Strategic Information System for Bell Studio Business Report

VerifiedAdded on 2022/12/15

|15

|3714

|64

Report

AI Summary

This report provides an in-depth analysis of the strategic information system implemented by Bell Studio, an Adelaide-based distributor of workmanship providers. The report examines the company's expenditure cycle, focusing on three key systems: the purchase system, cash disbursement system, and payroll system. It includes detailed discussions of data flow diagrams (DFDs) and system flowcharts for each system, illustrating the processes involved. The analysis covers the procedures for submitting purchase orders, receiving inventory, managing cash disbursements, and processing payroll. Furthermore, the report identifies potential shortcomings and risks associated with each system, enabling the Chief Operating Officer to assess the dangers, forms and inward controls for the use cycle. The report highlights the importance of integrated systems in managing business money, physical materials, and human resources, and offers insights into the application of these systems in a retail and manufacturing context.

Running head: STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Name of the student

Name of the university

Author notes

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Name of the student

Name of the university

Author notes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 1

|

Executive Summary:

This report investigates the Bell Studio business that is an Adelaide-based distributer

of workmanship providers. Considering the way that the organization has a brought

together bookkeeping framework with different systems administration terminals in

various area, this paper forms a top to bottom assessment of the use cycle

processes. For this reason, three frameworks that comprises the consumption the

cycle must be talked about: payroll system, cash disbursement system and the

purchases systems. The initial segment of this paper will give a review of the reports

as well as the applied frameworks Data Flow Diagram (DFD) shall be talked about in

the second segments. A short time later, the framework flowchart must be

investigated before the segment that talked about the potential shortcomings and

dangers of every framework.

|

Executive Summary:

This report investigates the Bell Studio business that is an Adelaide-based distributer

of workmanship providers. Considering the way that the organization has a brought

together bookkeeping framework with different systems administration terminals in

various area, this paper forms a top to bottom assessment of the use cycle

processes. For this reason, three frameworks that comprises the consumption the

cycle must be talked about: payroll system, cash disbursement system and the

purchases systems. The initial segment of this paper will give a review of the reports

as well as the applied frameworks Data Flow Diagram (DFD) shall be talked about in

the second segments. A short time later, the framework flowchart must be

investigated before the segment that talked about the potential shortcomings and

dangers of every framework.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 2

|

Table of Contents

Introduction:..........................................................................................................................................4

Purchase System....................................................................................................................................4

Cash Disbursement Systems:.................................................................................................................6

Payroll System:......................................................................................................................................7

Cash disbursement department:.....................................................................................................11

Inner Control Weaknesses and Risks in Each System..........................................................................13

Purchases System:...........................................................................................................................13

Cash Disbursement Systems:...........................................................................................................13

Payroll Systems:...............................................................................................................................13

Conclusion:..........................................................................................................................................13

|

Table of Contents

Introduction:..........................................................................................................................................4

Purchase System....................................................................................................................................4

Cash Disbursement Systems:.................................................................................................................6

Payroll System:......................................................................................................................................7

Cash disbursement department:.....................................................................................................11

Inner Control Weaknesses and Risks in Each System..........................................................................13

Purchases System:...........................................................................................................................13

Cash Disbursement Systems:...........................................................................................................13

Payroll Systems:...............................................................................................................................13

Conclusion:..........................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 3

|

Introduction:

The primary goal of the expenditure cycles is for empowering the change of

the organization's business money, physical materials and HR that improve different

capacities in the association. This paper investigations the consumption cycle (buys

frameworks, money dispensing frameworks and finance framework) in Bell Studio

association, including the assessment of the applicable shortcomings and dangers of

the frameworks. The primary reason for this report is for empowering the Chief

Operating Officer to assess the dangers, forms and inward controls for the use cycle.

