Contemporary Accounting Theory: CSR, Sustainability, and Dulux Group

VerifiedAdded on 2022/10/04

|19

|4489

|21

Report

AI Summary

This report delves into contemporary accounting theory, specifically examining the significance of corporate social responsibility (CSR) for businesses and its relationship with sustainability reporting. The report is divided into two main sections. The first section presents a literature review, emphasizing the importance of CSR for firms with financial objectives and exploring the holistic view of CSR by relating sustainability reports to other concepts. It also explains sustainability reporting using legitimacy and institutional theories. The second section evaluates the quality of Dulux Group Material Limited's sustainability report, assessing its reporting framework against the Global Reporting Initiative (GRI) sustainability index. The report also provides an overview of Dulux Group's governance, ownership, and financial performance. The analysis highlights the company's adherence to CSR principles and its commitment to transparent reporting, providing insights into how companies can effectively integrate sustainability into their core business strategies. The report concludes with an evaluation of Dulux Group's sustainability reporting quality based on the GRI guidelines.

Running head: CONTEMPORARY ACCOUNTING THEORY

Contemporary accounting theory

Name of the Student

Name of the University

Author Note

Contemporary accounting theory

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

Executive summary:

The report is prepared to determine the importance of the sustainability reporting and the

association between the corporate social responsibility and sustainability reporting. Two

sections incorporates the whole report, with the first section focusing on the literature review

explaining the importance of the corporate social responsibility and relevance of the reporting

concepts to the sustainability reporting. This also involves discussion on the explanation of

the sustainability reporting using the theories such as legitimacy and institutional theory.

Another section demonstrates the evaluation of the quality of sustainability report of Dulux

group material limited. This has been done by assessing the reporting framework of Dulux

against the sustainability index of the GRI.

Executive summary:

The report is prepared to determine the importance of the sustainability reporting and the

association between the corporate social responsibility and sustainability reporting. Two

sections incorporates the whole report, with the first section focusing on the literature review

explaining the importance of the corporate social responsibility and relevance of the reporting

concepts to the sustainability reporting. This also involves discussion on the explanation of

the sustainability reporting using the theories such as legitimacy and institutional theory.

Another section demonstrates the evaluation of the quality of sustainability report of Dulux

group material limited. This has been done by assessing the reporting framework of Dulux

against the sustainability index of the GRI.

CONTEMPORARY ACCOUNTING THEORY

Table of Contents

Introduction:...............................................................................................................................3

Part A:........................................................................................................................................3

i. Reviewing literature for explaining the importance of corporate social responsibility for

the firms with financial objectives:............................................................................................3

ii. Evaluating the holistic view of corporate social responsibility by determining the

compatibility of the sustainability reports with other concepts:................................................5

iii. Explaining the sustainability reporting essence using relevant theories:........................6

Part B:.........................................................................................................................................7

iv. Description of the governance, ownership and financial performance of Dulux Group

Material:.....................................................................................................................................7

v. Preparation of sustainability reporting index in accordance with the guidelines of GRI

(Global Reporting Initiatives)....................................................................................................9

vi. Evaluating the quality of sustainability reporting of the company against the scoring

index of sustainability reporting:.............................................................................................10

Conclusion:..............................................................................................................................13

Reference list:...........................................................................................................................15

Table of Contents

Introduction:...............................................................................................................................3

Part A:........................................................................................................................................3

i. Reviewing literature for explaining the importance of corporate social responsibility for

the firms with financial objectives:............................................................................................3

ii. Evaluating the holistic view of corporate social responsibility by determining the

compatibility of the sustainability reports with other concepts:................................................5

iii. Explaining the sustainability reporting essence using relevant theories:........................6

Part B:.........................................................................................................................................7

iv. Description of the governance, ownership and financial performance of Dulux Group

Material:.....................................................................................................................................7

v. Preparation of sustainability reporting index in accordance with the guidelines of GRI

(Global Reporting Initiatives)....................................................................................................9

vi. Evaluating the quality of sustainability reporting of the company against the scoring

index of sustainability reporting:.............................................................................................10

Conclusion:..............................................................................................................................13

Reference list:...........................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

Introduction:

The paper is developed to review the importance of corporate social responsibility to

the firms along with evaluating its holistic review. There are two sections incorporated in the

paper with the first section outlining the relevance of corporate social responsibility for the

firms with financial objectives by reviewing the literature and demonstrating the explanation

of the essence of sustainability reporting using applicable theories. The other section gives an

illustration of the relevance of such reporting system by retrieving information from the

sustainability report of the listed entity. The selected company for this purpose is Dulux

Group Material, which is a leading manufacturer and marketer of the products of premium

brands for maintaining, enhancing and protecting the spaces and places where people live and

work. The quality of sustainability report prepared by Dulux is evaluated against the

sustainability disclosure index of GRI (Global Reporting Initiative) in terms of the

information presented therein.

