Strategic Management Accounting: Case Study and Analysis Report

VerifiedAdded on 2020/10/22

|9

|2163

|474

Report

AI Summary

This report focuses on strategic management accounting, exploring key concepts through case studies and financial analysis. It begins with an introduction to strategic management accounting and evaluates various case scenarios to enhance understanding of several accounting concepts. The report develops budgets, including fixed, flexible, and actual budgets, to determine variances for direct material and direct labor. It then analyzes different transfer pricing methods, comparing their advantages and disadvantages. The report examines accounting techniques such as balance scorecards and benchmarking and their suitable formats for the given scenario. The report also includes a columnar statement, subdivision of labor and material variances, and identification of potential causes of material and labor variances. The report concludes with the application of these concepts to a business solution company, CD Limited, and recommends improvements using benchmarking techniques.

Strategic Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 2...................................................................................................................................1

a. Columnar statement.................................................................................................................1

b. Sub division of labour and material variances........................................................................1

c. Identification of possible causes of material and labour variances.........................................1

QUESTION 3...................................................................................................................................1

QUESTION 4...................................................................................................................................3

(I) Balance score card..................................................................................................................3

(ii) Benchmarking.......................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDIX......................................................................................................................................7

a. Columnar statement.................................................................................................................7

b. Sub division of labour and material variances........................................................................7

INTRODUCTION...........................................................................................................................1

QUESTION 2...................................................................................................................................1

a. Columnar statement.................................................................................................................1

b. Sub division of labour and material variances........................................................................1

c. Identification of possible causes of material and labour variances.........................................1

QUESTION 3...................................................................................................................................1

QUESTION 4...................................................................................................................................3

(I) Balance score card..................................................................................................................3

(ii) Benchmarking.......................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDIX......................................................................................................................................7

a. Columnar statement.................................................................................................................7

b. Sub division of labour and material variances........................................................................7

INTRODUCTION

Strategic management accounting is branch of management accounting which focus on

the information i.e. related to the external factors of an organisation. This process combines

management information with strategic business objectives. In this project report, various case

scenario are evaluated in order to have a better understanding towards several accounting

concepts. Budgets such as fixed, flexible and actual are developed in order to ascertain variances

for direct material and direct labour. Two transfer pricing methods are evaluated along with their

advantages and disadvantages. The main aim of this project is to examine various accounting

techniques such as balance scorecard and benchmarking along with their suitable formate which

is appropriate for the given scenario.

QUESTION 2

a. Columnar statement

Refer appendix

b. Sub division of labour and material variances

Refer appendix

c. Identification of possible causes of material and labour variances

Causes of variation in material price, variance are fluctuating in market price, purchases

of non standardised material, delivery costs, emergency purchases etc. and cause of changes in

material usage ,variance are in quality of material i.e. low, careless handling, excessive wastage

etc. In this case, there is difference between the budgeted production quantity and actual

production quantity which is 2000 units and 18750 units. The price of material fluctuated from

24 to 23.4, possible causes of these changes in labour variance is due to abnormal overtime

below or above standard rates because of emergency operations. In this case, the labour hours

changes from 12 to 12.53, variable production overhead varies from 3 to 3.07.

QUESTION 3

Transfer pricing – Transfer pricing refers to the set of rules and regulations which are

developed for the pricing transactions within an organisation. According to this process, an

enterprise sets an arrangement for the prices of goods and services. This concept is used by

various companies in order to transfer products between different departments or subsidiary

1

Strategic management accounting is branch of management accounting which focus on

the information i.e. related to the external factors of an organisation. This process combines

management information with strategic business objectives. In this project report, various case

scenario are evaluated in order to have a better understanding towards several accounting

concepts. Budgets such as fixed, flexible and actual are developed in order to ascertain variances

for direct material and direct labour. Two transfer pricing methods are evaluated along with their

advantages and disadvantages. The main aim of this project is to examine various accounting

techniques such as balance scorecard and benchmarking along with their suitable formate which

is appropriate for the given scenario.

QUESTION 2

a. Columnar statement

Refer appendix

b. Sub division of labour and material variances

Refer appendix

c. Identification of possible causes of material and labour variances

Causes of variation in material price, variance are fluctuating in market price, purchases

of non standardised material, delivery costs, emergency purchases etc. and cause of changes in

material usage ,variance are in quality of material i.e. low, careless handling, excessive wastage

etc. In this case, there is difference between the budgeted production quantity and actual

production quantity which is 2000 units and 18750 units. The price of material fluctuated from

24 to 23.4, possible causes of these changes in labour variance is due to abnormal overtime

below or above standard rates because of emergency operations. In this case, the labour hours

changes from 12 to 12.53, variable production overhead varies from 3 to 3.07.

