Retirement Planning: Superannuation Advice for Sutton Family Case

VerifiedAdded on 2023/06/05

|27

|9610

|107

Case Study

AI Summary

This case study presents a financial plan for Graham and Anna Sutton, who are seeking advice on managing their wealth for retirement. Graham, a mining engineer, and Anna, a personal assistant, aim to retire in nine years and maintain their current lifestyle. The advice includes strategies for managing their self-managed super fund (SMSF), property investments, and other assets to achieve a post-retirement income of $125,000 per year. The plan considers their risk profile, estate planning, and cash flow projections, as well as aged care considerations for Anna's mother. Recommendations focus on dividend income, safe investment options, and asset allocation to ensure a secure and comfortable retirement.

Page1

SUPERANNUATION AND RETIREMENT ADVICE

Letter to Client

18 September 2018

Mr Graham Sutton and Ms Anna Sutton

1, White Ave, Wollongong NSW 2550

Dear Graham and Anna,

I, Jess Craig, Senior Financial Planner associated with All Out Financial Planning

welcome you to the boutique financial planning and advising company in NSW. I thank

you on behalf of All Out Financial Planning for giving us this opportunity to resolve

your financial situation and to offer our most professional and sincere advice for your

post-retirement financial needs. A copy of our valuable Financial Service Guide was

presented to you on your first visit to our office, I am sure you must have taken out

some of your time for studying it.

I assure you that our final Statement of Advice (SoA), which will be based on facts and

financial data provided by you, will meet your required future goals. We will make this

SoA appropriate for your post-retirement needs and will advise you sincerely about your

objectives, as specifically desired by you. I would like to reiterate that the SoA should

be considered as a personal financial advice which has been prepared to meet your

financial objectives. All information about our fees, commission and other interests or

associations helpful to your objectives has also been included in the SoA.

We are also providing you our Product Disclosure Statement (PDS) containing various

financial products which you may find purposeful. We can also arrange for you any

specific financial product that you would like to recommend. We are confident that

information provided in the PDS will not only guide you in making the right choice, it

will also help you in taking the right decision about the most suitable product.

SUPERANNUATION AND RETIREMENT ADVICE

Letter to Client

18 September 2018

Mr Graham Sutton and Ms Anna Sutton

1, White Ave, Wollongong NSW 2550

Dear Graham and Anna,

I, Jess Craig, Senior Financial Planner associated with All Out Financial Planning

welcome you to the boutique financial planning and advising company in NSW. I thank

you on behalf of All Out Financial Planning for giving us this opportunity to resolve

your financial situation and to offer our most professional and sincere advice for your

post-retirement financial needs. A copy of our valuable Financial Service Guide was

presented to you on your first visit to our office, I am sure you must have taken out

some of your time for studying it.

I assure you that our final Statement of Advice (SoA), which will be based on facts and

financial data provided by you, will meet your required future goals. We will make this

SoA appropriate for your post-retirement needs and will advise you sincerely about your

objectives, as specifically desired by you. I would like to reiterate that the SoA should

be considered as a personal financial advice which has been prepared to meet your

financial objectives. All information about our fees, commission and other interests or

associations helpful to your objectives has also been included in the SoA.

We are also providing you our Product Disclosure Statement (PDS) containing various

financial products which you may find purposeful. We can also arrange for you any

specific financial product that you would like to recommend. We are confident that

information provided in the PDS will not only guide you in making the right choice, it

will also help you in taking the right decision about the most suitable product.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page2

Please note that since this SoA has been prepared on the basis of the data and facts

given by you, the outcome and impact of the SoA will depend largely on the

authenticity and correctness of that information. Hence, we request you to ensure that

the data and facts given by you are complete and accurate. We also request you to

assess this SoA’s appropriateness in relation to your personal circumstances, before you

decide to act upon the advice given in it.

I also have noted the latest development in your and Anna’s careers. This, along with

the fact that you are planning to make estate planning arrangements when you move to

Perth, is an important financial aspect worth considering and which is discussed in this

SoA. I also noted that you do not feel comfortable in discussing details of social security

entitlements, hence I have tried to explain them in easy terms. The most important

aspect which is of concern for you at this stage is about your and Anna’s income

prospects post-retirement. I have paid special attention to this issue by providing most

relevant advice in the SoA.

Since the financial assumptions, benefits and gains which I have discussed in the SoA

have a short life, the validity of my advice is limited to a three month period. To further

discuss your long term future financial position, my advice will be to arrange another

meeting once you have thoroughly studied the attached SoA. Please feel free in

contacting if any further clarification is required of me.

Looking forward towards a long association in the coming years,

Yours Sincerely,

Jess Craig

Please note that since this SoA has been prepared on the basis of the data and facts

given by you, the outcome and impact of the SoA will depend largely on the

authenticity and correctness of that information. Hence, we request you to ensure that

the data and facts given by you are complete and accurate. We also request you to

assess this SoA’s appropriateness in relation to your personal circumstances, before you

decide to act upon the advice given in it.

I also have noted the latest development in your and Anna’s careers. This, along with

the fact that you are planning to make estate planning arrangements when you move to

Perth, is an important financial aspect worth considering and which is discussed in this

SoA. I also noted that you do not feel comfortable in discussing details of social security

entitlements, hence I have tried to explain them in easy terms. The most important

aspect which is of concern for you at this stage is about your and Anna’s income

prospects post-retirement. I have paid special attention to this issue by providing most

relevant advice in the SoA.

