Critical Evaluation of Strategic Management Accounting Tools BFK503

VerifiedAdded on 2022/08/12

|28

|4151

|28

Report

AI Summary

This report critically evaluates Strategic Management Accounting (SMA) tools and their application in decision-making and communication. It begins by defining SMA according to Roslender (2003) and assesses its role in providing firms with an economic advantage. The report then delves into various aspects of SMA, including costing techniques (activity-based costing, life cycle costing, etc.), planning, control, performance measurement, strategic decision-making, competitor accounting, and customer accounting. The analysis extends to a case study involving a book manufacturing company, exploring value engineering to close a cost gap. Additionally, the report examines cost-plus transfer pricing, its mechanics, and implications for divisional performance within a company. Finally, the report discusses the benefits and issues associated with the Balanced Scorecard, along with recommendations for its implementation and integration with research and market expansion strategies.

Running head: STRATEGIC MANAGEMENT ACCOUNTING

Strategic management accounting

Name of the student

Name of the university

Student ID

Author note

Table of Contents

Strategic management accounting

Name of the student

Name of the university

Student ID

Author note

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

STRATEGIC MANAGEMENT ACCOUNTING

Task1................................................................................................................................................3

Costing.............................................................................................................................................4

Planning, control and performance measurement...........................................................................4

Strategic decision making................................................................................................................4

Competitor accounting.....................................................................................................................4

Customer accounting.......................................................................................................................5

Quality dimension............................................................................................................................6

Flexibility dimension.......................................................................................................................7

Cost dimension................................................................................................................................7

Task2................................................................................................................................................7

B. Value Engineering................................................................................................................8

Suggestion for closing the cost gap.................................................................................................9

C. Implication of the value engineering....................................................................................9

Lack of understading the concept..................................................................................................10

Task3..............................................................................................................................................10

How the cost plus transfer pricing method works.........................................................................11

Task4..............................................................................................................................................14

Benifits...........................................................................................................................................16

Provide a clear picture...................................................................................................................16

STRATEGIC MANAGEMENT ACCOUNTING

Task1................................................................................................................................................3

Costing.............................................................................................................................................4

Planning, control and performance measurement...........................................................................4

Strategic decision making................................................................................................................4

Competitor accounting.....................................................................................................................4

Customer accounting.......................................................................................................................5

Quality dimension............................................................................................................................6

Flexibility dimension.......................................................................................................................7

Cost dimension................................................................................................................................7

Task2................................................................................................................................................7

B. Value Engineering................................................................................................................8

Suggestion for closing the cost gap.................................................................................................9

C. Implication of the value engineering....................................................................................9

Lack of understading the concept..................................................................................................10

Task3..............................................................................................................................................10

How the cost plus transfer pricing method works.........................................................................11

Task4..............................................................................................................................................14

Benifits...........................................................................................................................................16

Provide a clear picture...................................................................................................................16

2

STRATEGIC MANAGEMENT ACCOUNTING

Signals a company performance....................................................................................................16

Helps to achieve the goal...............................................................................................................17

Issues regarding Balanced Scorecard............................................................................................17

Expensive and time consuming.....................................................................................................17

Poor support from employees........................................................................................................17

Decrease cost and increase the sales..............................................................................................18

Research on quality control...........................................................................................................18

Expanding the market....................................................................................................................19

Alignment of the science research based of the company.............................................................19

Develop the projects......................................................................................................................19

Advise on the implementation.......................................................................................................19

Research more on the product.......................................................................................................19

Qualitative research.......................................................................................................................19

Reference.......................................................................................................................................21

STRATEGIC MANAGEMENT ACCOUNTING

Signals a company performance....................................................................................................16

Helps to achieve the goal...............................................................................................................17

Issues regarding Balanced Scorecard............................................................................................17

Expensive and time consuming.....................................................................................................17

Poor support from employees........................................................................................................17

Decrease cost and increase the sales..............................................................................................18

Research on quality control...........................................................................................................18

Expanding the market....................................................................................................................19

Alignment of the science research based of the company.............................................................19

Develop the projects......................................................................................................................19

Advise on the implementation.......................................................................................................19

Research more on the product.......................................................................................................19

Qualitative research.......................................................................................................................19

Reference.......................................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

STRATEGIC MANAGEMENT ACCOUNTING

Task1

A.

