Timberwell Construction: Governance, Ethics, and Sustainability Report

VerifiedAdded on 2020/12/24

|13

|3205

|398

Report

AI Summary

This report provides a comprehensive analysis of Timberwell Construction's sustainability practices, focusing on economic, environmental, and social pillars. It examines the company's adherence to GRI standards, including disclosures on financial implications of climate change, confirmed incidents of corruption, and legal actions related to anti-competitive behavior. The environmental section assesses energy consumption, impacts on biodiversity, and non-compliance with environmental regulations. The social sustainability component explores employee hires, turnover, incidents of discrimination, and community engagement. The report analyzes management approaches to address these issues, highlighting specific allegations and the company's responses. It concludes by emphasizing the importance of sustainable practices for brand positioning and stakeholder trust.

GOVERNANCE ETHICS

AND SUSTAINABILITY

AND SUSTAINABILITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

(A.) ECONOMIC SUSTAINABILITY...........................................................................................1

I) Disclosure 201-2 Financial implications and other risks and opportunities due to climatic

change.........................................................................................................................................1

ii) Disclosure 205-3 confirmed incidents of corruption and action taken...................................2

Iii) Disclosure 206-1 legal action for anti-competitive behaviour, anti-trust and monopoly

practises.......................................................................................................................................2

Management approach to issue:..................................................................................................3

(B.) ENVIRONMENTAL SUSTAINABILITY..............................................................................4

I) Disclosure 302-1 Energy consumption within the organisation..............................................4

(ii.) Disclosure 304-2 significant impacts of activities, products and services on biodiversity..4

iii.) Disclosure 307-1 Non-compliance with environmental laws and regulations.....................5

Management approach to issue:..................................................................................................5

SOCIAL SUSTAINABILITY.........................................................................................................6

I). Disclosure 401-1 New employee hires and employee turnover.............................................6

ii.) Disclosure 406-1 Incidents of discrimination and corrective actions taken..........................7

iii.) Disclosure 413-1 Operations with local community engagement, impact assessments and

development programs................................................................................................................7

Management approach to case study:.........................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

.......................................................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

(A.) ECONOMIC SUSTAINABILITY...........................................................................................1

I) Disclosure 201-2 Financial implications and other risks and opportunities due to climatic

change.........................................................................................................................................1

ii) Disclosure 205-3 confirmed incidents of corruption and action taken...................................2

Iii) Disclosure 206-1 legal action for anti-competitive behaviour, anti-trust and monopoly

practises.......................................................................................................................................2

Management approach to issue:..................................................................................................3

(B.) ENVIRONMENTAL SUSTAINABILITY..............................................................................4

I) Disclosure 302-1 Energy consumption within the organisation..............................................4

(ii.) Disclosure 304-2 significant impacts of activities, products and services on biodiversity..4

iii.) Disclosure 307-1 Non-compliance with environmental laws and regulations.....................5

Management approach to issue:..................................................................................................5

SOCIAL SUSTAINABILITY.........................................................................................................6

I). Disclosure 401-1 New employee hires and employee turnover.............................................6

ii.) Disclosure 406-1 Incidents of discrimination and corrective actions taken..........................7

iii.) Disclosure 413-1 Operations with local community engagement, impact assessments and

development programs................................................................................................................7

Management approach to case study:.........................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

.......................................................................................................................................................11

INTRODUCTION

Sustainability means to meet the needs to present without compromising future

generations abilities (Pérez‐López, Moreno‐Romero and Barkemeyer, 2015). Every type of

business needs to comply with corporate sustainability in order to protect environment in which

its business is established. Generally it has three pillars that is economic, environment and social

which formally considered as people, planet and profits. Modern businesses must have to

provide sustainability report for developing brand positioning and to achieve stakeholders trust.

Industries must have to decide to prepare such reports for achieving support from customers,

government and from shareholders.

For developing sustainability report, GRI standards are the first global standards which

introduced by government for business industries (Diouf and Boiral, 2017). Therefore, in this

report explanation will be provided on three pillars in context with company. In this report

selected company is Timberwell Construction which deals in building apartment complexes in

Stanwell Council district. Further, three piller will be elaborated with complaint which filled by

one of its employee Dennis McCabe.

