Superannuation Investment Decision: Benefit Plan vs. Choice Plan?

VerifiedAdded on 2023/06/12

|10

|2599

|81

Report

AI Summary

This report provides an analysis of superannuation investment choices, focusing on the factors tertiary sector employees should consider when deciding between defined benefit plans and investment choice plans. It discusses the importance of superannuation contributions for retirement savings and the role of financial institutions in managing these funds. The report also examines relevant factors such as risk tolerance, portfolio management skills, and the concept of the time value of money. It emphasizes the need for careful analysis and strategic planning to maximize investment returns and ensure a secure financial future. The report concludes with a recommendation for employees to make informed decisions based on their individual circumstances and risk preferences.

Superannuation

Executive Summary

Funding to superannuation is a major strategy because it helps the workers to multiply the

savings. It is a prudent approach because it will lead to benefits in the future. However, the

investment must be done in a prudent manner. In this report, the major emphasis will be on

the major factors that need to be taken into consideration by the tertiary sector employees

whether to place the superannuation contribution in the Defined benefit plan or the

investment choice plan. Further, various issues that surrounds the investment such as time

value of money, taxes are discussed.

1

Executive Summary

Funding to superannuation is a major strategy because it helps the workers to multiply the

savings. It is a prudent approach because it will lead to benefits in the future. However, the

investment must be done in a prudent manner. In this report, the major emphasis will be on

the major factors that need to be taken into consideration by the tertiary sector employees

whether to place the superannuation contribution in the Defined benefit plan or the

investment choice plan. Further, various issues that surrounds the investment such as time

value of money, taxes are discussed.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation

Contents

Introduction...........................................................................................................................................2

Superannuation contributions...............................................................................................................2

Relevant Factors that are to be taken into account...............................................................................4

The concept of time value of money.....................................................................................................5

Recommendation..................................................................................................................................6

Conclusion.............................................................................................................................................6

References.............................................................................................................................................8

2

Contents

Introduction...........................................................................................................................................2

Superannuation contributions...............................................................................................................2

Relevant Factors that are to be taken into account...............................................................................4

The concept of time value of money.....................................................................................................5

Recommendation..................................................................................................................................6

Conclusion.............................................................................................................................................6

References.............................................................................................................................................8

2

Superannuation

Introduction

The use of the contribution made for the superannuation has been a very keen strategy which

has indulged the workers to make saving and then use those funds in the future to invest those

funds in some kind of scheme which will allow them to multiply their savings. There should

be an analysis made before investing money of the superannuation funds because in the

tertiary sector employment there are several different types of factors which are affecting the

plan whether to invest in the investment choice or defined benefit plans. Also, time plays a

very important role in these types of cases which is thus affecting the decision making

process. If the investors will make a detailed analysis of the market, then they will be able to

determine the prices of the assets or stocks which can be helpful while making decisions

relating to the investment strategies (Power, 2014). These types of analysis mention the roles

of the fund managers in the process of deciding portfolios.

Superannuation contributions

The main purpose of contributions of the superannuation funds is to indulge the employees in

the habit of saving and thus making them invest the saved amounts in the future so that they

can have a peaceful and healthy retirement. Many of the countries have made the process of

collection of the superannuation funds necessary for the employers in which they collect the

funds on behalf of employees thus making the process mandatory in nature (Laux, 2014).

Because of the mandated rules of collecting the superannuation funds, there has been a huge

increase in the funds collected from the process thus making the role of the financial

institutions to invest the money in a proper factual manner so that it can provide the

individuals with proper returns on their saving investment (Kollmorgen , 2015).

