ACCT2262 Superannuation & Retirement: A Detailed Case Study

VerifiedAdded on 2023/04/25

|14

|3592

|382

Case Study

AI Summary

This document presents a comprehensive case study focused on superannuation and retirement planning for a couple, Thomas and Jessica. Acting as a financial advisor, the solution assesses their current financial situation, goals, and objectives, and recommends a Transition to Retirement (TTR) strategy to optimize their retirement income and minimize tax implications. The analysis incorporates data from a client fact sheet and utilizes the MoneySmart calculator to project the outcomes of the proposed strategy, including superannuation fund requirements and retirement income projections. The solution details the rationale behind the TTR recommendation, highlighting its potential benefits in terms of reduced working hours, enhanced savings, and the ability to maintain their desired standard of living during retirement. Furthermore, the document includes superannuation planning considerations for both Thomas and Jessica, emphasizing the need to increase contributions to meet their retirement goals. Desklib provides students with access to similar case studies and solved assignments.

Running head: SUPERANNIUATION AND RETIREMENT

Superannuation and Retirement

Name of the Student:

Name of the University:

Author’s Note:

Superannuation and Retirement

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

SUPERANNIUATION AND RETIREMENT

Table of Contents

No table of contents entries found.

SUPERANNIUATION AND RETIREMENT

Table of Contents

No table of contents entries found.

2

SUPERANNIUATION AND RETIREMENT

Covering Letter

Thomas and Jessica

Address Line 1:

Address line 2:

Date:

Dear Thomas and Jessica

I would like to thank you for the opportunity for setting up this meeting for taking financial

advice from us.

From the meeting and also client sheet data all confidential information was made available to us

which provided a clear understanding of your situation, goals, objectives and also your attitude

towards an investment.

It is to be noted that from the information which was provided by you we have formulated a

Statement of Advice (SoA). The SoA would be consisting of recommendations regarding

different situations which shows your goals and objectives and also your attitude towards risks

related to investments and also returns which is expected by you. The SoA would be analyzing

all the supporting materials which is provided by you and on the basis of the same

recommendations is to be provided. In case, any details have been missed out or not considered

please bring the same to our notice so that appropriate amendments can be brought about in the

SoA.

It is also brought to your notice that if the SoA is not implemented within a period of 30 days

than revision needs to be made into the statement of advice. I would be thank you again for

choosing our services and we will be looking forward to assist you in any way in future as well.

Yours faithfully

SUPERANNIUATION AND RETIREMENT

Covering Letter

Thomas and Jessica

Address Line 1:

Address line 2:

Date:

Dear Thomas and Jessica

I would like to thank you for the opportunity for setting up this meeting for taking financial

advice from us.

From the meeting and also client sheet data all confidential information was made available to us

which provided a clear understanding of your situation, goals, objectives and also your attitude

towards an investment.

It is to be noted that from the information which was provided by you we have formulated a

Statement of Advice (SoA). The SoA would be consisting of recommendations regarding

different situations which shows your goals and objectives and also your attitude towards risks

related to investments and also returns which is expected by you. The SoA would be analyzing

all the supporting materials which is provided by you and on the basis of the same

recommendations is to be provided. In case, any details have been missed out or not considered

please bring the same to our notice so that appropriate amendments can be brought about in the

SoA.

It is also brought to your notice that if the SoA is not implemented within a period of 30 days

than revision needs to be made into the statement of advice. I would be thank you again for

choosing our services and we will be looking forward to assist you in any way in future as well.

Yours faithfully

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

SUPERANNIUATION AND RETIREMENT

Introduction

Role of an Advisor

The role of the adviser is to provide financial advice to the client and the objective of the

advisor is to ensure that the financial goals and objectives of the clients are given priority. The

advisor would be suggesting strategies and products so that the goals and objectives of the client

are fulfilled. The advisor would not act outside the scope of the client while providing advisory

services to the client. The advisor should have a bachelor’s degree and the specific financial

planning course qualification that would be sufficient in order to provide effective consultation.

It is to be also ensured that the financial planning course which should be registered with the

government of Australia.

Scope of Advice

The products and services which we are authorised to provide our opinion are financial

products which are normally Australian securities or International equities along with investment

options in balanced funds. We are also authorised to provide consultancy services to the clients

for mutual funds, shares and securities. The service of the consultant includes financial

consultation along with evaluation and assessment of the products where the clients have

undertaken investments in order to sustain their level of investment. The steps which would be

taken by use would be within the scope of services which the client want from us.

Reports aim

The report which is formulated has the following aims and objectives and the same are

listed below in details:

The report would be stating the roles and objectives of the clients along future

expectations of the clients.

The report would also be including recommendations which the client need to implement

so the goals and objectives of the clients can be achieved.

The report would be demonstrating financial projections which would be supporting the

recommendations provided.

