Comprehensive Accounting Report: Surfstitch Group Financial Analysis

VerifiedAdded on 2019/11/08

|11

|2269

|272

Report

AI Summary

This report provides a detailed accounting analysis of Surfstitch Group, examining its financial performance in 2015 and 2016. The analysis includes changes in key metrics like goodwill, investment in subsidiaries, and cash position, highlighting significant decreases. The report delves into selling, distribution, and administration expenses, noting substantial increases and an impairment loss. It evaluates the company's restructuring efforts and advises against investment based on the financial data. Furthermore, the report discusses the importance of continuous disclosure rules, referencing relevant regulations and their impact on investors, market efficiency, and corporate governance. It also explores exceptions to disclosure rules and the significance of compliance systems for listed companies.

ACCOUNTING OF SURFSTITCH GROUP 1

ACCOUNTING OF SURFSTITCH

GROUP

ACCOUNTING OF SURFSTITCH

GROUP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING OF SURFSTITCH GROUP 2

Contents

Part I:..........................................................................................................................................3

Part 1:......................................................................................................................................3

Part 2:......................................................................................................................................3

Part 3:......................................................................................................................................3

Part 4:......................................................................................................................................4

Part II:.........................................................................................................................................4

References:.................................................................................................................................8

Contents

Part I:..........................................................................................................................................3

Part 1:......................................................................................................................................3

Part 2:......................................................................................................................................3

Part 3:......................................................................................................................................3

Part 4:......................................................................................................................................4

Part II:.........................................................................................................................................4

References:.................................................................................................................................8