There is three economic sectors primary, secondary and tertiary sector which have been the

relevant part of the economic sections of the superannuation contributions. The main function

of the tertiary employees is to give the employees proper advice for the investments they

need to make and also they play a major role in the implementation of the wisdom in the

productivity of different sectors. Previously the contribution of the funds was restricted to

three percent of the employee’s salary but it has now been increased to nine percent since the

year 2005. The employees indulge in the payment of the funds are also being made to pay a

specified percentage of the investments (Power, 2014). It should be duly noted that the use of

such systems have been promoted in order to mould the social security systems of the

3

Introduction

The use of the contribution made for the superannuation has been a very keen strategy which

has indulged the workers to make saving and then use those funds in the future to invest those

funds in some kind of scheme which will allow them to multiply their savings. There should

be an analysis made before investing money of the superannuation funds because in the

tertiary sector employment there are several different types of factors which are affecting the

plan whether to invest in the investment choice or defined benefit plans. Also, time plays a

very important role in these types of cases which is thus affecting the decision making

process. If the investors will make a detailed analysis of the market, then they will be able to

determine the prices of the assets or stocks which can be helpful while making decisions

relating to the investment strategies (Power, 2014). These types of analysis mention the roles

of the fund managers in the process of deciding portfolios.

Superannuation contributions

The main purpose of contributions of the superannuation funds is to indulge the employees in

the habit of saving and thus making them invest the saved amounts in the future so that they

can have a peaceful and healthy retirement. Many of the countries have made the process of

collection of the superannuation funds necessary for the employers in which they collect the

funds on behalf of employees thus making the process mandatory in nature (Laux, 2014).

Because of the mandated rules of collecting the superannuation funds, there has been a huge

increase in the funds collected from the process thus making the role of the financial

institutions to invest the money in a proper factual manner so that it can provide the

individuals with proper returns on their saving investment (Kollmorgen , 2015).

There is three economic sectors primary, secondary and tertiary sector which have been the

relevant part of the economic sections of the superannuation contributions. The main function

of the tertiary employees is to give the employees proper advice for the investments they

need to make and also they play a major role in the implementation of the wisdom in the

productivity of different sectors. Previously the contribution of the funds was restricted to

three percent of the employee’s salary but it has now been increased to nine percent since the

year 2005. The employees indulge in the payment of the funds are also being made to pay a

specified percentage of the investments (Power, 2014). It should be duly noted that the use of

such systems have been promoted in order to mould the social security systems of the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