QUESTION 3

Transfer pricing – Transfer pricing refers to the set of rules and regulations which are

developed for the pricing transactions within an organisation. According to this process, an

enterprise sets an arrangement for the prices of goods and services. This concept is used by

various companies in order to transfer products between different departments or subsidiary

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

companies of the same parent organisation. Some of the methods of transfer pricing along with

their advantages and disadvantages are discussed below:

Market base transfer pricing

Market base transfer pricing is the methods of setting transfer prices that are aligned with

those that are found on the open market. It is an option to support the idea of decentralised

decision making. Market base transfer pricing explains why other type of transfer prices are

more likely to fulfil the desired function (Flamholtz, 2012).

Advantages: Top level managers are not disturbed with any kind of problem in the firm.

Managers have right to control the results and when managers have rights, they are more

satisfied with the work. Decentralised decision making help to provide better results due to

which company has right to set the transfer prices. This method provides competitive external

market so that the products can be modified accordingly. And it help to show the contribution of

each division of the company's profit. Market base transfer pricing does not allow any gains or

losses in efficiency of the selling division.

Disadvantages: There is no establish market price and this is very difficult to find the

perfect market pricing. Most of the time, market price is not appropriate because company is

spending less on promotional activities (Huizinga, 2012). When market base transfer pricing is

fixed then it will be difficult to shift the resources from low priority to high priority. Those

products which are highly specialised are not suitable for market base transfer pricing.

Full cost transfer prices

Full cost transfer pricing is a price arrangement method under which sum of direct

material costs, direct labour costs, overhead costs and selling costs which is determined in order

to ascertain profit margin.

Formula = Total production costs + selling and administrative costs + markup / number of units

expected to sell

Advantages: This method is considered as the most easiest technique of transfer pricing

as it has simple formula which can be calculated at any level of an organisation. With the help of

this method, organisation can earn more profit as the cost which are determined are said to be

more reliable and specific. This method facilitates the organisation by providing them benefits,

by which they can provide justification of their price increase to their clients (Jones, 2011).

2

their advantages and disadvantages are discussed below:

Market base transfer pricing

Market base transfer pricing is the methods of setting transfer prices that are aligned with

those that are found on the open market. It is an option to support the idea of decentralised

decision making. Market base transfer pricing explains why other type of transfer prices are

more likely to fulfil the desired function (Flamholtz, 2012).

Advantages: Top level managers are not disturbed with any kind of problem in the firm.

Managers have right to control the results and when managers have rights, they are more

satisfied with the work. Decentralised decision making help to provide better results due to

which company has right to set the transfer prices. This method provides competitive external

market so that the products can be modified accordingly. And it help to show the contribution of

each division of the company's profit. Market base transfer pricing does not allow any gains or

losses in efficiency of the selling division.

Disadvantages: There is no establish market price and this is very difficult to find the

perfect market pricing. Most of the time, market price is not appropriate because company is

spending less on promotional activities (Huizinga, 2012). When market base transfer pricing is

fixed then it will be difficult to shift the resources from low priority to high priority. Those

products which are highly specialised are not suitable for market base transfer pricing.

Full cost transfer prices

Full cost transfer pricing is a price arrangement method under which sum of direct

material costs, direct labour costs, overhead costs and selling costs which is determined in order

to ascertain profit margin.

Formula = Total production costs + selling and administrative costs + markup / number of units

expected to sell

Advantages: This method is considered as the most easiest technique of transfer pricing

as it has simple formula which can be calculated at any level of an organisation. With the help of

this method, organisation can earn more profit as the cost which are determined are said to be

more reliable and specific. This method facilitates the organisation by providing them benefits,

by which they can provide justification of their price increase to their clients (Jones, 2011).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

