review help to demonstrate performance.

The environmental and social review plays a key role in order to evaluate performance of a

company during a particular time period. Basically, it defines different kinds of tasks and

activities to achieve compliance with implementation of proper policies and regulations

(Mitchell, 2017). In the absence of proper planning of rules and regulations of environmental

review this might become difficult for companies to stay in competition. In the context of Tesco

plc, this is essential for them to review environmental and social aspect so that they can meet

their objectives.

There are likely to be disputes and conflicts of interest if a group of individuals come together

just to work on anything. Due to potential conflicts between stakeholders of companies, the idea

of corporate governance becomes essential. There are mostly disputes between upper manager

and investors, but they may occur between several parties and citizens. Corporate governance

reports include mechanisms to ensure that businesses are dedicated to corporate governance

practices and compliance with all relevant laws and regulations for shareholders. Corporate

governance is basically a set of procedures, practices, systems and associations that are enforced

and kept to account for the purpose of managing and directing organizations. Corporate

governance requires the policies and practices that companies rely on to make good decisions in

company governance. It is a dynamic term in which the frameworks and values define the rights

and duties of the many different persons inherently involved in companies, including, though not

limited to, the roles and obligations. Procedures of governance involve processes that lead board

members to set targets and how they approach goal-setting in the light of social, legislative and

business problems and circumstances. Corporate governance reports illustrate how businesses

track the company's activities, strategies, procedures and actions, and also the effects on their

agents and decision makers of their behavior.

CSR towards customers: The definition of corporate social responsibility or CSR is composed of

three main parts which serve as its four principles (Lasserre, 2017). These are the financial,

social, and environmental obligation. For a corporation to successfully fulfill its obligations.

Social responsibility is the most recent component of CSR in which companies take an active

role in social concerns and community relations. The purpose of transparency would be to

include consumers or the purchasing public as stakeholders. The idea of providing consumers

The environmental and social review plays a key role in order to evaluate performance of a

company during a particular time period. Basically, it defines different kinds of tasks and

activities to achieve compliance with implementation of proper policies and regulations

(Mitchell, 2017). In the absence of proper planning of rules and regulations of environmental

review this might become difficult for companies to stay in competition. In the context of Tesco

plc, this is essential for them to review environmental and social aspect so that they can meet

their objectives.

There are likely to be disputes and conflicts of interest if a group of individuals come together

just to work on anything. Due to potential conflicts between stakeholders of companies, the idea

of corporate governance becomes essential. There are mostly disputes between upper manager

and investors, but they may occur between several parties and citizens. Corporate governance

reports include mechanisms to ensure that businesses are dedicated to corporate governance

practices and compliance with all relevant laws and regulations for shareholders. Corporate

governance is basically a set of procedures, practices, systems and associations that are enforced

and kept to account for the purpose of managing and directing organizations. Corporate

governance requires the policies and practices that companies rely on to make good decisions in

company governance. It is a dynamic term in which the frameworks and values define the rights

and duties of the many different persons inherently involved in companies, including, though not

limited to, the roles and obligations. Procedures of governance involve processes that lead board

members to set targets and how they approach goal-setting in the light of social, legislative and

business problems and circumstances. Corporate governance reports illustrate how businesses

track the company's activities, strategies, procedures and actions, and also the effects on their

agents and decision makers of their behavior.

CSR towards customers: The definition of corporate social responsibility or CSR is composed of

three main parts which serve as its four principles (Lasserre, 2017). These are the financial,

social, and environmental obligation. For a corporation to successfully fulfill its obligations.

Social responsibility is the most recent component of CSR in which companies take an active

role in social concerns and community relations. The purpose of transparency would be to

include consumers or the purchasing public as stakeholders. The idea of providing consumers

with respect and fulfillment is nothing new to companies, but being accountable to customers has

an effect on profitability. Customer satisfaction, simply put, is how the consumers are

appropriately handled if, for example, they have grievances and inquiries. Companies are

obligated to give such problems prompt and courteous consideration. They must uphold fair

standards of advertising and trading and not deceive customers into anything that is not true.

Companies are also responsible for supplying both current and prospective consumers with full

product, service, and business details to the purchasing public.

CSR towards employees- The firms are treated an investment by a corporation. In particular, if

we speak about skilled labor, manpower resources are not so easy to acquire (RA, 2017).