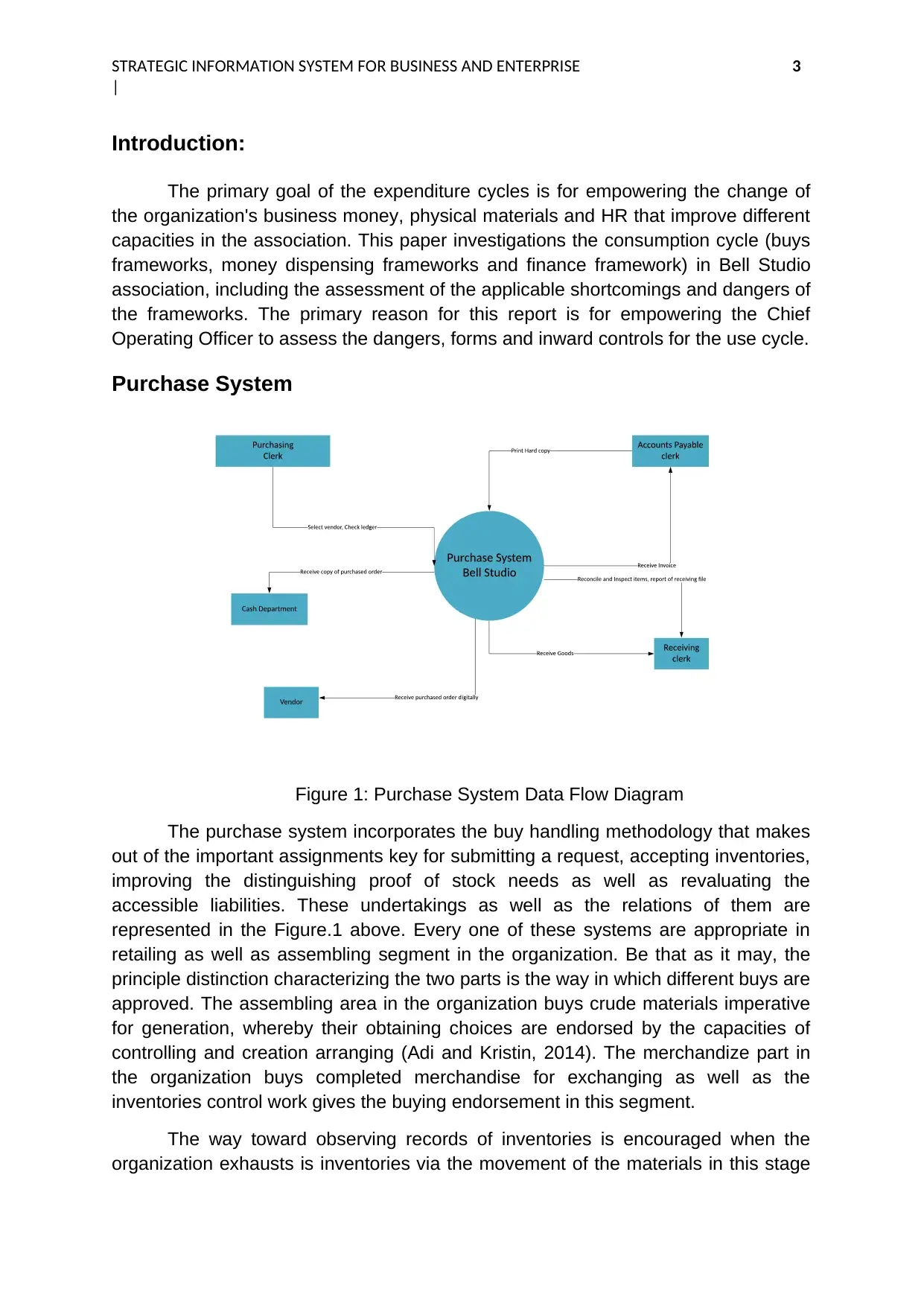

Purchase System

Figure 1: Purchase System Data Flow Diagram

The purchase system incorporates the buy handling methodology that makes

out of the important assignments key for submitting a request, accepting inventories,

improving the distinguishing proof of stock needs as well as revaluating the

accessible liabilities. These undertakings as well as the relations of them are

represented in the Figure.1 above. Every one of these systems are appropriate in

retailing as well as assembling segment in the organization. Be that as it may, the

principle distinction characterizing the two parts is the way in which different buys are

approved. The assembling area in the organization buys crude materials imperative

for generation, whereby their obtaining choices are endorsed by the capacities of

controlling and creation arranging (Adi and Kristin, 2014). The merchandize part in

the organization buys completed merchandise for exchanging as well as the

inventories control work gives the buying endorsement in this segment.

The way toward observing records of inventories is encouraged when the

organization exhausts is inventories via the movement of the materials in this stage

|

Introduction:

The primary goal of the expenditure cycles is for empowering the change of

the organization's business money, physical materials and HR that improve different

capacities in the association. This paper investigations the consumption cycle (buys

frameworks, money dispensing frameworks and finance framework) in Bell Studio

association, including the assessment of the applicable shortcomings and dangers of

the frameworks. The primary reason for this report is for empowering the Chief

Operating Officer to assess the dangers, forms and inward controls for the use cycle.

Purchase System

Figure 1: Purchase System Data Flow Diagram

The purchase system incorporates the buy handling methodology that makes

out of the important assignments key for submitting a request, accepting inventories,

improving the distinguishing proof of stock needs as well as revaluating the

accessible liabilities. These undertakings as well as the relations of them are

represented in the Figure.1 above. Every one of these systems are appropriate in

retailing as well as assembling segment in the organization. Be that as it may, the

principle distinction characterizing the two parts is the way in which different buys are

approved. The assembling area in the organization buys crude materials imperative

for generation, whereby their obtaining choices are endorsed by the capacities of

controlling and creation arranging (Adi and Kristin, 2014). The merchandize part in

the organization buys completed merchandise for exchanging as well as the

inventories control work gives the buying endorsement in this segment.

The way toward observing records of inventories is encouraged when the

organization exhausts is inventories via the movement of the materials in this stage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 4

|

of product. It is the change cycle as well as the exchanging of completed

merchandise to the buyers through the income cycle. The stock controls the records

as well screens the completed items and its stock dimensions. Upon that drop into

the dimension of the foreordaining and inventories point of reordering, there is

requirement for the buy assistant to set up the buy request work, which will start the

acquiring procedure.

From there on, buy order is fundable as well as changes in various

associations. Normally, the organization will encourage and set up a discrete buy

demand for different stock things where it is needed to be. Resultantly, different

buying demands might be obviously for an accessible seller and these orders should

be consolidated into one buying request before this is forwarded to the merchant

(Fauzi and Setyawan, 2018). This type of framework enables each obtaining request

to be connected to more than one requisitions of purchase.

The arrangement of the buy request work acquires the buying orders, sorted

out by the seller at whatever point required. Subsequently, that Purchase Order (PO)

duplicate is intended for the separate sellers as demonstrated in the Data Flow

Diagram (DFD) in Figure 1. Furthermore, another duplicate is exchanged to the

acquiring division for the setup of the Account Payable (AP) capacities implied for

brief recording of the documents that are AP pending. Consequently, a visually

impaired duplicate of the document is then sent for Receiving the Goods capacities.

Numerous organizations experience a period slack between accepting

merchandise and putting in a request. Amid this stage, different PO duplicates will be

incorporated into the brief documents in the record payable division, and no

monetary viewpoint is being executed (Fedaghi, 2014). At the crossroads, the Bell

Studio association yet has not gotten any of the inventories or caused any budgetary

commitments. In such manner, there is no need even of encouraging the creation of

formal sections in the bookkeeping records. In any case, the organization may

choose the making of a notice section in reference for pending stock related

commitment as well as receipts.

This following stage in this cycle will include the receipt based inventories

thereby products come and the getting report is readied. These merchandises are

then accommodated with the pressing Digital Purchase Order (DPO) and slip. The

duplicates of the report incorporate the information on amount and costs of the

things got. The primary reason for these archives is to empower the getting

representative to assess and tally inventories before drafting of the accepting report

(Gautam, 2010). Generally, the getting office is occupied as well the staffs of them

as exposed to weight of emptying the conveyance vehicles or marking filling

charges. In such of the cases, the getting agent may be furnished with the applicable

information on thing amount and acknowledge a conveyance of items in reference

for that given information.

|

of product. It is the change cycle as well as the exchanging of completed

merchandise to the buyers through the income cycle. The stock controls the records

as well screens the completed items and its stock dimensions. Upon that drop into

the dimension of the foreordaining and inventories point of reordering, there is

requirement for the buy assistant to set up the buy request work, which will start the

acquiring procedure.

From there on, buy order is fundable as well as changes in various

associations. Normally, the organization will encourage and set up a discrete buy

demand for different stock things where it is needed to be. Resultantly, different

buying demands might be obviously for an accessible seller and these orders should

be consolidated into one buying request before this is forwarded to the merchant

(Fauzi and Setyawan, 2018). This type of framework enables each obtaining request

to be connected to more than one requisitions of purchase.

