Strategic Management Accounting Report: Wattle Jet Case Study Analysis

VerifiedAdded on 2023/06/10

|5

|651

|374

Report

AI Summary

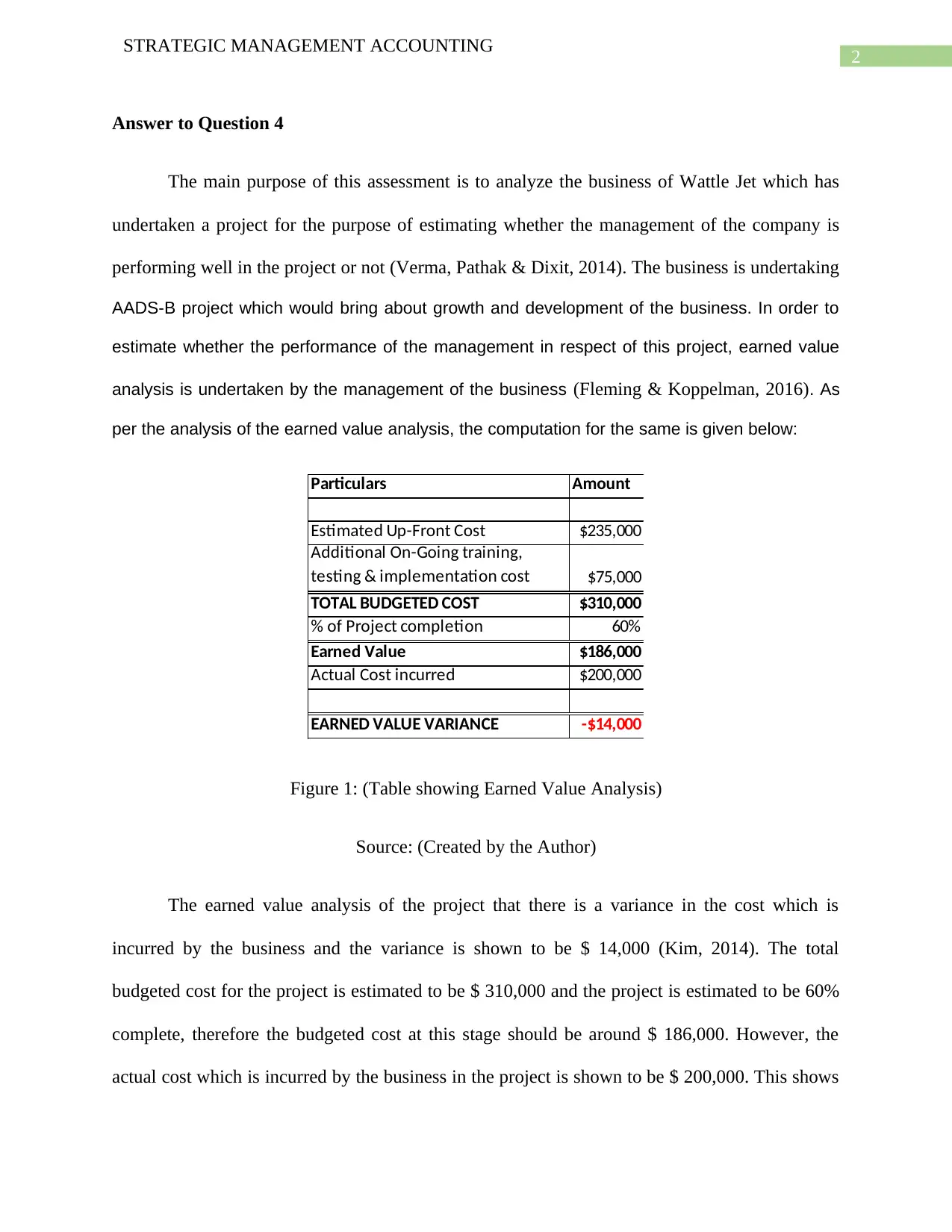

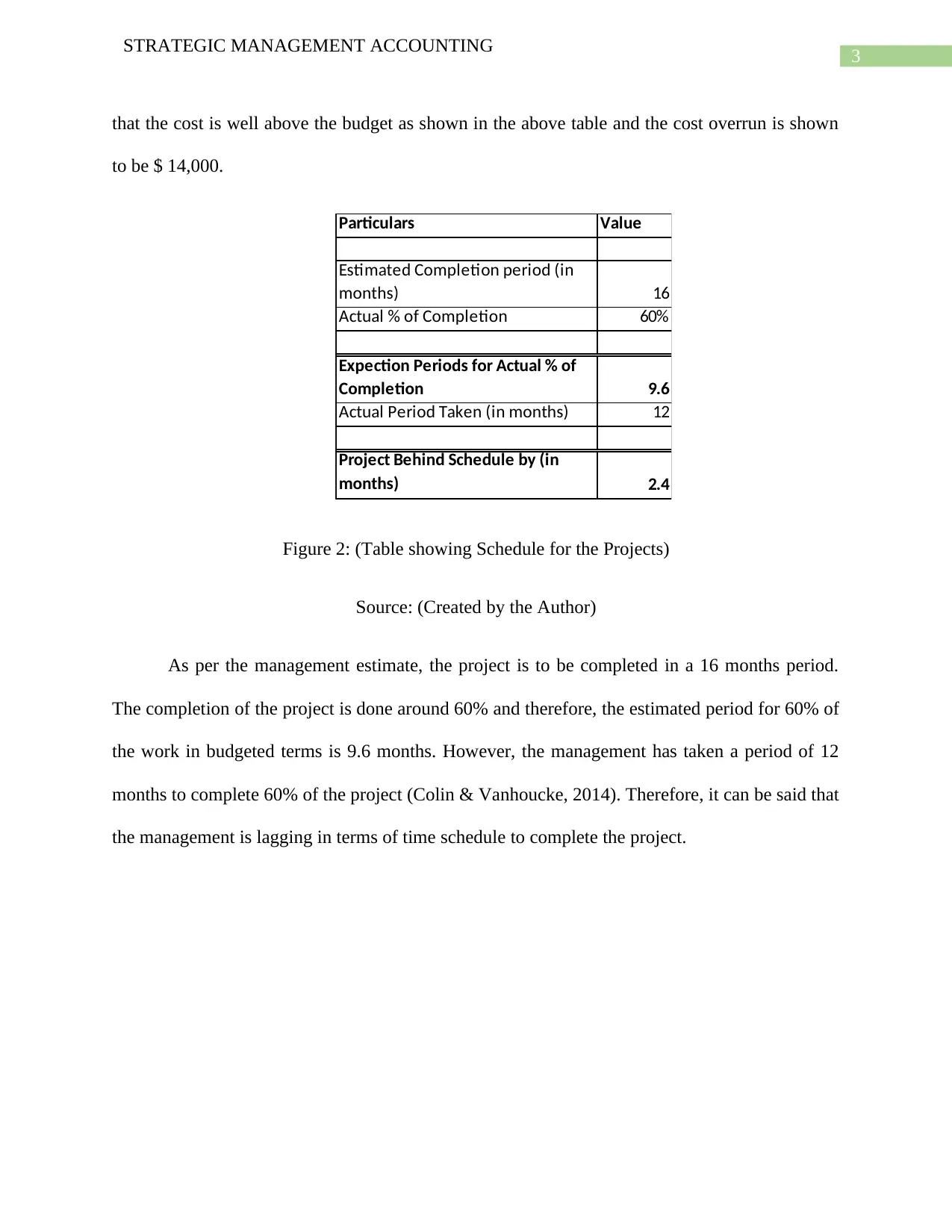

This report presents a strategic management accounting analysis of the Wattle Jet case study. The analysis focuses on the company's AADS-B project, examining its financial performance using earned value analysis. The report calculates cost and schedule variances, highlighting a cost overrun of $14,000 and a delay in project completion. The analysis compares the budgeted costs and schedule with the actual figures, revealing inefficiencies in project management. The report also references the assignment brief, which required an analysis of Wattle Jet's stakeholders, their value, and related strategic objectives. The report offers insights into project performance, including cost and schedule variance. The report also includes a review of the company's strategic planning process, or lack thereof, with a focus on the identification of stakeholders, their value, and strategic objectives.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.