Part A:

i. Reviewing literature for explaining the importance of corporate social

responsibility for the firms with financial objectives:

One of the most prominent business eras is the corporate social responsibility which, is

becoming an indispensable part of any organization. Any individual organization the most

significant goal of the corporate social responsibility is to make sure that all the companies

should have a good output with a positive effect on the society. It is becoming very essential

that all the business practices by the companies nowadays should be carried out in an ethical

manner, so CSR takes into account all these factors into account and makes sure that all the

Introduction:

The paper is developed to review the importance of corporate social responsibility to

the firms along with evaluating its holistic review. There are two sections incorporated in the

paper with the first section outlining the relevance of corporate social responsibility for the

firms with financial objectives by reviewing the literature and demonstrating the explanation

of the essence of sustainability reporting using applicable theories. The other section gives an

illustration of the relevance of such reporting system by retrieving information from the

sustainability report of the listed entity. The selected company for this purpose is Dulux

Group Material, which is a leading manufacturer and marketer of the products of premium

brands for maintaining, enhancing and protecting the spaces and places where people live and

work. The quality of sustainability report prepared by Dulux is evaluated against the

sustainability disclosure index of GRI (Global Reporting Initiative) in terms of the

information presented therein.

Part A:

i. Reviewing literature for explaining the importance of corporate social

responsibility for the firms with financial objectives:

One of the most prominent business eras is the corporate social responsibility which, is

becoming an indispensable part of any organization. Any individual organization the most

significant goal of the corporate social responsibility is to make sure that all the companies

should have a good output with a positive effect on the society. It is becoming very essential

that all the business practices by the companies nowadays should be carried out in an ethical

manner, so CSR takes into account all these factors into account and makes sure that all the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

practices and the method adopted by any business enterprise should be ethical and

environmentally, socially and economically accepted by all in and within the organization.

Moreover, there should be a maximum creation of the shared value for the owners of the

enterprise which includes its employees, shareholders and stakeholders ((Dumay et al., 2017).

Talking about the corporate social responsibility, one can describe it as a type of self-

regulation adopted by any private business enterprise which, targets at maintaining the

societal goals and targets. There are certain strategies that the CSR has taken into

consideration for running any organization that is to make positive impact not only on the

environment but also on the stakeholders, also the consumers, employees, investors and the

communities. From the ethical point of view, at times, CSR are adopted in the organization

because of the ethical beliefs of the senior management. For an instance, the company’s

managing director believes that it is environmentally objectionable to hamper the

environment. By implementation and operation of CSR in any organization operates with a

perspective of obtaining long term profits while the critics argue that CSR being the

economic role of the organization (Thomas, 2019). However, these were later on studied on a

wider scale which compared the existing econometric studies explaining the relationship in

between the social and financial performance. This finally came to a conclusion that the

contradictory results of the previous studies reporting positive, negative and the neutral and

the financial impact were due to flawed empirical analysis and also claims that the study is

appropriately specified, so it can declared that corporate social responsibility has a very

impact on the financial outcomes of the organization. Moreover, it is titled that CSR to aid

the targets and missions of the organization as well as to assist in representing to the

consumers what the company aims at serving its customers (Maas et al., 2016).

practices and the method adopted by any business enterprise should be ethical and

environmentally, socially and economically accepted by all in and within the organization.

Moreover, there should be a maximum creation of the shared value for the owners of the

enterprise which includes its employees, shareholders and stakeholders ((Dumay et al., 2017).

