Strategic and Sustainability Accounting Report: Accent Group Analysis

VerifiedAdded on 2022/10/19

|23

|3598

|118

Report

AI Summary

This report provides a comprehensive analysis of strategic and sustainability accounting, focusing on three key areas: sustainability, transfer pricing, and capital investment analysis, using the case of Accent Group Limited. The sustainability section examines the environmental and social risks associated with Accent Group's operations, emphasizing the importance of identifying and managing these risks through relevant performance objectives and KPIs. The transfer pricing component delves into the internal transfer of rubber within Vans, evaluating the financial implications of different pricing strategies and the potential benefits of sourcing from external suppliers. Finally, the capital investment analysis assesses a proposal to upgrade Accent Group's stores, considering the financial impact and the importance of customer experience. The report concludes with recommendations for Accent Group to improve its sustainability practices, optimize transfer pricing decisions, and make informed capital investment choices.

Running head: STRATEGIC AND SUSTAINABILITY ACCOUNTING 1

Strategic and Sustainability Accounting

Name

Institutional Affiliation

Strategic and Sustainability Accounting

Name

Institutional Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC AND SUSTAINABILITY ACCOUNTING 2

STRATEGIC AND SUSTAINABILITY ACCOUNTING

Executive Summary

Three topics have been discussed in this assignment including sustainability, transfer

pricing in Vans, and capital investment analysis in Accent Group Limited. It has been

demonstrated that a company must consider both environmental and social risks to be

sustainable. It is also showcase in this paper that the Vans can buy the raw materials from

external suppliers since it is cheaper as compared to buy within or transferring within the two

departments. It is also recommended that the Company should proceed with the proposal to

upgrade the stores for increased customer experiences.

STRATEGIC AND SUSTAINABILITY ACCOUNTING

Executive Summary

Three topics have been discussed in this assignment including sustainability, transfer

pricing in Vans, and capital investment analysis in Accent Group Limited. It has been

demonstrated that a company must consider both environmental and social risks to be

sustainable. It is also showcase in this paper that the Vans can buy the raw materials from

external suppliers since it is cheaper as compared to buy within or transferring within the two

departments. It is also recommended that the Company should proceed with the proposal to

upgrade the stores for increased customer experiences.

STRATEGIC AND SUSTAINABILITY ACCOUNTING 3

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Question 1: Sustainability................................................................................................................4

Question 2: Transfer Pricing............................................................................................................8

Question 3: Capital Investment Analysis......................................................................................13

Conclusion.....................................................................................................................................18

Appendix........................................................................................................................................19

References......................................................................................................................................21

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Question 1: Sustainability................................................................................................................4

Question 2: Transfer Pricing............................................................................................................8

Question 3: Capital Investment Analysis......................................................................................13

Conclusion.....................................................................................................................................18

Appendix........................................................................................................................................19

References......................................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STRATEGIC AND SUSTAINABILITY ACCOUNTING 4

Introduction

This paper is sectioned into three parts each tackling a separate questions. The first part

has discusses sustainability based on the case of Accent Group Limited. It looks at the impacts of

the Group on environment and society in range of ways. It is held that management of the Group

understands and manage their social and environment risks by benefiting from identification of

appropriate social and environmental performance objectives and use appropriate KPIs to track

its performance towards the identified objectives. The next topic discussed is the transfer pricing

in respect of Vans’ production of lifestyle footwear. The analysis of the hypothetical data

regarding transfer of rubber to its Assembly department from Rubber department is performed to

determine whether it is best to buy from external suppliers or not. Topic 3 discussed is on capital

investment analysis using the Accent Group Limited management case which has received a

proposal from Hype DC manager regarding upgrade of stores to enhance experience of

customers.

Question 1: Sustainability

Conserving environment remains a fundamental issue which must be tackled by Accent

Group Limited given the nature of its operations and products’ impacts on society and

environment in many ways. It remains vital the Group’s management to comprehend and

manage their social and environmental risks. Thus, the Group must correctly identify relevant

social and environmental performance objectives. The Group should use relevant KPIs

performance measures to track the performance towards the set objectives. Accent Group

Limited remains the regional leader in performance and lifestyle footwear’s retail and

distribution, with more than stores crossways ten different retail banners alongside exclusive

distribution rights for ten international brands crossways New Zealand Australia.

Introduction

This paper is sectioned into three parts each tackling a separate questions. The first part

has discusses sustainability based on the case of Accent Group Limited. It looks at the impacts of

the Group on environment and society in range of ways. It is held that management of the Group

understands and manage their social and environment risks by benefiting from identification of

appropriate social and environmental performance objectives and use appropriate KPIs to track

its performance towards the identified objectives. The next topic discussed is the transfer pricing

in respect of Vans’ production of lifestyle footwear. The analysis of the hypothetical data

regarding transfer of rubber to its Assembly department from Rubber department is performed to

determine whether it is best to buy from external suppliers or not. Topic 3 discussed is on capital

investment analysis using the Accent Group Limited management case which has received a

proposal from Hype DC manager regarding upgrade of stores to enhance experience of

customers.

Question 1: Sustainability

Conserving environment remains a fundamental issue which must be tackled by Accent

Group Limited given the nature of its operations and products’ impacts on society and

environment in many ways. It remains vital the Group’s management to comprehend and

manage their social and environmental risks. Thus, the Group must correctly identify relevant

social and environmental performance objectives. The Group should use relevant KPIs

performance measures to track the performance towards the set objectives. Accent Group

Limited remains the regional leader in performance and lifestyle footwear’s retail and

distribution, with more than stores crossways ten different retail banners alongside exclusive

distribution rights for ten international brands crossways New Zealand Australia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC AND SUSTAINABILITY ACCOUNTING 5

The ever increasing demand for shoes raises the production and manufacture of shoes

every year. This leads to various environmental impacts of shoe industry which cannot be

negated much longer. Shoes manufacture, distribution and sales pose various threats to wellbeing

of the planet as a range of toxins, fossil fuels and chemicals being produced as well as leaked

into the environment during the initial and final stages of shoe life cycle. Such chemicals remain

harmful to both the humans and wildlife which come into contact with them, and consequently,

triggers health problems (social risks) (Davila, Herrera, Hunter, Martin & Winkler, 2019).