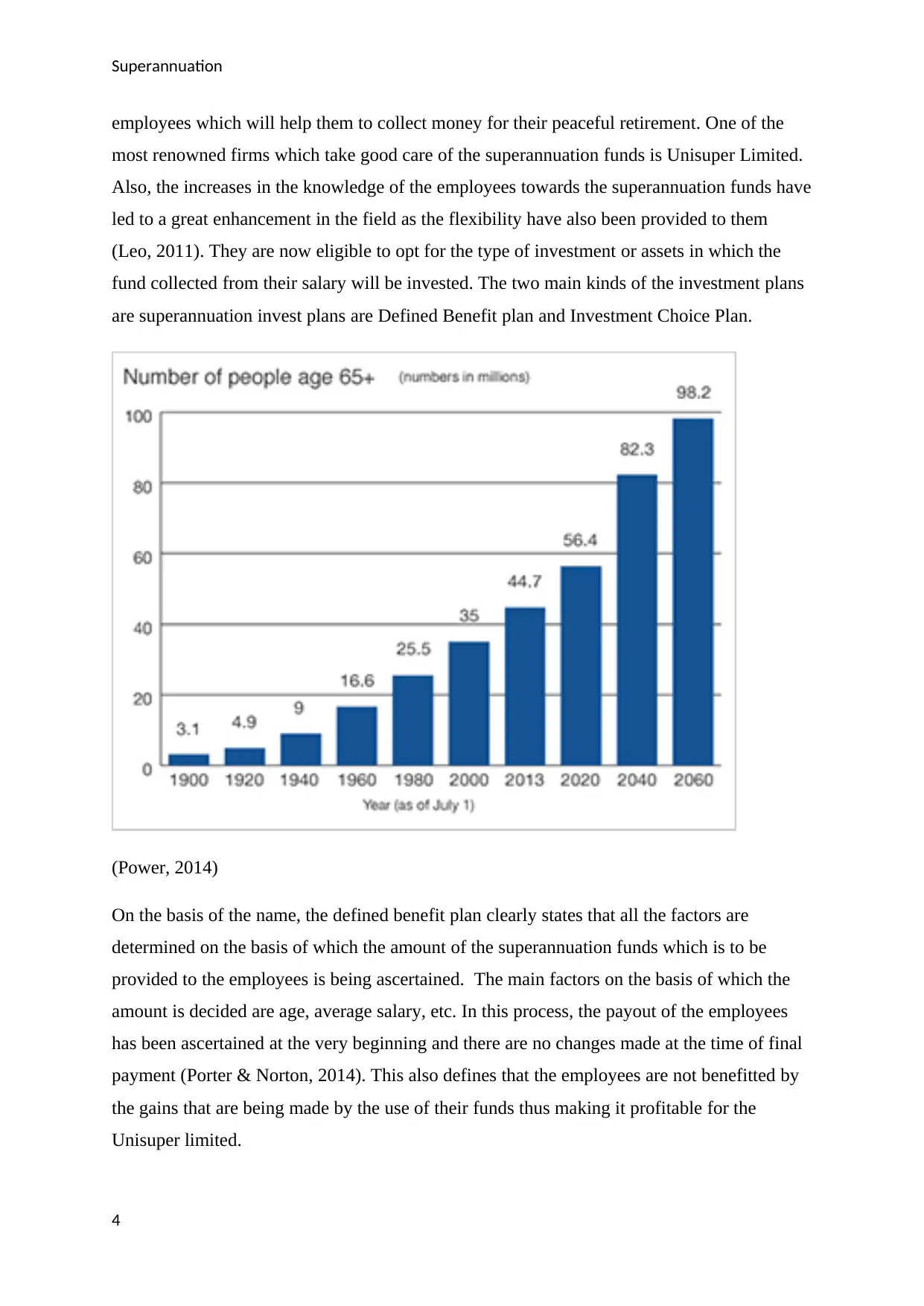

Superannuation

employees which will help them to collect money for their peaceful retirement. One of the

most renowned firms which take good care of the superannuation funds is Unisuper Limited.

Also, the increases in the knowledge of the employees towards the superannuation funds have

led to a great enhancement in the field as the flexibility have also been provided to them

(Leo, 2011). They are now eligible to opt for the type of investment or assets in which the

fund collected from their salary will be invested. The two main kinds of the investment plans

are superannuation invest plans are Defined Benefit plan and Investment Choice Plan.

(Power, 2014)

On the basis of the name, the defined benefit plan clearly states that all the factors are

determined on the basis of which the amount of the superannuation funds which is to be

provided to the employees is being ascertained. The main factors on the basis of which the

amount is decided are age, average salary, etc. In this process, the payout of the employees

has been ascertained at the very beginning and there are no changes made at the time of final

payment (Porter & Norton, 2014). This also defines that the employees are not benefitted by

the gains that are being made by the use of their funds thus making it profitable for the

Unisuper limited.

4

employees which will help them to collect money for their peaceful retirement. One of the

most renowned firms which take good care of the superannuation funds is Unisuper Limited.

Also, the increases in the knowledge of the employees towards the superannuation funds have

led to a great enhancement in the field as the flexibility have also been provided to them

(Leo, 2011). They are now eligible to opt for the type of investment or assets in which the

fund collected from their salary will be invested. The two main kinds of the investment plans

are superannuation invest plans are Defined Benefit plan and Investment Choice Plan.

(Power, 2014)

On the basis of the name, the defined benefit plan clearly states that all the factors are

determined on the basis of which the amount of the superannuation funds which is to be

provided to the employees is being ascertained. The main factors on the basis of which the

amount is decided are age, average salary, etc. In this process, the payout of the employees

has been ascertained at the very beginning and there are no changes made at the time of final

payment (Porter & Norton, 2014). This also defines that the employees are not benefitted by

the gains that are being made by the use of their funds thus making it profitable for the

