Report on Superannuation Contributions and Investment Strategies

VerifiedAdded on 2021/06/17

|10

|2521

|27

Report

AI Summary

This report provides a comprehensive analysis of superannuation, a crucial strategy for accelerating savings and securing future financial stability. It delves into the intricacies of superannuation contributions, emphasizing their role in fostering savings habits and providing employees with various investment avenues. The report explores key factors influencing investment decisions within the tertiary sector, specifically comparing defined benefit plans and investment choice plans, and highlights the significance of the time value of money in financial planning. It examines relevant market conditions and risk assessments that employees must consider when choosing investment plans, offering insights into portfolio selection and the potential impact of investment choices on financial outcomes. Recommendations are provided to navigate market fluctuations and optimize investment strategies. The report underscores the importance of professional financial advice and the role of fund managers in guiding investment decisions to maximize client profits. The report emphasizes the need for long-term strategic planning in investments, recommending a thorough understanding of market dynamics and the time value of money to achieve maximum returns. Ultimately, the report concludes that thoughtful superannuation investments are essential for achieving financial security.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

Superannuation

BUSINESS ACCOUNTING

1

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

Superannuation

BUSINESS ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation

Executive Summary

Superannuation can be defined as a string strategy that helps the workers to accelerate the

savings. It is one of the major approach that will help to provide advantage in future.

However, it needs to be noted that investment should be directed in a proper manner. The

following report will shed light on the important factors that needs to be assess by the

employees of the tertiary sector whether to place the contribution of superannuation in the

Defined benefit plan pr the investment plan. Other issues are even considered in the report.

2

Executive Summary

Superannuation can be defined as a string strategy that helps the workers to accelerate the

savings. It is one of the major approach that will help to provide advantage in future.

However, it needs to be noted that investment should be directed in a proper manner. The

following report will shed light on the important factors that needs to be assess by the

employees of the tertiary sector whether to place the contribution of superannuation in the

Defined benefit plan pr the investment plan. Other issues are even considered in the report.

2

Superannuation

Contents

Introduction...........................................................................................................................................3

Superannuation contributions...............................................................................................................3

Relevant factors that are taken into account........................................................................................5

The concept of the time value of money...............................................................................................6

Recommendations.................................................................................................................................7

Conclusion.............................................................................................................................................7

References.............................................................................................................................................9

3

Contents

Introduction...........................................................................................................................................3

Superannuation contributions...............................................................................................................3

Relevant factors that are taken into account........................................................................................5

The concept of the time value of money...............................................................................................6

Recommendations.................................................................................................................................7

Conclusion.............................................................................................................................................7

References.............................................................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation

Introduction

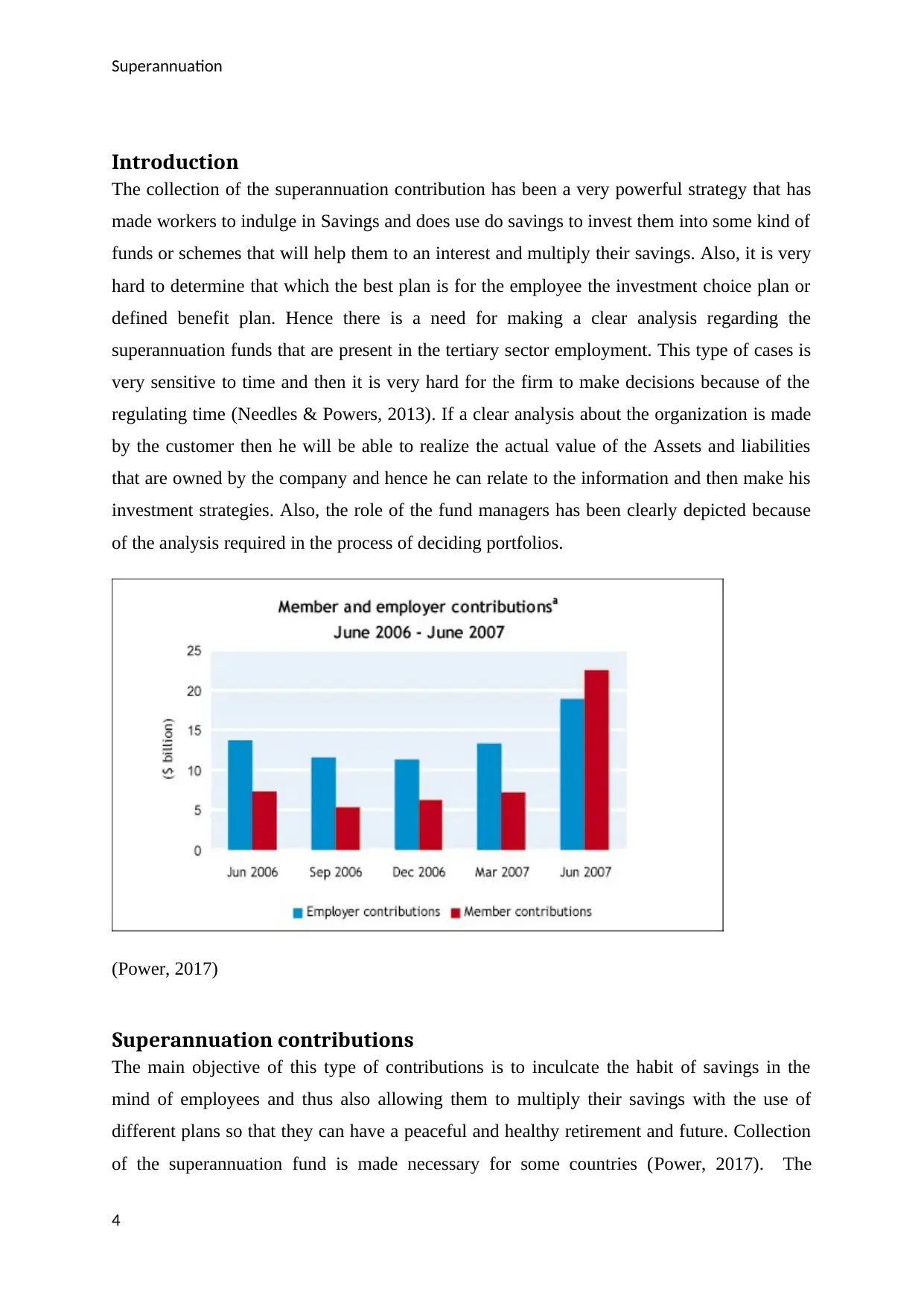

The collection of the superannuation contribution has been a very powerful strategy that has

made workers to indulge in Savings and does use do savings to invest them into some kind of

funds or schemes that will help them to an interest and multiply their savings. Also, it is very

hard to determine that which the best plan is for the employee the investment choice plan or

defined benefit plan. Hence there is a need for making a clear analysis regarding the

superannuation funds that are present in the tertiary sector employment. This type of cases is

very sensitive to time and then it is very hard for the firm to make decisions because of the

regulating time (Needles & Powers, 2013). If a clear analysis about the organization is made

by the customer then he will be able to realize the actual value of the Assets and liabilities

that are owned by the company and hence he can relate to the information and then make his

investment strategies. Also, the role of the fund managers has been clearly depicted because

of the analysis required in the process of deciding portfolios.

(Power, 2017)

Superannuation contributions

The main objective of this type of contributions is to inculcate the habit of savings in the

mind of employees and thus also allowing them to multiply their savings with the use of

different plans so that they can have a peaceful and healthy retirement and future. Collection

of the superannuation fund is made necessary for some countries (Power, 2017). The

4

Introduction

The collection of the superannuation contribution has been a very powerful strategy that has

made workers to indulge in Savings and does use do savings to invest them into some kind of

funds or schemes that will help them to an interest and multiply their savings. Also, it is very

hard to determine that which the best plan is for the employee the investment choice plan or

defined benefit plan. Hence there is a need for making a clear analysis regarding the

superannuation funds that are present in the tertiary sector employment. This type of cases is

very sensitive to time and then it is very hard for the firm to make decisions because of the

regulating time (Needles & Powers, 2013). If a clear analysis about the organization is made

by the customer then he will be able to realize the actual value of the Assets and liabilities

that are owned by the company and hence he can relate to the information and then make his

investment strategies. Also, the role of the fund managers has been clearly depicted because

of the analysis required in the process of deciding portfolios.