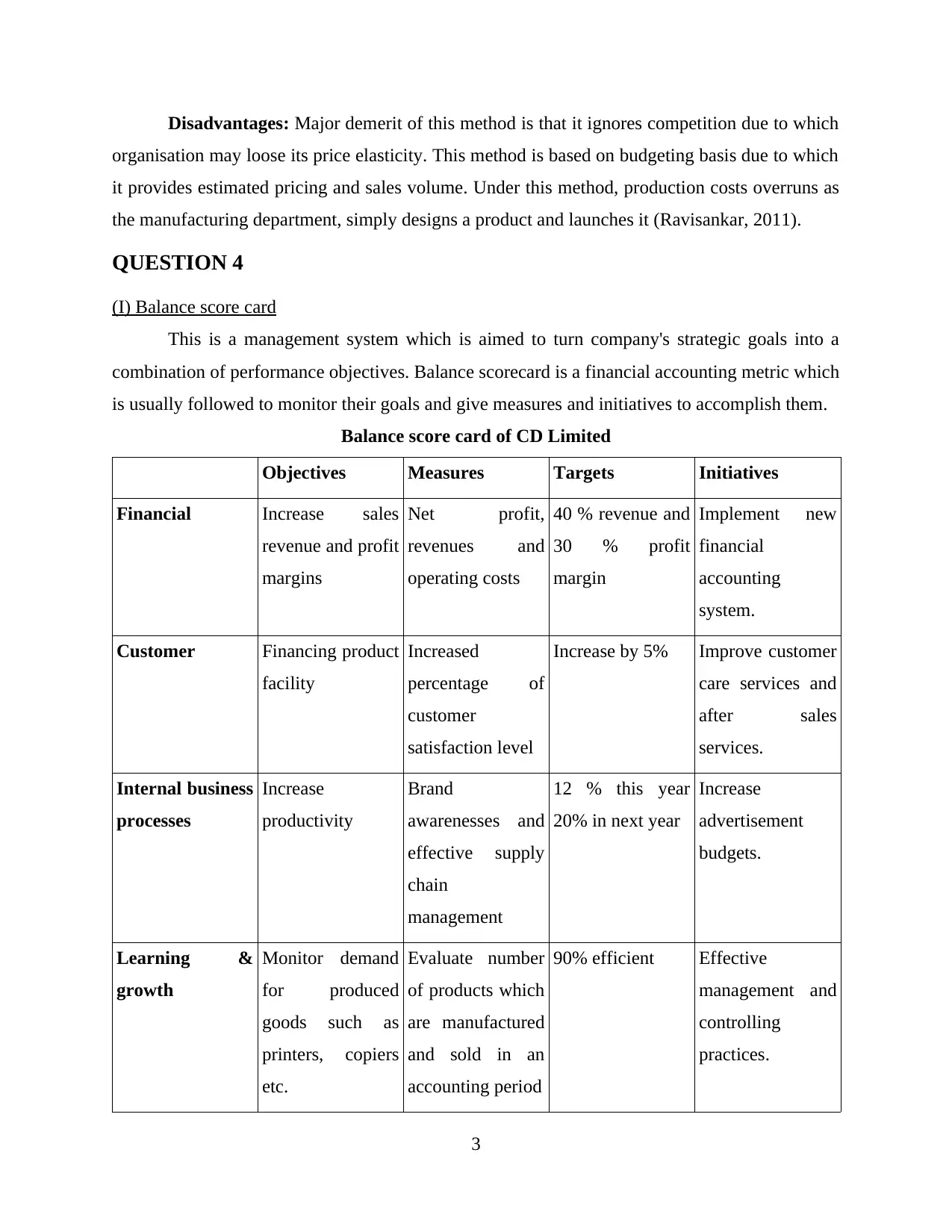

Disadvantages: Major demerit of this method is that it ignores competition due to which

organisation may loose its price elasticity. This method is based on budgeting basis due to which

it provides estimated pricing and sales volume. Under this method, production costs overruns as

the manufacturing department, simply designs a product and launches it (Ravisankar, 2011).

QUESTION 4

(I) Balance score card

This is a management system which is aimed to turn company's strategic goals into a

combination of performance objectives. Balance scorecard is a financial accounting metric which

is usually followed to monitor their goals and give measures and initiatives to accomplish them.

Balance score card of CD Limited

Objectives Measures Targets Initiatives

Financial Increase sales

revenue and profit

margins

Net profit,

revenues and

operating costs

40 % revenue and

30 % profit

margin

Implement new

financial

accounting

system.

Customer Financing product

facility

Increased

percentage of

customer

satisfaction level

Increase by 5% Improve customer

care services and

after sales

services.

Internal business

processes

Increase

productivity

Brand

awarenesses and

effective supply

chain

management

12 % this year

20% in next year

Increase

advertisement

budgets.

