University Accounting Research Proposal: Sustainability Reporting

VerifiedAdded on 2022/11/19

|15

|2818

|264

Report

AI Summary

This research proposal delves into the effectiveness of sustainability reporting by companies. It examines the practical and theoretical motivations behind sustainability reporting, emphasizing its importance for stakeholders and its role in enhancing market efficiency. The literature review explores sustainability reporting practices, the theoretical framework (legitimacy, stakeholder, and agency theories), and critical analyses of existing research. The proposal investigates whether companies' sustainability reports accurately reflect their practices. The research aims to determine the consistency of companies' sustainability reporting practices with their actual sustainability efforts. The hypothesis suggests that inconsistencies may exist between reported practices and actual implementations. The research paper uses existing research to evaluate the effectiveness of the disclosures made by the companies on sustainability. The goal is to establish the commitment of the organizations to sustainability reporting practices, and the impact of the reports on the decision-making of stakeholders. The appendix provides details of other research papers on the topic.

Running Head: CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSUES IN ACCOUNTING

Name of the Student

Name of the University

Author Note

CONTEMPORARY ISSUES IN ACCOUNTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Practical Motivation...................................................................................................................2

Theoretical Motivation...............................................................................................................2

Literature Review.......................................................................................................................3

Hypothesis..................................................................................................................................7

Reference....................................................................................................................................8

Appendix..................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Practical Motivation...................................................................................................................2

Theoretical Motivation...............................................................................................................2

Literature Review.......................................................................................................................3

Hypothesis..................................................................................................................................7

Reference....................................................................................................................................8

Appendix..................................................................................................................................10

2CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

During recent years, the most critical issues faced by the business organization are

sustainability, which is having greater potential for influencing the overall profitability as

well as performance of the company. Sustainability report is the report by the organization,

which provides the information about the social, economic, environmental as well as

governance performance. It enables the business organization for considering the impacts of

the wider ranges of issues of the sustainability that enables them for being more transparent

about the opportunities as well as risks faced by them (Sandberg and Holmlund 2015).

The concerns are increasing regarding negative impacts of the products as well as

activities on social and environmental well-being of the business organizations. Therefore, it

becomes necessary for checking the effectiveness of implementations of the sustainability.

Hence, under this research paper, discussion will be done on the effectiveness of the

implementations of sustainability reporting by the companies.

Practical Motivation

The practical motivation behind the effectiveness of the sustainability reporting is the

practice of sustainability reporting, which is of great help to the stakeholders. The widespread

practice of sustainability reporting creates transparency and can help the markets for

functioning in more efficient manner. The stakeholders such as investor, government and

customer base their decision after having knowledge of the level of effectiveness of the

sustainability reporting practices by the concerned company.

Theoretical Motivation

Despite of the increasing interests of the practitioners as well as academics in

studying about the topic of sustainability, there exists certain gap in the aspects of the

effectiveness in the implementations of the sustainability reporting practices by the

Introduction

During recent years, the most critical issues faced by the business organization are

sustainability, which is having greater potential for influencing the overall profitability as

well as performance of the company. Sustainability report is the report by the organization,

which provides the information about the social, economic, environmental as well as

governance performance. It enables the business organization for considering the impacts of

the wider ranges of issues of the sustainability that enables them for being more transparent

about the opportunities as well as risks faced by them (Sandberg and Holmlund 2015).

The concerns are increasing regarding negative impacts of the products as well as

activities on social and environmental well-being of the business organizations. Therefore, it

becomes necessary for checking the effectiveness of implementations of the sustainability.

Hence, under this research paper, discussion will be done on the effectiveness of the

implementations of sustainability reporting by the companies.

Practical Motivation

The practical motivation behind the effectiveness of the sustainability reporting is the

practice of sustainability reporting, which is of great help to the stakeholders. The widespread

practice of sustainability reporting creates transparency and can help the markets for

functioning in more efficient manner. The stakeholders such as investor, government and

customer base their decision after having knowledge of the level of effectiveness of the

sustainability reporting practices by the concerned company.