Working people often enjoy a company that is not only prosperous but also puts emphasis on its

workers. Because of the increasing liberalization and high in the world market, many businesses

work hard to improve efficiency, simplify operations, or deliver improved investor benefit. For a

company to accomplish all this, they should have skilled and competent individuals and maintain

the best workers in the sector. Companies that have practiced corporate responsibility have found

that CSR operations have been successful in rising the retention of employees. This is not only

true for working professionals, but also for workers. For most organizations, employee

engagement has become increasingly common in order to boost the end result by making people

who work socially conscious. Many effective companies owe much of their prosperity to the

creation and implementation of volunteer employee initiatives that are now used to track and

measure their effect on society.

Task 2

a) Explain the purpose and relevance of the chosen ratios.

Current Ratio:

Current ratio is a liquidity ratio that measure whether a company has ability to meet its short

term requirement. It is calculated by dividing current assets with current liability (Malyshenko,

2016). The reason to choose current ratio is that it assesses a company's short term financial

an effect on profitability. Customer satisfaction, simply put, is how the consumers are

appropriately handled if, for example, they have grievances and inquiries. Companies are

obligated to give such problems prompt and courteous consideration. They must uphold fair

standards of advertising and trading and not deceive customers into anything that is not true.

Companies are also responsible for supplying both current and prospective consumers with full

product, service, and business details to the purchasing public.

CSR towards employees- The firms are treated an investment by a corporation. In particular, if

we speak about skilled labor, manpower resources are not so easy to acquire (RA, 2017).

Working people often enjoy a company that is not only prosperous but also puts emphasis on its

workers. Because of the increasing liberalization and high in the world market, many businesses

work hard to improve efficiency, simplify operations, or deliver improved investor benefit. For a

company to accomplish all this, they should have skilled and competent individuals and maintain

the best workers in the sector. Companies that have practiced corporate responsibility have found

that CSR operations have been successful in rising the retention of employees. This is not only

true for working professionals, but also for workers. For most organizations, employee

engagement has become increasingly common in order to boost the end result by making people

who work socially conscious. Many effective companies owe much of their prosperity to the

creation and implementation of volunteer employee initiatives that are now used to track and

measure their effect on society.

Task 2

a) Explain the purpose and relevance of the chosen ratios.

Current Ratio:

Current ratio is a liquidity ratio that measure whether a company has ability to meet its short

term requirement. It is calculated by dividing current assets with current liability (Malyshenko,

2016). The reason to choose current ratio is that it assesses a company's short term financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

position. High current ratio indicate stability within company and less current ratio shows risk of

liquidity within company.

Quick Ratio:

Quick ratio is a type of liquidity ratio which is also called Acid- Test ratio. This ratio measures a

company's ability to use cash or quick assets to retire its current liability. It is calculated by

dividing quick assets with current liability. Reason to choose quick ration is that it measures

more accurately how current assets pay off current liability and it only include liquid assets

which convert in cash or is cash ready.

Receivable turnover ratio:

Receivable turnover ratio is also called debtor's turnover ratio. It measures a company's ability to

extend credit or in collecting its receivable. It measures how many time a customer pays dues in

a year. High receivable turnover indicate the efficiency of company to bring back business

owned money.

Trade payable ratio:

Trade payable ratio measure how many times a company pays off its supplier and creditor during

a period of time (Morden, 2016). Higher trade payable turnover ratio shows that company is

paying off its supplier in a timely manner. It also shows that the company has adequate cash to

meet short term debt.

Inventory Turnover Ratio:

Days of inventory is a financial ratio that measure the average time in a day a company take to

convert its inventory in to cash. It is calculated by dividing average inventory with cost of goods

sold and multiply by 365 days. It is the best ratio to measure company's efficiency to convent

inventory into sales.

b) Include the results for each chosen ratio and reasons for the movement between the two years.

