University Accounting Report: Superannuation Fund Analysis

VerifiedAdded on 2023/06/03

|13

|3330

|218

Case Study

AI Summary

This case study presents an internal memorandum analyzing the teacher's annual superannuation fund, addressing the Director-General of the Department of Education. The report meticulously examines the fund's financial health, considering various scenarios and inputs like years of service, salary increases, retiree rates, mortality rates, and administration expenses. The analysis includes a discussion on different alternatives (A, B, R, and W), cost of living adjustments, long-term rates of return, productivity factors, employee contribution rates, and government contributions. The key results section focuses on the Net Present Value (NPV) of unfunded liability and the ratio of assets to liability NPV, providing a comprehensive assessment of the fund's stability and its ability to meet future obligations. The study utilizes Microsoft Excel to develop a decision support system, offering a best-practice approach to financial planning and risk management for the superannuation fund.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Authors Note:

Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Part C

Internal Memorandum

To

Ms. Anne Nolan

Director General

Department of Education

Date:

Subject: Report in respect of the teacher’s annual superannuation fund

Dear mam

Through the report a conscious effort is being made to ensure that the position of the

superannuation fund in respect of the resources available for it and the returns generated by it

is duly reflected. The primary objective of the fund is to provide financial freedom to the

esteemed teachers of the various public educational institutions operating within the country.

For the purpose of analysing the present situation of the superannuation fund an effort has

been made to ensure that different scenarios are being studied (Marshall & Steinbart, 2017).

The study of the various scenarios will enable us to understand the implications of the

changes in the inputs on the financial health of the superannuation fund.

The summary of the various inputs, constants and other factors determining the results

of the various models or scenarios being used for analysis are as follows:

Constants-

a) Years of service:

Part C

Internal Memorandum

To

Ms. Anne Nolan

Director General

Department of Education

Date:

Subject: Report in respect of the teacher’s annual superannuation fund

Dear mam

Through the report a conscious effort is being made to ensure that the position of the

superannuation fund in respect of the resources available for it and the returns generated by it

is duly reflected. The primary objective of the fund is to provide financial freedom to the

esteemed teachers of the various public educational institutions operating within the country.

For the purpose of analysing the present situation of the superannuation fund an effort has

been made to ensure that different scenarios are being studied (Marshall & Steinbart, 2017).

The study of the various scenarios will enable us to understand the implications of the

changes in the inputs on the financial health of the superannuation fund.

The summary of the various inputs, constants and other factors determining the results

of the various models or scenarios being used for analysis are as follows:

Constants-

a) Years of service:

2ACCOUNTING

This reflects the number of years that the teachers are expected to work for an

institution. This is necessary for the purpose of determination of the period for which

the teachers are entitled to receive the pension. This also helps in the determination of

the period for which the assets will remain invested in the market. The longer the

period of investment, the larger will be the returns generated by the stock market in

respect of it (Hassan et al., 2017). For the purpose of calculation it has been

ascertained that the average number of years of service to be rendered by the teachers

will be equal to 30 years.

b) Increase in the salaries of the teachers:

This input reflects the change in the basic salary of teachers in the various public

institutions across the country. This plays a key role in calculating the amount of

benefit that is going to accrue in respect of the teachers for the relevant period. The

reason for this is that with the change in the basic salary of the teachers the amount of

the remuneration of the teachers also increases. Along with it the total amount that is

contributed by the teachers towards investment in the stock market and the amount

that has to be contributed by the state in proportion to the teachers contribution also

changes (Teittinen & Granlund, 2017). For the purpose of conducting the analysis it

has been ascertained that the rate of increase in the salaries of the teachers will be

equal to 1% every year.

c) Retiree rate:

This input reflects the number of teachers that are going to retire in the upcoming

years. This input is necessary for the purpose of determination of the amount of cash

flow in respect of the payment of the superannuation fund by the government. The

input is very necessary because it gives the state an expected figure in respect of the

amount of cash outflow that is going to be executed on its part for the relevant period

This reflects the number of years that the teachers are expected to work for an

institution. This is necessary for the purpose of determination of the period for which

the teachers are entitled to receive the pension. This also helps in the determination of

the period for which the assets will remain invested in the market. The longer the

period of investment, the larger will be the returns generated by the stock market in

respect of it (Hassan et al., 2017). For the purpose of calculation it has been

ascertained that the average number of years of service to be rendered by the teachers

will be equal to 30 years.

b) Increase in the salaries of the teachers:

This input reflects the change in the basic salary of teachers in the various public

institutions across the country. This plays a key role in calculating the amount of

benefit that is going to accrue in respect of the teachers for the relevant period. The

reason for this is that with the change in the basic salary of the teachers the amount of

the remuneration of the teachers also increases. Along with it the total amount that is

contributed by the teachers towards investment in the stock market and the amount

that has to be contributed by the state in proportion to the teachers contribution also

changes (Teittinen & Granlund, 2017). For the purpose of conducting the analysis it

has been ascertained that the rate of increase in the salaries of the teachers will be

equal to 1% every year.

c) Retiree rate:

This input reflects the number of teachers that are going to retire in the upcoming

years. This input is necessary for the purpose of determination of the amount of cash

flow in respect of the payment of the superannuation fund by the government. The

input is very necessary because it gives the state an expected figure in respect of the

amount of cash outflow that is going to be executed on its part for the relevant period

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

of time. For the purpose of calculation it has been ascertained that the retiree rate will

be equal to 4% each year.

d) Mortality rate:

This input is concerned with the number of teachers who are expected to pass away

each year. It is very important that this input is being included in the calculation

because the teachers who will be dead will be collecting their dues in respect of the

superannuation immediately. This can lead to massive pressure on the state in terms

of the cash outflow in the relevant period of time. The other effect of the same will be

that the returns that are being generated in respect of the investment made in the stock

exchange will reduce significantly (Apostolou et al., 2014). The reason for this is that

the period for which the investment was being invested gets reduced. For the purpose

of calculation it has be ascertained that the mortality rate will be fixed at 5%. It has

also been observed that due to the mortality rate prevailing in the recent times, the

period after which the investment in the superannuation is taken out by the teachers

stands out at average of around 20 years.

e) Final year salary:

This input suggests the amount of salary that is payable to the teachers in the last year

of their service to the institution. This is important for the calculation because of the

fact that higher the salary, higher will be the amount invested in the stock exchange

and higher will be the amount payable to the teachers in respect of their investment in

superannuation fund. Due consideration has to be given also to the fact that the final

salary payable to the teachers in their last year of service will increase over the period

of time. For the purpose of calculation it has been ascertained that the average last

year salary of the teachers stood at $96975.

f) Administration expense:

of time. For the purpose of calculation it has been ascertained that the retiree rate will

be equal to 4% each year.

d) Mortality rate:

This input is concerned with the number of teachers who are expected to pass away

each year. It is very important that this input is being included in the calculation

because the teachers who will be dead will be collecting their dues in respect of the

superannuation immediately. This can lead to massive pressure on the state in terms

of the cash outflow in the relevant period of time. The other effect of the same will be

that the returns that are being generated in respect of the investment made in the stock

exchange will reduce significantly (Apostolou et al., 2014). The reason for this is that

the period for which the investment was being invested gets reduced. For the purpose

of calculation it has be ascertained that the mortality rate will be fixed at 5%. It has

also been observed that due to the mortality rate prevailing in the recent times, the

period after which the investment in the superannuation is taken out by the teachers

stands out at average of around 20 years.

e) Final year salary:

This input suggests the amount of salary that is payable to the teachers in the last year

of their service to the institution. This is important for the calculation because of the

fact that higher the salary, higher will be the amount invested in the stock exchange

and higher will be the amount payable to the teachers in respect of their investment in

superannuation fund. Due consideration has to be given also to the fact that the final

salary payable to the teachers in their last year of service will increase over the period

of time. For the purpose of calculation it has been ascertained that the average last

year salary of the teachers stood at $96975.

f) Administration expense:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

This input reflects the amount that is being spent by the state in respect of the

administering the funds collected by the teachers and the amount contributed by the

state in respect of the superannuation funds. The input is important due to the fact that

the administration expense have a direct bearing on the returns that is being generated

by the superannuation funds and its effective and efficient management over the

period of time. Due consideration and effort has to be made by the state in order to

ascertain that the administration expense in respect of management of the funds is

reduced over the period of time (Trigo et al., 2014). The reduction in the

administration expense is necessary to ensure that the majority of the cash outflow is

done by the state to increase the returns of the investment of the teachers and not on

functions that have very less overall value in terms of retirement benefits of the

teachers.

g) Pay-out rate factor:

This input gives an indication to the state in respect of the amount that is being given

out from the total funds to the teachers for the relevant period of time. it is important

to ensure that actual outflow of cash takes place in the relevant period of time in

respect of prompt payment to the teachers in exchange of their investment and the

contribution made by the state.

h) Discounting rate:

This input dictates the present value of the investment that has been contributed by the

state and the teachers in respect of the superannuation fund. The discounting rate is of

crucial importance the reason for this is that depending upon the discounting rate the

present value of the investment over the period of time is determined.