Theoretical Motivation

Despite of the increasing interests of the practitioners as well as academics in

studying about the topic of sustainability, there exists certain gap in the aspects of the

effectiveness in the implementations of the sustainability reporting practices by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ISSUES IN ACCOUNTING

companies. Therefore, in order to address the gap, this research paper aims for reviewing the

effectiveness of the practices of the sustainability reporting of the companies in relation to the

consistency of the current practices of sustainability disclosures.

Literature Review

Sustainability Reporting Practices

The changing environment of the global business has insisted the business

organizations for looking beyond the financial performances. The business organization has

realized the significance of the integrating the social as well as environmental issues with the

strategy of the business. Sustainability reporting is the method in the accounting of the

sustainability that deals with preparation of the sustainable report, which is consists of

mission, vision as well as goals of company. It helps in focusing on non-financial information

disclosures of the performance of the firm to the external parties. The sustainability deals

with the social, economic as well as environmental performances of the organization (Hoque

2017).

The effectiveness of the sustainability reporting practices by the company is

dependent upon the intention of the company in its implementation, as it should depict the

real picture of the organization to the stakeholders of the company. Here the independent

variable is sustainability reporting practices and the dependent variable is the intention or

consistency in the implementations of the sustainability practices.

Theoretical Framework

The legitimacy is refereed as the condition that exists when the value system of the

organization is in the harmony with the society’s value system. This theory explains that it is

important for meeting the norms as well as expectations of the society for ensuring the

survival of the firm in the long run. The arguments by the proponents of the theory states that

companies. Therefore, in order to address the gap, this research paper aims for reviewing the

effectiveness of the practices of the sustainability reporting of the companies in relation to the

consistency of the current practices of sustainability disclosures.

Literature Review

Sustainability Reporting Practices

The changing environment of the global business has insisted the business

organizations for looking beyond the financial performances. The business organization has

realized the significance of the integrating the social as well as environmental issues with the

strategy of the business. Sustainability reporting is the method in the accounting of the

sustainability that deals with preparation of the sustainable report, which is consists of

mission, vision as well as goals of company. It helps in focusing on non-financial information

disclosures of the performance of the firm to the external parties. The sustainability deals

with the social, economic as well as environmental performances of the organization (Hoque

2017).

The effectiveness of the sustainability reporting practices by the company is

dependent upon the intention of the company in its implementation, as it should depict the

real picture of the organization to the stakeholders of the company. Here the independent

variable is sustainability reporting practices and the dependent variable is the intention or

consistency in the implementations of the sustainability practices.

Theoretical Framework

The legitimacy is refereed as the condition that exists when the value system of the

organization is in the harmony with the society’s value system. This theory explains that it is

important for meeting the norms as well as expectations of the society for ensuring the

survival of the firm in the long run. The arguments by the proponents of the theory states that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ISSUES IN ACCOUNTING

the reporting of sustainability tends for reducing the risks of the boycotts as well as

regulatory actions and strengthens the license of the firm for operating (Maas, Schaltegger

and Crutzen 2016).

The theory of stakeholders upholds that the firms have the accountability towards the

broader ranges of the stakeholders rather than just shareholders, which are customers,

government, environment, community, creditors and others. The significance of the

sustainability reporting is towards strengthening of the relationships between the firm as well

as society, under which it operates. If the interest of the stakeholders were ignored then it

would have greater impact on the public image that would be unfavorably affecting their

financial performances (Herremans, Nazari and Mahmoudian 2016).

The theory of agency is based on the relationships between managers as well as

owners. In between the managers of the company and the other stakeholders, there exists

conflict of the interest as well as asymmetry of the information. The significance of this

theory has gained after the wake of the scandals of corporate governance. If there are no any

public disclosures by the company then there is rise in the perceived risks by the investors. In

this respect, sustainability reporting to reduce the asymmetry of information as well as risks

perceived by the investors, reduced cost of capital and increase the efficiencies of the market

(Ehnert et al. 2016).