Moreover, footwear manufacturing emits huge volumes of carbon dioxide that contributes to the

already severe effects on global warming and climate change (Reisman & Olazabal, 2016).

One of the severe environment impact of shoes arise from manufacturing stages; and

sadly, majority of people believe that footwear solely becomes a threat to environment after

being disposed of. Enormous amounts of chemicals and machinery are needed to produce

footwear. Powering these machines require the use of large amount of fossil fuels which emit

greenhouse gases when burned. Coal is one of the energy sources which was often utilized in

powering footwear factories because it is cheap, but its burning emits carbon monoxide that ends

up in atmosphere leading greenhouse effects and hence a negative impact (Tsai & Jhong, 2019).

The transportation and distribution of shoes also emits carbon dioxide since transportation

remains an important aspects of marketing footwear industry since most manufacturing firms

build factories in developing economies for cheap labor. Because factories are located far away,

transportation and distribution using ships, airplane, and trucks require to deliver products to

retailers.

The third environmental impact is that chemicals used in process of manufacturing

contribute negatively to the environment through pollution which socially affects people, and

The ever increasing demand for shoes raises the production and manufacture of shoes

every year. This leads to various environmental impacts of shoe industry which cannot be

negated much longer. Shoes manufacture, distribution and sales pose various threats to wellbeing

of the planet as a range of toxins, fossil fuels and chemicals being produced as well as leaked

into the environment during the initial and final stages of shoe life cycle. Such chemicals remain

harmful to both the humans and wildlife which come into contact with them, and consequently,

triggers health problems (social risks) (Davila, Herrera, Hunter, Martin & Winkler, 2019).

Moreover, footwear manufacturing emits huge volumes of carbon dioxide that contributes to the

already severe effects on global warming and climate change (Reisman & Olazabal, 2016).

One of the severe environment impact of shoes arise from manufacturing stages; and

sadly, majority of people believe that footwear solely becomes a threat to environment after

being disposed of. Enormous amounts of chemicals and machinery are needed to produce

footwear. Powering these machines require the use of large amount of fossil fuels which emit

greenhouse gases when burned. Coal is one of the energy sources which was often utilized in

powering footwear factories because it is cheap, but its burning emits carbon monoxide that ends

up in atmosphere leading greenhouse effects and hence a negative impact (Tsai & Jhong, 2019).

The transportation and distribution of shoes also emits carbon dioxide since transportation

remains an important aspects of marketing footwear industry since most manufacturing firms

build factories in developing economies for cheap labor. Because factories are located far away,

transportation and distribution using ships, airplane, and trucks require to deliver products to

retailers.

The third environmental impact is that chemicals used in process of manufacturing

contribute negatively to the environment through pollution which socially affects people, and

STRATEGIC AND SUSTAINABILITY ACCOUNTING 6

wildlife health. Several chemical adhesives alongside tanning chemicals are utilized in

processing different footwear parts. Such chemicals leak easily into water and environment via

factories’ discharges hence harmful to wildlife and people who consume such infected plants and

water. Thus, manufacturing process for footwear pose several risks to environment because of

large volumes of carbon dioxide being emitted and various chemicals utilized in manufacturing

footwear (Munny et al., 2019).

Footwear disposal further contributes to significant environment and social impacts as

thrown out shoes end up in landfills which contaminate the soil and drinking water for people

because the chemicals utilized in manufacturing gradually begin to leak into soil as footwear

slowly begin to decompose. Such has significant effect on both humans and wildlife since bio-

magnification alongside bioaccumulation might take place as wildlife consumed by humans

might have drunk contaminated water or fed on contaminated plants (Herghiligiu, Mihai,

Sarghie, Bizarro & Arias, 2016). This might culminate in several health effects like cancer.

Finally, footwear disposal has a huge effect on social and environment as several chemicals

begin to leak and pollute water and soil.