(Power, 2017)

Superannuation contributions

The main objective of this type of contributions is to inculcate the habit of savings in the

mind of employees and thus also allowing them to multiply their savings with the use of

different plans so that they can have a peaceful and healthy retirement and future. Collection

of the superannuation fund is made necessary for some countries (Power, 2017). The

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation

collection is made necessary for the employer to collect money from the employees as a

superannuation fund and then invest them on their behalf also making this process mandatory

in nature. Because the system has been made mandatory for the organisation to collect

superannuation friends, there have been observed tremendous increase that has been seen in

the superannuation fund that have been collected by the employees which have also lead to

improve the role of Financial Institutions in order to invest the money in best deals or

schemes so that the individuals and their the employees can be provided with the best returns

on their savings investment (Power, 2017).

The three main economic sectors upon which the superannuation contributions are dependent

are Primary, secondary and tertiary sectors. The main objective of the function that is to be

completed by the superannuation funds is to help the tertiary sector employees to get the best

advice relating to the investments they make and also help implementation of new and

improved methods of wisdom that will help to increase the productivity of different sectors. It

was previously noticed that the percentage of a superannuation fund that was collected from

employees was 3% but by the year 2005 it has been increased to 9%. The employees need to

indulge in this kind of activities and then make payments regarding the superannuation funds

as a percentage of their salary which is paid to the employer and does is used by them to

invest in opportunities that will provide benefits for both the firm and employee. These types

of systems help to create social security among employees by the collection of money for

their Peaceful retirement and thus promoting the habit of savings among them. After the

analysis of market one of the most renowned organizations that were able to take good care

and invest the superannuation fund in a profitable manner was considered to be ABC Limited

(Ross et. al, 2014). With the increase in time, the employees are also coming to know about

this kind of Investment plans in which they are able to save there are two salaries and also at

the same time are able to earn interest on them by investing them in a particular manner. The

employees are given two different kinds of investment plans in which the superannuation

fund which was the part of the salary are being invested. The choices are defined benefit plan

and investment choice plan.

The name of defined benefit plan makes it clear that all the factors are prepared on the basis

of the percentage of the superannuation fund which has been provided by the employee in

order to invest. The factors through the amount of the superannuation fund are decided are

age, average salary, etc. Also, the amount that the employee will receive after the completion

of the defined benefit plan is clearly mentioned and there are no changes in the amount of

5

collection is made necessary for the employer to collect money from the employees as a

superannuation fund and then invest them on their behalf also making this process mandatory

in nature. Because the system has been made mandatory for the organisation to collect

superannuation friends, there have been observed tremendous increase that has been seen in

the superannuation fund that have been collected by the employees which have also lead to

improve the role of Financial Institutions in order to invest the money in best deals or

schemes so that the individuals and their the employees can be provided with the best returns

on their savings investment (Power, 2017).

The three main economic sectors upon which the superannuation contributions are dependent

are Primary, secondary and tertiary sectors. The main objective of the function that is to be

completed by the superannuation funds is to help the tertiary sector employees to get the best

advice relating to the investments they make and also help implementation of new and

improved methods of wisdom that will help to increase the productivity of different sectors. It

was previously noticed that the percentage of a superannuation fund that was collected from

employees was 3% but by the year 2005 it has been increased to 9%. The employees need to

indulge in this kind of activities and then make payments regarding the superannuation funds

as a percentage of their salary which is paid to the employer and does is used by them to

invest in opportunities that will provide benefits for both the firm and employee. These types

of systems help to create social security among employees by the collection of money for

their Peaceful retirement and thus promoting the habit of savings among them. After the

analysis of market one of the most renowned organizations that were able to take good care

and invest the superannuation fund in a profitable manner was considered to be ABC Limited

(Ross et. al, 2014). With the increase in time, the employees are also coming to know about

this kind of Investment plans in which they are able to save there are two salaries and also at

the same time are able to earn interest on them by investing them in a particular manner. The

employees are given two different kinds of investment plans in which the superannuation

fund which was the part of the salary are being invested. The choices are defined benefit plan

and investment choice plan.