SUPERANNIUATION AND RETIREMENT

Introduction

Role of an Advisor

The role of the adviser is to provide financial advice to the client and the objective of the

advisor is to ensure that the financial goals and objectives of the clients are given priority. The

advisor would be suggesting strategies and products so that the goals and objectives of the client

are fulfilled. The advisor would not act outside the scope of the client while providing advisory

services to the client. The advisor should have a bachelor’s degree and the specific financial

planning course qualification that would be sufficient in order to provide effective consultation.

It is to be also ensured that the financial planning course which should be registered with the

government of Australia.

Scope of Advice

The products and services which we are authorised to provide our opinion are financial

products which are normally Australian securities or International equities along with investment

options in balanced funds. We are also authorised to provide consultancy services to the clients

for mutual funds, shares and securities. The service of the consultant includes financial

consultation along with evaluation and assessment of the products where the clients have

undertaken investments in order to sustain their level of investment. The steps which would be

taken by use would be within the scope of services which the client want from us.

Reports aim

The report which is formulated has the following aims and objectives and the same are

listed below in details:

The report would be stating the roles and objectives of the clients along future

expectations of the clients.

The report would also be including recommendations which the client need to implement

so the goals and objectives of the clients can be achieved.

The report would be demonstrating financial projections which would be supporting the

recommendations provided.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

SUPERANNIUATION AND RETIREMENT

Discussion

Goals and Objectives

As per the information which is provided in the client fact sheet, the following are your

objectives and needs which you want to be fulfilled:

You want to make appropriate plans for your retirement and the plans needs to be

formulated considering a period of five years of time considering the financial year

2017/18.

To pay off the mortgage amount which is due on your home by the time of your

retirement and also save an amount of $ 55,000 for meeting your desire to purchase a

new car and also go on a holiday trip with your family.

You want the retirement planning to be in such a way that you have a retirement income

of $ 57,000 which would meet your expectations and needs.

You want to provide $ 40,000 to each one of your children so that they can have a saving

plan of their own.

In addition to this, you want to make changes with your super funds and in every step,

you want to ensure that your tax implications on the investments are low.

Current Situation

As per the current situation which is stated in the facts sheet shows that you are thinking

to plan your retirement for which you need adequate cash requirements in order to meet your

current standards of living. In addition to this, the fact sheet shows that you have income which

is based on salary income for both you Thomas and Jessica. Thomas, you are currently engaged

as electricians and you are currently self-employed while you, Jessica is engaged in a florist

business. As per the fact sheet which you have provided, Thomas you have a income of $

130,000 while you, Jessica have a income of $ 30,000. The major expenses which is incurred by

you are mostly mortgage expenses for the residence property and also the investment property.

In addition to this, you have a household expenses of total $ 42,000 which covers the total

expenses which is incurred by you both. A better presentation of the income and costs for both of

you is presented below:

SUPERANNIUATION AND RETIREMENT

Discussion

Goals and Objectives

As per the information which is provided in the client fact sheet, the following are your

objectives and needs which you want to be fulfilled:

You want to make appropriate plans for your retirement and the plans needs to be

formulated considering a period of five years of time considering the financial year

2017/18.

To pay off the mortgage amount which is due on your home by the time of your

retirement and also save an amount of $ 55,000 for meeting your desire to purchase a

new car and also go on a holiday trip with your family.

You want the retirement planning to be in such a way that you have a retirement income

of $ 57,000 which would meet your expectations and needs.

You want to provide $ 40,000 to each one of your children so that they can have a saving

plan of their own.

In addition to this, you want to make changes with your super funds and in every step,

you want to ensure that your tax implications on the investments are low.

Current Situation

As per the current situation which is stated in the facts sheet shows that you are thinking

to plan your retirement for which you need adequate cash requirements in order to meet your

current standards of living. In addition to this, the fact sheet shows that you have income which

is based on salary income for both you Thomas and Jessica. Thomas, you are currently engaged

as electricians and you are currently self-employed while you, Jessica is engaged in a florist

business. As per the fact sheet which you have provided, Thomas you have a income of $

130,000 while you, Jessica have a income of $ 30,000. The major expenses which is incurred by

you are mostly mortgage expenses for the residence property and also the investment property.

