Strategic Management Accounting: Adelaide Company Analysis Report

VerifiedAdded on 2023/06/04

|8

|1572

|364

Report

AI Summary

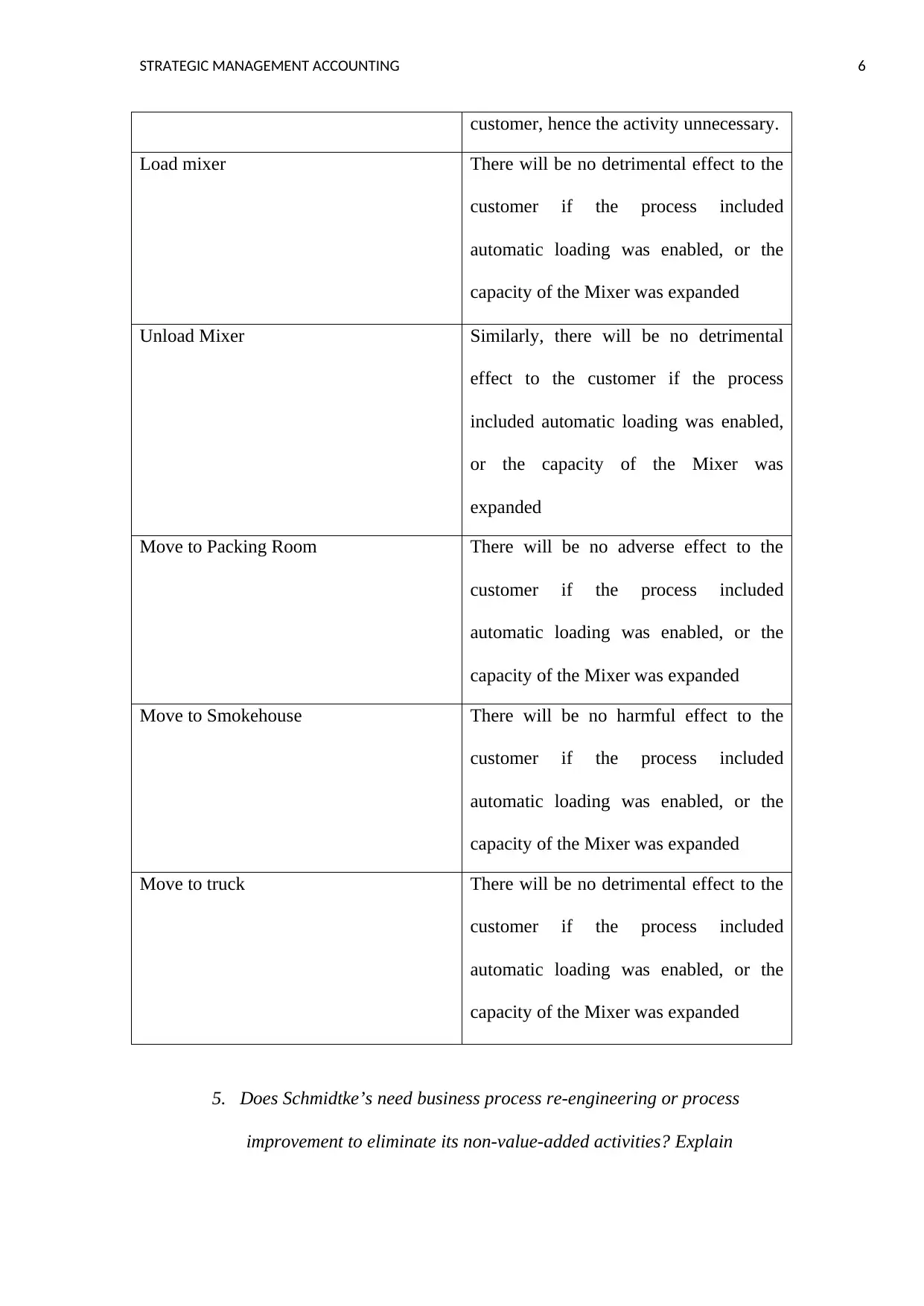

This report provides a strategic management accounting analysis of the Adelaide Company, focusing on its ability to sell mettwurst at a competitive price. It delves into the reasons behind Adelaide's cost advantage, including modern production facilities, ABC costing, and economies of scale. The report calculates the cost per stick of mettwurst under an absorption costing system and contrasts it with activity-based costing, explaining the potential inaccuracies of absorption costing. It identifies and evaluates non-value-added activities within the company's operations, recommending their elimination. The report concludes by assessing whether the company requires business process re-engineering or process improvement to eliminate these non-value-added activities, ultimately suggesting the need for business process re-engineering to achieve long-term strategic goals.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.