The name of defined benefit plan makes it clear that all the factors are prepared on the basis

of the percentage of the superannuation fund which has been provided by the employee in

order to invest. The factors through the amount of the superannuation fund are decided are

age, average salary, etc. Also, the amount that the employee will receive after the completion

of the defined benefit plan is clearly mentioned and there are no changes in the amount of

5

Superannuation

interest with the employee is going to get. This also states that the employee has nothing to

do with the loss or profit of unissued Limited thus making it profitable for them as they will

be getting a safe and secure method of investment with high returns.

On the other hand, the investment choice plan consists of the benefits that the company has

received after deducting the administrative expenses and management expenses from the

Investments. This type of plans allows the customers or the employees to decide in which

plan they are going to invest and thus the employees are being given the options of the secure

fund, share fund, trustees selection fund, stable fund, etc. to choose from and invest. The

employee should analyze them all considering all the conditions of the market on the basis of

the risks and returns and then invest money in the best concerns (Vaitilingam, 2014).

Relevant factors that are taken into account

When the employee decides in which plan he has to invest, he needs to make certain

decisions according to the market conditions and thus make specific regards on the basis of

proper analysis of all factors of risk that are present in the environment. For the investors or

employees who seek no risk and at the same time they want high returns, the define choice

plan is most suitable (Marsh, 2009). Similarly the employees you are not afraid in order to

invest their savings in the different type of investments, they should pursue the investment

6

interest with the employee is going to get. This also states that the employee has nothing to

do with the loss or profit of unissued Limited thus making it profitable for them as they will

be getting a safe and secure method of investment with high returns.

On the other hand, the investment choice plan consists of the benefits that the company has

received after deducting the administrative expenses and management expenses from the

Investments. This type of plans allows the customers or the employees to decide in which

plan they are going to invest and thus the employees are being given the options of the secure

fund, share fund, trustees selection fund, stable fund, etc. to choose from and invest. The

employee should analyze them all considering all the conditions of the market on the basis of

the risks and returns and then invest money in the best concerns (Vaitilingam, 2014).

Relevant factors that are taken into account

When the employee decides in which plan he has to invest, he needs to make certain

decisions according to the market conditions and thus make specific regards on the basis of

proper analysis of all factors of risk that are present in the environment. For the investors or

employees who seek no risk and at the same time they want high returns, the define choice

plan is most suitable (Marsh, 2009). Similarly the employees you are not afraid in order to

invest their savings in the different type of investments, they should pursue the investment

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation

choice plan because the amount of the returns at are received are much higher if correct

analysis and proper decision making have been taken into consideration.

There are many factors which help the employees in order to determine the plan in which

they are going to invest. The first step towards choosing of the plan is to ascertain the specific

portfolio in which the employee seeks to invest his money by the use of his knowledge and

experience and thus allowing him to gain greater Returns or even maybe partial losses (Petty

et. al, 2012). If there is any mistake made by the employee in choosing the portfolio then this

inability will cause him to suffer loss which will make it difficult for him to safeguard his

future. The best way in order to get vitamins and also be saving from the responsibility of

investment is to ask the employer to invest the part of the superannuation fund so that the

employee will be safe from any kind of losses or hazard in the upcoming future (Melville,

2013). Also, it is usual that employers would want to invest in investment choice plan as it is

more beneficial to the Employees and also the employee is already having a specified source

of income so they can use the extra funds in order to invest them and thus use their

knowledge to earn high interest on their savings. The defined benefit plan help the employee

to invest their savings in a source that will be providing them Returns at all costs and there is

no risk that prevails on this type of plans (Porter & Norton, 2014). Therefore a clear analysis

of the present environment should be taken into factor while preparing or making any

decisions regarding the investment choice the employee need to invest his savings in.