Talking about the corporate social responsibility, one can describe it as a type of self-

regulation adopted by any private business enterprise which, targets at maintaining the

societal goals and targets. There are certain strategies that the CSR has taken into

consideration for running any organization that is to make positive impact not only on the

environment but also on the stakeholders, also the consumers, employees, investors and the

communities. From the ethical point of view, at times, CSR are adopted in the organization

because of the ethical beliefs of the senior management. For an instance, the company’s

managing director believes that it is environmentally objectionable to hamper the

environment. By implementation and operation of CSR in any organization operates with a

perspective of obtaining long term profits while the critics argue that CSR being the

economic role of the organization (Thomas, 2019). However, these were later on studied on a

wider scale which compared the existing econometric studies explaining the relationship in

between the social and financial performance. This finally came to a conclusion that the

contradictory results of the previous studies reporting positive, negative and the neutral and

the financial impact were due to flawed empirical analysis and also claims that the study is

appropriately specified, so it can declared that corporate social responsibility has a very

impact on the financial outcomes of the organization. Moreover, it is titled that CSR to aid

the targets and missions of the organization as well as to assist in representing to the

consumers what the company aims at serving its customers (Maas et al., 2016).

CONTEMPORARY ACCOUNTING THEORY

ii. Evaluating the holistic view of corporate social responsibility by determining the

compatibility of the sustainability reports with other concepts:

For any workforce in any organization, it is very essential for any company as it is a

very thoughtful method of giving back to the society. When the businesses are conscious of

their social and environmental impact of the world, they can beneficial to the society by

giving back and helping back to find solutions to the everyday arising issues. For any

operating firm it is often believed by most of the executives in any organization practicing

CSR that implementation of the corporate social responsibility in the company can help to

improve the profits and thereby help in the overall growth of the organization. In the

marketplace, CSR also plays a very significant role by increasing the respect and reputation

of the company which ultimately results in increasing more and sales of the company,

consequently the overall productivity of the companies are increased and thereby it can be

also said enhance the loyalty of the employee and also attract better firm personnel. Whether

it is about championing about the women’s rights or protecting the women rights or

attempting to obliterate the poverty on a global scale. From the optical perspective point of

view the companies which are socially more and more responsible project that are very

attractive to the consumers and the shareholders alike, which assists in serving positively to

the consumers consequently affecting their bottom lines (Shnayder et al., 2016).

Additionally a rising number of it has assured to divide the corporate social

responsibilities into strategies and operations, thereby making and developing robust

measurements and reporting frameworks for obtaining both the strategic implementation of

CSR and measurement and consequently reporting frameworks in order to implement CSR

and respond to the stakeholder’s accountability requirements. But designing the sustainability

performance measurement systems within the organization for supporting the strategic

changes and the alterations which the CSR needs to make in the specific issues the company

ii. Evaluating the holistic view of corporate social responsibility by determining the

compatibility of the sustainability reports with other concepts:

For any workforce in any organization, it is very essential for any company as it is a

very thoughtful method of giving back to the society. When the businesses are conscious of

their social and environmental impact of the world, they can beneficial to the society by

giving back and helping back to find solutions to the everyday arising issues. For any

operating firm it is often believed by most of the executives in any organization practicing

CSR that implementation of the corporate social responsibility in the company can help to

improve the profits and thereby help in the overall growth of the organization. In the

marketplace, CSR also plays a very significant role by increasing the respect and reputation

of the company which ultimately results in increasing more and sales of the company,

consequently the overall productivity of the companies are increased and thereby it can be

also said enhance the loyalty of the employee and also attract better firm personnel. Whether

it is about championing about the women’s rights or protecting the women rights or

attempting to obliterate the poverty on a global scale. From the optical perspective point of

view the companies which are socially more and more responsible project that are very

attractive to the consumers and the shareholders alike, which assists in serving positively to

the consumers consequently affecting their bottom lines (Shnayder et al., 2016).

Additionally a rising number of it has assured to divide the corporate social

responsibilities into strategies and operations, thereby making and developing robust

measurements and reporting frameworks for obtaining both the strategic implementation of

CSR and measurement and consequently reporting frameworks in order to implement CSR

and respond to the stakeholder’s accountability requirements. But designing the sustainability

performance measurement systems within the organization for supporting the strategic

changes and the alterations which the CSR needs to make in the specific issues the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

has to face which is not appropriately reflected in the generic sustainability reporting

frameworks. For understanding the relationship in between the SPM and SR there needs to

make a number of exploratory cases. Thereby, it can be said that the corporate social

responsibility enables the companies to create the different values including the social,

environmental and economic values into the core strategy and operations. It will ultimately

assist in bringing in more and more opportunities whilst enhancing long term social and

environmental sustainability. CSR is a self-regulating business practice that helps any

company in being socially accountable that means ranging from the company itself, to its

stakeholders and finally the public (Schaltegger & Hörisch, 2016).

iii. Explaining the sustainability reporting essence using relevant theories:

The perspective of phenomena of sustainability is explained differently by different

theories such as legitimacy, stakeholder holder or institutional theory. The essence of

sustainability reporting of the country is explained by identifying two relevant theories that is

institutional theory and legitimacy theory. It is stated by the institutional theory that the

institutional field or environment governs the behavior of the firm which tends to make the

business practice uniform through the mimetic, coercive and normative. The existence of

institutional mechanism for the communication between the government institutions and

different stakeholders helps in strengthening the corporate social responsibility (Parsa et al.,

2018). The policy of CSR and the spending made by the company on CSR is driven due to

the institutional pressure. Any difference in the corporate governance at the national level is

explained by the institutional theory. The tendency of organization towards CSR

homogenization and increased use of the guidelines of sustainability reporting is driven by

the explicit CSR and adoption of operations of firms at global level (Bouten & Hoozée,

has to face which is not appropriately reflected in the generic sustainability reporting

frameworks. For understanding the relationship in between the SPM and SR there needs to

make a number of exploratory cases. Thereby, it can be said that the corporate social

responsibility enables the companies to create the different values including the social,

environmental and economic values into the core strategy and operations. It will ultimately

assist in bringing in more and more opportunities whilst enhancing long term social and

environmental sustainability. CSR is a self-regulating business practice that helps any

company in being socially accountable that means ranging from the company itself, to its

stakeholders and finally the public (Schaltegger & Hörisch, 2016).

iii. Explaining the sustainability reporting essence using relevant theories:

The perspective of phenomena of sustainability is explained differently by different

theories such as legitimacy, stakeholder holder or institutional theory. The essence of

sustainability reporting of the country is explained by identifying two relevant theories that is

institutional theory and legitimacy theory. It is stated by the institutional theory that the

institutional field or environment governs the behavior of the firm which tends to make the

business practice uniform through the mimetic, coercive and normative. The existence of

institutional mechanism for the communication between the government institutions and

different stakeholders helps in strengthening the corporate social responsibility (Parsa et al.,

2018). The policy of CSR and the spending made by the company on CSR is driven due to

the institutional pressure. Any difference in the corporate governance at the national level is

explained by the institutional theory. The tendency of organization towards CSR

homogenization and increased use of the guidelines of sustainability reporting is driven by

the explicit CSR and adoption of operations of firms at global level (Bouten & Hoozée,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

2015). It has been found that the most influential driver of reporting of CSR is the

government.

The behavior and attitude of organizations in developing and implementing the

voluntary environmental and social disclosure of the information that assist the organization

in fulfilling their objectives in a dynamic environment. When it comes to environmental and

social accounting, legitimacy theory is one of the most cited theories. As per the legitimacy

theory perspective, it is viewed that the behavior of the company is legitimized by the

information generated from corporate social reporting with the objective of influencing the

perception of the society towards the stakeholder and in influencing stakeholders. The usage

of the theory has been done in the literature for supporting the idea that the legitimacy crisis

would be voided by making social disclosure. Furthermore, it is also suggested by the

legitimacy theory that organization having poor environmental performance in an effort to

diminish the increment in the legitimacy threat by providing more extensive and positive

environmental disclosures. Any change in the legitimacy threat is responded by the

organization by way of decreasing environmental disclosure (Andriof et al, 2017).

Part B:

iv. Description of the governance, ownership and financial performance of Dulux

Group Material:

Dulux is a leading manufacturer and marketer of wood care coatings, decorative

paints that are premium branded and texture coatings. The company has become number one

brand for trade professionals and home owners with its heritage dating back to year 1918.

Dulux is regularly voted as the most trusted brand and it has grown to become the brand that

is known for trade professionals and home owners. The Dulux trade mark is the countries

2015). It has been found that the most influential driver of reporting of CSR is the

government.

The behavior and attitude of organizations in developing and implementing the

voluntary environmental and social disclosure of the information that assist the organization

in fulfilling their objectives in a dynamic environment. When it comes to environmental and

social accounting, legitimacy theory is one of the most cited theories. As per the legitimacy

theory perspective, it is viewed that the behavior of the company is legitimized by the

information generated from corporate social reporting with the objective of influencing the

perception of the society towards the stakeholder and in influencing stakeholders. The usage

of the theory has been done in the literature for supporting the idea that the legitimacy crisis

would be voided by making social disclosure. Furthermore, it is also suggested by the

legitimacy theory that organization having poor environmental performance in an effort to

diminish the increment in the legitimacy threat by providing more extensive and positive

environmental disclosures. Any change in the legitimacy threat is responded by the

organization by way of decreasing environmental disclosure (Andriof et al, 2017).

