Strategic Information Systems: HI5019 Report on Business Processes

VerifiedAdded on 2023/01/20

|23

|3354

|87

Report

AI Summary

This report provides a comprehensive overview of strategic information systems within a business context. It delves into the intricacies of transaction cycles, including payroll, purchasing, sales, and financing, highlighting their significance in operational efficiency. The report examines financial reporting, detailing its components, objectives, and importance in decision-making. It explores management reporting systems, outlining their role in providing timely information for effective business operations and the fundamentals of an effective system. The report also covers e-commerce, discussing its technologies, advantages, and impact on business. Furthermore, it analyzes internal control weaknesses within various systems, such as purchasing, cash disbursement, and payroll, and identifies associated risks like fraud and misappropriation of resources. The report also discusses the importance of separation of duties, authorization, asset security, and review and reconciliation processes to mitigate these risks. The report concludes by emphasizing the critical role of strategic information systems in business success.

Report

Table of Contents

Report................................................................................................................................1

Executive Summary...........................................................................................................1

Transaction cycles.............................................................................................................3

Types of transaction cycles:...........................................................................................3

Financial Reporting............................................................................................................3

Financial reporting components:....................................................................................3

Objective of Financial Reporting....................................................................................3

Importance of Financial Reporting.................................................................................3

Management Reporting System........................................................................................4

Reasons for acquiring management reporting system..................................................4

Fundamentals of an effective management reporting system.......................................4

E-commerce.......................................................................................................................4

E-commerce technology.................................................................................................5

Data flow diagram of purchases system...........................................................................6

Data flow diagram of cash disbursements system............................................................7

Data flow diagram of payroll system..................................................................................8

System flowchart of purchases system.............................................................................9

System flowchart of cash disbursements system............................................................10

System flowchart of payroll system.................................................................................11

Internal control weakness in each system and risks associated with the identified

weakness.........................................................................................................................12

1. Purchasing system:...............................................................................................12

Table of Contents

Report................................................................................................................................1

Executive Summary...........................................................................................................1

Transaction cycles.............................................................................................................3

Types of transaction cycles:...........................................................................................3

Financial Reporting............................................................................................................3

Financial reporting components:....................................................................................3

Objective of Financial Reporting....................................................................................3

Importance of Financial Reporting.................................................................................3

Management Reporting System........................................................................................4

Reasons for acquiring management reporting system..................................................4

Fundamentals of an effective management reporting system.......................................4

E-commerce.......................................................................................................................4

E-commerce technology.................................................................................................5

Data flow diagram of purchases system...........................................................................6

Data flow diagram of cash disbursements system............................................................7

Data flow diagram of payroll system..................................................................................8

System flowchart of purchases system.............................................................................9

System flowchart of cash disbursements system............................................................10

System flowchart of payroll system.................................................................................11

Internal control weakness in each system and risks associated with the identified

weakness.........................................................................................................................12

1. Purchasing system:...............................................................................................12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Separation of duties...........................................................................................12

2. Authorization.......................................................................................................12

3. Assets security...................................................................................................12

4. Review and reconciliation...................................................................................13

2. Cash System..........................................................................................................13

1. Accountability.....................................................................................................13

2. Security of assets...............................................................................................14

3. Review and reconciliation...................................................................................14

3. Payroll System.......................................................................................................14

1. Separation of duties...........................................................................................14

2. Authorization.......................................................................................................15

3. Security of assets...............................................................................................15

4. Review and reconciliation...................................................................................16

Conclusion.......................................................................................................................16

References.......................................................................................................................17

2. Authorization.......................................................................................................12

3. Assets security...................................................................................................12

4. Review and reconciliation...................................................................................13

2. Cash System..........................................................................................................13

1. Accountability.....................................................................................................13

2. Security of assets...............................................................................................14

3. Review and reconciliation...................................................................................14

3. Payroll System.......................................................................................................14

1. Separation of duties...........................................................................................14

2. Authorization.......................................................................................................15

3. Security of assets...............................................................................................15

4. Review and reconciliation...................................................................................16

Conclusion.......................................................................................................................16

References.......................................................................................................................17