Critical Analysis

Wan Nurul Karimah has stated that generally, the companies are having clear policy

of sustainability on their plans as well as their commitments towards the protection of the

environment as well as responsibility of the practices. In this concern, the most important

concern is translation of the policies as well as commitments into the measurable indicators,

which helps the firms for the assessing their position in relation to sustainability practices as

the reporting of sustainability tends for reducing the risks of the boycotts as well as

regulatory actions and strengthens the license of the firm for operating (Maas, Schaltegger

and Crutzen 2016).

The theory of stakeholders upholds that the firms have the accountability towards the

broader ranges of the stakeholders rather than just shareholders, which are customers,

government, environment, community, creditors and others. The significance of the

sustainability reporting is towards strengthening of the relationships between the firm as well

as society, under which it operates. If the interest of the stakeholders were ignored then it

would have greater impact on the public image that would be unfavorably affecting their

financial performances (Herremans, Nazari and Mahmoudian 2016).

The theory of agency is based on the relationships between managers as well as

owners. In between the managers of the company and the other stakeholders, there exists

conflict of the interest as well as asymmetry of the information. The significance of this

theory has gained after the wake of the scandals of corporate governance. If there are no any

public disclosures by the company then there is rise in the perceived risks by the investors. In

this respect, sustainability reporting to reduce the asymmetry of information as well as risks

perceived by the investors, reduced cost of capital and increase the efficiencies of the market

(Ehnert et al. 2016).

Critical Analysis

Wan Nurul Karimah has stated that generally, the companies are having clear policy

of sustainability on their plans as well as their commitments towards the protection of the

environment as well as responsibility of the practices. In this concern, the most important

concern is translation of the policies as well as commitments into the measurable indicators,

which helps the firms for the assessing their position in relation to sustainability practices as

5CONTEMPORARY ISSUES IN ACCOUNTING

well as identifying the priorities areas that helps in leading towards effective sustainability

strategy implementations (Wan Ahmad, de Brito and Tavasszy 2016).

Dinithi has stated that there exists relationship between extent of the reporting of the

sustainability and the characteristics of the company such as age, sizes as well as financial

performances of the company. He stated that sustainability reporting is considered more

significant for larger companies (Dissanayake, Tilt and Xydias-Lobo 2016).

Rodrigo has stated that the decision for publishing first sustainability report is driven

primarily by the internal motivations of the companies; however, for the subsequent reports,

there are combinations of the internal motivations as well as external stimuli (Lozano,

Nummert and Ceulemans 2016).

Colin Higgins has stated that there is the requirement for the new theoretical

explanations of the practices of the sustainability reporting. The companies that are having

lower-impact as well as less intensive will not be considered as the small minority of the

companies that is based on the fringe values (Higgins, Milne and Van Gramberg 2015).

Charl de Villiers has stated that the new conceptual model of the corporate

sustainability with the management control and reporting. This benefits of the integration is

consists of better internal communication as well as better operationalization of the ideals of

the sustainability with the help of balance scorecard as well as better BSC understanding by

the extensive engagement of stakeholders, which the sustainability calls for (De Villiers,

Rouse and Kerr 2016).

However, the study of this research paper add to the existing evidences a well as

ongoing evidences on whether the firms are implementing the sustainability practices on only

document for showing their stakeholders that they actually mean what they are publishing or

they are showing true picture of their sustainability practices. The intention is the behavioral

well as identifying the priorities areas that helps in leading towards effective sustainability

strategy implementations (Wan Ahmad, de Brito and Tavasszy 2016).

Dinithi has stated that there exists relationship between extent of the reporting of the

sustainability and the characteristics of the company such as age, sizes as well as financial

performances of the company. He stated that sustainability reporting is considered more

significant for larger companies (Dissanayake, Tilt and Xydias-Lobo 2016).

Rodrigo has stated that the decision for publishing first sustainability report is driven

primarily by the internal motivations of the companies; however, for the subsequent reports,

there are combinations of the internal motivations as well as external stimuli (Lozano,

Nummert and Ceulemans 2016).

Colin Higgins has stated that there is the requirement for the new theoretical

explanations of the practices of the sustainability reporting. The companies that are having

lower-impact as well as less intensive will not be considered as the small minority of the

companies that is based on the fringe values (Higgins, Milne and Van Gramberg 2015).