Since the financial assumptions, benefits and gains which I have discussed in the SoA

have a short life, the validity of my advice is limited to a three month period. To further

discuss your long term future financial position, my advice will be to arrange another

meeting once you have thoroughly studied the attached SoA. Please feel free in

contacting if any further clarification is required of me.

Looking forward towards a long association in the coming years,

Yours Sincerely,

Jess Craig

Page3

STATEMENT OF ADVISE

Executive Summary

Graham Sutton, a Mining Engineer by profession and his wife Anna

Sutton are seeking advice from an expert planning advisor about

managing their wealth for their post-retirement period which will be

nine years from now. Graham has plans start his own self-

managed super fund (SMSF) so that he can keep all their investments in

a composite investment plan earning them 6% net of taxes, fees and

charges. My advice to Graham and Anna is not to dispose off any of their

properties, which are giving them good income. With their current

investments in their own self-managed Super fund, giving them net of

6%. Their annual earning can be of $125,000 in the post-retirement

period and along with their super savings will add up to $2 million,

which at 6% net would give them $125,000 pa, which is more than they

plan to spend on post retirement living expenses.

Superannuati on and

Reti rement Advise

STATEMENT OF ADVISE

Executive Summary

Graham Sutton, a Mining Engineer by profession and his wife Anna

Sutton are seeking advice from an expert planning advisor about

managing their wealth for their post-retirement period which will be

nine years from now. Graham has plans start his own self-

managed super fund (SMSF) so that he can keep all their investments in

a composite investment plan earning them 6% net of taxes, fees and

charges. My advice to Graham and Anna is not to dispose off any of their

properties, which are giving them good income. With their current

investments in their own self-managed Super fund, giving them net of

6%. Their annual earning can be of $125,000 in the post-retirement

period and along with their super savings will add up to $2 million,

which at 6% net would give them $125,000 pa, which is more than they

plan to spend on post retirement living expenses.

Superannuati on and

Reti rement Advise

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page4

Table of Contents

Personal Details...............................................................................................................6

Financial Details..............................................................................................................7

Client’s Future Objectives..............................................................................................8

Client’s Financial Plan....................................................................................................9

Dividend Income..........................................................................................................9

01. Dividends Earned on Stock..........................................................................9

02. Dividends Earned on Funds.......................................................................10

03. Closed End Funds.......................................................................................10

Client’s Current Situation............................................................................................10

Graham’s Redundancy..............................................................................................10

Graham’s Superannuation........................................................................................10

Anna’s Superannuation.............................................................................................11

Investment Properties................................................................................................11

Graham’s & Anna’s Insurances...............................................................................11

Client’s Investment Planning.......................................................................................11

Interest income...........................................................................................................11

Other Safe Investment Options................................................................................12

01. Savings Bank Accounts...............................................................................12

02. Money Market Funds.................................................................................13

03. Government Securities................................................................................13

04. Real Estate Investment Trusts (REITs)....................................................13

05. Preferred Stocks..........................................................................................13

06. Retirement Income Funds..........................................................................14

High Yield Investments.............................................................................................14

Table of Contents

Personal Details...............................................................................................................6

Financial Details..............................................................................................................7

Client’s Future Objectives..............................................................................................8

Client’s Financial Plan....................................................................................................9

Dividend Income..........................................................................................................9

01. Dividends Earned on Stock..........................................................................9

02. Dividends Earned on Funds.......................................................................10

03. Closed End Funds.......................................................................................10

Client’s Current Situation............................................................................................10

Graham’s Redundancy..............................................................................................10

Graham’s Superannuation........................................................................................10

Anna’s Superannuation.............................................................................................11

Investment Properties................................................................................................11

Graham’s & Anna’s Insurances...............................................................................11

Client’s Investment Planning.......................................................................................11

Interest income...........................................................................................................11

Other Safe Investment Options................................................................................12

01. Savings Bank Accounts...............................................................................12

02. Money Market Funds.................................................................................13

03. Government Securities................................................................................13

04. Real Estate Investment Trusts (REITs)....................................................13

05. Preferred Stocks..........................................................................................13

06. Retirement Income Funds..........................................................................14

High Yield Investments.............................................................................................14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page5

Variable Investment Income.....................................................................................14

Guaranteed Investment Income...............................................................................16

Client’s Risk Profile......................................................................................................16

01. Conservative................................................................................................17

02. Cautious.......................................................................................................17

03. Moderate......................................................................................................17

04. Moderately Aggressive................................................................................17

05. Aggressive....................................................................................................17

Recommendation.......................................................................................................17

Client’s Strategy for Asset Allocation..........................................................................17

Client’s Estate Planning and Risk Management........................................................18

Conservative...............................................................................................................19

Moderate.....................................................................................................................19

Aggressive...................................................................................................................19

Client’s Cash Flow Projections....................................................................................20

Graham’s & Anna’s Retirement Plans........................................................................20

Anna’s mother Marie – Aged Care Considerations...................................................21

Advice on Goals and Strategies....................................................................................21

Goals to be achieved..................................................................................................21

Strategies Required....................................................................................................22

LIST OF REFERENCES..............................................................................................25

Variable Investment Income.....................................................................................14

Guaranteed Investment Income...............................................................................16

Client’s Risk Profile......................................................................................................16