Inputs-

This input reflects the amount that is being spent by the state in respect of the

administering the funds collected by the teachers and the amount contributed by the

state in respect of the superannuation funds. The input is important due to the fact that

the administration expense have a direct bearing on the returns that is being generated

by the superannuation funds and its effective and efficient management over the

period of time. Due consideration and effort has to be made by the state in order to

ascertain that the administration expense in respect of management of the funds is

reduced over the period of time (Trigo et al., 2014). The reduction in the

administration expense is necessary to ensure that the majority of the cash outflow is

done by the state to increase the returns of the investment of the teachers and not on

functions that have very less overall value in terms of retirement benefits of the

teachers.

g) Pay-out rate factor:

This input gives an indication to the state in respect of the amount that is being given

out from the total funds to the teachers for the relevant period of time. it is important

to ensure that actual outflow of cash takes place in the relevant period of time in

respect of prompt payment to the teachers in exchange of their investment and the

contribution made by the state.

h) Discounting rate:

This input dictates the present value of the investment that has been contributed by the

state and the teachers in respect of the superannuation fund. The discounting rate is of

crucial importance the reason for this is that depending upon the discounting rate the

present value of the investment over the period of time is determined.

Inputs-

5ACCOUNTING

For the purpose of calculation of the various alternatives and the corresponding effect of

the same in respect of the teacher’s superannuation funds have been properly described by

Director General.

a) Applicable case:

For the purpose of discussing the various alternatives an effort has been made to

include several scenarios. It has been ascertained that due study will be done of four

alternative situation, they are A, B, R and W.

b) Cost of living adjustment:

This input is necessary for the purpose of including the increasing cost of living in the

calculation of the returns that is being generated by the superannuation funds in

respect of the teachers. The input is of significant importance due to the fact that it is

virtually impossible to determine the real returns generated in respect of the teachers

without taking into consideration the rise in the prices of the commodities over the

period of time (Kurniawan et al., 2017). To ensure that the returns generated by the

investment is in corresponding to the prevailing economic condition, suitable

adjustment has to be made in the contribution done by the state. For the purpose of

calculating the amount in respect of the investment the rate of the increase in the cost

of living has been fixed at 3% annually.

c) Long term rate of return:

It is the input that gives the percentage of the return that will be generated in respect

of the teachers over the period of the investment that has been made by the teachers

and the state. This input is of crucial importance due to the fact that depending upon

the rate of return the amount of the investment to be received by the teachers will be

determined. For the purpose of calculation it has been ascertained that 7.5% will be

rate of returns generated by the investment.

For the purpose of calculation of the various alternatives and the corresponding effect of

the same in respect of the teacher’s superannuation funds have been properly described by

Director General.

a) Applicable case:

For the purpose of discussing the various alternatives an effort has been made to

include several scenarios. It has been ascertained that due study will be done of four

alternative situation, they are A, B, R and W.

b) Cost of living adjustment:

This input is necessary for the purpose of including the increasing cost of living in the

calculation of the returns that is being generated by the superannuation funds in

respect of the teachers. The input is of significant importance due to the fact that it is

virtually impossible to determine the real returns generated in respect of the teachers

without taking into consideration the rise in the prices of the commodities over the

period of time (Kurniawan et al., 2017). To ensure that the returns generated by the

investment is in corresponding to the prevailing economic condition, suitable

adjustment has to be made in the contribution done by the state. For the purpose of

calculating the amount in respect of the investment the rate of the increase in the cost

of living has been fixed at 3% annually.

c) Long term rate of return:

It is the input that gives the percentage of the return that will be generated in respect

of the teachers over the period of the investment that has been made by the teachers

and the state. This input is of crucial importance due to the fact that depending upon

the rate of return the amount of the investment to be received by the teachers will be

determined. For the purpose of calculation it has been ascertained that 7.5% will be

rate of returns generated by the investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING

d) Productivity factor:

It is the input that reflects the number of the teachers that leave the employment of the

institution over the period of the investment that has been made in respect of the

superannuation fund. This input is crucial because depending on this input the cash

flow of the state is significantly influenced. The teachers who leave the employment

immediately cash in the benefits of the superannuation funds. For the purpose of

calculation it has been ascertained that the rate of attrition will be fixed at 0.5%.

e) Employee contribution rate:

This input reflects the rate at which the teachers are expected to contribute towards

the superannuation fund. This input is of utmost importance because of the fact that

depending upon this rate the amount to be contributed to the superannuation fund is

determined. For the purpose of calculation it has been ascertained that 9.5% will be

taken as the rate at which the contribution has to be made by the teachers.

f) Final year salary take back:

This input reflects the implementation of a relatively new scheme under which the

Department of Education has started to cut down the final year payment of the

teachers. This scheme is necessary due to the fact that depending on the last year

salary the contribution made by the teachers and the state is influenced significantly.

