Hewlett-Packard: Superannuation Defined Benefit Plan Analysis Report

VerifiedAdded on 2022/11/24

|10

|2604

|500

Report

AI Summary

This report provides a detailed analysis of defined benefit plans, focusing on the superannuation contributions of tertiary sector employees. It explores the differences between defined benefit plans and investment choice plans, outlining the factors that influence employee decisions, such as financial stability, age, employee mobility, historical performance, and information availability. The report delves into the issues of time value of money and tax deductions, explaining their impact on investment choices. It examines the benefits of superannuation contributions, including future financial security. The analysis considers factors like employee demographics, gender, and the sense of security, and concludes by emphasizing the importance of selecting investment options that align with individual financial goals and risk tolerance. The report references the Australian context and the investment landscape.

Defined benefit plan

Module Number-

[DATE]

Hewlett-Packard

[Company address]

Module Number-

[DATE]

Hewlett-Packard

[Company address]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction...........................................................................................................................................1

Description of the different plans..........................................................................................................1

Investment choice plan......................................................................................................................2

Defined benefit plan..........................................................................................................................2

Factors of tertiary sector employees to decide the superannuation contribution in defined benefit plan

and other choice investment plan...........................................................................................................3

Issues of time value of money, tax deduction and other factors.............................................................5

Conclusion.............................................................................................................................................6

References.............................................................................................................................................7

Introduction...........................................................................................................................................1

Description of the different plans..........................................................................................................1

Investment choice plan......................................................................................................................2

Defined benefit plan..........................................................................................................................2

Factors of tertiary sector employees to decide the superannuation contribution in defined benefit plan

and other choice investment plan...........................................................................................................3

Issues of time value of money, tax deduction and other factors.............................................................5

Conclusion.............................................................................................................................................6

References.............................................................................................................................................7

Introduction

There are several various investment options used by tertiary sector employees to

create value on their investment. It is considered that due to the increasing tertiary sector of

the economy, the people are enabling to satisfy their service requirements. The difference

between the service requirement and its fulfillment is decreased to the sphere which can be

ignored. There was a problem in the tertiary economy about the demand by the consumer for

the services of high quality, which has been passed out now and now it is not a tension

anymore for the tertiary economy. To fulfill the requirements of customers, such economy

sector provides every possible service. In the current economic conditions, the development

of any economy can be measured when the focus of economy shifts to the tertiary sector from

the primary or secondary sector. The service list of the tertiary sector includes various

services and businesses such as Restaurants, transportation, salon services, schools, financial

institution, and others. The employees employed under such economic sector are called

tertiary sector employees. In addition to the basic salary, these employees get several other

benefits which can be in cash or in other kinds.

Superannuation contribution

The Superannuation contribution is one of the benefits provided to these employees.

This benefit is not paid to the employees in their service tenure but at a future date to provide

them security in the future. This is quite similar to the pension fund. For such benefit, both

employer and employee contribute a proportion of amount towards such a fund. The creation

of such a fund gives a spirit of future financial security to the employee. The creation of

funds has a variety of contribution which depends from country to country. In Australia, The

superannuation fund offers the employees two major option for contribution i.e. defined

benefit plan and other investment choices.

Description of the different plans

The tertiary employees have several options for investment to increase the overall return on

capital invested (Wall, 2015).

There are several various investment options used by tertiary sector employees to

create value on their investment. It is considered that due to the increasing tertiary sector of

the economy, the people are enabling to satisfy their service requirements. The difference

between the service requirement and its fulfillment is decreased to the sphere which can be

ignored. There was a problem in the tertiary economy about the demand by the consumer for

the services of high quality, which has been passed out now and now it is not a tension

anymore for the tertiary economy. To fulfill the requirements of customers, such economy

sector provides every possible service. In the current economic conditions, the development

of any economy can be measured when the focus of economy shifts to the tertiary sector from

the primary or secondary sector. The service list of the tertiary sector includes various

services and businesses such as Restaurants, transportation, salon services, schools, financial

institution, and others. The employees employed under such economic sector are called

tertiary sector employees. In addition to the basic salary, these employees get several other

benefits which can be in cash or in other kinds.

Superannuation contribution

The Superannuation contribution is one of the benefits provided to these employees.

This benefit is not paid to the employees in their service tenure but at a future date to provide

them security in the future. This is quite similar to the pension fund. For such benefit, both

employer and employee contribute a proportion of amount towards such a fund. The creation

of such a fund gives a spirit of future financial security to the employee. The creation of

funds has a variety of contribution which depends from country to country. In Australia, The

superannuation fund offers the employees two major option for contribution i.e. defined

benefit plan and other investment choices.