01. Conservative................................................................................................17

02. Cautious.......................................................................................................17

03. Moderate......................................................................................................17

04. Moderately Aggressive................................................................................17

05. Aggressive....................................................................................................17

Recommendation.......................................................................................................17

Client’s Strategy for Asset Allocation..........................................................................17

Client’s Estate Planning and Risk Management........................................................18

Conservative...............................................................................................................19

Moderate.....................................................................................................................19

Aggressive...................................................................................................................19

Client’s Cash Flow Projections....................................................................................20

Graham’s & Anna’s Retirement Plans........................................................................20

Anna’s mother Marie – Aged Care Considerations...................................................21

Advice on Goals and Strategies....................................................................................21

Goals to be achieved..................................................................................................21

Strategies Required....................................................................................................22

LIST OF REFERENCES..............................................................................................25

Page6

STATEMENT OF ADVICE

Personal Details

Graham Sutton and Anna Sutton, aged 53 and 51 respectively, were married some 25

years ago. They have two school going children, Sam, aged 15 years and Jodie, aged 13

years. Graham and Anna are keeping good health and are non-smokers. Both carry life

insurance from independent sources and also through their respective Super Funds.

Graham has been employed as a Senior Mining Engineer with BlueScope Steel for 26

years. He has been offered redundancy by BlueScope due structural changes in the

company and has already been offered employment in Pilbara Port Corporation in

Western Australia as Site Engineer on same salary. Anna, who has been devoting

herself to fulltime care of their two children, has also taken the offer of employment

from All Brains Inc. in Perth as Personal Assistant to the Development Manager of the

company and will be joining in three month time.

Presently aged 53 and 51 years respectively, Graham and Anna plan to retire when

Graham reaches 62 years of age. They are seeking professional advice about their post-

retirement life so that they lead a secure and comfortable future for themselves as well

as their children whom they wish to support till they attain age of 24 years.

Personal Details of Mr. Graham Sutton and Ms. Anna Sutton

Name Graham Sutton Anna Sutton

Date of birth 06 October 1965 18 September 1963

Family Self, Wife & Two Children Self, Husband & Two Children

Marital Status Married Married

Occupation Salaried Employee-Engineer Personal Assistant

Employer Pilbara Port Corporation All Brains Inc.

Date of Joining 01 November 2018 1 December 2018

Salary Income $195,000 per annum (Gross) $52,000 per annum (Gross)

Interest Income $2,500 (On-line Savings Account) $2,500 (On-line Savings Account)

Income from

Rental Property $53,400 (Gross) $15,600 (Gross)

STATEMENT OF ADVICE

Personal Details

Graham Sutton and Anna Sutton, aged 53 and 51 respectively, were married some 25

years ago. They have two school going children, Sam, aged 15 years and Jodie, aged 13

years. Graham and Anna are keeping good health and are non-smokers. Both carry life

insurance from independent sources and also through their respective Super Funds.

Graham has been employed as a Senior Mining Engineer with BlueScope Steel for 26

years. He has been offered redundancy by BlueScope due structural changes in the

company and has already been offered employment in Pilbara Port Corporation in

Western Australia as Site Engineer on same salary. Anna, who has been devoting

herself to fulltime care of their two children, has also taken the offer of employment

from All Brains Inc. in Perth as Personal Assistant to the Development Manager of the

company and will be joining in three month time.

Presently aged 53 and 51 years respectively, Graham and Anna plan to retire when

Graham reaches 62 years of age. They are seeking professional advice about their post-

retirement life so that they lead a secure and comfortable future for themselves as well

as their children whom they wish to support till they attain age of 24 years.

Personal Details of Mr. Graham Sutton and Ms. Anna Sutton

Name Graham Sutton Anna Sutton

Date of birth 06 October 1965 18 September 1963

Family Self, Wife & Two Children Self, Husband & Two Children

Marital Status Married Married

Occupation Salaried Employee-Engineer Personal Assistant

Employer Pilbara Port Corporation All Brains Inc.

Date of Joining 01 November 2018 1 December 2018

Salary Income $195,000 per annum (Gross) $52,000 per annum (Gross)

Interest Income $2,500 (On-line Savings Account) $2,500 (On-line Savings Account)

Income from

Rental Property $53,400 (Gross) $15,600 (Gross)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page7