MAIN BODY

(A.) ECONOMIC SUSTAINABILITY

Economic sustainability is the process of increasing economic ability to support defined

level of economic production in nation. Information which contained in this reporting convince

stakeholders about company's potential competitive resources and its low level of risk.

I) Disclosure 201-2 Financial implications and other risks and opportunities due to climatic

change

This is the disclosure through which company have to disclose details relating to risk and

opportunities which occurred due to climatic change (GRI 201: Economic Performance, 2016).

Reporting organisation will prepare report with following requirements:

a.) risk and opportunities which arises with the climatic change and which have potential to

change business operations, revenue and expenditures which are as follows-

Description of risk and opportunities with classification of physical and regulatory or

other changes.

Description of impact which occurred because of risk and opportunities.

1

Sustainability means to meet the needs to present without compromising future

generations abilities (Pérez‐López, Moreno‐Romero and Barkemeyer, 2015). Every type of

business needs to comply with corporate sustainability in order to protect environment in which

its business is established. Generally it has three pillars that is economic, environment and social

which formally considered as people, planet and profits. Modern businesses must have to

provide sustainability report for developing brand positioning and to achieve stakeholders trust.

Industries must have to decide to prepare such reports for achieving support from customers,

government and from shareholders.

For developing sustainability report, GRI standards are the first global standards which

introduced by government for business industries (Diouf and Boiral, 2017). Therefore, in this

report explanation will be provided on three pillars in context with company. In this report

selected company is Timberwell Construction which deals in building apartment complexes in

Stanwell Council district. Further, three piller will be elaborated with complaint which filled by

one of its employee Dennis McCabe.

MAIN BODY

(A.) ECONOMIC SUSTAINABILITY

Economic sustainability is the process of increasing economic ability to support defined

level of economic production in nation. Information which contained in this reporting convince

stakeholders about company's potential competitive resources and its low level of risk.

I) Disclosure 201-2 Financial implications and other risks and opportunities due to climatic

change

This is the disclosure through which company have to disclose details relating to risk and

opportunities which occurred due to climatic change (GRI 201: Economic Performance, 2016).

Reporting organisation will prepare report with following requirements:

a.) risk and opportunities which arises with the climatic change and which have potential to

change business operations, revenue and expenditures which are as follows-

Description of risk and opportunities with classification of physical and regulatory or

other changes.

Description of impact which occurred because of risk and opportunities.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Before taking an action, description of financial implication posted by risk and

opportunity.

Details of method which used to mitigate risk and opportunities.

Cost which required to manage such risk and opportunity.

b.) If company did not have effective system to calculate financial implications, costs or to make

projects related to revenue then company shall have to report its plans to develop such necessary

system (Epstein, 2018).

ii) Disclosure 205-3 confirmed incidents of corruption and action taken

Disclosure 205 relates to anti-corruption which means that companies must have to

disclose information which relates to operations assessed for risks which comply with

corruption, communication and training for anti-corruption policies and procedures and about

confirmed incidents of corruption and action taken (Disclosure 205-3: Confirmed Incidents of

Corruption and Action Taken, 2019).

Reporting organisation must have to report the following information:

Total number and nature related to confirmed incidents of corruption.

Number of incidents in which employee dismissed for bad behaviour and corruption.

Total incidents where termination has been handed over for business contract.

Any public legal cases has been brought against organisation or its employees during

financial year.

Iii) Disclosure 206-1 legal action for anti-competitive behaviour, anti-trust and monopoly

practises

This is the disclosure which sets out reporting requirement for entities regarding their

anti-competitive behaviour (GRI 206: Anti-Competitive Behaviour, 2016). Therefore, reporting

requirements for organisations are as follows-

Entity must have to disclose legal actions pending or get completed during financial year

which regards to anti-competitive behaviour, violation of anti-trust and monopoly

practises which identified in organisation business practises.

Further, entity also have to disclose main outcomes related to legal actions including

decisions or judgements.

2

opportunity.

Details of method which used to mitigate risk and opportunities.

Cost which required to manage such risk and opportunity.

b.) If company did not have effective system to calculate financial implications, costs or to make

projects related to revenue then company shall have to report its plans to develop such necessary

system (Epstein, 2018).

ii) Disclosure 205-3 confirmed incidents of corruption and action taken

Disclosure 205 relates to anti-corruption which means that companies must have to

disclose information which relates to operations assessed for risks which comply with

corruption, communication and training for anti-corruption policies and procedures and about

confirmed incidents of corruption and action taken (Disclosure 205-3: Confirmed Incidents of

Corruption and Action Taken, 2019).