Unisuper limited.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation

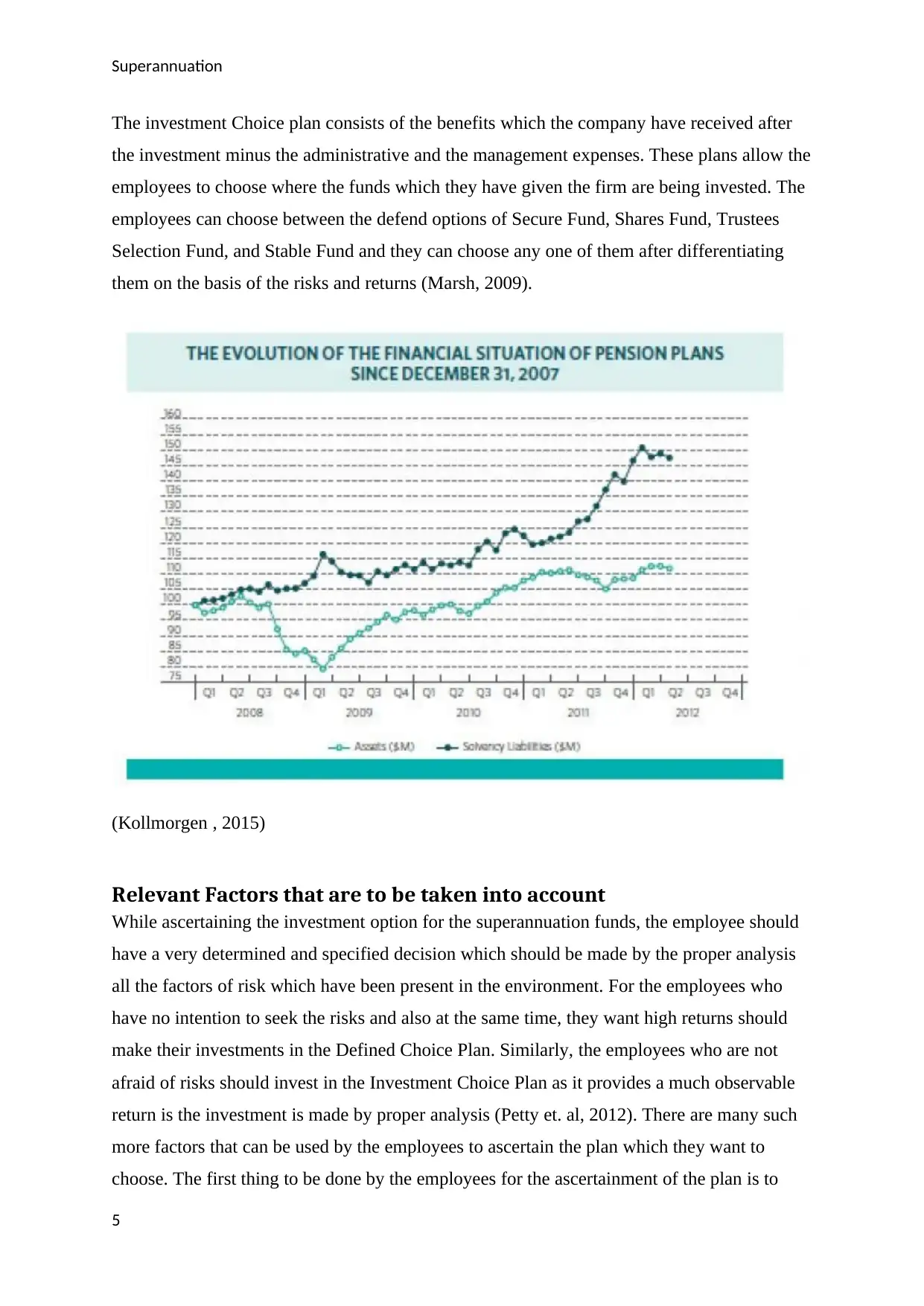

The investment Choice plan consists of the benefits which the company have received after

the investment minus the administrative and the management expenses. These plans allow the

employees to choose where the funds which they have given the firm are being invested. The

employees can choose between the defend options of Secure Fund, Shares Fund, Trustees

Selection Fund, and Stable Fund and they can choose any one of them after differentiating

them on the basis of the risks and returns (Marsh, 2009).

