Strategic Management Accounting Report: Value Chain and Strategies

VerifiedAdded on 2023/05/31

|18

|4400

|305

Report

AI Summary

This report delves into strategic management accounting, focusing on value chain analysis and its enhancement using various strategic management tools. It provides insights into techniques for developing, implementing, and monitoring strategies, including SWOT analysis, gap analysis, and Michael Porter’s Value Chain. The report also examines the strategic management cycle, the leadership role of professional accountants, and the influence of organizational and industry factors on value chain analysis. Furthermore, it explores the characteristics of effective strategic and corporate social responsibilities for performance measurement and control systems. The report advises Ansell Strategic on selecting, planning, implementing, controlling, and monitoring strategies to improve their value chain and overall performance. It also discusses the role of organizations and industries in value chain analysis and the design and structure of value-adding activities, value drivers, and value chains. The report concludes with a summary of key findings and recommendations for Ansell Strategic to achieve its objectives.

Strategic Management Accounting

Name of the Student

Name of the University

Author’s Note

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................2

1. Enhancement of Value Chain with Various Strategic Management Tools.................................2

2. Techniques to Develop, Implement and Monitor Strategies.......................................................4

3. a. Strategic Management Cycle...................................................................................................6

3. b. Leadership Role of Professional Accountants in Strategic Management................................8

4. a. Role of Organization and Industry in Value Chain Analysis..................................................8

4. b. Design and Structure of Value Adding Activities, Value Drivers and Value Chains.............9

5. Characteristics of Effective Strategic and Corporate Social Responsibilities for Measuring

Performance and Control System..................................................................................................10

6. Strategic Management Accounting to Select, Plan, Implement, Control and Monitor.............11

Conclusion.....................................................................................................................................12

References......................................................................................................................................14

Introduction......................................................................................................................................2

1. Enhancement of Value Chain with Various Strategic Management Tools.................................2

2. Techniques to Develop, Implement and Monitor Strategies.......................................................4

3. a. Strategic Management Cycle...................................................................................................6

3. b. Leadership Role of Professional Accountants in Strategic Management................................8

4. a. Role of Organization and Industry in Value Chain Analysis..................................................8

4. b. Design and Structure of Value Adding Activities, Value Drivers and Value Chains.............9

5. Characteristics of Effective Strategic and Corporate Social Responsibilities for Measuring

Performance and Control System..................................................................................................10

6. Strategic Management Accounting to Select, Plan, Implement, Control and Monitor.............11

Conclusion.....................................................................................................................................12

References......................................................................................................................................14

Introduction

The business organizations are needed to take into consideration some specific aspect for

enhancing the overall performance of their business and Value Chain Analysis can be considered

as one of them. Value chain can be considered as a set of activities performed by the companies

in a specific industry for delivering a valuable product to the customers and to add value to the

provided services to the customers (Darmawan, Putra and Wiguna 2014). In simplified words,

value chain helps the companies in adding values to their customers and other stakeholders.

There is a relation between the value chain of the companies with strategic management and

strategic management accounting as the companies can improve the performance of their value

chain with the help of various strategic management tools. At the same time, organizations and

industries also have impact on the value chain of the companies (de Souza and Márcio de

Almeida 2013). The main aim of this report is the analysis and evaluation of various components

of value chain by considering the aspects of strategic management accounting. More specifically,

this report involves in providing advices to Ansell Strategic with the aim to achieve the

objectives for improving the value chain.

1. Enhancement of Value Chain with Various Strategic Management Tools

The earlier discussion has mentioned the fact that the companies can enhance their value

chain with the assistance of various strategic management tools and this aspect is also applicable

for Ansell Strategic. The following discussion provides the description of certain strategic

management tools to enhance the value chain of Ansell Strategic:

The business organizations are needed to take into consideration some specific aspect for

enhancing the overall performance of their business and Value Chain Analysis can be considered

as one of them. Value chain can be considered as a set of activities performed by the companies

in a specific industry for delivering a valuable product to the customers and to add value to the

provided services to the customers (Darmawan, Putra and Wiguna 2014). In simplified words,

value chain helps the companies in adding values to their customers and other stakeholders.

There is a relation between the value chain of the companies with strategic management and

strategic management accounting as the companies can improve the performance of their value

chain with the help of various strategic management tools. At the same time, organizations and

industries also have impact on the value chain of the companies (de Souza and Márcio de

Almeida 2013). The main aim of this report is the analysis and evaluation of various components

of value chain by considering the aspects of strategic management accounting. More specifically,

this report involves in providing advices to Ansell Strategic with the aim to achieve the

objectives for improving the value chain.