In addition to this, you have a household expenses of total $ 42,000 which covers the total

expenses which is incurred by you both. A better presentation of the income and costs for both of

you is presented below:

5

SUPERANNIUATION AND RETIREMENT

Current Position of Thomas and Jessica West

SUPERANNIUATION AND RETIREMENT

Current Position of Thomas and Jessica West

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

SUPERANNIUATION AND RETIREMENT

Particulars Thomas Jessica Total

Salary $ 130,000.00

$

30,000.00 $ 160,000.00

Investment Income (gross) $ 4,500.00

$

9,500.00 $ 14,000.00

Concessional Contributions Super -$ 10,000.00 -$ 10,000.00

Personal Income $ - $ - $ -

Other Income $ - $ - $ -

TAXABLE INCOME $ 124,500.00

$

39,500.00 $ 164,000.00

Income Tax (approx.) incl Medicare Levy $ 36,187.00

$

5,174.50 $ 41,361.50

Net Income $ 88,313.00

$

34,325.50 $ 122,638.50

EXPENDITURE

Mortgage principle home (approx.) $ 28,500.00

Mortgage investment property (approx.) $ 8,250.00

Household Expenses $ 42,000.00

TOTAL EXPENDITURE (approx..) $ 78,750.00

Annual Income Surplus/Deficit $ 43,888.50

As per your requirement, you needed a monthly income of $ 79,000 which is not

currently meeting as per the presentation which is provided above. In addition to this, you have

specified that you would be requiring a sum of $ 57,000 after your retirement for maintaining

your current standard of living. As per the discussion we had earlier, it is clear that you want to

lower that amount of taxes which is paid by you on your earnings. This would be considered in

the recommendations which I would be developing for you. The forecast above shows that you

are meet up with your obligations effectively but are not able to maintain the required revenue

which you are expecting. This shows that you are currently not meeting the expectations which

you have set and therefore consideration is required to be made in the area. Therefore, this is an

area where you would be requiring advices in order to improve your current situation and also

appropriately make provisions for your future.

As per your asset positioning in the fact sheet which you have presented effectively

shows all the assets which you have including the investment property. The fact sheet also shows

the investments which you have made in your respective super funds and also the insurance

coverage which is provided by the same. The analysis of your position reveals that you require

SUPERANNIUATION AND RETIREMENT

Particulars Thomas Jessica Total

Salary $ 130,000.00

$

30,000.00 $ 160,000.00

Investment Income (gross) $ 4,500.00

$

9,500.00 $ 14,000.00

Concessional Contributions Super -$ 10,000.00 -$ 10,000.00

Personal Income $ - $ - $ -

Other Income $ - $ - $ -

TAXABLE INCOME $ 124,500.00

$

39,500.00 $ 164,000.00

Income Tax (approx.) incl Medicare Levy $ 36,187.00

$

5,174.50 $ 41,361.50

Net Income $ 88,313.00

$

34,325.50 $ 122,638.50

EXPENDITURE

Mortgage principle home (approx.) $ 28,500.00

Mortgage investment property (approx.) $ 8,250.00

Household Expenses $ 42,000.00

TOTAL EXPENDITURE (approx..) $ 78,750.00

Annual Income Surplus/Deficit $ 43,888.50

As per your requirement, you needed a monthly income of $ 79,000 which is not

currently meeting as per the presentation which is provided above. In addition to this, you have

specified that you would be requiring a sum of $ 57,000 after your retirement for maintaining

your current standard of living. As per the discussion we had earlier, it is clear that you want to

lower that amount of taxes which is paid by you on your earnings. This would be considered in

the recommendations which I would be developing for you. The forecast above shows that you

are meet up with your obligations effectively but are not able to maintain the required revenue

which you are expecting. This shows that you are currently not meeting the expectations which

you have set and therefore consideration is required to be made in the area. Therefore, this is an

area where you would be requiring advices in order to improve your current situation and also

appropriately make provisions for your future.

As per your asset positioning in the fact sheet which you have presented effectively

shows all the assets which you have including the investment property. The fact sheet also shows

the investments which you have made in your respective super funds and also the insurance

coverage which is provided by the same. The analysis of your position reveals that you require

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

SUPERANNIUATION AND RETIREMENT

financial advice regarding retirement planning and also improve the net income so that a proper

standard of living can be maintained.

Proposed Strategy

I have analysed your financial situation and also considered the objectives and needs

which you have for future. I would like to suggest the Transition to Retirement option for your

case. This option requires the applicants to reach their preservation age. In your case, both of you

have reached your preservation age and therefore as per my opinion this option would be most

appropriate as this would help in improving your current position and also enhancing your future

position effectively.

In order to establish a TTR pension fund and transfer a portion from super fund into the

same. It would also be wise to keep a small portion of your savings in super funds so that

employer contribution and other contribution which you can make can be saved appropriately.

The option of TTR requires the clients to deposit a sum from the super fund in the pension fund

established. The TTR scheme would allow you to work for lesser working hours during these

five years period till retirement and appropriately contribute to your income. As per the current

situation of the market, you can expect a return between 4% to 10%. As per my opinion this

would help you to meet the net income requirement and also help in retirement period planning.

The TTR scheme though would be taking a portion of your savings in present but as your

retirement requirement is quite I anticipate that the same would be enough to meet you needs. As

per the information which you provided in the fact sheet, the after-retirement income which you

want to maintain is $ 57,000 and I believe that the same would be possible with TTR Scheme.