(Kollmorgen , 2015)

Relevant Factors that are to be taken into account

While ascertaining the investment option for the superannuation funds, the employee should

have a very determined and specified decision which should be made by the proper analysis

all the factors of risk which have been present in the environment. For the employees who

have no intention to seek the risks and also at the same time, they want high returns should

make their investments in the Defined Choice Plan. Similarly, the employees who are not

afraid of risks should invest in the Investment Choice Plan as it provides a much observable

return is the investment is made by proper analysis (Petty et. al, 2012). There are many such

more factors that can be used by the employees to ascertain the plan which they want to

choose. The first thing to be done by the employees for the ascertainment of the plan is to

5

The investment Choice plan consists of the benefits which the company have received after

the investment minus the administrative and the management expenses. These plans allow the

employees to choose where the funds which they have given the firm are being invested. The

employees can choose between the defend options of Secure Fund, Shares Fund, Trustees

Selection Fund, and Stable Fund and they can choose any one of them after differentiating

them on the basis of the risks and returns (Marsh, 2009).

(Kollmorgen , 2015)

Relevant Factors that are to be taken into account

While ascertaining the investment option for the superannuation funds, the employee should

have a very determined and specified decision which should be made by the proper analysis

all the factors of risk which have been present in the environment. For the employees who

have no intention to seek the risks and also at the same time, they want high returns should

make their investments in the Defined Choice Plan. Similarly, the employees who are not

afraid of risks should invest in the Investment Choice Plan as it provides a much observable

return is the investment is made by proper analysis (Petty et. al, 2012). There are many such

more factors that can be used by the employees to ascertain the plan which they want to

choose. The first thing to be done by the employees for the ascertainment of the plan is to

5

Superannuation

find and select the portfolio in which it will invest by the use of his knowledge and

experience thus allowing him to get greater returns instead of the partial losses (Ross et. al,

2014). The inability to manage the portfolios will lead the employees to suffer loss which will

make them unable to live a peaceful future. The best way to deal is to give the employer the

responsibility to invest so that is any loss is experienced then it will be suffered by the

employer thus keeping the employee safe from any kind of hazard. The use of the Investment

Choice plan is also beneficial as the employees have a specified source of income which is

providing them with their expenses, thus they can use the extra funds to invest in the plans

which may provide them with high returns and thus making the income much more beneficial

(Kollmorgen , 2015). Defined investment plan provides them with less but sure returns thus

making the choice between the two to be very hard to assess (Parrino et. al, 2012). Therefore

all the decisions should be made in the accordance to the present environment and thus the

employees should take the decisions of investment only after the proper analysis of all the

prevailing factors.

The concept of time value of money

Future cash flows can be attributed to the fact that time is money and this can be said because

of the financial decisions that are taken up by companies now which lay more importance on

the expenses and the lying future opportunities for their business. These types of concepts are

very important for the existing business policies. It is known that money’s value gets

degraded as time passes so it is important to invest in the areas rather and get profit at present

while waiting for it in a long-term scale (Vaitilingam, 2014). Present term investments can be

of more importance as it will earn interests to the investors which can be later used when and

where demanded and required. The investor re much more concerned with the existing value

of money because they want to trade now. Time value of money can be defined as the

demarcation line that the present and the future values of money have between them. Also,

the current value of money plays a key role in deciding the type of investments from their

superannuation contributions that one should undertake to get the maximum output

(Vaitilingam, 2014).

It is seen that the working staff of the companies invest a limited amount of their salary ion

superannuation funds till the date hey get money for their services. It is seen that this

collected money comes with some interest and the total amount is further invested to

maximize it. But it should also be known that this collected amount cannot be generated

6

find and select the portfolio in which it will invest by the use of his knowledge and

experience thus allowing him to get greater returns instead of the partial losses (Ross et. al,

2014). The inability to manage the portfolios will lead the employees to suffer loss which will

make them unable to live a peaceful future. The best way to deal is to give the employer the

responsibility to invest so that is any loss is experienced then it will be suffered by the

employer thus keeping the employee safe from any kind of hazard. The use of the Investment

Choice plan is also beneficial as the employees have a specified source of income which is

providing them with their expenses, thus they can use the extra funds to invest in the plans

which may provide them with high returns and thus making the income much more beneficial

(Kollmorgen , 2015). Defined investment plan provides them with less but sure returns thus

making the choice between the two to be very hard to assess (Parrino et. al, 2012). Therefore

all the decisions should be made in the accordance to the present environment and thus the

employees should take the decisions of investment only after the proper analysis of all the

prevailing factors.