Learning &

growth

Monitor demand

for produced

goods such as

printers, copiers

etc.

Evaluate number

of products which

are manufactured

and sold in an

accounting period

90% efficient Effective

management and

controlling

practices.

3

organisation may loose its price elasticity. This method is based on budgeting basis due to which

it provides estimated pricing and sales volume. Under this method, production costs overruns as

the manufacturing department, simply designs a product and launches it (Ravisankar, 2011).

QUESTION 4

(I) Balance score card

This is a management system which is aimed to turn company's strategic goals into a

combination of performance objectives. Balance scorecard is a financial accounting metric which

is usually followed to monitor their goals and give measures and initiatives to accomplish them.

Balance score card of CD Limited

Objectives Measures Targets Initiatives

Financial Increase sales

revenue and profit

margins

Net profit,

revenues and

operating costs

40 % revenue and

30 % profit

margin

Implement new

financial

accounting

system.

Customer Financing product

facility

Increased

percentage of

customer

satisfaction level

Increase by 5% Improve customer

care services and

after sales

services.

Internal business

processes

Increase

productivity

Brand

awarenesses and

effective supply

chain

management

12 % this year

20% in next year

Increase

advertisement

budgets.

Learning &

growth

Monitor demand

for produced

goods such as

printers, copiers

etc.

Evaluate number

of products which

are manufactured

and sold in an

accounting period

90% efficient Effective

management and

controlling

practices.

3

CD Limited is a business solution company which manufactures and delivers business

equipments to local entities such as scanners, fax machineries, printers etc. They has decided to

use balance scorecard in order to measure their performance. This method can be used by the

organisation in various ways such as:

By using this technique, the sited organisation can develop better strategic plans which

gives a powerful framework for creating a communication strategy.

An organisation can have better management information by using this technique. This

method can help in proper decision making process as it evaluates all the objectives and

provides measures and initiatives for those goals (Weil, 2013).

(ii) Benchmarking

Benchmarking is a measurement which is used to ascertain level of quality in

organisational policies, plans, strategies, programs etc. In this measurement, actual results are

compared with the budgeted estimates in order to ascertain deviation between actual and

estimates and find reasons for it. The main objectives of this technique is to find what

improvements can be done in a company to achieve their desired profitability and to analyse

performance of their competitive firms. Information which is obtained by this technique is used

to enhance financial and managerial performance of the business operations of an organisation.

CD Limited has decided to use this technique in order to measure and improve their financial

position. This company deals in manufacturing business utility equipments and in order to use

this technique, the company need to prepare benchmarking report which can help in determining

the health of the business organisation (Benchmarking, 2018). There are various ways by which

performance of CD Limited can be improved using this technique and they are:

Using benchmarking technique, CD Limited can gain an independent perspective by

comparison of performance with competitive firms.

It helps to ascertain all the performance gaps and their reasons which will guide in

identify areas of improvements.

With the assistance of benchmarking technique, CD limited can perform external and

internal analyses which will help in preparing projects and reports that can give us a

useful perspective on good performance. It can used as an effective tool which can

determine effectiveness of product lines, business units and even the performance of

particular employees.

4

equipments to local entities such as scanners, fax machineries, printers etc. They has decided to

use balance scorecard in order to measure their performance. This method can be used by the

organisation in various ways such as:

By using this technique, the sited organisation can develop better strategic plans which

gives a powerful framework for creating a communication strategy.

An organisation can have better management information by using this technique. This

method can help in proper decision making process as it evaluates all the objectives and

provides measures and initiatives for those goals (Weil, 2013).

(ii) Benchmarking

Benchmarking is a measurement which is used to ascertain level of quality in

organisational policies, plans, strategies, programs etc. In this measurement, actual results are

compared with the budgeted estimates in order to ascertain deviation between actual and

estimates and find reasons for it. The main objectives of this technique is to find what

improvements can be done in a company to achieve their desired profitability and to analyse

performance of their competitive firms. Information which is obtained by this technique is used

to enhance financial and managerial performance of the business operations of an organisation.

CD Limited has decided to use this technique in order to measure and improve their financial

position. This company deals in manufacturing business utility equipments and in order to use

this technique, the company need to prepare benchmarking report which can help in determining

the health of the business organisation (Benchmarking, 2018). There are various ways by which

performance of CD Limited can be improved using this technique and they are:

Using benchmarking technique, CD Limited can gain an independent perspective by

comparison of performance with competitive firms.