ACCOUNTING OF SURFSTITCH GROUP 3

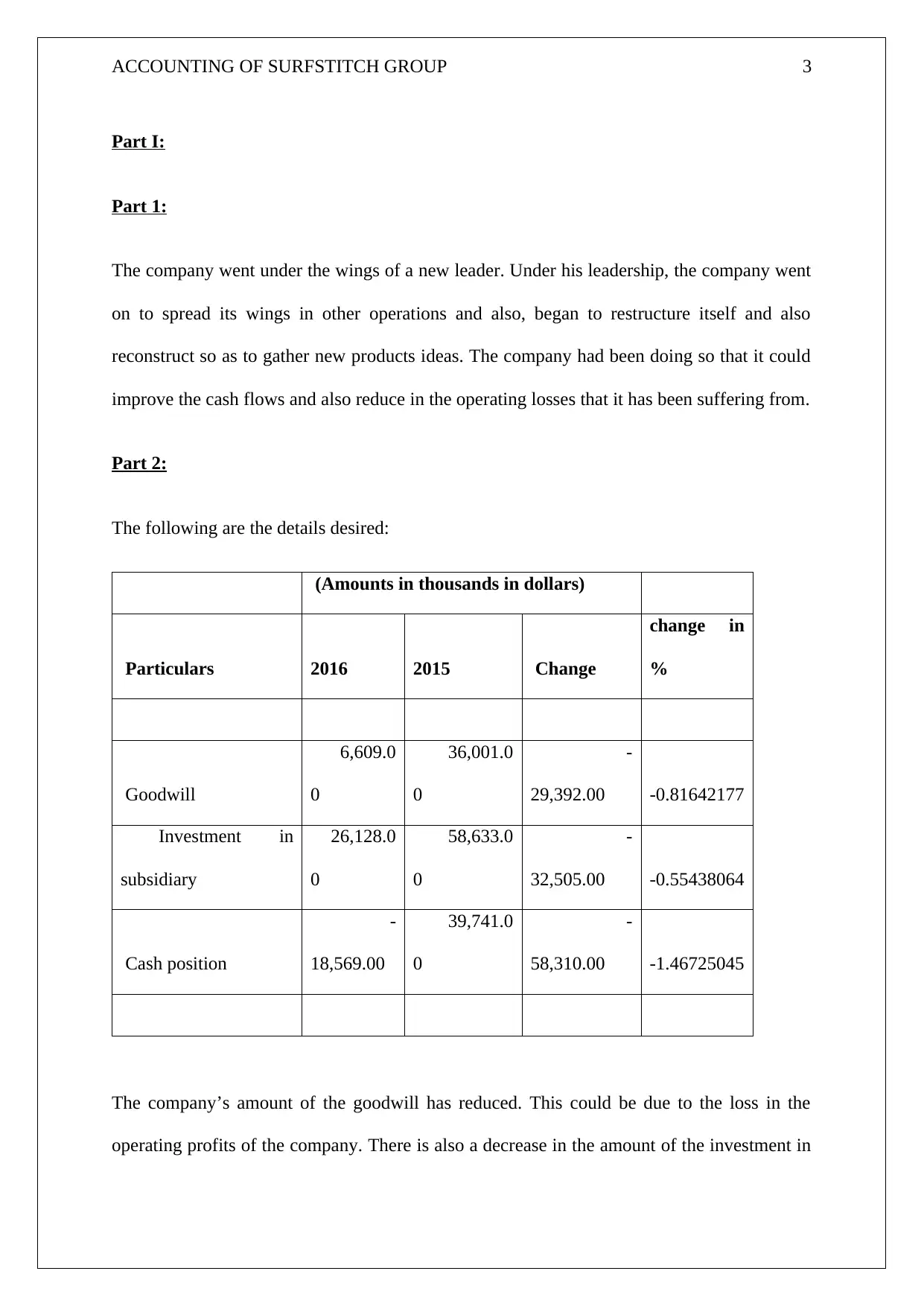

Part I:

Part 1:

The company went under the wings of a new leader. Under his leadership, the company went

on to spread its wings in other operations and also, began to restructure itself and also

reconstruct so as to gather new products ideas. The company had been doing so that it could

improve the cash flows and also reduce in the operating losses that it has been suffering from.

Part 2:

The following are the details desired:

(Amounts in thousands in dollars)

Particulars 2016 2015 Change

change in

%

Goodwill

6,609.0

0

36,001.0

0

-

29,392.00 -0.81642177

Investment in

subsidiary

26,128.0

0

58,633.0

0

-

32,505.00 -0.55438064

Cash position

-

18,569.00

39,741.0

0

-

58,310.00 -1.46725045

The company’s amount of the goodwill has reduced. This could be due to the loss in the

operating profits of the company. There is also a decrease in the amount of the investment in

Part I:

Part 1:

The company went under the wings of a new leader. Under his leadership, the company went

on to spread its wings in other operations and also, began to restructure itself and also

reconstruct so as to gather new products ideas. The company had been doing so that it could

improve the cash flows and also reduce in the operating losses that it has been suffering from.

Part 2:

The following are the details desired:

(Amounts in thousands in dollars)

Particulars 2016 2015 Change

change in

%

Goodwill

6,609.0

0

36,001.0

0

-

29,392.00 -0.81642177

Investment in

subsidiary

26,128.0

0

58,633.0

0

-

32,505.00 -0.55438064

Cash position

-

18,569.00

39,741.0

0

-

58,310.00 -1.46725045

The company’s amount of the goodwill has reduced. This could be due to the loss in the

operating profits of the company. There is also a decrease in the amount of the investment in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING OF SURFSTITCH GROUP 4

the subsidiary. The decrease is at least by 50%. The cash position of the company has again

reduced. The company has earned losses in all the 3 segments of the cash flow statement. The

first being the cash flows from operating activities, second being the cash flows from

investing activities and the third being the cash flows from financing activities.

Part 3:

The following are the desired details:

(Amounts in thousands in dollars)

Particulars 2016 2015 Change

change in

%

Selling and

distribution

1,01,268.0

0

44,683.0

0

56,585.0

0

1.26636528

4

Administration

49,237.0

0

7,424.0

0

41,813.0

0

5.63213900

9

Impairment

88,999.0

0 -

88,999.0

0 #DIV/0!

The above table shows that there has been a major increase in the amount of the selling and

distribution expenses. The company has also increased the amount that it spent towards the

administration expenses. The company had 0 impairment during the year 2015 and now, it

has the impairment loss of about $90,000 thousand. The rise in the expenses is mainly due to

the subsidiary. The decrease is at least by 50%. The cash position of the company has again

reduced. The company has earned losses in all the 3 segments of the cash flow statement. The

first being the cash flows from operating activities, second being the cash flows from

investing activities and the third being the cash flows from financing activities.