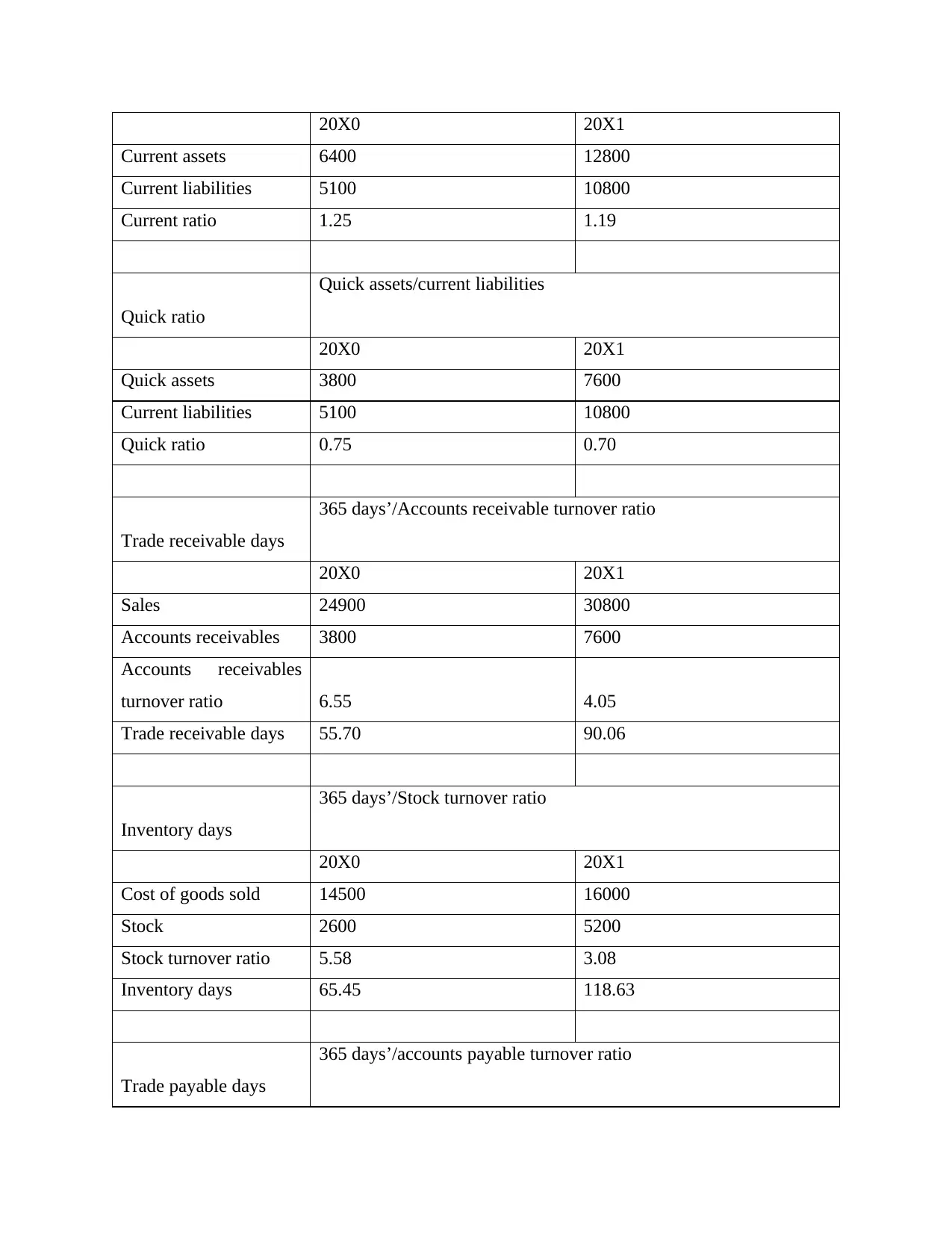

Current ratio

Current assets/current liabilities

liquidity within company.

Quick Ratio:

Quick ratio is a type of liquidity ratio which is also called Acid- Test ratio. This ratio measures a

company's ability to use cash or quick assets to retire its current liability. It is calculated by

dividing quick assets with current liability. Reason to choose quick ration is that it measures

more accurately how current assets pay off current liability and it only include liquid assets

which convert in cash or is cash ready.

Receivable turnover ratio:

Receivable turnover ratio is also called debtor's turnover ratio. It measures a company's ability to

extend credit or in collecting its receivable. It measures how many time a customer pays dues in

a year. High receivable turnover indicate the efficiency of company to bring back business

owned money.

Trade payable ratio:

Trade payable ratio measure how many times a company pays off its supplier and creditor during

a period of time (Morden, 2016). Higher trade payable turnover ratio shows that company is

paying off its supplier in a timely manner. It also shows that the company has adequate cash to

meet short term debt.

