Strategic Information System Report: Revenue and Expenditure Cycles

VerifiedAdded on 2022/08/25

|8

|2145

|17

Report

AI Summary

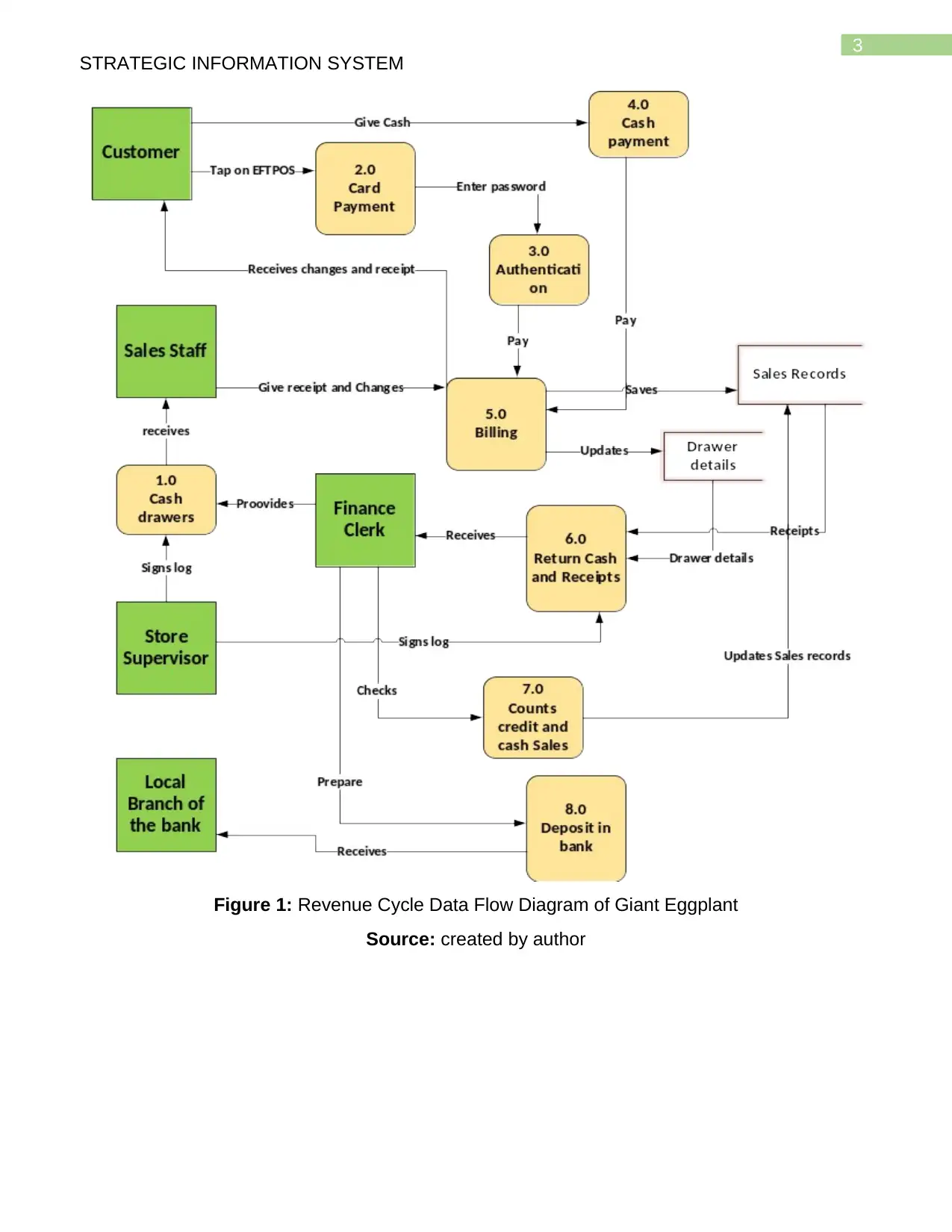

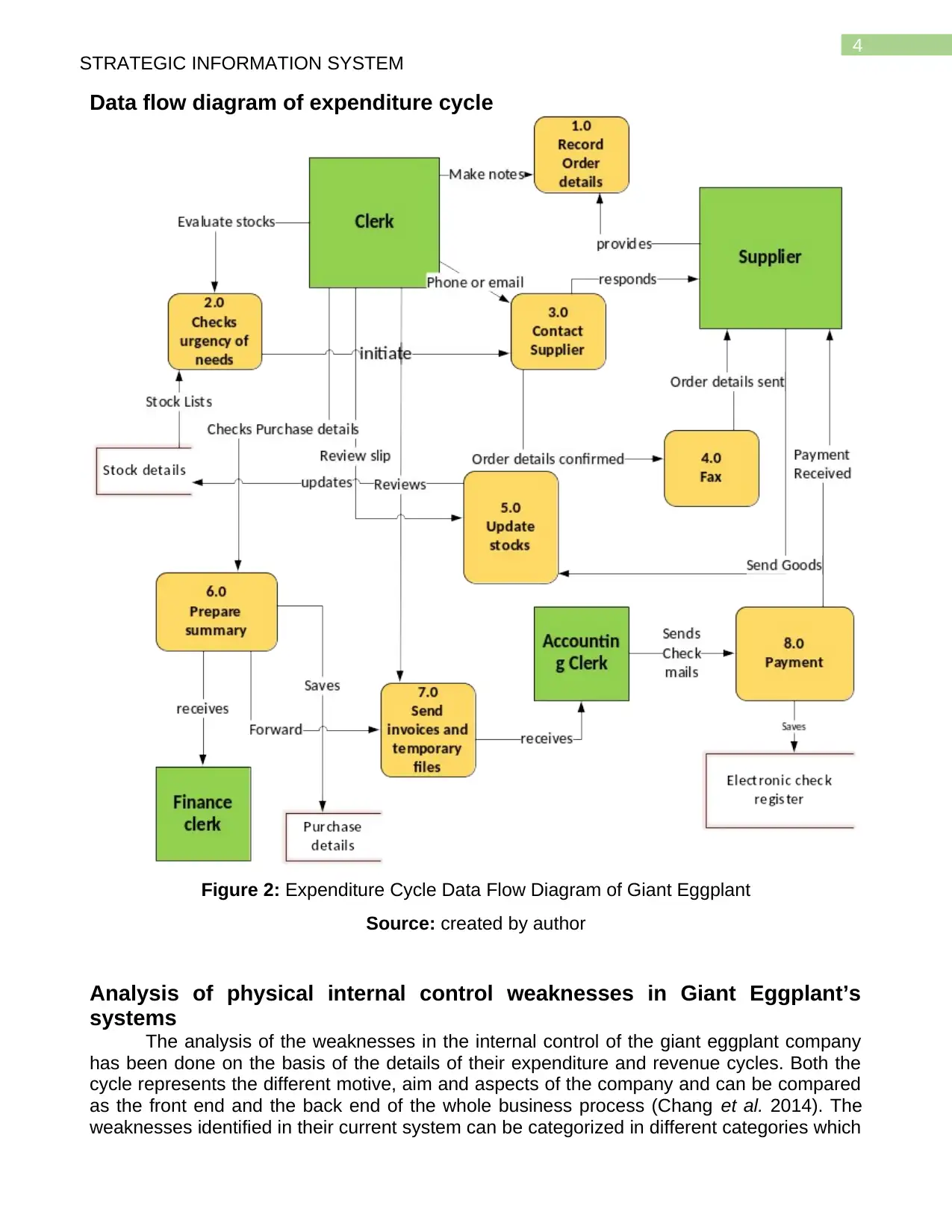

This report provides a comprehensive analysis of the strategic information system (SIS) for the Giant Eggplant company, a fruit and vegetable business. It begins with an introduction to the company, its current challenges, and the objectives of the report. The core of the report includes data flow diagrams (DFDs) for both the revenue and expenditure cycles, visually representing the flow of data and processes within the company. Following the DFDs, the report delves into an analysis of the physical internal control weaknesses within Giant Eggplant’s systems, categorizing the weaknesses into organizational, process, documentation, asset, management, and authorization controls. Specific examples of weaknesses are provided for both the revenue and expenditure cycles. The report then proposes descriptions of IT controls that should be in place to address the identified weaknesses, offering recommendations for improved management policies, automated systems, and enhanced security measures. The report concludes by summarizing the key findings and recommendations, emphasizing the importance of implementing the suggested controls to mitigate risks and improve overall business performance. References to the cited sources are included.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.