Description of the different plans

The tertiary employees have several options for investment to increase the overall return on

capital invested (Wall, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Investment choice plan

As the name says the investment choice plan provides the employees a chance to invest their

amount in an investment portfolio. In this type of fund, the contribution made by the

employer is fixed to a certain proportion of the salary of the employee. Such investment

option provides the interest benefit to the employee n his invested amount. Different

investment options have several portfolios comprising shares, property or both. As per

research, almost 80% Australian population opt to invest in the ‘Growth' or ‘Balanced'

investment options wherein around 80% share of investment performs in the growth of assets

i.e. share and property (Hall, Foxon, and Bolton, 2016).

Defined benefit plan

This plan is termed defined and the employer and employee have the knowledge about the

proportion attributable to the employee's fund. This is an employer's sponsored plan i.e. all

the risk and decisions under such plan shall be maintained by the employer only. The task of

investment management shall also be done by the employer. There is a certain rate of

contribution shall be defined in which proportion the employer shall make the contribution. If

there is a lower rate than the desired then it has to be met by the employer. The payment of

such fund shall be made to the employee in several forms such as in a lump sum amount or a

pension or a combination of both. The calculation of such benefit shall be computed by

considering several factors on the part of the employee such as the age of the employee, his

pay role, years of service provided by employee and salary at the time of retirement

(Stefanescu., Wang, Xie, and Yang, 2018).

As the name says the investment choice plan provides the employees a chance to invest their

amount in an investment portfolio. In this type of fund, the contribution made by the

employer is fixed to a certain proportion of the salary of the employee. Such investment

option provides the interest benefit to the employee n his invested amount. Different

investment options have several portfolios comprising shares, property or both. As per

research, almost 80% Australian population opt to invest in the ‘Growth' or ‘Balanced'

investment options wherein around 80% share of investment performs in the growth of assets

i.e. share and property (Hall, Foxon, and Bolton, 2016).

Defined benefit plan

This plan is termed defined and the employer and employee have the knowledge about the

proportion attributable to the employee's fund. This is an employer's sponsored plan i.e. all

the risk and decisions under such plan shall be maintained by the employer only. The task of

investment management shall also be done by the employer. There is a certain rate of

contribution shall be defined in which proportion the employer shall make the contribution. If

there is a lower rate than the desired then it has to be met by the employer. The payment of

such fund shall be made to the employee in several forms such as in a lump sum amount or a

pension or a combination of both. The calculation of such benefit shall be computed by

considering several factors on the part of the employee such as the age of the employee, his

pay role, years of service provided by employee and salary at the time of retirement

(Stefanescu., Wang, Xie, and Yang, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