Inventory Turnover Ratio:

Days of inventory is a financial ratio that measure the average time in a day a company take to

convert its inventory in to cash. It is calculated by dividing average inventory with cost of goods

sold and multiply by 365 days. It is the best ratio to measure company's efficiency to convent

inventory into sales.

b) Include the results for each chosen ratio and reasons for the movement between the two years.

Current ratio

Current assets/current liabilities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20X0 20X1

Current assets 6400 12800

Current liabilities 5100 10800

Current ratio 1.25 1.19

Quick ratio

Quick assets/current liabilities

20X0 20X1

Quick assets 3800 7600

Current liabilities 5100 10800

Quick ratio 0.75 0.70

Trade receivable days

365 days’/Accounts receivable turnover ratio

20X0 20X1

Sales 24900 30800

Accounts receivables 3800 7600

Accounts receivables

turnover ratio 6.55 4.05

Trade receivable days 55.70 90.06

Inventory days

365 days’/Stock turnover ratio

20X0 20X1

Cost of goods sold 14500 16000

Stock 2600 5200

Stock turnover ratio 5.58 3.08

Inventory days 65.45 118.63

Trade payable days

365 days’/accounts payable turnover ratio

Current assets 6400 12800

Current liabilities 5100 10800

Current ratio 1.25 1.19

Quick ratio

Quick assets/current liabilities

20X0 20X1

Quick assets 3800 7600

Current liabilities 5100 10800

Quick ratio 0.75 0.70

Trade receivable days

365 days’/Accounts receivable turnover ratio

20X0 20X1

Sales 24900 30800

Accounts receivables 3800 7600

Accounts receivables

turnover ratio 6.55 4.05

Trade receivable days 55.70 90.06

Inventory days

365 days’/Stock turnover ratio

20X0 20X1

Cost of goods sold 14500 16000

Stock 2600 5200

Stock turnover ratio 5.58 3.08

Inventory days 65.45 118.63

Trade payable days

365 days’/accounts payable turnover ratio

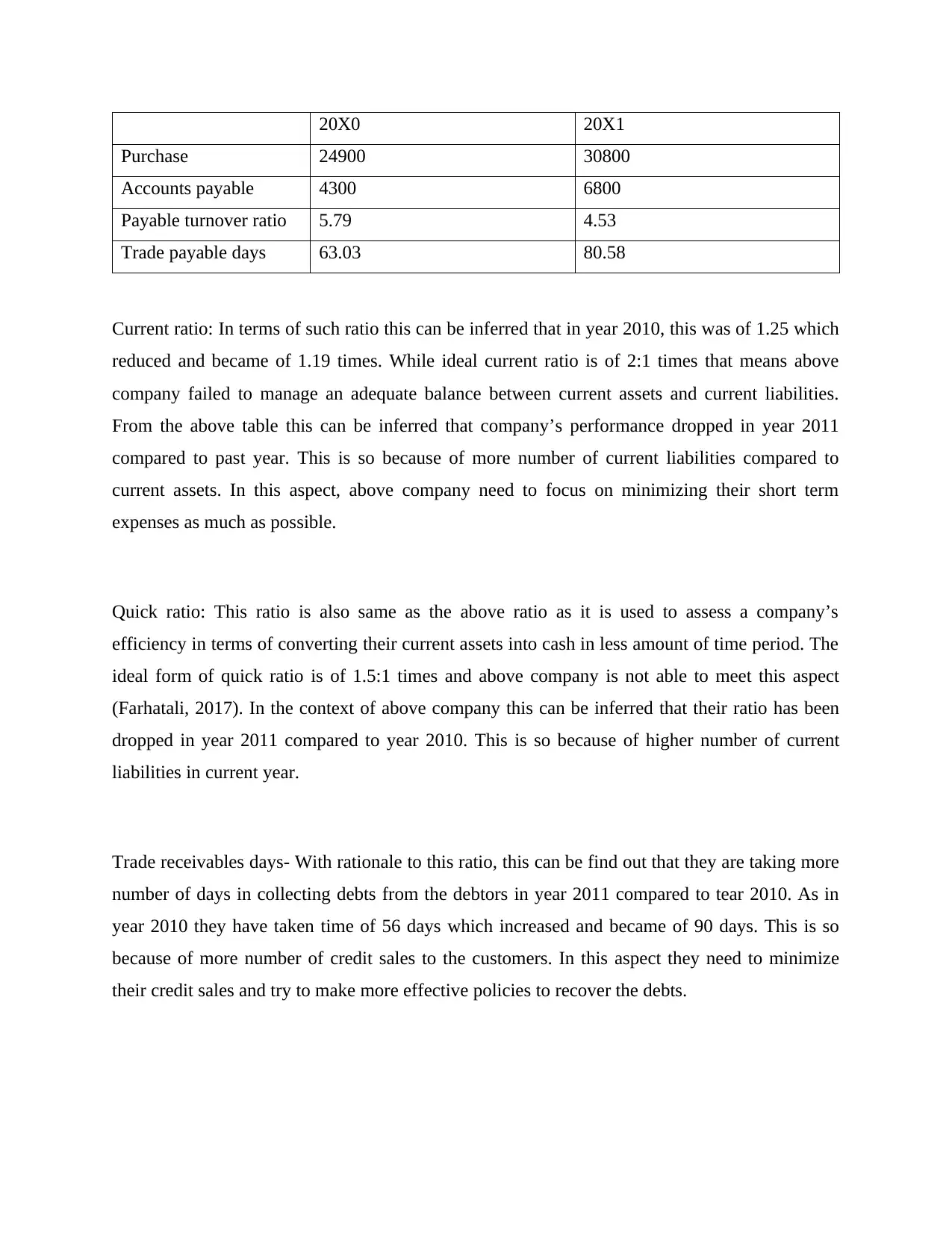

20X0 20X1

Purchase 24900 30800

Accounts payable 4300 6800

Payable turnover ratio 5.79 4.53

Trade payable days 63.03 80.58

Current ratio: In terms of such ratio this can be inferred that in year 2010, this was of 1.25 which

reduced and became of 1.19 times. While ideal current ratio is of 2:1 times that means above

company failed to manage an adequate balance between current assets and current liabilities.

From the above table this can be inferred that company’s performance dropped in year 2011