It helps to ascertain all the performance gaps and their reasons which will guide in

identify areas of improvements.

With the assistance of benchmarking technique, CD limited can perform external and

internal analyses which will help in preparing projects and reports that can give us a

useful perspective on good performance. It can used as an effective tool which can

determine effectiveness of product lines, business units and even the performance of

particular employees.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benchmarking can develop a standard for processes and tasks. This can motivate CD

Limited to invest in resources which can provide calculation of metrics and KPIs.

Regardless of adopting industry, having a strong base can be considered as key of

successful business practices.

From the help of benchmarking an organisation can understand their own performance

and can identify the improvements measures which can be adapted by comparing their

own performance with their competitors (Yalcin, 2012).

CONCLUSION

From the above project report, it can be concluded that accounting systems and

techniques are the vital techniques for any organisation. Accounting methods such as

benchmarking and balance score card i.e. prepared and interpreted in order to measure financial

performance of the given business entities. Numerous budgets and variances are calculated for

ascertaining estimate and deficits in the business operations along with several transfer pricing

methods such as market based transfer prices and full cost transfer prices.

5

Limited to invest in resources which can provide calculation of metrics and KPIs.

Regardless of adopting industry, having a strong base can be considered as key of

successful business practices.

From the help of benchmarking an organisation can understand their own performance

and can identify the improvements measures which can be adapted by comparing their

own performance with their competitors (Yalcin, 2012).

CONCLUSION

From the above project report, it can be concluded that accounting systems and

techniques are the vital techniques for any organisation. Accounting methods such as

benchmarking and balance score card i.e. prepared and interpreted in order to measure financial

performance of the given business entities. Numerous budgets and variances are calculated for

ascertaining estimate and deficits in the business operations along with several transfer pricing

methods such as market based transfer prices and full cost transfer prices.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Flamholtz, E. G., 2012. Human resource accounting: Advances in concepts, methods and

applications. Springer Science & Business Media.

Huizinga, H. and Laeven, L., 2012. Bank valuation and accounting discretion during a financial

crisis. Journal of Financial Economics, 106(3). pp.614-634.

Jones, M. ed., 2011. Creative accounting, fraud and international accounting scandals. John

Wiley & Sons.

Ravisankar, P., and et. al., 2011. Detection of financial statement fraud and feature selection

using data mining techniques. Decision Support Systems, 50(2). pp.491-500.

Weil, R. L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Yalcin, N., Bayrakdaroglu, A. and Kahraman, C., 2012. Application of fuzzy multi-criteria

decision making methods for financial performance evaluation of Turkish

manufacturing industries. Expert Systems with Applications, 39(1). pp.350-364.

Online

Benchmarking. 2018. [Online]. Available

through:<http://asq.org/learn-about-quality/benchmarking/overview/overview.html>.

6

Books and Journals:

Flamholtz, E. G., 2012. Human resource accounting: Advances in concepts, methods and

applications. Springer Science & Business Media.

Huizinga, H. and Laeven, L., 2012. Bank valuation and accounting discretion during a financial

crisis. Journal of Financial Economics, 106(3). pp.614-634.

Jones, M. ed., 2011. Creative accounting, fraud and international accounting scandals. John

Wiley & Sons.

Ravisankar, P., and et. al., 2011. Detection of financial statement fraud and feature selection

using data mining techniques. Decision Support Systems, 50(2). pp.491-500.

Weil, R. L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Yalcin, N., Bayrakdaroglu, A. and Kahraman, C., 2012. Application of fuzzy multi-criteria

decision making methods for financial performance evaluation of Turkish

manufacturing industries. Expert Systems with Applications, 39(1). pp.350-364.

Online

Benchmarking. 2018. [Online]. Available

through:<http://asq.org/learn-about-quality/benchmarking/overview/overview.html>.