The only consideration which needs to be taken into account is that you would be having lesser

amount of funds in hand at the time of your retirement. But in my opinion that would be fine as

your requirement is not much and you would also be having some savings which would be

generated from your contributions and your employee contribution to your super funds. The

reasons due which I am suggesting TTR scheme is that the scheme has significant benefits such

as reduced working hours, appropriate savings during the time of retirement. The most important

reason which made me consider the TTR option as appropriate is after considering your current

needs and your expectations of a standard of living. The TTR option would enable you to

achieve the expected income marker in yearly basis and therefore you would be able to maintain

SUPERANNIUATION AND RETIREMENT

financial advice regarding retirement planning and also improve the net income so that a proper

standard of living can be maintained.

Proposed Strategy

I have analysed your financial situation and also considered the objectives and needs

which you have for future. I would like to suggest the Transition to Retirement option for your

case. This option requires the applicants to reach their preservation age. In your case, both of you

have reached your preservation age and therefore as per my opinion this option would be most

appropriate as this would help in improving your current position and also enhancing your future

position effectively.

In order to establish a TTR pension fund and transfer a portion from super fund into the

same. It would also be wise to keep a small portion of your savings in super funds so that

employer contribution and other contribution which you can make can be saved appropriately.

The option of TTR requires the clients to deposit a sum from the super fund in the pension fund

established. The TTR scheme would allow you to work for lesser working hours during these

five years period till retirement and appropriately contribute to your income. As per the current

situation of the market, you can expect a return between 4% to 10%. As per my opinion this

would help you to meet the net income requirement and also help in retirement period planning.

The TTR scheme though would be taking a portion of your savings in present but as your

retirement requirement is quite I anticipate that the same would be enough to meet you needs. As

per the information which you provided in the fact sheet, the after-retirement income which you

want to maintain is $ 57,000 and I believe that the same would be possible with TTR Scheme.

The only consideration which needs to be taken into account is that you would be having lesser

amount of funds in hand at the time of your retirement. But in my opinion that would be fine as

your requirement is not much and you would also be having some savings which would be

generated from your contributions and your employee contribution to your super funds. The

reasons due which I am suggesting TTR scheme is that the scheme has significant benefits such

as reduced working hours, appropriate savings during the time of retirement. The most important

reason which made me consider the TTR option as appropriate is after considering your current

needs and your expectations of a standard of living. The TTR option would enable you to

achieve the expected income marker in yearly basis and therefore you would be able to maintain

8

SUPERANNIUATION AND RETIREMENT

your desired standard of Living. In addition to this judgement from the nature of investments

which you like to undertake, I believe that you both follow a balanced type approach while

making investments.