The concept of Strategic Management Accounting 1was presented in management

accounting domain by Simmonds for the first time in 1981. Several studies and development

followed by the scholars, have encompassed SMA and development of the management

accounting with the alignment of the strategic management that comprehends the formulation,

implementation and the strategy control. It also refers for marketing and other managerial

functions. they have reflected that SMA approves an external or outward looking theory which

implies the customers, competitors and market focus. It also adopts a forward looking orientation

that provides a strategic orientation.

According to the Roslender and Hart 2003, “SMA is identified as a generic approach to

accounting for strategic positioning, defined by an attempt to integrate insights from

management accounting and marketing management within a strategic management

framework”2.

1 Carlsson-Wall, Martin, Kalle Kraus, and Johnny Lind. "Strategic management accounting in

close inter-organisational relationships." Accounting and Business Research 45.1 (2015): 27-54.

2 close inter-organisational relationships." Accounting and Business Research 45.1 (2015): 27-54.

Theriou, Nikolaos G. "Strategic Management Process and the Importance of Structured

Formality, Financial and Non-Financial Information." European Research Studies 18.2 (2015):

3.

STRATEGIC MANAGEMENT ACCOUNTING

Task1

A.

The concept of Strategic Management Accounting 1was presented in management

accounting domain by Simmonds for the first time in 1981. Several studies and development

followed by the scholars, have encompassed SMA and development of the management

accounting with the alignment of the strategic management that comprehends the formulation,

implementation and the strategy control. It also refers for marketing and other managerial

functions. they have reflected that SMA approves an external or outward looking theory which

implies the customers, competitors and market focus. It also adopts a forward looking orientation

that provides a strategic orientation.

According to the Roslender and Hart 2003, “SMA is identified as a generic approach to

accounting for strategic positioning, defined by an attempt to integrate insights from

management accounting and marketing management within a strategic management

framework”2.

1 Carlsson-Wall, Martin, Kalle Kraus, and Johnny Lind. "Strategic management accounting in

close inter-organisational relationships." Accounting and Business Research 45.1 (2015): 27-54.

2 close inter-organisational relationships." Accounting and Business Research 45.1 (2015): 27-54.

Theriou, Nikolaos G. "Strategic Management Process and the Importance of Structured

Formality, Financial and Non-Financial Information." European Research Studies 18.2 (2015):

3.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

STRATEGIC MANAGEMENT ACCOUNTING

In the context of strategic managemet accounting dimensions, thre are three aspects as

follows:

Costing

There are six techniques were involved with this mechanism to determine, analyse and

manage the cost in a strategic manner. This techniques are activity based costing, attribute

costing, life cycle costing, quality costing, target costing and value chain costing. It represents an

important element in an external and forward looking orientation and the development of the

strategies3.

Planning, control and performance measurement

To relate this category, benchmarking and integrated performance measurements are the

main techniques. For implementing the benchmarking with its forward looking orientation,

organization is searching for the best practice competitors by the enhancing and strategic

positioning and Guilding4.

3 Chen, Xu. "Instruments of Strategy Management Accounting and Their Application in Inter-

Organizational Cost Management." ICCREM 2015. 2015. 33-41.

4 Pendleton, Scott Drew, et al. "Perception, planning, control, and coordination for autonomous

vehicles." Machines 5.1 (2017): 6.

STRATEGIC MANAGEMENT ACCOUNTING

In the context of strategic managemet accounting dimensions, thre are three aspects as

follows:

Costing

There are six techniques were involved with this mechanism to determine, analyse and

manage the cost in a strategic manner. This techniques are activity based costing, attribute

costing, life cycle costing, quality costing, target costing and value chain costing. It represents an

important element in an external and forward looking orientation and the development of the

strategies3.

Planning, control and performance measurement

To relate this category, benchmarking and integrated performance measurements are the

main techniques. For implementing the benchmarking with its forward looking orientation,

organization is searching for the best practice competitors by the enhancing and strategic

positioning and Guilding4.

3 Chen, Xu. "Instruments of Strategy Management Accounting and Their Application in Inter-

Organizational Cost Management." ICCREM 2015. 2015. 33-41.

4 Pendleton, Scott Drew, et al. "Perception, planning, control, and coordination for autonomous

vehicles." Machines 5.1 (2017): 6.

5

STRATEGIC MANAGEMENT ACCOUNTING

Strategic decision making

It is the parctivce of three effective techniques of strategic orientation of the company,

this techniques are involved strategic costing, strategic pricing and brand valuation. All of this

techniques are conformed as external and forward looking orientations5.