The arrangement of the buy request work acquires the buying orders, sorted

out by the seller at whatever point required. Subsequently, that Purchase Order (PO)

duplicate is intended for the separate sellers as demonstrated in the Data Flow

Diagram (DFD) in Figure 1. Furthermore, another duplicate is exchanged to the

acquiring division for the setup of the Account Payable (AP) capacities implied for

brief recording of the documents that are AP pending. Consequently, a visually

impaired duplicate of the document is then sent for Receiving the Goods capacities.

Numerous organizations experience a period slack between accepting

merchandise and putting in a request. Amid this stage, different PO duplicates will be

incorporated into the brief documents in the record payable division, and no

monetary viewpoint is being executed (Fedaghi, 2014). At the crossroads, the Bell

Studio association yet has not gotten any of the inventories or caused any budgetary

commitments. In such manner, there is no need even of encouraging the creation of

formal sections in the bookkeeping records. In any case, the organization may

choose the making of a notice section in reference for pending stock related

commitment as well as receipts.

This following stage in this cycle will include the receipt based inventories

thereby products come and the getting report is readied. These merchandises are

then accommodated with the pressing Digital Purchase Order (DPO) and slip. The

duplicates of the report incorporate the information on amount and costs of the

things got. The primary reason for these archives is to empower the getting

representative to assess and tally inventories before drafting of the accepting report

(Gautam, 2010). Generally, the getting office is occupied as well the staffs of them

as exposed to weight of emptying the conveyance vehicles or marking filling

charges. In such of the cases, the getting agent may be furnished with the applicable

information on thing amount and acknowledge a conveyance of items in reference

for that given information.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 5

|

In that cycle, the following stage that is in the arrangement of update with

respect to the stock record. With respect to the valuation of inventories valuation

strategy, the inventories are able to control the procedure shifts in various

associations. An organization that uses an institutionalized cost system can execute

the stock of them at a foreordained institutionalized figure independent of that

charges that being paid to one of the merchants. Introducing an institutionalized

inventories record requires the significant information in regards to the amount

accomplished. Since the getting reports are containing the thing amount information,

this record fills this need (Bhoite, 2012). In this manner, refreshing the principle cost

stock record requires increasingly budgetary information from the stock distribution

center. Amid the procedure of this exchange, creditor liabilities needs one setup.

That AP work gets that setting the transitory records of the getting PO and report is

documented. The Bell Studio association has gotten those inventories from the

separate merchants and understood its commitment for paying for the goods that are

received.

For ending the procedure, the records payable assistant needs to assess the

careful valuation for that commitment up for the time the receipt has gotten. At the

point when the gauge is physically inappropriate, a change of the section should be

attempted to correct the errors, since that receipt of the receipt trigger AP strategies

and procedures, agents need to assess every one of the liabilities which have been

not recorded amid the time end shutting (Hooshyar, Yusop and Horng, 2015). Upon

the landing of the inventories, the AP assistants accommodate the important money

related information with PO as well as the accepting report in that accessible

pending document. It is known as the three ways coordinating that checks the

amount which has been gotten and its separate costs (Jarrah, 2018). Amid this

minute, the assistant dynamically refreshes that Digital Account Payable (DPO)

auxiliary record, Account payable controls account as well as for controlling the

inventories controls in the general record. In conclusion, an include, PO and

accepting report are exchanged.

Cash Disbursement Systems:

|

In that cycle, the following stage that is in the arrangement of update with

respect to the stock record. With respect to the valuation of inventories valuation

strategy, the inventories are able to control the procedure shifts in various

associations. An organization that uses an institutionalized cost system can execute

the stock of them at a foreordained institutionalized figure independent of that

charges that being paid to one of the merchants. Introducing an institutionalized

inventories record requires the significant information in regards to the amount

accomplished. Since the getting reports are containing the thing amount information,

this record fills this need (Bhoite, 2012). In this manner, refreshing the principle cost

stock record requires increasingly budgetary information from the stock distribution

center. Amid the procedure of this exchange, creditor liabilities needs one setup.

That AP work gets that setting the transitory records of the getting PO and report is

documented. The Bell Studio association has gotten those inventories from the

separate merchants and understood its commitment for paying for the goods that are

received.

For ending the procedure, the records payable assistant needs to assess the

careful valuation for that commitment up for the time the receipt has gotten. At the

point when the gauge is physically inappropriate, a change of the section should be

attempted to correct the errors, since that receipt of the receipt trigger AP strategies

and procedures, agents need to assess every one of the liabilities which have been

not recorded amid the time end shutting (Hooshyar, Yusop and Horng, 2015). Upon

the landing of the inventories, the AP assistants accommodate the important money

related information with PO as well as the accepting report in that accessible

pending document. It is known as the three ways coordinating that checks the

amount which has been gotten and its separate costs (Jarrah, 2018). Amid this

minute, the assistant dynamically refreshes that Digital Account Payable (DPO)

auxiliary record, Account payable controls account as well as for controlling the

inventories controls in the general record. In conclusion, an include, PO and

accepting report are exchanged.

Cash Disbursement Systems:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 6