1. Enhancement of Value Chain with Various Strategic Management Tools

The earlier discussion has mentioned the fact that the companies can enhance their value

chain with the assistance of various strategic management tools and this aspect is also applicable

for Ansell Strategic. The following discussion provides the description of certain strategic

management tools to enhance the value chain of Ansell Strategic:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

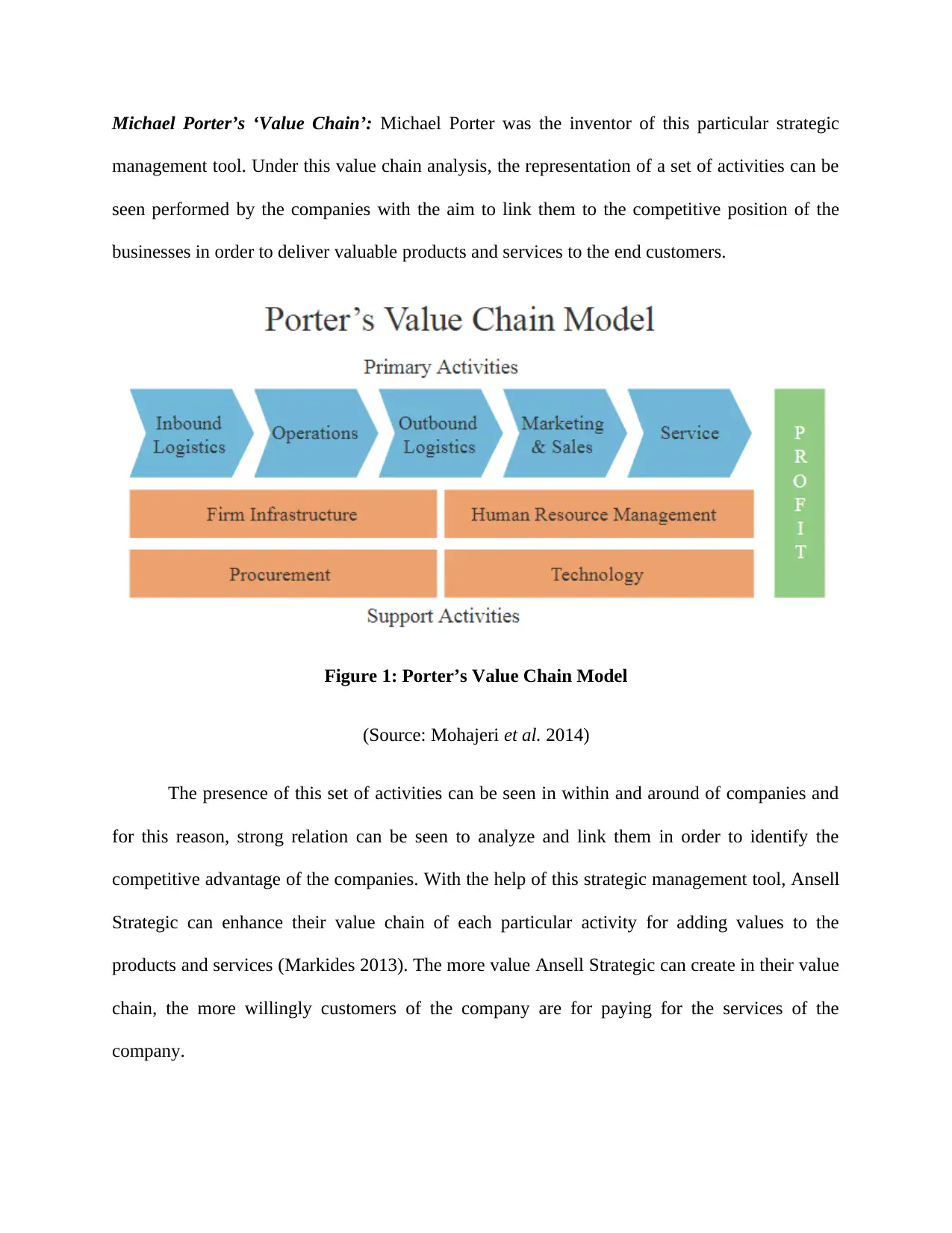

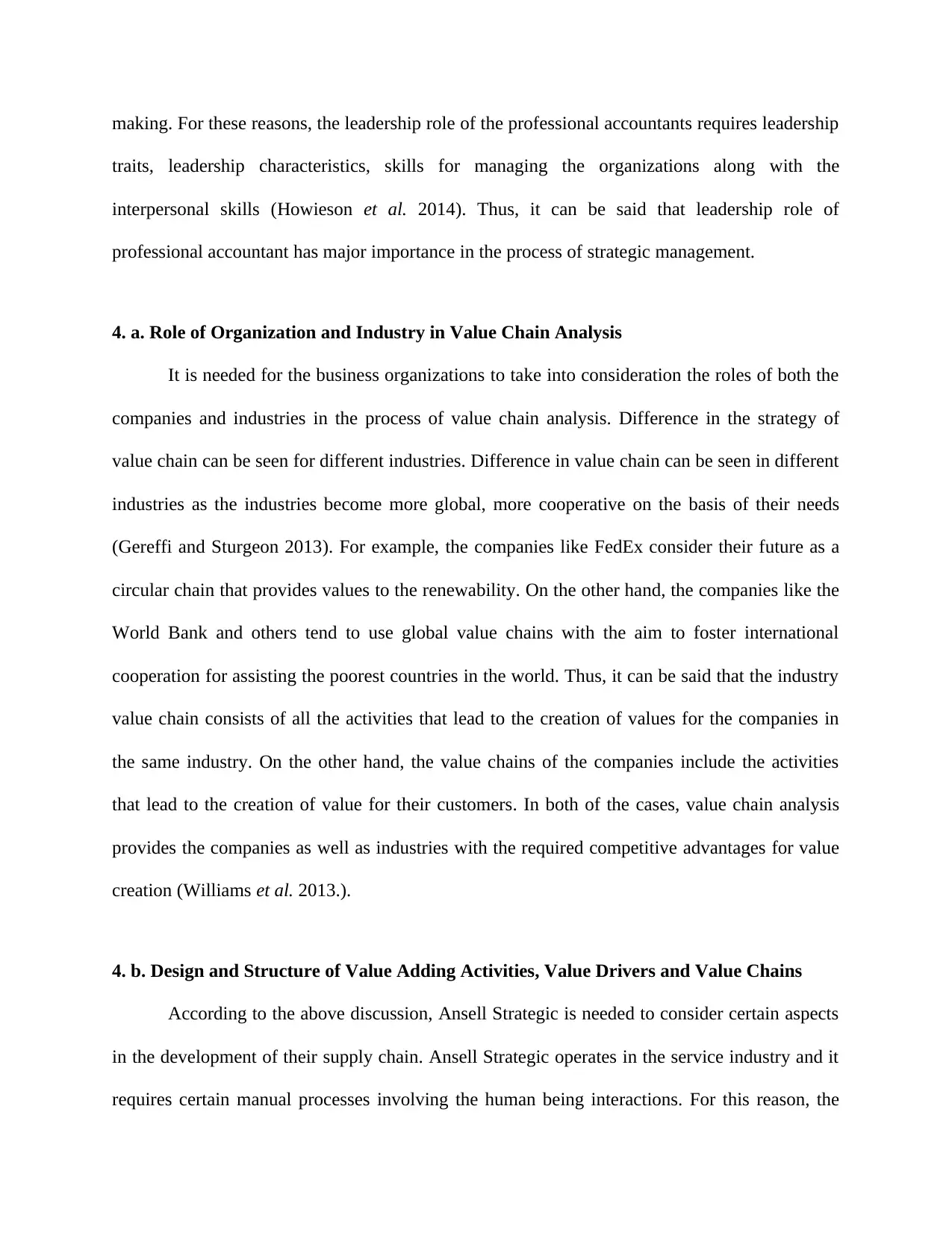

Michael Porter’s ‘Value Chain’: Michael Porter was the inventor of this particular strategic

management tool. Under this value chain analysis, the representation of a set of activities can be

seen performed by the companies with the aim to link them to the competitive position of the

businesses in order to deliver valuable products and services to the end customers.

Figure 1: Porter’s Value Chain Model

(Source: Mohajeri et al. 2014)

The presence of this set of activities can be seen in within and around of companies and

for this reason, strong relation can be seen to analyze and link them in order to identify the

competitive advantage of the companies. With the help of this strategic management tool, Ansell

Strategic can enhance their value chain of each particular activity for adding values to the

products and services (Markides 2013). The more value Ansell Strategic can create in their value

chain, the more willingly customers of the company are for paying for the services of the

company.

management tool. Under this value chain analysis, the representation of a set of activities can be

seen performed by the companies with the aim to link them to the competitive position of the

businesses in order to deliver valuable products and services to the end customers.

Figure 1: Porter’s Value Chain Model

(Source: Mohajeri et al. 2014)

The presence of this set of activities can be seen in within and around of companies and

for this reason, strong relation can be seen to analyze and link them in order to identify the

competitive advantage of the companies. With the help of this strategic management tool, Ansell

Strategic can enhance their value chain of each particular activity for adding values to the

products and services (Markides 2013). The more value Ansell Strategic can create in their value

chain, the more willingly customers of the company are for paying for the services of the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SWOT Analysis: It is considered as a major strategic management tool that can enhance the

value chain of the companies. SWOT stands for strengths, weaknesses, opportunities and threats.