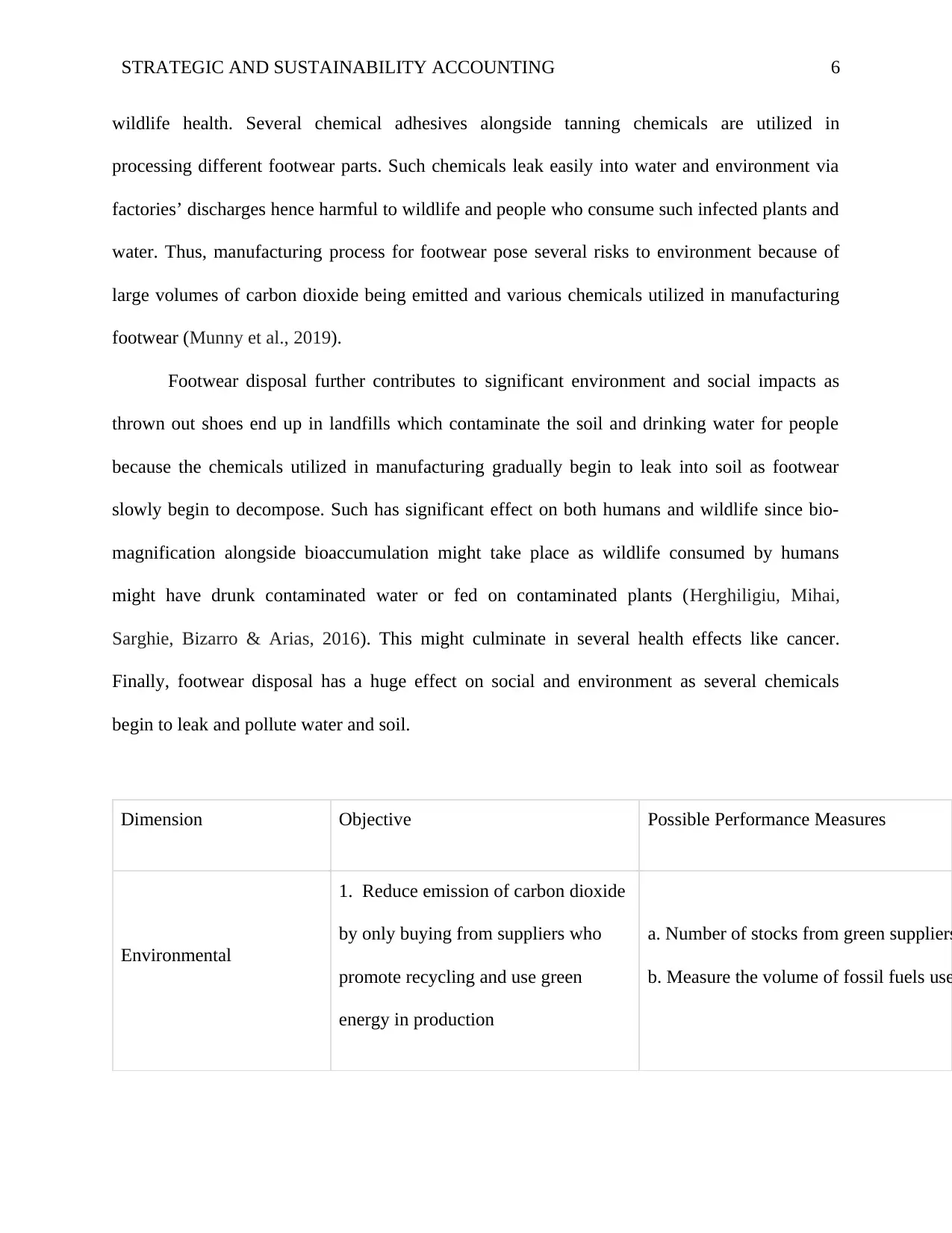

Dimension Objective Possible Performance Measures

Environmental

1. Reduce emission of carbon dioxide

by only buying from suppliers who

promote recycling and use green

energy in production

a. Number of stocks from green suppliers

b. Measure the volume of fossil fuels use

wildlife health. Several chemical adhesives alongside tanning chemicals are utilized in

processing different footwear parts. Such chemicals leak easily into water and environment via

factories’ discharges hence harmful to wildlife and people who consume such infected plants and

water. Thus, manufacturing process for footwear pose several risks to environment because of

large volumes of carbon dioxide being emitted and various chemicals utilized in manufacturing

footwear (Munny et al., 2019).

Footwear disposal further contributes to significant environment and social impacts as

thrown out shoes end up in landfills which contaminate the soil and drinking water for people

because the chemicals utilized in manufacturing gradually begin to leak into soil as footwear

slowly begin to decompose. Such has significant effect on both humans and wildlife since bio-

magnification alongside bioaccumulation might take place as wildlife consumed by humans

might have drunk contaminated water or fed on contaminated plants (Herghiligiu, Mihai,

Sarghie, Bizarro & Arias, 2016). This might culminate in several health effects like cancer.

Finally, footwear disposal has a huge effect on social and environment as several chemicals

begin to leak and pollute water and soil.

