Case Study: Strategic Marketing in the Australian Dairy Industry

VerifiedAdded on 2023/06/15

|16

|4479

|324

Case Study

AI Summary

This case study analyzes the Australian dairy industry using the 7-step case analysis framework. It addresses the product life cycle of cheese and butter, suggesting marketing strategies for each stage, and interprets a portfolio matrix for dairy producer DP A based on milk sales data. It also examines the impact of supermarket pricing strategies on the dairy industry and recommends steps for dairy producers to manage supermarket market power. The analysis includes insights on changing consumer preferences, market share, and the importance of focusing on growing product categories like UHT milk. This document is available on Desklib, a platform offering a wide range of study resources and solved assignments for students.

Running Head: Strategic Marketing

Australian Daily Industry

Strategic Marketing

Case Study Questions

Australian Daily Industry

Strategic Marketing

Case Study Questions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Marketing P a g e | 1

Table of Content

Introduction...........................................................................................................................................2

Question 1.............................................................................................................................................3

Answer 1................................................................................................................................................3

Product life cycle Stages....................................................................................................................4

Introduction Stage.................................................................................................................4

Growth stage-........................................................................................................................4

Maturity stage.......................................................................................................................4

Decline stage..........................................................................................................................4

Marketing Strategies.........................................................................................................................5

Question 2.............................................................................................................................................6

Answer 2................................................................................................................................................6

Exhibit 4.............................................................................................................................................7

Interpretation....................................................................................................................................8

Exhibit 5.............................................................................................................................................8

Question 4...........................................................................................................................................10

Answer.................................................................................................................................................11

References...........................................................................................................................................14

Table of Content

Introduction...........................................................................................................................................2

Question 1.............................................................................................................................................3

Answer 1................................................................................................................................................3

Product life cycle Stages....................................................................................................................4

Introduction Stage.................................................................................................................4

Growth stage-........................................................................................................................4

Maturity stage.......................................................................................................................4

Decline stage..........................................................................................................................4

Marketing Strategies.........................................................................................................................5

Question 2.............................................................................................................................................6

Answer 2................................................................................................................................................6

Exhibit 4.............................................................................................................................................7

Interpretation....................................................................................................................................8

Exhibit 5.............................................................................................................................................8

Question 4...........................................................................................................................................10

Answer.................................................................................................................................................11

References...........................................................................................................................................14

Strategic Marketing P a g e | 2

Introduction

The case study here is based on the Australian Dairy Milk industry; the report contains many

exhibits and insights on the sale of different dairy products. It has been seen that the

Australian industry despite facing a tough time in the year 2008 was resilient; however its

international demand was falling (Australia, 2017). The case study has 4 questions which

need to be answered in the purview of 7 step case analysis framework, which goes as:

Situation Analysis

Assumption and missing information

Statement of Problem

Development of alternatives

Evaluation of alternatives and recommendation

Implementation

Evaluation and Control

Introduction

The case study here is based on the Australian Dairy Milk industry; the report contains many

exhibits and insights on the sale of different dairy products. It has been seen that the

Australian industry despite facing a tough time in the year 2008 was resilient; however its

international demand was falling (Australia, 2017). The case study has 4 questions which

need to be answered in the purview of 7 step case analysis framework, which goes as:

Situation Analysis

Assumption and missing information

Statement of Problem

Development of alternatives

Evaluation of alternatives and recommendation

Implementation

Evaluation and Control

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Marketing P a g e | 3

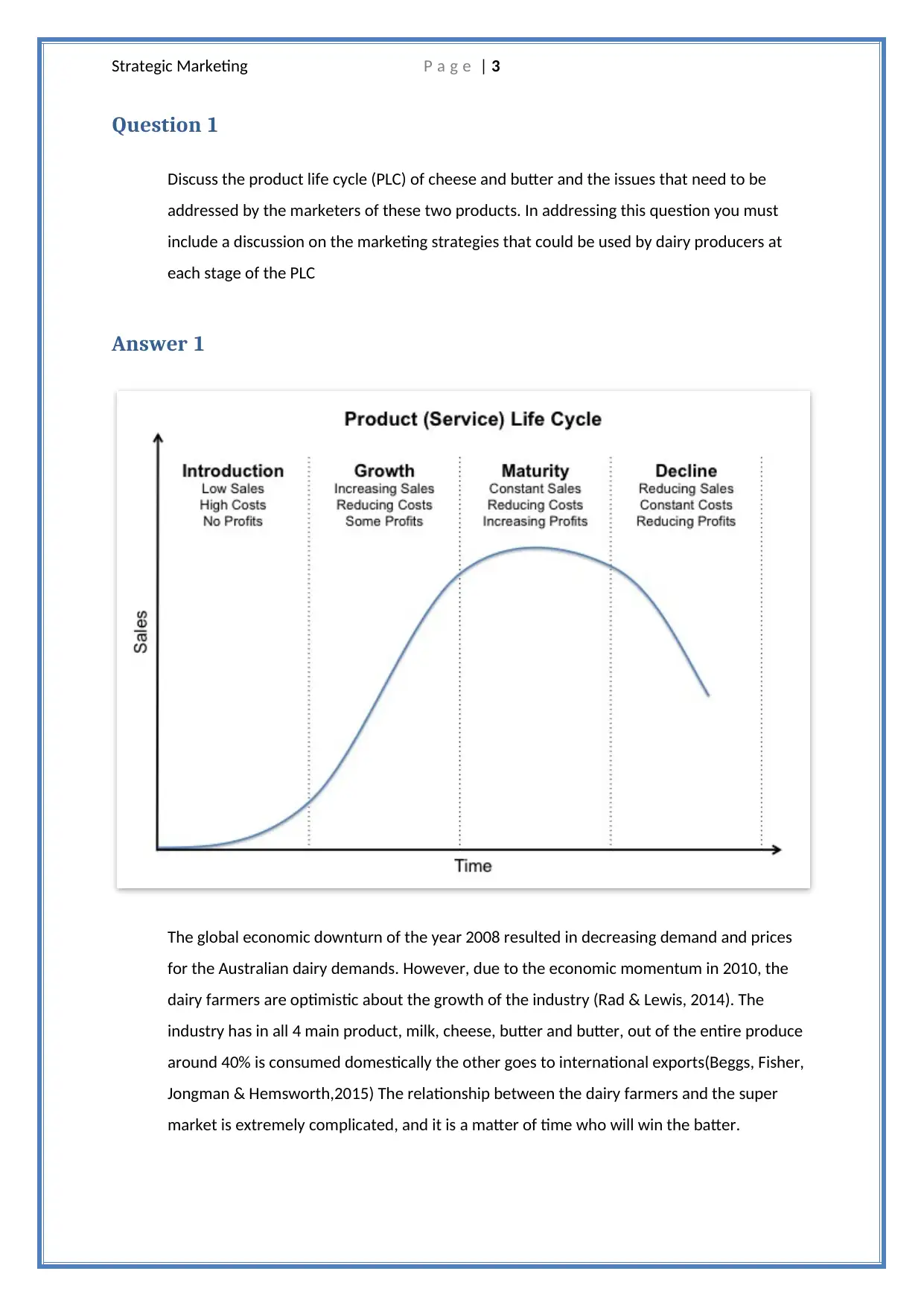

Question 1

Discuss the product life cycle (PLC) of cheese and butter and the issues that need to be

addressed by the marketers of these two products. In addressing this question you must

include a discussion on the marketing strategies that could be used by dairy producers at

each stage of the PLC

Answer 1

The global economic downturn of the year 2008 resulted in decreasing demand and prices

for the Australian dairy demands. However, due to the economic momentum in 2010, the

dairy farmers are optimistic about the growth of the industry (Rad & Lewis, 2014). The

industry has in all 4 main product, milk, cheese, butter and butter, out of the entire produce

around 40% is consumed domestically the other goes to international exports(Beggs, Fisher,

Jongman & Hemsworth,2015) The relationship between the dairy farmers and the super

market is extremely complicated, and it is a matter of time who will win the batter.

Question 1

Discuss the product life cycle (PLC) of cheese and butter and the issues that need to be

addressed by the marketers of these two products. In addressing this question you must

include a discussion on the marketing strategies that could be used by dairy producers at

each stage of the PLC

Answer 1

The global economic downturn of the year 2008 resulted in decreasing demand and prices

for the Australian dairy demands. However, due to the economic momentum in 2010, the

dairy farmers are optimistic about the growth of the industry (Rad & Lewis, 2014). The

industry has in all 4 main product, milk, cheese, butter and butter, out of the entire produce

around 40% is consumed domestically the other goes to international exports(Beggs, Fisher,

Jongman & Hemsworth,2015) The relationship between the dairy farmers and the super

market is extremely complicated, and it is a matter of time who will win the batter.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Marketing P a g e | 4

Life can be seen as a series of development and changes which results in peak, decline and

eventually demise. Similarly, consumer products also go through the four distinct cycles in

the entire life, the implication of life cycle stages for managers is to create strategies to

maximize the profits of the company (Stark, 2015).

Product life cycle Stages

Introduction Stage-This is the stage when the product is new and unknown to the

customers, people involved in the early age are innovators and some being part of the early

adopters. During this stage the strategy has to be proactive in order to win over other

customers. Butter and cheese are the products which are already known to the marketers;

hence they don’t have to spend much in increasing the awareness of the product. However,

they have to use different variant of Cheese which are becoming popular in the market to

increase the penetration. In terms of monetary transaction, the revenues and profits are low

and negative and the industry has to be buckled up towards the marketing

spend(Armstrong, Kotler, Harker & Brennan,2015)

Growth stage-At this stage, customers have good awareness about the product and the

company earns benefit from the stage. At the same time, the production capacity can be

increased of butter and cheese resulting in the economies of scale. In this stage, competition

increases and price becomes an important part of the marketing strategy here (Bilir, 2014).

Maturity stage-This is the stage of the PLC when the market becomes extremely saturated.

This stage is accompanied by reducing production cost which eventually leads to economies

of scale and experience. Cheese and Butter are already in the maturity stage, and the

industry is in price wars with the supermarkets (Fantake & Jolliet, 2016).

Decline stage-This is the last stage of the PLC and is masked by decreasing or stabilized

sales. This stage results in lower price margins. At this point the product is discontinued, this

is the stage which is most useful for butter and cheese, Form this point they should start the

PLC of different variety of cheese and butter to further penetrate the market (Tao & Yu,

2018).

The analysis of Product life cycle for Butter and Cheese of dairy industry of Australia implies

that the product is in the maturity stage and before it gets to decline stage it should

introduce new variant of butter and cheese to again start the new Product life cycle with

new variant.

Life can be seen as a series of development and changes which results in peak, decline and

eventually demise. Similarly, consumer products also go through the four distinct cycles in

the entire life, the implication of life cycle stages for managers is to create strategies to

maximize the profits of the company (Stark, 2015).

Product life cycle Stages

Introduction Stage-This is the stage when the product is new and unknown to the

customers, people involved in the early age are innovators and some being part of the early

adopters. During this stage the strategy has to be proactive in order to win over other

customers. Butter and cheese are the products which are already known to the marketers;

hence they don’t have to spend much in increasing the awareness of the product. However,

they have to use different variant of Cheese which are becoming popular in the market to

increase the penetration. In terms of monetary transaction, the revenues and profits are low

and negative and the industry has to be buckled up towards the marketing

spend(Armstrong, Kotler, Harker & Brennan,2015)

Growth stage-At this stage, customers have good awareness about the product and the

company earns benefit from the stage. At the same time, the production capacity can be

increased of butter and cheese resulting in the economies of scale. In this stage, competition

increases and price becomes an important part of the marketing strategy here (Bilir, 2014).

Maturity stage-This is the stage of the PLC when the market becomes extremely saturated.

This stage is accompanied by reducing production cost which eventually leads to economies

of scale and experience. Cheese and Butter are already in the maturity stage, and the

industry is in price wars with the supermarkets (Fantake & Jolliet, 2016).

Decline stage-This is the last stage of the PLC and is masked by decreasing or stabilized

sales. This stage results in lower price margins. At this point the product is discontinued, this

is the stage which is most useful for butter and cheese, Form this point they should start the

PLC of different variety of cheese and butter to further penetrate the market (Tao & Yu,

2018).