Part 3:

The following are the desired details:

(Amounts in thousands in dollars)

Particulars 2016 2015 Change

change in

%

Selling and

distribution

1,01,268.0

0

44,683.0

0

56,585.0

0

1.26636528

4

Administration

49,237.0

0

7,424.0

0

41,813.0

0

5.63213900

9

Impairment

88,999.0

0 -

88,999.0

0 #DIV/0!

The above table shows that there has been a major increase in the amount of the selling and

distribution expenses. The company has also increased the amount that it spent towards the

administration expenses. The company had 0 impairment during the year 2015 and now, it

has the impairment loss of about $90,000 thousand. The rise in the expenses is mainly due to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING OF SURFSTITCH GROUP 5

the increase in the amount of the revenue as well. The revenue of the company increased to

up to 3 times.

Part 4:

Any investor would like to have an investment that is able to give him profit when he sells his

investment along with a regular return on his investment. But as the annual report of the year

2016 states , the company was not able to comply with its targets that were set earlier and

also went on to restructure itself and reprogram itself. This shows that the company is still

inventing and in the course of hit and trial method. Hence, the investment in this company is

not recommended.

Part II:

As per the listing rule 3.1, each company is duty bound to disclose the information which

could affect any prudent investor from making an investment in the company.

The following are some of the examples of the same, though not limited to:

Any information that would result in the change in the activities or on the transactions

of the company

Any information that is mineral or hydrocarbon discovery

Any information which is related with the material acquisition or the disposals of any

asset

Any information which is related with the granting or withdrawal of any material

license

Any information which pertains to the variation or the termination of any material

agreement

the increase in the amount of the revenue as well. The revenue of the company increased to

up to 3 times.

Part 4:

Any investor would like to have an investment that is able to give him profit when he sells his

investment along with a regular return on his investment. But as the annual report of the year

2016 states , the company was not able to comply with its targets that were set earlier and

also went on to restructure itself and reprogram itself. This shows that the company is still

inventing and in the course of hit and trial method. Hence, the investment in this company is

not recommended.

Part II:

As per the listing rule 3.1, each company is duty bound to disclose the information which

could affect any prudent investor from making an investment in the company.

The following are some of the examples of the same, though not limited to:

Any information that would result in the change in the activities or on the transactions

of the company

Any information that is mineral or hydrocarbon discovery

Any information which is related with the material acquisition or the disposals of any

asset

Any information which is related with the granting or withdrawal of any material

license

Any information which pertains to the variation or the termination of any material

agreement

ACCOUNTING OF SURFSTITCH GROUP 6

Any information which is related to the plaintiff or defendant in any case pending in

court

Any information which would affect the share price of the company in the market

Any information which would lead to a change in the expectations in the market

Any information which relates with the appointment of any liquidator etc. of the

company

Any information related with the event of default under or in an event which entitles

the financier to terminate or any material which affects the material financial facility

Any information which is related to the subscription of the securities or with the issue

of the securities

Giving or receiving of the notice which intends to make a takeover of the company

Any rating that would be applied by the rating agency to the entity or its securities

Change information which pertains to the stated change in the rating given by the

agency to the company

The investors are prone to some information which relates with the issue of securities. There

is a broad set information which is available at the disposal of the investors. Such is the

information which varies all across the dimensions of the business and its characteristics

which includes in the timeliness, quality, routine etc. There are many pieces of information

which are of an utmost importance for the investors. The example include the record of the

past earnings of the company, forecasts of the earnings etc. another is the example of the

voluntary earnings of the company which have been estimated by the management. These are

the issues that are of interest for the investors. There is an improved disclosure of the

activities due to the implications for the efficiency in the capital market and due to the

subsequent allocation of the resources in the economy. The increased and the timely

Any information which is related to the plaintiff or defendant in any case pending in

court

Any information which would affect the share price of the company in the market

Any information which would lead to a change in the expectations in the market

Any information which relates with the appointment of any liquidator etc. of the

company

Any information related with the event of default under or in an event which entitles

the financier to terminate or any material which affects the material financial facility

Any information which is related to the subscription of the securities or with the issue

of the securities

Giving or receiving of the notice which intends to make a takeover of the company

Any rating that would be applied by the rating agency to the entity or its securities

