Strategic Resource Management Report for Samsung Plc Analysis

VerifiedAdded on 2020/01/07

|12

|3195

|175

Report

AI Summary

This report provides a comprehensive analysis of strategic resource management within Samsung Plc. It begins with an introduction to strategic management and its importance, followed by an examination of financial data and its role in informing business strategy. The report delves into financial statement analysis, including income statements, balance sheets, and cash flow statements, and uses ratio analysis to assess the company's financial performance. It also explores the impact of creative accounting techniques, the limitations of ratio analysis tools, and the significance of cash flow management when evaluating capital expenditure proposals. Furthermore, the report includes a capital expenditure appraisal, evaluating the options of replacing or purchasing new machinery using methods such as payback period and accounting rate of return. The analysis provides recommendations based on financial interpretations, offering insights into strategic planning and decision-making processes to improve Samsung Plc's efficiency and profitability.

Strategic Resource

Management

1

Management

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Financial data information to inform business strategy.........................................................3

1.2 Significance of financial and information to formulate business strategy.............................4

1.3 Risk assessment regarding financial business decisions........................................................4

3.1 Technique used for appraising strategic capital expenditure projects...................................5

TASK 2............................................................................................................................................5

2.1 Financial statement analysis..................................................................................................5

2.2 Ratio analysis.........................................................................................................................6

2.3 Recommendations related to financial statement interpretation............................................7

TASK 3............................................................................................................................................7

3.2 Impact of creative accounting techniques when making strategic decisions.........................7

3.3 Limitations of ratio analysis tools..........................................................................................7

3.4 Significance of cash flow management when evaluating proposals for capital expenditures

......................................................................................................................................................8

TASK 4 ...........................................................................................................................................8

4.1 Capital expenditure appraisal.................................................................................................8

CONCLUSION..............................................................................................................................13

REFERENCE.................................................................................................................................14

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Financial data information to inform business strategy.........................................................3

1.2 Significance of financial and information to formulate business strategy.............................4

1.3 Risk assessment regarding financial business decisions........................................................4

3.1 Technique used for appraising strategic capital expenditure projects...................................5

TASK 2............................................................................................................................................5

2.1 Financial statement analysis..................................................................................................5

2.2 Ratio analysis.........................................................................................................................6

2.3 Recommendations related to financial statement interpretation............................................7

TASK 3............................................................................................................................................7

3.2 Impact of creative accounting techniques when making strategic decisions.........................7

3.3 Limitations of ratio analysis tools..........................................................................................7

3.4 Significance of cash flow management when evaluating proposals for capital expenditures

......................................................................................................................................................8

TASK 4 ...........................................................................................................................................8

4.1 Capital expenditure appraisal.................................................................................................8

CONCLUSION..............................................................................................................................13

REFERENCE.................................................................................................................................14

2

INTRODUCTION

Strategic management is a concept for formulating and implementing strategies to reduce

issues occur at workplace. In this regarding improving effectiveness of entity by following

overall strategic plans. The present report is based on understanding strategic resource

management tools of Samsung Plc. It is public limited wide spread organization of UK that

provide electronic items to million customers. However, financial data and information analysis

for analyzing current organization's performance can be described. In accordance to this, critical

evaluation on collected data for strategic planning procedure and decreasing risks occur at

enterprise is to be expressed. Moreover, financial statements' interpretation to present economic

position of firm including ratio analysis and fund/cash flow statement. Along with this, cash flow

management and balancing expenditure for business operations is to determined. Thus, capital

expenditure appraisal for further investment to purchase new machinery equipment can be

expressed. Hence, proper strategic management and planning for entity's increasing efficiency is

to understood through this assignment.

TASK 1

1.1 Financial data information to inform business strategy

Covered in attached ppt.

1.2 Significance of financial and information to formulate business strategy

Covered in attached ppt.

1.3 Risk assessment regarding financial business decisions

Covered in attached ppt.

3.1 Technique used for appraising strategic capital expenditure projects

Covered in attached ppt.

TASK 2

2.1 Financial statement analysis

Financial statements including income statement, profit and loss account, balance sheet,

fund/cash flow statements are analyzed. On the basis of which, various tools and techniques are

created enhancing profitability of firm at high level (Brewster and et.al., 2016). In this regard,

3

Strategic management is a concept for formulating and implementing strategies to reduce

issues occur at workplace. In this regarding improving effectiveness of entity by following

overall strategic plans. The present report is based on understanding strategic resource

management tools of Samsung Plc. It is public limited wide spread organization of UK that

provide electronic items to million customers. However, financial data and information analysis

for analyzing current organization's performance can be described. In accordance to this, critical

evaluation on collected data for strategic planning procedure and decreasing risks occur at

enterprise is to be expressed. Moreover, financial statements' interpretation to present economic

position of firm including ratio analysis and fund/cash flow statement. Along with this, cash flow

management and balancing expenditure for business operations is to determined. Thus, capital

expenditure appraisal for further investment to purchase new machinery equipment can be

expressed. Hence, proper strategic management and planning for entity's increasing efficiency is

to understood through this assignment.

TASK 1

1.1 Financial data information to inform business strategy

Covered in attached ppt.

1.2 Significance of financial and information to formulate business strategy

Covered in attached ppt.

1.3 Risk assessment regarding financial business decisions

Covered in attached ppt.

3.1 Technique used for appraising strategic capital expenditure projects

Covered in attached ppt.

TASK 2

2.1 Financial statement analysis

Financial statements including income statement, profit and loss account, balance sheet,

fund/cash flow statements are analyzed. On the basis of which, various tools and techniques are

created enhancing profitability of firm at high level (Brewster and et.al., 2016). In this regard,

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

finance department's manager recognizes last years' business performance regarding incurred

expenses and gained revenue that presents profit earning capacity of entity. Moreover, different

statements are identified through data interpretation and evaluating ratios related to profitability

and liquidity. In this process, economic growth of firm is obtained and varieties of ideas are

created for effective business management. However, statements' analysis is beneficial for

accomplishing tasks and increasing efficiencies of organization at high level (Edelman and et.

al., 2016). By comparing last two years' business performance, systematic strategic planning

procedure is created for decision making and implementing strategies. Thus, financial statement

analysis is useful for economic stability and improving monetary profile of organization at large

scale through implementing different strategies.