The analysis of Product life cycle for Butter and Cheese of dairy industry of Australia implies

that the product is in the maturity stage and before it gets to decline stage it should

introduce new variant of butter and cheese to again start the new Product life cycle with

new variant.

Strategic Marketing P a g e | 5

Marketing Strategies

As mentioned in the earlier section dairy producers have to adopt various strategies for the

optimum utilization of the product life cycle stages

Product Life cycle Stage Marketing Strategies

Introduction Rapid skimming-This strategy is launching the

product at high price to make maximum

profit and high level of promotion.

Slow skimming-This stage is characterized by

high price and low promotions.

Rapid penetration-In this strategy the product is

launched at a low price followed by

aggressive promotion.

Slow penetration-Launch the product at low

price and low promotions(Kotabe &

Helsen, 2014)

Growth The following strategies are helpful during the

growth stage:

Improvement in the quality of product

Addition of new variant in the existing

product and add customer support

service.

Entering into new market segments.

Skimming the price if the profits are still

low.

Increase in the distribution channel to

manage the increasing demand (Charter

& Tischner, 2017).

Maturity The following strategies are to be used here:

Market Modification-Redefining the

target market, moving to different

segment, tries to win the competitors

customers and so on.

Product Modification-adjusting the

product in terms of quality, pricing,

packaging, promotion in accordance

with the marketing mix(Lockrey, 2015)

Decline The strategies which the farm producers should

adopt here are:

Reduction in the promotional

expenditure.

Reduction in the number of distribution

centres.

Implementing price cuts.

Maintain the product and wait for

competitor to remove their product

from the market(Ottman, 2017)

Reduction in the price to sell out the

entire inventory.

Marketing Strategies

As mentioned in the earlier section dairy producers have to adopt various strategies for the

optimum utilization of the product life cycle stages

Product Life cycle Stage Marketing Strategies

Introduction Rapid skimming-This strategy is launching the

product at high price to make maximum

profit and high level of promotion.

Slow skimming-This stage is characterized by

high price and low promotions.

Rapid penetration-In this strategy the product is

launched at a low price followed by

aggressive promotion.

Slow penetration-Launch the product at low

price and low promotions(Kotabe &

Helsen, 2014)

Growth The following strategies are helpful during the

growth stage:

Improvement in the quality of product

Addition of new variant in the existing

product and add customer support

service.

Entering into new market segments.

Skimming the price if the profits are still

low.

Increase in the distribution channel to

manage the increasing demand (Charter

& Tischner, 2017).

Maturity The following strategies are to be used here:

Market Modification-Redefining the

target market, moving to different

segment, tries to win the competitors

customers and so on.

Product Modification-adjusting the

product in terms of quality, pricing,

packaging, promotion in accordance

with the marketing mix(Lockrey, 2015)

Decline The strategies which the farm producers should

adopt here are:

Reduction in the promotional

expenditure.

Reduction in the number of distribution

centres.

Implementing price cuts.

Maintain the product and wait for

competitor to remove their product

from the market(Ottman, 2017)

Reduction in the price to sell out the

entire inventory.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Marketing P a g e | 6

Hence, it is very important and critical to reassess the Product life cycle of the dairy products

and change the pricing strategy to better suit the needs of the customer to ensure

consistent sale in the dairy items. It has been observed in the case study, how different

consumers have been moving to different variety of products of cheese and milk. Health

conscious people are moving from high fat milk to low fat milk and so on. Thus, assessing the

business market and creating strategies in accordance with the Product life cycle will help

Australian farm industry to achieve momentum in the growth.

Question 2

Using the information provided in Exhibit 4 and 5 elaborate and interpret a portfolio matrix

for the dairy producer DP A. In responding to this question it is recommended only milk sales

for 2008-09 and 2009-10 periods are used.