Executive Summary

This detailed report contains essential concepts about strategic information system for

business and enterprise. Some of these concepts that are explained include transaction

cycles, financial reporting, management reporting systems, e-commerce, and various

internal controls weaknesses and risks. In every business identifying transaction cycles

and particular tasks within the cycles, are very important to determine the efficiency and

effectiveness of a business and every report of each transaction cycle play a role in

business efficiency. For financial reporting, the department in charge should provide

financial reports and statements accurately and timely thus enabling better decision

making. In the business or an enterprise, there must be a way in which information is

provided to different personnel at various management levels in order to plan, control,

and make decisions which will have a positive effect to the company. Due to the

advancement in technology more so internet, there is increased urge in increasing the

delivery speed in the business where e-commerce that relies on the internet

accessibility has such feature hence the need of e-commerce in businesses. The

Internal Control processes within a business or organization are put in place to make

sure information is accurate reliable, on time, the organization assets are well protected,

laws and regulations are adhered to, and resources are used efficiently and in an

economical way whereby they still have weaknesses and risks. Internal controls basic

intentions are irregularities and errors prevention, problems identification, and ensure

that actions are taken correctively.

This detailed report contains essential concepts about strategic information system for

business and enterprise. Some of these concepts that are explained include transaction

cycles, financial reporting, management reporting systems, e-commerce, and various

internal controls weaknesses and risks. In every business identifying transaction cycles

and particular tasks within the cycles, are very important to determine the efficiency and

effectiveness of a business and every report of each transaction cycle play a role in

business efficiency. For financial reporting, the department in charge should provide

financial reports and statements accurately and timely thus enabling better decision

making. In the business or an enterprise, there must be a way in which information is

provided to different personnel at various management levels in order to plan, control,

and make decisions which will have a positive effect to the company. Due to the

advancement in technology more so internet, there is increased urge in increasing the

delivery speed in the business where e-commerce that relies on the internet

accessibility has such feature hence the need of e-commerce in businesses. The

Internal Control processes within a business or organization are put in place to make

sure information is accurate reliable, on time, the organization assets are well protected,

laws and regulations are adhered to, and resources are used efficiently and in an

economical way whereby they still have weaknesses and risks. Internal controls basic

intentions are irregularities and errors prevention, problems identification, and ensure

that actions are taken correctively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Strategic information systems implementation in business strategies expose a business

to better opportunities. These strategies may be about financial reporting, e-commerce

or even transaction cycles strategies which affect business growth and also internal

control practices should also be considered and if they are not considered there are

risks associated with them. Some of these strategies and internal control practices are

discussed below:

Transaction cycles

Basically, transaction cycles are the interlacing transaction of a business or businesses.

These cycles may be separated in accordance with particular functions such as

purchases, payments, finances, payroll or sales.

Types of transaction cycles:

1. Payroll cycle. This is whereby a business handles everything about employee

payments. Some of the functions of this cycle are: Issuing payment cheques,

taxes deductions, recording of the time of every employee, overtime worked

hours verification

2. Purchasing cycle. This type of cycle is where the business deals with the order

purchases form different and convenient suppliers. Supplier payment and

receiving of goods.

3. Sales cycle: It handles the orders from the customers, review and corrects it.

4. Financing cycle.

Financial Reporting

Financial reporting is a process of revealing financial information of a business over a

particular period of time to the stakeholders (creditors, investors, government) where

this information is all about financial status and performance of the business/ Mostly,

financial reporting is done quarterly or annually.

Strategic information systems implementation in business strategies expose a business

to better opportunities. These strategies may be about financial reporting, e-commerce

or even transaction cycles strategies which affect business growth and also internal

control practices should also be considered and if they are not considered there are

risks associated with them. Some of these strategies and internal control practices are

discussed below:

Transaction cycles

Basically, transaction cycles are the interlacing transaction of a business or businesses.

These cycles may be separated in accordance with particular functions such as

purchases, payments, finances, payroll or sales.