Hence, the scheme was introduced to ensure that the last year salary of the employees

is being reduced a little bit (Peters et al., 2016).

g) Government contribution factor:

This input reflects the amount of contribution that has to be made on part of the

government to the funds. The contribution of the government is directly related to the

contribution made by the teachers or in other words the amount to be contributed by

d) Productivity factor:

It is the input that reflects the number of the teachers that leave the employment of the

institution over the period of the investment that has been made in respect of the

superannuation fund. This input is crucial because depending on this input the cash

flow of the state is significantly influenced. The teachers who leave the employment

immediately cash in the benefits of the superannuation funds. For the purpose of

calculation it has been ascertained that the rate of attrition will be fixed at 0.5%.

e) Employee contribution rate:

This input reflects the rate at which the teachers are expected to contribute towards

the superannuation fund. This input is of utmost importance because of the fact that

depending upon this rate the amount to be contributed to the superannuation fund is

determined. For the purpose of calculation it has been ascertained that 9.5% will be

taken as the rate at which the contribution has to be made by the teachers.

f) Final year salary take back:

This input reflects the implementation of a relatively new scheme under which the

Department of Education has started to cut down the final year payment of the

teachers. This scheme is necessary due to the fact that depending on the last year

salary the contribution made by the teachers and the state is influenced significantly.

Hence, the scheme was introduced to ensure that the last year salary of the employees

is being reduced a little bit (Peters et al., 2016).

g) Government contribution factor:

This input reflects the amount of contribution that has to be made on part of the

government to the funds. The contribution of the government is directly related to the

contribution made by the teachers or in other words the amount to be contributed by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

the government is the function of teacher’s contribution and the government

contribution factor. For the purpose of calculation it has been ascertained

Summary of key result section-

a) NPV of unfunded liability:

An unfunded liability is that portion of the debt or liability which has not been

adequately covered with corresponding value of assets saving and investments. It is of

utmost necessary that the liability on the part of the state in respect of the payment of

the superannuation fund is duly covered with the requisite assets, savings or

investments. This result is of utmost importance due to the fact that the bearing it has

on the security of the payment to the beneficiaries of the fund is very significant.

Hence an effort has to be made on the part of the state to ensure that the amount of the

unfunded liability has to be reduced over the period of time (Marshall et al., 2015).

Depending upon the various alternative scenarios the value of the unfunded liability

will change.

b) The ratio of assets to liability NPV:

This result depicts the relationship between the superannuation fund’s assets and the

fund’s liability. The relationship is of significant importance because the final

payment and the ability of the state to pay the amount pertaining to the beneficiaries

depend significantly on the ratio of the assets and liabilities of the funds (Pearlson et

al., 2016).

Justification for not changing the inputs provided by the Director General:

For the purpose of conducting the analysis of the situation pertaining to the

superannuation fund it is necessary that suitable inputs are being taken into due consideration.

In respect of this the Director General has provided several inputs. The requirement of the

the government is the function of teacher’s contribution and the government

contribution factor. For the purpose of calculation it has been ascertained

Summary of key result section-

a) NPV of unfunded liability:

An unfunded liability is that portion of the debt or liability which has not been

adequately covered with corresponding value of assets saving and investments. It is of

utmost necessary that the liability on the part of the state in respect of the payment of

the superannuation fund is duly covered with the requisite assets, savings or

investments. This result is of utmost importance due to the fact that the bearing it has

on the security of the payment to the beneficiaries of the fund is very significant.

Hence an effort has to be made on the part of the state to ensure that the amount of the

unfunded liability has to be reduced over the period of time (Marshall et al., 2015).

Depending upon the various alternative scenarios the value of the unfunded liability

will change.

b) The ratio of assets to liability NPV:

This result depicts the relationship between the superannuation fund’s assets and the

fund’s liability. The relationship is of significant importance because the final

payment and the ability of the state to pay the amount pertaining to the beneficiaries

depend significantly on the ratio of the assets and liabilities of the funds (Pearlson et

al., 2016).

Justification for not changing the inputs provided by the Director General:

For the purpose of conducting the analysis of the situation pertaining to the

superannuation fund it is necessary that suitable inputs are being taken into due consideration.