Part B:

iv. Description of the governance, ownership and financial performance of Dulux

Group Material:

Dulux is a leading manufacturer and marketer of wood care coatings, decorative

paints that are premium branded and texture coatings. The company has become number one

brand for trade professionals and home owners with its heritage dating back to year 1918.

Dulux is regularly voted as the most trusted brand and it has grown to become the brand that

is known for trade professionals and home owners. The Dulux trade mark is the countries

CONTEMPORARY ACCOUNTING THEORY

such as Papua New Guinea, New Zealand, Australia, Fiji and Samoa is owned by the

company Dulux Group Limited. The sustainable and strong competitive advantage of the

company lies in the core capabilities of the organization such as the platform for compelling

growth options and stable earnings profile. Such capabilities and core values of the

organization has helped in developing and findings a market leading solution for retail,

consumers and trade consumers (duluxgroup.com.au 2019).

Dulux delivers for its shareholders due to its strong framework of corporate

governance which makes the management and the directors committed to conduct the

business in a fair, ethical and transparent manner in accordance with the corporate

governance standards. A culture of compliance valuing the accountability, corporate integrity

and continuous improvement is fostered in the organization due to robust corporate

governance framework. The governance policy framework of Dulux Group incorporates

political donation, code of conduct, bribery, fraud and corruption control, continuous

disclosure, share trading policy and consumer and competition law (Baumgartner & Rauter,

2017).

Looking at the financial performance of the company, it is observed that the revenue

in both the countries of operation that is Australia and New Zealand grew by 5.3% and 2.3%

respectively. There has been modest increase in the market of protective, powder, wood care

and texture coatings along with the new construction market. In the current financial year, a

solid financial results were generated with an increase in the net profit after tax by 5.4%. An

increase in the amount of EBIT, EBITDA and EBIT as a percentage of sales has also

increased. The financial outlook for the financial year 2019 is the company is targeting

continued EBIT growth and revenue for the full year margin. Given the strong market

growth, the revenue growth is slightly biased with the moderate increase in the raw material.

It is expected that the net expected cost would increase low to mid-single digits with an

such as Papua New Guinea, New Zealand, Australia, Fiji and Samoa is owned by the

company Dulux Group Limited. The sustainable and strong competitive advantage of the

company lies in the core capabilities of the organization such as the platform for compelling

growth options and stable earnings profile. Such capabilities and core values of the

organization has helped in developing and findings a market leading solution for retail,

consumers and trade consumers (duluxgroup.com.au 2019).

Dulux delivers for its shareholders due to its strong framework of corporate

governance which makes the management and the directors committed to conduct the

business in a fair, ethical and transparent manner in accordance with the corporate

governance standards. A culture of compliance valuing the accountability, corporate integrity

and continuous improvement is fostered in the organization due to robust corporate

governance framework. The governance policy framework of Dulux Group incorporates

political donation, code of conduct, bribery, fraud and corruption control, continuous

disclosure, share trading policy and consumer and competition law (Baumgartner & Rauter,

2017).

Looking at the financial performance of the company, it is observed that the revenue

in both the countries of operation that is Australia and New Zealand grew by 5.3% and 2.3%

respectively. There has been modest increase in the market of protective, powder, wood care

and texture coatings along with the new construction market. In the current financial year, a

solid financial results were generated with an increase in the net profit after tax by 5.4%. An

increase in the amount of EBIT, EBITDA and EBIT as a percentage of sales has also

increased. The financial outlook for the financial year 2019 is the company is targeting

continued EBIT growth and revenue for the full year margin. Given the strong market

growth, the revenue growth is slightly biased with the moderate increase in the raw material.

It is expected that the net expected cost would increase low to mid-single digits with an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

increase in the rate in first half. Growth in earnings has been driven by an improvement in

margin and revenue along with increasing investment in growth projects and marketing

(Parsa et al., 2018). The traditional and new distribution channel helps in targeting profit and

revenue growth. Furthermore, the dividends payable to the shareholders has also increased to

28.0 cents as against 14 cents indicating 5.7% from the prior year. Shareholders are provided

with the superior return by maintaining appropriate level of funds to the expansion of value

generation and generating strong cash.