Change information which pertains to the stated change in the rating given by the

agency to the company

The investors are prone to some information which relates with the issue of securities. There

is a broad set information which is available at the disposal of the investors. Such is the

information which varies all across the dimensions of the business and its characteristics

which includes in the timeliness, quality, routine etc. There are many pieces of information

which are of an utmost importance for the investors. The example include the record of the

past earnings of the company, forecasts of the earnings etc. another is the example of the

voluntary earnings of the company which have been estimated by the management. These are

the issues that are of interest for the investors. There is an improved disclosure of the

activities due to the implications for the efficiency in the capital market and due to the

subsequent allocation of the resources in the economy. The increased and the timely

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING OF SURFSTITCH GROUP 7

disclosure of the information would lead to lesser insider trading of the information available

with the management.

The new rules regarding the following of the continuous disclosure policies aims at

disclosure of these issues at the correct time only.

It puts pressure on the boards that requires in the bold and clear regulatory response. This is

the current uncertainty which merely means that the country is having an increased balanced

approach when it comes to following of these rules and is also transparent market when the

same is at stake.

Even when the intention of the ASX is the relaxation of the disclosure obligations which

allows the listed companies to meet the commercial objectives, changes to this rule is

required and hence, must be same. Rather it would be good if the country could adopted the

periodic disclosure approach which is being followed currently in the country of the United

States. The main reason for the launch of this rule was the fact that after the year 2000, there

were many of the legislative changes along with an increased enforcement action by the

ASIC that led to the increased disclosure of the forecasts of the management’s earnings

which were non routine in nature. In respect of the routine forecasts, there was a significant

increase in the disclosure of the forecast which has been observed. This is just in line with the

finding that there is an increased disclosure which serves as the bad news for the non-routine

forecasts.

The reason behind this was not only reducing the amount of the information which is

available between the managers and the investors but also, between the difference categories

of the investors. An effective and a timely disclosure serves as a good measure of the good

governance and also reinforces in the principles 5 which relates with the principles and the

recommendations of corporate governance. When a company breaches this rule, then the

disclosure of the information would lead to lesser insider trading of the information available

with the management.

The new rules regarding the following of the continuous disclosure policies aims at

disclosure of these issues at the correct time only.

It puts pressure on the boards that requires in the bold and clear regulatory response. This is

the current uncertainty which merely means that the country is having an increased balanced

approach when it comes to following of these rules and is also transparent market when the

same is at stake.

Even when the intention of the ASX is the relaxation of the disclosure obligations which

allows the listed companies to meet the commercial objectives, changes to this rule is

required and hence, must be same. Rather it would be good if the country could adopted the

periodic disclosure approach which is being followed currently in the country of the United

States. The main reason for the launch of this rule was the fact that after the year 2000, there

were many of the legislative changes along with an increased enforcement action by the

ASIC that led to the increased disclosure of the forecasts of the management’s earnings

which were non routine in nature. In respect of the routine forecasts, there was a significant

increase in the disclosure of the forecast which has been observed. This is just in line with the

finding that there is an increased disclosure which serves as the bad news for the non-routine

forecasts.

The reason behind this was not only reducing the amount of the information which is

available between the managers and the investors but also, between the difference categories

of the investors. An effective and a timely disclosure serves as a good measure of the good

governance and also reinforces in the principles 5 which relates with the principles and the

recommendations of corporate governance. When a company breaches this rule, then the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING OF SURFSTITCH GROUP 8

company would be exposed to civil penalty proceedings and has a maximum fine of $ 1

million accompanied by the penalty proceedings and the enforceable undertakings and with

the use of the infringement notices that were introduced in the year 2004. Even if the

company complies with the infringement notice, even then the ASIC would go against the

company to levy the penalty as against the company but this penalty would never affect the

right of the third parties that would have been affected by the conduct of the company. This is

as per section 1317 HA (the conversation, 2017).