Competitor accounting

In this practice includes, competitor caost assessment, competitor cost appraisal

performance and the competitive position monitoring. This techniques is very useful in terms of

strategic decision making process by the external orientations which includes thw strategy

formulations and strategy monitoring6.

Customer accounting

Under this technique, focus on customers and comprise customers profitability, cost

analysis, analysis of life time customer profitability and the valuation of the customer as assets.

Like the other practice these three practice also follow the external and forward looking

orientation7.

5 Auvinen, Heidi, et al. "Process supporting strategic decision-making in systemic

transitions." Technological Forecasting and Social Change 94 (2015): 97-114.

6 Alsoboa, Sliman, and Mohammad M. Alalaya. "Practices of competitor accounting and its

influence on the competitive advantages: an empirical study in jordanian manufacturing

companies." Global Journal of Management and Business Research (2015).

STRATEGIC MANAGEMENT ACCOUNTING

Strategic decision making

It is the parctivce of three effective techniques of strategic orientation of the company,

this techniques are involved strategic costing, strategic pricing and brand valuation. All of this

techniques are conformed as external and forward looking orientations5.

Competitor accounting

In this practice includes, competitor caost assessment, competitor cost appraisal

performance and the competitive position monitoring. This techniques is very useful in terms of

strategic decision making process by the external orientations which includes thw strategy

formulations and strategy monitoring6.

Customer accounting

Under this technique, focus on customers and comprise customers profitability, cost

analysis, analysis of life time customer profitability and the valuation of the customer as assets.

Like the other practice these three practice also follow the external and forward looking

orientation7.

5 Auvinen, Heidi, et al. "Process supporting strategic decision-making in systemic

transitions." Technological Forecasting and Social Change 94 (2015): 97-114.

6 Alsoboa, Sliman, and Mohammad M. Alalaya. "Practices of competitor accounting and its

influence on the competitive advantages: an empirical study in jordanian manufacturing

companies." Global Journal of Management and Business Research (2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

STRATEGIC MANAGEMENT ACCOUNTING

As mentioned of above, the main consideration of the the management accounting

technique is the external orientation of the technique and its capability to provide the future

information. The information provided by the these methodology is very important to formulate

and to monitor the strategy and value creation.

The Second aspects refers the conceptualizing and the operationalizing strategic

management accounting is the involvement of management accountant in this process. The

imnporatnace of this involvement is addressed in terms of the managements accountant’s role to

develop the strategic management accounting system and to emphasize several organizational

functions. The active character of the management accountant was also identified in claiming

that the perception of the competitors actions and reactions are largely depends on the immersion

of the management accountant. The importance of the participation of the managements

accountant in the several organizational activities and in the improvement of the management

accounting system alongwith the strategic orientation. The main illustration is that the strategic

management accountant exhebits a large vision of the enterprise and gthe key skills to promote

the organizational changes to prevent the uncertainity and intense competition8.

7Cimaglobal.Com,

https://www.cimaglobal.com/Documents/Thought_leadership_docs/Management/financial

accounting/Academic-Research-Report-Strategic-Management-Process.pdf. Accessed 28 Feb

2020.

8Cimaglobal.Com,

https://www.cimaglobal.com/Documents/Thought_leadership_docs/Management/financial

accounting/Academic-Research-Report-Strategic-Management-Process.pdf. Accessed 28 Feb

2020.

STRATEGIC MANAGEMENT ACCOUNTING

As mentioned of above, the main consideration of the the management accounting

technique is the external orientation of the technique and its capability to provide the future

information. The information provided by the these methodology is very important to formulate

and to monitor the strategy and value creation.

The Second aspects refers the conceptualizing and the operationalizing strategic

management accounting is the involvement of management accountant in this process. The

imnporatnace of this involvement is addressed in terms of the managements accountant’s role to

develop the strategic management accounting system and to emphasize several organizational

functions. The active character of the management accountant was also identified in claiming

that the perception of the competitors actions and reactions are largely depends on the immersion

of the management accountant. The importance of the participation of the managements

accountant in the several organizational activities and in the improvement of the management

accounting system alongwith the strategic orientation. The main illustration is that the strategic

management accountant exhebits a large vision of the enterprise and gthe key skills to promote

the organizational changes to prevent the uncertainity and intense competition8.

7Cimaglobal.Com,

https://www.cimaglobal.com/Documents/Thought_leadership_docs/Management/financial

accounting/Academic-Research-Report-Strategic-Management-Process.pdf. Accessed 28 Feb

2020.