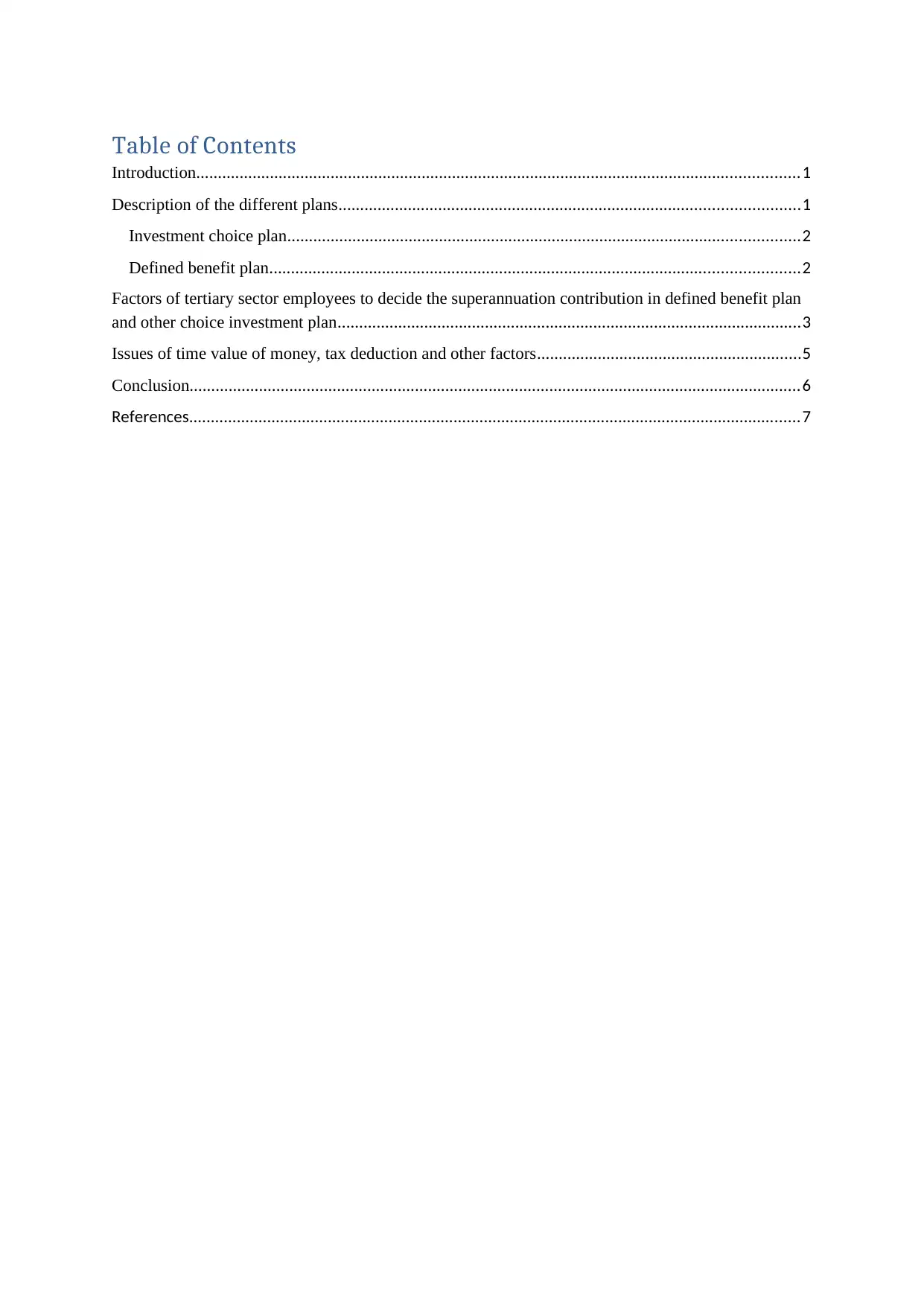

(Defined benefit plan, 2019)

Factors of tertiary sector employees to decide the superannuation contribution in

defined benefit plan and other choice investment plan

It is not an easy decision for tertiary sector employees to select the appropriate investment

plan between both plans to invest their superannuation fund. While making such decision

various factors are considered by the employee due to the high-level uncertainty of the

financial results of both plans. The advantage and disadvantages attached to the plans are also

considered during the decision making. However, the factors can be changed with the

changing economic condition. The factors which are considered are mentioned below

(Collado, 2018).

Financial stability: The factor which influences the decision of investment making at large

level is the financial stability of the employee. The employee who is making the investment

of his superannuation fund should be financially stable. The employees having strong

financial status are less interested in bearing risk and they generally go for the investment

choice plan. It is analysed that employees with limited financial stability are more interested

in the defined benefit plans due to the lower risk factor. For making the fair decision of

investment of superannuation fund there is a need to assess the financial stability of an

employee to obtain the better returns.

Age of employee: The employees at their younger age are more interested in investing their

funds in investment choice plan because there is a large period between their investment and

Factors of tertiary sector employees to decide the superannuation contribution in

defined benefit plan and other choice investment plan

It is not an easy decision for tertiary sector employees to select the appropriate investment

plan between both plans to invest their superannuation fund. While making such decision

various factors are considered by the employee due to the high-level uncertainty of the

financial results of both plans. The advantage and disadvantages attached to the plans are also

considered during the decision making. However, the factors can be changed with the

changing economic condition. The factors which are considered are mentioned below

(Collado, 2018).

Financial stability: The factor which influences the decision of investment making at large

level is the financial stability of the employee. The employee who is making the investment

of his superannuation fund should be financially stable. The employees having strong

financial status are less interested in bearing risk and they generally go for the investment

choice plan. It is analysed that employees with limited financial stability are more interested

in the defined benefit plans due to the lower risk factor. For making the fair decision of

investment of superannuation fund there is a need to assess the financial stability of an

employee to obtain the better returns.