SWOT analysis is regarded as a crucial tool of strategic management that the business

organizations use to identify their strengths and weaknesses; and the opportunities and threats

from them (Hill, Jones and Schilling 2014). This particular tool involves in the identification of

the activities that can lead in value adding to the products and services along with the

unproductive or weak activities. Thus, with the aim of this particle tool, Ansell Strategic can

enhance their value chain and it will ultimately lead to the improvement of performance of their

businesses. Apart from this, Ansell Strategic will also be able in spotting the opportunities and

weaknesses in their value chain (Hill, Jones and Schilling 2014). Hence, it can be said on the

overall basis that SWOT analysis can enhance the value chain of Ansell Strategic.

Gap Analysis: Gap analysis is considered as another important strategic management tool that

helps the business organizations in identifying the current position of the business in the industry

or market. It also helps the companies in the analysis of their progress towards the achievement

of the strategic goals (Morden 2016). More elaborately, the application of gap analysis assists the

companies in measuring the difference between the goals of the companies and their current

position in achieving them. It needs to be mentioned that Ansell Strategic can use the tool of gap

analysis to improve their value chain as it will show their current progress in terms to achieve the

targets related to add value to their products and services (Morden 2016). With the help of gap

analysis, Ansell Strategic will be able in improving the performance of their business activities.

value chain of the companies. SWOT stands for strengths, weaknesses, opportunities and threats.

SWOT analysis is regarded as a crucial tool of strategic management that the business

organizations use to identify their strengths and weaknesses; and the opportunities and threats

from them (Hill, Jones and Schilling 2014). This particular tool involves in the identification of

the activities that can lead in value adding to the products and services along with the

unproductive or weak activities. Thus, with the aim of this particle tool, Ansell Strategic can

enhance their value chain and it will ultimately lead to the improvement of performance of their

businesses. Apart from this, Ansell Strategic will also be able in spotting the opportunities and

weaknesses in their value chain (Hill, Jones and Schilling 2014). Hence, it can be said on the

overall basis that SWOT analysis can enhance the value chain of Ansell Strategic.