Reporting organisation must have to report the following information:

Total number and nature related to confirmed incidents of corruption.

Number of incidents in which employee dismissed for bad behaviour and corruption.

Total incidents where termination has been handed over for business contract.

Any public legal cases has been brought against organisation or its employees during

financial year.

Iii) Disclosure 206-1 legal action for anti-competitive behaviour, anti-trust and monopoly

practises

This is the disclosure which sets out reporting requirement for entities regarding their

anti-competitive behaviour (GRI 206: Anti-Competitive Behaviour, 2016). Therefore, reporting

requirements for organisations are as follows-

Entity must have to disclose legal actions pending or get completed during financial year

which regards to anti-competitive behaviour, violation of anti-trust and monopoly

practises which identified in organisation business practises.

Further, entity also have to disclose main outcomes related to legal actions including

decisions or judgements.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

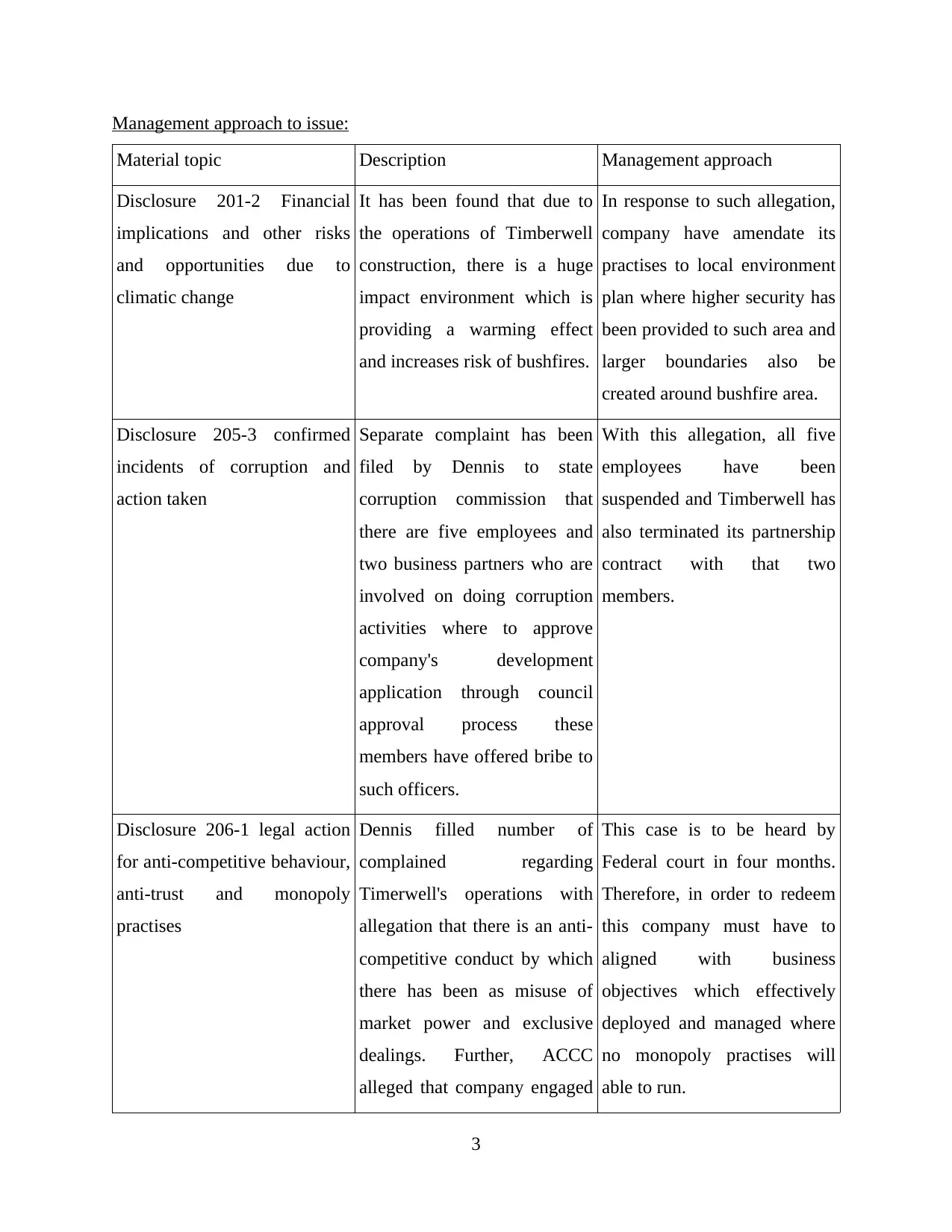

Management approach to issue:

Material topic Description Management approach

Disclosure 201-2 Financial

implications and other risks

and opportunities due to

climatic change

It has been found that due to

the operations of Timberwell

construction, there is a huge

impact environment which is

providing a warming effect

and increases risk of bushfires.

In response to such allegation,

company have amendate its

practises to local environment

plan where higher security has

been provided to such area and

larger boundaries also be

created around bushfire area.

Disclosure 205-3 confirmed

incidents of corruption and

action taken

Separate complaint has been

filed by Dennis to state

corruption commission that

there are five employees and

two business partners who are

involved on doing corruption

activities where to approve

company's development

application through council

approval process these

members have offered bribe to

such officers.

With this allegation, all five

employees have been

suspended and Timberwell has

also terminated its partnership

contract with that two

members.

Disclosure 206-1 legal action

for anti-competitive behaviour,

anti-trust and monopoly

practises

Dennis filled number of

complained regarding

Timerwell's operations with

allegation that there is an anti-

competitive conduct by which

there has been as misuse of

market power and exclusive

dealings. Further, ACCC

alleged that company engaged

This case is to be heard by

Federal court in four months.

Therefore, in order to redeem

this company must have to

aligned with business

objectives which effectively

deployed and managed where

no monopoly practises will

able to run.

3

Material topic Description Management approach

Disclosure 201-2 Financial

implications and other risks

and opportunities due to

climatic change

It has been found that due to

the operations of Timberwell

construction, there is a huge

impact environment which is

providing a warming effect

and increases risk of bushfires.

In response to such allegation,

company have amendate its

practises to local environment

plan where higher security has

been provided to such area and

larger boundaries also be

created around bushfire area.

Disclosure 205-3 confirmed

incidents of corruption and

action taken

Separate complaint has been

filed by Dennis to state

corruption commission that

there are five employees and

two business partners who are

involved on doing corruption

activities where to approve

company's development

application through council

approval process these

members have offered bribe to

such officers.

With this allegation, all five

employees have been

suspended and Timberwell has

also terminated its partnership

contract with that two

members.

Disclosure 206-1 legal action

for anti-competitive behaviour,

anti-trust and monopoly

practises

Dennis filled number of

complained regarding

Timerwell's operations with

allegation that there is an anti-

competitive conduct by which

there has been as misuse of

market power and exclusive

dealings. Further, ACCC

alleged that company engaged

This case is to be heard by

Federal court in four months.

Therefore, in order to redeem

this company must have to

aligned with business

objectives which effectively

deployed and managed where

no monopoly practises will

able to run.

3

in such activities to prevent

entrance of new development

in market.

(B.) ENVIRONMENTAL SUSTAINABILITY

Environmental sustainability is the process of maintaining factors and practises which

helps in developing contribution for quality of environment on a long term basis. Some of

disclosure which every company must have to disclose is as follows-

I) Disclosure 302-1 Energy consumption within the organisation

This is the disclosure which related to contribution of energy consumption from non-

renewable resources lead to climatic change (GRI Disclosure 302-1, 2019). The reporting

requirement of organisation is as follows-

a.) entity must have to disclose total amount of fuel consumption within organisation from the

use of non-renewable sources.

b.) entity have to disclose consumption of total fuel within organisation from renewable

resources.

c.) multiplies such total in:

electricity consumption/sold

heating consumption/sold

cooling consumption/sold

steam consumption/sold

d.) entity also have top disclose total consumption of energy within the organisation in multiples

e.) calculation method of standards, methodologies, assumptions used and source of used

conversion factor (Alshuwaikhat and et,al., 2017).