The concept of the time value of money

It is a Universal fact that time is money and this is said because financial decisions that are

taken by the companies lay more importance on the expenses and the future opportunities for

their businesses. The existing business policies are affected a lot by this type of concepts. It

will be profitable for the firm if they invest their money and do not keep it in a liquid form

because it is said that the value of the money degraded time and thus investment in a proper

plan will help to secure it. It is very important for the form to make investments at present so

that so that the returns that will be gained in future can be used by them in order to meet the

demands which are required (Parrino et. al, 2012). The investors are more derived with the

current returns that they will receive from the market if they trade. The present market

conditions and the current value of money also help in deciding which type of investment

plan we should use in order to invest our superannuation contribution in order to get

maximum output.

7

choice plan because the amount of the returns at are received are much higher if correct

analysis and proper decision making have been taken into consideration.

There are many factors which help the employees in order to determine the plan in which

they are going to invest. The first step towards choosing of the plan is to ascertain the specific

portfolio in which the employee seeks to invest his money by the use of his knowledge and

experience and thus allowing him to gain greater Returns or even maybe partial losses (Petty

et. al, 2012). If there is any mistake made by the employee in choosing the portfolio then this

inability will cause him to suffer loss which will make it difficult for him to safeguard his

future. The best way in order to get vitamins and also be saving from the responsibility of

investment is to ask the employer to invest the part of the superannuation fund so that the

employee will be safe from any kind of losses or hazard in the upcoming future (Melville,

2013). Also, it is usual that employers would want to invest in investment choice plan as it is

more beneficial to the Employees and also the employee is already having a specified source

of income so they can use the extra funds in order to invest them and thus use their

knowledge to earn high interest on their savings. The defined benefit plan help the employee

to invest their savings in a source that will be providing them Returns at all costs and there is

no risk that prevails on this type of plans (Porter & Norton, 2014). Therefore a clear analysis

of the present environment should be taken into factor while preparing or making any

decisions regarding the investment choice the employee need to invest his savings in.

The concept of the time value of money

It is a Universal fact that time is money and this is said because financial decisions that are

taken by the companies lay more importance on the expenses and the future opportunities for

their businesses. The existing business policies are affected a lot by this type of concepts. It

will be profitable for the firm if they invest their money and do not keep it in a liquid form

because it is said that the value of the money degraded time and thus investment in a proper

plan will help to secure it. It is very important for the form to make investments at present so

that so that the returns that will be gained in future can be used by them in order to meet the

demands which are required (Parrino et. al, 2012). The investors are more derived with the

current returns that they will receive from the market if they trade. The present market

conditions and the current value of money also help in deciding which type of investment

plan we should use in order to invest our superannuation contribution in order to get

maximum output.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation

It has also been observed that the working step of the companies I said to invest a specified

amount of their salary in the superannuation fund till they get paid for their services. It has

been observed that the employees use of superannuation funds to indulge in Savings and then

use the savings in order to make the investment so that they can earn higher interest on them.

Also, this method is very long and thus evaluation should be made beforehand so that the

assumptions made if are incorrect then proper measures can be taken. It has been observed

that long-term investments are more profitable than the short ones. Hands a strategic plan

should formulate in order to get the maximum benefits out of the investment that the

employee has made. The employee should understand that the investments are not always

profitable and there may be a negative time in which a downfall is experienced. Thus level of

patients required is very high in the form of investment because of the long-term plan and

also all the decisions made by the employee should be taken in relation to the time value of

money.

Recommendations

There is always confusion because of the low stock prices and also the peak prices that

change over time. Thus a professional advice may help the employees in order to evaluate the

decisions upon the market and then make investment plans according to it. In the cases of

pension plans, it is the duty of the manager to deliver the investment mode in which the best

output is offered. The management should check all the present Ranges and areas in which

the employees can make the choice of their Investments. If all the measures that are required

in the state of security and concerns related to the portfolio are considered then the risks can

be eliminated successfully (Merchant, 2012). Also, the increased tax rate and the selection

should be taken as a fact by the fund manager does helping him to find the right path so that

he can maximize his client’s profit.