In respect of this the Director General has provided several inputs. The requirement of the

8ACCOUNTING

requisite inputs has already been fulfilled by the Director General, the reason for this being

that all the factors ranging from the employment of the employees to their termination has

been duly adjudged and included in the calculation of the superannuation fund. There is no

additional requirement for changing the inputs due to the fact that already all the factors

having an impact on the decision made by the state in respect of the superannuation funds

have been taken into consideration by the Director General (Huerta & Jensen, 2017).

Analysis of the various cases being presented for calculation:

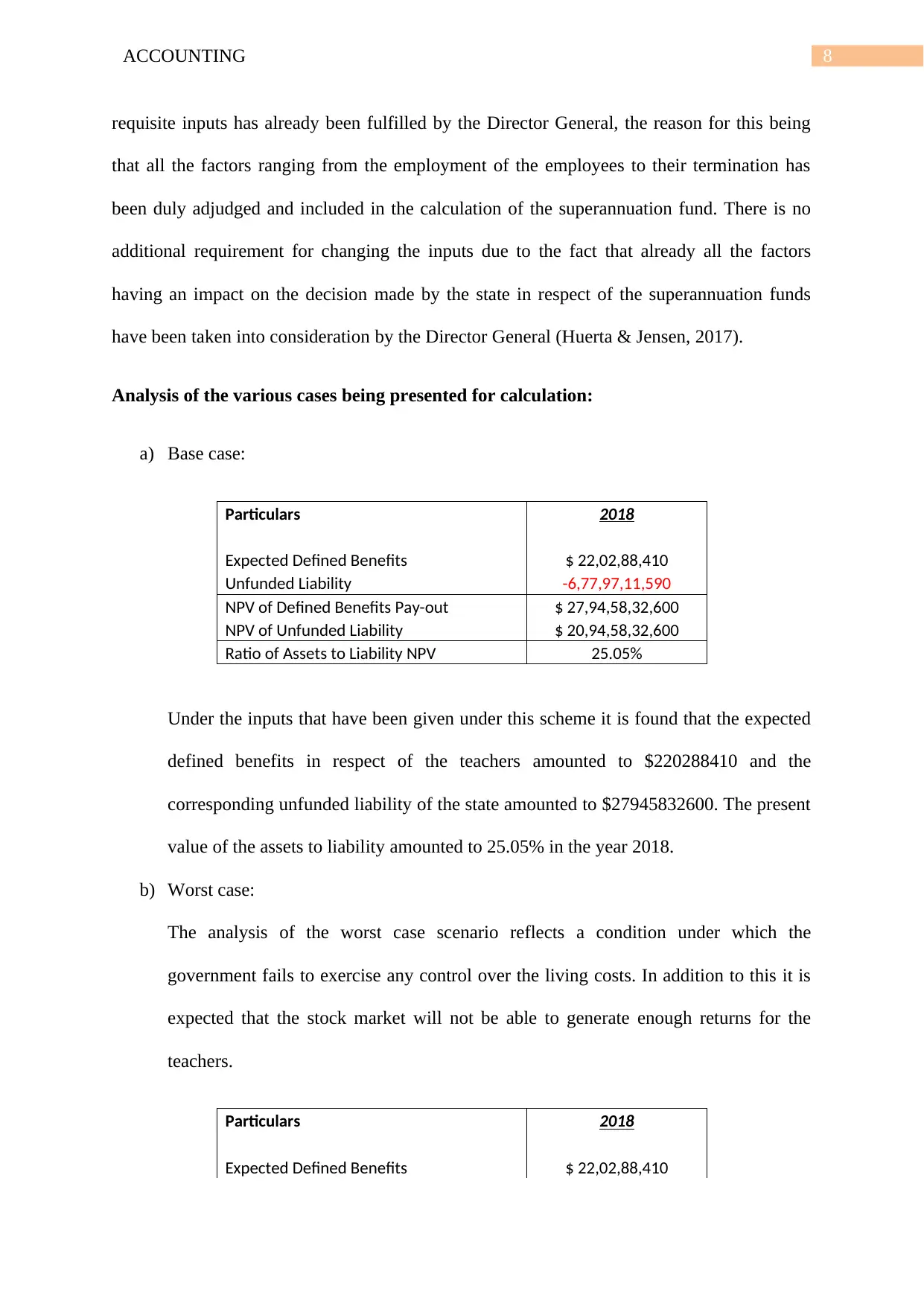

a) Base case:

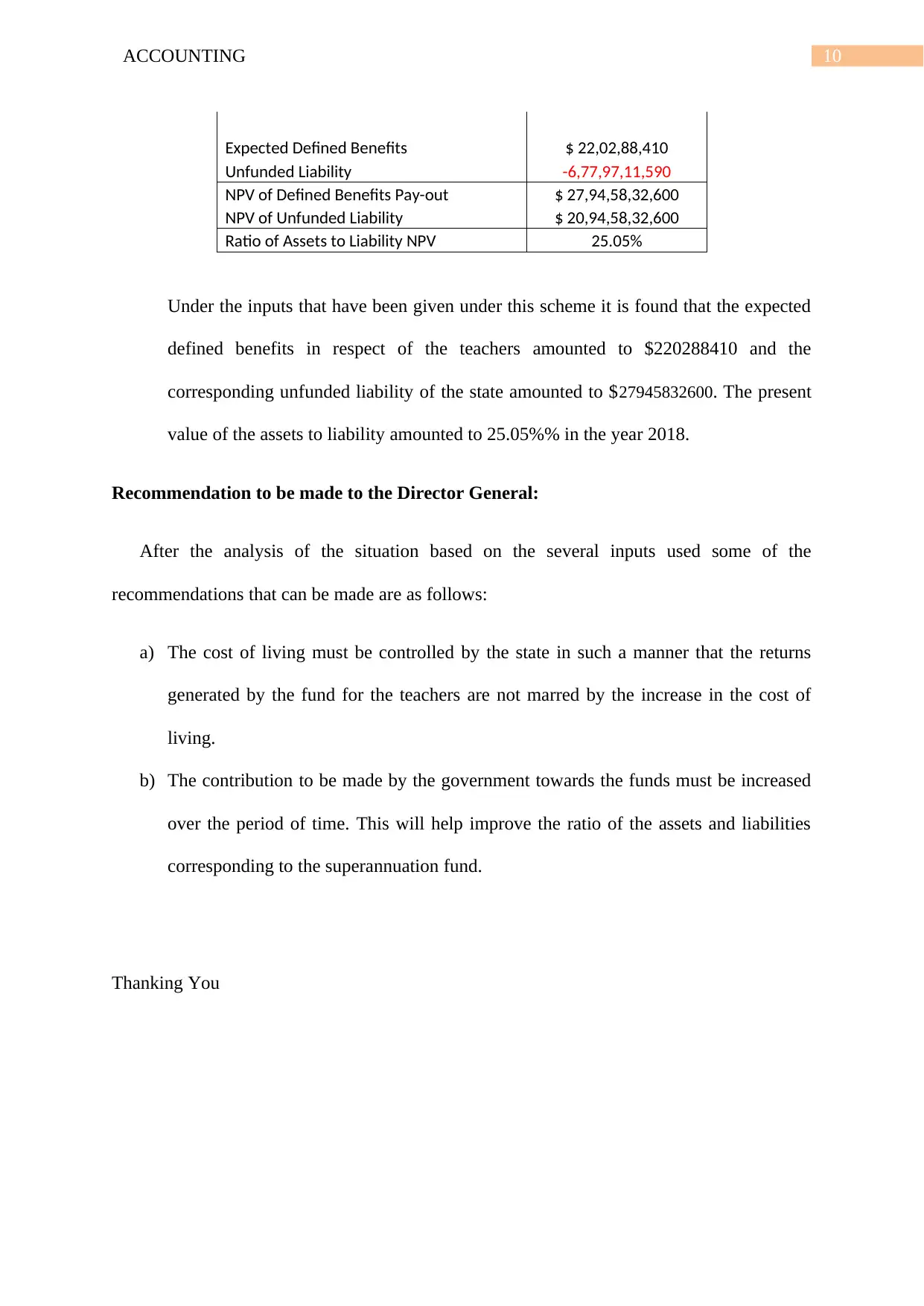

Particulars 2018

Expected Defined Benefits $ 22,02,88,410

Unfunded Liability -6,77,97,11,590

NPV of Defined Benefits Pay-out $ 27,94,58,32,600

NPV of Unfunded Liability $ 20,94,58,32,600

Ratio of Assets to Liability NPV 25.05%

Under the inputs that have been given under this scheme it is found that the expected

defined benefits in respect of the teachers amounted to $220288410 and the

corresponding unfunded liability of the state amounted to $27945832600. The present

value of the assets to liability amounted to 25.05% in the year 2018.

b) Worst case:

The analysis of the worst case scenario reflects a condition under which the

government fails to exercise any control over the living costs. In addition to this it is

expected that the stock market will not be able to generate enough returns for the

teachers.