(ii.) Disclosure 304-2 significant impacts of activities, products and services on biodiversity

This disclosure has been developed to protect environmental dimension in sustainability

concern which has impact upon living as well as non-living natural systems of environment

(304: Biodiversity, 2018). This protection is important to endure survival of plant and animal

species. The reporting requirements of organisation is as follows-

a.) entity must have to disclose nature of significant impact on biodiversity with reference to:

4

entrance of new development

in market.

(B.) ENVIRONMENTAL SUSTAINABILITY

Environmental sustainability is the process of maintaining factors and practises which

helps in developing contribution for quality of environment on a long term basis. Some of

disclosure which every company must have to disclose is as follows-

I) Disclosure 302-1 Energy consumption within the organisation

This is the disclosure which related to contribution of energy consumption from non-

renewable resources lead to climatic change (GRI Disclosure 302-1, 2019). The reporting

requirement of organisation is as follows-

a.) entity must have to disclose total amount of fuel consumption within organisation from the

use of non-renewable sources.

b.) entity have to disclose consumption of total fuel within organisation from renewable

resources.

c.) multiplies such total in:

electricity consumption/sold

heating consumption/sold

cooling consumption/sold

steam consumption/sold

d.) entity also have top disclose total consumption of energy within the organisation in multiples

e.) calculation method of standards, methodologies, assumptions used and source of used

conversion factor (Alshuwaikhat and et,al., 2017).

(ii.) Disclosure 304-2 significant impacts of activities, products and services on biodiversity

This disclosure has been developed to protect environmental dimension in sustainability

concern which has impact upon living as well as non-living natural systems of environment

(304: Biodiversity, 2018). This protection is important to endure survival of plant and animal

species. The reporting requirements of organisation is as follows-

a.) entity must have to disclose nature of significant impact on biodiversity with reference to:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Construction of manufacturing plants, mines or transport infrastructure,

pollution which caused because of business operations,

introduction of invasive pests, species,

decrease in species,

conversion of habitat

b.) entity also have to disclose significant direct and indirect positive or negative impact upon:

affected species

impacted areas

duration of impact

reversibility and irreversibility of impacts

iii.) Disclosure 307-1 Non-compliance with environmental laws and regulations

This disclosure have been developed to comply with reporting requirement related to

environment concern. Main motive of such disclosure is to protect business environment with

some rules and regulations (Disclosure 307-1: Non-compliance with environmental laws and

regulations, 2019.). The reporting requirements of organisation are as follows-

a.) entity must have to report significant fines and non-monetary sanctions which are non-

compliance with laws and regulations related to environment in terms of:

total values of significant fines in monetary terms,

total number of non-monetary sanctions,

cases which brought mechanisms of dispute resolution

b.) company also have to report brief statement of fact when they have not identified and did not

comply with environmental laws and practises.

Management approach to issue:

Material Description Management approach

Disclosure 302-1 Energy

consumption within the

organisation

An allegation has been

developed on Timerwell

construction that company is

using huge amount of fuel

consumption because of which

its availability decreasing in

With the release of second

media, Timberwell

construction explained its

energy consumption table

which shows that it has

effective fuel consumption

5

pollution which caused because of business operations,

introduction of invasive pests, species,

decrease in species,

conversion of habitat

b.) entity also have to disclose significant direct and indirect positive or negative impact upon:

affected species

impacted areas

duration of impact

reversibility and irreversibility of impacts

iii.) Disclosure 307-1 Non-compliance with environmental laws and regulations

This disclosure have been developed to comply with reporting requirement related to

environment concern. Main motive of such disclosure is to protect business environment with

some rules and regulations (Disclosure 307-1: Non-compliance with environmental laws and

regulations, 2019.). The reporting requirements of organisation are as follows-

a.) entity must have to report significant fines and non-monetary sanctions which are non-

compliance with laws and regulations related to environment in terms of:

total values of significant fines in monetary terms,

total number of non-monetary sanctions,

cases which brought mechanisms of dispute resolution

b.) company also have to report brief statement of fact when they have not identified and did not

comply with environmental laws and practises.

Management approach to issue:

Material Description Management approach

Disclosure 302-1 Energy

consumption within the

organisation

An allegation has been

developed on Timerwell

construction that company is

using huge amount of fuel

consumption because of which

its availability decreasing in

With the release of second

media, Timberwell

construction explained its

energy consumption table

which shows that it has

effective fuel consumption

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

environment. It is also been

alleged that company is not

energy efficient organisation.

from renewable resources

practises where at least 50% is

used within next three years.