|

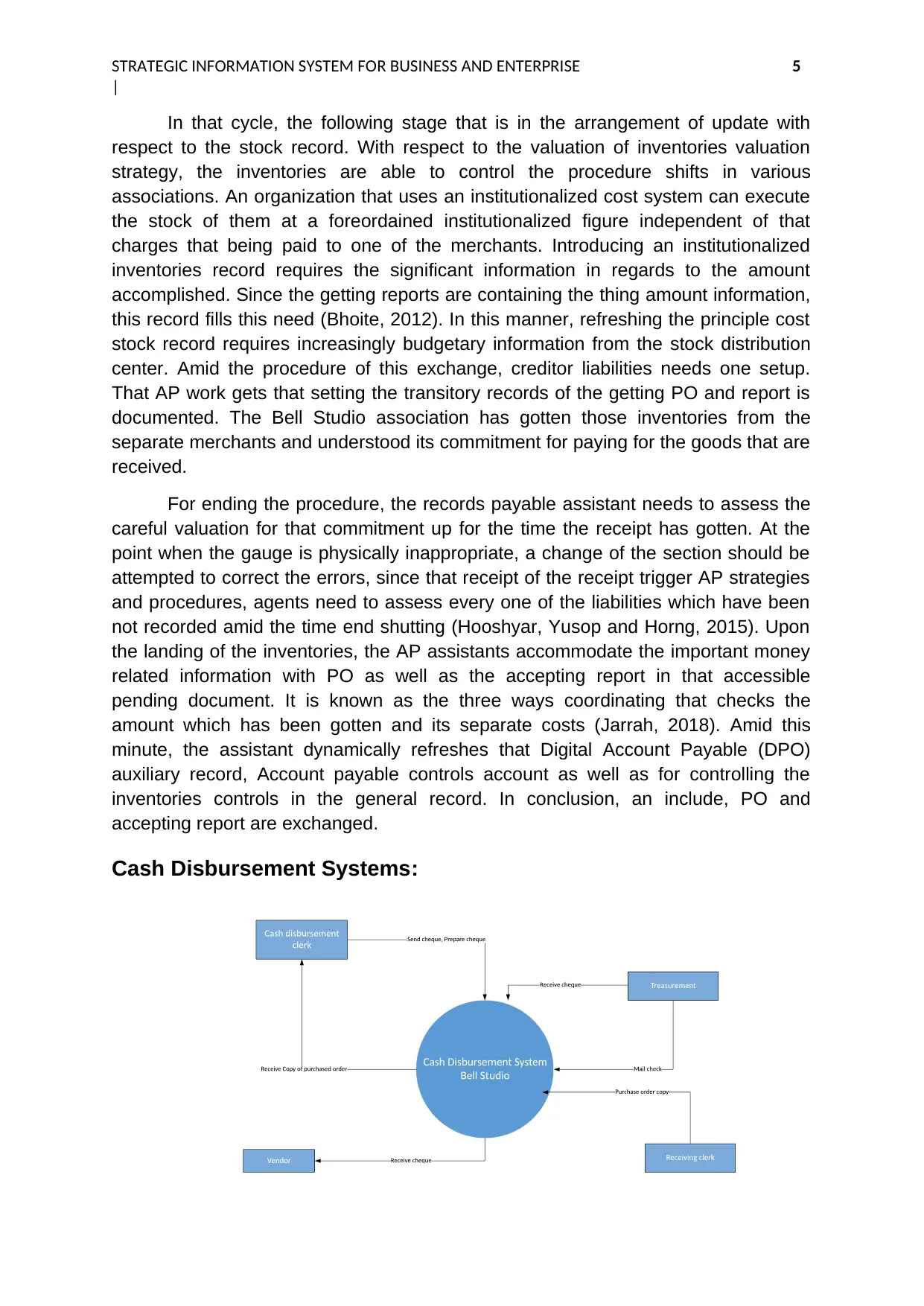

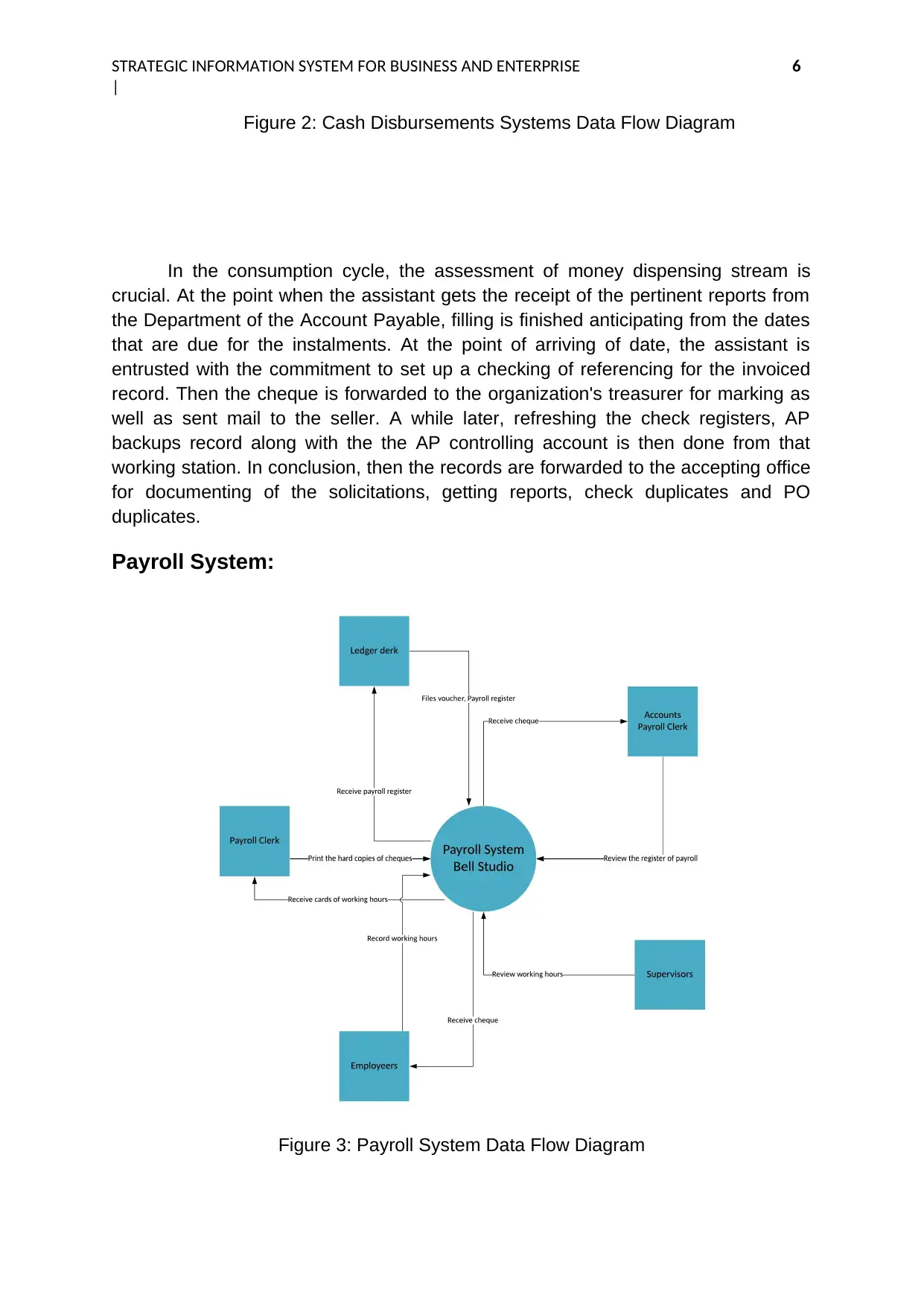

Figure 2: Cash Disbursements Systems Data Flow Diagram

In the consumption cycle, the assessment of money dispensing stream is

crucial. At the point when the assistant gets the receipt of the pertinent reports from

the Department of the Account Payable, filling is finished anticipating from the dates

that are due for the instalments. At the point of arriving of date, the assistant is

entrusted with the commitment to set up a checking of referencing for the invoiced

record. Then the cheque is forwarded to the organization's treasurer for marking as

well as sent mail to the seller. A while later, refreshing the check registers, AP

backups record along with the the AP controlling account is then done from that

working station. In conclusion, then the records are forwarded to the accepting office

for documenting of the solicitations, getting reports, check duplicates and PO

duplicates.