2.2 Ratio analysis

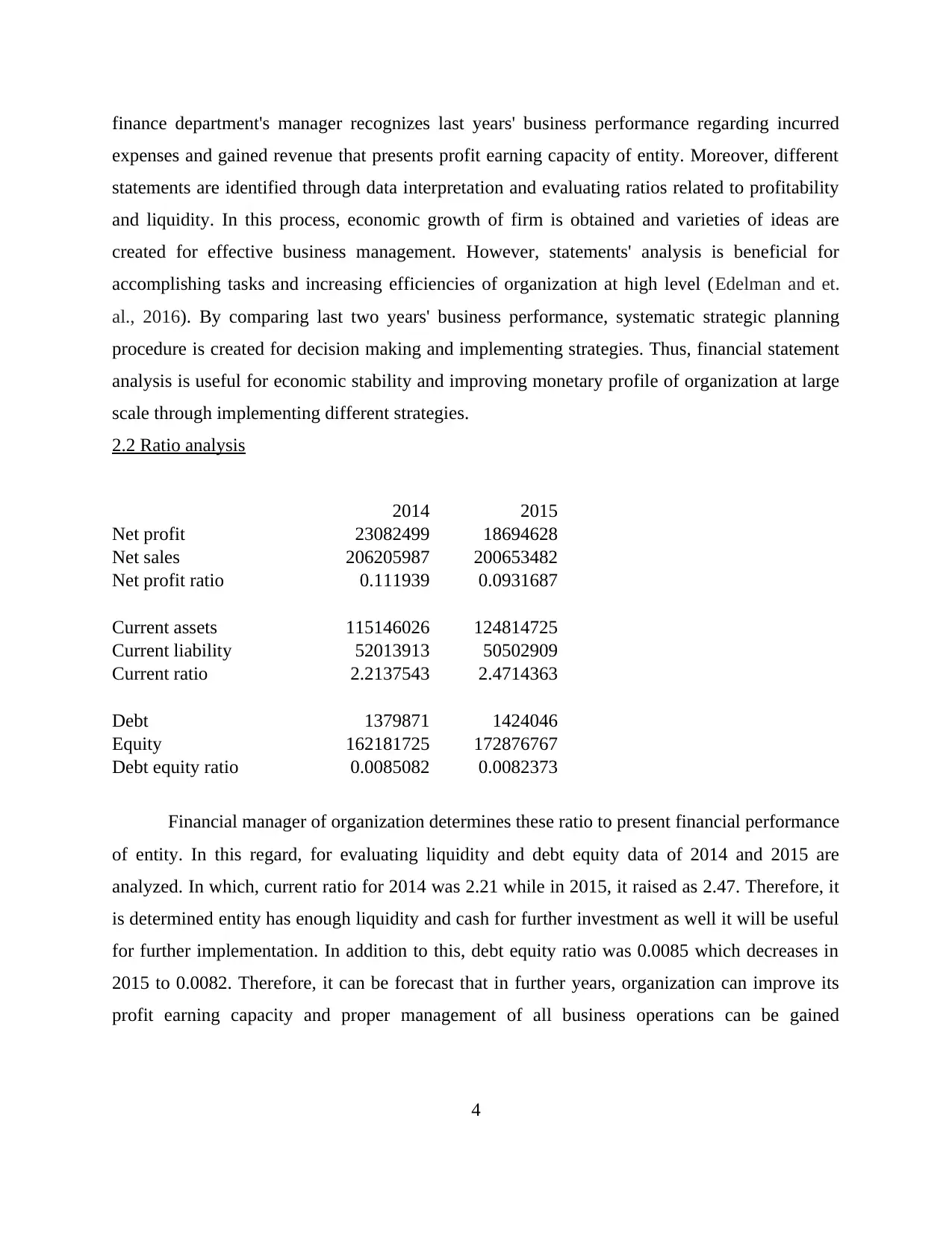

2014 2015

Net profit 23082499 18694628

Net sales 206205987 200653482

Net profit ratio 0.111939 0.0931687

Current assets 115146026 124814725

Current liability 52013913 50502909

Current ratio 2.2137543 2.4714363

Debt 1379871 1424046

Equity 162181725 172876767

Debt equity ratio 0.0085082 0.0082373

Financial manager of organization determines these ratio to present financial performance

of entity. In this regard, for evaluating liquidity and debt equity data of 2014 and 2015 are

analyzed. In which, current ratio for 2014 was 2.21 while in 2015, it raised as 2.47. Therefore, it

is determined entity has enough liquidity and cash for further investment as well it will be useful

for further implementation. In addition to this, debt equity ratio was 0.0085 which decreases in

2015 to 0.0082. Therefore, it can be forecast that in further years, organization can improve its

profit earning capacity and proper management of all business operations can be gained

4

expenses and gained revenue that presents profit earning capacity of entity. Moreover, different

statements are identified through data interpretation and evaluating ratios related to profitability

and liquidity. In this process, economic growth of firm is obtained and varieties of ideas are

created for effective business management. However, statements' analysis is beneficial for

accomplishing tasks and increasing efficiencies of organization at high level (Edelman and et.

al., 2016). By comparing last two years' business performance, systematic strategic planning

procedure is created for decision making and implementing strategies. Thus, financial statement

analysis is useful for economic stability and improving monetary profile of organization at large

scale through implementing different strategies.

2.2 Ratio analysis

2014 2015

Net profit 23082499 18694628

Net sales 206205987 200653482

Net profit ratio 0.111939 0.0931687

Current assets 115146026 124814725

Current liability 52013913 50502909

Current ratio 2.2137543 2.4714363

Debt 1379871 1424046

Equity 162181725 172876767

Debt equity ratio 0.0085082 0.0082373

Financial manager of organization determines these ratio to present financial performance

of entity. In this regard, for evaluating liquidity and debt equity data of 2014 and 2015 are

analyzed. In which, current ratio for 2014 was 2.21 while in 2015, it raised as 2.47. Therefore, it

is determined entity has enough liquidity and cash for further investment as well it will be useful

for further implementation. In addition to this, debt equity ratio was 0.0085 which decreases in

2015 to 0.0082. Therefore, it can be forecast that in further years, organization can improve its

profit earning capacity and proper management of all business operations can be gained

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

efficiently. Thus, in future time, entity can develop its efficiencies and quality services at high

level.

2.3 Recommendations related to financial statement interpretation

Finance department manager recognizes financial statement through ratio analysis and

presenting economic performance at high level. it is determined that entity can improve its profit

earning capability and quality services in future time for better work performance. However, it is

interrelated with strategic planning and decision making process to enhance quality services at

high level.