The primary motive for this is to gain an understanding and the confidence, and the

participation by the investors in the securities market. This is further expected to improve in

depth, liquidity and the efficiency of these markets. This rule would make sure that the share

price of the securities in the market indicates the correct underlying economic value of the

same. It would reduce in the volatility of the prices of the securities since the investors have

an access to an increased amount of information all about disclosing in the performance and

the prospects of the entity and the information could be rapidly be factored into the prices of

the securities of the company. This affects the information which is price sensitive. The

following of this rule would minimise in the risk of any information which is not available in

the market from being used by the investors so as to achieve a windfall gain. Also, there are

some of the other forms of market abuses that could result in the withholding of the

disclosing of the materially sensitive information.

The companies would voluntarily disclose in the information which could affect the prices of

the securities in the market (treasury, 2017).

This information is of an utmost importance and this information must not be made available

to any person or any third party unless and until it is made available for the use by the general

public. There are some of the exceptions to this rule: the first being the information that is not

company would be exposed to civil penalty proceedings and has a maximum fine of $ 1

million accompanied by the penalty proceedings and the enforceable undertakings and with

the use of the infringement notices that were introduced in the year 2004. Even if the

company complies with the infringement notice, even then the ASIC would go against the

company to levy the penalty as against the company but this penalty would never affect the

right of the third parties that would have been affected by the conduct of the company. This is

as per section 1317 HA (the conversation, 2017).

The primary motive for this is to gain an understanding and the confidence, and the

participation by the investors in the securities market. This is further expected to improve in

depth, liquidity and the efficiency of these markets. This rule would make sure that the share

price of the securities in the market indicates the correct underlying economic value of the

same. It would reduce in the volatility of the prices of the securities since the investors have

an access to an increased amount of information all about disclosing in the performance and

the prospects of the entity and the information could be rapidly be factored into the prices of

the securities of the company. This affects the information which is price sensitive. The

following of this rule would minimise in the risk of any information which is not available in

the market from being used by the investors so as to achieve a windfall gain. Also, there are

some of the other forms of market abuses that could result in the withholding of the

disclosing of the materially sensitive information.

The companies would voluntarily disclose in the information which could affect the prices of

the securities in the market (treasury, 2017).

This information is of an utmost importance and this information must not be made available

to any person or any third party unless and until it is made available for the use by the general

public. There are some of the exceptions to this rule: the first being the information that is not

ACCOUNTING OF SURFSTITCH GROUP 9

permitted by rules and the regulations in the environment in which the company operates.

These exceptions have the limited allowance for the communications between the rating

agencies and the advisers in the normal course of the business (Thomson reuters, 2017).

There is a communication with the person with whom the company has been negotiate. Or

even intends to negotiate. In all of the above cases, the people in possession of this

information have to keep in the information confidential and to themselves (FSA, 2017).

The exceptions to this rule are termed as the safe harbour rules. These are the provisions or

the rules that permit the disallowance of the formation form being available to the public in

case, certain conditions are met. These conditions are as follows:

Any information would not be made available to the people when any person is not

expected to possess the same

Any information would not be made available to the people which relates to the

breach of any rule or regulation of law (NZX,2017).

The compliance of this rule is very necessary. And also vital for each and every ASC listed

company. The company in addition to following up of this rule has to have a strong

compliance system which would help in raising the dense of the people that are involved in

the contravention of these obligations.

Section 674 (2B) of the Corporations Act, 2001 states the fact that the due diligence defence

could take place when any reasonable person had exercised a reasonable care and carried on

his duty so as to not make such of the information public. He ensured the compliance by

helping the company in complying with this obligation and believed on a reasonable ground

that the company complied with such obligation.

permitted by rules and the regulations in the environment in which the company operates.

These exceptions have the limited allowance for the communications between the rating

agencies and the advisers in the normal course of the business (Thomson reuters, 2017).

There is a communication with the person with whom the company has been negotiate. Or

even intends to negotiate. In all of the above cases, the people in possession of this

information have to keep in the information confidential and to themselves (FSA, 2017).

The exceptions to this rule are termed as the safe harbour rules. These are the provisions or

the rules that permit the disallowance of the formation form being available to the public in

case, certain conditions are met. These conditions are as follows:

Any information would not be made available to the people when any person is not

expected to possess the same

Any information would not be made available to the people which relates to the

breach of any rule or regulation of law (NZX,2017).

The compliance of this rule is very necessary. And also vital for each and every ASC listed

company. The company in addition to following up of this rule has to have a strong

compliance system which would help in raising the dense of the people that are involved in

the contravention of these obligations.