compared to past year. This is so because of more number of current liabilities compared to

current assets. In this aspect, above company need to focus on minimizing their short term

expenses as much as possible.

Quick ratio: This ratio is also same as the above ratio as it is used to assess a company’s

efficiency in terms of converting their current assets into cash in less amount of time period. The

ideal form of quick ratio is of 1.5:1 times and above company is not able to meet this aspect

(Farhatali, 2017). In the context of above company this can be inferred that their ratio has been

dropped in year 2011 compared to year 2010. This is so because of higher number of current

liabilities in current year.

Trade receivables days- With rationale to this ratio, this can be find out that they are taking more

number of days in collecting debts from the debtors in year 2011 compared to tear 2010. As in

year 2010 they have taken time of 56 days which increased and became of 90 days. This is so

because of more number of credit sales to the customers. In this aspect they need to minimize

their credit sales and try to make more effective policies to recover the debts.

Purchase 24900 30800

Accounts payable 4300 6800

Payable turnover ratio 5.79 4.53

Trade payable days 63.03 80.58

Current ratio: In terms of such ratio this can be inferred that in year 2010, this was of 1.25 which

reduced and became of 1.19 times. While ideal current ratio is of 2:1 times that means above

company failed to manage an adequate balance between current assets and current liabilities.

From the above table this can be inferred that company’s performance dropped in year 2011

compared to past year. This is so because of more number of current liabilities compared to

current assets. In this aspect, above company need to focus on minimizing their short term

expenses as much as possible.

Quick ratio: This ratio is also same as the above ratio as it is used to assess a company’s

efficiency in terms of converting their current assets into cash in less amount of time period. The

ideal form of quick ratio is of 1.5:1 times and above company is not able to meet this aspect

(Farhatali, 2017). In the context of above company this can be inferred that their ratio has been

dropped in year 2011 compared to year 2010. This is so because of higher number of current

liabilities in current year.