8Cimaglobal.Com,

https://www.cimaglobal.com/Documents/Thought_leadership_docs/Management/financial

accounting/Academic-Research-Report-Strategic-Management-Process.pdf. Accessed 28 Feb

2020.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

STRATEGIC MANAGEMENT ACCOUNTING

The study also suggests that the gap between traditional management accounting 9and

strategic management can be occupied by the management accountant involvement of the

strategic decision making process. Which helps the senior managers to make informed. Timely

decisions.

In addition to the above aspects, the third most important elements that allows the

management accountant proactive in the context of business management and decision making

process. He should have a commercial skills and take the erxpansion strategy in terms of

financial orientation to adopt the non orientation factors like customer, competitors, markets,

external and internal matter in general.

Refering the dimensions, the concept of the competitive advantage 10introduce a

framework for the company to formulate and implement the strategies that make a better

positions than its competitor by the better utilistaion of the technical, financial, physical and

organizational capabilities and resources. The study finds several dimensions like quality,

flexibility, cost.

9 Angelakis, George, et al. "Traditional and currently developed management accounting

practices–A Greek study." (2015).

10 David, Fred, and Forest R. David. Strategic management: A competitive advantage approach,

concepts and cases. Pearson–Prentice Hall, 2016.

STRATEGIC MANAGEMENT ACCOUNTING

The study also suggests that the gap between traditional management accounting 9and

strategic management can be occupied by the management accountant involvement of the

strategic decision making process. Which helps the senior managers to make informed. Timely

decisions.

In addition to the above aspects, the third most important elements that allows the

management accountant proactive in the context of business management and decision making

process. He should have a commercial skills and take the erxpansion strategy in terms of

financial orientation to adopt the non orientation factors like customer, competitors, markets,

external and internal matter in general.

Refering the dimensions, the concept of the competitive advantage 10introduce a

framework for the company to formulate and implement the strategies that make a better

positions than its competitor by the better utilistaion of the technical, financial, physical and

organizational capabilities and resources. The study finds several dimensions like quality,

flexibility, cost.

9 Angelakis, George, et al. "Traditional and currently developed management accounting

practices–A Greek study." (2015).

10 David, Fred, and Forest R. David. Strategic management: A competitive advantage approach,

concepts and cases. Pearson–Prentice Hall, 2016.

8

STRATEGIC MANAGEMENT ACCOUNTING

Quality dimension

Quality is an important economic advantage that refers the performance of the products

that surely meet the expactations of the customer. Quality dimensions derive the company’s

ability to deliver the right product to meet the consumers need. The high quality products that

contributes company’s reputation improve11.

Flexibility dimension

It describes the flexibility of a quick responding to changes that may occure in product

design to meet the customer’s needs. It also refers that this dimension is the ability to quickly

produce the wide range of products, introduce a new products and modify the existing products

as a response to the customer needs. Flexibility is also described as the ability to change from the

traditional method to the new one12.

Cost dimension

It emphasizes that the company must focus on the production cost and the marketing cost

so that the company would deliver the aproduct at a lower rate. The lower cost of the product

11Hrmars.Com,

http://hrmars.com/hrmars_papers/Strategic_Management_Accounting_and_the_Dimensions_of_

Competitive_Advantage_Testing_the_Associations_in_Saudi_Industrial_Sector.pdf. Accessed

28 Feb 2020.

12 Carlsson-Wall, Martin, Kalle Kraus, and Johnny Lind. "Strategic management accounting in

close inter-organisational relationships." Accounting and Business Research 45.1 (2015): 27-54.

STRATEGIC MANAGEMENT ACCOUNTING

Quality dimension

Quality is an important economic advantage that refers the performance of the products

that surely meet the expactations of the customer. Quality dimensions derive the company’s

ability to deliver the right product to meet the consumers need. The high quality products that

contributes company’s reputation improve11.

Flexibility dimension

It describes the flexibility of a quick responding to changes that may occure in product

design to meet the customer’s needs. It also refers that this dimension is the ability to quickly

produce the wide range of products, introduce a new products and modify the existing products

as a response to the customer needs. Flexibility is also described as the ability to change from the

traditional method to the new one12.