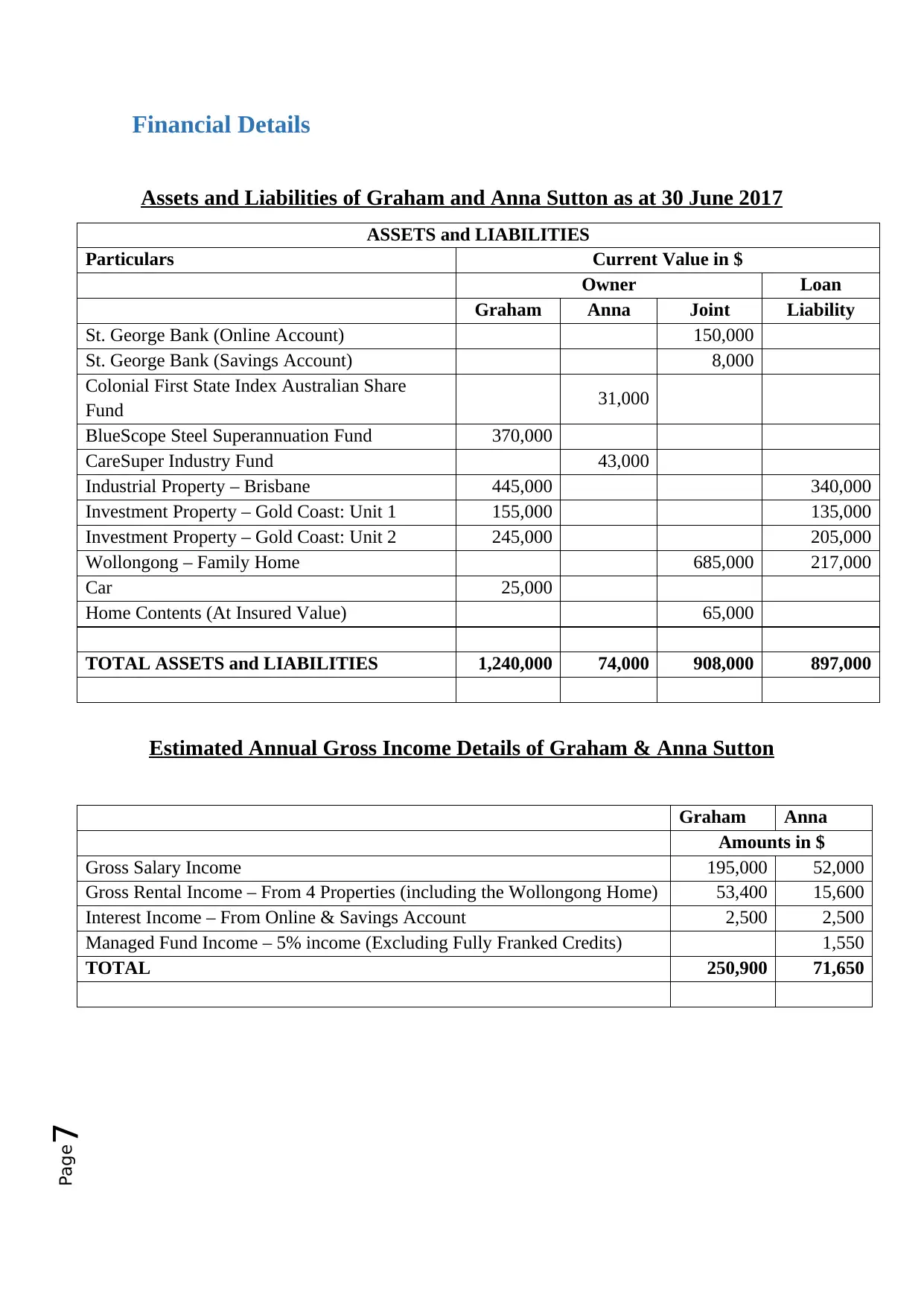

Financial Details

Assets and Liabilities of Graham and Anna Sutton as at 30 June 2017

ASSETS and LIABILITIES

Particulars Current Value in $

Owner Loan

Graham Anna Joint Liability

St. George Bank (Online Account) 150,000

St. George Bank (Savings Account) 8,000

Colonial First State Index Australian Share

Fund 31,000

BlueScope Steel Superannuation Fund 370,000

CareSuper Industry Fund 43,000

Industrial Property – Brisbane 445,000 340,000

Investment Property – Gold Coast: Unit 1 155,000 135,000

Investment Property – Gold Coast: Unit 2 245,000 205,000

Wollongong – Family Home 685,000 217,000

Car 25,000

Home Contents (At Insured Value) 65,000

TOTAL ASSETS and LIABILITIES 1,240,000 74,000 908,000 897,000

Estimated Annual Gross Income Details of Graham & Anna Sutton

Graham Anna

Amounts in $

Gross Salary Income 195,000 52,000

Gross Rental Income – From 4 Properties (including the Wollongong Home) 53,400 15,600

Interest Income – From Online & Savings Account 2,500 2,500

Managed Fund Income – 5% income (Excluding Fully Franked Credits) 1,550

TOTAL 250,900 71,650

Financial Details

Assets and Liabilities of Graham and Anna Sutton as at 30 June 2017

ASSETS and LIABILITIES

Particulars Current Value in $

Owner Loan

Graham Anna Joint Liability

St. George Bank (Online Account) 150,000

St. George Bank (Savings Account) 8,000

Colonial First State Index Australian Share

Fund 31,000

BlueScope Steel Superannuation Fund 370,000

CareSuper Industry Fund 43,000

Industrial Property – Brisbane 445,000 340,000

Investment Property – Gold Coast: Unit 1 155,000 135,000

Investment Property – Gold Coast: Unit 2 245,000 205,000

Wollongong – Family Home 685,000 217,000

Car 25,000

Home Contents (At Insured Value) 65,000

TOTAL ASSETS and LIABILITIES 1,240,000 74,000 908,000 897,000

Estimated Annual Gross Income Details of Graham & Anna Sutton

Graham Anna

Amounts in $

Gross Salary Income 195,000 52,000

Gross Rental Income – From 4 Properties (including the Wollongong Home) 53,400 15,600