TASK 3

3.2 Impact of creative accounting techniques when making strategic decisions

Creative accounting is a system to manage balance sheet. It provides different guidelines

and instructions for operating business activities related to incurring expenditures and gaining

revenue. However, proper balance between expenses and income is achieved through this

process. On the basis of its evaluation, strategic decisions are taken for implementing quality

services and efficiencies of firm at high level (Donovan, 2016). Moreover, creative accounting

components are important for preparing planning procedure and making decisions regarding

business activities. In addition to this, through using creative accounting tools, ideas are created

for creations and innovations in business operation. Thereby, decisions are made efficiently and

systematic estimation for planning procedure is obtained. However, it impacts on strategic

management and decision making tools for financial management as well increasing efficiencies

in future time. Along with this, decision making process can be proceed for implementing

business and competitive strategies that is helpful for financial development and improving

business performance to operate business activities. Moreover, auditors analyzes entire activities

and business management that is helpful for transferring information related to expenditure and

income. Along with this, trading skills and its account is managed thoroughly that impacts on

strategic decision making process. Thus, creative accounting is beneficial for effective goodwill

of organization as well managing inventories efficiently.

5

level.

2.3 Recommendations related to financial statement interpretation

Finance department manager recognizes financial statement through ratio analysis and

presenting economic performance at high level. it is determined that entity can improve its profit

earning capability and quality services in future time for better work performance. However, it is

interrelated with strategic planning and decision making process to enhance quality services at

high level.

TASK 3

3.2 Impact of creative accounting techniques when making strategic decisions

Creative accounting is a system to manage balance sheet. It provides different guidelines

and instructions for operating business activities related to incurring expenditures and gaining

revenue. However, proper balance between expenses and income is achieved through this

process. On the basis of its evaluation, strategic decisions are taken for implementing quality

services and efficiencies of firm at high level (Donovan, 2016). Moreover, creative accounting

components are important for preparing planning procedure and making decisions regarding

business activities. In addition to this, through using creative accounting tools, ideas are created

for creations and innovations in business operation. Thereby, decisions are made efficiently and

systematic estimation for planning procedure is obtained. However, it impacts on strategic

management and decision making tools for financial management as well increasing efficiencies

in future time. Along with this, decision making process can be proceed for implementing

business and competitive strategies that is helpful for financial development and improving

business performance to operate business activities. Moreover, auditors analyzes entire activities

and business management that is helpful for transferring information related to expenditure and

income. Along with this, trading skills and its account is managed thoroughly that impacts on

strategic decision making process. Thus, creative accounting is beneficial for effective goodwill

of organization as well managing inventories efficiently.

5

3.3 Limitations of ratio analysis tools

Ratio analysis is a financial component that is helpful to identify financial performance of

organization. Through this technique, comparison between last years' performance to present

year is created that impacts on organization's effectiveness. In addition to this, overall business

operations are analyzed through profitability, liquidity and debt equity ratios. Therefore, proper

entity's performance is obtained as well several ideas are created for operating business activities

in future time. As per critical evaluation, it is evaluated that ratio analysis is unable due to wrong

predictions over business operations. In accordance to this, inaccurate data interpretation is

difficult to set appropriate planning procedure and making decisions for strategic management.

Including this, occurrence of uncertain problems are not suitable for further business operations.

Moreover, it is difficult to analyze overall business activities as well determining so many ratios

that affects on financial performance of entity. Hence, it is required for manager of organization

to apply ratio analysis technique for identifying financial statements and making further

decisions related to business operations in future time (Ball and et. al., 2015).

3.4 Significance of cash flow management when evaluating proposals for capital expenditures

Cash flow is an approach for evaluating difference between outflows and inflows. In this

process, incurred expenditures and gained revenue are recognized for further investment and

getting sources to funding. It is significant for preparing strategies and making decisions related

to further implementation and enhancing its efficiencies for proper financial development. In

addition to this, financial position of organization is recognized that leads to create different

ideas that is helpful to enhance profitability of organization at high level. In addition to this,

capital expenditures are related to incurring expenses to operate further business activities are

determined. However, cash flow management is useful for evaluating proposals for capital

expenditures (Verschoor, 2015). Thus, cash flow management is crucial for implementing

strategies and increasing quality services for further business operations as well increasing

revenue for profitability.

TASK 4

4.1 Capital expenditure appraisal

Many-times, company has to put huge investment in the capital projects like for

acquisition of new machinery for the technological success, geographical expansion and others.

6

Ratio analysis is a financial component that is helpful to identify financial performance of

organization. Through this technique, comparison between last years' performance to present

year is created that impacts on organization's effectiveness. In addition to this, overall business

operations are analyzed through profitability, liquidity and debt equity ratios. Therefore, proper

entity's performance is obtained as well several ideas are created for operating business activities

in future time. As per critical evaluation, it is evaluated that ratio analysis is unable due to wrong

predictions over business operations. In accordance to this, inaccurate data interpretation is

difficult to set appropriate planning procedure and making decisions for strategic management.

Including this, occurrence of uncertain problems are not suitable for further business operations.

Moreover, it is difficult to analyze overall business activities as well determining so many ratios

that affects on financial performance of entity. Hence, it is required for manager of organization

to apply ratio analysis technique for identifying financial statements and making further

decisions related to business operations in future time (Ball and et. al., 2015).

3.4 Significance of cash flow management when evaluating proposals for capital expenditures

Cash flow is an approach for evaluating difference between outflows and inflows. In this

process, incurred expenditures and gained revenue are recognized for further investment and

getting sources to funding. It is significant for preparing strategies and making decisions related

to further implementation and enhancing its efficiencies for proper financial development. In

addition to this, financial position of organization is recognized that leads to create different

ideas that is helpful to enhance profitability of organization at high level. In addition to this,

capital expenditures are related to incurring expenses to operate further business activities are

determined. However, cash flow management is useful for evaluating proposals for capital

expenditures (Verschoor, 2015). Thus, cash flow management is crucial for implementing

strategies and increasing quality services for further business operations as well increasing

revenue for profitability.