Age of employee: The employees at their younger age are more interested in investing their

funds in investment choice plan because there is a large period between their investment and

retirement. The large period of investment enables them to effectively utilize the movements

to obtain more benefits. Also, they can change their portfolio as per the changes in the market

to gain high benefits. Similarly, the employees of older age are less expected to invest their

funds in investment choice plan due to the short time period and large risk factor. These

employees totally depend on their retirement benefits for their survival in the future (Bae et

al. 2018).

Employee mobility: The employees who are used to switch their jobs in a very short time of

period also seem to be interested in the investment choice plan. The plan provides them the

option to keep together all the accumulated benefits from several employers. Also, the

employee can invest his amount as per his own will so the employees are preferred to choose

the investment choice plan as the option of defined benefit plan will result into the opening of

different defined benefit plans for every different employer under which the employee has

served. This results in the segregation of the overall benefits of the employees.

Historical performance of the plans: While deciding about the option for investment the past

performance of both the plans is compared. The performance can be compared for the last

one year, six months or for quarterly. Also, the performance graph depends on the analysis in

which plan a large number of employees has invested. The historical performance depicts the

changes in return on the basis of capital invested by the investors (Yen, et al. 2016).

Level of information available with the employees: The investment decision of employees

get affected by the knowledge they have about the current and past market performances of

the investment options and market conditions. The employees have a strong knowledge

regarding the market performances of each plan can wisely choose their investment option.

The employees with excessive knowledge are opting for the investment choice plan as such

information can be utilized to gain higher interest incomes. The less aware employees go for

the defined benefit plan (Lee, et al. 2017).

Gender: The gender of employee has a significant role in the decision making regarding

selection investment option. It is observed that men are less risk-averse than women. Men are

likely to go for a more risky plan to gain higher returns on their investments.

Sense of being secure: The sense of insecurity in the mind of employees also affects the

decision of investment. The employees who do not want to take more risk and have will to

invest in a secure investment plan generally opt the defined benefit plan due to the less

attached risk. On the other hand, the investment choice plan is more dependent on the market

movements and the security is uncertain in such a plan (Josa-Fombellida, López-Casado, and

Rincón-Zapatero, 2018).

to obtain more benefits. Also, they can change their portfolio as per the changes in the market

to gain high benefits. Similarly, the employees of older age are less expected to invest their

funds in investment choice plan due to the short time period and large risk factor. These

employees totally depend on their retirement benefits for their survival in the future (Bae et

al. 2018).

Employee mobility: The employees who are used to switch their jobs in a very short time of

period also seem to be interested in the investment choice plan. The plan provides them the

option to keep together all the accumulated benefits from several employers. Also, the

employee can invest his amount as per his own will so the employees are preferred to choose

the investment choice plan as the option of defined benefit plan will result into the opening of

different defined benefit plans for every different employer under which the employee has

served. This results in the segregation of the overall benefits of the employees.

Historical performance of the plans: While deciding about the option for investment the past

performance of both the plans is compared. The performance can be compared for the last

one year, six months or for quarterly. Also, the performance graph depends on the analysis in

which plan a large number of employees has invested. The historical performance depicts the

changes in return on the basis of capital invested by the investors (Yen, et al. 2016).

Level of information available with the employees: The investment decision of employees

get affected by the knowledge they have about the current and past market performances of

the investment options and market conditions. The employees have a strong knowledge

regarding the market performances of each plan can wisely choose their investment option.

The employees with excessive knowledge are opting for the investment choice plan as such

information can be utilized to gain higher interest incomes. The less aware employees go for

the defined benefit plan (Lee, et al. 2017).

Gender: The gender of employee has a significant role in the decision making regarding

selection investment option. It is observed that men are less risk-averse than women. Men are

likely to go for a more risky plan to gain higher returns on their investments.

Sense of being secure: The sense of insecurity in the mind of employees also affects the

decision of investment. The employees who do not want to take more risk and have will to

invest in a secure investment plan generally opt the defined benefit plan due to the less

attached risk. On the other hand, the investment choice plan is more dependent on the market

movements and the security is uncertain in such a plan (Josa-Fombellida, López-Casado, and

Rincón-Zapatero, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Apart from all these above discussed factors, the personal interest of employee is a major

determinant in the selection of investment plan.

Issues of time value of money, tax deduction and other factors

The choice of investment of an employee for investing his superannuation fund also gets

affected by the time value of money as well as the concerned taxes in the economy. The

impact of these factors is discussed as follows (Lin., MacMinn, and Tian, 2015).