Dimension Objective Possible Performance Measures

Environmental

1. Reduce emission of carbon dioxide

by only buying from suppliers who

promote recycling and use green

energy in production

a. Number of stocks from green suppliers

b. Measure the volume of fossil fuels use

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

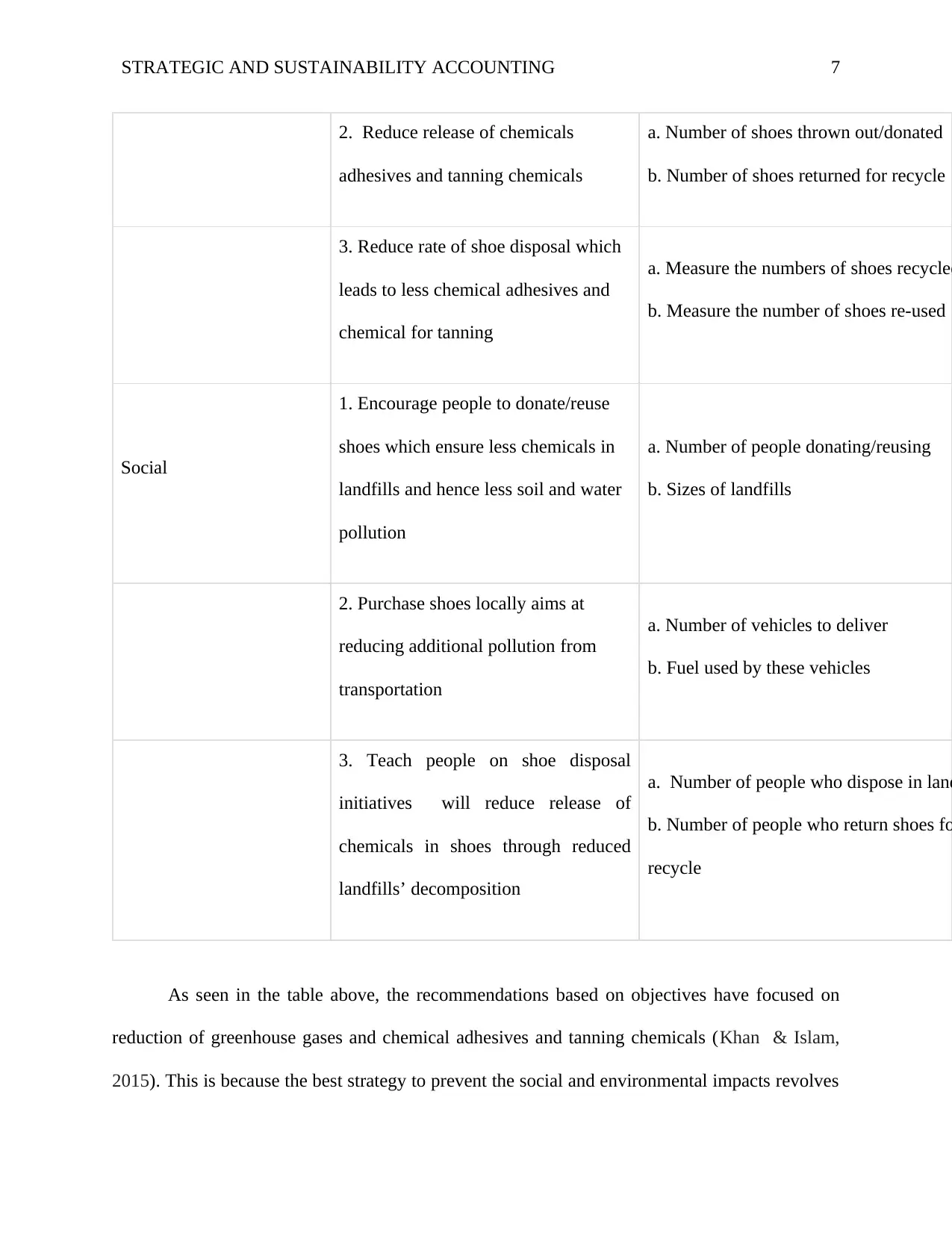

STRATEGIC AND SUSTAINABILITY ACCOUNTING 7

2. Reduce release of chemicals

adhesives and tanning chemicals

a. Number of shoes thrown out/donated

b. Number of shoes returned for recycle

3. Reduce rate of shoe disposal which

leads to less chemical adhesives and

chemical for tanning

a. Measure the numbers of shoes recycled

b. Measure the number of shoes re-used

Social

1. Encourage people to donate/reuse

shoes which ensure less chemicals in

landfills and hence less soil and water

pollution

a. Number of people donating/reusing

b. Sizes of landfills

2. Purchase shoes locally aims at

reducing additional pollution from

transportation

a. Number of vehicles to deliver

b. Fuel used by these vehicles

3. Teach people on shoe disposal

initiatives will reduce release of

chemicals in shoes through reduced

landfills’ decomposition

a. Number of people who dispose in land

b. Number of people who return shoes fo

recycle

As seen in the table above, the recommendations based on objectives have focused on

reduction of greenhouse gases and chemical adhesives and tanning chemicals (Khan & Islam,

2015). This is because the best strategy to prevent the social and environmental impacts revolves

2. Reduce release of chemicals

adhesives and tanning chemicals

a. Number of shoes thrown out/donated

b. Number of shoes returned for recycle

3. Reduce rate of shoe disposal which

leads to less chemical adhesives and

chemical for tanning

a. Measure the numbers of shoes recycled

b. Measure the number of shoes re-used

Social

1. Encourage people to donate/reuse

shoes which ensure less chemicals in

landfills and hence less soil and water

pollution

a. Number of people donating/reusing

b. Sizes of landfills

2. Purchase shoes locally aims at

reducing additional pollution from

transportation

a. Number of vehicles to deliver

b. Fuel used by these vehicles

3. Teach people on shoe disposal

initiatives will reduce release of

chemicals in shoes through reduced

landfills’ decomposition

a. Number of people who dispose in land

b. Number of people who return shoes fo

recycle

As seen in the table above, the recommendations based on objectives have focused on

reduction of greenhouse gases and chemical adhesives and tanning chemicals (Khan & Islam,

2015). This is because the best strategy to prevent the social and environmental impacts revolves

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC AND SUSTAINABILITY ACCOUNTING 8

around recycling, re-use or donating used shoes to deter disposal in landfills. As already

implemented by Nike, “Re-use-a-shoe” culture must be encouraged. Thus, the Group will greatly

reduce pollution by encouraging its customers to re-use or donate. The group should also

purchase from locally to avoid additional pollution through transportation which further emit

greenhouse gases. Purchasing footwear from green suppliers is effective since it means it will

encourage footwear manufacturers to use green energy in production hence less pollution (García

& Prieto, 2019).

Question 2: Transfer Pricing

I.