Types of transaction cycles:

1. Payroll cycle. This is whereby a business handles everything about employee

payments. Some of the functions of this cycle are: Issuing payment cheques,

taxes deductions, recording of the time of every employee, overtime worked

hours verification

2. Purchasing cycle. This type of cycle is where the business deals with the order

purchases form different and convenient suppliers. Supplier payment and

receiving of goods.

3. Sales cycle: It handles the orders from the customers, review and corrects it.

4. Financing cycle.

Financial Reporting

Financial reporting is a process of revealing financial information of a business over a

particular period of time to the stakeholders (creditors, investors, government) where

this information is all about financial status and performance of the business/ Mostly,

financial reporting is done quarterly or annually.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In every department f a business or organization records and reports about their

financial state to stakeholders. Most of the departments' functions may be dependent or

interdependent where they are all linked to the finance department. So, Financial

Reporting is the very essential and critical activity of any business or company that is

either making a profit or not. (Elliott and Elliott, 2009)

Financial reporting components:

1. Finance statements which involve loss accounts, such flow statements, balance

sheet, profit accounts

2. Financial statements’ notes

3. Financial reports that are quarterly and annually

4. If it is a public company, management analysis and discussion are done

Objective of Financial Reporting

Financial reporting has a major objective which is providing financial information of a

business which states the financial position, financial performance, and any financial

change to help in making decisions.

Importance of Financial Reporting

1) Assist the business to agree and do according to the regulatory requirements

where quarterly or annual reports should be published in the business or

company is listed.

2) It enhances the auditing of financial statements in a company

3) Enables the stakeholders to easily plan, analyze and make financial decisions

effectively.

4) It enables the business to easily identify means of getting capital.

5) If a company has well-furnished financial statements and reports, it is able to bid,

contract labor, etc.

financial state to stakeholders. Most of the departments' functions may be dependent or

interdependent where they are all linked to the finance department. So, Financial

Reporting is the very essential and critical activity of any business or company that is

either making a profit or not. (Elliott and Elliott, 2009)

Financial reporting components:

1. Finance statements which involve loss accounts, such flow statements, balance

sheet, profit accounts

2. Financial statements’ notes

3. Financial reports that are quarterly and annually

4. If it is a public company, management analysis and discussion are done

Objective of Financial Reporting

Financial reporting has a major objective which is providing financial information of a

business which states the financial position, financial performance, and any financial

change to help in making decisions.

Importance of Financial Reporting

1) Assist the business to agree and do according to the regulatory requirements

where quarterly or annual reports should be published in the business or

company is listed.

2) It enhances the auditing of financial statements in a company

3) Enables the stakeholders to easily plan, analyze and make financial decisions

effectively.

4) It enables the business to easily identify means of getting capital.

5) If a company has well-furnished financial statements and reports, it is able to bid,

contract labor, etc.

Management Reporting System

A management reporting system is a phase in the control system under management

that provides information to the business. This information includes various statements

and reports in the business (Antonelli, de Almeida, Colauto, & Longhi, 2014). These

management systems help in making sure that information is timely for the effective

running of activities thus making them very important in any business.

Reasons for acquiring management reporting system

Management reporting systems assist getting data that is required by executive such as

managers to make decisions in a business. The data may be about finance, the number

of employees, salaries customers or clients, products or services, business assets,

performance in investments, etc. Management reporting has a wide scope. Frequent

reports requirement for decision making and analyzing the trends in business. It helps to

eliminate data redundancy while may result in an error (Mancini, Dameri, & Bonollo,

2016).

Fundamentals of an effective management reporting system

An effective management system should generate better reports which are timely,

proper information flow, and format used should be correct and easy to understand

Flexibility-The management reporting system should be flexible in such a way

that it responds to the requirements set and show some insights when standards

that are predefined are deviated from. If management reporting system is

localized, it simplifies the processes to be carried out.

Accuracy of the system is expected. In terms of reporting, there shouldn't be any

inconsistency or discrepancy. Due to the way the system is involved in critical

company information or results, it's a must for it to be accurate.

Cost efficiency. It shouldn't be hard for assembly of reports where they should

also provide acceptable cost justification and with a better cost efficiency

A management reporting system is a phase in the control system under management

that provides information to the business. This information includes various statements

and reports in the business (Antonelli, de Almeida, Colauto, & Longhi, 2014). These

management systems help in making sure that information is timely for the effective

running of activities thus making them very important in any business.