Money Smart Calculator

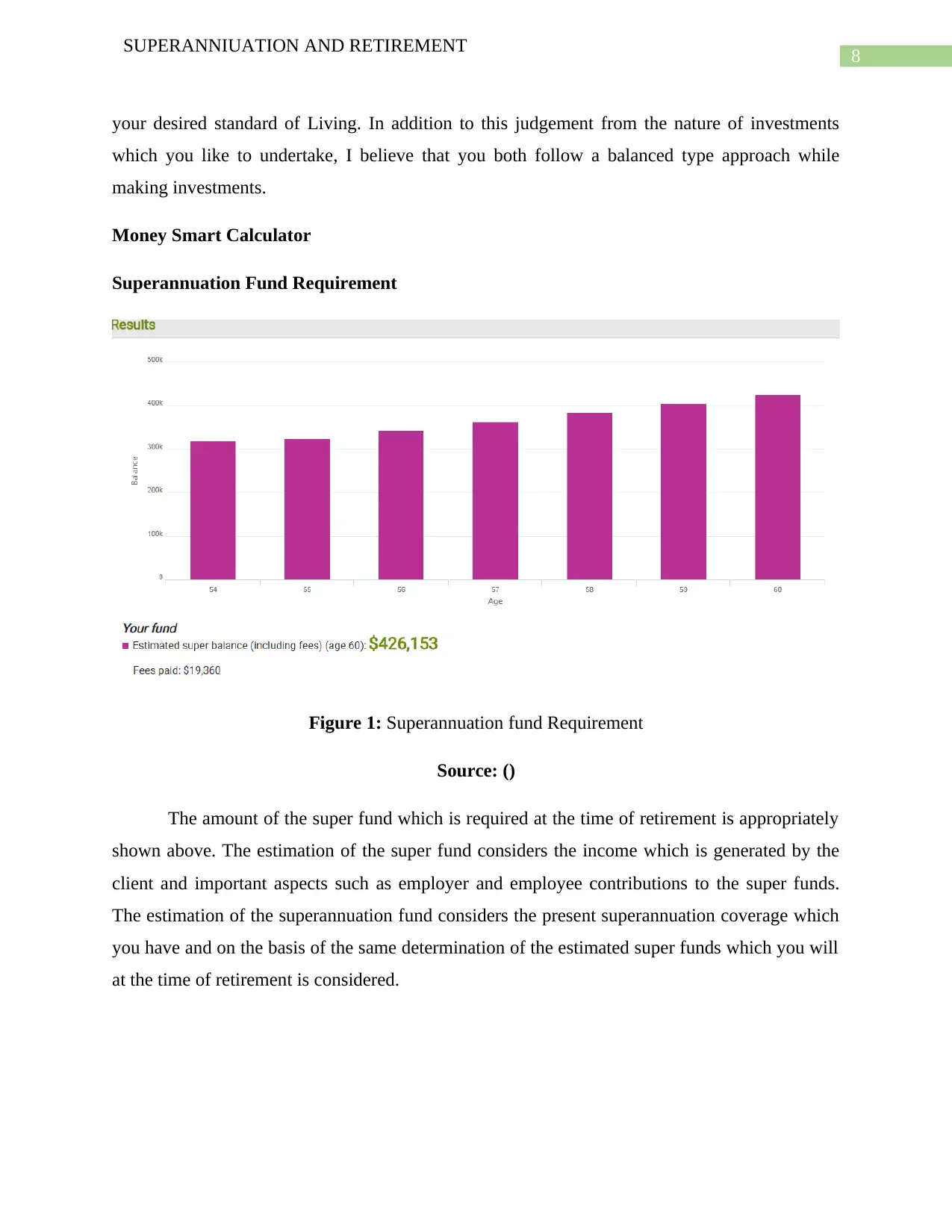

Superannuation Fund Requirement

Figure 1: Superannuation fund Requirement

Source: ()

The amount of the super fund which is required at the time of retirement is appropriately

shown above. The estimation of the super fund considers the income which is generated by the

client and important aspects such as employer and employee contributions to the super funds.

The estimation of the superannuation fund considers the present superannuation coverage which

you have and on the basis of the same determination of the estimated super funds which you will

at the time of retirement is considered.

SUPERANNIUATION AND RETIREMENT

your desired standard of Living. In addition to this judgement from the nature of investments

which you like to undertake, I believe that you both follow a balanced type approach while

making investments.

Money Smart Calculator

Superannuation Fund Requirement

Figure 1: Superannuation fund Requirement

Source: ()

The amount of the super fund which is required at the time of retirement is appropriately

shown above. The estimation of the super fund considers the income which is generated by the

client and important aspects such as employer and employee contributions to the super funds.

The estimation of the superannuation fund considers the present superannuation coverage which

you have and on the basis of the same determination of the estimated super funds which you will

at the time of retirement is considered.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