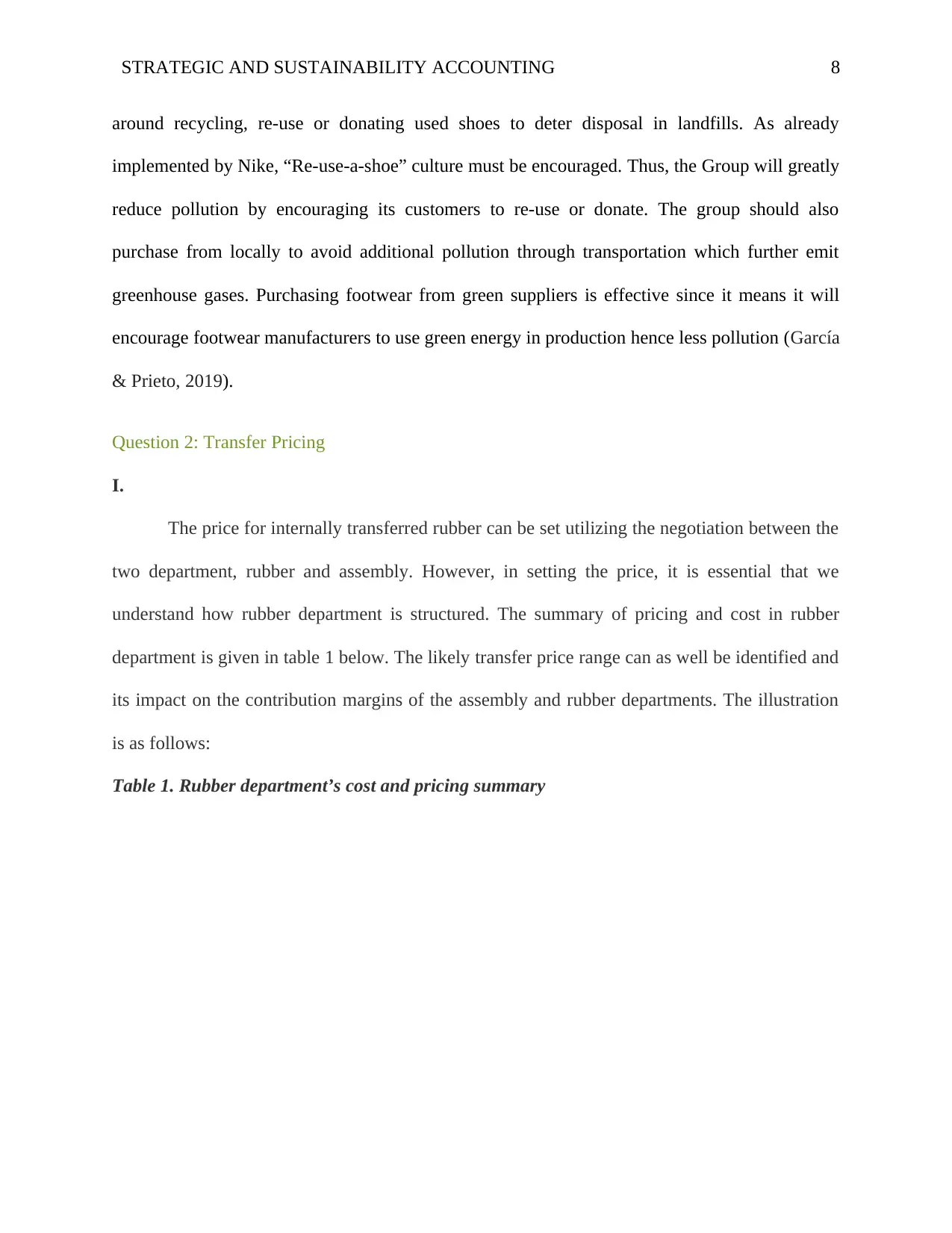

The price for internally transferred rubber can be set utilizing the negotiation between the

two department, rubber and assembly. However, in setting the price, it is essential that we

understand how rubber department is structured. The summary of pricing and cost in rubber

department is given in table 1 below. The likely transfer price range can as well be identified and

its impact on the contribution margins of the assembly and rubber departments. The illustration

is as follows:

Table 1. Rubber department’s cost and pricing summary

around recycling, re-use or donating used shoes to deter disposal in landfills. As already

implemented by Nike, “Re-use-a-shoe” culture must be encouraged. Thus, the Group will greatly

reduce pollution by encouraging its customers to re-use or donate. The group should also

purchase from locally to avoid additional pollution through transportation which further emit

greenhouse gases. Purchasing footwear from green suppliers is effective since it means it will

encourage footwear manufacturers to use green energy in production hence less pollution (García

& Prieto, 2019).

Question 2: Transfer Pricing

I.

The price for internally transferred rubber can be set utilizing the negotiation between the

two department, rubber and assembly. However, in setting the price, it is essential that we

understand how rubber department is structured. The summary of pricing and cost in rubber

department is given in table 1 below. The likely transfer price range can as well be identified and

its impact on the contribution margins of the assembly and rubber departments. The illustration

is as follows:

Table 1. Rubber department’s cost and pricing summary

STRATEGIC AND SUSTAINABILITY ACCOUNTING 9

Price Range: As seen in table 1 above, the price range can be determined. The minimum

transfer price to be set by Rubber department needs to be equivalent to the manufacture’s

Variable Cost (VC) which is 1.30 dollars. Because the outside market exists for the product at

2.00 dollars, the maximum price which can be set to sell to the assembly department shall be

equivalent to VC plus contribution forgone (1.30 + 0.70=2.00 dollars). Therefore, the maximum

transfer price shall be 2.00 dollars. The range is thus from 1.30$ to $2.00$.

Table 2: Impacts of Transfer pricing (price range) on margin of each department

Price Range: As seen in table 1 above, the price range can be determined. The minimum

transfer price to be set by Rubber department needs to be equivalent to the manufacture’s

Variable Cost (VC) which is 1.30 dollars. Because the outside market exists for the product at

2.00 dollars, the maximum price which can be set to sell to the assembly department shall be

equivalent to VC plus contribution forgone (1.30 + 0.70=2.00 dollars). Therefore, the maximum

transfer price shall be 2.00 dollars. The range is thus from 1.30$ to $2.00$.