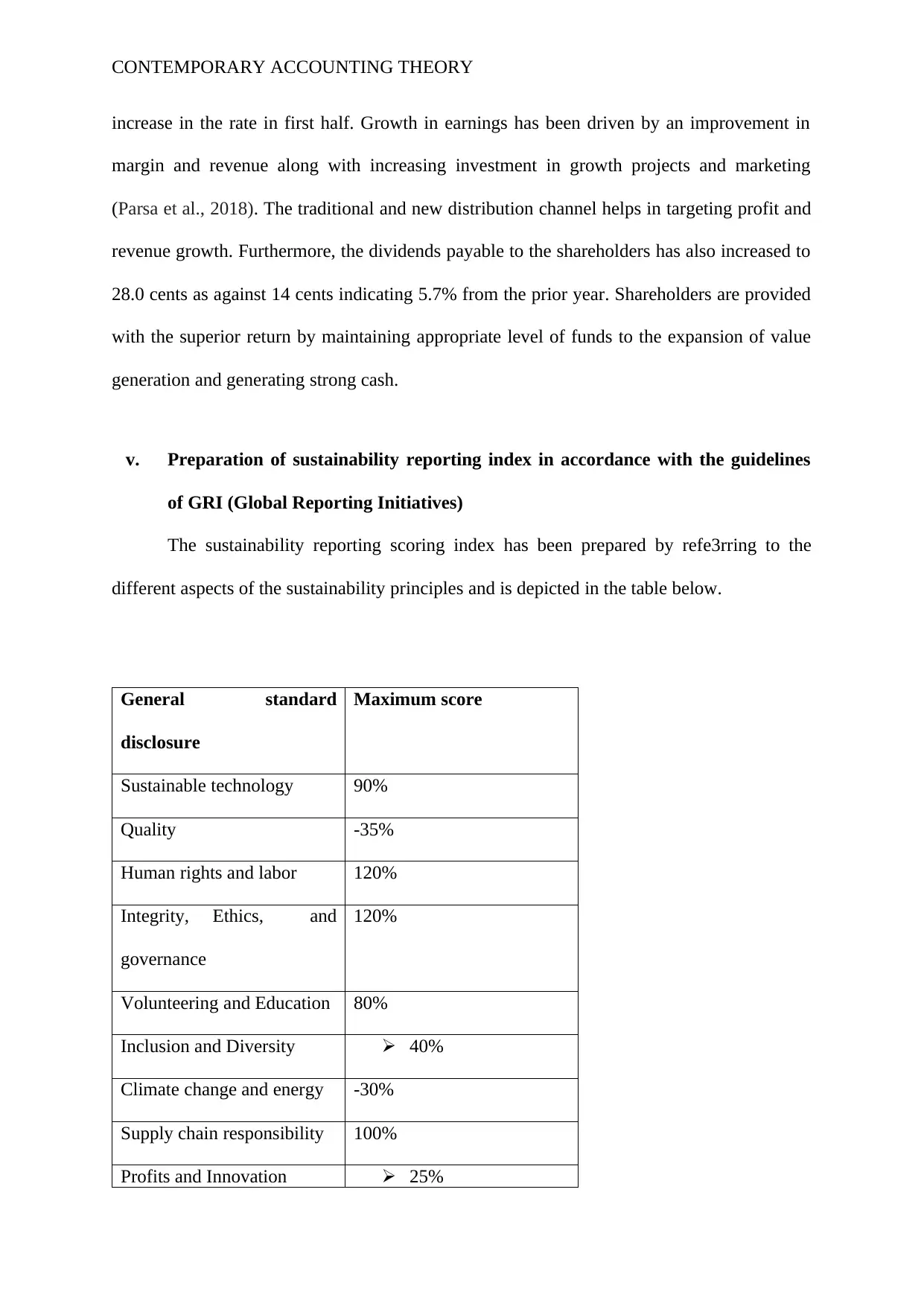

v. Preparation of sustainability reporting index in accordance with the guidelines

of GRI (Global Reporting Initiatives)

The sustainability reporting scoring index has been prepared by refe3rring to the

different aspects of the sustainability principles and is depicted in the table below.

General standard

disclosure

Maximum score

Sustainable technology 90%

Quality -35%

Human rights and labor 120%

Integrity, Ethics, and

governance

120%

Volunteering and Education 80%

Inclusion and Diversity 40%

Climate change and energy -30%

Supply chain responsibility 100%

Profits and Innovation 25%

increase in the rate in first half. Growth in earnings has been driven by an improvement in

margin and revenue along with increasing investment in growth projects and marketing

(Parsa et al., 2018). The traditional and new distribution channel helps in targeting profit and

revenue growth. Furthermore, the dividends payable to the shareholders has also increased to

28.0 cents as against 14 cents indicating 5.7% from the prior year. Shareholders are provided

with the superior return by maintaining appropriate level of funds to the expansion of value

generation and generating strong cash.

v. Preparation of sustainability reporting index in accordance with the guidelines

of GRI (Global Reporting Initiatives)

The sustainability reporting scoring index has been prepared by refe3rring to the

different aspects of the sustainability principles and is depicted in the table below.