Answer 2

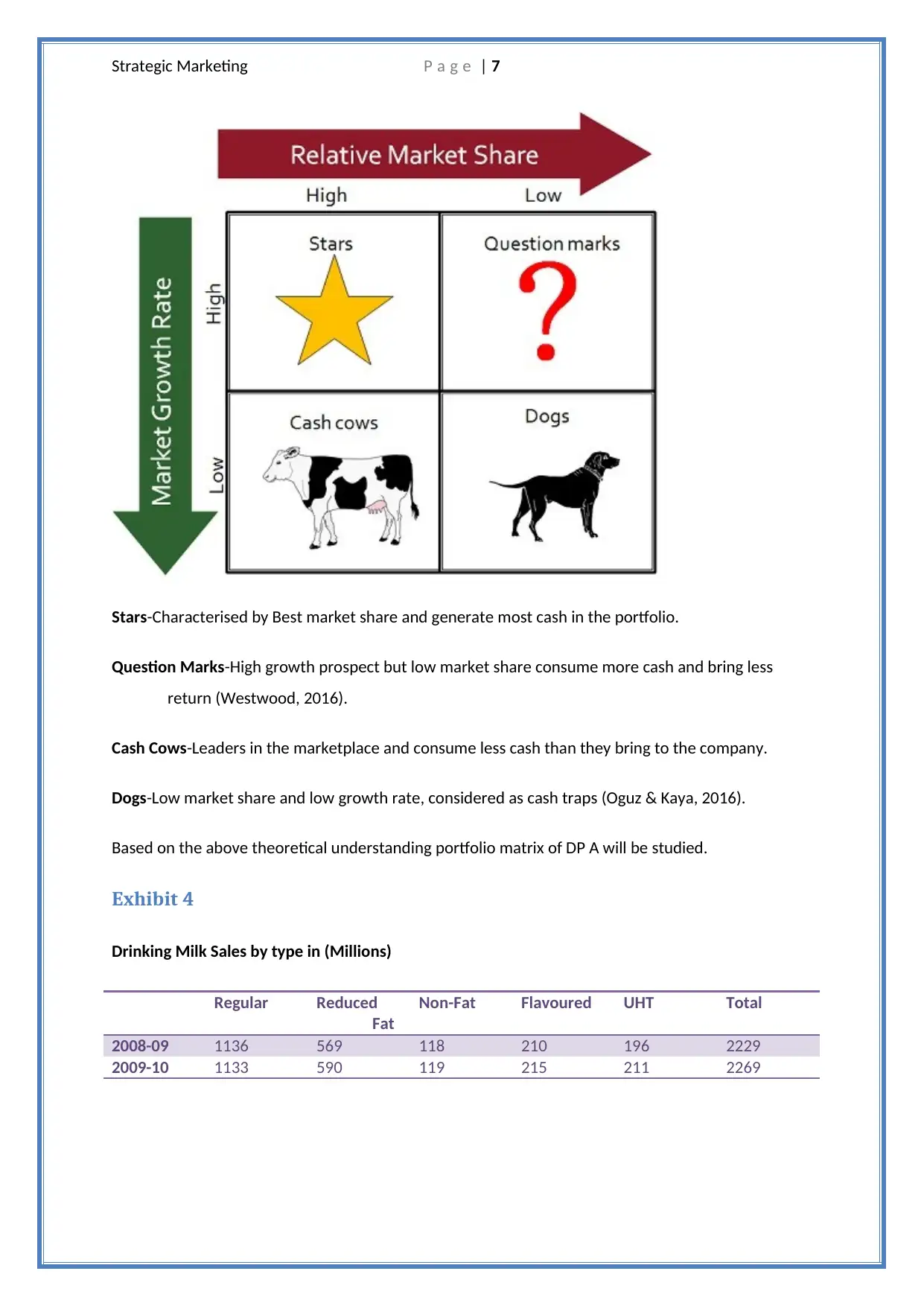

A portfolio matrix can be understood as a chart which is used to define products in terms of

both the growth in their industry and their specific market share. A BCG matrix is used to

define the portfolio matrix of any organization (Gito & Kumar, 2014). There are 4 quadrants

in Portfolio matrix which define the growth and the specific market share in the industry:

Hence, it is very important and critical to reassess the Product life cycle of the dairy products

and change the pricing strategy to better suit the needs of the customer to ensure

consistent sale in the dairy items. It has been observed in the case study, how different

consumers have been moving to different variety of products of cheese and milk. Health

conscious people are moving from high fat milk to low fat milk and so on. Thus, assessing the

business market and creating strategies in accordance with the Product life cycle will help

Australian farm industry to achieve momentum in the growth.

Question 2

Using the information provided in Exhibit 4 and 5 elaborate and interpret a portfolio matrix

for the dairy producer DP A. In responding to this question it is recommended only milk sales

for 2008-09 and 2009-10 periods are used.

Answer 2

A portfolio matrix can be understood as a chart which is used to define products in terms of

both the growth in their industry and their specific market share. A BCG matrix is used to

define the portfolio matrix of any organization (Gito & Kumar, 2014). There are 4 quadrants

in Portfolio matrix which define the growth and the specific market share in the industry:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Marketing P a g e | 7

Stars-Characterised by Best market share and generate most cash in the portfolio.

Question Marks-High growth prospect but low market share consume more cash and bring less

return (Westwood, 2016).

Cash Cows-Leaders in the marketplace and consume less cash than they bring to the company.

Dogs-Low market share and low growth rate, considered as cash traps (Oguz & Kaya, 2016).

Based on the above theoretical understanding portfolio matrix of DP A will be studied.

Exhibit 4

Drinking Milk Sales by type in (Millions)

Regular Reduced

Fat

Non-Fat Flavoured UHT Total

2008-09 1136 569 118 210 196 2229

2009-10 1133 590 119 215 211 2269

Stars-Characterised by Best market share and generate most cash in the portfolio.

Question Marks-High growth prospect but low market share consume more cash and bring less

return (Westwood, 2016).

Cash Cows-Leaders in the marketplace and consume less cash than they bring to the company.

Dogs-Low market share and low growth rate, considered as cash traps (Oguz & Kaya, 2016).

Based on the above theoretical understanding portfolio matrix of DP A will be studied.

Exhibit 4

Drinking Milk Sales by type in (Millions)