TASK 4

4.1 Capital expenditure appraisal

Many-times, company has to put huge investment in the capital projects like for

acquisition of new machinery for the technological success, geographical expansion and others.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

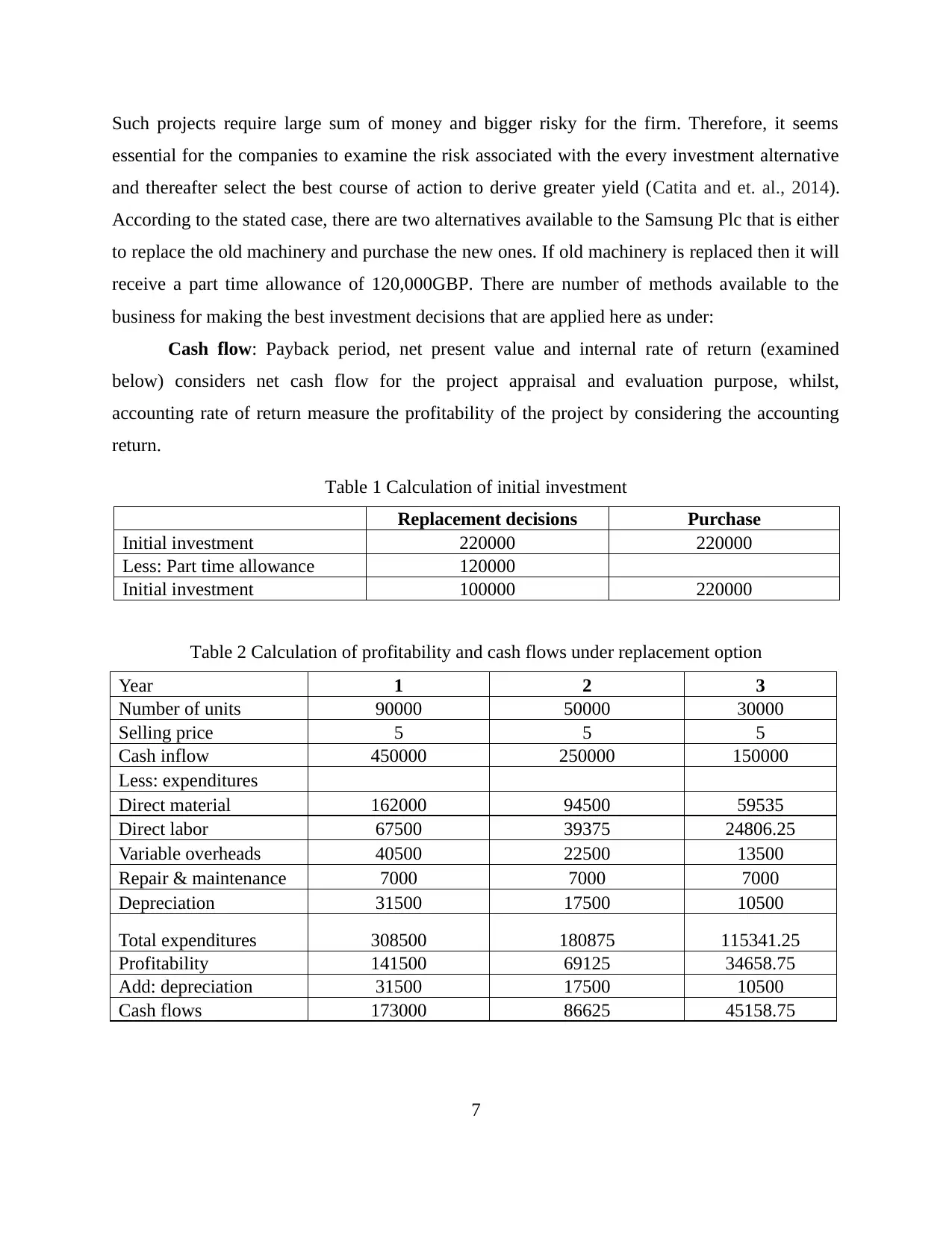

Such projects require large sum of money and bigger risky for the firm. Therefore, it seems

essential for the companies to examine the risk associated with the every investment alternative

and thereafter select the best course of action to derive greater yield (Catita and et. al., 2014).

According to the stated case, there are two alternatives available to the Samsung Plc that is either

to replace the old machinery and purchase the new ones. If old machinery is replaced then it will

receive a part time allowance of 120,000GBP. There are number of methods available to the

business for making the best investment decisions that are applied here as under:

Cash flow: Payback period, net present value and internal rate of return (examined

below) considers net cash flow for the project appraisal and evaluation purpose, whilst,

accounting rate of return measure the profitability of the project by considering the accounting

return.

Table 1 Calculation of initial investment

Replacement decisions Purchase

Initial investment 220000 220000

Less: Part time allowance 120000

Initial investment 100000 220000

Table 2 Calculation of profitability and cash flows under replacement option

Year 1 2 3

Number of units 90000 50000 30000

Selling price 5 5 5

Cash inflow 450000 250000 150000

Less: expenditures

Direct material 162000 94500 59535

Direct labor 67500 39375 24806.25

Variable overheads 40500 22500 13500

Repair & maintenance 7000 7000 7000

Depreciation 31500 17500 10500

Total expenditures 308500 180875 115341.25

Profitability 141500 69125 34658.75

Add: depreciation 31500 17500 10500

Cash flows 173000 86625 45158.75

7

essential for the companies to examine the risk associated with the every investment alternative

and thereafter select the best course of action to derive greater yield (Catita and et. al., 2014).

According to the stated case, there are two alternatives available to the Samsung Plc that is either

to replace the old machinery and purchase the new ones. If old machinery is replaced then it will

receive a part time allowance of 120,000GBP. There are number of methods available to the

business for making the best investment decisions that are applied here as under:

Cash flow: Payback period, net present value and internal rate of return (examined

below) considers net cash flow for the project appraisal and evaluation purpose, whilst,

accounting rate of return measure the profitability of the project by considering the accounting

return.