Disclosure 304-2 significant

impacts of activities, products

and services on biodiversity

It has been alligated that with

the construction work of

Timerwell, it is estimated that

the density which developed

for the site would irreversibly

convert the habitat called rare

Wallum sedge frog.

With the first release of media,

company explained that they

are working with Stanwell

council and environmental

groups to develop strategy for

managing proposed

development site to conserve

Wallum sedge frog.

Disclosure 307-1 Non-

compliance with

environmental laws and

regulations

A separate complaint has been

filled to department of

Environment and energy and it

is found with the investigation

by department that company is

critically endangering

ecological community and

coastal grasslands because of

which fined has been charged

to company with $200000 for

clearing 0.45 hectare of

community.

With this allegation,

Timberwell was ordered for

reviewing their vegetation

management plan, because of

company extend its audit

program for contractors and

also implemented

rehabilitation plan at cost of

more than $440000.

SOCIAL SUSTAINABILITY

Social sustainability considered as ability to meet and develop procedure and structure for

meeting needs of the present member but also to develop abilities which maintain needs of the

future generations. Certain disclosures in this section is as follows-

6

alleged that company is not

energy efficient organisation.

from renewable resources

practises where at least 50% is

used within next three years.

Disclosure 304-2 significant

impacts of activities, products

and services on biodiversity

It has been alligated that with

the construction work of

Timerwell, it is estimated that

the density which developed

for the site would irreversibly

convert the habitat called rare

Wallum sedge frog.

With the first release of media,

company explained that they

are working with Stanwell

council and environmental

groups to develop strategy for

managing proposed

development site to conserve

Wallum sedge frog.

Disclosure 307-1 Non-

compliance with

environmental laws and

regulations

A separate complaint has been

filled to department of

Environment and energy and it

is found with the investigation

by department that company is

critically endangering

ecological community and

coastal grasslands because of

which fined has been charged

to company with $200000 for

clearing 0.45 hectare of

community.

With this allegation,

Timberwell was ordered for

reviewing their vegetation

management plan, because of

company extend its audit

program for contractors and

also implemented

rehabilitation plan at cost of

more than $440000.

SOCIAL SUSTAINABILITY

Social sustainability considered as ability to meet and develop procedure and structure for

meeting needs of the present member but also to develop abilities which maintain needs of the

future generations. Certain disclosures in this section is as follows-

6

I). Disclosure 401-1 New employee hires and employee turnover

This is the reporting disclosures which sets out the requirements of employment in any

type of business industry. Through this disclosure an approach to employment has been

developed where elements like job creation, hiring, recruitment, retention and related practises

been more emphasized (GRI 401: Employment (Containing Standard Interpretation 1), 2016).

The reporting requirement of organisation is as follows-

a.) entity must have to report total number and rate of new employee appointed during

financial year by age group, gender and region.

b.) further, entity also have to report total number and rate of employee turnover during

reporting period which is also by age group, gender and region (Eizenberg and Jabareen, 2017).

ii.) Disclosure 406-1 Incidents of discrimination and corrective actions taken

This standard have been developed to set out the topic discrimination from the

workplace. With this implementation, organisation is been expected to avoid any type of

discrimination against any person at the workplace (GRI Disclosure 406-1, 2019). Reporting

requirement of such disclosure in organisation is as follows-

a.) entity must have to report, total number of incidents which occurred in organisation during

financial year,

b.) disclosure of action and incidents with reference to:

review of incidents by organisation,

plans which implemented as remedy,

review of plan through internal management review process,

incident which has no longer subject to action,

iii.) Disclosure 413-1 Operations with local community engagement, impact assessments and

development programs

This disclosure has been set out for the topic of local community which defined as

persons or groups which living and working in certain areas which impacted economically,

socially and environmentally (GRI Disclosure 413-1, 2019). The reporting requirement of

organisation is as follows-

a.) entity must have to disclose operations which has been conducted for local community

engagement, impact assessment and through development programs with the use of:

7

This is the reporting disclosures which sets out the requirements of employment in any

type of business industry. Through this disclosure an approach to employment has been

developed where elements like job creation, hiring, recruitment, retention and related practises

been more emphasized (GRI 401: Employment (Containing Standard Interpretation 1), 2016).

