Financial Performance Analysis of Stratford Yachts Limited Report

VerifiedAdded on 2020/12/10

|12

|2504

|101

Report

AI Summary

This report provides a comprehensive overview of managing financial resources. It begins by differentiating between financial and management accounting, highlighting their key differences in terms of purpose, objectives, time frame, and information used. The report then explores the purpose of various financial statements for both profit and non-profit entities, including balance sheets, income statements, and cash flow statements. It identifies different stakeholder groups, such as owners, investors, management, lenders, employees, government, and customers, and evaluates their respective information requirements. The second part of the report focuses on a financial performance analysis of Stratford Yachts Limited, calculating key financial ratios such as net profit margin, return on capital employed, and asset turnover. The analysis assesses the company's performance based on liquidity and profitability, discussing the implications of the calculated ratios and comparing them to industry standards. The report concludes with an evaluation of the company's financial position, highlighting areas of strength and weakness and offering recommendations for improvement.

MANAGING

FINANCIAL

RESOURCES

FINANCIAL

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Explaining difference between financial account and management account........................3

1.2 Identifying and explaining purpose of different financial statements in a profit and non-

profit entities...............................................................................................................................5

1.3 Identifying the different groups of stakeholders and evaluating their different information

requirement.................................................................................................................................6

TASK 2............................................................................................................................................8

2.1 Calculate below mentioned ratio...........................................................................................8

2.2 Report on performance of Stratford Yachts Limited on basis of liquidity and profitability.9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Explaining difference between financial account and management account........................3

1.2 Identifying and explaining purpose of different financial statements in a profit and non-

profit entities...............................................................................................................................5

1.3 Identifying the different groups of stakeholders and evaluating their different information

requirement.................................................................................................................................6

TASK 2............................................................................................................................................8

2.1 Calculate below mentioned ratio...........................................................................................8

2.2 Report on performance of Stratford Yachts Limited on basis of liquidity and profitability.9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The organization has very important aspect of managing financial resources. The present

report is giving brief discussion about basic concepts of both financial and management

accounting as well along with its key variations. Further it is reflecting requirement of financial

and managerial requirements. In the same series it has elaborated various objective of statements

in business which are profitable or non profitable. In the last part of report it had interpreted

financial position of Stratford Yachts Limited in terms of profitability and liquidity analysis

along with specific ratio analysis.

TASK 1

1.1 Explaining difference between financial account and management account.

The key difference between financial and management accounting are:

Basis of difference Financial Accounting Management Accounting

Meaning Financial Accounting gives the

true and fair view of the

financial position of the

company. Financial accounts

are prepared so that the

stakeholders and investors can

analyse the financial

performance of the company

with the past performance.

Financial accounts help the

stakeholder to analyse the

financial statement of the

company and to decide whether

to invest in the company or not

(Financial Accounting vs

Management Accounting,

Management accounting is

prepared for the managers to

have the better understanding

of the management of the

organization. It provides the

information within the

organisation. The

information from the

management accounts helps

the managers to formulates

the policies, planning,

forecasting and controlling

the day to day operations of

the company for the effective

working of business

organisation.

The organization has very important aspect of managing financial resources. The present

report is giving brief discussion about basic concepts of both financial and management

accounting as well along with its key variations. Further it is reflecting requirement of financial

and managerial requirements. In the same series it has elaborated various objective of statements

in business which are profitable or non profitable. In the last part of report it had interpreted

financial position of Stratford Yachts Limited in terms of profitability and liquidity analysis

along with specific ratio analysis.

TASK 1

1.1 Explaining difference between financial account and management account.

The key difference between financial and management accounting are:

Basis of difference Financial Accounting Management Accounting

Meaning Financial Accounting gives the

true and fair view of the

financial position of the

company. Financial accounts

are prepared so that the

stakeholders and investors can

analyse the financial

performance of the company

with the past performance.

Financial accounts help the

stakeholder to analyse the

financial statement of the

company and to decide whether

to invest in the company or not

(Financial Accounting vs

Management Accounting,

Management accounting is

prepared for the managers to

have the better understanding

of the management of the

organization. It provides the

information within the

organisation. The

information from the

management accounts helps

the managers to formulates

the policies, planning,

forecasting and controlling

the day to day operations of

the company for the effective

working of business

organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018).