Regular Reduced

Fat

Non-Fat Flavoured UHT Total

2008-09 1136 569 118 210 196 2229

2009-10 1133 590 119 215 211 2269

Strategic Marketing P a g e | 8

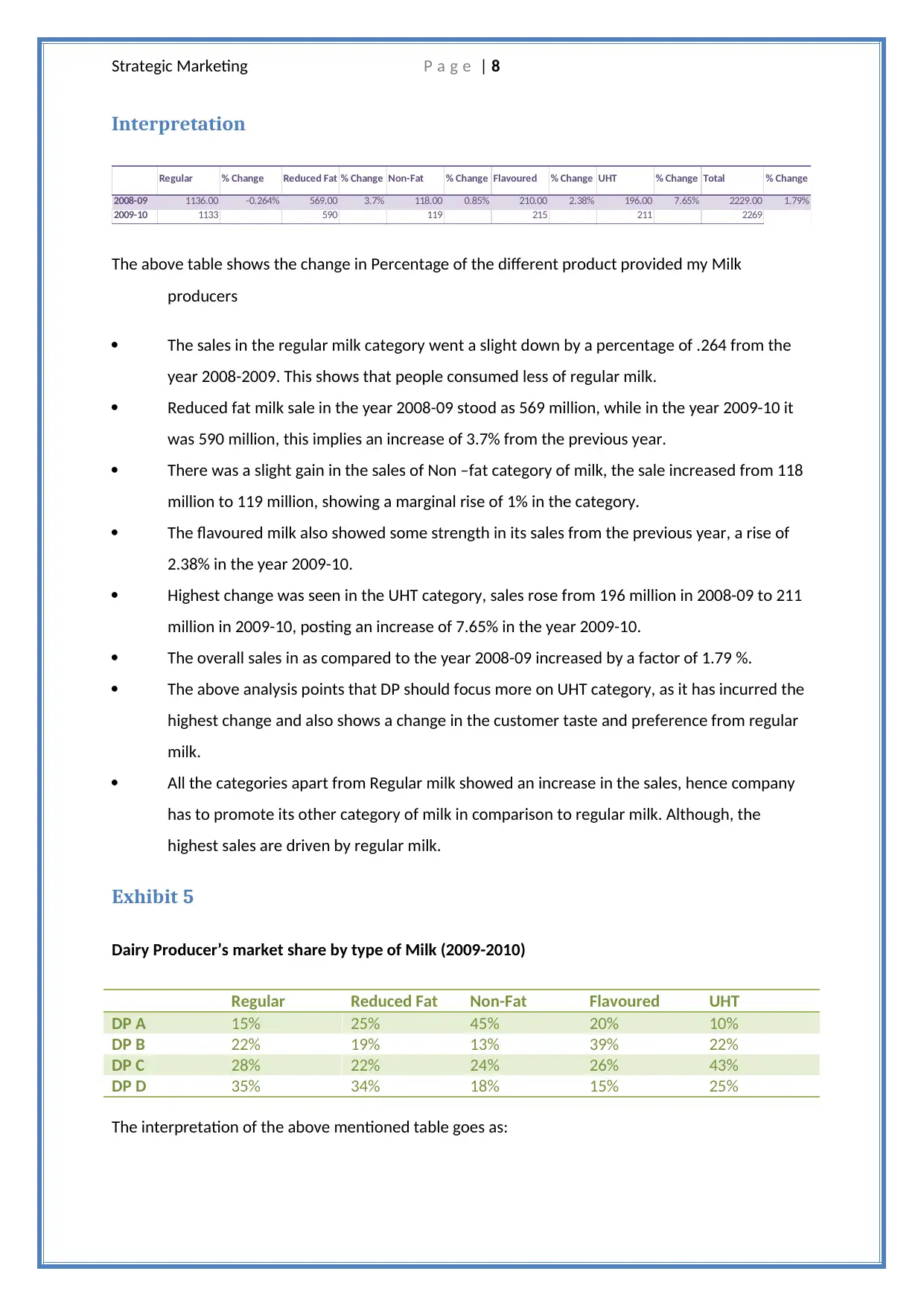

Interpretation

Regular % Change Reduced Fat % Change Non-Fat % Change Flavoured % Change UHT % Change Total % Change

2008-09 1136.00 -0.264% 569.00 3.7% 118.00 0.85% 210.00 2.38% 196.00 7.65% 2229.00 1.79%

2009-10 1133 590 119 215 211 2269

The above table shows the change in Percentage of the different product provided my Milk

producers

The sales in the regular milk category went a slight down by a percentage of .264 from the

year 2008-2009. This shows that people consumed less of regular milk.

Reduced fat milk sale in the year 2008-09 stood as 569 million, while in the year 2009-10 it

was 590 million, this implies an increase of 3.7% from the previous year.

There was a slight gain in the sales of Non –fat category of milk, the sale increased from 118

million to 119 million, showing a marginal rise of 1% in the category.

The flavoured milk also showed some strength in its sales from the previous year, a rise of

2.38% in the year 2009-10.

Highest change was seen in the UHT category, sales rose from 196 million in 2008-09 to 211

million in 2009-10, posting an increase of 7.65% in the year 2009-10.

The overall sales in as compared to the year 2008-09 increased by a factor of 1.79 %.

The above analysis points that DP should focus more on UHT category, as it has incurred the

highest change and also shows a change in the customer taste and preference from regular

milk.

All the categories apart from Regular milk showed an increase in the sales, hence company

has to promote its other category of milk in comparison to regular milk. Although, the

highest sales are driven by regular milk.

Exhibit 5

Dairy Producer’s market share by type of Milk (2009-2010)

Regular Reduced Fat Non-Fat Flavoured UHT

DP A 15% 25% 45% 20% 10%

DP B 22% 19% 13% 39% 22%

DP C 28% 22% 24% 26% 43%

DP D 35% 34% 18% 15% 25%

The interpretation of the above mentioned table goes as:

Interpretation

Regular % Change Reduced Fat % Change Non-Fat % Change Flavoured % Change UHT % Change Total % Change

2008-09 1136.00 -0.264% 569.00 3.7% 118.00 0.85% 210.00 2.38% 196.00 7.65% 2229.00 1.79%

2009-10 1133 590 119 215 211 2269

The above table shows the change in Percentage of the different product provided my Milk

producers

The sales in the regular milk category went a slight down by a percentage of .264 from the

year 2008-2009. This shows that people consumed less of regular milk.

Reduced fat milk sale in the year 2008-09 stood as 569 million, while in the year 2009-10 it

was 590 million, this implies an increase of 3.7% from the previous year.

There was a slight gain in the sales of Non –fat category of milk, the sale increased from 118

million to 119 million, showing a marginal rise of 1% in the category.

The flavoured milk also showed some strength in its sales from the previous year, a rise of

2.38% in the year 2009-10.

Highest change was seen in the UHT category, sales rose from 196 million in 2008-09 to 211

million in 2009-10, posting an increase of 7.65% in the year 2009-10.

The overall sales in as compared to the year 2008-09 increased by a factor of 1.79 %.

The above analysis points that DP should focus more on UHT category, as it has incurred the

highest change and also shows a change in the customer taste and preference from regular

milk.

All the categories apart from Regular milk showed an increase in the sales, hence company

has to promote its other category of milk in comparison to regular milk. Although, the

highest sales are driven by regular milk.

Exhibit 5

Dairy Producer’s market share by type of Milk (2009-2010)

Regular Reduced Fat Non-Fat Flavoured UHT

DP A 15% 25% 45% 20% 10%

DP B 22% 19% 13% 39% 22%

DP C 28% 22% 24% 26% 43%

DP D 35% 34% 18% 15% 25%

The interpretation of the above mentioned table goes as:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