Interest Income – From Online & Savings Account 2,500 2,500

Managed Fund Income – 5% income (Excluding Fully Franked Credits) 1,550

TOTAL 250,900 71,650

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page8

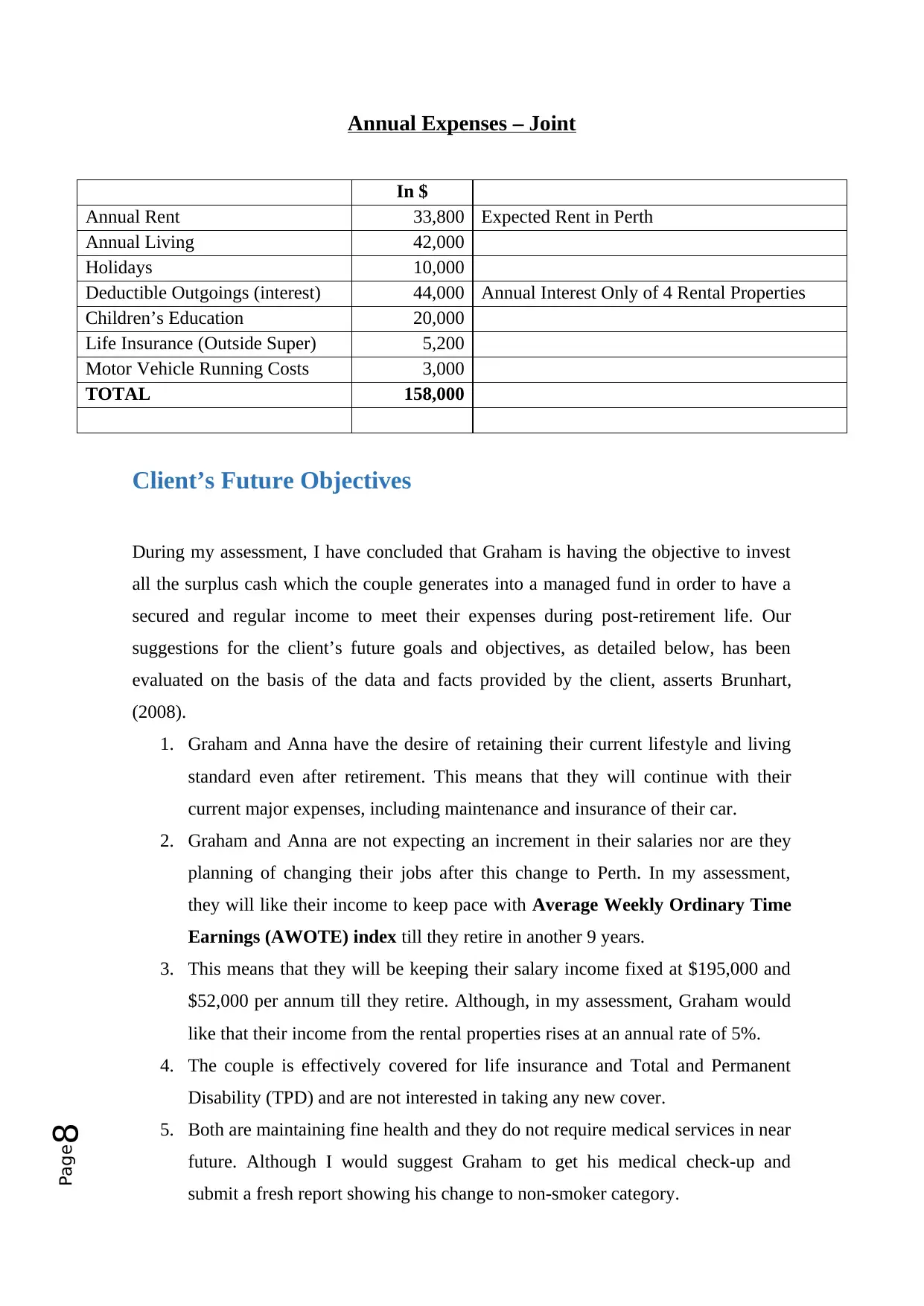

Annual Expenses – Joint

In $

Annual Rent 33,800 Expected Rent in Perth

Annual Living 42,000

Holidays 10,000

Deductible Outgoings (interest) 44,000 Annual Interest Only of 4 Rental Properties

Children’s Education 20,000

Life Insurance (Outside Super) 5,200

Motor Vehicle Running Costs 3,000

TOTAL 158,000

Client’s Future Objectives

During my assessment, I have concluded that Graham is having the objective to invest

all the surplus cash which the couple generates into a managed fund in order to have a

secured and regular income to meet their expenses during post-retirement life. Our

suggestions for the client’s future goals and objectives, as detailed below, has been

evaluated on the basis of the data and facts provided by the client, asserts Brunhart,

(2008).

1. Graham and Anna have the desire of retaining their current lifestyle and living

standard even after retirement. This means that they will continue with their

current major expenses, including maintenance and insurance of their car.

2. Graham and Anna are not expecting an increment in their salaries nor are they

planning of changing their jobs after this change to Perth. In my assessment,

they will like their income to keep pace with Average Weekly Ordinary Time

Earnings (AWOTE) index till they retire in another 9 years.

3. This means that they will be keeping their salary income fixed at $195,000 and

$52,000 per annum till they retire. Although, in my assessment, Graham would

like that their income from the rental properties rises at an annual rate of 5%.

4. The couple is effectively covered for life insurance and Total and Permanent

Disability (TPD) and are not interested in taking any new cover.