Charl de Villiers has stated that the new conceptual model of the corporate

sustainability with the management control and reporting. This benefits of the integration is

consists of better internal communication as well as better operationalization of the ideals of

the sustainability with the help of balance scorecard as well as better BSC understanding by

the extensive engagement of stakeholders, which the sustainability calls for (De Villiers,

Rouse and Kerr 2016).

However, the study of this research paper add to the existing evidences a well as

ongoing evidences on whether the firms are implementing the sustainability practices on only

document for showing their stakeholders that they actually mean what they are publishing or

they are showing true picture of their sustainability practices. The intention is the behavioral

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ISSUES IN ACCOUNTING

aspect of the company that holds with the company’s board. Therefore, agency theory,

stakeholders theory as well as legitimacy theory best fits in this research paper (Stacchezzini,

Melloni and Lai 2016).

This research paper focuses on the intention of the company in relation to the

publishing effective sustainability reporting practices. There are various companies who

publishes the sustainability report for just showing that how much socio, economic, political,

community, environment and other aspects have value for them but in real they are not very

much concerned with the practices. It is because of they have to abide by the laws relating to

the sustainability such as GRI, the companies have to make the disclosures by showing their

concerns. However, whether or not they are committed towards the effective sustainability

reporting practices needs to be examined (George et al. 2016).

There are various previous studies done by the researchers on the sustainability

practices and has provided the evidences in relation to the various concerns of its practices

but none of the previous research has highlighted the concern regarding the effectiveness of

the disclosures made by the companies on the sustainability areas.

Therefore, the conclusion that can be derived from the analysis is that the

effectiveness of the sustainability reporting depends heavily upon the intentions of the

company on the various issues of the sustainability such as towards customers, environment,

community, government, environment and people. The sustainability reporting practices

adopted by the companies plays important role for the stakeholders. All the major and minor

decisions taken by the stakeholders are dependent upon the company’s disclosures of their

sustainable practices. Hence, there is need for the research on the commitment of the

organization in the disclosures of the sustainability reporting practices.

aspect of the company that holds with the company’s board. Therefore, agency theory,

stakeholders theory as well as legitimacy theory best fits in this research paper (Stacchezzini,

Melloni and Lai 2016).

This research paper focuses on the intention of the company in relation to the

publishing effective sustainability reporting practices. There are various companies who

publishes the sustainability report for just showing that how much socio, economic, political,

community, environment and other aspects have value for them but in real they are not very

much concerned with the practices. It is because of they have to abide by the laws relating to

the sustainability such as GRI, the companies have to make the disclosures by showing their

concerns. However, whether or not they are committed towards the effective sustainability

reporting practices needs to be examined (George et al. 2016).

There are various previous studies done by the researchers on the sustainability

practices and has provided the evidences in relation to the various concerns of its practices

but none of the previous research has highlighted the concern regarding the effectiveness of

the disclosures made by the companies on the sustainability areas.

Therefore, the conclusion that can be derived from the analysis is that the

effectiveness of the sustainability reporting depends heavily upon the intentions of the

company on the various issues of the sustainability such as towards customers, environment,

community, government, environment and people. The sustainability reporting practices

adopted by the companies plays important role for the stakeholders. All the major and minor

decisions taken by the stakeholders are dependent upon the company’s disclosures of their

sustainable practices. Hence, there is need for the research on the commitment of the

organization in the disclosures of the sustainability reporting practices.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

Hypothesis

The hypotheses that can be developed after the deep understanding of the

sustainability practices in the business organization are as follows:

H0- The companies’ implements sustainability reporting practices effectively and

their report depicts actual picture of their practices.

H1- The companies does not implement sustainability reporting effectively as there

are differences in what they report and what is the actual situation.

Hypothesis

The hypotheses that can be developed after the deep understanding of the

sustainability practices in the business organization are as follows:

H0- The companies’ implements sustainability reporting practices effectively and

their report depicts actual picture of their practices.