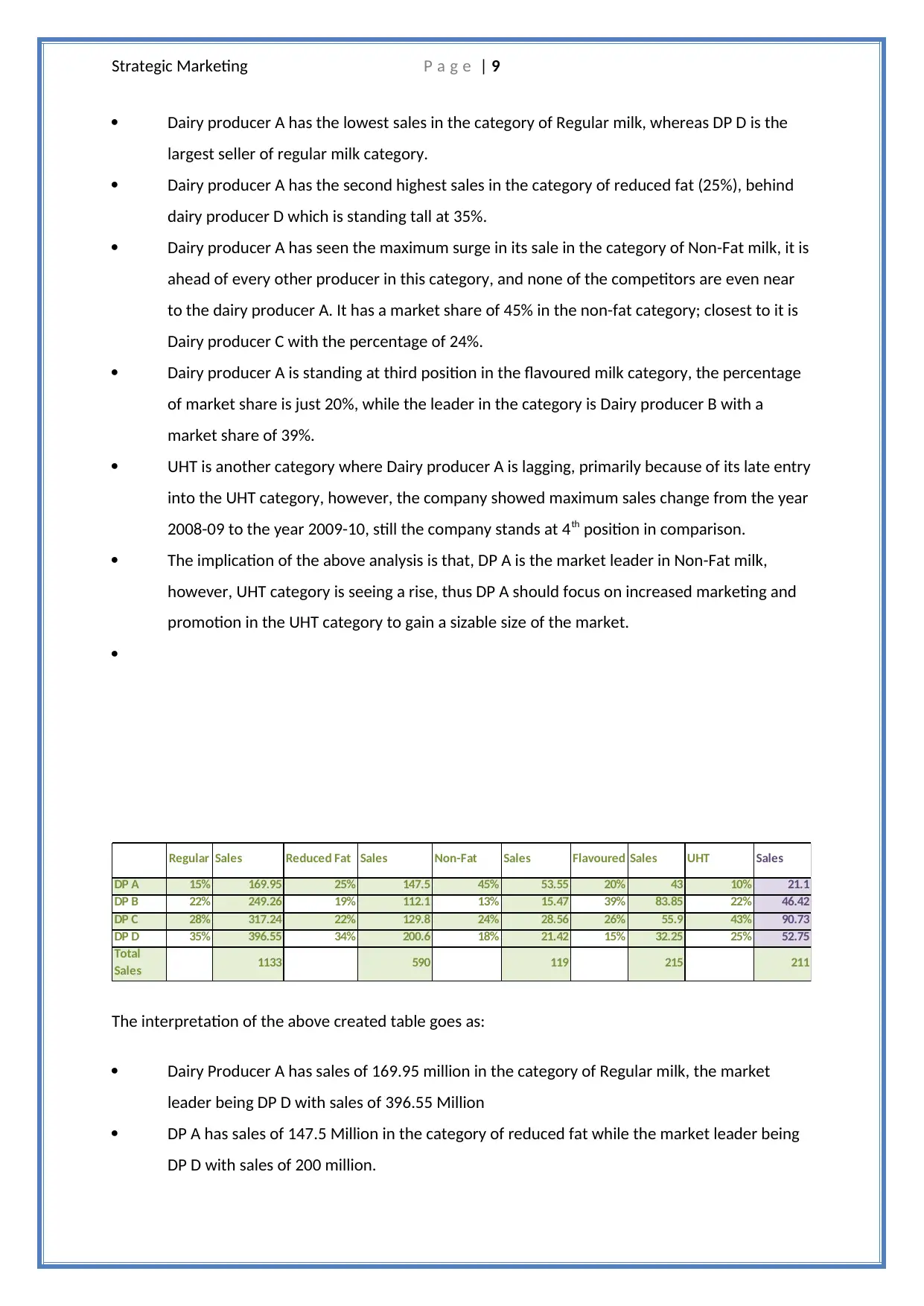

Strategic Marketing P a g e | 9

Dairy producer A has the lowest sales in the category of Regular milk, whereas DP D is the

largest seller of regular milk category.

Dairy producer A has the second highest sales in the category of reduced fat (25%), behind

dairy producer D which is standing tall at 35%.

Dairy producer A has seen the maximum surge in its sale in the category of Non-Fat milk, it is

ahead of every other producer in this category, and none of the competitors are even near

to the dairy producer A. It has a market share of 45% in the non-fat category; closest to it is

Dairy producer C with the percentage of 24%.

Dairy producer A is standing at third position in the flavoured milk category, the percentage

of market share is just 20%, while the leader in the category is Dairy producer B with a

market share of 39%.

UHT is another category where Dairy producer A is lagging, primarily because of its late entry

into the UHT category, however, the company showed maximum sales change from the year

2008-09 to the year 2009-10, still the company stands at 4th position in comparison.

The implication of the above analysis is that, DP A is the market leader in Non-Fat milk,

however, UHT category is seeing a rise, thus DP A should focus on increased marketing and

promotion in the UHT category to gain a sizable size of the market.

Regular Sales Reduced Fat Sales Non-Fat Sales Flavoured Sales UHT Sales

DP A 15% 169.95 25% 147.5 45% 53.55 20% 43 10% 21.1

DP B 22% 249.26 19% 112.1 13% 15.47 39% 83.85 22% 46.42

DP C 28% 317.24 22% 129.8 24% 28.56 26% 55.9 43% 90.73

DP D 35% 396.55 34% 200.6 18% 21.42 15% 32.25 25% 52.75

Total

Sales 1133 590 119 215 211

The interpretation of the above created table goes as:

Dairy Producer A has sales of 169.95 million in the category of Regular milk, the market

leader being DP D with sales of 396.55 Million

DP A has sales of 147.5 Million in the category of reduced fat while the market leader being

DP D with sales of 200 million.

Dairy producer A has the lowest sales in the category of Regular milk, whereas DP D is the

largest seller of regular milk category.

Dairy producer A has the second highest sales in the category of reduced fat (25%), behind

dairy producer D which is standing tall at 35%.

Dairy producer A has seen the maximum surge in its sale in the category of Non-Fat milk, it is

ahead of every other producer in this category, and none of the competitors are even near

to the dairy producer A. It has a market share of 45% in the non-fat category; closest to it is

Dairy producer C with the percentage of 24%.

Dairy producer A is standing at third position in the flavoured milk category, the percentage

of market share is just 20%, while the leader in the category is Dairy producer B with a

market share of 39%.

UHT is another category where Dairy producer A is lagging, primarily because of its late entry

into the UHT category, however, the company showed maximum sales change from the year

2008-09 to the year 2009-10, still the company stands at 4th position in comparison.

The implication of the above analysis is that, DP A is the market leader in Non-Fat milk,

however, UHT category is seeing a rise, thus DP A should focus on increased marketing and

promotion in the UHT category to gain a sizable size of the market.