Particulars 2018

Expected Defined Benefits $ 22,02,88,410

requisite inputs has already been fulfilled by the Director General, the reason for this being

that all the factors ranging from the employment of the employees to their termination has

been duly adjudged and included in the calculation of the superannuation fund. There is no

additional requirement for changing the inputs due to the fact that already all the factors

having an impact on the decision made by the state in respect of the superannuation funds

have been taken into consideration by the Director General (Huerta & Jensen, 2017).

Analysis of the various cases being presented for calculation:

a) Base case:

Particulars 2018

Expected Defined Benefits $ 22,02,88,410

Unfunded Liability -6,77,97,11,590

NPV of Defined Benefits Pay-out $ 27,94,58,32,600

NPV of Unfunded Liability $ 20,94,58,32,600

Ratio of Assets to Liability NPV 25.05%

Under the inputs that have been given under this scheme it is found that the expected

defined benefits in respect of the teachers amounted to $220288410 and the

corresponding unfunded liability of the state amounted to $27945832600. The present

value of the assets to liability amounted to 25.05% in the year 2018.

b) Worst case:

The analysis of the worst case scenario reflects a condition under which the

government fails to exercise any control over the living costs. In addition to this it is

expected that the stock market will not be able to generate enough returns for the

teachers.

Particulars 2018

Expected Defined Benefits $ 22,02,88,410

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

Unfunded Liability -6,77,97,11,590

NPV of Defined Benefits Pay-out $ 29,41,81,85,969

NPV of Unfunded Liability $ 22,41,81,85,969

Ratio of Assets to Liability NPV 23.79%

Under the inputs that have been given under this scheme it is found that the expected

defined benefits in respect of the teachers amounted to $220288410 and the

corresponding unfunded liability of the state amounted to $29418185969. The present

value of the assets to liability amounted to 23.79 % in the year 2018.

c) Aggressive case:

Under the aggressive case an ideal situation has been analysed. Under the same the

cost of living is effectively controlled by the state. The productivity factor is also

favourable for the government and in addition to that the contribution made by the

employees has also increased significantly.

Particulars 2018

Expected Defined Benefits $ 22,02,88,410

Unfunded Liability -6,77,97,11,590

NPV of Defined Benefits Pay-out $ 18,32,19,17,851

NPV of Unfunded Liability $ 11,32,19,17,851

Ratio of Assets to Liability NPV 38.21%

Under the inputs that have been given under this scheme it is found that the expected

defined benefits in respect of the teachers amounted to $220288410 and the

corresponding unfunded liability of the state amounted to $18, 32, 19, 17,851. The

present value of the assets to liability amounted to 38.21% in the year 2018.

d) Rescue case:

In this case a scenario is run under which the government is contributing at a rate

which is sufficient enough to bail it out of the current superannuation fund.

Particulars 2018

Unfunded Liability -6,77,97,11,590

NPV of Defined Benefits Pay-out $ 29,41,81,85,969

NPV of Unfunded Liability $ 22,41,81,85,969

Ratio of Assets to Liability NPV 23.79%

Under the inputs that have been given under this scheme it is found that the expected

defined benefits in respect of the teachers amounted to $220288410 and the

corresponding unfunded liability of the state amounted to $29418185969. The present

value of the assets to liability amounted to 23.79 % in the year 2018.

c) Aggressive case:

Under the aggressive case an ideal situation has been analysed. Under the same the

cost of living is effectively controlled by the state. The productivity factor is also

favourable for the government and in addition to that the contribution made by the

employees has also increased significantly.

Particulars 2018

Expected Defined Benefits $ 22,02,88,410

Unfunded Liability -6,77,97,11,590

NPV of Defined Benefits Pay-out $ 18,32,19,17,851

NPV of Unfunded Liability $ 11,32,19,17,851

Ratio of Assets to Liability NPV 38.21%

Under the inputs that have been given under this scheme it is found that the expected

defined benefits in respect of the teachers amounted to $220288410 and the

corresponding unfunded liability of the state amounted to $18, 32, 19, 17,851. The

present value of the assets to liability amounted to 38.21% in the year 2018.

d) Rescue case:

In this case a scenario is run under which the government is contributing at a rate

which is sufficient enough to bail it out of the current superannuation fund.

Particulars 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

Expected Defined Benefits $ 22,02,88,410

Unfunded Liability -6,77,97,11,590

NPV of Defined Benefits Pay-out $ 27,94,58,32,600

NPV of Unfunded Liability $ 20,94,58,32,600

Ratio of Assets to Liability NPV 25.05%

Under the inputs that have been given under this scheme it is found that the expected

defined benefits in respect of the teachers amounted to $220288410 and the

corresponding unfunded liability of the state amounted to $27945832600. The present

value of the assets to liability amounted to 25.05%% in the year 2018.