Objectives Financial accounting is

prepared to show the accurate

and true picture of financial

position of a company by

analysing daily financial

statements and transactions to

the outside parties.

Management accounts are

prepared to help the

management of the

organisation to analyse the

operation and make the

correct decisions and

strategies for the business

operations and to maximised

the profit.

Time frame Financial accounts are made at

the end financial year or on

quarterly basis.

Management accounts are

prepared as per the need and

requirement of the company.

Basis of making The past performance of the

company is the base to make

the financial accounts.

Management accounting can

be done by past information

or the predictive information

on the basis of decision

making.

Information Financial accounts are mostly

quantitative, and it is

mandatory by law to prepare

financial accounts of all

companies.

Management accounting can

be made on both quantitative

and qualitative basis and

there is no statutory

requirement to prepare the

management accounting.

1.2 Identifying and explaining purpose of different financial statements in a profit and non- profit

entities.

The purpose of the profit organization is to maximize its profit for their owner. To

Objectives Financial accounting is

prepared to show the accurate

and true picture of financial

position of a company by

analysing daily financial

statements and transactions to

the outside parties.

Management accounts are

prepared to help the

management of the

organisation to analyse the

operation and make the

correct decisions and

strategies for the business

operations and to maximised

the profit.

Time frame Financial accounts are made at

the end financial year or on

quarterly basis.

Management accounts are

prepared as per the need and

requirement of the company.

Basis of making The past performance of the

company is the base to make

the financial accounts.

Management accounting can

be done by past information

or the predictive information

on the basis of decision

making.

Information Financial accounts are mostly

quantitative, and it is

mandatory by law to prepare

financial accounts of all

companies.

Management accounting can

be made on both quantitative

and qualitative basis and

there is no statutory

requirement to prepare the

management accounting.

1.2 Identifying and explaining purpose of different financial statements in a profit and non- profit

entities.

The purpose of the profit organization is to maximize its profit for their owner. To

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

achieve the purpose various financial statements are prepared to for profit organizations.

The financial statements for profit organizations are:

1) Balance Sheet:

For the profit organizations, Balance sheet is an important financial statement which

gives the clear picture of a financial position of a company. Balance sheet shows the assets and

liabilities of the company. After assets and liabilities the balance sheet shows the owner's equity

which is the net worth of the company. It is an important statement which helps the stakeholders

and investors to decide whether to invest in the company or not (Minnis and Sutherland, 2017).

2) Income statement:

The revenue of a company is evaluated through the income statement over a specific time

period. The income statement shows what the company is earned or lost in a specific time period.

The statement shows the company's profitability and increasing assets which correlate to the

future dividends and the return on investment to the shareholders and owners.

3) Cash flow statement:

The inflow or the outflow of the cash in a specific time period is represented through the

cash flow statements. All the profit and non-profit organization has cash flow system as it is an

integral part of the financial system which is used to evaluate the transaction of many in different

activities in business organization. Stratford Yachts Ltd. Has fallen under the profit organisation,

it should follow the various financial statements like balance sheet, income statement and cash

flow statement for the financial analysis of the company. Non-profit organisation are those which

are not owned by shareholder or investors and not intended to earn profit they generally work on

a charitable basis. Non-profit organisation uses a different financial statements.

The non-profit financial statements are:

1)Statement of financial position:

The financial statements for profit organizations are:

1) Balance Sheet:

For the profit organizations, Balance sheet is an important financial statement which

gives the clear picture of a financial position of a company. Balance sheet shows the assets and

liabilities of the company. After assets and liabilities the balance sheet shows the owner's equity

which is the net worth of the company. It is an important statement which helps the stakeholders

and investors to decide whether to invest in the company or not (Minnis and Sutherland, 2017).

2) Income statement:

The revenue of a company is evaluated through the income statement over a specific time

period. The income statement shows what the company is earned or lost in a specific time period.

The statement shows the company's profitability and increasing assets which correlate to the

future dividends and the return on investment to the shareholders and owners.