Cost dimension

It emphasizes that the company must focus on the production cost and the marketing cost

so that the company would deliver the aproduct at a lower rate. The lower cost of the product

11Hrmars.Com,

http://hrmars.com/hrmars_papers/Strategic_Management_Accounting_and_the_Dimensions_of_

Competitive_Advantage_Testing_the_Associations_in_Saudi_Industrial_Sector.pdf. Accessed

28 Feb 2020.

12 Carlsson-Wall, Martin, Kalle Kraus, and Johnny Lind. "Strategic management accounting in

close inter-organisational relationships." Accounting and Business Research 45.1 (2015): 27-54.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

STRATEGIC MANAGEMENT ACCOUNTING

assures the company to acquire a higher market share as the basis of its success and superiority.

From the economic and financial perspective, low price of the products increase the demand as

well as the profit margin13.

Task2

A.

13 "Strategic Management Accounting Definition: An Introduction". Hotspotfinance, 2016,

https://www.hotspotfinance.com/strategic-management-accounting-definition-introduction/.

Accessed 28 Feb 2020

STRATEGIC MANAGEMENT ACCOUNTING

assures the company to acquire a higher market share as the basis of its success and superiority.

From the economic and financial perspective, low price of the products increase the demand as

well as the profit margin13.

Task2

A.

13 "Strategic Management Accounting Definition: An Introduction". Hotspotfinance, 2016,

https://www.hotspotfinance.com/strategic-management-accounting-definition-introduction/.