5. Both are maintaining fine health and they do not require medical services in near

future. Although I would suggest Graham to get his medical check-up and

submit a fresh report showing his change to non-smoker category.

Annual Expenses – Joint

In $

Annual Rent 33,800 Expected Rent in Perth

Annual Living 42,000

Holidays 10,000

Deductible Outgoings (interest) 44,000 Annual Interest Only of 4 Rental Properties

Children’s Education 20,000

Life Insurance (Outside Super) 5,200

Motor Vehicle Running Costs 3,000

TOTAL 158,000

Client’s Future Objectives

During my assessment, I have concluded that Graham is having the objective to invest

all the surplus cash which the couple generates into a managed fund in order to have a

secured and regular income to meet their expenses during post-retirement life. Our

suggestions for the client’s future goals and objectives, as detailed below, has been

evaluated on the basis of the data and facts provided by the client, asserts Brunhart,

(2008).

1. Graham and Anna have the desire of retaining their current lifestyle and living

standard even after retirement. This means that they will continue with their

current major expenses, including maintenance and insurance of their car.

2. Graham and Anna are not expecting an increment in their salaries nor are they

planning of changing their jobs after this change to Perth. In my assessment,

they will like their income to keep pace with Average Weekly Ordinary Time

Earnings (AWOTE) index till they retire in another 9 years.

3. This means that they will be keeping their salary income fixed at $195,000 and

$52,000 per annum till they retire. Although, in my assessment, Graham would

like that their income from the rental properties rises at an annual rate of 5%.

4. The couple is effectively covered for life insurance and Total and Permanent

Disability (TPD) and are not interested in taking any new cover.

5. Both are maintaining fine health and they do not require medical services in near

future. Although I would suggest Graham to get his medical check-up and

submit a fresh report showing his change to non-smoker category.

Page9

6. My advice to Graham would be to pay-off their Wollongong home loan balance

of $217,000 before the couple retires as this decision will make their post-retired

living more comfortable.

7. The couple’s decision of buying a home in Perth as their main residence, after

converting their Wollongong residence into a rental property, is a good move.

8. I have also assessed, after talking to Graham, that he has the desire to fix his

income at a minimum of 6% during his post-retirement period.

9. I suggest that the couple should achieve this by investing in good market

oriented funds. This will allow the couple not only in having secured earning in

their post-retirement life but will also help to adjust their expenses with

inflation.

Client’s Financial Plan

After making an assessment of the couple’s requirements and also keeping in mind the

couple’s balanced and stable approach towards growth for their investments, I suggest

the following investment options for the growth of the couple’s investments and for

providing them a steady income in their post-retirement life, as per Ashhurst, (2009).

Dividend Income

Although it is not considered mandatory, listed companies still prefer to pay dividends

to their shareholders. Below are some of the best options in the prevalent system which

can earn good income through these managed funds and dividend paying stocks, as per

Ezra, Collie & Smith, (2009).

01. Dividends Earned on Stock

An investor calculates the ‘Dividend Yield’ as the income from a stock and from my

experience I know that this income will depend on market price of the stock. All

investors chose stocks for their investments which offer a high dividend yield. Since the

yield depends on the share’s market price, in case the price falls, the dividend payment

also falls, assert Hallman & Rosenbloom, (2003). An increase in the dividend yield will

show that more investors have started investing in that particular stock and hence there

is an increase in its market price. Keeping this theory in mind, many companies have

started paying fixed dividends but still, the fluctuation in the share price in market

dictates the dividend yield of the share, as explained by Lange & King, (2009).

6. My advice to Graham would be to pay-off their Wollongong home loan balance

of $217,000 before the couple retires as this decision will make their post-retired

living more comfortable.

7. The couple’s decision of buying a home in Perth as their main residence, after

converting their Wollongong residence into a rental property, is a good move.

8. I have also assessed, after talking to Graham, that he has the desire to fix his

income at a minimum of 6% during his post-retirement period.

9. I suggest that the couple should achieve this by investing in good market

oriented funds. This will allow the couple not only in having secured earning in

their post-retirement life but will also help to adjust their expenses with

inflation.

Client’s Financial Plan

After making an assessment of the couple’s requirements and also keeping in mind the

couple’s balanced and stable approach towards growth for their investments, I suggest

the following investment options for the growth of the couple’s investments and for

providing them a steady income in their post-retirement life, as per Ashhurst, (2009).

Dividend Income

Although it is not considered mandatory, listed companies still prefer to pay dividends

to their shareholders. Below are some of the best options in the prevalent system which

can earn good income through these managed funds and dividend paying stocks, as per

Ezra, Collie & Smith, (2009).

01. Dividends Earned on Stock

An investor calculates the ‘Dividend Yield’ as the income from a stock and from my

experience I know that this income will depend on market price of the stock. All

investors chose stocks for their investments which offer a high dividend yield. Since the

yield depends on the share’s market price, in case the price falls, the dividend payment

also falls, assert Hallman & Rosenbloom, (2003). An increase in the dividend yield will

show that more investors have started investing in that particular stock and hence there

is an increase in its market price. Keeping this theory in mind, many companies have

started paying fixed dividends but still, the fluctuation in the share price in market

dictates the dividend yield of the share, as explained by Lange & King, (2009).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page10

02. Dividends Earned on Funds

Payment of dividends by listed companies has always depended on their share’s market

value. On the other hand, dividends payments of Managed Fund are always calculated

on the market value of ‘A Basket of Stocks’. On these basis, the Managed Funds are

paying their dividends either on a ‘Variable’ or a ‘Fixed’ rates to the investors who

invest in their portfolios of ‘Basket of Stocks’, explain Hallman & Rosenbloom, (2003).