H1- The companies does not implement sustainability reporting effectively as there

are differences in what they report and what is the actual situation.

8CONTEMPORARY ISSUES IN ACCOUNTING

Reference

De Villiers, C., Rouse, P. and Kerr, J., 2016. A new conceptual model of influences driving

sustainability based on case evidence of the integration of corporate sustainability

management control and reporting. Journal of Cleaner Production, 136, pp.78-85.

Dissanayake, D., Tilt, C. and Xydias-Lobo, M., 2016. Sustainability reporting by publicly

listed companies in Sri Lanka. Journal of Cleaner Production, 129, pp.169-182.

Ehnert, I., Parsa, S., Roper, I., Wagner, M. and Muller-Camen, M., 2016. Reporting on

sustainability and HRM: A comparative study of sustainability reporting practices by the

world's largest companies. The International Journal of Human Resource

Management, 27(1), pp.88-108.

George, R.A., Siti-Nabiha, A.K., Jalaludin, D. and Abdalla, Y.A., 2016. Barriers to and

enablers of sustainability integration in the performance management systems of an oil and

gas company. Journal of Cleaner Production, 136, pp.197-212.

Herremans, I.M., Nazari, J.A. and Mahmoudian, F., 2016. Stakeholder relationships,

engagement, and sustainability reporting. Journal of Business Ethics, 138(3), pp.417-435.

Higgins, C., Milne, M.J. and Van Gramberg, B., 2015. The uptake of sustainability reporting

in Australia. Journal of Business Ethics, 129(2), pp.445-468.

Hoque, M.E., 2017. Why company should adopt integrated reporting?. International Journal

of Economics and Financial Issues, 7(1), pp.241-248.

Lozano, R., Nummert, B. and Ceulemans, K., 2016. Elucidating the relationship between

sustainability reporting and organisational change management for sustainability. Journal of

cleaner production, 125, pp.168-188.

Reference

De Villiers, C., Rouse, P. and Kerr, J., 2016. A new conceptual model of influences driving

sustainability based on case evidence of the integration of corporate sustainability

management control and reporting. Journal of Cleaner Production, 136, pp.78-85.

Dissanayake, D., Tilt, C. and Xydias-Lobo, M., 2016. Sustainability reporting by publicly

listed companies in Sri Lanka. Journal of Cleaner Production, 129, pp.169-182.

Ehnert, I., Parsa, S., Roper, I., Wagner, M. and Muller-Camen, M., 2016. Reporting on

sustainability and HRM: A comparative study of sustainability reporting practices by the

world's largest companies. The International Journal of Human Resource

Management, 27(1), pp.88-108.

George, R.A., Siti-Nabiha, A.K., Jalaludin, D. and Abdalla, Y.A., 2016. Barriers to and

enablers of sustainability integration in the performance management systems of an oil and

gas company. Journal of Cleaner Production, 136, pp.197-212.

Herremans, I.M., Nazari, J.A. and Mahmoudian, F., 2016. Stakeholder relationships,

engagement, and sustainability reporting. Journal of Business Ethics, 138(3), pp.417-435.

Higgins, C., Milne, M.J. and Van Gramberg, B., 2015. The uptake of sustainability reporting

in Australia. Journal of Business Ethics, 129(2), pp.445-468.

Hoque, M.E., 2017. Why company should adopt integrated reporting?. International Journal

of Economics and Financial Issues, 7(1), pp.241-248.

Lozano, R., Nummert, B. and Ceulemans, K., 2016. Elucidating the relationship between

sustainability reporting and organisational change management for sustainability. Journal of

cleaner production, 125, pp.168-188.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ISSUES IN ACCOUNTING

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Advancing the integration of corporate

sustainability measurement, management and reporting. Journal of cleaner production, 133,

pp.859-862.

Sandberg, M. and Holmlund, M., 2015. Impression management tactics in sustainability

reporting. Social Responsibility Journal, 11(4), pp.677-689.

Stacchezzini, R., Melloni, G. and Lai, A., 2016. Sustainability management and reporting: the

role of integrated reporting for communicating corporate sustainability management. Journal

of Cleaner Production, 136, pp.102-110.