Regular Sales Reduced Fat Sales Non-Fat Sales Flavoured Sales UHT Sales

DP A 15% 169.95 25% 147.5 45% 53.55 20% 43 10% 21.1

DP B 22% 249.26 19% 112.1 13% 15.47 39% 83.85 22% 46.42

DP C 28% 317.24 22% 129.8 24% 28.56 26% 55.9 43% 90.73

DP D 35% 396.55 34% 200.6 18% 21.42 15% 32.25 25% 52.75

Total

Sales 1133 590 119 215 211

The interpretation of the above created table goes as:

Dairy Producer A has sales of 169.95 million in the category of Regular milk, the market

leader being DP D with sales of 396.55 Million

DP A has sales of 147.5 Million in the category of reduced fat while the market leader being

DP D with sales of 200 million.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Marketing P a g e | 10

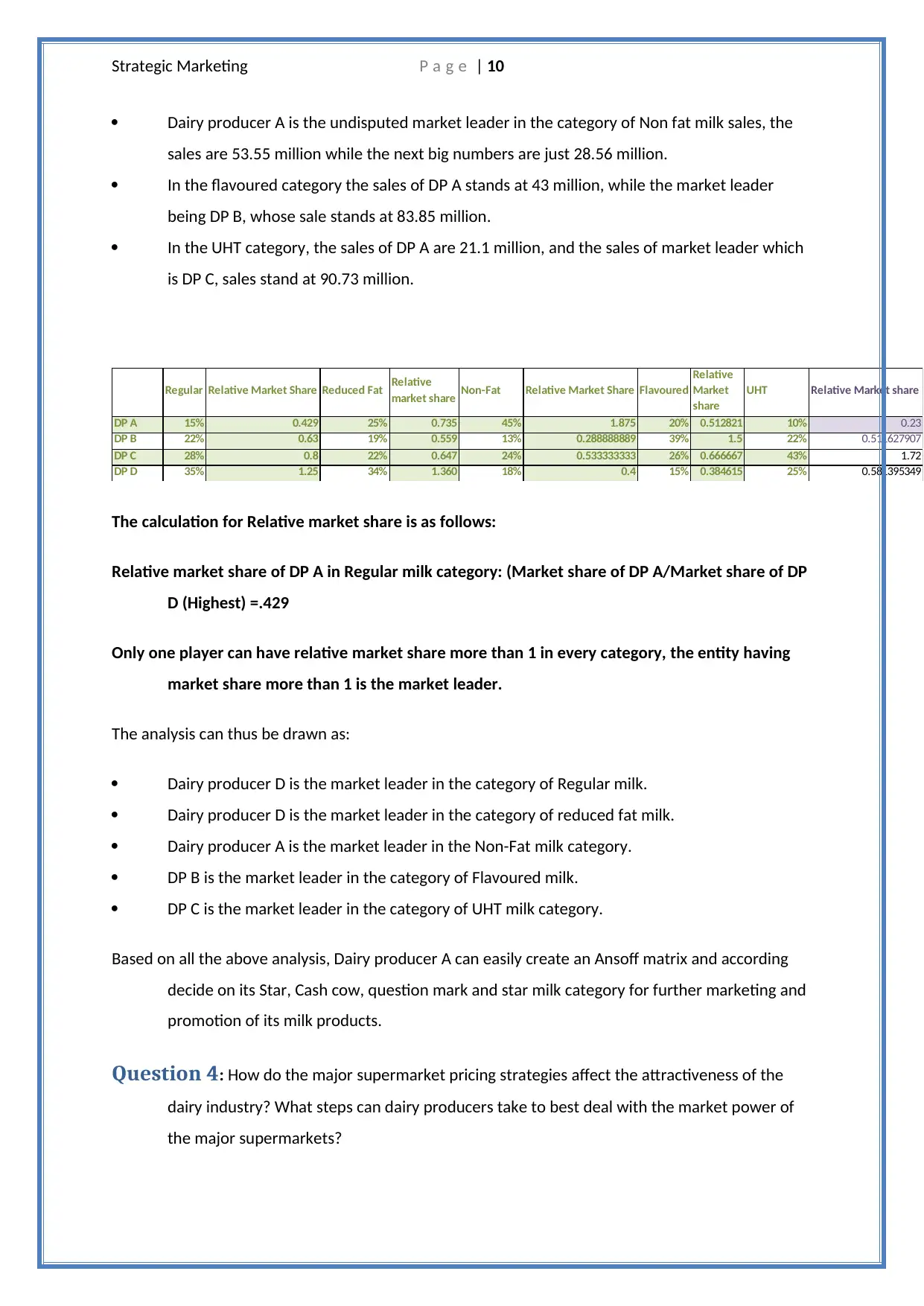

Dairy producer A is the undisputed market leader in the category of Non fat milk sales, the

sales are 53.55 million while the next big numbers are just 28.56 million.

In the flavoured category the sales of DP A stands at 43 million, while the market leader

being DP B, whose sale stands at 83.85 million.

In the UHT category, the sales of DP A are 21.1 million, and the sales of market leader which

is DP C, sales stand at 90.73 million.

Regular Relative Market Share Reduced Fat Relative

market share Non-Fat Relative Market Share Flavoured

Relative

Market

share

UHT Relative Market share

DP A 15% 0.429 25% 0.735 45% 1.875 20% 0.512821 10% 0.23

DP B 22% 0.63 19% 0.559 13% 0.288888889 39% 1.5 22% 0.511627907

DP C 28% 0.8 22% 0.647 24% 0.533333333 26% 0.666667 43% 1.72

DP D 35% 1.25 34% 1.360 18% 0.4 15% 0.384615 25% 0.581395349

The calculation for Relative market share is as follows:

Relative market share of DP A in Regular milk category: (Market share of DP A/Market share of DP

D (Highest) =.429

Only one player can have relative market share more than 1 in every category, the entity having

market share more than 1 is the market leader.

The analysis can thus be drawn as:

Dairy producer D is the market leader in the category of Regular milk.

Dairy producer D is the market leader in the category of reduced fat milk.

Dairy producer A is the market leader in the Non-Fat milk category.

DP B is the market leader in the category of Flavoured milk.

DP C is the market leader in the category of UHT milk category.

Based on all the above analysis, Dairy producer A can easily create an Ansoff matrix and according

decide on its Star, Cash cow, question mark and star milk category for further marketing and

promotion of its milk products.

Question 4: How do the major supermarket pricing strategies affect the attractiveness of the

dairy industry? What steps can dairy producers take to best deal with the market power of

the major supermarkets?