Table 2: Impacts of Transfer pricing (price range) on margin of each department

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STRATEGIC AND SUSTAINABILITY ACCOUNTING

10

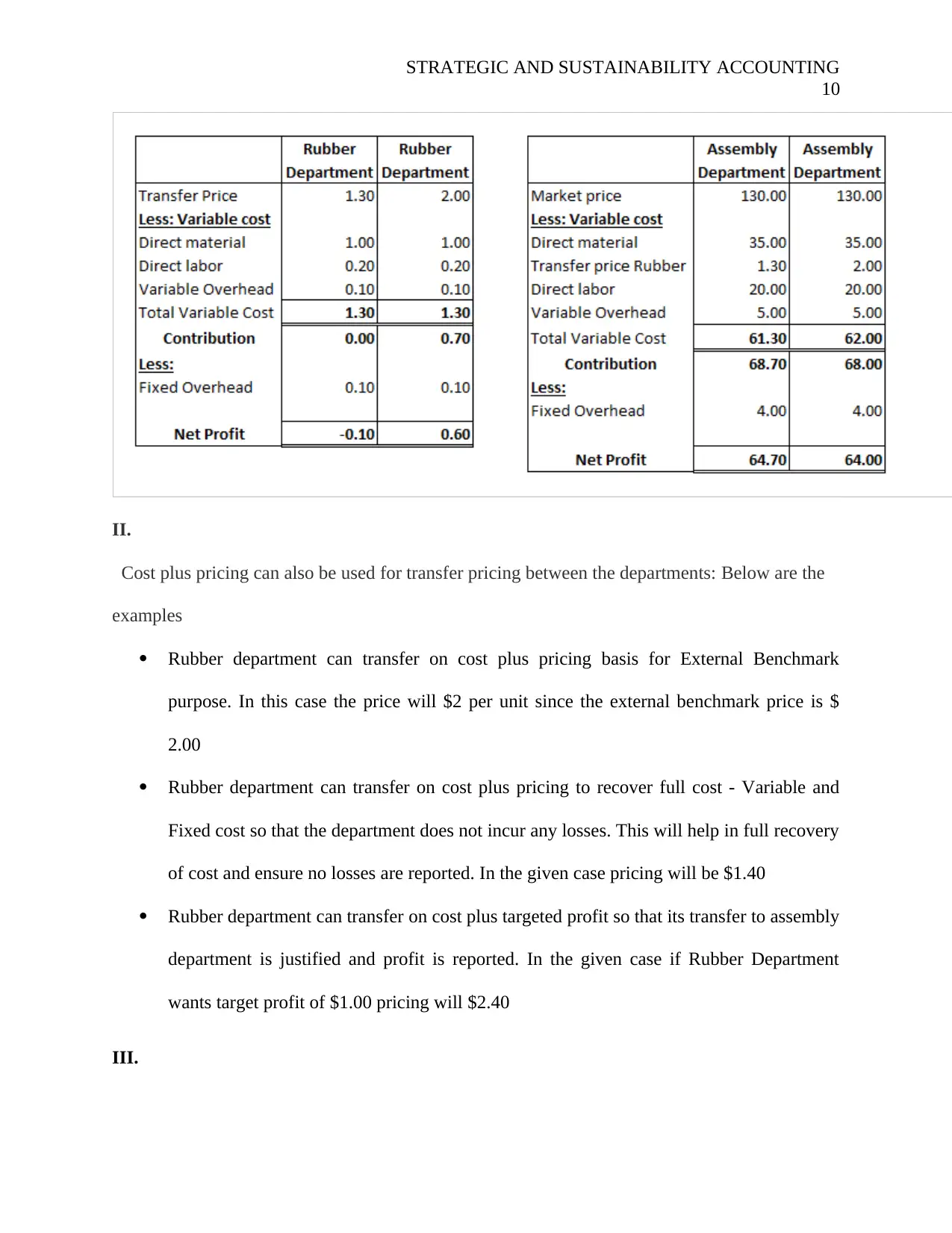

II.

Cost plus pricing can also be used for transfer pricing between the departments: Below are the

examples

Rubber department can transfer on cost plus pricing basis for External Benchmark

purpose. In this case the price will $2 per unit since the external benchmark price is $

2.00

Rubber department can transfer on cost plus pricing to recover full cost - Variable and

Fixed cost so that the department does not incur any losses. This will help in full recovery

of cost and ensure no losses are reported. In the given case pricing will be $1.40

Rubber department can transfer on cost plus targeted profit so that its transfer to assembly

department is justified and profit is reported. In the given case if Rubber Department

wants target profit of $1.00 pricing will $2.40

III.

10

II.

Cost plus pricing can also be used for transfer pricing between the departments: Below are the

examples

Rubber department can transfer on cost plus pricing basis for External Benchmark

purpose. In this case the price will $2 per unit since the external benchmark price is $

2.00

Rubber department can transfer on cost plus pricing to recover full cost - Variable and

Fixed cost so that the department does not incur any losses. This will help in full recovery

of cost and ensure no losses are reported. In the given case pricing will be $1.40

Rubber department can transfer on cost plus targeted profit so that its transfer to assembly

department is justified and profit is reported. In the given case if Rubber Department

wants target profit of $1.00 pricing will $2.40

III.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC AND SUSTAINABILITY ACCOUNTING

