Strategic Information Systems Analysis for Bell Studio (HI5019)

VerifiedAdded on 2023/01/18

|19

|3341

|95

Case Study

AI Summary

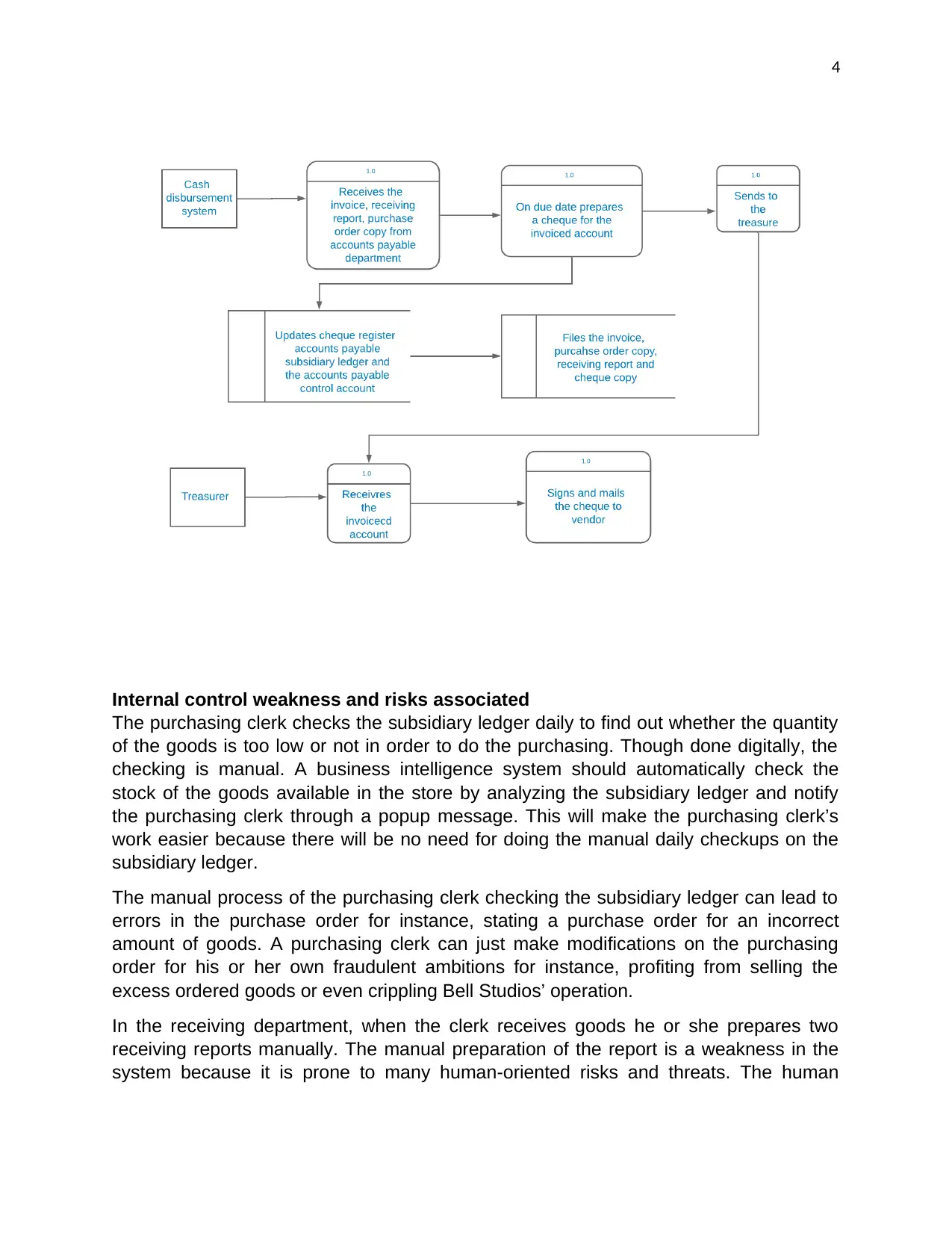

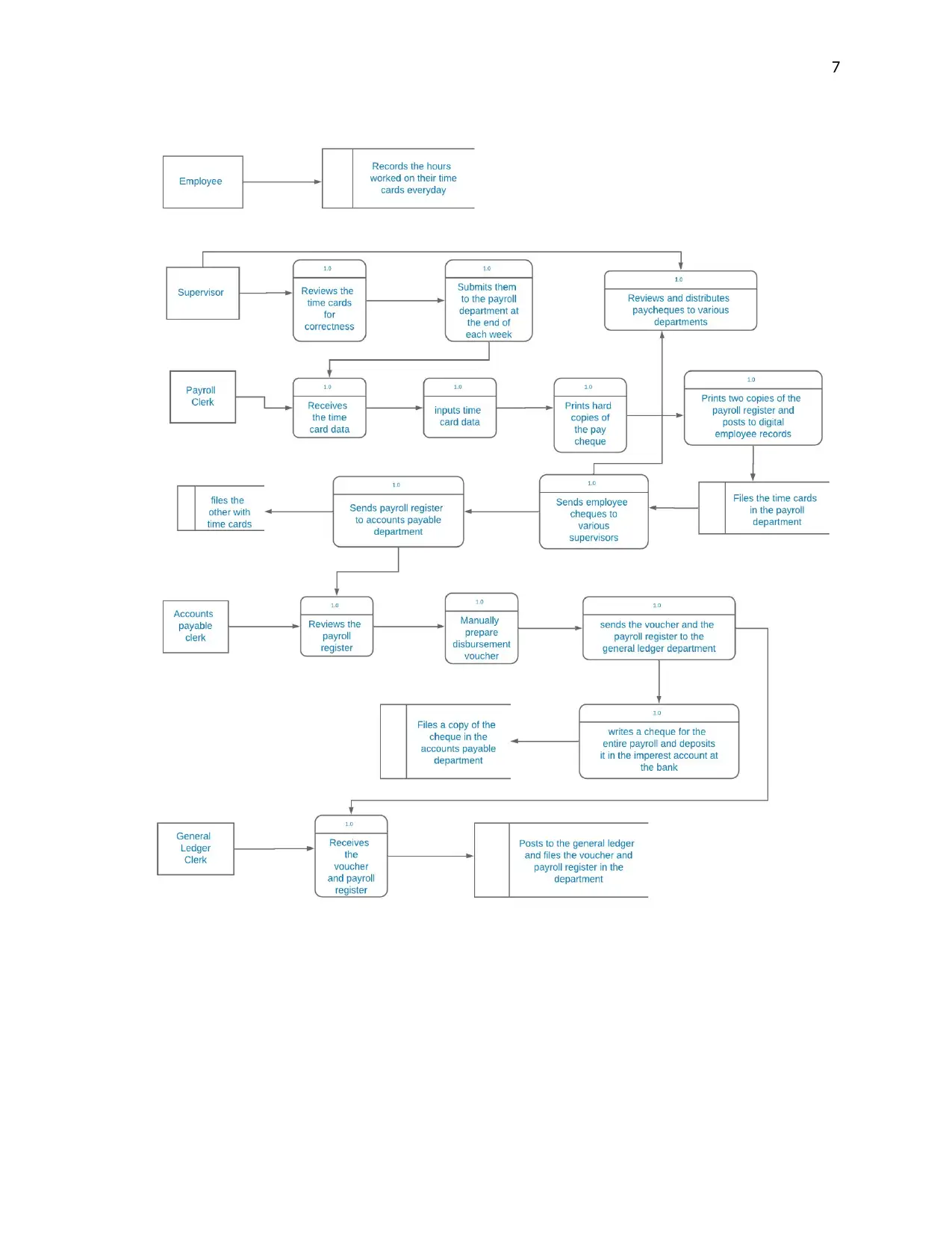

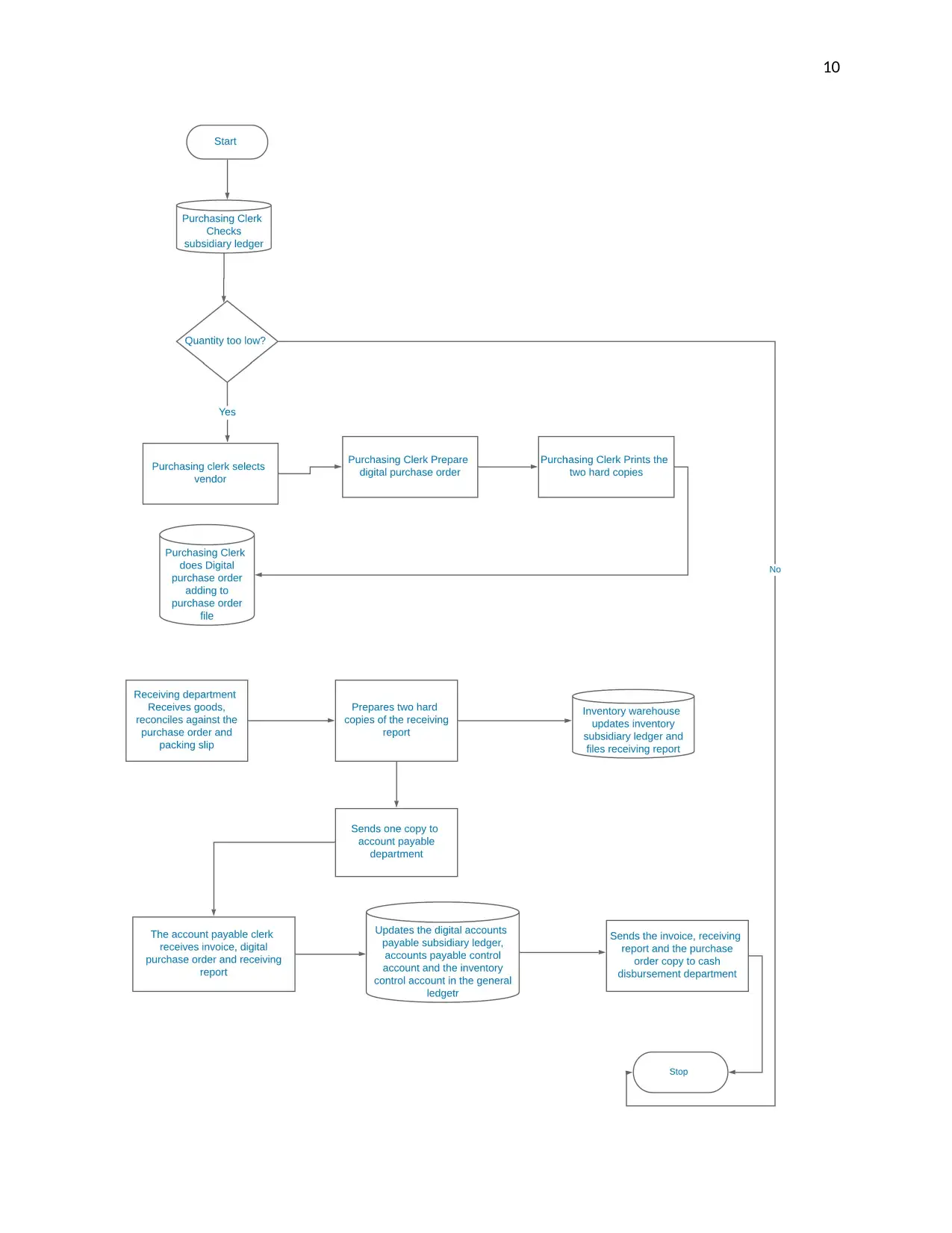

This report presents a comprehensive analysis of Bell Studio's expenditure cycle, focusing on the purchasing, cash disbursement, and payroll systems. It utilizes data flow diagrams and system flowcharts to illustrate the processes and identifies internal control weaknesses, such as manual data entry, lack of automated alerts, and inadequate data storage. The report thoroughly examines the associated risks, including errors, fraud, and data loss, and proposes remedies such as implementing a business intelligence system, centralized database storage, and improved employee attendance tracking. The analysis also includes detailed system flowcharts for the purchases, cash disbursement, and payroll systems, along with identified internal control weaknesses and recommended solutions for each system to improve operational efficiency and reduce risks.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.