The concept of time value of money

Future cash flows can be attributed to the fact that time is money and this can be said because

of the financial decisions that are taken up by companies now which lay more importance on

the expenses and the lying future opportunities for their business. These types of concepts are

very important for the existing business policies. It is known that money’s value gets

degraded as time passes so it is important to invest in the areas rather and get profit at present

while waiting for it in a long-term scale (Vaitilingam, 2014). Present term investments can be

of more importance as it will earn interests to the investors which can be later used when and

where demanded and required. The investor re much more concerned with the existing value

of money because they want to trade now. Time value of money can be defined as the

demarcation line that the present and the future values of money have between them. Also,

the current value of money plays a key role in deciding the type of investments from their

superannuation contributions that one should undertake to get the maximum output

(Vaitilingam, 2014).

It is seen that the working staff of the companies invest a limited amount of their salary ion

superannuation funds till the date hey get money for their services. It is seen that this

collected money comes with some interest and the total amount is further invested to

maximize it. But it should also be known that this collected amount cannot be generated

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation

within a quick succession and takes a long time to summon up (Needles & Powers, 2013). So

it is advised that the employees investing the particular amount of money should make an

evaluation beforehand to make assumptions about the money they would receive in the

future. It is said that long terms will incur more benefits to the employees. But it is also

necessary that one has a well-attained knowledge about the investments he/she is making

without which it can happen that the invested money gets degraded because of the silly

decisions made without perfect knowledge (Merchant, 2012). It is advised that one should

have a strategic plan to make the maximum benefits out of the investment. It must also be

known that the investments knot always incur benefits because there can be a negative time

which has a downfall. The undertaking plans of the employees must be perfect to cater the

investments to their expectation. Also, the level of patience is very important because a high

level of patience is required in making the investment and getting its output. So it all depends

on the decisions that one makes in relation to the time value of money.

Recommendation

There is always a confusion prevailing as to buy the low price stocks or to sell the stocks

which are at their peak because both may change over time. Though a professional’s advice

may help generate some value decisions but overpowering the market is a totally different

thing and one can also see that they are gaining benefits from stocks that were vulnerable in

nature. As in the case of pension funds, it is the duty of the manager to deliver investment

mode which has better outputs. Different types of portfolios covering various areas and

ranges must be present in hand of the manager for a different choice of peoples. If all the

correct security measures and enhanced fund featured are tapped into the portfolio then the

pin risks can be successfully eliminated (Melville, 2013). But most of the cases are found

away from this category. Also, the existing tax rates should also be paid attention to by the

fund’s manager because individual tax condition changes the selections made. But this also

set the right path for the manager to maximize the output for its client.

7

within a quick succession and takes a long time to summon up (Needles & Powers, 2013). So

it is advised that the employees investing the particular amount of money should make an

evaluation beforehand to make assumptions about the money they would receive in the

future. It is said that long terms will incur more benefits to the employees. But it is also

necessary that one has a well-attained knowledge about the investments he/she is making

without which it can happen that the invested money gets degraded because of the silly

decisions made without perfect knowledge (Merchant, 2012). It is advised that one should

have a strategic plan to make the maximum benefits out of the investment. It must also be

known that the investments knot always incur benefits because there can be a negative time

which has a downfall. The undertaking plans of the employees must be perfect to cater the

investments to their expectation. Also, the level of patience is very important because a high

level of patience is required in making the investment and getting its output. So it all depends

on the decisions that one makes in relation to the time value of money.

Recommendation

There is always a confusion prevailing as to buy the low price stocks or to sell the stocks

which are at their peak because both may change over time. Though a professional’s advice

may help generate some value decisions but overpowering the market is a totally different

thing and one can also see that they are gaining benefits from stocks that were vulnerable in

nature. As in the case of pension funds, it is the duty of the manager to deliver investment

mode which has better outputs. Different types of portfolios covering various areas and

ranges must be present in hand of the manager for a different choice of peoples. If all the

correct security measures and enhanced fund featured are tapped into the portfolio then the

pin risks can be successfully eliminated (Melville, 2013). But most of the cases are found

away from this category. Also, the existing tax rates should also be paid attention to by the

fund’s manager because individual tax condition changes the selections made. But this also

set the right path for the manager to maximize the output for its client.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation

Conclusion

Efficient saving of money is done by the employees when they invest some part of their

earnings in the superannuation funds. This is not all because this process also helps them to

demarcate between Investment Choice Plan and Defined Choice Plan and to choose the one

which is perfect caters to their strategic plans. The time value of money theory is also an

essential one and it allows to choose the right mode of investment at the right time and to

maintain patience so that the outputs can be maximized and caters to the expectations. As in

relation to the EMH, it is advised that pin along with portfolios is not necessary for the fund

managers as they leave the whole process open for the pin risks which may either make

losses or gains to the user.