11

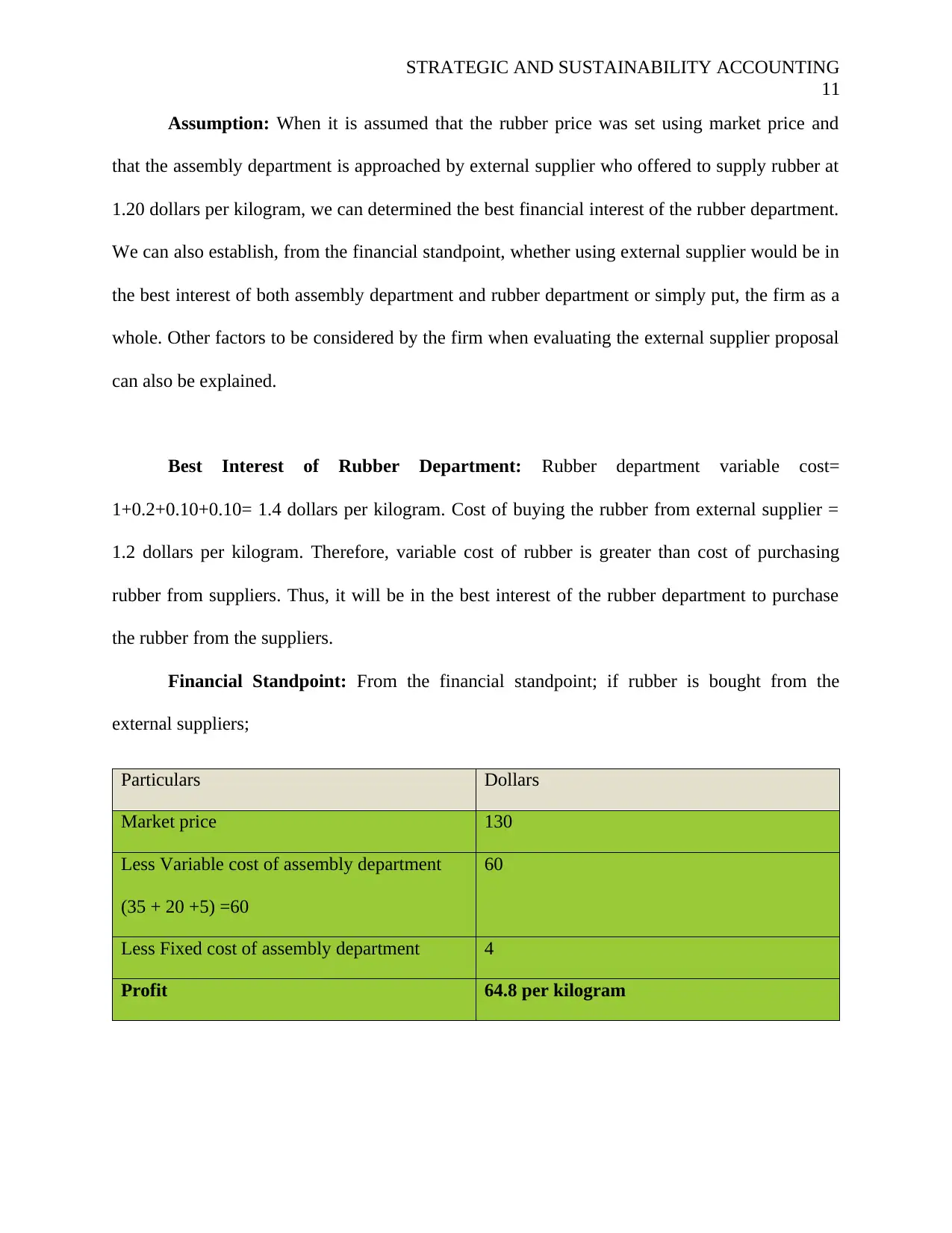

Assumption: When it is assumed that the rubber price was set using market price and

that the assembly department is approached by external supplier who offered to supply rubber at

1.20 dollars per kilogram, we can determined the best financial interest of the rubber department.

We can also establish, from the financial standpoint, whether using external supplier would be in

the best interest of both assembly department and rubber department or simply put, the firm as a

whole. Other factors to be considered by the firm when evaluating the external supplier proposal

can also be explained.

Best Interest of Rubber Department: Rubber department variable cost=

1+0.2+0.10+0.10= 1.4 dollars per kilogram. Cost of buying the rubber from external supplier =

1.2 dollars per kilogram. Therefore, variable cost of rubber is greater than cost of purchasing

rubber from suppliers. Thus, it will be in the best interest of the rubber department to purchase

the rubber from the suppliers.

Financial Standpoint: From the financial standpoint; if rubber is bought from the

external suppliers;

Particulars Dollars

Market price 130

Less Variable cost of assembly department

(35 + 20 +5) =60

60

Less Fixed cost of assembly department 4

Profit 64.8 per kilogram

11

Assumption: When it is assumed that the rubber price was set using market price and

that the assembly department is approached by external supplier who offered to supply rubber at

1.20 dollars per kilogram, we can determined the best financial interest of the rubber department.

We can also establish, from the financial standpoint, whether using external supplier would be in

the best interest of both assembly department and rubber department or simply put, the firm as a

whole. Other factors to be considered by the firm when evaluating the external supplier proposal

can also be explained.

Best Interest of Rubber Department: Rubber department variable cost=

1+0.2+0.10+0.10= 1.4 dollars per kilogram. Cost of buying the rubber from external supplier =

1.2 dollars per kilogram. Therefore, variable cost of rubber is greater than cost of purchasing

rubber from suppliers. Thus, it will be in the best interest of the rubber department to purchase

the rubber from the suppliers.