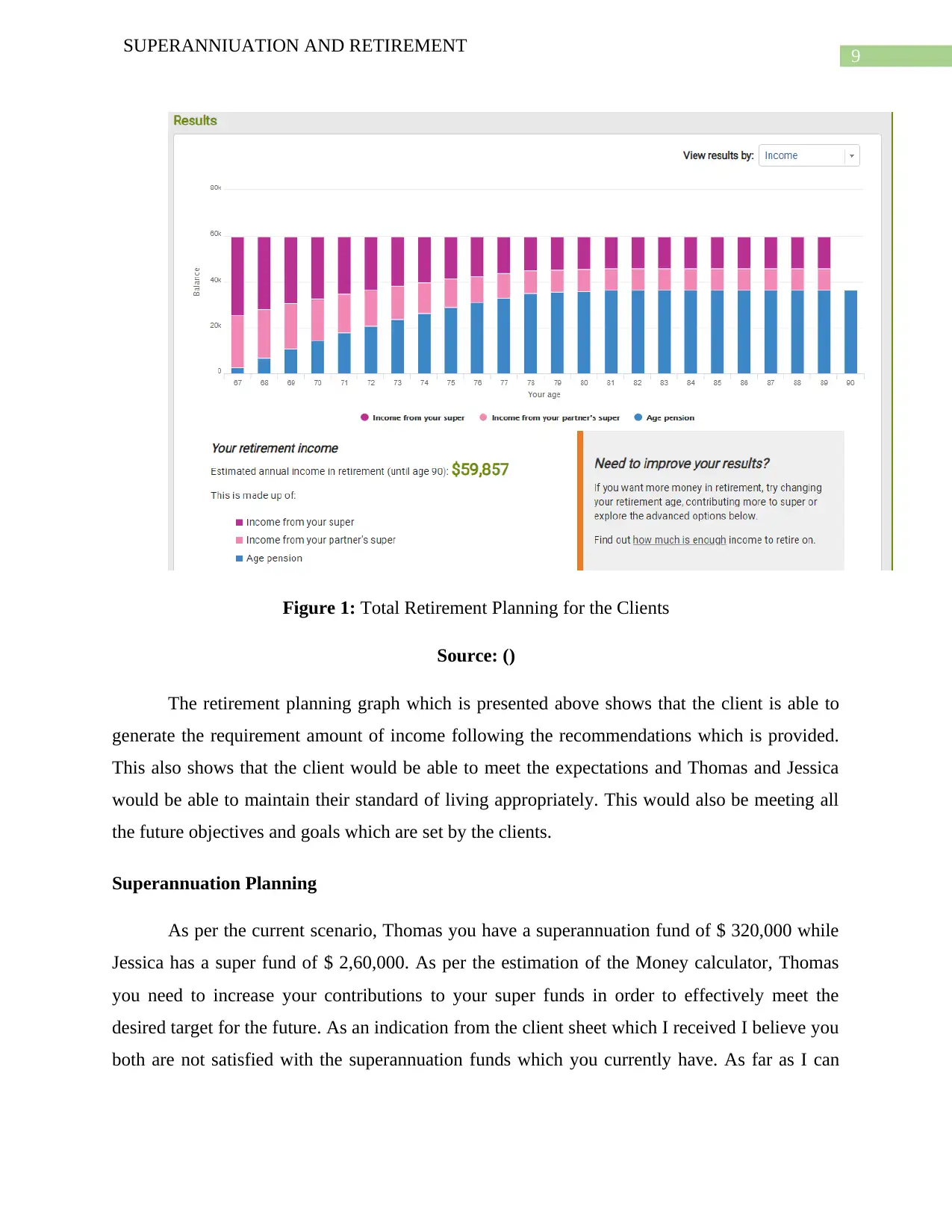

SUPERANNIUATION AND RETIREMENT

Figure 1: Total Retirement Planning for the Clients

Source: ()

The retirement planning graph which is presented above shows that the client is able to

generate the requirement amount of income following the recommendations which is provided.

This also shows that the client would be able to meet the expectations and Thomas and Jessica

would be able to maintain their standard of living appropriately. This would also be meeting all

the future objectives and goals which are set by the clients.

Superannuation Planning

As per the current scenario, Thomas you have a superannuation fund of $ 320,000 while

Jessica has a super fund of $ 2,60,000. As per the estimation of the Money calculator, Thomas

you need to increase your contributions to your super funds in order to effectively meet the

desired target for the future. As an indication from the client sheet which I received I believe you

both are not satisfied with the superannuation funds which you currently have. As far as I can

SUPERANNIUATION AND RETIREMENT

Figure 1: Total Retirement Planning for the Clients

Source: ()

The retirement planning graph which is presented above shows that the client is able to

generate the requirement amount of income following the recommendations which is provided.

This also shows that the client would be able to meet the expectations and Thomas and Jessica

would be able to maintain their standard of living appropriately. This would also be meeting all

the future objectives and goals which are set by the clients.

Superannuation Planning

As per the current scenario, Thomas you have a superannuation fund of $ 320,000 while

Jessica has a super fund of $ 2,60,000. As per the estimation of the Money calculator, Thomas

you need to increase your contributions to your super funds in order to effectively meet the

desired target for the future. As an indication from the client sheet which I received I believe you

both are not satisfied with the superannuation funds which you currently have. As far as I can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

SUPERANNIUATION AND RETIREMENT

understand, this is mainly due to the low coverage which you are getting and also because of the

tax consideration which is associated with the funds.

Thomas, you are self employed and therefore you have to manage your own funds and as

per the fact sheet most of the contributions are done by yourself for an amount of $ 10,000.

While in your case Jessica, your contribution to the super fund is $ 2,850. Now, there is a thing

which I would like to explain to you guys regarding superannuation funds. I believe that your

products are appropriate but you need to increase your contribution to the fund in order to

effectively save up appropriate cash which would be necessary for guys to maintain for the

future. There is a also a option of concessional super contribution which can help you to

effectively keep the tax liabilities concerning super funds limited. One of the concessional super

payments is the employer’s contribution to the superannuation funds which is not applicable in

your case Thomas as you are self-employed. The other popular option available to you is salary

sacrifice arrangements which can help you both to save a portion of your salary which would be

then be applicable to tax at a concessional rate or 15%. Salary sacrifice is an option which is

available to you both which allows you to keep out a portion of your salary which is pre-taxed

and the same can be contributed to your superannuation fund and the same would be treated as

concessional payments which is made by you. I would like to recommend this system to you as I

believe that this would help you to set up an appropriate fund for your retirement and also lead to

considerable amount of savings in the present. I would suggest to you Thomas that you proceed

with a salary sacrifice of $ 10,000 from your gross earnings while Jessica you would be

sacrificing an amount of $ 5,000 from your gross wages. This would be taken out from your

gross wages before any tax claims are made on the same. The regulations which have been

introduced in respect of super contribution would treat your contributions as concessional

contribution thereby lower rate of tax would be applied on the same. It is also to be noted that the

maximum contribution which you can make in such an option is $ 25,000 above which

concessional rate of taxation would not be applicable. In order to effectively show the outcomes

which, you can expect when you implement this salary sacrifice option, I have presented an

estimated forecast for your situation for the purpose of better analysis for your situation. The

forecast summarising your situation for now and when you adopt the salary sacrifice plan is

presented below:

SUPERANNIUATION AND RETIREMENT

understand, this is mainly due to the low coverage which you are getting and also because of the

tax consideration which is associated with the funds.