Table 1 Calculation of initial investment

Replacement decisions Purchase

Initial investment 220000 220000

Less: Part time allowance 120000

Initial investment 100000 220000

Table 2 Calculation of profitability and cash flows under replacement option

Year 1 2 3

Number of units 90000 50000 30000

Selling price 5 5 5

Cash inflow 450000 250000 150000

Less: expenditures

Direct material 162000 94500 59535

Direct labor 67500 39375 24806.25

Variable overheads 40500 22500 13500

Repair & maintenance 7000 7000 7000

Depreciation 31500 17500 10500

Total expenditures 308500 180875 115341.25

Profitability 141500 69125 34658.75

Add: depreciation 31500 17500 10500

Cash flows 173000 86625 45158.75

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 3 Calculation of profitability and cash flows under purchase option

Year 1 2 3

Number of units 90000 50000 30000

Selling price 5 5 5

Cash inflow 450000 250000 150000

Less: expenditures

Direct material 162000 94500 59535

Direct labor 54000 31500 19845

Variable overheads 27000 15000 9000

Repair & maintenance 1000 1000 1000

depreciation 49500 27500 16500

Total expenditures 293500 169500 105880

Profitability 156500 80500 44120

Add: Depreciation 49500 27500 16500

Add: Residual value 75000

Cash flows 206000 108000 135620

Non-discounted/traditional methods

Payback period: This is a non-discounted method which is useful for the risk averse

investors to find out the time length which the project will take to recover the beginning outlay

(Stanley and et. al., 2013). Shorter the duration is founded attractive for the investor or vice-

versa.

Table 4 Calculation of payback period under replacement

Year Cash flows Cumulative cash flows

Beginning investment -100000 -100000

1 173000 73000

2 86625 159625

3 45158.75 204783.75

Payback period = 100,000/173,000

= 0.58 year

= 0.58*12 = 7 months

Table 5 Calculation of payback period under buying option

Year Cash flows

Cumulative cash

flows

Beginning investment -220000 -220000

1 206000 -14000

2 108000 94000

8

Year 1 2 3

Number of units 90000 50000 30000

Selling price 5 5 5

Cash inflow 450000 250000 150000

Less: expenditures

Direct material 162000 94500 59535

Direct labor 54000 31500 19845

Variable overheads 27000 15000 9000

Repair & maintenance 1000 1000 1000

depreciation 49500 27500 16500

Total expenditures 293500 169500 105880

Profitability 156500 80500 44120

Add: Depreciation 49500 27500 16500

Add: Residual value 75000

Cash flows 206000 108000 135620

Non-discounted/traditional methods

Payback period: This is a non-discounted method which is useful for the risk averse

investors to find out the time length which the project will take to recover the beginning outlay

(Stanley and et. al., 2013). Shorter the duration is founded attractive for the investor or vice-

versa.

Table 4 Calculation of payback period under replacement

Year Cash flows Cumulative cash flows

Beginning investment -100000 -100000

1 173000 73000

2 86625 159625

3 45158.75 204783.75

Payback period = 100,000/173,000

= 0.58 year

= 0.58*12 = 7 months

Table 5 Calculation of payback period under buying option

Year Cash flows

Cumulative cash

flows

Beginning investment -220000 -220000

1 206000 -14000

2 108000 94000

8

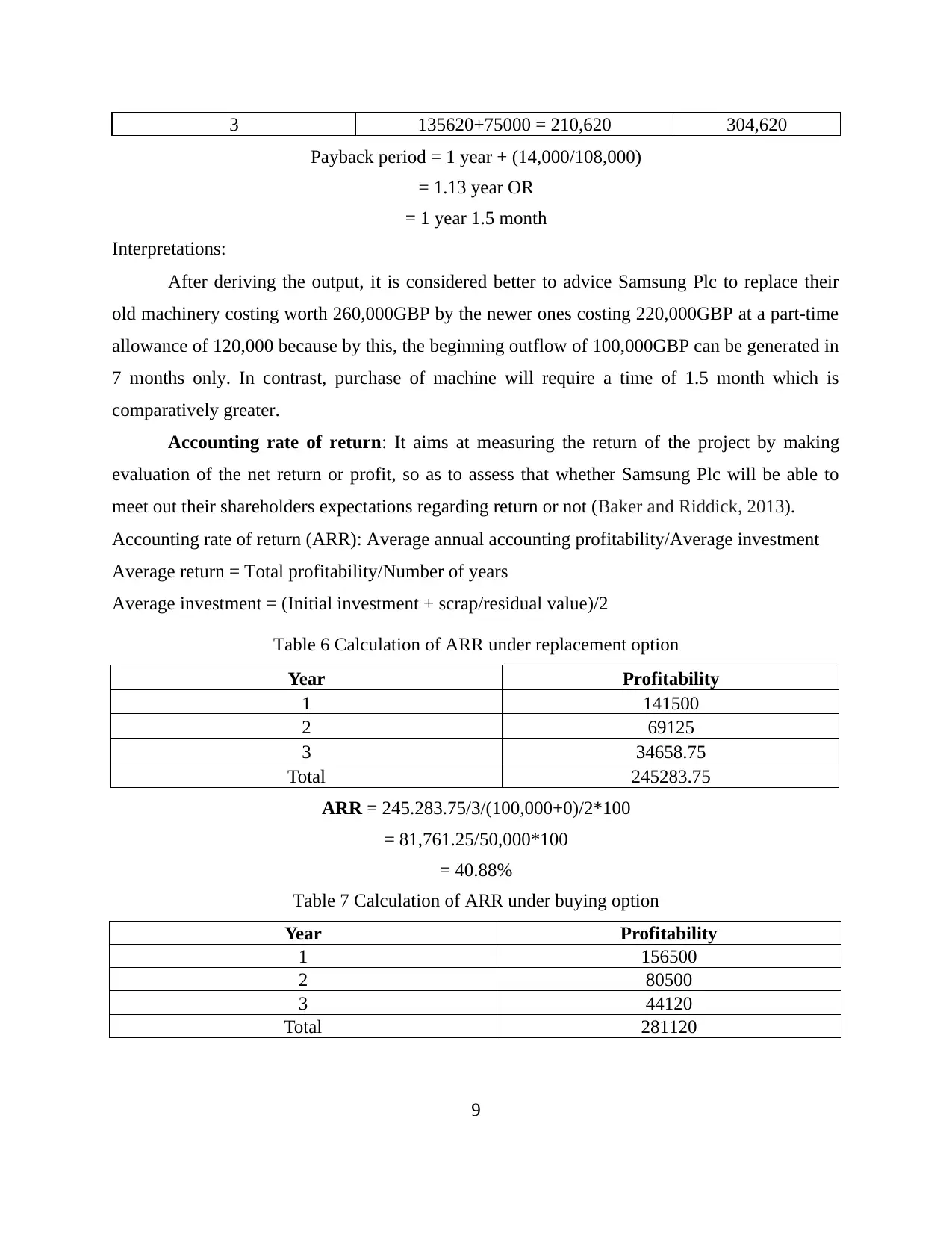

3 135620+75000 = 210,620 304,620

Payback period = 1 year + (14,000/108,000)

= 1.13 year OR

= 1 year 1.5 month

Interpretations:

After deriving the output, it is considered better to advice Samsung Plc to replace their

old machinery costing worth 260,000GBP by the newer ones costing 220,000GBP at a part-time

allowance of 120,000 because by this, the beginning outflow of 100,000GBP can be generated in

7 months only. In contrast, purchase of machine will require a time of 1.5 month which is

comparatively greater.