Gap Analysis: Gap analysis is considered as another important strategic management tool that

helps the business organizations in identifying the current position of the business in the industry

or market. It also helps the companies in the analysis of their progress towards the achievement

of the strategic goals (Morden 2016). More elaborately, the application of gap analysis assists the

companies in measuring the difference between the goals of the companies and their current

position in achieving them. It needs to be mentioned that Ansell Strategic can use the tool of gap

analysis to improve their value chain as it will show their current progress in terms to achieve the

targets related to add value to their products and services (Morden 2016). With the help of gap

analysis, Ansell Strategic will be able in improving the performance of their business activities.

2. Techniques to Develop, Implement and Monitor Strategies

At the time to develop, implement and monitor the business strategies, it is needed for the

business organizations to consider certain steps; and they are applicable for Ansell Strategic. The

examination and application of these steps are discussed below:

Step 1: At the time of the development of the strategies, Ansell Strategic is needed to designate

the employees to be accountable for achieving the objectives and activities. The company is

required to set the goals and objectives that need to be achieved with the strategies. In the

strategy development process, Ansell Strategic needs to consider what they are expecting from

the employees and staffs related to the strategy (Parmenter 2015). In addition, they are needed to

consider the aspects of communication required for the development of the strategy along with

the results that will be derived from the development and implementation of the strategies.

Step 2: In this particular step or phase, it is needed for Ansell Strategic to address the critical

issues based on the priority by developing strategies to resolve them. At the same time, there is a

need to review of the action plans so that necessary enhancements can be brought. Most

impotently, Ansell Strategic is needed to ensure certain aspect like relation of realistic as well as

measurable objectives with the strategies, designation of responsible individuals for the lead

roles, inclusion of the appropriate people in the strategies, setting of realistic timeline and the

presence of the required resources (Powell et al. 2015).

Step 3: After the development of the strategies, the strategy development committee or the

strategy implementation strategy will involve in their review with the aim to identify the

opportunities to coordinate and combine the required resources (Bryson 2018). The need for

Ansell Strategic is to look for opportunities for collaborating as well as clarifying the role of the

At the time to develop, implement and monitor the business strategies, it is needed for the

business organizations to consider certain steps; and they are applicable for Ansell Strategic. The

examination and application of these steps are discussed below:

Step 1: At the time of the development of the strategies, Ansell Strategic is needed to designate

the employees to be accountable for achieving the objectives and activities. The company is

required to set the goals and objectives that need to be achieved with the strategies. In the

strategy development process, Ansell Strategic needs to consider what they are expecting from

the employees and staffs related to the strategy (Parmenter 2015). In addition, they are needed to

consider the aspects of communication required for the development of the strategy along with

the results that will be derived from the development and implementation of the strategies.

Step 2: In this particular step or phase, it is needed for Ansell Strategic to address the critical

issues based on the priority by developing strategies to resolve them. At the same time, there is a

need to review of the action plans so that necessary enhancements can be brought. Most

impotently, Ansell Strategic is needed to ensure certain aspect like relation of realistic as well as

measurable objectives with the strategies, designation of responsible individuals for the lead

roles, inclusion of the appropriate people in the strategies, setting of realistic timeline and the

presence of the required resources (Powell et al. 2015).

Step 3: After the development of the strategies, the strategy development committee or the

strategy implementation strategy will involve in their review with the aim to identify the

opportunities to coordinate and combine the required resources (Bryson 2018). The need for

Ansell Strategic is to look for opportunities for collaborating as well as clarifying the role of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

committee. In addition, the management of Ansell Strategic needs to ensure regular contact with

the implementation team with the aim to ensure that all the implementation activities are on

track.

Step 4: After the above step, it is needed for Ansell Strategic to involve in the evaluation of the

implemented strategies with the aim to assess the extent of the accomplishment of the goals and

objectives. Ansell Strategic can do this by simply tracking the activities as well as progress

towards achieving the goals and objectives. In the presence of these steps, Ansell Strategic will

be able in assessing the fact that whether they have been successful in achieving the goals and

objectives (Dhaliwal et al. 2014).

Step 5: In this last step, the requirement for Ansell Strategic is to make the necessary corrections

as per the results of the evaluation of the strategies. In this phrase, the main aim of Ansell

Strategic will be to spot any kind of inefficiencies in the business activities. In case the company

find any loophole or inefficiency in the process, the need for the management is to take the

corrective measures with the aim to eradicate those efficiencies from the strategies. Thus, Ansell

Strategic needs to follow all these steps in the process to develop, implement and monitor

strategies (Powell et al. 2015).