Taxes: Taxation is imposing on the person to pay a certain amount to the government out of

his income. The income also includes the retirement benefit availed by the employee. There

are certain conditions where the person availing the retirement benefits is not needed to be

paid the tax on it. These conditions include incapacity or death of the employee. Apart from

these situations, all the employees are bound to pay taxes on these benefits. In defined benefit

plan the employee is liable to pay the tax on the amount of employer's contribution

accumulated during the working period of the employee. There is no additional tax would

apply in this case. It is analysed that the investment made in the portfolio of investment

which also added up with the interest fund. Hence the tax is imposed on both contribution

amount and interest income from the investment. Due to such reason, many employees

choose the investment option of defined benefit plan (Krishnan, Cumbie, and Ice, 2017).

Time value of money: The concept of the time value of money enhances the worth of idle

money in the future. The concept is based on the theory that the value of one rupee would be

more than the value it will have in the future due to the inflation which will diminish its value

in the future. Hence, from the point of view of the time value of money concept the

investment choice plan will be the better one as the investment made by the employee in

present will come out in future as increased amount with the interest income. While in the

other investment plan of defined benefit, the accumulated amount of superannuation fund

shall remain the same and adds nothing (Cobb, 2015).

Conclusion

After the entire discussion about the employment benefits under the tertiary sector of

the economy, we can state that to motivate the employees to attract them towards such sector

of the economy it is required to provide them some benefits added to their salary. These

benefits, in addition, encourage the employees to go in the tertiary sector of the economy

instead of the primary and secondary sectors of the economy. In the end, after analyzing all

determinant in the selection of investment plan.

Issues of time value of money, tax deduction and other factors

The choice of investment of an employee for investing his superannuation fund also gets

affected by the time value of money as well as the concerned taxes in the economy. The

impact of these factors is discussed as follows (Lin., MacMinn, and Tian, 2015).

Taxes: Taxation is imposing on the person to pay a certain amount to the government out of

his income. The income also includes the retirement benefit availed by the employee. There

are certain conditions where the person availing the retirement benefits is not needed to be

paid the tax on it. These conditions include incapacity or death of the employee. Apart from

these situations, all the employees are bound to pay taxes on these benefits. In defined benefit

plan the employee is liable to pay the tax on the amount of employer's contribution

accumulated during the working period of the employee. There is no additional tax would

apply in this case. It is analysed that the investment made in the portfolio of investment

which also added up with the interest fund. Hence the tax is imposed on both contribution

amount and interest income from the investment. Due to such reason, many employees

choose the investment option of defined benefit plan (Krishnan, Cumbie, and Ice, 2017).

Time value of money: The concept of the time value of money enhances the worth of idle

money in the future. The concept is based on the theory that the value of one rupee would be

more than the value it will have in the future due to the inflation which will diminish its value

in the future. Hence, from the point of view of the time value of money concept the

investment choice plan will be the better one as the investment made by the employee in

present will come out in future as increased amount with the interest income. While in the

other investment plan of defined benefit, the accumulated amount of superannuation fund

shall remain the same and adds nothing (Cobb, 2015).

Conclusion

After the entire discussion about the employment benefits under the tertiary sector of

the economy, we can state that to motivate the employees to attract them towards such sector

of the economy it is required to provide them some benefits added to their salary. These

benefits, in addition, encourage the employees to go in the tertiary sector of the economy

instead of the primary and secondary sectors of the economy. In the end, after analyzing all

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the investment plans and their relevant factors we can say that employees should go with the

investment option which provides them the higher returns and with the risk factor suitable to

them.

investment option which provides them the higher returns and with the risk factor suitable to

them.

References

Bae, S. U., Hur, H., Min, B. S., Baik, S. H., Lee, K. Y., and Kim, N. K. (2018). Which

Patients with Isolated Para-aortic Lymph Node Metastasis Will Truly Benefit from Extended

Lymph Node Dissection for Colon Cancer?. Cancer research and treatment: official journal

of Korean Cancer Association, 50(3), 712.

Cobb, J. A. (2015). Risky business: The decline of defined benefit pensions and firms’

shifting of risk. Organization Science, 26(5), 1332-1350.

Collado, M. (2018). Defined benefit plans in the big picture. Journal of Accountancy, 225(2),

60.

Defined benefit plan, (2019), Financing the civic energy sector, available at

https://www.uss.co.uk/how-uss-invests/the-fund/performance Accessed on 20th/05/2019

Hall, S., Foxon, T. J., and Bolton, R. (2016). Financing the civic energy sector: How financial

institutions affect ownership models in Germany and the United Kingdom. Energy Research

and Social Science, 12, 5-15.