Accounting rate of return: It aims at measuring the return of the project by making

evaluation of the net return or profit, so as to assess that whether Samsung Plc will be able to

meet out their shareholders expectations regarding return or not (Baker and Riddick, 2013).

Accounting rate of return (ARR): Average annual accounting profitability/Average investment

Average return = Total profitability/Number of years

Average investment = (Initial investment + scrap/residual value)/2

Table 6 Calculation of ARR under replacement option

Year Profitability

1 141500

2 69125

3 34658.75

Total 245283.75

ARR = 245.283.75/3/(100,000+0)/2*100

= 81,761.25/50,000*100

= 40.88%

Table 7 Calculation of ARR under buying option

Year Profitability

1 156500

2 80500

3 44120

Total 281120

9

Payback period = 1 year + (14,000/108,000)

= 1.13 year OR

= 1 year 1.5 month

Interpretations:

After deriving the output, it is considered better to advice Samsung Plc to replace their

old machinery costing worth 260,000GBP by the newer ones costing 220,000GBP at a part-time

allowance of 120,000 because by this, the beginning outflow of 100,000GBP can be generated in

7 months only. In contrast, purchase of machine will require a time of 1.5 month which is

comparatively greater.

Accounting rate of return: It aims at measuring the return of the project by making

evaluation of the net return or profit, so as to assess that whether Samsung Plc will be able to

meet out their shareholders expectations regarding return or not (Baker and Riddick, 2013).

Accounting rate of return (ARR): Average annual accounting profitability/Average investment

Average return = Total profitability/Number of years

Average investment = (Initial investment + scrap/residual value)/2

Table 6 Calculation of ARR under replacement option

Year Profitability

1 141500

2 69125

3 34658.75

Total 245283.75

ARR = 245.283.75/3/(100,000+0)/2*100

= 81,761.25/50,000*100

= 40.88%

Table 7 Calculation of ARR under buying option

Year Profitability

1 156500

2 80500

3 44120

Total 281120

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

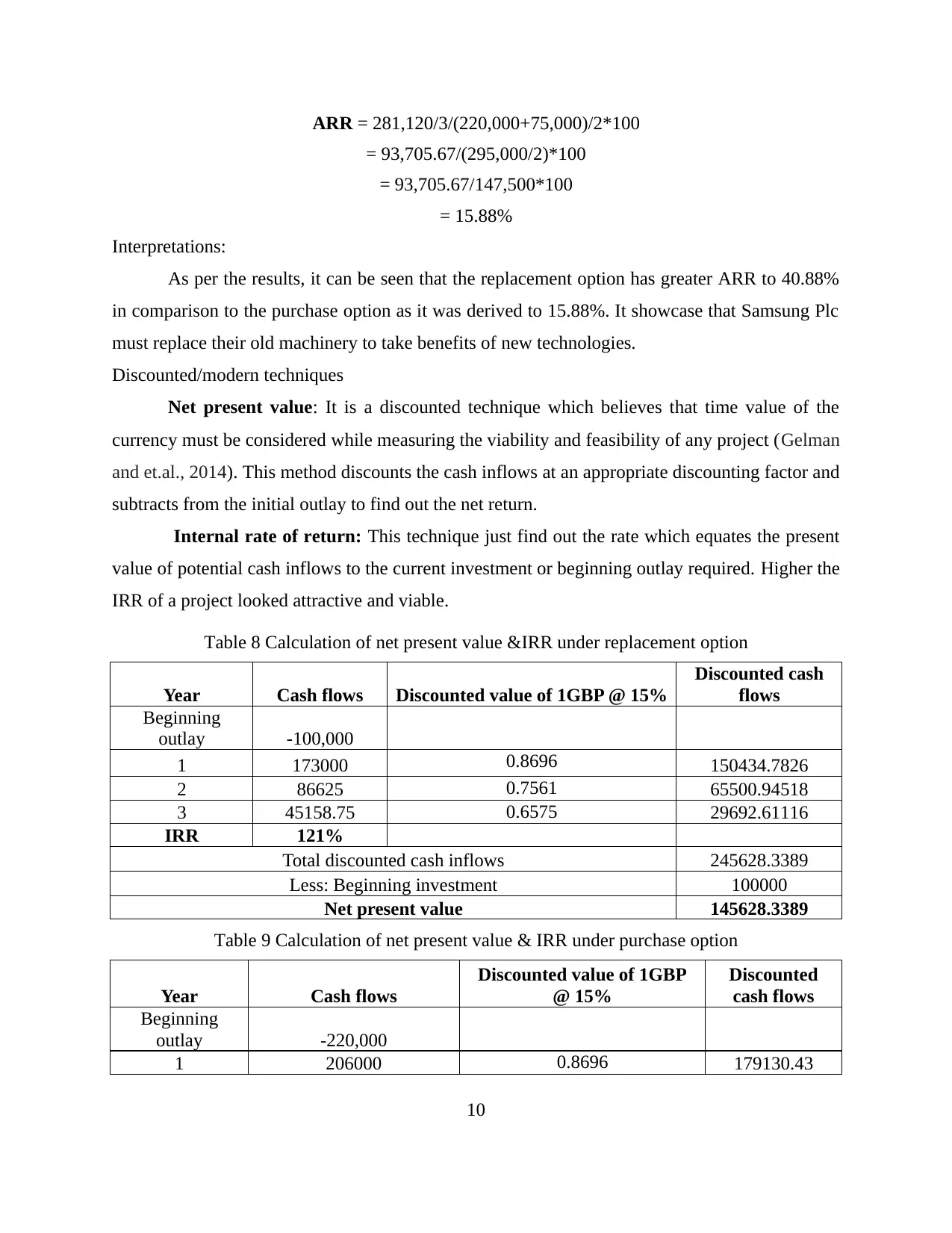

ARR = 281,120/3/(220,000+75,000)/2*100

= 93,705.67/(295,000/2)*100

= 93,705.67/147,500*100

= 15.88%

Interpretations:

As per the results, it can be seen that the replacement option has greater ARR to 40.88%

in comparison to the purchase option as it was derived to 15.88%. It showcase that Samsung Plc

must replace their old machinery to take benefits of new technologies.