Trade receivables days- With rationale to this ratio, this can be find out that they are taking more

number of days in collecting debts from the debtors in year 2011 compared to tear 2010. As in

year 2010 they have taken time of 56 days which increased and became of 90 days. This is so

because of more number of credit sales to the customers. In this aspect they need to minimize

their credit sales and try to make more effective policies to recover the debts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory days- In terms of this, above company is taking too much amount of time in

converting goods into finished products in year 2011 compared to year 2010. This is so because

of more number of stock and higher amount of cost of goods sold in year 2011. Hence above

company needs to minimize their cost of goods sold lower as much as possible. If they will do so

than this will be easier for them to meet the need and demand of customers in an effective

manner.

Trade payable days- With rationale to this ratio, this can be find out that they are taking more

number of days in paying debts to the creditors in year 2011 compared to tear 2010. As in year

2010 they have taken time of 63 days which increased and became of 80 days. This is so because

of more number of credit purchase from suppliers. In this aspect they need to minimize their

credit purchase and try to make more effective policies to pay the debts.

c) Highlight any aspects of the performance of Benedict Co. which would give cause for

concern.

From the above analysis of ratio, it can be find out that the performance of company in all ratio is

dropping in current year compared to past year. As well as they are not able to meet ideal form of

ratio under each aspect. Below detailed analysis has been done:

Current Ratio: The ideal form of current ratio is 2:1 and the company is not able to meet

that ratio. Ratio is also decreasing in current year in compare to previous year ratio and it

shows company's poor liquidity. Company should maintain adequate liquidity level to

fulfil day to day requirement. Poor liquidity shows risk of liquidity for stakeholders of the

company.

Quick Ratio: Ideal quick ratio of a firm is 1:1 and the company is fail to meet that

proportion. The decreasing ratio of above company shows that they are not capable to

pay off the current liability. This may become concern in future to make payment of short

term debts.

converting goods into finished products in year 2011 compared to year 2010. This is so because

of more number of stock and higher amount of cost of goods sold in year 2011. Hence above

company needs to minimize their cost of goods sold lower as much as possible. If they will do so

than this will be easier for them to meet the need and demand of customers in an effective

manner.

Trade payable days- With rationale to this ratio, this can be find out that they are taking more

number of days in paying debts to the creditors in year 2011 compared to tear 2010. As in year

2010 they have taken time of 63 days which increased and became of 80 days. This is so because

of more number of credit purchase from suppliers. In this aspect they need to minimize their

credit purchase and try to make more effective policies to pay the debts.

c) Highlight any aspects of the performance of Benedict Co. which would give cause for

concern.

From the above analysis of ratio, it can be find out that the performance of company in all ratio is

dropping in current year compared to past year. As well as they are not able to meet ideal form of

ratio under each aspect. Below detailed analysis has been done:

Current Ratio: The ideal form of current ratio is 2:1 and the company is not able to meet

that ratio. Ratio is also decreasing in current year in compare to previous year ratio and it

shows company's poor liquidity. Company should maintain adequate liquidity level to

fulfil day to day requirement. Poor liquidity shows risk of liquidity for stakeholders of the

company.

Quick Ratio: Ideal quick ratio of a firm is 1:1 and the company is fail to meet that

proportion. The decreasing ratio of above company shows that they are not capable to

pay off the current liability. This may become concern in future to make payment of short

term debts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trade receivables days- Company is taking too much time in order to recover their debts

from debtors and this is an issue because they need to aware about their recovering

amount. The concern may become of lack of cash availability for operating different

kinds of operations and activities for upcoming time period.

Inventory days- In the context of such ratio, company’s performance is poor in both year

and this is an issue for them. It is so because they are taking too much time to convert

goods into prepared products. In future time period this may lead to higher cost as well as

competitors may beat them if they will not deliver products on time.

Trade payable days- In terms of such ratio, this can be stated that it is a reason of concern

for above company. This is so because they are taking more number of days to make

payment to their creditors. This may lead to a core risk in future time period for above

company. This is so because if they will not make payment to their creditors on time than

there may be risk of decrease in goodwill.

d) Critically evaluate the application of financial ratios in interpreting and measuring the

performance of a company.

Standardized method of comparison: Financial ratio provide a standard of comparing

company and industry (Oladeji, Oyewo and Akinjare, 2016). These methods put all the

company on same path and judge them on their performance instead of their size, sales

volume and market share. Ratio provide information related to capability of company in

profitability, financing the business and other factors.