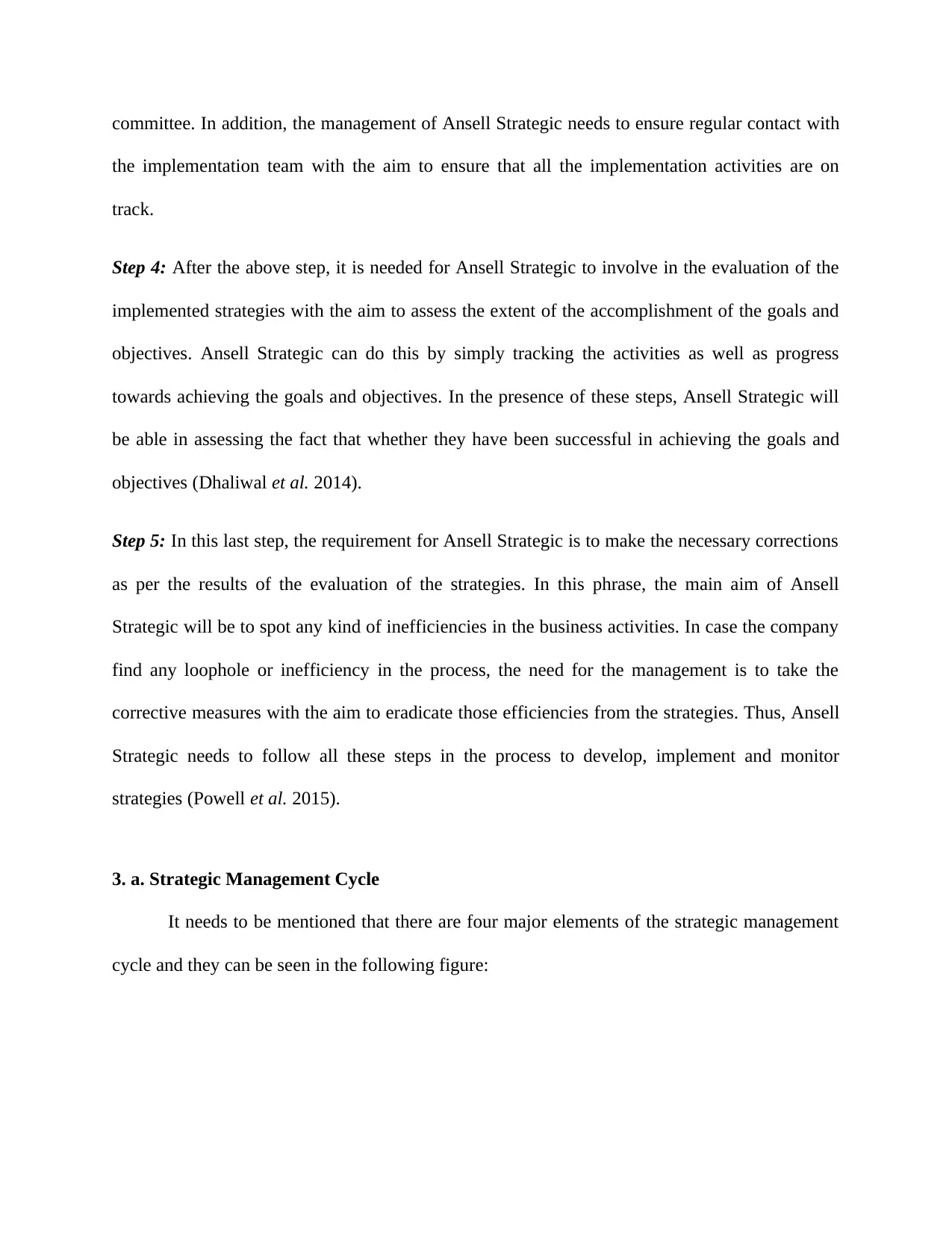

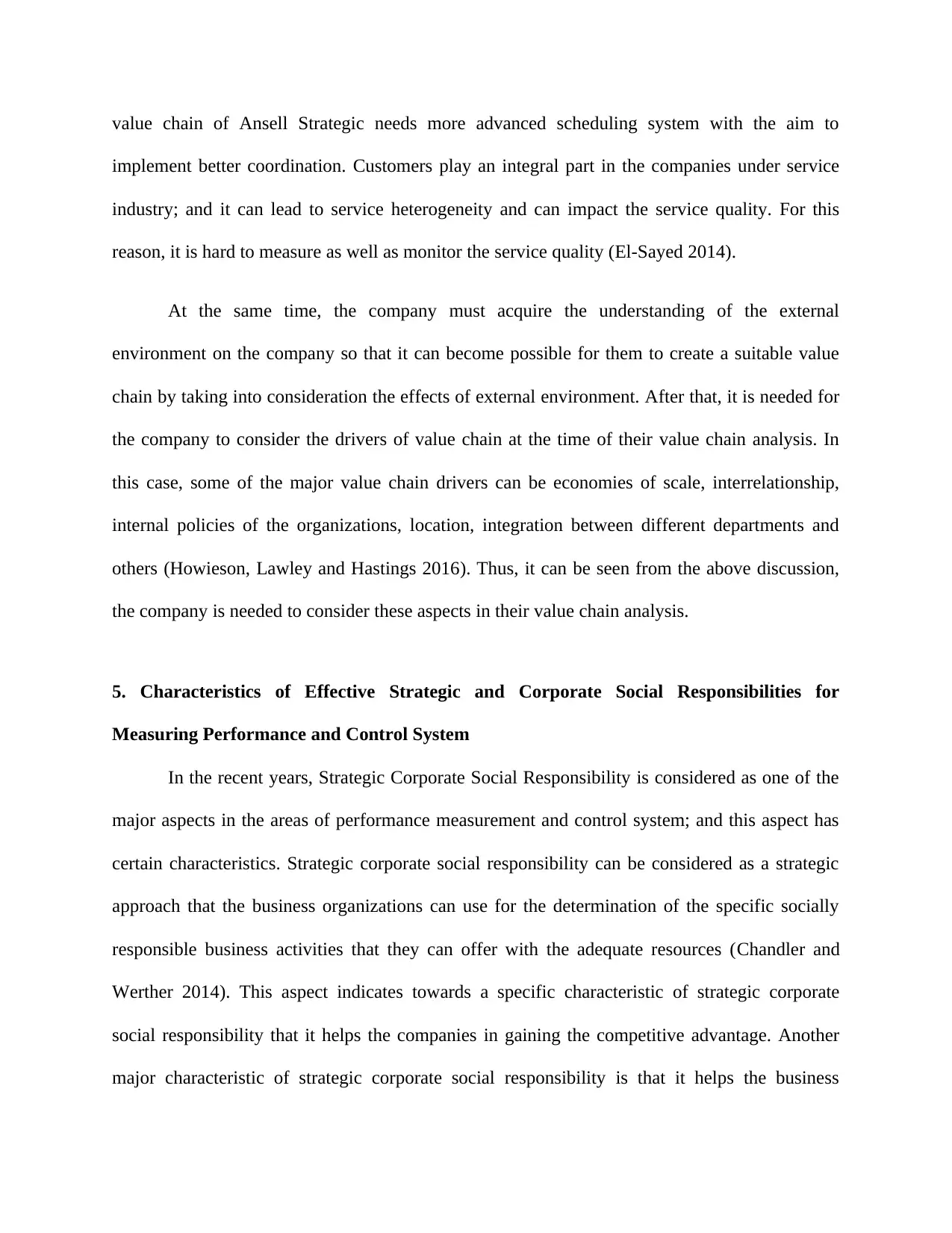

3. a. Strategic Management Cycle

It needs to be mentioned that there are four major elements of the strategic management

cycle and they can be seen in the following figure:

the implementation team with the aim to ensure that all the implementation activities are on

track.

Step 4: After the above step, it is needed for Ansell Strategic to involve in the evaluation of the

implemented strategies with the aim to assess the extent of the accomplishment of the goals and

objectives. Ansell Strategic can do this by simply tracking the activities as well as progress

towards achieving the goals and objectives. In the presence of these steps, Ansell Strategic will

be able in assessing the fact that whether they have been successful in achieving the goals and

objectives (Dhaliwal et al. 2014).

Step 5: In this last step, the requirement for Ansell Strategic is to make the necessary corrections

as per the results of the evaluation of the strategies. In this phrase, the main aim of Ansell

Strategic will be to spot any kind of inefficiencies in the business activities. In case the company

find any loophole or inefficiency in the process, the need for the management is to take the

corrective measures with the aim to eradicate those efficiencies from the strategies. Thus, Ansell

Strategic needs to follow all these steps in the process to develop, implement and monitor

strategies (Powell et al. 2015).

3. a. Strategic Management Cycle

It needs to be mentioned that there are four major elements of the strategic management

cycle and they can be seen in the following figure:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 2: Strategic Management Cycle

(Source: Rothaermel 2015)

Strategy Formulation: This stage involve in identifying the organizational objective that needs

to be achieved through the strategies. In this stage, managements of the companies analyze what

the competitors are doing with the aim to respond. Brainstorming is considered as a major aspect

in this stage as the managements of the companies use to gather ideas from different employees