3) Cash flow statement:

The inflow or the outflow of the cash in a specific time period is represented through the

cash flow statements. All the profit and non-profit organization has cash flow system as it is an

integral part of the financial system which is used to evaluate the transaction of many in different

activities in business organization. Stratford Yachts Ltd. Has fallen under the profit organisation,

it should follow the various financial statements like balance sheet, income statement and cash

flow statement for the financial analysis of the company. Non-profit organisation are those which

are not owned by shareholder or investors and not intended to earn profit they generally work on

a charitable basis. Non-profit organisation uses a different financial statements.

The non-profit financial statements are:

1)Statement of financial position:

The balance sheet of non-profit organisation is termed as statement of financial position as there

are no shareholder or investors in non-profit organisation. But unlike balance sheet the leftover

after the liabilities and assets is called net assets. In non-profit organisation the net asset is

further divided into unrestricted net assets, temporarily restricted net assets, and permanently

restricted net assets which based on the donor restrictions (Cascino and et. al., 2014).

2)Statement of activities:

In non-profit organisation revenue is not generated through selling of goods and services,

but the sources of funds are grants, donation fundraising etc. Non-profit organisation also have

day to day operative expenses. Statements of activities shows the surplus or the deficit with the

net of sources of funds and expenses. This statements help the company to check how much they

are spending the money.

3)Cash flow statements:

For business organization, cash flow statement is very important, in non-profit

organisation apart from revenue they also get cash from donations, governments, grants. So they

maintain different statements that shows the source and use of funds from each donors.

1.3 Identifying the different groups of stakeholders and evaluating their different information

requirement.

The various group of stakeholders are:

1. Owners and Investors:

The financial information is important for the shareholder and investors of the company

to decide whether to invest in the company or not. Financial statements help them to analyse the

return in investment.

2. Management:

are no shareholder or investors in non-profit organisation. But unlike balance sheet the leftover

after the liabilities and assets is called net assets. In non-profit organisation the net asset is

further divided into unrestricted net assets, temporarily restricted net assets, and permanently

restricted net assets which based on the donor restrictions (Cascino and et. al., 2014).

2)Statement of activities:

In non-profit organisation revenue is not generated through selling of goods and services,

but the sources of funds are grants, donation fundraising etc. Non-profit organisation also have

day to day operative expenses. Statements of activities shows the surplus or the deficit with the

net of sources of funds and expenses. This statements help the company to check how much they

are spending the money.

3)Cash flow statements:

For business organization, cash flow statement is very important, in non-profit

organisation apart from revenue they also get cash from donations, governments, grants. So they

maintain different statements that shows the source and use of funds from each donors.

1.3 Identifying the different groups of stakeholders and evaluating their different information

requirement.

The various group of stakeholders are:

1. Owners and Investors:

The financial information is important for the shareholder and investors of the company

to decide whether to invest in the company or not. Financial statements help them to analyse the

return in investment.

2. Management:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The managers of the organisation needs to analyse the accounting information of business

and checking the performance with the past performance which will help them for better decision

making.

3. Lenders:

The banks and other financial institution which are granting loans to the organisation can

need accounting information to check the ability of the company to repay the loan at the

maturity.

4.Employee:

The employment security and growth opportunities is the basic needs of the employees.

The employee have interest in knowing the company's stability and profitability. The financial

position and performance of the company can give them the career development opportunities.

5.Government:

Different government agencies and tax authority will be interested in knowing the entity's

financial position for tax and regulation purpose. The financial statement is the base for the tax

authorities for accessing the amount of tax collected from the business.

6. Customers:

The customers who are in long term contract with the company will be interested in

knowing the financial position and the company's ability to continue its existence and maintain

to continue its existence (Edmund and Lyamtane, 2018).

and checking the performance with the past performance which will help them for better decision

making.

3. Lenders:

The banks and other financial institution which are granting loans to the organisation can

need accounting information to check the ability of the company to repay the loan at the

maturity.

4.Employee:

The employment security and growth opportunities is the basic needs of the employees.

The employee have interest in knowing the company's stability and profitability. The financial

position and performance of the company can give them the career development opportunities.

5.Government:

Different government agencies and tax authority will be interested in knowing the entity's

financial position for tax and regulation purpose. The financial statement is the base for the tax

authorities for accessing the amount of tax collected from the business.