Reasons for acquiring management reporting system

Management reporting systems assist getting data that is required by executive such as

managers to make decisions in a business. The data may be about finance, the number

of employees, salaries customers or clients, products or services, business assets,

performance in investments, etc. Management reporting has a wide scope. Frequent

reports requirement for decision making and analyzing the trends in business. It helps to

eliminate data redundancy while may result in an error (Mancini, Dameri, & Bonollo,

2016).

Fundamentals of an effective management reporting system

An effective management system should generate better reports which are timely,

proper information flow, and format used should be correct and easy to understand

Flexibility-The management reporting system should be flexible in such a way

that it responds to the requirements set and show some insights when standards

that are predefined are deviated from. If management reporting system is

localized, it simplifies the processes to be carried out.

Accuracy of the system is expected. In terms of reporting, there shouldn't be any

inconsistency or discrepancy. Due to the way the system is involved in critical

company information or results, it's a must for it to be accurate.

Cost efficiency. It shouldn't be hard for assembly of reports where they should

also provide acceptable cost justification and with a better cost efficiency

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analysis, the business is able to make a decision whether to adopt the

management reporting system or not.

Reports which are well-detailed help the management to make sound decisions

The mode of report delivery whether automated of manual also critical matter on

the success of the management reporting system.

The level of consistency that a management reporting system that should

maintain should be very high. (Bourgeois ,David, 2014).

E-commerce

E-commerce the use of the Internet and the Web to transact business. More formally,

digitally enabled commercial transactions between and among organizations and

individuals. As the internet is becoming more accessible, the growth of e-commerce

increases and businesses and organizations are taking this advantage.

E-commerce technology

Is ubiquitous—it is available just about everywhere, at all times, making it

possible to shop from your desktop, at home, at work, or even from your car.

Has global reach, permitting commercial transactions to cross-cultural and

national boundaries far more conveniently and cost-effectively than is true in

traditional commerce (Bernroider & Mitlohner, 2015).

Operates according to universal standards shared by all nations around the

world. In contrast, most traditional commerce technologies differ from one nation

to the next.

Provides information richness, which refers to the complexity and content of a

message. It enables an online merchant to deliver marketing messages with text,

video, and audio to an audience of millions, in a way not possible with traditional

commerce technologies such as radio, television, or magazines.

management reporting system or not.

Reports which are well-detailed help the management to make sound decisions

The mode of report delivery whether automated of manual also critical matter on

the success of the management reporting system.

The level of consistency that a management reporting system that should

maintain should be very high. (Bourgeois ,David, 2014).

E-commerce

E-commerce the use of the Internet and the Web to transact business. More formally,

digitally enabled commercial transactions between and among organizations and

individuals. As the internet is becoming more accessible, the growth of e-commerce

increases and businesses and organizations are taking this advantage.

E-commerce technology

Is ubiquitous—it is available just about everywhere, at all times, making it

possible to shop from your desktop, at home, at work, or even from your car.

Has global reach, permitting commercial transactions to cross-cultural and

national boundaries far more conveniently and cost-effectively than is true in

traditional commerce (Bernroider & Mitlohner, 2015).

Operates according to universal standards shared by all nations around the

world. In contrast, most traditional commerce technologies differ from one nation

to the next.

Provides information richness, which refers to the complexity and content of a

message. It enables an online merchant to deliver marketing messages with text,

video, and audio to an audience of millions, in a way not possible with traditional

commerce technologies such as radio, television, or magazines.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Is interactive—it allows for two-way communication between merchant and

consumer and enables the merchant to engage a consumer in ways similar to a

face-to-face experience, but on a much more massive, global scale.

Increases information density (the total amount and quality of information

available to all market participants). Through Internet, there is efficient

information processing where it is timely and accurate. (Alewine, Allport, &Shen,

2016).

