BUS300: Governance, Sustainability, and Ethics Presentation Analysis

VerifiedAdded on 2022/09/28

|12

|1169

|22

Presentation

AI Summary

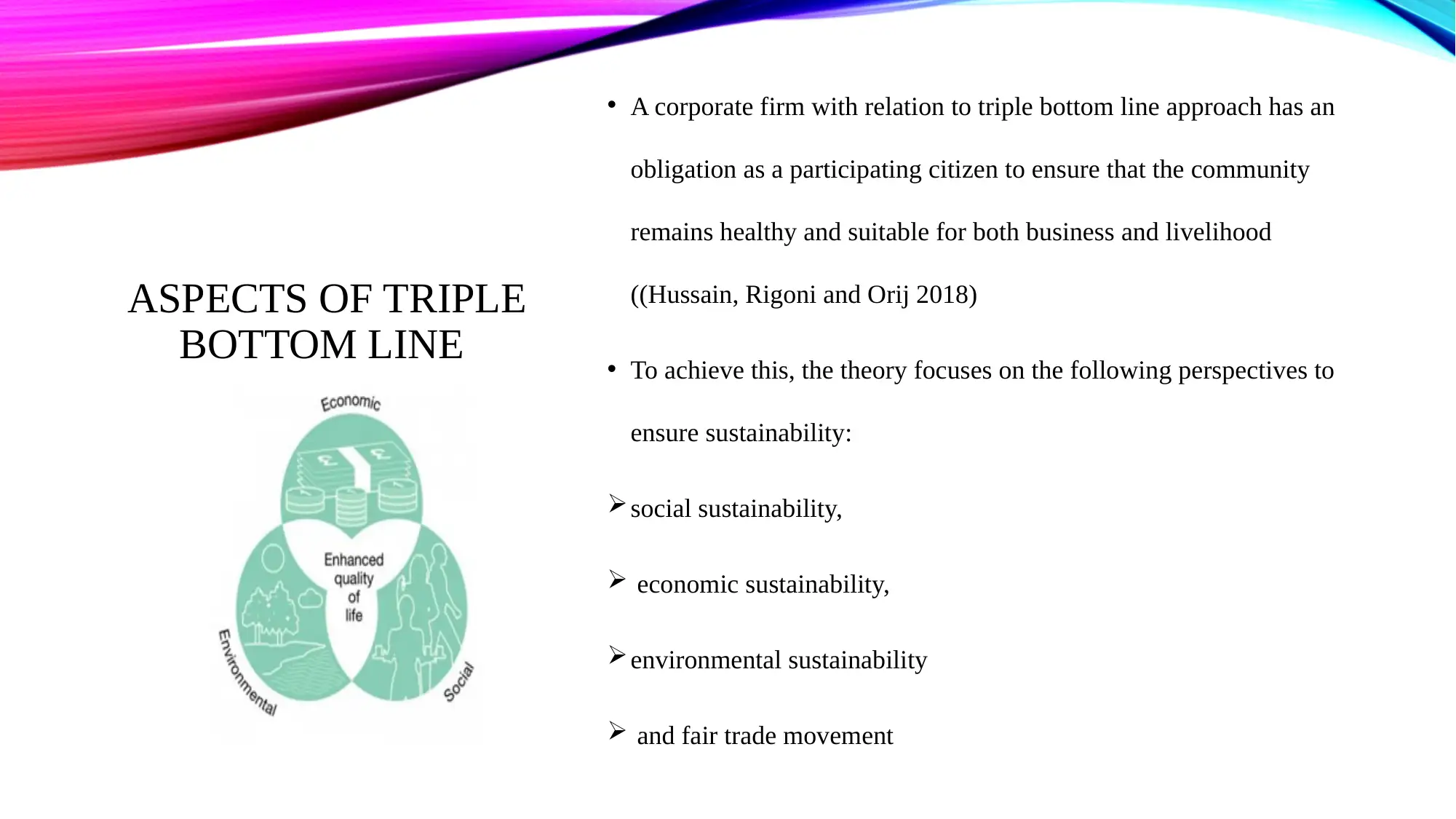

This presentation delves into the realm of corporate governance, sustainability, and ethics, examining the motivations behind corporate information disclosure. It explores key theoretical frameworks such as Stakeholder Theory, Corporate Social Responsibility (CSR), and the Triple Bottom Line, analyzing their implications for business practices. The presentation argues for the Stakeholder Theory's persuasiveness and highlights the interconnectedness between CSR reporting and environmental responsibility. It also examines the role of the Triple Bottom Line in driving other bottom lines, such as economic, social, and environmental measures, all of which are integral to sustainability. The conclusion emphasizes the shift of business entities towards meeting sustainability objectives through various theoretical frameworks. The presentation includes references using the Harvard Referencing Style.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.