On these basis, the Managed Funds are in a position to pay steady and regular dividends

to the investors and have been seldom found in failing on the payment system, as the

payment is based on distribution of an ‘Average Yield System’ income earned by them.

However, I still advise all my clients to carefully read the terms and conditions before

making any investment in Managed Funds, since the investor is required to authorize

the management of the Managed Funds for selling any stock or bond, which is owned

by the Managed Fund on behalf of the investor, to fulfil their minimum payment

guarantee condition, as detailed by Gitman, Joehnk & Billingsley, (2010).

03. Closed End Funds

Those Managed Funds which have the strategy to actively trade only in stocks and

bonds which pay dividend are called Closed End Funds. A Listed Companies pays

dividend on a quarterly basis, but a Closed End Fund pays dividend on annual basis,

asserts O’Shea (ed.), (2004). In this way, a Closed End Fund earns quarterly but pays at

the end of the year. The fund earns four dividends in one financial year but pays only

one to the investor. My advice to my clients is not to invest in these type of funds as

they have a high risk factor, as per Vice, (2010).

Client’s Current Situation

Graham’s Redundancy

It has been stated by Graham that his redundancy payment, after tax, from BlueScope

Steel will be $175,000. He would seek a suitable investment strategy for this money, so

that his money is safe and secure and yields him good returns post-retirement, as per

Alexander & Fogarty, (2009).

Graham’s Superannuation

After his retirement from BlueScope Steel, Graham is also expecting release of about

$370,000 from the BlueScope Steel Employer Fund. According to Graham, this current

02. Dividends Earned on Funds

Payment of dividends by listed companies has always depended on their share’s market

value. On the other hand, dividends payments of Managed Fund are always calculated

on the market value of ‘A Basket of Stocks’. On these basis, the Managed Funds are

paying their dividends either on a ‘Variable’ or a ‘Fixed’ rates to the investors who

invest in their portfolios of ‘Basket of Stocks’, explain Hallman & Rosenbloom, (2003).

On these basis, the Managed Funds are in a position to pay steady and regular dividends

to the investors and have been seldom found in failing on the payment system, as the

payment is based on distribution of an ‘Average Yield System’ income earned by them.

However, I still advise all my clients to carefully read the terms and conditions before

making any investment in Managed Funds, since the investor is required to authorize

the management of the Managed Funds for selling any stock or bond, which is owned

by the Managed Fund on behalf of the investor, to fulfil their minimum payment

guarantee condition, as detailed by Gitman, Joehnk & Billingsley, (2010).

03. Closed End Funds

Those Managed Funds which have the strategy to actively trade only in stocks and

bonds which pay dividend are called Closed End Funds. A Listed Companies pays

dividend on a quarterly basis, but a Closed End Fund pays dividend on annual basis,

asserts O’Shea (ed.), (2004). In this way, a Closed End Fund earns quarterly but pays at

the end of the year. The fund earns four dividends in one financial year but pays only

one to the investor. My advice to my clients is not to invest in these type of funds as

they have a high risk factor, as per Vice, (2010).

Client’s Current Situation

Graham’s Redundancy

It has been stated by Graham that his redundancy payment, after tax, from BlueScope

Steel will be $175,000. He would seek a suitable investment strategy for this money, so

that his money is safe and secure and yields him good returns post-retirement, as per

Alexander & Fogarty, (2009).

Graham’s Superannuation

After his retirement from BlueScope Steel, Graham is also expecting release of about

$370,000 from the BlueScope Steel Employer Fund. According to Graham, this current

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page11

value amount from the Super Fund carries a Tax Free Component of $22,000 and a

Taxed Component of $348,000. He is also seeking advice on how to securely invest this

amount for a secure and better yield in his post-retirement life, assert Nethercott, Devos

& Richardson, (2010).

Anna’s Superannuation

Till the time Anna was in service, she had accumulated a Super Fund balance of

$43,000 in CareSuper Industry Fund. Now, since she has decided to undertake

employment again when the couple shift to Perth, Graham and Anna are interested in

safe investment of this amount with a high-yield source during their post-retirement

period.

Investment Properties

In the income year 2011-12, Graham and Anna had invested in three rental income

properties, over an 18 month period. Two of these are residential properties, located in

Gold Coast and the third is an industrial property in Brisbane. Now that they are shifting

to Perth, the couple is interested in letting-out their residence in Wollongong, thus

creating their fourth rental property. The couple has declared the following as the

purchase price of these four properties.

1. Gold Coast: Unit-1 $159,000

2. Gold Coast: Unit-2 $268,000

3. Brisbane Industrial Property $385,000

4. Wollongong Residence $310,000

Graham’s & Anna’s Insurances

Graham and Anna have life insurance cover through their respective Super Funds. They

have also got cover of life and Permanent Disability Cover (TPD) through private

insurance companies. The couple is assured that their insurance coverage is adequate

and they do not wish to have any further guidance on this subject. However, they would

welcome advice on how the insurance policies perform.