Wan Ahmad, W.N.K., de Brito, M.P. and Tavasszy, L.A., 2016. Sustainable supply chain

management in the oil and gas industry: a review of corporate sustainability reporting

practices. Benchmarking: An International Journal, 23(6), pp.1423-1444.

Appendix

Author/s Date Title Journal Type of If empirical, Summary of contribution to the

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Advancing the integration of corporate

sustainability measurement, management and reporting. Journal of cleaner production, 133,

pp.859-862.

Sandberg, M. and Holmlund, M., 2015. Impression management tactics in sustainability

reporting. Social Responsibility Journal, 11(4), pp.677-689.

Stacchezzini, R., Melloni, G. and Lai, A., 2016. Sustainability management and reporting: the

role of integrated reporting for communicating corporate sustainability management. Journal

of Cleaner Production, 136, pp.102-110.

Wan Ahmad, W.N.K., de Brito, M.P. and Tavasszy, L.A., 2016. Sustainable supply chain

management in the oil and gas industry: a review of corporate sustainability reporting

practices. Benchmarking: An International Journal, 23(6), pp.1423-1444.

Appendix

Author/s Date Title Journal Type of If empirical, Summary of contribution to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ISSUES IN ACCOUNTING

Paper

(Theoretical

or Empirical)

dependent &

independent

variables

research question (100 words)