Discounted/modern techniques

Net present value: It is a discounted technique which believes that time value of the

currency must be considered while measuring the viability and feasibility of any project (Gelman

and et.al., 2014). This method discounts the cash inflows at an appropriate discounting factor and

subtracts from the initial outlay to find out the net return.

Internal rate of return: This technique just find out the rate which equates the present

value of potential cash inflows to the current investment or beginning outlay required. Higher the

IRR of a project looked attractive and viable.

Table 8 Calculation of net present value &IRR under replacement option

Year Cash flows Discounted value of 1GBP @ 15%

Discounted cash

flows

Beginning

outlay -100,000

1 173000 0.8696 150434.7826

2 86625 0.7561 65500.94518

3 45158.75 0.6575 29692.61116

IRR 121%

Total discounted cash inflows 245628.3389

Less: Beginning investment 100000

Net present value 145628.3389

Table 9 Calculation of net present value & IRR under purchase option

Year Cash flows

Discounted value of 1GBP

@ 15%

Discounted

cash flows

Beginning

outlay -220,000

1 206000 0.8696 179130.43

10

= 93,705.67/(295,000/2)*100

= 93,705.67/147,500*100

= 15.88%

Interpretations:

As per the results, it can be seen that the replacement option has greater ARR to 40.88%

in comparison to the purchase option as it was derived to 15.88%. It showcase that Samsung Plc

must replace their old machinery to take benefits of new technologies.

Discounted/modern techniques

Net present value: It is a discounted technique which believes that time value of the

currency must be considered while measuring the viability and feasibility of any project (Gelman

and et.al., 2014). This method discounts the cash inflows at an appropriate discounting factor and

subtracts from the initial outlay to find out the net return.

Internal rate of return: This technique just find out the rate which equates the present

value of potential cash inflows to the current investment or beginning outlay required. Higher the

IRR of a project looked attractive and viable.

Table 8 Calculation of net present value &IRR under replacement option

Year Cash flows Discounted value of 1GBP @ 15%

Discounted cash

flows

Beginning

outlay -100,000

1 173000 0.8696 150434.7826

2 86625 0.7561 65500.94518

3 45158.75 0.6575 29692.61116

IRR 121%

Total discounted cash inflows 245628.3389

Less: Beginning investment 100000

Net present value 145628.3389

Table 9 Calculation of net present value & IRR under purchase option

Year Cash flows

Discounted value of 1GBP

@ 15%

Discounted

cash flows

Beginning

outlay -220,000

1 206000 0.8696 179130.43

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

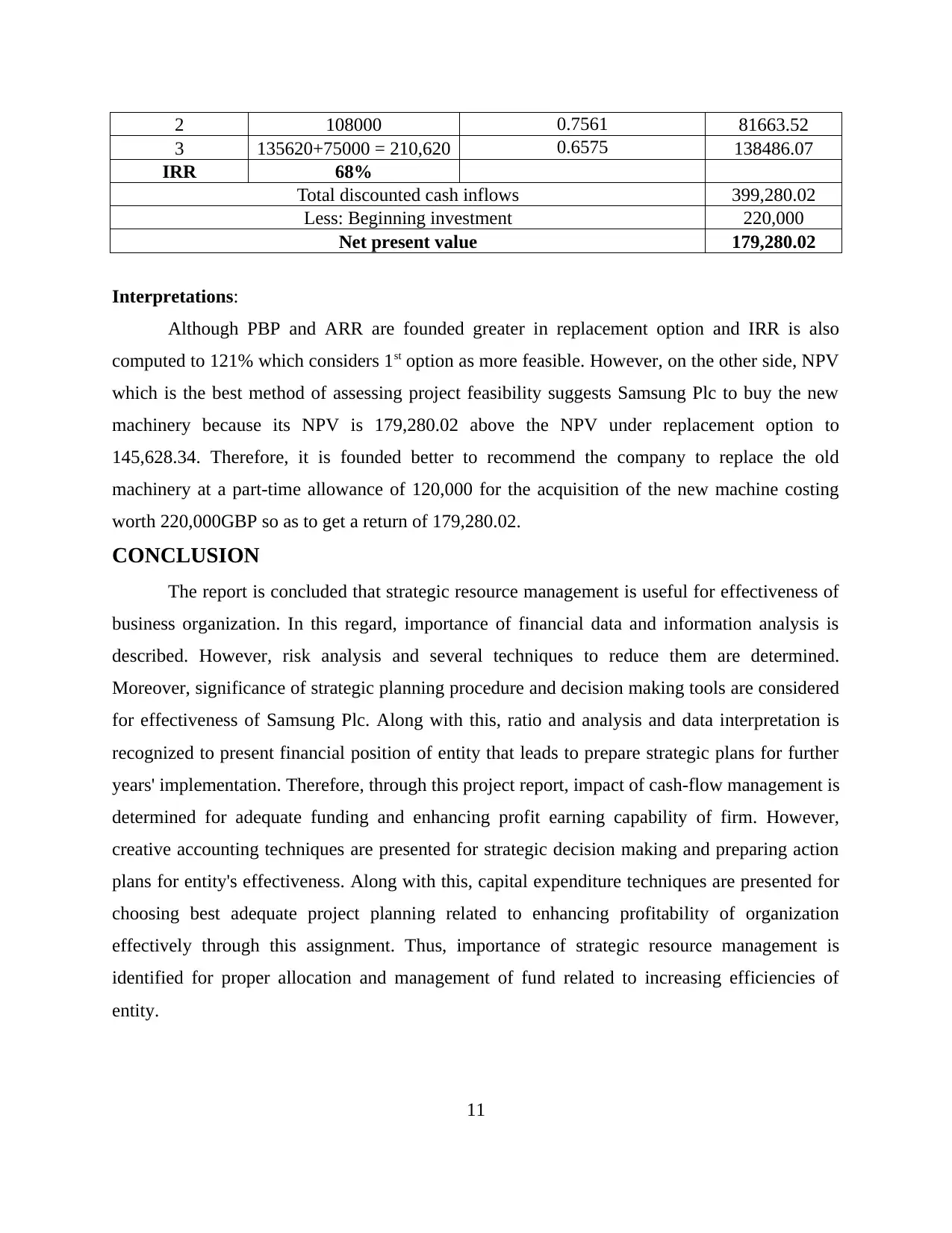

2 108000 0.7561 81663.52

3 135620+75000 = 210,620 0.6575 138486.07

IRR 68%

Total discounted cash inflows 399,280.02

Less: Beginning investment 220,000

Net present value 179,280.02

Interpretations:

Although PBP and ARR are founded greater in replacement option and IRR is also

computed to 121% which considers 1st option as more feasible. However, on the other side, NPV

which is the best method of assessing project feasibility suggests Samsung Plc to buy the new

machinery because its NPV is 179,280.02 above the NPV under replacement option to

145,628.34. Therefore, it is founded better to recommend the company to replace the old

machinery at a part-time allowance of 120,000 for the acquisition of the new machine costing

worth 220,000GBP so as to get a return of 179,280.02.