General standard

disclosure

Maximum score

Sustainable technology 90%

Quality -35%

Human rights and labor 120%

Integrity, Ethics, and

governance

120%

Volunteering and Education 80%

Inclusion and Diversity 40%

Climate change and energy -30%

Supply chain responsibility 100%

Profits and Innovation 25%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

Safety and Health < 0.15%

Waste and Chemicals 100%

Water -15%

Community 60%

Development and

engagement

+ 20

Supporting family 80%

Employee safety < 0.25%

vi. Evaluating the quality of sustainability reporting of the company against the

scoring index of sustainability reporting:

Adoption of framework of GRI (Global Reporting Initiative) has not been done formally

by Dulux Group Material. However, the sustainability report is prepared by company by

referring to the core principles of the reporting framework of GRI as it is related to social,

environmental, governance and social performance and practice. It is observed from the

sustainability report of Dulux group material limited that different aspects of sustainability

that is environmental, economic, corporate and social has been explained referring to the

guidelines of GRI sustainability reporting framework. It is also observed that the

sustainability report of Dulux group material has reported quantitatively the extent to which

there have been the mitigation of the impact of the products and services on the environment

during the reporting period (Gallego & Ortas, 2017).

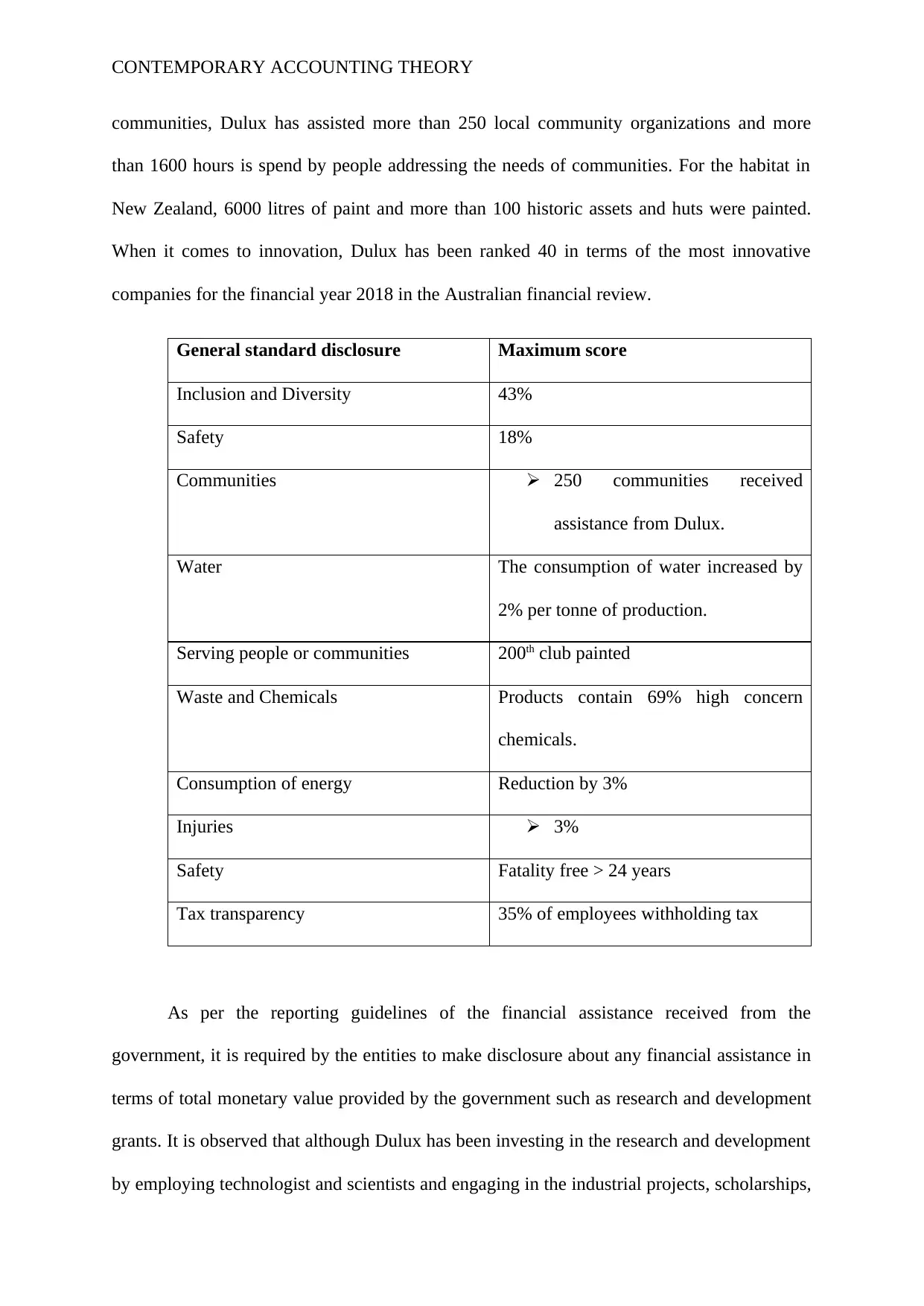

Sustainability goals have been achieved in terms of increased participation in the local

communities and safety performance improvement. For improving its relation with

Safety and Health < 0.15%

Waste and Chemicals 100%

Water -15%

Community 60%

Development and

engagement

+ 20

Supporting family 80%

Employee safety < 0.25%

vi. Evaluating the quality of sustainability reporting of the company against the

scoring index of sustainability reporting:

Adoption of framework of GRI (Global Reporting Initiative) has not been done formally

by Dulux Group Material. However, the sustainability report is prepared by company by

referring to the core principles of the reporting framework of GRI as it is related to social,

environmental, governance and social performance and practice. It is observed from the

sustainability report of Dulux group material limited that different aspects of sustainability

that is environmental, economic, corporate and social has been explained referring to the

guidelines of GRI sustainability reporting framework. It is also observed that the

sustainability report of Dulux group material has reported quantitatively the extent to which

there have been the mitigation of the impact of the products and services on the environment

during the reporting period (Gallego & Ortas, 2017).