and staffs of the companies with the aim to develop strategies (Eden and Ackermann 2013).

Planning: This stage involves in specifying the broad aims into action plans for the ease of the

organizational employee and staffs. More specifically, the planning process involves in

translating the top level strategies into the actionable activities for the purpose of

implementation. Many business organizations opt for SMART target for the purpose of activity

planning. In this stage, strategies began to become reality (Ginter, Duncan and Swayne 2018).

Implementation: Enactment of the strategies can be seen in the stage of implementation. This

stage in strategic management cycle involves in the use of the action plans and it leads to the

happening of the real works. The aim of this stage is to solve the real world business problems.

(Source: Rothaermel 2015)

Strategy Formulation: This stage involve in identifying the organizational objective that needs

to be achieved through the strategies. In this stage, managements of the companies analyze what

the competitors are doing with the aim to respond. Brainstorming is considered as a major aspect

in this stage as the managements of the companies use to gather ideas from different employees

and staffs of the companies with the aim to develop strategies (Eden and Ackermann 2013).

Planning: This stage involves in specifying the broad aims into action plans for the ease of the

organizational employee and staffs. More specifically, the planning process involves in

translating the top level strategies into the actionable activities for the purpose of

implementation. Many business organizations opt for SMART target for the purpose of activity

planning. In this stage, strategies began to become reality (Ginter, Duncan and Swayne 2018).

Implementation: Enactment of the strategies can be seen in the stage of implementation. This

stage in strategic management cycle involves in the use of the action plans and it leads to the

happening of the real works. The aim of this stage is to solve the real world business problems.

This step requires the adaptation as well as modifications of certain plans (Alkhafaji and Nelson

2013).