Conclusion

The value of the savings is achieved when employees invest their earnings in the

superannuation fund in a thoughtful manner. Also, the decisions regarding to the type of

investment plan the employee needs to take into factor should be made correctly. The time

value of money and the mode of the investment are very crucial decisions that need to be

taken into fact at the time of investing and taking decisions towards catering the Expectations

8

It has also been observed that the working step of the companies I said to invest a specified

amount of their salary in the superannuation fund till they get paid for their services. It has

been observed that the employees use of superannuation funds to indulge in Savings and then

use the savings in order to make the investment so that they can earn higher interest on them.

Also, this method is very long and thus evaluation should be made beforehand so that the

assumptions made if are incorrect then proper measures can be taken. It has been observed

that long-term investments are more profitable than the short ones. Hands a strategic plan

should formulate in order to get the maximum benefits out of the investment that the

employee has made. The employee should understand that the investments are not always

profitable and there may be a negative time in which a downfall is experienced. Thus level of

patients required is very high in the form of investment because of the long-term plan and

also all the decisions made by the employee should be taken in relation to the time value of

money.

Recommendations

There is always confusion because of the low stock prices and also the peak prices that

change over time. Thus a professional advice may help the employees in order to evaluate the

decisions upon the market and then make investment plans according to it. In the cases of

pension plans, it is the duty of the manager to deliver the investment mode in which the best

output is offered. The management should check all the present Ranges and areas in which

the employees can make the choice of their Investments. If all the measures that are required

in the state of security and concerns related to the portfolio are considered then the risks can

be eliminated successfully (Merchant, 2012). Also, the increased tax rate and the selection

should be taken as a fact by the fund manager does helping him to find the right path so that

he can maximize his client’s profit.

Conclusion

The value of the savings is achieved when employees invest their earnings in the

superannuation fund in a thoughtful manner. Also, the decisions regarding to the type of

investment plan the employee needs to take into factor should be made correctly. The time

value of money and the mode of the investment are very crucial decisions that need to be

taken into fact at the time of investing and taking decisions towards catering the Expectations

8

Superannuation

of employees. Also, it has been advised to the managers to leave the whole process by

pinning risks that me either lead to loss or may lead to profit for the customers.

9

of employees. Also, it has been advised to the managers to leave the whole process by

pinning risks that me either lead to loss or may lead to profit for the customers.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation

References

Marsh, C. (2009) Mastering financial management. Harlow: Financial Times Prentice Hall.

Melville, A. (2013) International Financial Reporting – A Practical Guide. 4th edition.

Pearson, Education Limited, UK

Merchant, K. A. (2012) Making Management Accounting Research More Useful. Pacific

Accounting Review. [online]. 24(3), 1-34. Available from

Needles, B.E & Powers, M. (2013) Principles of Financial Accounting. Financial Accounting

Series: Cengage Learning.

Needles, B.E. and Powers, M. (2013) Principles of Financial Accounting. Financial

Accounting Series: Cengage Learning.

Parrino, R, Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

Porter, G. and Norton, C. (2014) Financial Accounting: The Impact on Decision Maker.

Texas: Cengage Learning

Power, T. (2017) Fund choice: Comparing super funds in 8 steps [online]. Available at:

https://www.superguide.com.au/boost-your-superannuation/comparing-super-funds-in-8-

steps [Accessed 18 May 2018]

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall.

10

References

Marsh, C. (2009) Mastering financial management. Harlow: Financial Times Prentice Hall.

Melville, A. (2013) International Financial Reporting – A Practical Guide. 4th edition.

Pearson, Education Limited, UK

Merchant, K. A. (2012) Making Management Accounting Research More Useful. Pacific

Accounting Review. [online]. 24(3), 1-34. Available from

Needles, B.E & Powers, M. (2013) Principles of Financial Accounting. Financial Accounting

Series: Cengage Learning.

Needles, B.E. and Powers, M. (2013) Principles of Financial Accounting. Financial

Accounting Series: Cengage Learning.

Parrino, R, Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

Porter, G. and Norton, C. (2014) Financial Accounting: The Impact on Decision Maker.

Texas: Cengage Learning

Power, T. (2017) Fund choice: Comparing super funds in 8 steps [online]. Available at:

https://www.superguide.com.au/boost-your-superannuation/comparing-super-funds-in-8-

steps [Accessed 18 May 2018]

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.