Accessed 28 Feb 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

STRATEGIC MANAGEMENT ACCOUNTING

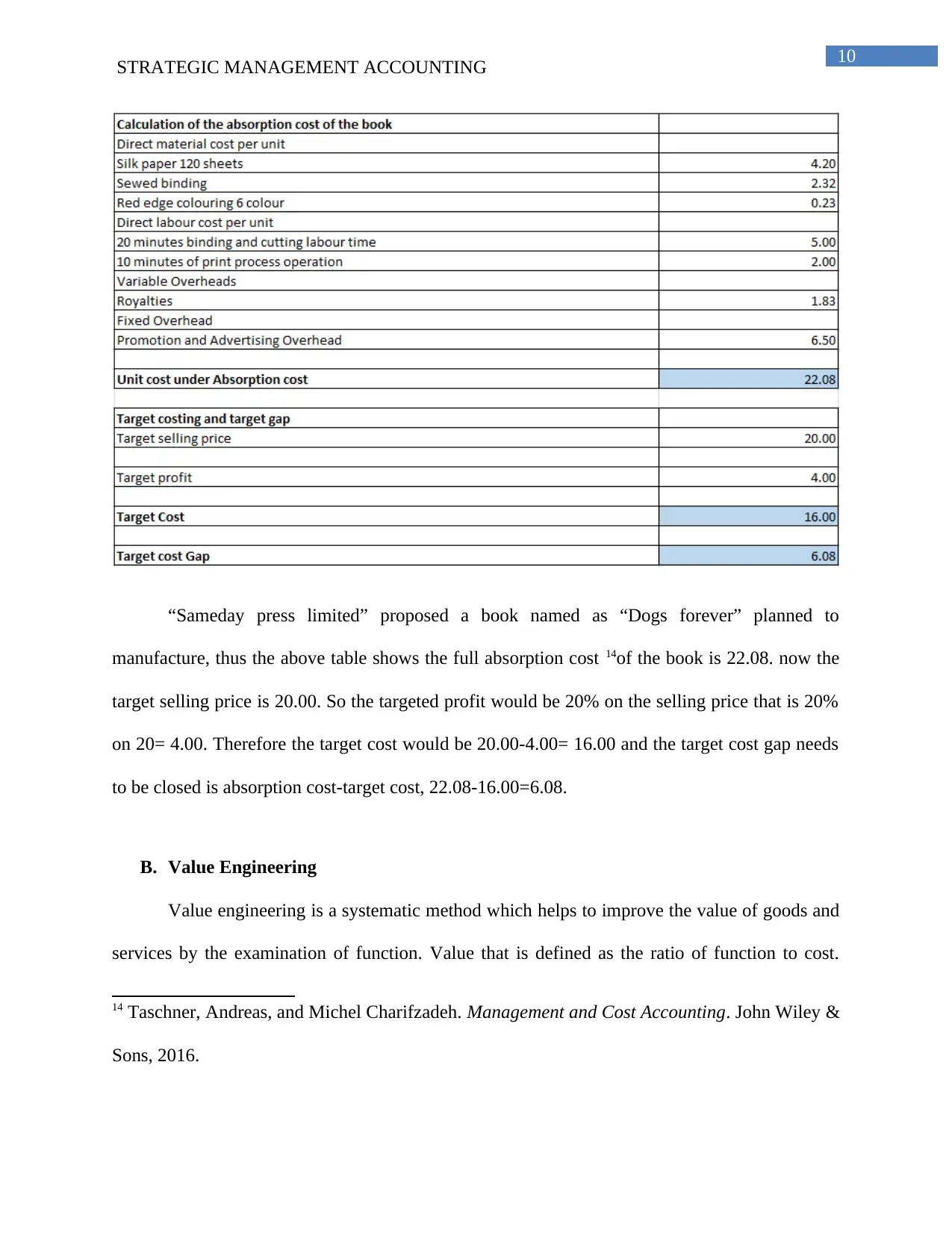

“Sameday press limited” proposed a book named as “Dogs forever” planned to

manufacture, thus the above table shows the full absorption cost 14of the book is 22.08. now the

target selling price is 20.00. So the targeted profit would be 20% on the selling price that is 20%

on 20= 4.00. Therefore the target cost would be 20.00-4.00= 16.00 and the target cost gap needs

to be closed is absorption cost-target cost, 22.08-16.00=6.08.

B. Value Engineering

Value engineering is a systematic method which helps to improve the value of goods and

services by the examination of function. Value that is defined as the ratio of function to cost.

14 Taschner, Andreas, and Michel Charifzadeh. Management and Cost Accounting. John Wiley &

Sons, 2016.

STRATEGIC MANAGEMENT ACCOUNTING

“Sameday press limited” proposed a book named as “Dogs forever” planned to

manufacture, thus the above table shows the full absorption cost 14of the book is 22.08. now the

target selling price is 20.00. So the targeted profit would be 20% on the selling price that is 20%

on 20= 4.00. Therefore the target cost would be 20.00-4.00= 16.00 and the target cost gap needs

to be closed is absorption cost-target cost, 22.08-16.00=6.08.

B. Value Engineering

Value engineering is a systematic method which helps to improve the value of goods and

services by the examination of function. Value that is defined as the ratio of function to cost.

14 Taschner, Andreas, and Michel Charifzadeh. Management and Cost Accounting. John Wiley &

Sons, 2016.

11

STRATEGIC MANAGEMENT ACCOUNTING

Value engineering is sometimes ecxamined within the project management or industrial

engineering. It creates a technique in which the value of an outcome is optimized by making a

mix of performance and costs15.

This procedure follows a structured process that is based exclusively on function. It simly

use the rational logic and the analysis of function to address the relationships that increase the

value. It could be considered as the quantitative method which is very similar to the scientific

method. The value engineering process is hypothesis based conclusion, it approaches the test

realationships and operation research which uses the model building to classify the predictive

relationship.

Suggestion for closing the cost gap

There are certain way to close the cost gap 16that exist between the current estimated cost

levels and the target cost. It is essential to close the target cost gap at the cdesign stage. Below

mentioned ways are need to follow:

Product’ feature review

Remove that features from the product that add to the cost but do not significantly add

value to the product.

Cost reduction will happen while the team approach is adopted.

15 Cooper, Robin. Target costing and value engineering. Routledge, 2017.

16 Guajardo, Mario, and Mikael Rönnqvist. "A review on cost allocation methods in collaborative

transportation." International transactions in operational research 23.3 (2016): 371-392.

STRATEGIC MANAGEMENT ACCOUNTING

Value engineering is sometimes ecxamined within the project management or industrial

engineering. It creates a technique in which the value of an outcome is optimized by making a

mix of performance and costs15.

This procedure follows a structured process that is based exclusively on function. It simly

use the rational logic and the analysis of function to address the relationships that increase the

value. It could be considered as the quantitative method which is very similar to the scientific

method. The value engineering process is hypothesis based conclusion, it approaches the test

realationships and operation research which uses the model building to classify the predictive

relationship.

Suggestion for closing the cost gap

There are certain way to close the cost gap 16that exist between the current estimated cost

levels and the target cost. It is essential to close the target cost gap at the cdesign stage. Below

mentioned ways are need to follow:

Product’ feature review

Remove that features from the product that add to the cost but do not significantly add

value to the product.

Cost reduction will happen while the team approach is adopted.

15 Cooper, Robin. Target costing and value engineering. Routledge, 2017.

16 Guajardo, Mario, and Mikael Rönnqvist. "A review on cost allocation methods in collaborative

transportation." International transactions in operational research 23.3 (2016): 371-392.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.