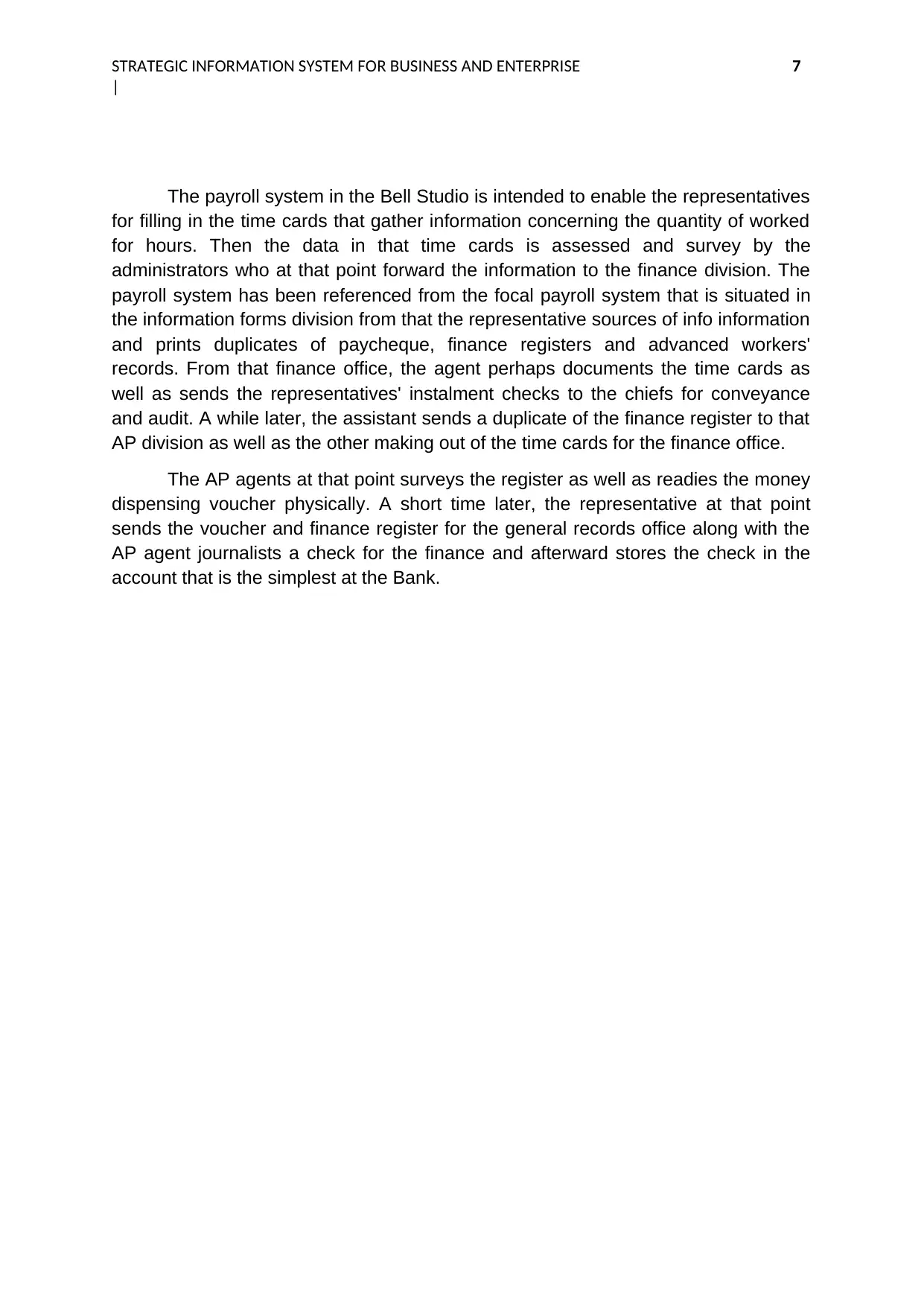

Payroll System:

Figure 3: Payroll System Data Flow Diagram

|

Figure 2: Cash Disbursements Systems Data Flow Diagram

In the consumption cycle, the assessment of money dispensing stream is

crucial. At the point when the assistant gets the receipt of the pertinent reports from

the Department of the Account Payable, filling is finished anticipating from the dates

that are due for the instalments. At the point of arriving of date, the assistant is

entrusted with the commitment to set up a checking of referencing for the invoiced

record. Then the cheque is forwarded to the organization's treasurer for marking as

well as sent mail to the seller. A while later, refreshing the check registers, AP

backups record along with the the AP controlling account is then done from that

working station. In conclusion, then the records are forwarded to the accepting office

for documenting of the solicitations, getting reports, check duplicates and PO

duplicates.

Payroll System:

Figure 3: Payroll System Data Flow Diagram

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 7

|

The payroll system in the Bell Studio is intended to enable the representatives

for filling in the time cards that gather information concerning the quantity of worked

for hours. Then the data in that time cards is assessed and survey by the

administrators who at that point forward the information to the finance division. The

payroll system has been referenced from the focal payroll system that is situated in

the information forms division from that the representative sources of info information

and prints duplicates of paycheque, finance registers and advanced workers'

records. From that finance office, the agent perhaps documents the time cards as

well as sends the representatives' instalment checks to the chiefs for conveyance

and audit. A while later, the assistant sends a duplicate of the finance register to that

AP division as well as the other making out of the time cards for the finance office.

The AP agents at that point surveys the register as well as readies the money

dispensing voucher physically. A short time later, the representative at that point

sends the voucher and finance register for the general records office along with the

AP agent journalists a check for the finance and afterward stores the check in the

account that is the simplest at the Bank.

|

The payroll system in the Bell Studio is intended to enable the representatives

for filling in the time cards that gather information concerning the quantity of worked

for hours. Then the data in that time cards is assessed and survey by the

administrators who at that point forward the information to the finance division. The

payroll system has been referenced from the focal payroll system that is situated in

the information forms division from that the representative sources of info information

and prints duplicates of paycheque, finance registers and advanced workers'

records. From that finance office, the agent perhaps documents the time cards as

well as sends the representatives' instalment checks to the chiefs for conveyance

and audit. A while later, the assistant sends a duplicate of the finance register to that

AP division as well as the other making out of the time cards for the finance office.