6. Customers:

The customers who are in long term contract with the company will be interested in

knowing the financial position and the company's ability to continue its existence and maintain

to continue its existence (Edmund and Lyamtane, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

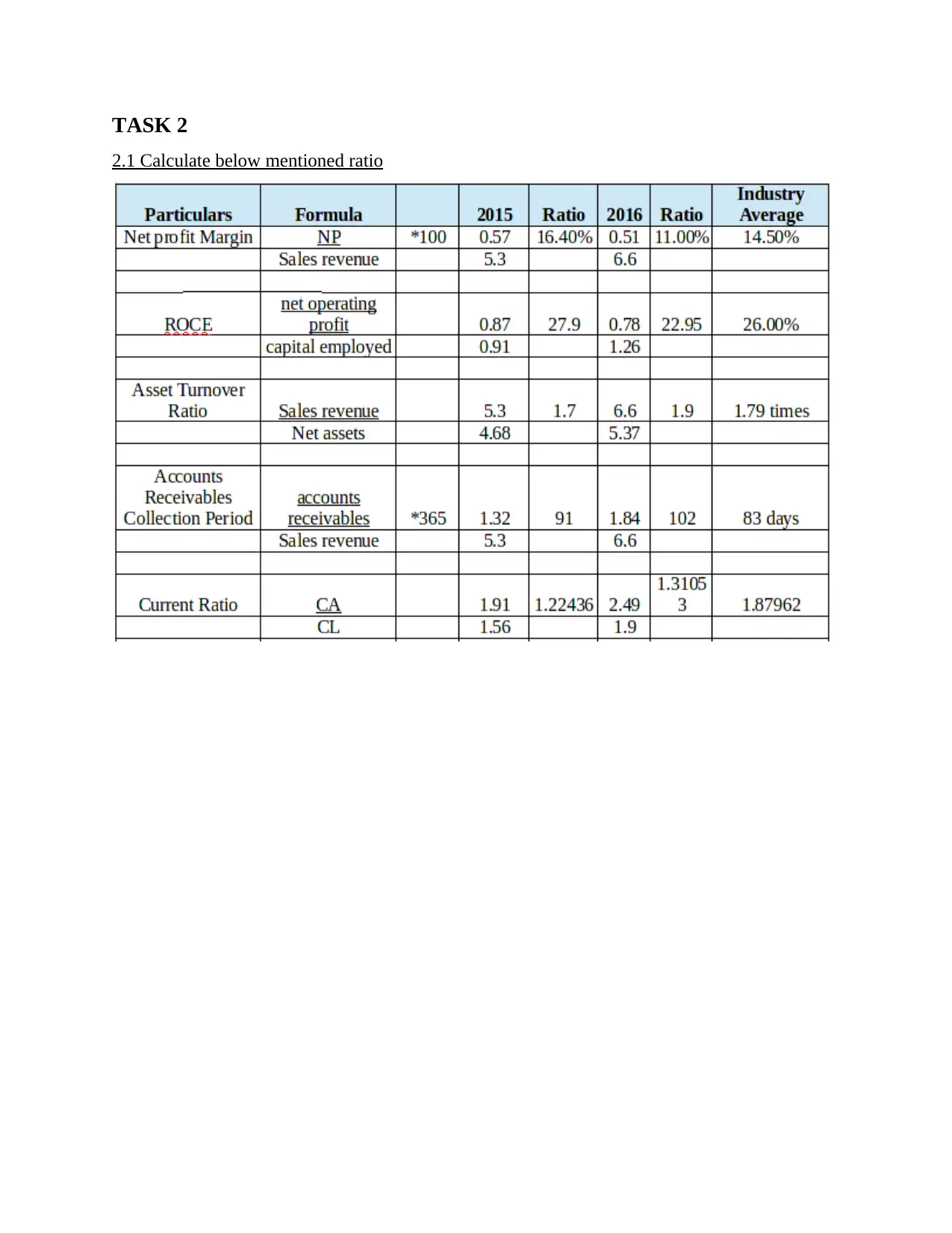

2.1 Calculate below mentioned ratio

2.1 Calculate below mentioned ratio

2.2 Report on performance of Stratford Yachts Limited on basis of liquidity and profitability

Net profit margin: It is reflecting net income which has been earned with sales which

has been gained. The organization has given net profit as 11% in year 2015 but due to

sales revenue it had decreased to 8% in year 2015. The industry standards are above the

calculated ratio, so in simple words it is not able to transform sales in terms of profit. So

it can be interpreted that it should lay special emphasis on increasing sales.