Permits personalization and customization. Merchants can target their marketing

messages to specific individuals by adjusting the message to a person’s name,

interests, and past purchases. Because of the increase in information density, a

great deal of information about the consumer’s past purchases and behavior can

be stored and used by online merchants. The result is a level of personalization

and customization unthinkable with existing commerce technologies. (Dallard,

Yuthas, 2013)

consumer and enables the merchant to engage a consumer in ways similar to a

face-to-face experience, but on a much more massive, global scale.

Increases information density (the total amount and quality of information

available to all market participants). Through Internet, there is efficient

information processing where it is timely and accurate. (Alewine, Allport, &Shen,

2016).

Permits personalization and customization. Merchants can target their marketing

messages to specific individuals by adjusting the message to a person’s name,

interests, and past purchases. Because of the increase in information density, a

great deal of information about the consumer’s past purchases and behavior can

be stored and used by online merchants. The result is a level of personalization

and customization unthinkable with existing commerce technologies. (Dallard,

Yuthas, 2013)

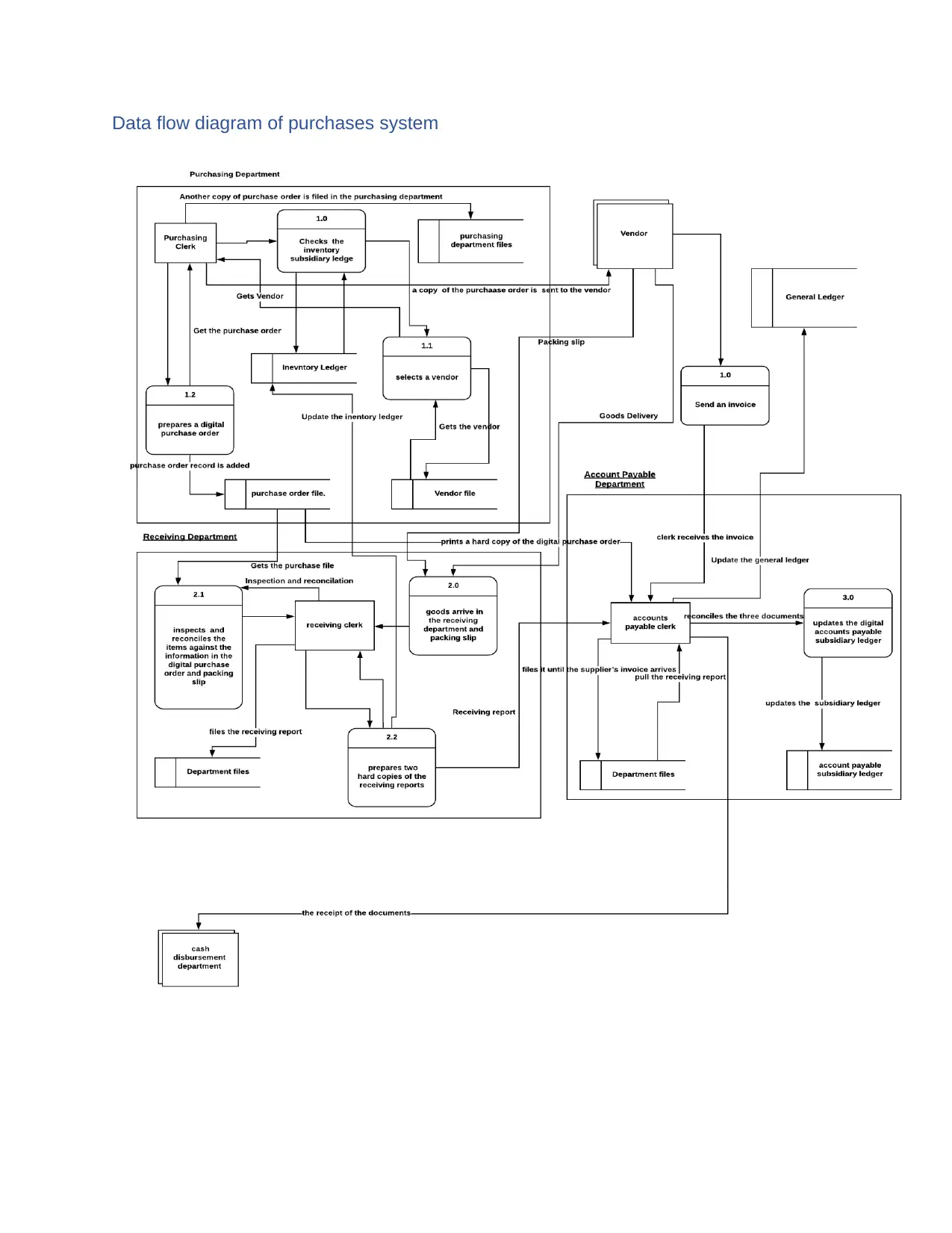

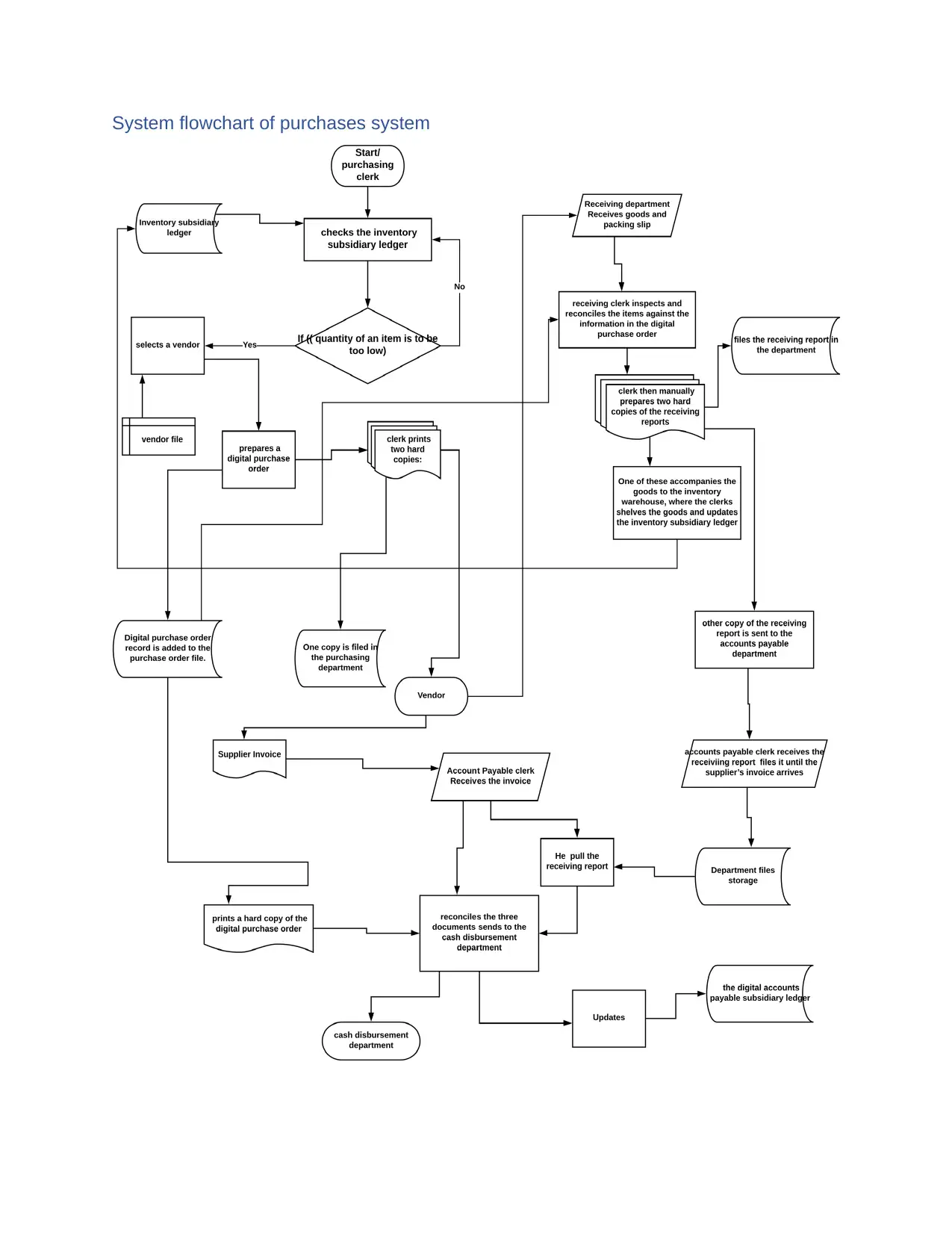

Data flow diagram of purchases system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