Recommendation to be made to the Director General:

After the analysis of the situation based on the several inputs used some of the

recommendations that can be made are as follows:

a) The cost of living must be controlled by the state in such a manner that the returns

generated by the fund for the teachers are not marred by the increase in the cost of

living.

b) The contribution to be made by the government towards the funds must be increased

over the period of time. This will help improve the ratio of the assets and liabilities

corresponding to the superannuation fund.

Thanking You

Expected Defined Benefits $ 22,02,88,410

Unfunded Liability -6,77,97,11,590

NPV of Defined Benefits Pay-out $ 27,94,58,32,600

NPV of Unfunded Liability $ 20,94,58,32,600

Ratio of Assets to Liability NPV 25.05%

Under the inputs that have been given under this scheme it is found that the expected

defined benefits in respect of the teachers amounted to $220288410 and the

corresponding unfunded liability of the state amounted to $27945832600. The present

value of the assets to liability amounted to 25.05%% in the year 2018.

Recommendation to be made to the Director General:

After the analysis of the situation based on the several inputs used some of the

recommendations that can be made are as follows:

a) The cost of living must be controlled by the state in such a manner that the returns

generated by the fund for the teachers are not marred by the increase in the cost of

living.

b) The contribution to be made by the government towards the funds must be increased

over the period of time. This will help improve the ratio of the assets and liabilities

corresponding to the superannuation fund.

Thanking You

11ACCOUNTING

Reference

Apostolou, B., Dorminey, J. W., Hassell, J. M., & Rebele, J. E. (2014). A summary and

analysis of education research in accounting information systems (AIS). Journal of

Accounting Education, 32(2), 99-112.

Hassan, H., Nasir, M. H. M., & Khairudin, N. (2017). Accounting Information Systems.

In SHS Web of Conferences(Vol. 34). EDP Sciences.

Huerta, E., & Jensen, S. (2017). An accounting information systems perspective on data

analytics and Big Data. Journal of Information Systems, 31(3), 101-114.

Kurniawan, Y., Karsen, M., vin Adiprasetyo, A., Juwitasary, H., & Tapia, D. F. C. (2017,

November). Accounting information systems implementation:(A case study

approach). In Information Management and Technology (ICIMTech), 2017

International Conference on (pp. 294-299). IEEE.

Marshall, B. R., & Steinbart, P. J. (2017). ACCOUNTING INFORMATION SYSTEMS.

PEARSON EDUCATION LIMITED.

Marshall, B., Curry, M., & Kawalek, P. (2015). International Journal of Accounting

Information Systems. International Journal of Accounting Information Systems, 19,

17-28.

Pearlson, K. E., Saunders, C. S., & Galletta, D. F. (2016). Managing and Using Information

Systems, Binder Ready Version: A Strategic Approach. John Wiley & Sons.

Peters, M. D., Wieder, B., Sutton, S. G., & Wakefield, J. (2016). International Journal of

Accounting Information Systems. International Journal of Accounting Information

Systems, 21, 1-17.

Reference

Apostolou, B., Dorminey, J. W., Hassell, J. M., & Rebele, J. E. (2014). A summary and

analysis of education research in accounting information systems (AIS). Journal of

Accounting Education, 32(2), 99-112.

Hassan, H., Nasir, M. H. M., & Khairudin, N. (2017). Accounting Information Systems.

In SHS Web of Conferences(Vol. 34). EDP Sciences.

Huerta, E., & Jensen, S. (2017). An accounting information systems perspective on data

analytics and Big Data. Journal of Information Systems, 31(3), 101-114.

Kurniawan, Y., Karsen, M., vin Adiprasetyo, A., Juwitasary, H., & Tapia, D. F. C. (2017,

November). Accounting information systems implementation:(A case study

approach). In Information Management and Technology (ICIMTech), 2017

International Conference on (pp. 294-299). IEEE.

Marshall, B. R., & Steinbart, P. J. (2017). ACCOUNTING INFORMATION SYSTEMS.

PEARSON EDUCATION LIMITED.

Marshall, B., Curry, M., & Kawalek, P. (2015). International Journal of Accounting

Information Systems. International Journal of Accounting Information Systems, 19,

17-28.

Pearlson, K. E., Saunders, C. S., & Galletta, D. F. (2016). Managing and Using Information

Systems, Binder Ready Version: A Strategic Approach. John Wiley & Sons.

Peters, M. D., Wieder, B., Sutton, S. G., & Wakefield, J. (2016). International Journal of

Accounting Information Systems. International Journal of Accounting Information

Systems, 21, 1-17.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.