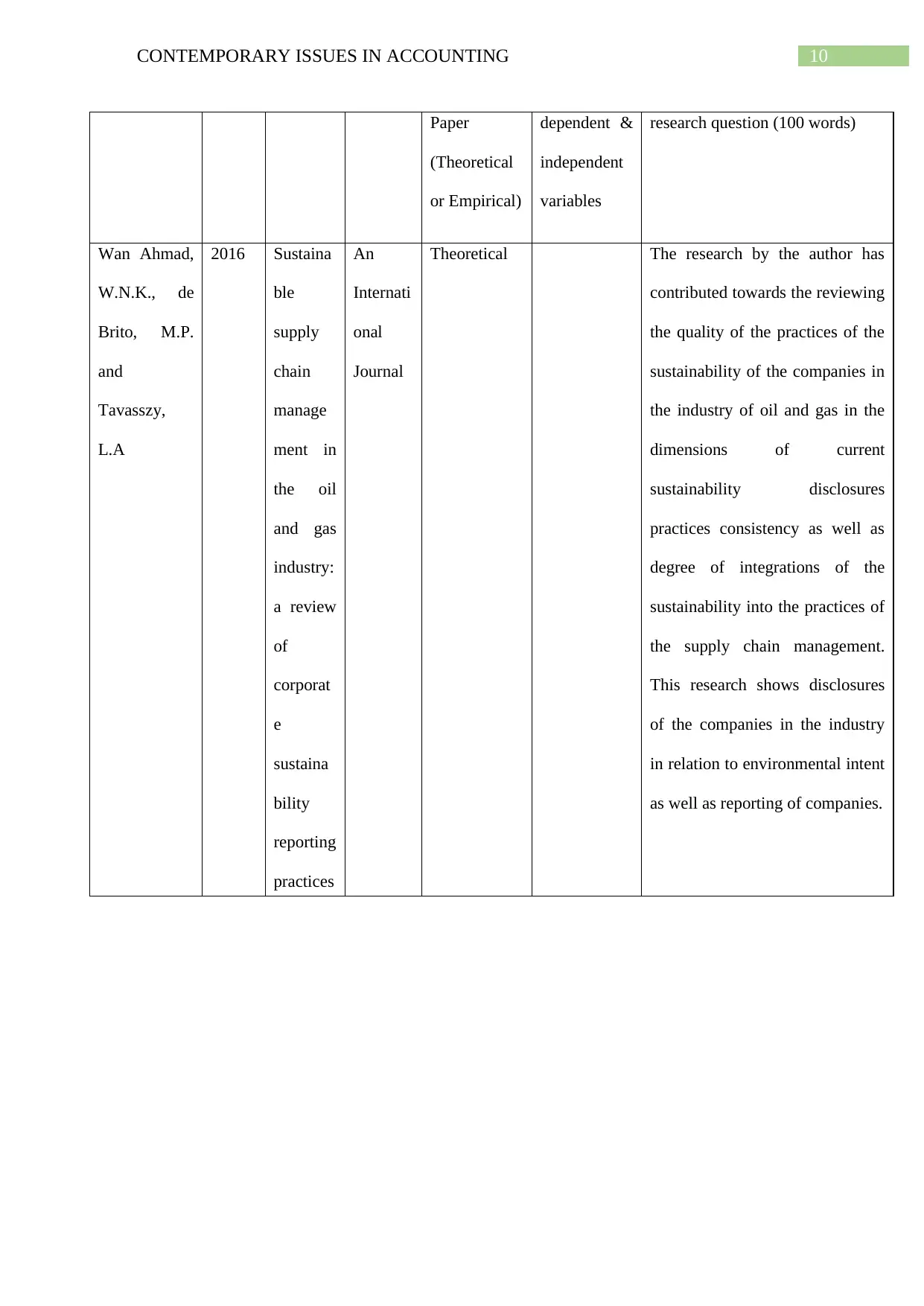

Wan Ahmad,

W.N.K., de

Brito, M.P.

and

Tavasszy,

L.A

2016 Sustaina

ble

supply

chain

manage

ment in

the oil

and gas

industry:

a review

of

corporat

e

sustaina

bility

reporting

practices

An

Internati

onal

Journal

Theoretical The research by the author has

contributed towards the reviewing

the quality of the practices of the

sustainability of the companies in

the industry of oil and gas in the

dimensions of current

sustainability disclosures

practices consistency as well as

degree of integrations of the

sustainability into the practices of

the supply chain management.

This research shows disclosures

of the companies in the industry

in relation to environmental intent

as well as reporting of companies.

Paper

(Theoretical

or Empirical)

dependent &

independent

variables

research question (100 words)

Wan Ahmad,

W.N.K., de

Brito, M.P.

and

Tavasszy,

L.A

2016 Sustaina

ble

supply

chain

manage

ment in

the oil

and gas

industry:

a review

of

corporat

e

sustaina

bility

reporting

practices

An

Internati

onal

Journal

Theoretical The research by the author has

contributed towards the reviewing

the quality of the practices of the

sustainability of the companies in

the industry of oil and gas in the

dimensions of current

sustainability disclosures

practices consistency as well as

degree of integrations of the

sustainability into the practices of

the supply chain management.

This research shows disclosures

of the companies in the industry

in relation to environmental intent

as well as reporting of companies.