Financial Standpoint: From the financial standpoint; if rubber is bought from the

external suppliers;

Particulars Dollars

Market price 130

Less Variable cost of assembly department

(35 + 20 +5) =60

60

Less Fixed cost of assembly department 4

Profit 64.8 per kilogram

STRATEGIC AND SUSTAINABILITY ACCOUNTING

12

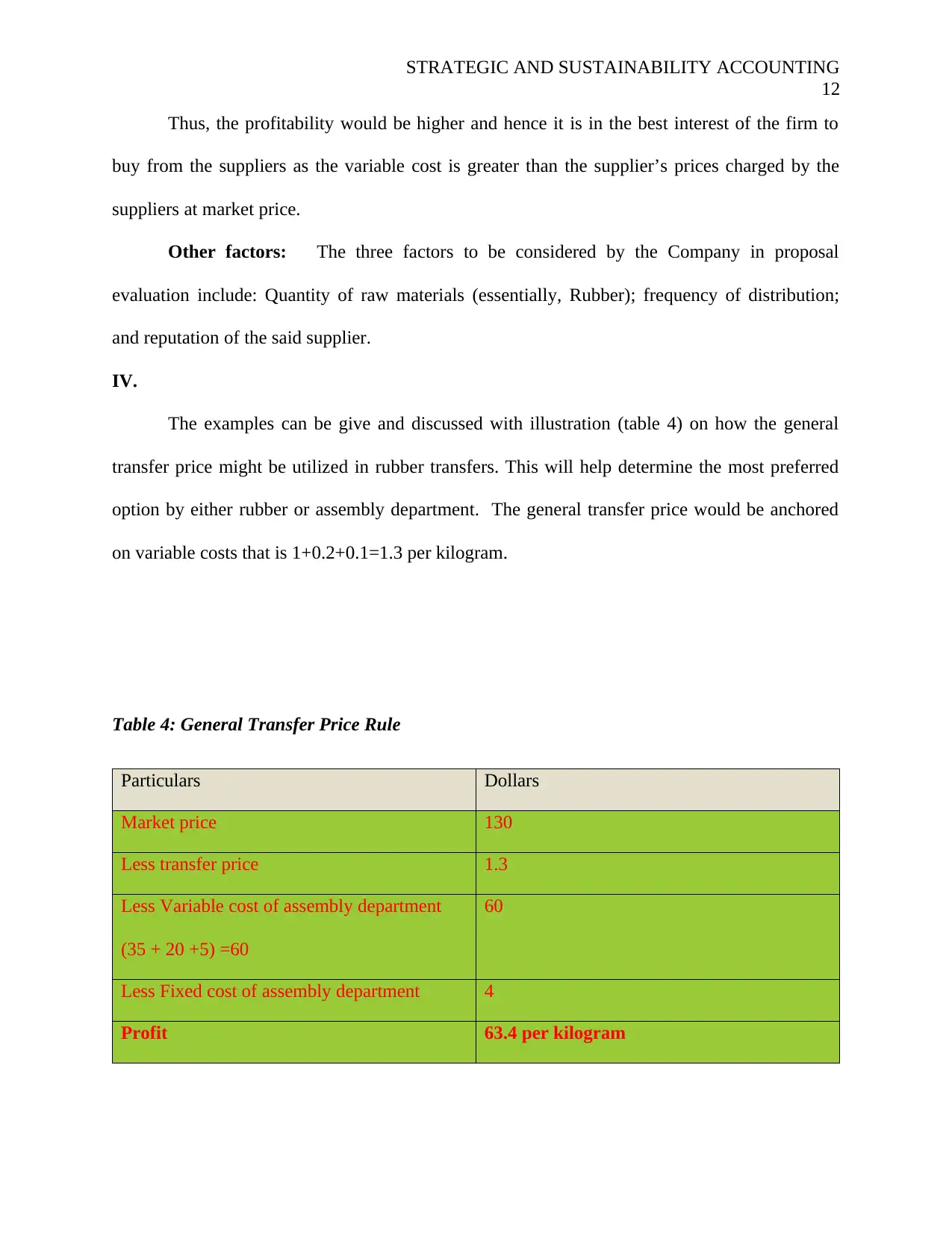

Thus, the profitability would be higher and hence it is in the best interest of the firm to

buy from the suppliers as the variable cost is greater than the supplier’s prices charged by the

suppliers at market price.

Other factors: The three factors to be considered by the Company in proposal

evaluation include: Quantity of raw materials (essentially, Rubber); frequency of distribution;

and reputation of the said supplier.

IV.

The examples can be give and discussed with illustration (table 4) on how the general

transfer price might be utilized in rubber transfers. This will help determine the most preferred

option by either rubber or assembly department. The general transfer price would be anchored

on variable costs that is 1+0.2+0.1=1.3 per kilogram.

Table 4: General Transfer Price Rule

Particulars Dollars

Market price 130

Less transfer price 1.3

Less Variable cost of assembly department

(35 + 20 +5) =60

60

Less Fixed cost of assembly department 4

Profit 63.4 per kilogram

12

Thus, the profitability would be higher and hence it is in the best interest of the firm to

buy from the suppliers as the variable cost is greater than the supplier’s prices charged by the

suppliers at market price.

Other factors: The three factors to be considered by the Company in proposal

evaluation include: Quantity of raw materials (essentially, Rubber); frequency of distribution;

and reputation of the said supplier.

IV.

The examples can be give and discussed with illustration (table 4) on how the general

transfer price might be utilized in rubber transfers. This will help determine the most preferred

option by either rubber or assembly department. The general transfer price would be anchored

on variable costs that is 1+0.2+0.1=1.3 per kilogram.

Table 4: General Transfer Price Rule

Particulars Dollars

Market price 130

Less transfer price 1.3

Less Variable cost of assembly department

(35 + 20 +5) =60

60

Less Fixed cost of assembly department 4

Profit 63.4 per kilogram

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.