The AP agents at that point surveys the register as well as readies the money

dispensing voucher physically. A short time later, the representative at that point

sends the voucher and finance register for the general records office along with the

AP agent journalists a check for the finance and afterward stores the check in the

account that is the simplest at the Bank.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 8

|

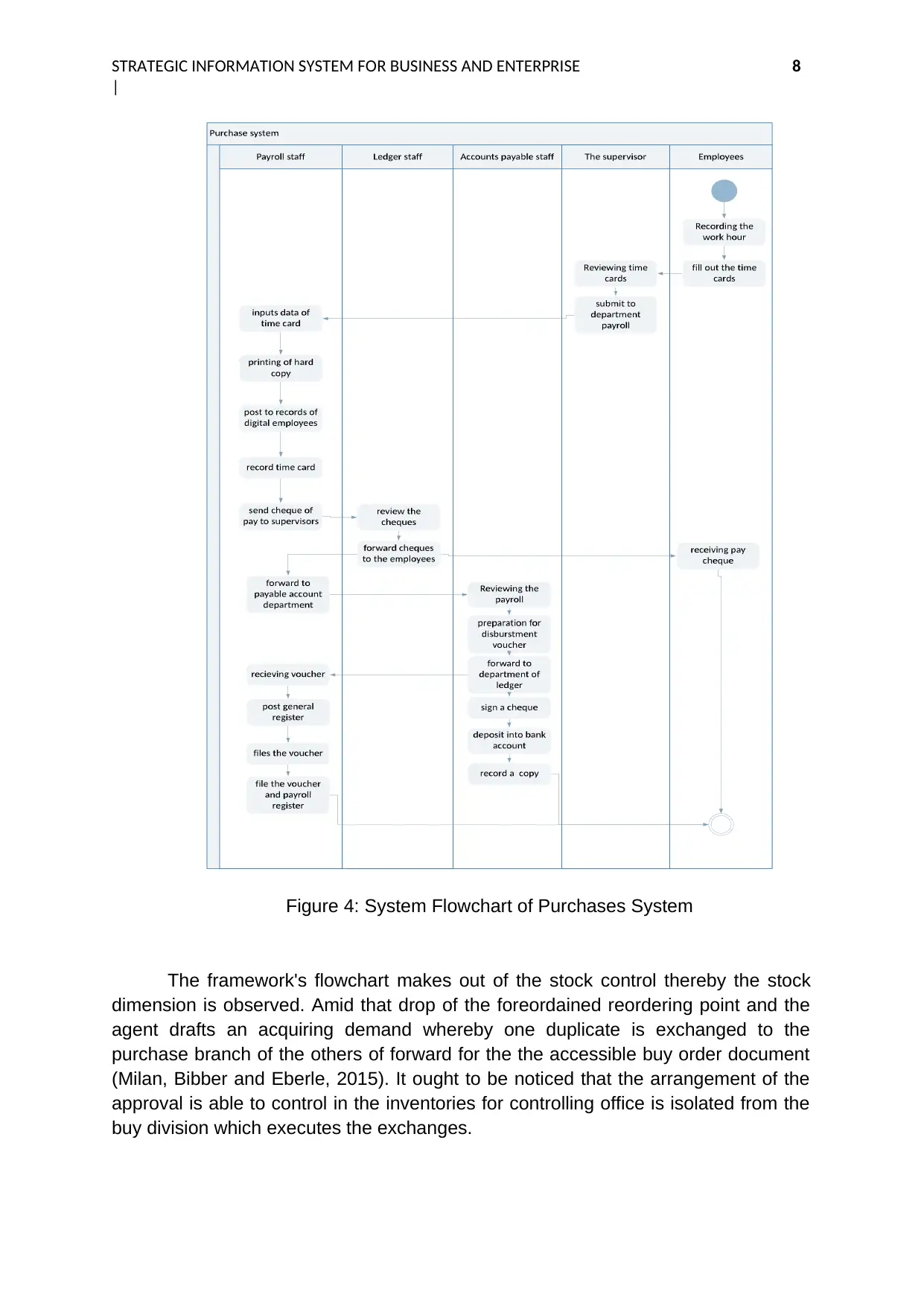

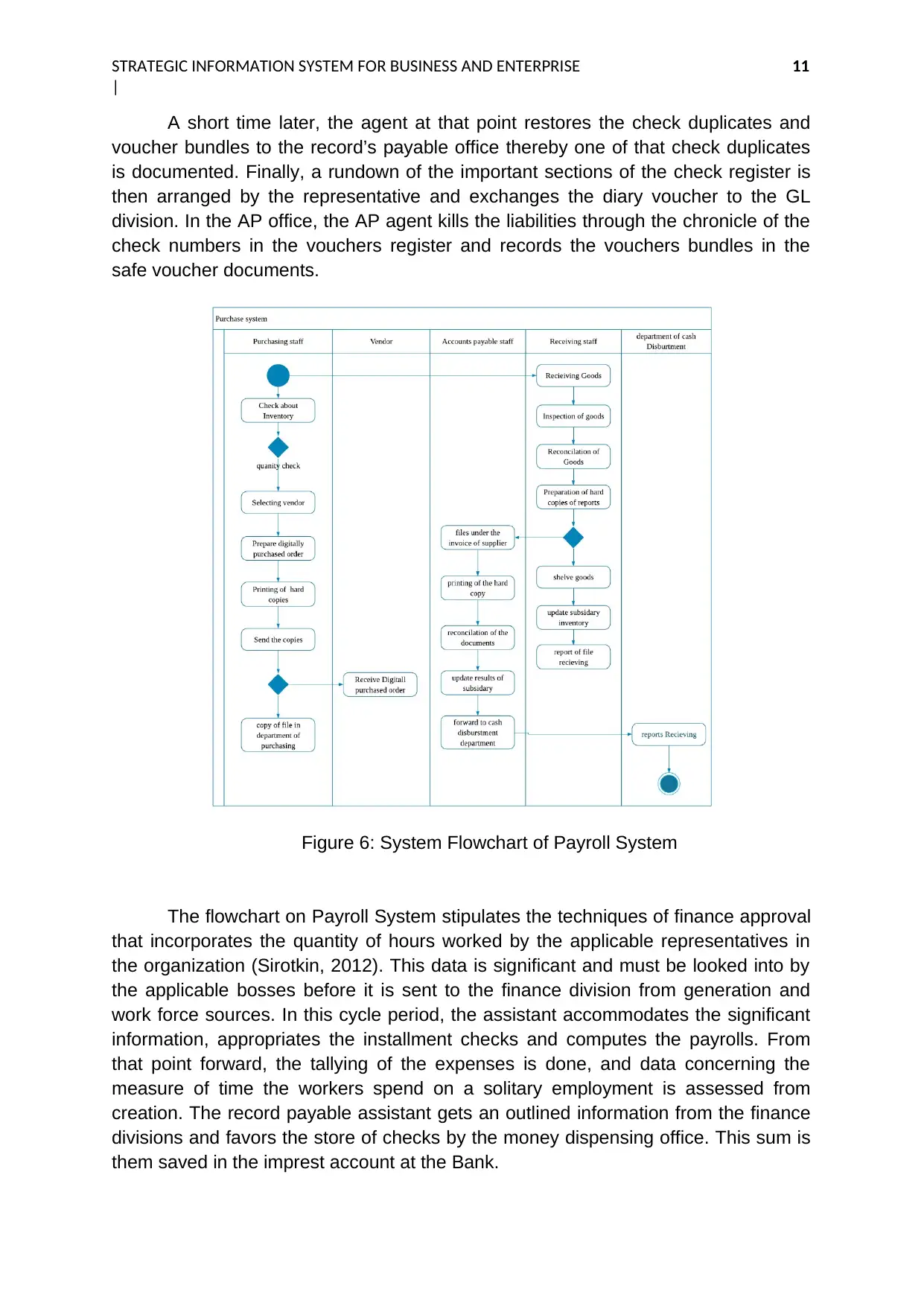

Figure 4: System Flowchart of Purchases System

The framework's flowchart makes out of the stock control thereby the stock

dimension is observed. Amid that drop of the foreordained reordering point and the

agent drafts an acquiring demand whereby one duplicate is exchanged to the

purchase branch of the others of forward for the the accessible buy order document

(Milan, Bibber and Eberle, 2015). It ought to be noticed that the arrangement of the

approval is able to control in the inventories for controlling office is isolated from the

buy division which executes the exchanges.

|

Figure 4: System Flowchart of Purchases System

The framework's flowchart makes out of the stock control thereby the stock

dimension is observed. Amid that drop of the foreordained reordering point and the

agent drafts an acquiring demand whereby one duplicate is exchanged to the

purchase branch of the others of forward for the the accessible buy order document

(Milan, Bibber and Eberle, 2015). It ought to be noticed that the arrangement of the

approval is able to control in the inventories for controlling office is isolated from the

buy division which executes the exchanges.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 9

|

This procedure pursues the buy demand, arranging by merchants and

readiness of that PO for each of the sellers in the obtaining division stock dimension

is observed (Zhang and Fang, 2013). Amid this stage, two of the duplicates of the

buy orders are exchanged to the seller as well as the PO duplicate is exchanged to

the stock control for recording with accessible buying demand. The merchandise that

start from the sellers are then accommodated with the visually impaired duplicates of

that PO. At the point, the assessment process and physical checking is finished, the

getting representative at that point gets ready distinctive reports that express the

condition along with the amount of the inventories. One of that duplicates of the

getting reports that it is forwarded to the stock division went with the physical stock

(Nakamoto, 2017). The rest of the duplicate is exchanged to the buy office and the