Review: This particular step helps the managements of the companies in assessing their actual

position and where they want to be. This stage involves in the identification of the strong as well

as weak areas of the strategies with the aim to take corrective measures. This stage provides the

managements with the scope to bring continuous improvements in the implemented strategies for

the businesses (Simon, Fischbach and Schoder 2014).

3. b. Leadership Role of Professional Accountants in Strategic Management

Leadership role of the professional accountants involves that the professional accountants

always respond to the contiguously changing expectations of the companies, societies and

financial markets. It indicates towards various roles of the professional accountants like

leadership in management, operations, management control and stakeholders and accounting

communication (Goretzki, Strauss and Weber 2013). Many instances can be seen where the

accounting professionals have aspired to the roles of accounting leadership like Chief Financial

Officer, Financial Controller and others. Under these roles, the professional accountants become

responsible for all the financial matters and aspects in the companies and it demands technical

skills and specialized knowledge in the accounting areas like taxation, financial reporting,

treasury and others (Goretzki, Strauss and Weber 2013).

Business organizations emphasize on the aspect of financial leadership with the aim to

ensure that all the financial and accounting activities support the good performance of the whole

organization. For this reason, the requirement for the professional accountants is to fulfill their

basic duties along with providing support in the processes of operations and tragic decision-

2013).

Review: This particular step helps the managements of the companies in assessing their actual

position and where they want to be. This stage involves in the identification of the strong as well

as weak areas of the strategies with the aim to take corrective measures. This stage provides the

managements with the scope to bring continuous improvements in the implemented strategies for

the businesses (Simon, Fischbach and Schoder 2014).

3. b. Leadership Role of Professional Accountants in Strategic Management

Leadership role of the professional accountants involves that the professional accountants

always respond to the contiguously changing expectations of the companies, societies and

financial markets. It indicates towards various roles of the professional accountants like

leadership in management, operations, management control and stakeholders and accounting

communication (Goretzki, Strauss and Weber 2013). Many instances can be seen where the

accounting professionals have aspired to the roles of accounting leadership like Chief Financial

Officer, Financial Controller and others. Under these roles, the professional accountants become

responsible for all the financial matters and aspects in the companies and it demands technical

skills and specialized knowledge in the accounting areas like taxation, financial reporting,

treasury and others (Goretzki, Strauss and Weber 2013).

Business organizations emphasize on the aspect of financial leadership with the aim to

ensure that all the financial and accounting activities support the good performance of the whole

organization. For this reason, the requirement for the professional accountants is to fulfill their

basic duties along with providing support in the processes of operations and tragic decision-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

making. For these reasons, the leadership role of the professional accountants requires leadership

traits, leadership characteristics, skills for managing the organizations along with the

interpersonal skills (Howieson et al. 2014). Thus, it can be said that leadership role of

professional accountant has major importance in the process of strategic management.

4. a. Role of Organization and Industry in Value Chain Analysis

It is needed for the business organizations to take into consideration the roles of both the

companies and industries in the process of value chain analysis. Difference in the strategy of

value chain can be seen for different industries. Difference in value chain can be seen in different

industries as the industries become more global, more cooperative on the basis of their needs

(Gereffi and Sturgeon 2013). For example, the companies like FedEx consider their future as a

circular chain that provides values to the renewability. On the other hand, the companies like the

World Bank and others tend to use global value chains with the aim to foster international

cooperation for assisting the poorest countries in the world. Thus, it can be said that the industry

value chain consists of all the activities that lead to the creation of values for the companies in

the same industry. On the other hand, the value chains of the companies include the activities

that lead to the creation of value for their customers. In both of the cases, value chain analysis

provides the companies as well as industries with the required competitive advantages for value

creation (Williams et al. 2013.).

4. b. Design and Structure of Value Adding Activities, Value Drivers and Value Chains

According to the above discussion, Ansell Strategic is needed to consider certain aspects

in the development of their supply chain. Ansell Strategic operates in the service industry and it

requires certain manual processes involving the human being interactions. For this reason, the

traits, leadership characteristics, skills for managing the organizations along with the

interpersonal skills (Howieson et al. 2014). Thus, it can be said that leadership role of

professional accountant has major importance in the process of strategic management.

4. a. Role of Organization and Industry in Value Chain Analysis

It is needed for the business organizations to take into consideration the roles of both the

companies and industries in the process of value chain analysis. Difference in the strategy of

value chain can be seen for different industries. Difference in value chain can be seen in different

industries as the industries become more global, more cooperative on the basis of their needs

(Gereffi and Sturgeon 2013). For example, the companies like FedEx consider their future as a

circular chain that provides values to the renewability. On the other hand, the companies like the

World Bank and others tend to use global value chains with the aim to foster international

cooperation for assisting the poorest countries in the world. Thus, it can be said that the industry

value chain consists of all the activities that lead to the creation of values for the companies in

the same industry. On the other hand, the value chains of the companies include the activities

that lead to the creation of value for their customers. In both of the cases, value chain analysis

provides the companies as well as industries with the required competitive advantages for value

creation (Williams et al. 2013.).

4. b. Design and Structure of Value Adding Activities, Value Drivers and Value Chains

According to the above discussion, Ansell Strategic is needed to consider certain aspects

in the development of their supply chain. Ansell Strategic operates in the service industry and it

requires certain manual processes involving the human being interactions. For this reason, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

value chain of Ansell Strategic needs more advanced scheduling system with the aim to

implement better coordination. Customers play an integral part in the companies under service

industry; and it can lead to service heterogeneity and can impact the service quality. For this

reason, it is hard to measure as well as monitor the service quality (El-Sayed 2014).