Dairy producer A is the undisputed market leader in the category of Non fat milk sales, the

sales are 53.55 million while the next big numbers are just 28.56 million.

In the flavoured category the sales of DP A stands at 43 million, while the market leader

being DP B, whose sale stands at 83.85 million.

In the UHT category, the sales of DP A are 21.1 million, and the sales of market leader which

is DP C, sales stand at 90.73 million.

Regular Relative Market Share Reduced Fat Relative

market share Non-Fat Relative Market Share Flavoured

Relative

Market

share

UHT Relative Market share

DP A 15% 0.429 25% 0.735 45% 1.875 20% 0.512821 10% 0.23

DP B 22% 0.63 19% 0.559 13% 0.288888889 39% 1.5 22% 0.511627907

DP C 28% 0.8 22% 0.647 24% 0.533333333 26% 0.666667 43% 1.72

DP D 35% 1.25 34% 1.360 18% 0.4 15% 0.384615 25% 0.581395349

The calculation for Relative market share is as follows:

Relative market share of DP A in Regular milk category: (Market share of DP A/Market share of DP

D (Highest) =.429

Only one player can have relative market share more than 1 in every category, the entity having

market share more than 1 is the market leader.

The analysis can thus be drawn as:

Dairy producer D is the market leader in the category of Regular milk.

Dairy producer D is the market leader in the category of reduced fat milk.

Dairy producer A is the market leader in the Non-Fat milk category.

DP B is the market leader in the category of Flavoured milk.

DP C is the market leader in the category of UHT milk category.

Based on all the above analysis, Dairy producer A can easily create an Ansoff matrix and according

decide on its Star, Cash cow, question mark and star milk category for further marketing and

promotion of its milk products.

Question 4: How do the major supermarket pricing strategies affect the attractiveness of the

dairy industry? What steps can dairy producers take to best deal with the market power of

the major supermarkets?

Strategic Marketing P a g e | 11

Answer

According to the case study, the relationship between the dairy farmers and the

supermarkets is complex in nature. A fear or uncertainty on the future of Australian dairy

farm industry is clearly visible from the case study. Plethora of dairy farmers is leaving the

farms due to deregulation in the industry. At the same time, the prices offered to the dairy

farmers are way less in comparison to what it is being sold at in the supermarkets. Also, the

gaining popularity of the private labels is hampering the dairy farmer’s big time; the

supermarkets are reducing the prices of the milk to increase the bulk sale which is

hampering the farmers (Richards, Kjaernes & Vik, 2016).

Another contentious issue is the rate supermarkets are offering to the dairy farmers,

supermarkets in order to win the raging war have reduced the price of milk significantly. A

number of supermarkets followed suit against Coles, in a bid to increase the price of the

milk. However, nothing has happened since then. According to Coles, it exports most of the

milk which is being sold in its store, and this is affecting Australian dollar as well. More so,

the supermarkets are offering great discounts to stay atop of the business, for example,

Coles is offering 1 litre of milk at $2 and 3 litres of milk at $3, it makes the consumer

perceive the rate of the milk is only $1. Over the last four years the price of the milk has not

changed even a bit (Atkins & Bowler, 2016). This is seriously squeezing the margins of the

dairy farmers, who are uncertain about their future and looking for other alternatives.

Recently, Woolworth’s has been appointed. On the consumer front, there are a lot of mixed

reviews, most of them are in favour of price wars, as they are benefitting from it immensely,

but ultimately it is the farmers who are losing out on the revenue and thus the profit

margins. It has been said over and over again that Supermarkets by increasing the price of

the milk will not be able to do with the plight of the farmers; in actual it is the big gap in the

supply and demand which is hampering the farmers (Issac & Dixon, 2016). However, there

are number of steps the farmers can take to prevent their best interest against the giant

power of supermarkets

Getting regulation in the Dairy market

The situation presently in Australia is far than worsened, it is high time that government

intervenes and save the dairy farmers from getting into the well of misery. In Australia, the

government allows the market forces to determine the price of a commodity; this has to be

changed at least for the dairy farmers. A regulation in the Milk industry will ensure that the

Answer

According to the case study, the relationship between the dairy farmers and the

supermarkets is complex in nature. A fear or uncertainty on the future of Australian dairy

farm industry is clearly visible from the case study. Plethora of dairy farmers is leaving the

farms due to deregulation in the industry. At the same time, the prices offered to the dairy

farmers are way less in comparison to what it is being sold at in the supermarkets. Also, the

gaining popularity of the private labels is hampering the dairy farmer’s big time; the

supermarkets are reducing the prices of the milk to increase the bulk sale which is

hampering the farmers (Richards, Kjaernes & Vik, 2016).

Another contentious issue is the rate supermarkets are offering to the dairy farmers,

supermarkets in order to win the raging war have reduced the price of milk significantly. A

number of supermarkets followed suit against Coles, in a bid to increase the price of the

milk. However, nothing has happened since then. According to Coles, it exports most of the

milk which is being sold in its store, and this is affecting Australian dollar as well. More so,

the supermarkets are offering great discounts to stay atop of the business, for example,

Coles is offering 1 litre of milk at $2 and 3 litres of milk at $3, it makes the consumer

perceive the rate of the milk is only $1. Over the last four years the price of the milk has not

changed even a bit (Atkins & Bowler, 2016). This is seriously squeezing the margins of the

dairy farmers, who are uncertain about their future and looking for other alternatives.

Recently, Woolworth’s has been appointed. On the consumer front, there are a lot of mixed

reviews, most of them are in favour of price wars, as they are benefitting from it immensely,

but ultimately it is the farmers who are losing out on the revenue and thus the profit

margins. It has been said over and over again that Supermarkets by increasing the price of

the milk will not be able to do with the plight of the farmers; in actual it is the big gap in the

supply and demand which is hampering the farmers (Issac & Dixon, 2016). However, there

are number of steps the farmers can take to prevent their best interest against the giant

power of supermarkets

Getting regulation in the Dairy market

The situation presently in Australia is far than worsened, it is high time that government

intervenes and save the dairy farmers from getting into the well of misery. In Australia, the

government allows the market forces to determine the price of a commodity; this has to be

changed at least for the dairy farmers. A regulation in the Milk industry will ensure that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.