Josa-Fombellida, R., López-Casado, P., and Rincón-Zapatero, J. P. (2018). Portfolio

optimization in a defined benefit pension plan where the risky assets are processes with

constant elasticity of variance. Insurance: Mathematics and Economics, 82, 73-86.

Krishnan, V. S., Cumbie, J., and Ice, R. (2017). Defined benefit plans vs. defined

contribution plans: An evaluation framework using random returns.

Lee, J., Chen, Y. J., Wu, M. H., Chang, C. L., Chen, T. C., Chen, J. R., and Yang, Y. C.

(2017). PO-0712: Benefit of semi-extended field radiotherapy in patients with locally

advanced cervical cancer. Radiotherapy and Oncology, 123, S373-S374.

Lin, Y., MacMinn, R. D., and Tian, R. (2015). De-risking defined benefit plans. Insurance:

Mathematics and Economics, 63, 52-65.

Stefanescu, I., Wang, Y., Xie, K., and Yang, J. (2018). Pay me now (and later): Pension

benefit manipulation before plan freezes and executive retirement. Journal of Financial

Economics, 127(1), 152-173.

Bae, S. U., Hur, H., Min, B. S., Baik, S. H., Lee, K. Y., and Kim, N. K. (2018). Which

Patients with Isolated Para-aortic Lymph Node Metastasis Will Truly Benefit from Extended

Lymph Node Dissection for Colon Cancer?. Cancer research and treatment: official journal

of Korean Cancer Association, 50(3), 712.

Cobb, J. A. (2015). Risky business: The decline of defined benefit pensions and firms’

shifting of risk. Organization Science, 26(5), 1332-1350.

Collado, M. (2018). Defined benefit plans in the big picture. Journal of Accountancy, 225(2),

60.

Defined benefit plan, (2019), Financing the civic energy sector, available at

https://www.uss.co.uk/how-uss-invests/the-fund/performance Accessed on 20th/05/2019

Hall, S., Foxon, T. J., and Bolton, R. (2016). Financing the civic energy sector: How financial

institutions affect ownership models in Germany and the United Kingdom. Energy Research

and Social Science, 12, 5-15.

Josa-Fombellida, R., López-Casado, P., and Rincón-Zapatero, J. P. (2018). Portfolio

optimization in a defined benefit pension plan where the risky assets are processes with

constant elasticity of variance. Insurance: Mathematics and Economics, 82, 73-86.

Krishnan, V. S., Cumbie, J., and Ice, R. (2017). Defined benefit plans vs. defined

contribution plans: An evaluation framework using random returns.

Lee, J., Chen, Y. J., Wu, M. H., Chang, C. L., Chen, T. C., Chen, J. R., and Yang, Y. C.

(2017). PO-0712: Benefit of semi-extended field radiotherapy in patients with locally

advanced cervical cancer. Radiotherapy and Oncology, 123, S373-S374.

Lin, Y., MacMinn, R. D., and Tian, R. (2015). De-risking defined benefit plans. Insurance:

Mathematics and Economics, 63, 52-65.

Stefanescu, I., Wang, Y., Xie, K., and Yang, J. (2018). Pay me now (and later): Pension

benefit manipulation before plan freezes and executive retirement. Journal of Financial

Economics, 127(1), 152-173.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Wall, S. (2015). Dimensions of Precariousness in an Emerging Sector of Self‐Employment:

A Study of Self‐Employed Nurses. Gender, Work and Organization, 22(3), 221-236.

Yen, T. C., Lai, C. H., Ma, S. Y., Huang, K. G., Huang, H. J., Hong, J. H., ... and Chang, T.

C. (2016). Comparative benefits and limitations of 18 F-FDG PET and CT-MRI in

documented or suspected recurrent cervical cancer. European journal of nuclear medicine

and molecular imaging, 33(12), 1399-1407.

A Study of Self‐Employed Nurses. Gender, Work and Organization, 22(3), 221-236.

Yen, T. C., Lai, C. H., Ma, S. Y., Huang, K. G., Huang, H. J., Hong, J. H., ... and Chang, T.

C. (2016). Comparative benefits and limitations of 18 F-FDG PET and CT-MRI in

documented or suspected recurrent cervical cancer. European journal of nuclear medicine

and molecular imaging, 33(12), 1399-1407.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.