11CONTEMPORARY ISSUES IN ACCOUNTING

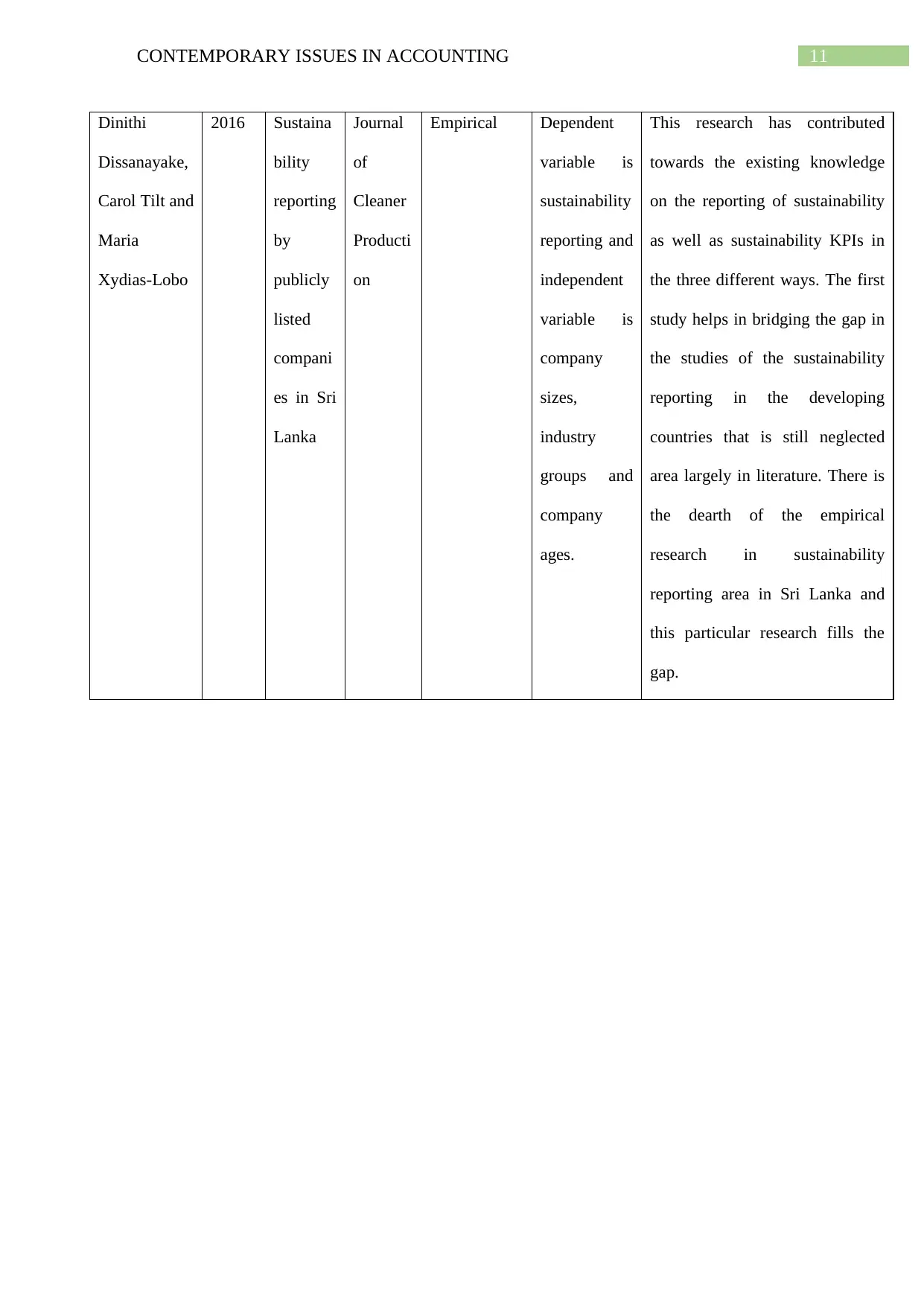

Dinithi

Dissanayake,

Carol Tilt and

Maria

Xydias-Lobo

2016 Sustaina

bility

reporting

by

publicly

listed

compani

es in Sri

Lanka

Journal

of

Cleaner

Producti

on

Empirical Dependent

variable is

sustainability

reporting and

independent

variable is

company

sizes,

industry

groups and

company

ages.

This research has contributed

towards the existing knowledge

on the reporting of sustainability

as well as sustainability KPIs in

the three different ways. The first

study helps in bridging the gap in

the studies of the sustainability

reporting in the developing

countries that is still neglected

area largely in literature. There is

the dearth of the empirical

research in sustainability

reporting area in Sri Lanka and

this particular research fills the

gap.

Dinithi

Dissanayake,

Carol Tilt and

Maria

Xydias-Lobo

2016 Sustaina

bility

reporting

by

publicly

listed

compani

es in Sri

Lanka

Journal

of

Cleaner

Producti

on

Empirical Dependent

variable is

sustainability

reporting and

independent

variable is

company

sizes,

industry

groups and

company

ages.

This research has contributed

towards the existing knowledge

on the reporting of sustainability

as well as sustainability KPIs in

the three different ways. The first

study helps in bridging the gap in

the studies of the sustainability

reporting in the developing

countries that is still neglected

area largely in literature. There is

the dearth of the empirical

research in sustainability

reporting area in Sri Lanka and

this particular research fills the

gap.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.