Industry analysis and benchmark: Performance of a company can be measured by ratio as

it discloses the trends of specific industry. To make strategy for organization of small

business, industry benchmark is used and it measure their performance against that

industry.

Stock valuation for strength and weakness: By understanding the ratio analyst can

identify strength and weakness of a particular company or industry. To identify the

strength of the company, fundamental analysis is used with the intention of investigation.

It helps to identify company’s fundamental strength by analysis of firm's ratio to increase

value of their stock and profit opportunity. It also indicates weaker market players of the

industry.

from debtors and this is an issue because they need to aware about their recovering

amount. The concern may become of lack of cash availability for operating different

kinds of operations and activities for upcoming time period.

Inventory days- In the context of such ratio, company’s performance is poor in both year

and this is an issue for them. It is so because they are taking too much time to convert

goods into prepared products. In future time period this may lead to higher cost as well as

competitors may beat them if they will not deliver products on time.

Trade payable days- In terms of such ratio, this can be stated that it is a reason of concern

for above company. This is so because they are taking more number of days to make

payment to their creditors. This may lead to a core risk in future time period for above

company. This is so because if they will not make payment to their creditors on time than

there may be risk of decrease in goodwill.

d) Critically evaluate the application of financial ratios in interpreting and measuring the

performance of a company.

Standardized method of comparison: Financial ratio provide a standard of comparing

company and industry (Oladeji, Oyewo and Akinjare, 2016). These methods put all the

company on same path and judge them on their performance instead of their size, sales

volume and market share. Ratio provide information related to capability of company in

profitability, financing the business and other factors.

Industry analysis and benchmark: Performance of a company can be measured by ratio as

it discloses the trends of specific industry. To make strategy for organization of small

business, industry benchmark is used and it measure their performance against that

industry.

Stock valuation for strength and weakness: By understanding the ratio analyst can

identify strength and weakness of a particular company or industry. To identify the

strength of the company, fundamental analysis is used with the intention of investigation.

It helps to identify company’s fundamental strength by analysis of firm's ratio to increase

value of their stock and profit opportunity. It also indicates weaker market players of the

industry.

Planning and performance: It help the entrepreneur in preparing business presentation

and business plan for the investor and lender (Nestor, 2016). It uses industry trends as

base for small business owner to set performance goals in term of particular ratio to give

investor a particular view in the company.

Assess the liquidity of the firm: Ratio helps in assessing the capability of firm to meet its

short term obligation. Short term obligation includes short term debts which can be paid

within the period of less than 12 months. Short term debt include salary, wages, payment

of supplier.

Analysis of financial statement: Financial statement provide essential data to

shareholders. Ratio analysis helps to interpret data from balance sheet and income

statements (Patel, 2016). Different investor has different interest in the result of financial

interest as shareholders want growth in dividend payment while creditors want repayment

of their dues on timely basis.

CONCLUSION

On the basis of above report this can be concluded that management of funds and other aspects is

too crucial for companies to sustain in competitive environment. From first part of report this can

be concluded that companies need to consider the importance to their stakeholders and try to

fulfill their needs. Tesco Plc has both kinds of stakeholders including internal and external. In

addition to this, from second part of report this can be concluded that Benedict company's

performance is poor under each aspect which need to improve as soon as possible.

and business plan for the investor and lender (Nestor, 2016). It uses industry trends as

base for small business owner to set performance goals in term of particular ratio to give

investor a particular view in the company.

Assess the liquidity of the firm: Ratio helps in assessing the capability of firm to meet its

short term obligation. Short term obligation includes short term debts which can be paid

within the period of less than 12 months. Short term debt include salary, wages, payment

of supplier.

Analysis of financial statement: Financial statement provide essential data to

shareholders. Ratio analysis helps to interpret data from balance sheet and income

statements (Patel, 2016). Different investor has different interest in the result of financial

interest as shareholders want growth in dividend payment while creditors want repayment

of their dues on timely basis.

CONCLUSION

On the basis of above report this can be concluded that management of funds and other aspects is

too crucial for companies to sustain in competitive environment. From first part of report this can

be concluded that companies need to consider the importance to their stakeholders and try to

fulfill their needs. Tesco Plc has both kinds of stakeholders including internal and external. In

addition to this, from second part of report this can be concluded that Benedict company's

performance is poor under each aspect which need to improve as soon as possible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.