HI5019: Strategic Information Systems Report - Bell Studio

VerifiedAdded on 2023/03/17

|19

|3347

|20

Report

AI Summary

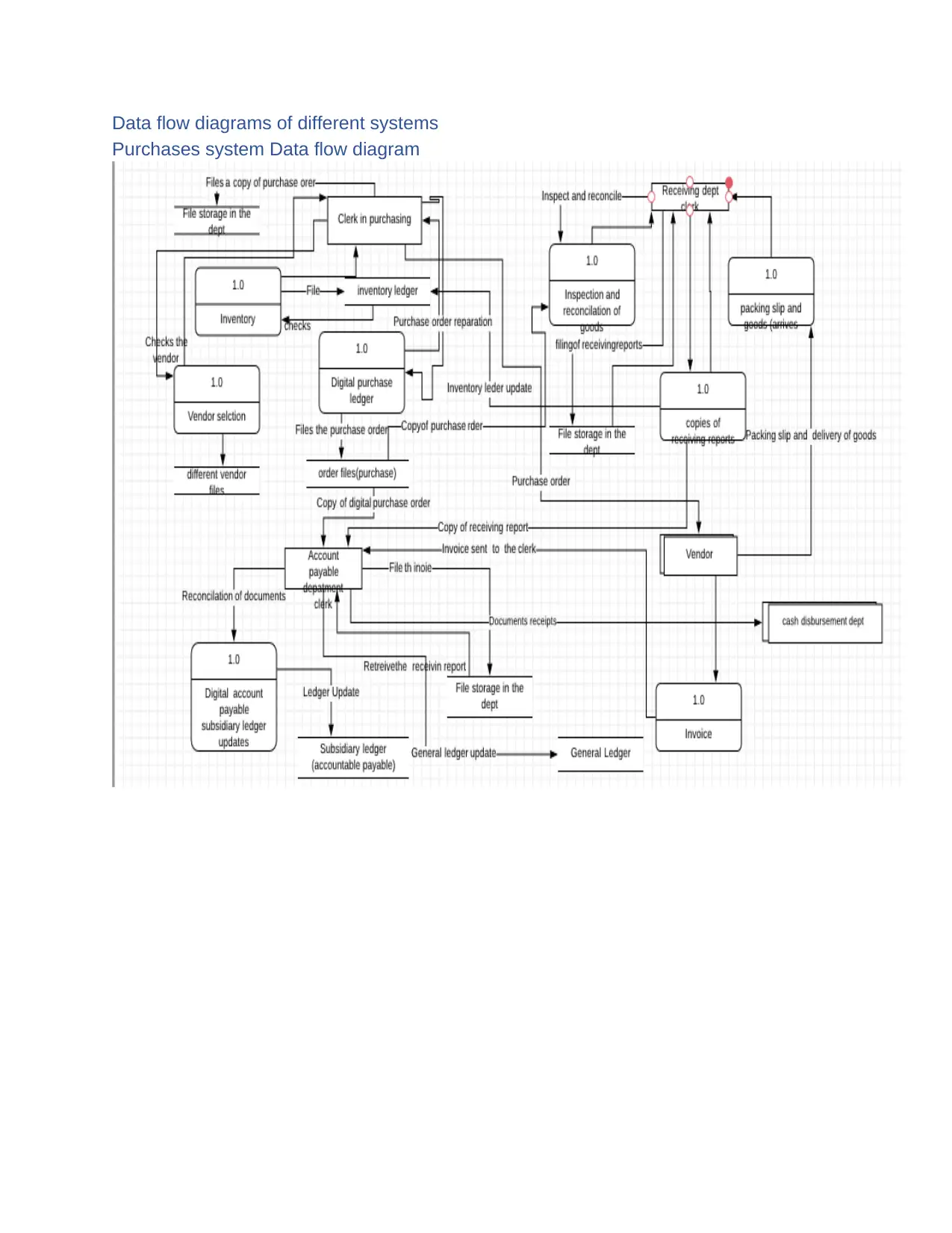

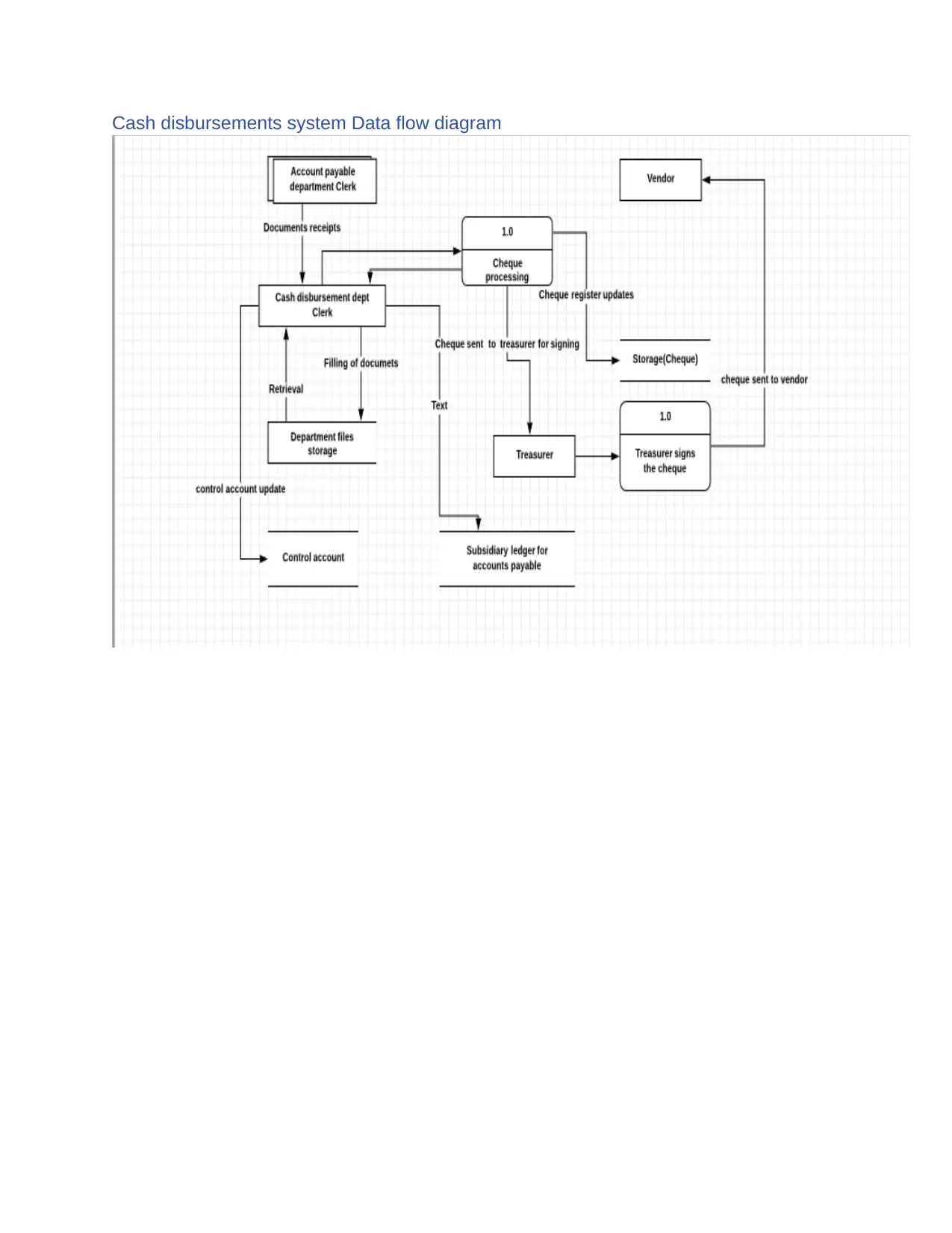

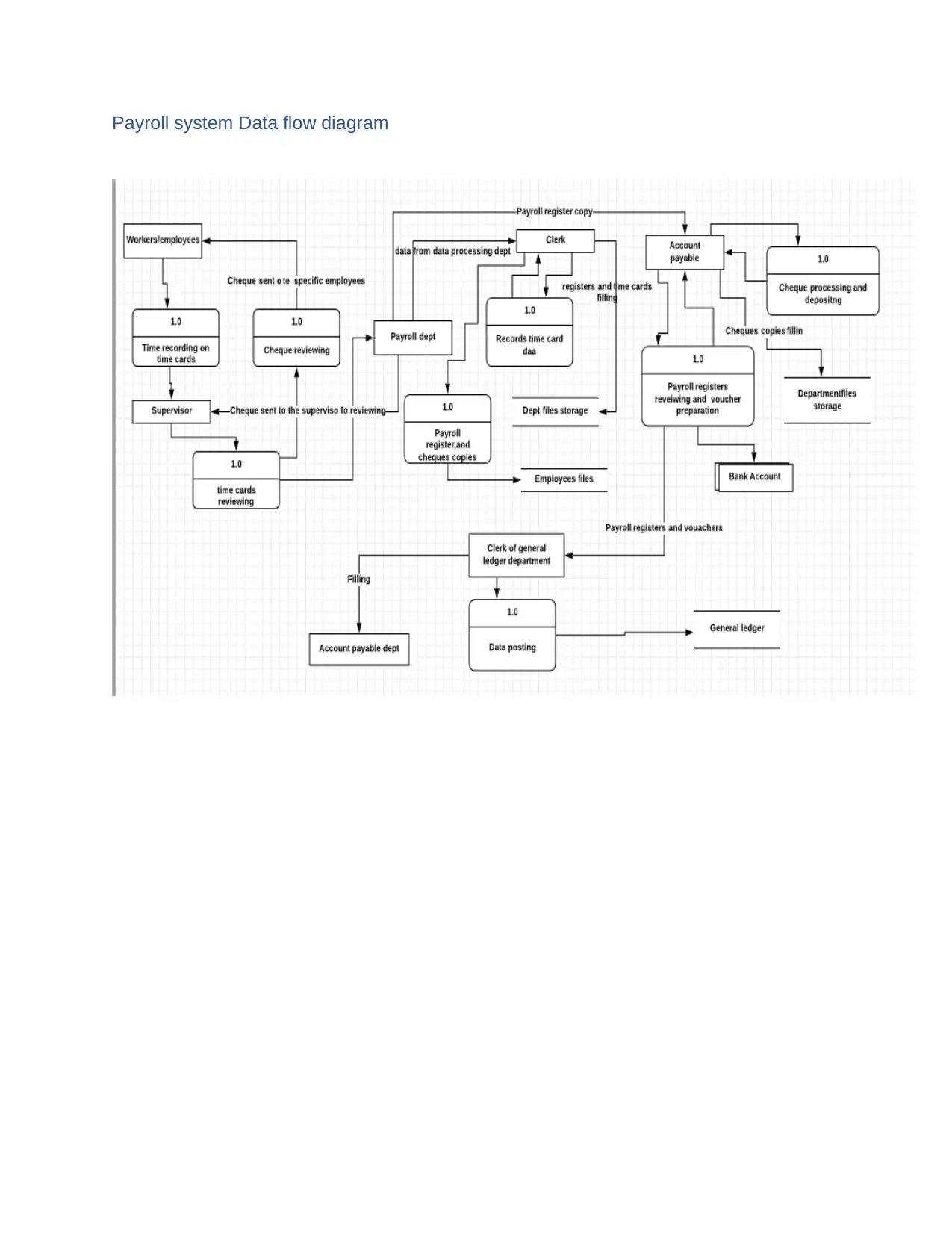

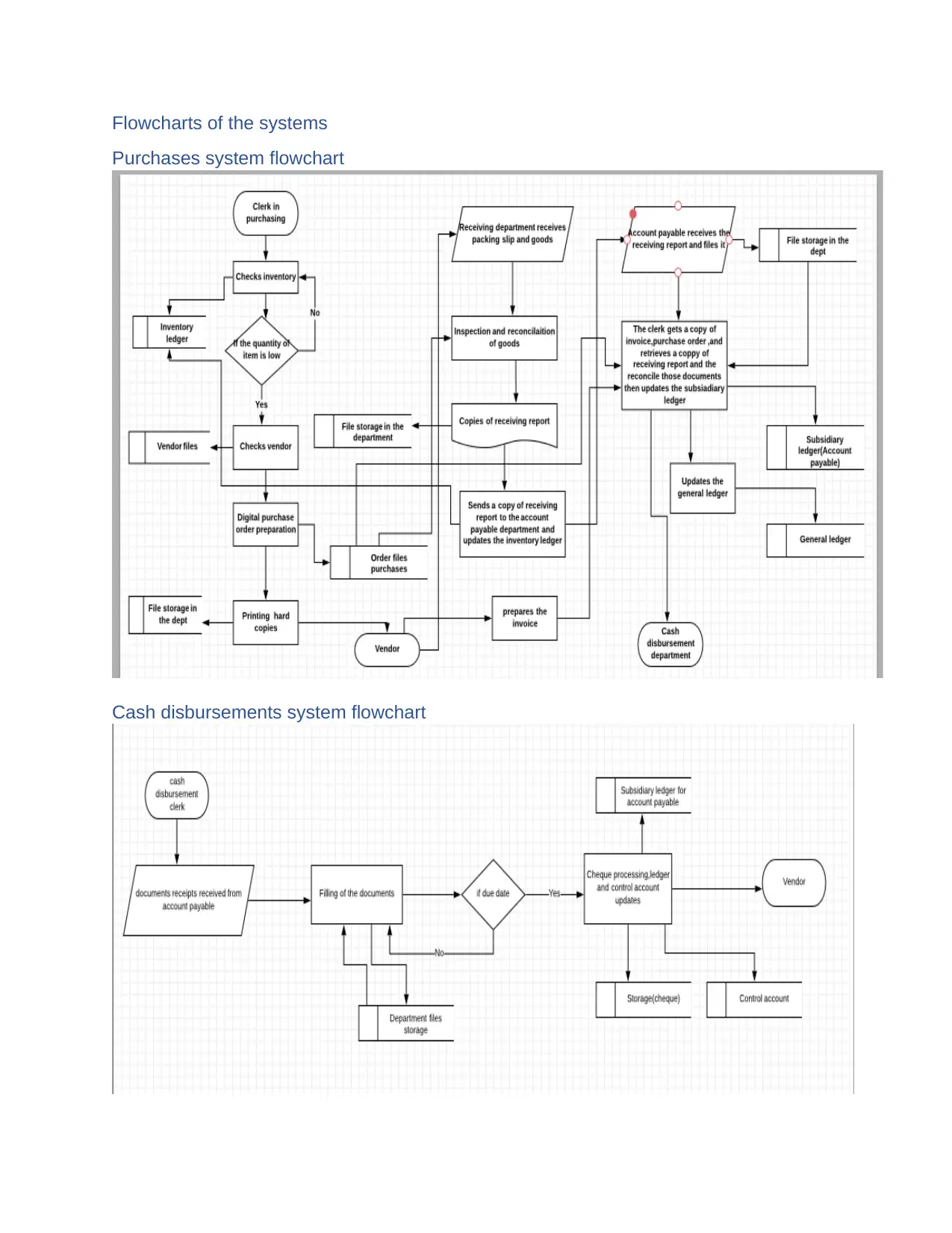

This report provides a comprehensive overview of strategic information systems for businesses and enterprises, focusing on key areas such as e-commerce, financial reporting, transaction cycles, and management reporting systems. It explores the importance of accurate and timely financial information for decision-making, detailing the components and benefits of financial reporting. The report also examines different types of transaction cycles, including payroll, purchasing, sales, and financing cycles. It highlights the features and types of e-commerce, its advantages, and potential risks. Furthermore, the document includes data flow diagrams and flowcharts of various systems like purchases, cash disbursements, and payroll, followed by an analysis of potential weaknesses and risks within these systems. The report concludes with a discussion of internal control practices, their weaknesses, and associated risks, encompassing review and reconciliation, asset security, separation of duties, and authorization processes. This analysis is crucial for understanding and mitigating potential issues within business operations.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.