Section 674 (2B) of the Corporations Act, 2001 states the fact that the due diligence defence

could take place when any reasonable person had exercised a reasonable care and carried on

his duty so as to not make such of the information public. He ensured the compliance by

helping the company in complying with this obligation and believed on a reasonable ground

that the company complied with such obligation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING OF SURFSTITCH GROUP 10

When a company has a robust compliance system, then that shows that it took all reasonable

precautions and had all the procedures in place so as to avoid any breaches of this rule

(Claytonutz, 2017).

In the nutshell, the introduction of this rule is good for the company because each investor

plays with his own brain. Each investor is exposed to the same quality of the information as

each one does. Exposing one to limited information about the company and exposing the

other to immense information about the company would give an undue advantage to the

investor that has limited amount of information. Hence, this is not good and though this rule

is now. But I am confident that this new rule would serve the purpose for which the same has

been introduced.

When a company has a robust compliance system, then that shows that it took all reasonable

precautions and had all the procedures in place so as to avoid any breaches of this rule

(Claytonutz, 2017).

In the nutshell, the introduction of this rule is good for the company because each investor

plays with his own brain. Each investor is exposed to the same quality of the information as

each one does. Exposing one to limited information about the company and exposing the

other to immense information about the company would give an undue advantage to the

investor that has limited amount of information. Hence, this is not good and though this rule

is now. But I am confident that this new rule would serve the purpose for which the same has

been introduced.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING OF SURFSTITCH GROUP 11

References:

Compliance with continuous disclosure obligations - Knowledge - Clayton Utz.

(2017). Claytonutz.com. Retrieved 13 September 2017, from

https://www.claytonutz.com/knowledge/2008/january/compliance-with-continuous-

disclosure-obligations

Continuous Disclosure. (2014). nzx.com. Retrieved 13 September 2017, from

https://nzx.com/files/static/cms-documents/Final%20Continuous%20Disclosure

%20Guidance%20Note%2019%20December%202014%20(1).pdf

Explainer: Continuous disclosure obligations. (2017). The Conversation. Retrieved 13

September 2017, from http://theconversation.com/explainer-continuous-disclosure-

obligations-16894

North, G. (2017). A call for bold and effective disclosure

framework. sites.thomsonreuters.com.au. Retrieved 13 September 2017, from

http://sites.thomsonreuters.com.au/journals/files/2010/10/j04_v028_CSLJ_pt05_north.pd

f

Part 8. (2017). Archive.treasury.gov.au. Retrieved 13 September 2017, from

https://archive.treasury.gov.au/documents/403/HTML/docshell.asp?URL=Ch8.asp

Principles for Ongoing Disclosure and Material Development Reporting by Listed Entities.

(2017). www.fsa.go.jp. Retrieved 13 September 2017, from

http://www.fsa.go.jp/inter/ios/press05.pdf

References:

Compliance with continuous disclosure obligations - Knowledge - Clayton Utz.

(2017). Claytonutz.com. Retrieved 13 September 2017, from

https://www.claytonutz.com/knowledge/2008/january/compliance-with-continuous-

disclosure-obligations

Continuous Disclosure. (2014). nzx.com. Retrieved 13 September 2017, from

https://nzx.com/files/static/cms-documents/Final%20Continuous%20Disclosure

%20Guidance%20Note%2019%20December%202014%20(1).pdf

Explainer: Continuous disclosure obligations. (2017). The Conversation. Retrieved 13

September 2017, from http://theconversation.com/explainer-continuous-disclosure-

obligations-16894

North, G. (2017). A call for bold and effective disclosure

framework. sites.thomsonreuters.com.au. Retrieved 13 September 2017, from

http://sites.thomsonreuters.com.au/journals/files/2010/10/j04_v028_CSLJ_pt05_north.pd

f

Part 8. (2017). Archive.treasury.gov.au. Retrieved 13 September 2017, from

https://archive.treasury.gov.au/documents/403/HTML/docshell.asp?URL=Ch8.asp

Principles for Ongoing Disclosure and Material Development Reporting by Listed Entities.

(2017). www.fsa.go.jp. Retrieved 13 September 2017, from

http://www.fsa.go.jp/inter/ios/press05.pdf

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.