assistant is then ready to accommodate it with the PO that is accessible.

In the records payable office, the agent gets the arriving receipt whereby the

data is accommodated with the accessible pending archive document. From there

on, one record of that important exchanges in the diary buys and focuses, including

the backup record of AP is then arranged. This pursues a record of the liabilities,

thereby the agent sends the archives sourced, accepting reports and accessible

voucher payable documents. Amid the stage, that is an update of the computerized

record payable backups records which is done, including the controls of the AP

account as well as the inventories control accounts in the DL division from the work

station. Finally, the representative exchanges the solicitations, PO duplicates and

getting reports related to the money dispensing office.

Cash disbursement department:

|

This procedure pursues the buy demand, arranging by merchants and

readiness of that PO for each of the sellers in the obtaining division stock dimension

is observed (Zhang and Fang, 2013). Amid this stage, two of the duplicates of the

buy orders are exchanged to the seller as well as the PO duplicate is exchanged to

the stock control for recording with accessible buying demand. The merchandise that

start from the sellers are then accommodated with the visually impaired duplicates of

that PO. At the point, the assessment process and physical checking is finished, the

getting representative at that point gets ready distinctive reports that express the

condition along with the amount of the inventories. One of that duplicates of the

getting reports that it is forwarded to the stock division went with the physical stock

(Nakamoto, 2017). The rest of the duplicate is exchanged to the buy office and the

assistant is then ready to accommodate it with the PO that is accessible.

In the records payable office, the agent gets the arriving receipt whereby the

data is accommodated with the accessible pending archive document. From there

on, one record of that important exchanges in the diary buys and focuses, including

the backup record of AP is then arranged. This pursues a record of the liabilities,

thereby the agent sends the archives sourced, accepting reports and accessible

voucher payable documents. Amid the stage, that is an update of the computerized

record payable backups records which is done, including the controls of the AP

account as well as the inventories control accounts in the DL division from the work

station. Finally, the representative exchanges the solicitations, PO duplicates and

getting reports related to the money dispensing office.