6

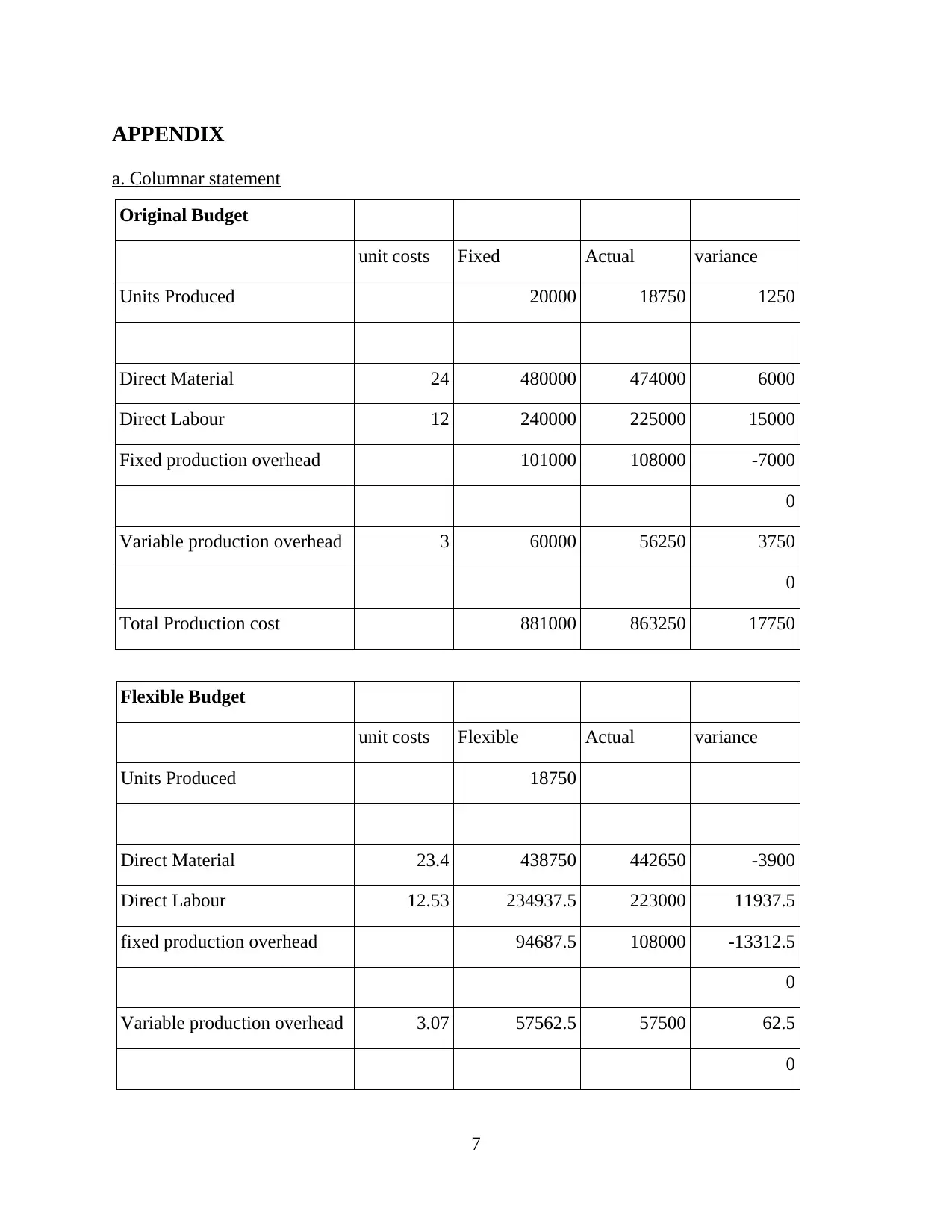

APPENDIX

a. Columnar statement

Original Budget

unit costs Fixed Actual variance

Units Produced 20000 18750 1250

Direct Material 24 480000 474000 6000

Direct Labour 12 240000 225000 15000

Fixed production overhead 101000 108000 -7000

0

Variable production overhead 3 60000 56250 3750

0

Total Production cost 881000 863250 17750

Flexible Budget

unit costs Flexible Actual variance

Units Produced 18750

Direct Material 23.4 438750 442650 -3900

Direct Labour 12.53 234937.5 223000 11937.5

fixed production overhead 94687.5 108000 -13312.5

0

Variable production overhead 3.07 57562.5 57500 62.5

0

7

a. Columnar statement

Original Budget

unit costs Fixed Actual variance

Units Produced 20000 18750 1250

Direct Material 24 480000 474000 6000

Direct Labour 12 240000 225000 15000

Fixed production overhead 101000 108000 -7000

0

Variable production overhead 3 60000 56250 3750

0

Total Production cost 881000 863250 17750

Flexible Budget

unit costs Flexible Actual variance

Units Produced 18750

Direct Material 23.4 438750 442650 -3900

Direct Labour 12.53 234937.5 223000 11937.5

fixed production overhead 94687.5 108000 -13312.5

0

Variable production overhead 3.07 57562.5 57500 62.5

0

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.