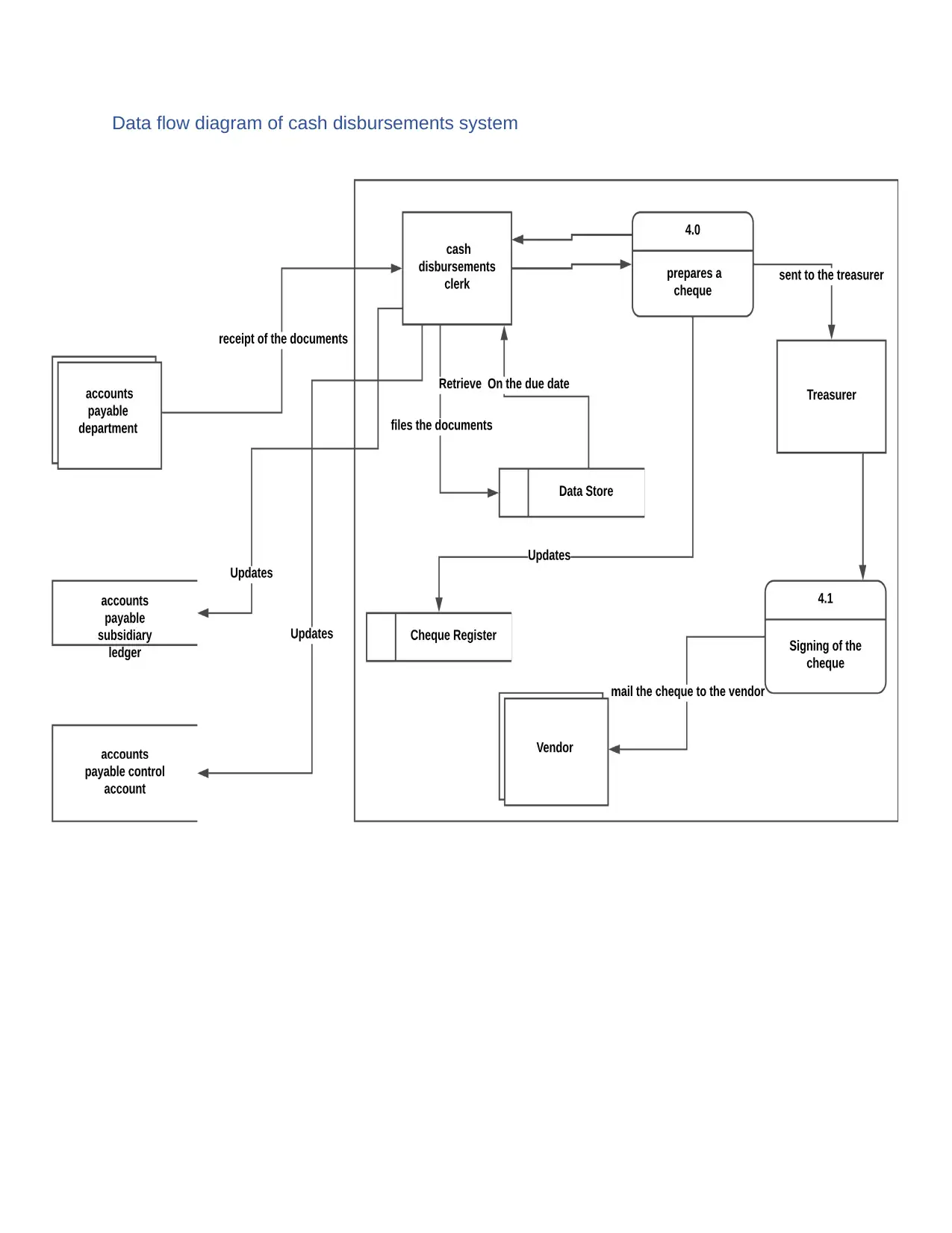

Data flow diagram of cash disbursements system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