Return on capital employed: The amount of profit is indicated by capital which is

employed for purpose of generating returns. The organization was able to gain return

which was above industry standard in year 2015 to 27.9 but due to issues in operation it

had decreased up to 22% . So on this context, organization must be able to improve

operations in very systematic aspect which will direct impact financial of the organization

(Hayes, 2015).

Asset Turnover ratio: It is replicated as ratio of efficiency which is tracing ability of

company for incurring sales through assets. From the above ratio analysis, Stratford

Yachts has efficiently applicable its assets in very systematic return as it is reflecting in

Net profit margin: It is reflecting net income which has been earned with sales which

has been gained. The organization has given net profit as 11% in year 2015 but due to

sales revenue it had decreased to 8% in year 2015. The industry standards are above the

calculated ratio, so in simple words it is not able to transform sales in terms of profit. So

it can be interpreted that it should lay special emphasis on increasing sales.

Return on capital employed: The amount of profit is indicated by capital which is

employed for purpose of generating returns. The organization was able to gain return

which was above industry standard in year 2015 to 27.9 but due to issues in operation it

had decreased up to 22% . So on this context, organization must be able to improve

operations in very systematic aspect which will direct impact financial of the organization

(Hayes, 2015).

Asset Turnover ratio: It is replicated as ratio of efficiency which is tracing ability of

company for incurring sales through assets. From the above ratio analysis, Stratford

Yachts has efficiently applicable its assets in very systematic return as it is reflecting in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this ratio, because it has attained industry standards and in next year it had increased its

level as over-attainment of meeting industry standards.