Cash disbursement department:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 10

|

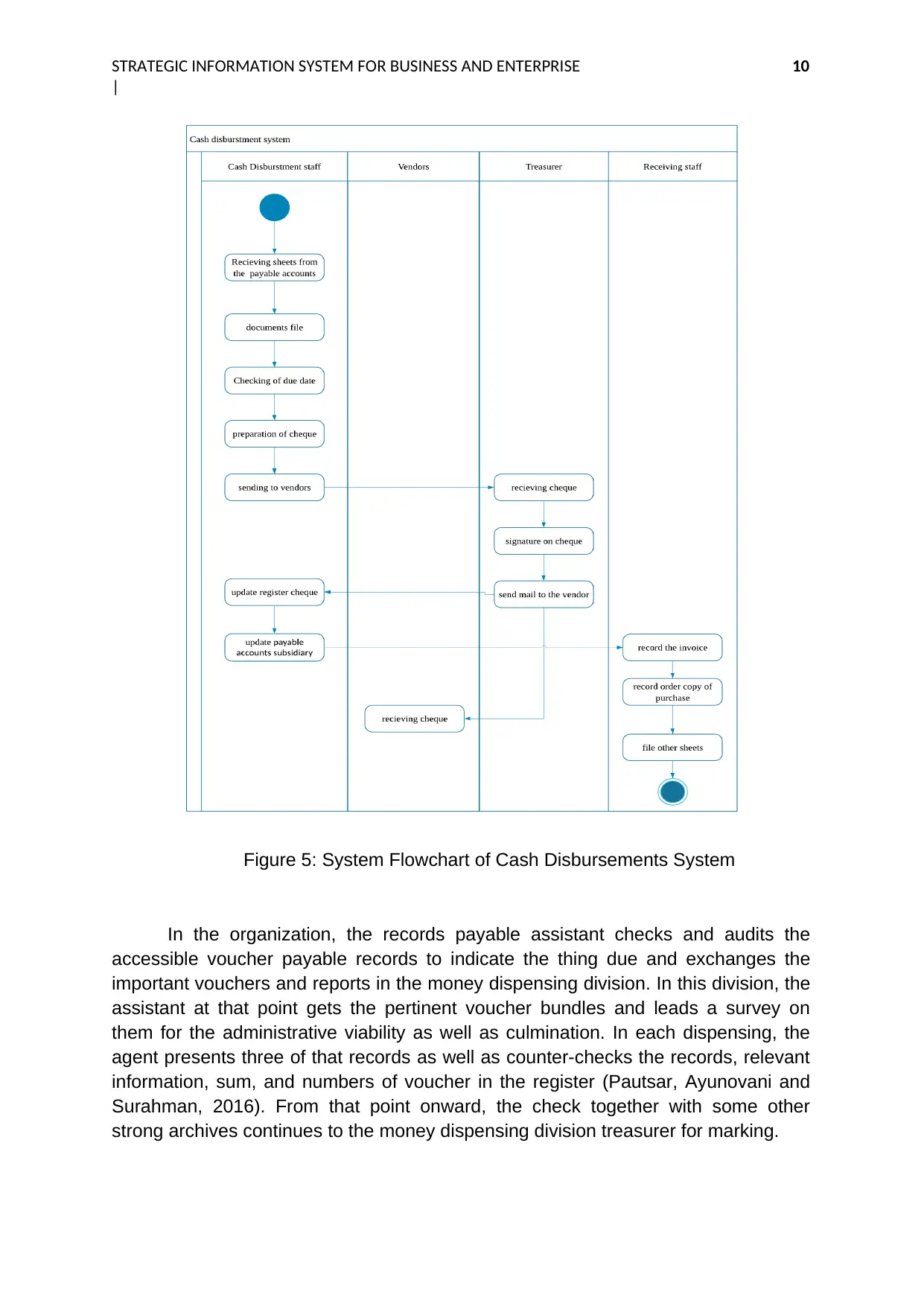

Figure 5: System Flowchart of Cash Disbursements System

In the organization, the records payable assistant checks and audits the

accessible voucher payable records to indicate the thing due and exchanges the

important vouchers and reports in the money dispensing division. In this division, the

assistant at that point gets the pertinent voucher bundles and leads a survey on

them for the administrative viability as well as culmination. In each dispensing, the

agent presents three of that records as well as counter-checks the records, relevant

information, sum, and numbers of voucher in the register (Pautsar, Ayunovani and

Surahman, 2016). From that point onward, the check together with some other

strong archives continues to the money dispensing division treasurer for marking.

|

Figure 5: System Flowchart of Cash Disbursements System

In the organization, the records payable assistant checks and audits the

accessible voucher payable records to indicate the thing due and exchanges the

important vouchers and reports in the money dispensing division. In this division, the

assistant at that point gets the pertinent voucher bundles and leads a survey on

them for the administrative viability as well as culmination. In each dispensing, the

agent presents three of that records as well as counter-checks the records, relevant

information, sum, and numbers of voucher in the register (Pautsar, Ayunovani and

Surahman, 2016). From that point onward, the check together with some other

strong archives continues to the money dispensing division treasurer for marking.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE 11

|

A short time later, the agent at that point restores the check duplicates and

voucher bundles to the record’s payable office thereby one of that check duplicates

is documented. Finally, a rundown of the important sections of the check register is

then arranged by the representative and exchanges the diary voucher to the GL

division. In the AP office, the AP agent kills the liabilities through the chronicle of the

check numbers in the vouchers register and records the vouchers bundles in the

safe voucher documents.

Figure 6: System Flowchart of Payroll System

The flowchart on Payroll System stipulates the techniques of finance approval

that incorporates the quantity of hours worked by the applicable representatives in

the organization (Sirotkin, 2012). This data is significant and must be looked into by

the applicable bosses before it is sent to the finance division from generation and

work force sources. In this cycle period, the assistant accommodates the significant

information, appropriates the installment checks and computes the payrolls. From

that point forward, the tallying of the expenses is done, and data concerning the

measure of time the workers spend on a solitary employment is assessed from

creation. The record payable assistant gets an outlined information from the finance

divisions and favors the store of checks by the money dispensing office. This sum is

them saved in the imprest account at the Bank.

|

A short time later, the agent at that point restores the check duplicates and

voucher bundles to the record’s payable office thereby one of that check duplicates

is documented. Finally, a rundown of the important sections of the check register is

then arranged by the representative and exchanges the diary voucher to the GL

division. In the AP office, the AP agent kills the liabilities through the chronicle of the

check numbers in the vouchers register and records the vouchers bundles in the

safe voucher documents.

Figure 6: System Flowchart of Payroll System

The flowchart on Payroll System stipulates the techniques of finance approval

that incorporates the quantity of hours worked by the applicable representatives in

the organization (Sirotkin, 2012). This data is significant and must be looked into by

the applicable bosses before it is sent to the finance division from generation and

work force sources. In this cycle period, the assistant accommodates the significant

information, appropriates the installment checks and computes the payrolls. From

that point forward, the tallying of the expenses is done, and data concerning the

measure of time the workers spend on a solitary employment is assessed from

creation. The record payable assistant gets an outlined information from the finance

divisions and favors the store of checks by the money dispensing office. This sum is

them saved in the imprest account at the Bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.