Client’s Investment Planning

Interest income

I suggest to my client’s that compared to the dividend paying bonds or stocks, certain

managed funds also pay interest on the funds invested by the investors. In certain cases,

value amount from the Super Fund carries a Tax Free Component of $22,000 and a

Taxed Component of $348,000. He is also seeking advice on how to securely invest this

amount for a secure and better yield in his post-retirement life, assert Nethercott, Devos

& Richardson, (2010).

Anna’s Superannuation

Till the time Anna was in service, she had accumulated a Super Fund balance of

$43,000 in CareSuper Industry Fund. Now, since she has decided to undertake

employment again when the couple shift to Perth, Graham and Anna are interested in

safe investment of this amount with a high-yield source during their post-retirement

period.

Investment Properties

In the income year 2011-12, Graham and Anna had invested in three rental income

properties, over an 18 month period. Two of these are residential properties, located in

Gold Coast and the third is an industrial property in Brisbane. Now that they are shifting

to Perth, the couple is interested in letting-out their residence in Wollongong, thus

creating their fourth rental property. The couple has declared the following as the

purchase price of these four properties.

1. Gold Coast: Unit-1 $159,000

2. Gold Coast: Unit-2 $268,000

3. Brisbane Industrial Property $385,000

4. Wollongong Residence $310,000

Graham’s & Anna’s Insurances

Graham and Anna have life insurance cover through their respective Super Funds. They

have also got cover of life and Permanent Disability Cover (TPD) through private

insurance companies. The couple is assured that their insurance coverage is adequate

and they do not wish to have any further guidance on this subject. However, they would

welcome advice on how the insurance policies perform.

Client’s Investment Planning

Interest income

I suggest to my client’s that compared to the dividend paying bonds or stocks, certain

managed funds also pay interest on the funds invested by the investors. In certain cases,

Page12

some companies and government agencies also promise fixed interest amounts on the

investments made through bonds issued by them. Provisions of Australian Securities

and Investment Corporation (ASIC) also put certain restrictions on such

companies/agencies under which they are obliged to pay amount of interest before they

declare dividend on their stocks. Hence, the investments of our clients is more secure

under this interest paying option, both from view point of income earning and secure

investment, as per Barkoczy, (2011).

A ‘Certificates of Deposit’ (CD) is also issued by some companies and financial

institutions. This is an instrument which, when placed for a fixed period of time, gives

the investor a guaranteed interest income, which is higher than any other rate of interest.

If my clients wish to play safely (such as conservative investors), then in my opinion,

with this type of investment they can have a regular income, although it may be a low

one, as per Barkoczy, (2013). But I would surely recommend these securities for their

peace of mind. This type of investment is also good for the moderately aggressive

investor, who has the desire of investing their funds for a longer period and also re-

invest the interest they earn, with the aim that their investments grow steadily over a

period of time, say ten years, and their money also remains safe, asserts Barkoczy,

(2013).

Other Safe Investment Options

In my opinion, dividends and interests are not the only two options available for safe

returns in stock market. In my log career as an investment advisor, I have come across

the many options which are available to investors, and I am discussing them below for

your perusal, as detailed by Barkoczy, (2015). I have seen that these investment options

give a clear advantage to investors over other regular investment options in the stock

market as the investor can withdraw their investment at a comparatively short notice,

and without foregoing any part of their investment as loss for making a preponed

withdrawals, as per Barkoczy et al, (2010). I am of the opinion that these options are

most suitable for conservative as well as moderate investors, as these investors keep

their aims focussed on not:

losing a part of the principal investment;

Entering for shorter periods in the stock markets; and

linking their investments with the inflation effect.

some companies and government agencies also promise fixed interest amounts on the

investments made through bonds issued by them. Provisions of Australian Securities

and Investment Corporation (ASIC) also put certain restrictions on such

companies/agencies under which they are obliged to pay amount of interest before they

declare dividend on their stocks. Hence, the investments of our clients is more secure

under this interest paying option, both from view point of income earning and secure

investment, as per Barkoczy, (2011).

A ‘Certificates of Deposit’ (CD) is also issued by some companies and financial

institutions. This is an instrument which, when placed for a fixed period of time, gives

the investor a guaranteed interest income, which is higher than any other rate of interest.

If my clients wish to play safely (such as conservative investors), then in my opinion,

with this type of investment they can have a regular income, although it may be a low

one, as per Barkoczy, (2013). But I would surely recommend these securities for their

peace of mind. This type of investment is also good for the moderately aggressive

investor, who has the desire of investing their funds for a longer period and also re-

invest the interest they earn, with the aim that their investments grow steadily over a

period of time, say ten years, and their money also remains safe, asserts Barkoczy,

(2013).

Other Safe Investment Options

In my opinion, dividends and interests are not the only two options available for safe

returns in stock market. In my log career as an investment advisor, I have come across

the many options which are available to investors, and I am discussing them below for

your perusal, as detailed by Barkoczy, (2015). I have seen that these investment options

give a clear advantage to investors over other regular investment options in the stock

market as the investor can withdraw their investment at a comparatively short notice,

and without foregoing any part of their investment as loss for making a preponed

withdrawals, as per Barkoczy et al, (2010). I am of the opinion that these options are

most suitable for conservative as well as moderate investors, as these investors keep

their aims focussed on not:

losing a part of the principal investment;

Entering for shorter periods in the stock markets; and

linking their investments with the inflation effect.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.