Thomas, you are self employed and therefore you have to manage your own funds and as

per the fact sheet most of the contributions are done by yourself for an amount of $ 10,000.

While in your case Jessica, your contribution to the super fund is $ 2,850. Now, there is a thing

which I would like to explain to you guys regarding superannuation funds. I believe that your

products are appropriate but you need to increase your contribution to the fund in order to

effectively save up appropriate cash which would be necessary for guys to maintain for the

future. There is a also a option of concessional super contribution which can help you to

effectively keep the tax liabilities concerning super funds limited. One of the concessional super

payments is the employer’s contribution to the superannuation funds which is not applicable in

your case Thomas as you are self-employed. The other popular option available to you is salary

sacrifice arrangements which can help you both to save a portion of your salary which would be

then be applicable to tax at a concessional rate or 15%. Salary sacrifice is an option which is

available to you both which allows you to keep out a portion of your salary which is pre-taxed

and the same can be contributed to your superannuation fund and the same would be treated as

concessional payments which is made by you. I would like to recommend this system to you as I

believe that this would help you to set up an appropriate fund for your retirement and also lead to

considerable amount of savings in the present. I would suggest to you Thomas that you proceed

with a salary sacrifice of $ 10,000 from your gross earnings while Jessica you would be

sacrificing an amount of $ 5,000 from your gross wages. This would be taken out from your

gross wages before any tax claims are made on the same. The regulations which have been

introduced in respect of super contribution would treat your contributions as concessional

contribution thereby lower rate of tax would be applied on the same. It is also to be noted that the

maximum contribution which you can make in such an option is $ 25,000 above which

concessional rate of taxation would not be applicable. In order to effectively show the outcomes

which, you can expect when you implement this salary sacrifice option, I have presented an

estimated forecast for your situation for the purpose of better analysis for your situation. The

forecast summarising your situation for now and when you adopt the salary sacrifice plan is

presented below:

11

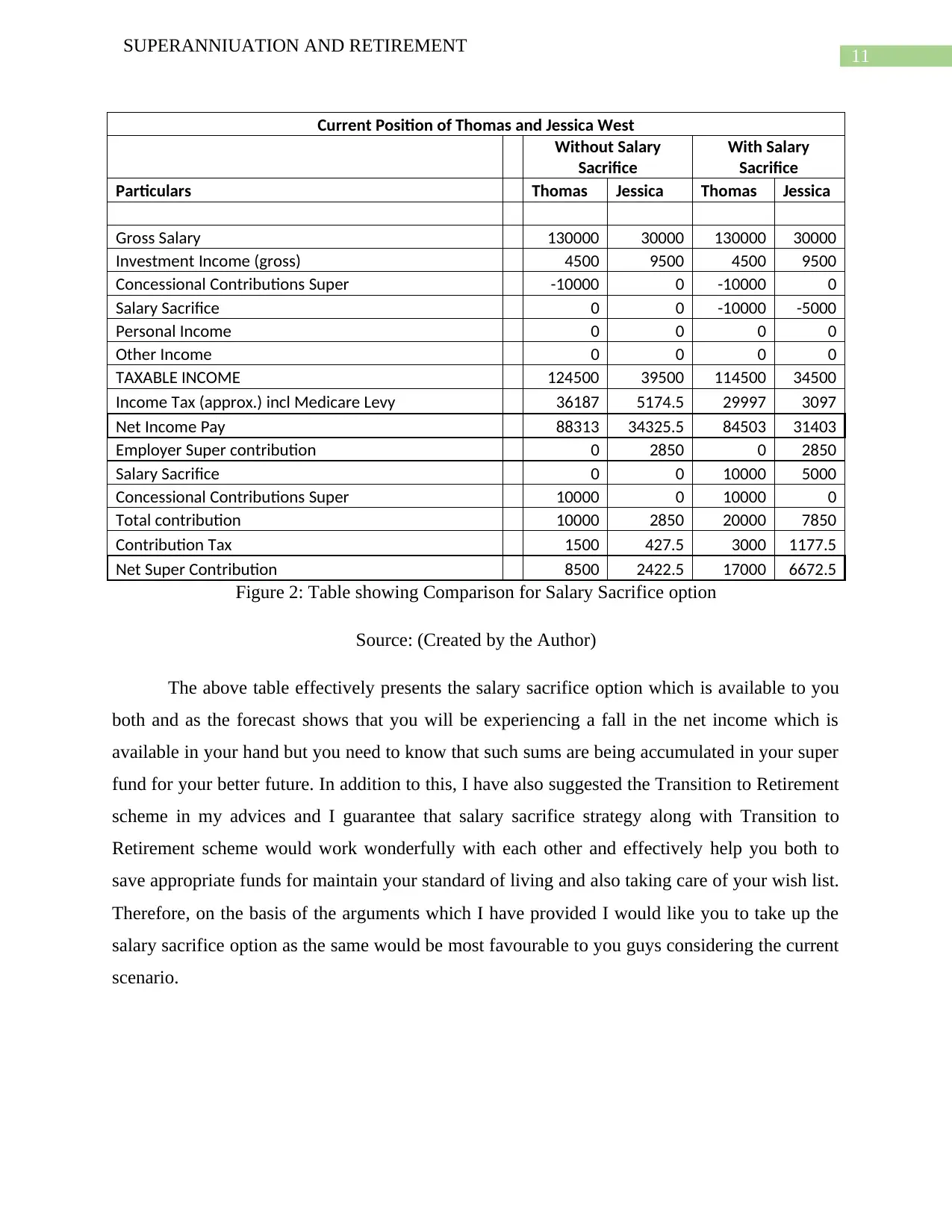

SUPERANNIUATION AND RETIREMENT

Current Position of Thomas and Jessica West

Without Salary

Sacrifice

With Salary

Sacrifice

Particulars Thomas Jessica Thomas Jessica

Gross Salary 130000 30000 130000 30000

Investment Income (gross) 4500 9500 4500 9500

Concessional Contributions Super -10000 0 -10000 0

Salary Sacrifice 0 0 -10000 -5000

Personal Income 0 0 0 0

Other Income 0 0 0 0

TAXABLE INCOME 124500 39500 114500 34500

Income Tax (approx.) incl Medicare Levy 36187 5174.5 29997 3097

Net Income Pay 88313 34325.5 84503 31403

Employer Super contribution 0 2850 0 2850

Salary Sacrifice 0 0 10000 5000

Concessional Contributions Super 10000 0 10000 0

Total contribution 10000 2850 20000 7850

Contribution Tax 1500 427.5 3000 1177.5

Net Super Contribution 8500 2422.5 17000 6672.5

Figure 2: Table showing Comparison for Salary Sacrifice option

Source: (Created by the Author)

The above table effectively presents the salary sacrifice option which is available to you

both and as the forecast shows that you will be experiencing a fall in the net income which is

available in your hand but you need to know that such sums are being accumulated in your super

fund for your better future. In addition to this, I have also suggested the Transition to Retirement

scheme in my advices and I guarantee that salary sacrifice strategy along with Transition to

Retirement scheme would work wonderfully with each other and effectively help you both to

save appropriate funds for maintain your standard of living and also taking care of your wish list.

Therefore, on the basis of the arguments which I have provided I would like you to take up the

salary sacrifice option as the same would be most favourable to you guys considering the current

scenario.

SUPERANNIUATION AND RETIREMENT

Current Position of Thomas and Jessica West

Without Salary

Sacrifice

With Salary

Sacrifice

Particulars Thomas Jessica Thomas Jessica

Gross Salary 130000 30000 130000 30000

Investment Income (gross) 4500 9500 4500 9500

Concessional Contributions Super -10000 0 -10000 0

Salary Sacrifice 0 0 -10000 -5000

Personal Income 0 0 0 0

Other Income 0 0 0 0

TAXABLE INCOME 124500 39500 114500 34500

Income Tax (approx.) incl Medicare Levy 36187 5174.5 29997 3097

Net Income Pay 88313 34325.5 84503 31403

Employer Super contribution 0 2850 0 2850

Salary Sacrifice 0 0 10000 5000

Concessional Contributions Super 10000 0 10000 0

Total contribution 10000 2850 20000 7850

Contribution Tax 1500 427.5 3000 1177.5

Net Super Contribution 8500 2422.5 17000 6672.5

Figure 2: Table showing Comparison for Salary Sacrifice option

Source: (Created by the Author)

The above table effectively presents the salary sacrifice option which is available to you

both and as the forecast shows that you will be experiencing a fall in the net income which is

available in your hand but you need to know that such sums are being accumulated in your super

fund for your better future. In addition to this, I have also suggested the Transition to Retirement

scheme in my advices and I guarantee that salary sacrifice strategy along with Transition to

Retirement scheme would work wonderfully with each other and effectively help you both to

save appropriate funds for maintain your standard of living and also taking care of your wish list.

Therefore, on the basis of the arguments which I have provided I would like you to take up the

salary sacrifice option as the same would be most favourable to you guys considering the current

scenario.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.