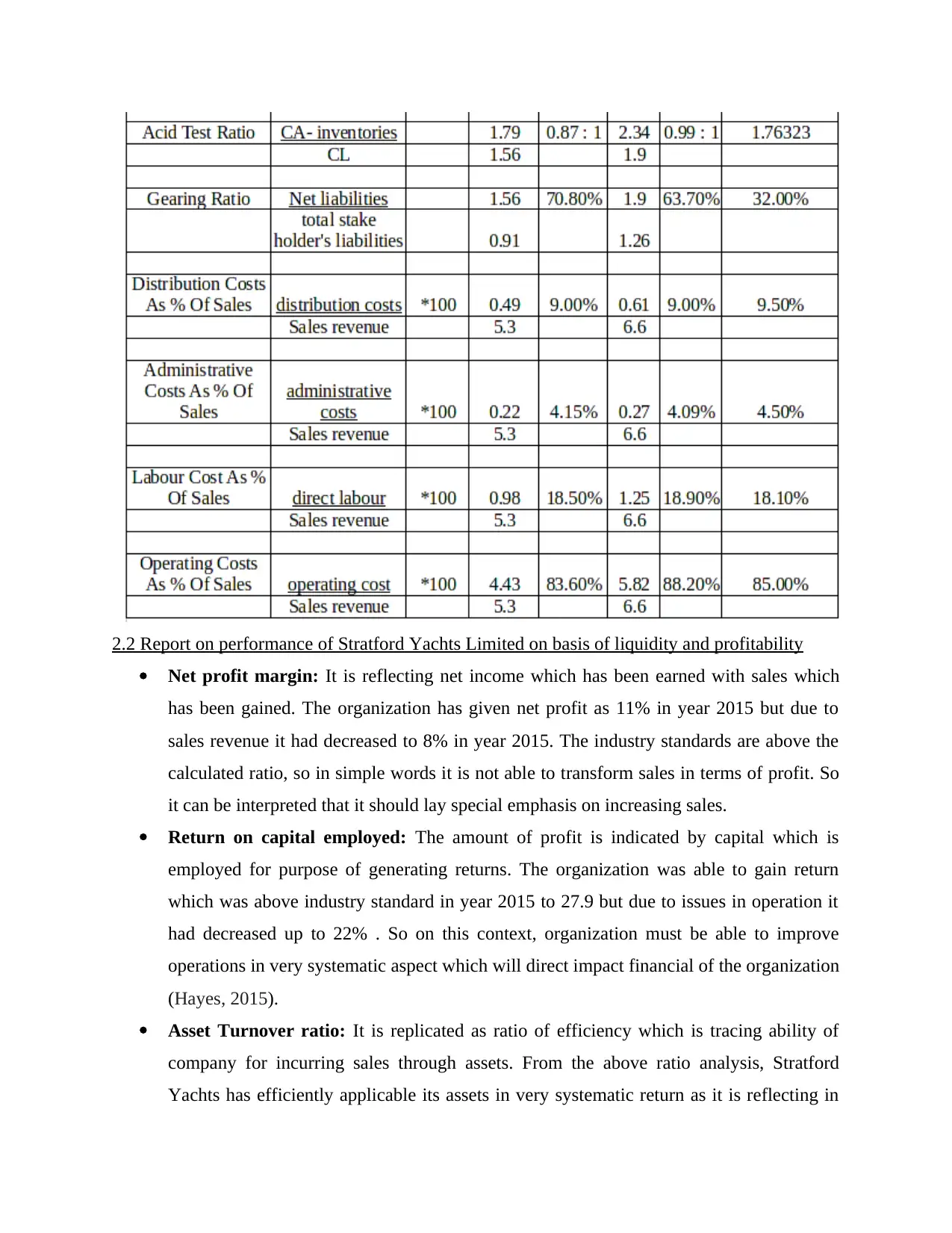

Accounts Receivable collection period: It is used for comparison of receivables which

are identified as outstanding for business to its sum of sales. From this perspective

organization has attained very good and strong position for getting accounts as it had

crossed industry standards which is 83 days so in this context, it should be able to

optimize this remaining money for generating resources and funds as blockage of money

will be avoided.

Current ratio: It is replicating organisation's liquidity position. The above mentioned

company is not able to match industry standard, but from above analysis it can be

interpreted that it is improving from previous year. As it is 1.5 which cannot be achieved

in less duration.

Quick ratio: It has direct relationship with current ratio as it reflects the assets which are

not converted in cash easily. The industry standard is not achievable neither is 2015 nor

in 2016.

Gearing ratio: It is major part of solvency ratio and in above organization, it is

exceeding standards of industry. It had created capability to repay its dividends in very

systematic aspect and large quantity as well.

Distribution costs as percentage of sales: It is replicated by dividing distribution cost to

total sales revenue. Sales will be not increased in above mentioned criteria. As in the year

2015 and 2016 it was stable but lower than industry standards which has very small

differences.

Administration cost as percentage of sales: The administration cost and revenue of

sales replicate performance. On the basis of mentioned ratio, it lacks ability to increase

sales and there is absence of increment in both year which has very less variation.

Labour cost as percentage of sales: It is representing sales on basis of variable cost. In

year 2016, standards have been met by organization as there is presence of small

difference in ratio. In the same series, for accomplishing organization's standard has to

raise direct labour with sales revenue and in this it had crossed specific industry standards

(Coggan and et. al., 2017).

level as over-attainment of meeting industry standards.

Accounts Receivable collection period: It is used for comparison of receivables which

are identified as outstanding for business to its sum of sales. From this perspective

organization has attained very good and strong position for getting accounts as it had

crossed industry standards which is 83 days so in this context, it should be able to

optimize this remaining money for generating resources and funds as blockage of money

will be avoided.

Current ratio: It is replicating organisation's liquidity position. The above mentioned

company is not able to match industry standard, but from above analysis it can be

interpreted that it is improving from previous year. As it is 1.5 which cannot be achieved

in less duration.

Quick ratio: It has direct relationship with current ratio as it reflects the assets which are

not converted in cash easily. The industry standard is not achievable neither is 2015 nor

in 2016.

Gearing ratio: It is major part of solvency ratio and in above organization, it is

exceeding standards of industry. It had created capability to repay its dividends in very

systematic aspect and large quantity as well.

Distribution costs as percentage of sales: It is replicated by dividing distribution cost to

total sales revenue. Sales will be not increased in above mentioned criteria. As in the year

2015 and 2016 it was stable but lower than industry standards which has very small

differences.

Administration cost as percentage of sales: The administration cost and revenue of

sales replicate performance. On the basis of mentioned ratio, it lacks ability to increase

sales and there is absence of increment in both year which has very less variation.

