Stryker Corporation: A Financial Analysis of PCB In-sourcing Project

VerifiedAdded on 2020/04/13

|6

|984

|41

Project

AI Summary

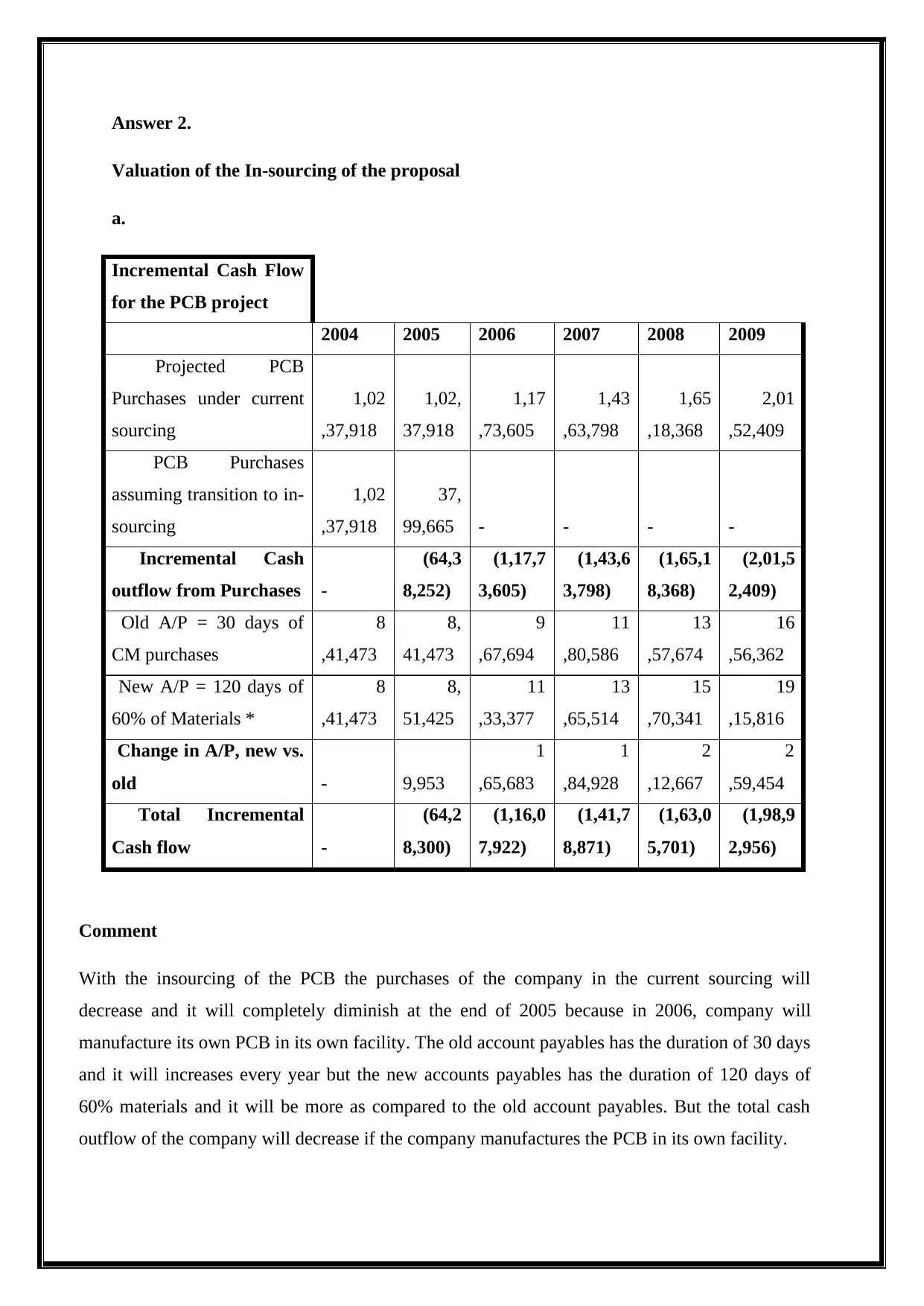

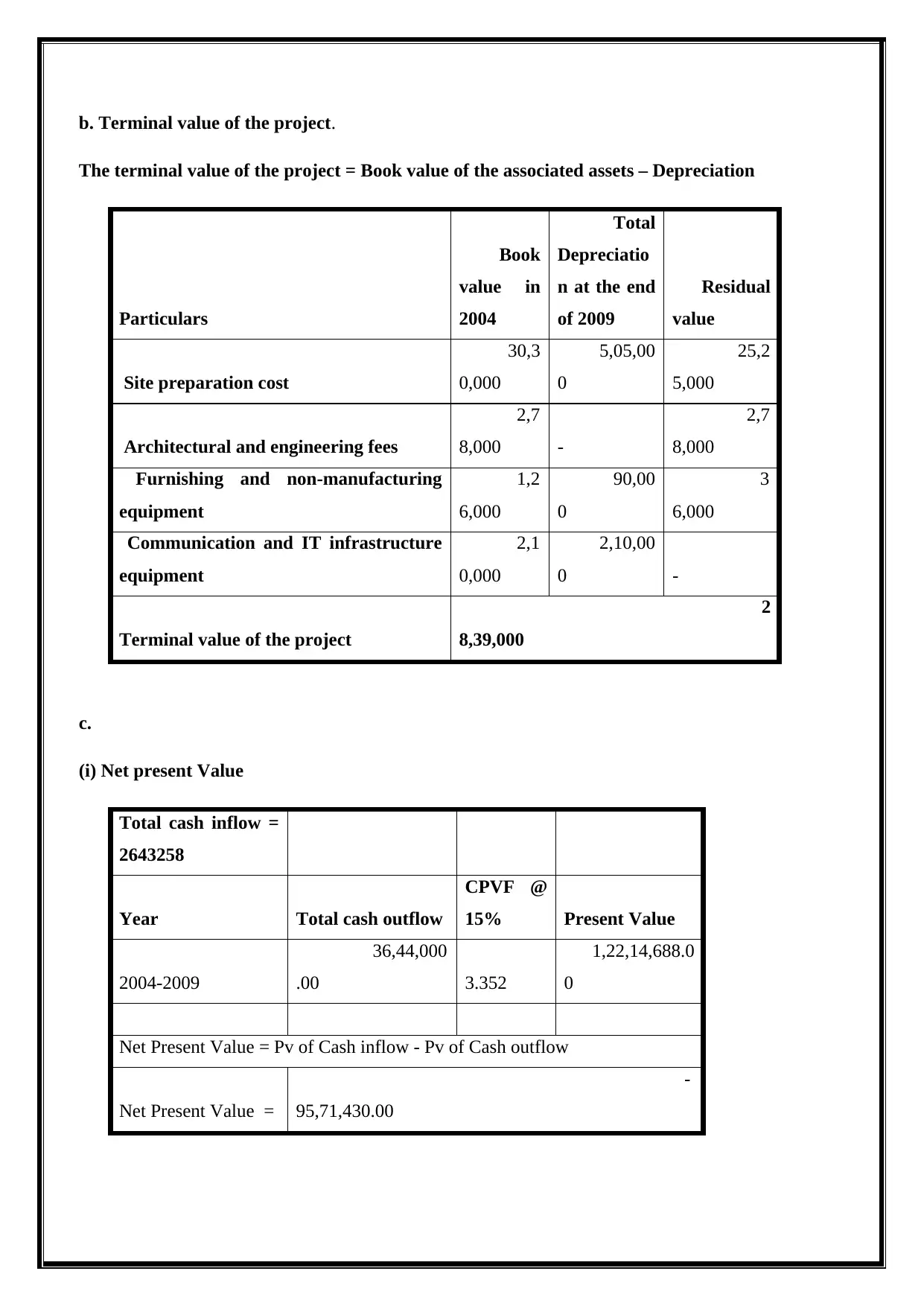

This corporate finance project analyzes Stryker Corporation's decision to in-source the production of printed circuit boards (PCBs). The project evaluates three options: maintaining the status quo with modifications, establishing a relationship with a single supplier, and insourcing PCB production. The analysis focuses on the third option, which involves significant capital investment. The project includes an executive summary, financial appraisal techniques such as Net Present Value (NPV), Payback Period, and Internal Rate of Return (IRR), and sensitivity analysis. The project also examines incremental cash flows, the terminal value of the project, and the payback period, concluding with a negative NPV, indicating the project's financial viability. The report also considers the strategic implications, risk factors, and the decision-making process involved in capital budgeting for the PCB project, including a review process at different stages.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.