At the same time, the company must acquire the understanding of the external

environment on the company so that it can become possible for them to create a suitable value

chain by taking into consideration the effects of external environment. After that, it is needed for

the company to consider the drivers of value chain at the time of their value chain analysis. In

this case, some of the major value chain drivers can be economies of scale, interrelationship,

internal policies of the organizations, location, integration between different departments and

others (Howieson, Lawley and Hastings 2016). Thus, it can be seen from the above discussion,

the company is needed to consider these aspects in their value chain analysis.

5. Characteristics of Effective Strategic and Corporate Social Responsibilities for

Measuring Performance and Control System

In the recent years, Strategic Corporate Social Responsibility is considered as one of the

major aspects in the areas of performance measurement and control system; and this aspect has

certain characteristics. Strategic corporate social responsibility can be considered as a strategic

approach that the business organizations can use for the determination of the specific socially

responsible business activities that they can offer with the adequate resources (Chandler and

Werther 2014). This aspect indicates towards a specific characteristic of strategic corporate

social responsibility that it helps the companies in gaining the competitive advantage. Another

major characteristic of strategic corporate social responsibility is that it helps the business

implement better coordination. Customers play an integral part in the companies under service

industry; and it can lead to service heterogeneity and can impact the service quality. For this

reason, it is hard to measure as well as monitor the service quality (El-Sayed 2014).

At the same time, the company must acquire the understanding of the external

environment on the company so that it can become possible for them to create a suitable value

chain by taking into consideration the effects of external environment. After that, it is needed for

the company to consider the drivers of value chain at the time of their value chain analysis. In

this case, some of the major value chain drivers can be economies of scale, interrelationship,

internal policies of the organizations, location, integration between different departments and

others (Howieson, Lawley and Hastings 2016). Thus, it can be seen from the above discussion,

the company is needed to consider these aspects in their value chain analysis.

5. Characteristics of Effective Strategic and Corporate Social Responsibilities for

Measuring Performance and Control System

In the recent years, Strategic Corporate Social Responsibility is considered as one of the

major aspects in the areas of performance measurement and control system; and this aspect has

certain characteristics. Strategic corporate social responsibility can be considered as a strategic

approach that the business organizations can use for the determination of the specific socially

responsible business activities that they can offer with the adequate resources (Chandler and

Werther 2014). This aspect indicates towards a specific characteristic of strategic corporate

social responsibility that it helps the companies in gaining the competitive advantage. Another

major characteristic of strategic corporate social responsibility is that it helps the business

organizations to follow the components of the generic strategies of business and this aspect helps

the companies in establishing effective control on the business operations (Chandler and Werther

2014).

At the same time, strategic corporate social responsibility helps the firms in maintaining

an optimal balance between the creations of economic value with the societal value. After that,

the business organizations can manage the relationship of different stakeholders with the

assistance of strategic corporate social responsibility. In case of the measurement of business

performance, one major characteristic of strategic corporate social responsibility is that it helps

the companies in the identification of the threats and opportunities in case of stakeholder

managements. In this way, they can measure the performance of their business. Most

importantly, business organizations become able in creating new business opportunities with the

help of strategic corporate social responsibility and it ensures the improved performance of the

business organizations (Michelon, Boesso and Kumar 2013).

6. Strategic Management Accounting to Select, Plan, Implement, Control and Monitor

It needs to be mentioned that there are certain strategic management accounting

techniques that can help Ansell Strategic in the process to select, plan, implement, control and

monitor the business activities; and they are discussed below:

Activity Based Costing can be regarded as a major strategic management accounting tool

that Ansell Strategic can implement to plan their costing activities as this method is based

on identifying the business activities performed by the companies. It will help the

company in knowing the causes of indirect cost of the companies so that the business

activities can be planned accordingly (Kaplan and Atkinson 2015).

the companies in establishing effective control on the business operations (Chandler and Werther

2014).

At the same time, strategic corporate social responsibility helps the firms in maintaining

an optimal balance between the creations of economic value with the societal value. After that,

the business organizations can manage the relationship of different stakeholders with the

assistance of strategic corporate social responsibility. In case of the measurement of business

performance, one major characteristic of strategic corporate social responsibility is that it helps

the companies in the identification of the threats and opportunities in case of stakeholder

managements. In this way, they can measure the performance of their business. Most

importantly, business organizations become able in creating new business opportunities with the

help of strategic corporate social responsibility and it ensures the improved performance of the

business organizations (Michelon, Boesso and Kumar 2013).

6. Strategic Management Accounting to Select, Plan, Implement, Control and Monitor

It needs to be mentioned that there are certain strategic management accounting

techniques that can help Ansell Strategic in the process to select, plan, implement, control and

monitor the business activities; and they are discussed below:

Activity Based Costing can be regarded as a major strategic management accounting tool

that Ansell Strategic can implement to plan their costing activities as this method is based

on identifying the business activities performed by the companies. It will help the

company in knowing the causes of indirect cost of the companies so that the business

activities can be planned accordingly (Kaplan and Atkinson 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.