CONCLUSION

The report is concluded that strategic resource management is useful for effectiveness of

business organization. In this regard, importance of financial data and information analysis is

described. However, risk analysis and several techniques to reduce them are determined.

Moreover, significance of strategic planning procedure and decision making tools are considered

for effectiveness of Samsung Plc. Along with this, ratio and analysis and data interpretation is

recognized to present financial position of entity that leads to prepare strategic plans for further

years' implementation. Therefore, through this project report, impact of cash-flow management is

determined for adequate funding and enhancing profit earning capability of firm. However,

creative accounting techniques are presented for strategic decision making and preparing action

plans for entity's effectiveness. Along with this, capital expenditure techniques are presented for

choosing best adequate project planning related to enhancing profitability of organization

effectively through this assignment. Thus, importance of strategic resource management is

identified for proper allocation and management of fund related to increasing efficiencies of

entity.

11

3 135620+75000 = 210,620 0.6575 138486.07

IRR 68%

Total discounted cash inflows 399,280.02

Less: Beginning investment 220,000

Net present value 179,280.02

Interpretations:

Although PBP and ARR are founded greater in replacement option and IRR is also

computed to 121% which considers 1st option as more feasible. However, on the other side, NPV

which is the best method of assessing project feasibility suggests Samsung Plc to buy the new

machinery because its NPV is 179,280.02 above the NPV under replacement option to

145,628.34. Therefore, it is founded better to recommend the company to replace the old

machinery at a part-time allowance of 120,000 for the acquisition of the new machine costing

worth 220,000GBP so as to get a return of 179,280.02.

CONCLUSION

The report is concluded that strategic resource management is useful for effectiveness of

business organization. In this regard, importance of financial data and information analysis is

described. However, risk analysis and several techniques to reduce them are determined.

Moreover, significance of strategic planning procedure and decision making tools are considered

for effectiveness of Samsung Plc. Along with this, ratio and analysis and data interpretation is

recognized to present financial position of entity that leads to prepare strategic plans for further

years' implementation. Therefore, through this project report, impact of cash-flow management is

determined for adequate funding and enhancing profit earning capability of firm. However,

creative accounting techniques are presented for strategic decision making and preparing action

plans for entity's effectiveness. Along with this, capital expenditure techniques are presented for

choosing best adequate project planning related to enhancing profitability of organization

effectively through this assignment. Thus, importance of strategic resource management is

identified for proper allocation and management of fund related to increasing efficiencies of

entity.

11

REFERENCE

Books and Journals

Baker, H.K. and Riddick, L.A., 2013. International finance: a survey. Oxford University Press.

Ball, R. and et. al., 2015. Deflating profitability. Journal of Financial Economics. 117(2). pp.

225-248.

Brewster, C. and et.al., 2016. New Challenges for European Resource Management. Springer.

Catita, C. and et. al., 2014. Extending solar potential analysis in buildings to vertical facades.

Computers & Geosciences. 66(2). pp. 1-12.

Donovan, R., 2016. Impactful written communication: information has value only if it drives

action. Strategic Finance. 97(10). pp. 19-21.

Edelman, B. and et. al., 2016. To groupon or not to groupon: The profitability of deep discounts.

Marketing Letters. 27(1). pp. 39-53.

Gelman, A. and et. al., 2014. Bayesian data analysis. Boca Raton, FL, USA: Chapman &

Hall/CRC.

Stanley, D.J. And et. al., 2013. The efficient market hypothesis: the applicability of quantitative

methods to foreign stocks traded as American depository receipts (ADRs). International

Journal of Entrepreneurship and Small Business. 19(3). pp. 293-308.

Uechi, L. and et. al., 2015. Sector dominance ratio analysis of financial markets. Physica A:

Statistical Mechanics and its Applications. 42(1). pp. 488-509.

Verschoor, C.C., 2015. Too big to jail? Banks and financial companies are being prosecuted and

penalized for large-scale frauds and unethical actions, but the people behind these events

still aren't facing jail time. Strategic Finance. 97(4). pp. 16-18.

12

Books and Journals

Baker, H.K. and Riddick, L.A., 2013. International finance: a survey. Oxford University Press.

Ball, R. and et. al., 2015. Deflating profitability. Journal of Financial Economics. 117(2). pp.

225-248.

Brewster, C. and et.al., 2016. New Challenges for European Resource Management. Springer.

Catita, C. and et. al., 2014. Extending solar potential analysis in buildings to vertical facades.

Computers & Geosciences. 66(2). pp. 1-12.

Donovan, R., 2016. Impactful written communication: information has value only if it drives

action. Strategic Finance. 97(10). pp. 19-21.

Edelman, B. and et. al., 2016. To groupon or not to groupon: The profitability of deep discounts.

Marketing Letters. 27(1). pp. 39-53.

Gelman, A. and et. al., 2014. Bayesian data analysis. Boca Raton, FL, USA: Chapman &

Hall/CRC.

Stanley, D.J. And et. al., 2013. The efficient market hypothesis: the applicability of quantitative

methods to foreign stocks traded as American depository receipts (ADRs). International

Journal of Entrepreneurship and Small Business. 19(3). pp. 293-308.

Uechi, L. and et. al., 2015. Sector dominance ratio analysis of financial markets. Physica A:

Statistical Mechanics and its Applications. 42(1). pp. 488-509.

Verschoor, C.C., 2015. Too big to jail? Banks and financial companies are being prosecuted and

penalized for large-scale frauds and unethical actions, but the people behind these events

still aren't facing jail time. Strategic Finance. 97(4). pp. 16-18.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.