The reporting requirement of organisation is as follows-

a.) entity must have to report total number and rate of new employee appointed during

financial year by age group, gender and region.

b.) further, entity also have to report total number and rate of employee turnover during

reporting period which is also by age group, gender and region (Eizenberg and Jabareen, 2017).

ii.) Disclosure 406-1 Incidents of discrimination and corrective actions taken

This standard have been developed to set out the topic discrimination from the

workplace. With this implementation, organisation is been expected to avoid any type of

discrimination against any person at the workplace (GRI Disclosure 406-1, 2019). Reporting

requirement of such disclosure in organisation is as follows-

a.) entity must have to report, total number of incidents which occurred in organisation during

financial year,

b.) disclosure of action and incidents with reference to:

review of incidents by organisation,

plans which implemented as remedy,

review of plan through internal management review process,

incident which has no longer subject to action,

iii.) Disclosure 413-1 Operations with local community engagement, impact assessments and

development programs

This disclosure has been set out for the topic of local community which defined as

persons or groups which living and working in certain areas which impacted economically,

socially and environmentally (GRI Disclosure 413-1, 2019). The reporting requirement of

organisation is as follows-

a.) entity must have to disclose operations which has been conducted for local community

engagement, impact assessment and through development programs with the use of:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

social impact assessment, gender impact assessment which based on participatory

processes,

impact upon environmental assessment and ongoing monitoring,

disclosure of result of impact upon social and environmental,

program which held for local community development,

etc.

Management approach to case study:

Material Description Management approach

Disclosure 401-1 New

employee hires and employee

turnover

It has been found with the

Timberwell case study that

there is a high employment

turnover of company and also

they did not have effective

staff engagement practises. Its

result appears that more than

17 employees in company has

leaved.

To manage such allegation,

company has increases worker

pay rates and implemented

monthly day off policies to

engage existing staff of

company.

Disclosure 406-1 Incidents of

discrimination and corrective

actions taken

One employee Dennis McCabe

filled allegation against

company regarding workplace

harassment. This has been

claim in fair work commission

where employee said that he

faces an discrimination by his

co-workers on the basis of age

because he was only employee

who is older than 50 years of

age and facing jokes related to

his age.

With this allegation, company

paid $4400 to employee and

also updated its anti-

discrimination policy and also

provided anti-discrimination

training to employees as per

the order to Commission.

Disclosure 413-1 Operations It has been found with the case With the third release of

8

processes,

impact upon environmental assessment and ongoing monitoring,

disclosure of result of impact upon social and environmental,

program which held for local community development,

etc.

Management approach to case study:

Material Description Management approach

Disclosure 401-1 New

employee hires and employee

turnover

It has been found with the

Timberwell case study that

there is a high employment

turnover of company and also

they did not have effective

staff engagement practises. Its

result appears that more than

17 employees in company has

leaved.

To manage such allegation,

company has increases worker

pay rates and implemented

monthly day off policies to

engage existing staff of

company.

Disclosure 406-1 Incidents of

discrimination and corrective

actions taken

One employee Dennis McCabe

filled allegation against

company regarding workplace

harassment. This has been

claim in fair work commission

where employee said that he

faces an discrimination by his

co-workers on the basis of age

because he was only employee

who is older than 50 years of

age and facing jokes related to

his age.

With this allegation, company

paid $4400 to employee and

also updated its anti-

discrimination policy and also

provided anti-discrimination

training to employees as per

the order to Commission.

Disclosure 413-1 Operations It has been found with the case With the third release of

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with local community

engagement, impact

assessments and development

programs

study that company has

considerable expenses for

engaging local communities,

perform impact assessment,

also have formulated social

development programs for the

development of residential

purpose.

media, company has started

initiatives for Environmental

impact assessments, local

residents meetings and local

community development

programs for meeting needs of

such peoples.

CONCLUSION

From the above report it can be concluded every company needs provide sustainability

report as per the standards of GRI on a range of economic, environmental and social impact. In

this report, issues which faced by Timberwell construction has been identified such as anti-

discrimination, anti-competitive, corruption, energy consumption allegation. Therefore, it can be

summarised that Company must have to develop practises which comply with standards of GRI

by which proper care will be taken to protect business environment.