8

Conclusion

Efficient saving of money is done by the employees when they invest some part of their

earnings in the superannuation funds. This is not all because this process also helps them to

demarcate between Investment Choice Plan and Defined Choice Plan and to choose the one

which is perfect caters to their strategic plans. The time value of money theory is also an

essential one and it allows to choose the right mode of investment at the right time and to

maintain patience so that the outputs can be maximized and caters to the expectations. As in

relation to the EMH, it is advised that pin along with portfolios is not necessary for the fund

managers as they leave the whole process open for the pin risks which may either make

losses or gains to the user.

8

Superannuation

References

Kollmorgen , A. (2015) Superannuation fund performance and fees [online]. Available at:

https://www.choice.com.au/money/financial-planning-and-investing/superannuation/articles/

superannuation-funds-performance-and-fees-191115 [Accessed 11 May 2018]

Laux, B. (2014) Discussion of The role of revenue recognition in performance reporting.

Accounting and Business Research. [online]. 44(4), 380-382. Available from

Leo, K. J. (2011). Company Accounting. Boston:McGraw Hill

Marsh, C. (2009) Mastering financial management. Harlow: Financial Times Prentice Hall.

Melville, A. (2013) International Financial Reporting – A Practical Guide. 4th edition.

Pearson, Education Limited, UK

Merchant, K. A. (2012) Making Management Accounting Research More Useful. Pacific

Accounting Review. [online]. 24(3), 1-34. Available from

Needles, B.E & Powers, M. (2013) Principles of Financial Accounting. Financial Accounting

Series: Cengage Learning.

Needles, B.E. and Powers, M. (2013) Principles of Financial Accounting. Financial

Accounting Series: Cengage Learning.

Parrino, R, Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

Porter, G. and Norton, C. (2014) Financial Accounting: The Impact on Decision Maker.

Texas: Cengage Learning

Power, T. (2017) Fund choice: Comparing super funds in 8 steps [online]. Available at:

https://www.superguide.com.au/boost-your-superannuation/comparing-super-funds-in-8-

steps [Accessed 11 May 2018]

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

9

References

Kollmorgen , A. (2015) Superannuation fund performance and fees [online]. Available at:

https://www.choice.com.au/money/financial-planning-and-investing/superannuation/articles/

superannuation-funds-performance-and-fees-191115 [Accessed 11 May 2018]

Laux, B. (2014) Discussion of The role of revenue recognition in performance reporting.

Accounting and Business Research. [online]. 44(4), 380-382. Available from

Leo, K. J. (2011). Company Accounting. Boston:McGraw Hill

Marsh, C. (2009) Mastering financial management. Harlow: Financial Times Prentice Hall.

Melville, A. (2013) International Financial Reporting – A Practical Guide. 4th edition.

Pearson, Education Limited, UK

Merchant, K. A. (2012) Making Management Accounting Research More Useful. Pacific

Accounting Review. [online]. 24(3), 1-34. Available from

Needles, B.E & Powers, M. (2013) Principles of Financial Accounting. Financial Accounting

Series: Cengage Learning.

Needles, B.E. and Powers, M. (2013) Principles of Financial Accounting. Financial

Accounting Series: Cengage Learning.

Parrino, R, Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

Porter, G. and Norton, C. (2014) Financial Accounting: The Impact on Decision Maker.

Texas: Cengage Learning

Power, T. (2017) Fund choice: Comparing super funds in 8 steps [online]. Available at:

https://www.superguide.com.au/boost-your-superannuation/comparing-super-funds-in-8-

steps [Accessed 11 May 2018]

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall.

10

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.