Labour cost as percentage of sales: It is representing sales on basis of variable cost. In

year 2016, standards have been met by organization as there is presence of small

difference in ratio. In the same series, for accomplishing organization's standard has to

raise direct labour with sales revenue and in this it had crossed specific industry standards

(Coggan and et. al., 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating cost as percentage of sales: Sales has been generated from operation's cost

which is specified in this stated ratio. In the year 2016, industry standards have been

exceeded along with increasing cost of production and sales revenue which had been

raised from previous year's comparison.

Stratford Yachts Limited financial performance had been evaluated in terms of

profitability in very stable manner and by measuring liquidity, it is not capable to gain good

position in industry. The organization had not yet met debt position or in simple words it can be

stated that debts of short term are not covered with so much ease as it is justified in liquidity

ratio.

CONCLUSION

From the above study it can be stated that managing financial resources are very

important aspect for any organization and especially for Stratford Yachts Limited. It helps in

keeping information in very systematic manner. It has been articulated from above report that

financial position has been reflected via statements of company. It has shown that by giving

information to various stakeholders which has their own way to observe requirement. Further it

can be summed up by this report that it had replicated organisation's profitability and liquidity is

working well in which there is lack of maintaining liquidity in easy aspect.

which is specified in this stated ratio. In the year 2016, industry standards have been

exceeded along with increasing cost of production and sales revenue which had been

raised from previous year's comparison.

Stratford Yachts Limited financial performance had been evaluated in terms of

profitability in very stable manner and by measuring liquidity, it is not capable to gain good

position in industry. The organization had not yet met debt position or in simple words it can be

stated that debts of short term are not covered with so much ease as it is justified in liquidity

ratio.

CONCLUSION

From the above study it can be stated that managing financial resources are very

important aspect for any organization and especially for Stratford Yachts Limited. It helps in

keeping information in very systematic manner. It has been articulated from above report that

financial position has been reflected via statements of company. It has shown that by giving

information to various stakeholders which has their own way to observe requirement. Further it

can be summed up by this report that it had replicated organisation's profitability and liquidity is

working well in which there is lack of maintaining liquidity in easy aspect.

REFERENCES

Books and Journals

Cascino, S. and et. al., 2014. Who uses financial reports and for what purpose? Evidence from

capital providers. Accounting in Europe. 11(2). pp.185-209.

Coggan, A. and et. al., 2017. Does asset specificity influence transaction costs and adoption? An

analysis of sugarcane farmers in the Great Barrier Reef catchments. Journal of

Environmental Economics and Policy. 6(1). pp.36-50.

Edmund, S. and Lyamtane, R. D. E., 2018. Effectiveness of the Heads of Schools in Managing

Financial Resources in Public Secondary Schools in Moshi Municipality. International

Journal of Scientific Research and Management. 6(05).

Hayes, P., 2015. Managing financial resources. Good Practice. (11). p.21.

Minnis, M. and Sutherland, A., 2017. Financial statements as monitoring mechanisms: Evidence

from small commercial loans. Journal of Accounting Research. 55(1). pp.197-233.

ONLINE

Financial Accounting vs Management Accounting. 2018. [Online]. Available through

:<https://www.wallstreetmojo.com/financial-accounting-vs-management-accounting/>.

Books and Journals

Cascino, S. and et. al., 2014. Who uses financial reports and for what purpose? Evidence from

capital providers. Accounting in Europe. 11(2). pp.185-209.

Coggan, A. and et. al., 2017. Does asset specificity influence transaction costs and adoption? An

analysis of sugarcane farmers in the Great Barrier Reef catchments. Journal of

Environmental Economics and Policy. 6(1). pp.36-50.

Edmund, S. and Lyamtane, R. D. E., 2018. Effectiveness of the Heads of Schools in Managing

Financial Resources in Public Secondary Schools in Moshi Municipality. International

Journal of Scientific Research and Management. 6(05).

Hayes, P., 2015. Managing financial resources. Good Practice. (11). p.21.

Minnis, M. and Sutherland, A., 2017. Financial statements as monitoring mechanisms: Evidence

from small commercial loans. Journal of Accounting Research. 55(1). pp.197-233.

ONLINE

Financial Accounting vs Management Accounting. 2018. [Online]. Available through

:<https://www.wallstreetmojo.com/financial-accounting-vs-management-accounting/>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.