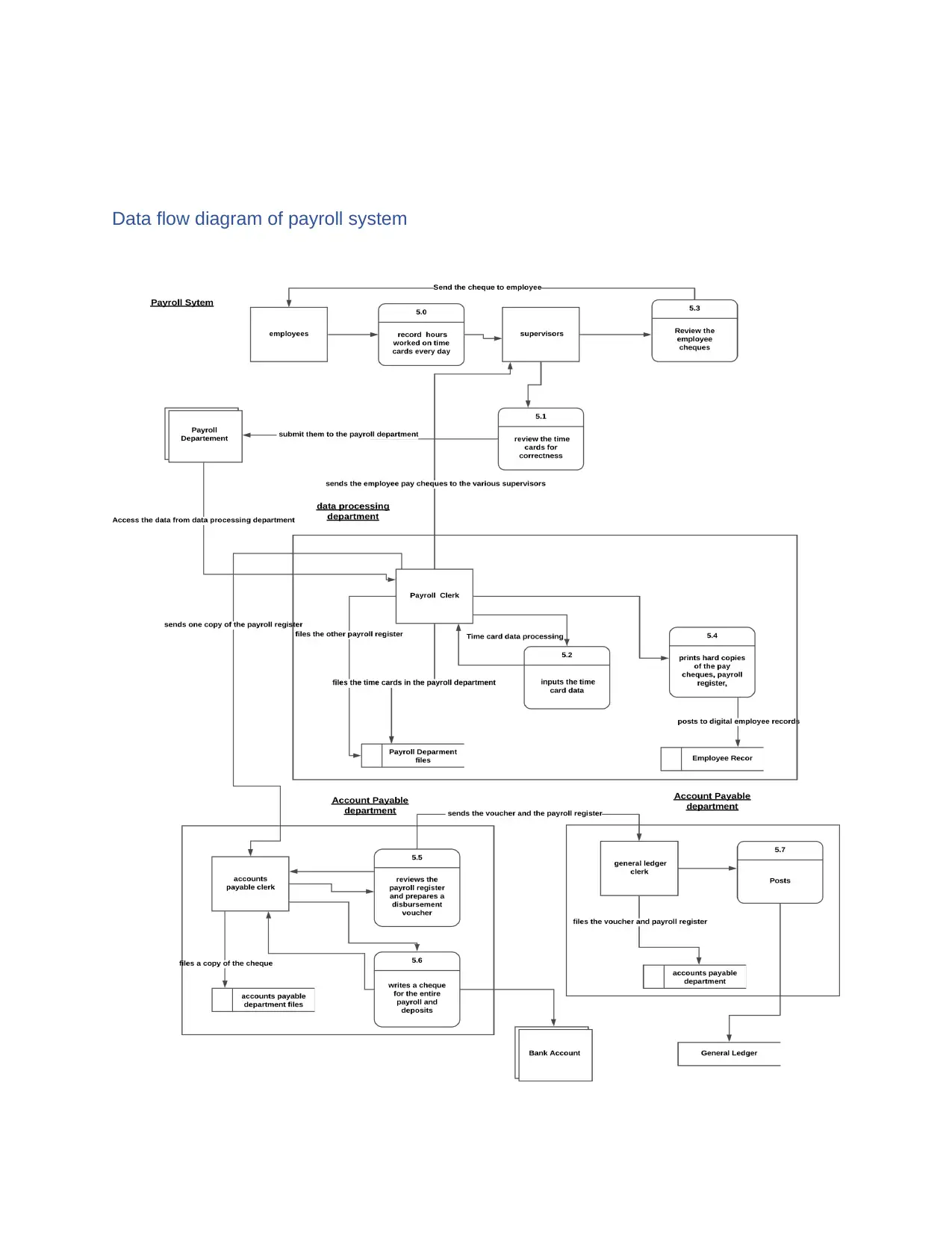

Data flow diagram of payroll system

System flowchart of purchases system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.