Sustainability goals have been achieved in terms of increased participation in the local

communities and safety performance improvement. For improving its relation with

CONTEMPORARY ACCOUNTING THEORY

communities, Dulux has assisted more than 250 local community organizations and more

than 1600 hours is spend by people addressing the needs of communities. For the habitat in

New Zealand, 6000 litres of paint and more than 100 historic assets and huts were painted.

When it comes to innovation, Dulux has been ranked 40 in terms of the most innovative

companies for the financial year 2018 in the Australian financial review.

General standard disclosure Maximum score

Inclusion and Diversity 43%

Safety 18%

Communities 250 communities received

assistance from Dulux.

Water The consumption of water increased by

2% per tonne of production.

Serving people or communities 200th club painted

Waste and Chemicals Products contain 69% high concern

chemicals.

Consumption of energy Reduction by 3%

Injuries 3%

Safety Fatality free > 24 years

Tax transparency 35% of employees withholding tax

As per the reporting guidelines of the financial assistance received from the

government, it is required by the entities to make disclosure about any financial assistance in

terms of total monetary value provided by the government such as research and development

grants. It is observed that although Dulux has been investing in the research and development

by employing technologist and scientists and engaging in the industrial projects, scholarships,

communities, Dulux has assisted more than 250 local community organizations and more

than 1600 hours is spend by people addressing the needs of communities. For the habitat in

New Zealand, 6000 litres of paint and more than 100 historic assets and huts were painted.

When it comes to innovation, Dulux has been ranked 40 in terms of the most innovative

companies for the financial year 2018 in the Australian financial review.

General standard disclosure Maximum score

Inclusion and Diversity 43%

Safety 18%

Communities 250 communities received

assistance from Dulux.

Water The consumption of water increased by

2% per tonne of production.

Serving people or communities 200th club painted

Waste and Chemicals Products contain 69% high concern

chemicals.

Consumption of energy Reduction by 3%

Injuries 3%

Safety Fatality free > 24 years

Tax transparency 35% of employees withholding tax

As per the reporting guidelines of the financial assistance received from the

government, it is required by the entities to make disclosure about any financial assistance in

terms of total monetary value provided by the government such as research and development

grants. It is observed that although Dulux has been investing in the research and development

by employing technologist and scientists and engaging in the industrial projects, scholarships,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.