9

engagement, impact

assessments and development

programs

study that company has

considerable expenses for

engaging local communities,

perform impact assessment,

also have formulated social

development programs for the

development of residential

purpose.

media, company has started

initiatives for Environmental

impact assessments, local

residents meetings and local

community development

programs for meeting needs of

such peoples.

CONCLUSION

From the above report it can be concluded every company needs provide sustainability

report as per the standards of GRI on a range of economic, environmental and social impact. In

this report, issues which faced by Timberwell construction has been identified such as anti-

discrimination, anti-competitive, corruption, energy consumption allegation. Therefore, it can be

summarised that Company must have to develop practises which comply with standards of GRI

by which proper care will be taken to protect business environment.

9

REFERENCES

Books and Journals

Alshuwaikhat, H.M and et,al., 2017. The development of a GIS-based model for campus

environmental sustainability assessment. Sustainability. 9(3). p.439.

Diouf, D. and Boiral, O., 2017. The quality of sustainability reports and impression

management: A stakeholder perspective. Accounting, Auditing & Accountability

Journal. 30(3). pp.643-667.

Eizenberg, E. and Jabareen, Y., 2017. Social sustainability: A new conceptual

framework. Sustainability. 9(1). p.68.

Epstein, M.J., 2018. Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

Pérez‐López, D., Moreno‐Romero, A. and Barkemeyer, R., 2015. Exploring the relationship

between sustainability reporting and sustainability management practices. Business

Strategy and the Environment. 24(8). pp.720-734.

Online

304: Biodiversity. 2018. [Online]. Available through <http://reports.clariant.com/2017/gri-

report/additional-information/gri-300-environmental-disclosures/304-biodiversity.html>

Disclosure 205-3: Confirmed Incidents of Corruption and Action Taken. 2019. [Online].

Available through <https://www.sika.com/content/corp/main/en/group/sustainability/gri-

standards/gri-205-anti-corruption/disclosure-205-3.html>

Disclosure 307-1: Non-compliance with environmental laws and regulations. 2019. [Online].

Available through <https://www.sika.com/content/corp/main/en/group/sustainability/gri-

standards/gri-307-environmental-compliance/disclosure-307-1.html>

GRI 201: Economic Performance. 2016. [Online]. Available through

<https://www.globalreporting.org/standards/gri-standards-download-center/gri-201-

economic-performance-2016/>

GRI 206: Anti-Competitive Behaviour. 2016. [Online]. Available through

<https://www.globalreporting.org/standards/gri-standards-download-center/gri-206-anti-

competitive-behavior-2016/>

10

Books and Journals

Alshuwaikhat, H.M and et,al., 2017. The development of a GIS-based model for campus

environmental sustainability assessment. Sustainability. 9(3). p.439.

Diouf, D. and Boiral, O., 2017. The quality of sustainability reports and impression

management: A stakeholder perspective. Accounting, Auditing & Accountability

Journal. 30(3). pp.643-667.

Eizenberg, E. and Jabareen, Y., 2017. Social sustainability: A new conceptual

framework. Sustainability. 9(1). p.68.

Epstein, M.J., 2018. Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

Pérez‐López, D., Moreno‐Romero, A. and Barkemeyer, R., 2015. Exploring the relationship

between sustainability reporting and sustainability management practices. Business

Strategy and the Environment. 24(8). pp.720-734.

Online

304: Biodiversity. 2018. [Online]. Available through <http://reports.clariant.com/2017/gri-

report/additional-information/gri-300-environmental-disclosures/304-biodiversity.html>

Disclosure 205-3: Confirmed Incidents of Corruption and Action Taken. 2019. [Online].

Available through <https://www.sika.com/content/corp/main/en/group/sustainability/gri-

standards/gri-205-anti-corruption/disclosure-205-3.html>

Disclosure 307-1: Non-compliance with environmental laws and regulations. 2019. [Online].

Available through <https://www.sika.com/content/corp/main/en/group/sustainability/gri-

standards/gri-307-environmental-compliance/disclosure-307-1.html>

GRI 201: Economic Performance. 2016. [Online]. Available through

<https://www.globalreporting.org/standards/gri-standards-download-center/gri-201-

economic-performance-2016/>

GRI 206: Anti-Competitive Behaviour. 2016. [Online]. Available through

<https://www.globalreporting.org/standards/gri-standards-download-center/gri-206-anti-

competitive-behavior-2016/>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.